Revisiting Sub-sampled Newton Methods

Abstract

Many machine learning models depend on solving a large scale optimization problem. Recently, sub-sampled Newton methods have emerged to attract much attention for optimization due to their efficiency at each iteration, rectified a weakness in the ordinary Newton method of suffering a high cost at each iteration while commanding a high convergence rate. In this work we propose two new efficient Newton-type methods, Refined Sub-sampled Newton and Refined Sketch Newton. Our methods exhibit a great advantage over existing sub-sampled Newton methods, especially when Hessian-vector multiplication can be calculated efficiently and Hessian matrix is ill-conditioned. Specifically, the proposed methods are shown to converge superlinearly in general case and quadratically under a little stronger assumption. The proposed methods can be generalized to a unifying framework for the convergence proof of several existing sub-sampled Newton methods, revealing new convergence properties. Finally, we empirically evaluate the performance of our methods on several standard datasets and the results show consistent improvement in computational efficiency.

1 Introduction

We consider the following optimization problem

| (1) |

where , functions , and is assumed to be far larger than (i.e., ). Many machine learning models can be expressed as (1) where each is the loss w.r.t. the -th sample. There are many such examples, e.g., logistic regressions, support vector machines, neural networks, and graphical models.

Many optimization algorithms to solve problem (1) are based on the following iteration:

| (2) |

where is the number of iterations. If is the identity matrix and , the resulting procedure is called Gradient Descent (GD) which achieves sublinear convergence for general smooth convex objective and linear convergence for smooth-strongly convex ones. When is large, the full gradient method is inefficient due to its iteration cost scaling linearly in . Consequently, stochastic gradient descent (SGD) has been a typical alternation [19, 13, 6]. Such a method samples a small mini-batch of data to construct an approximate gradient to achieve cheaper cost in each iteration. However, the convergence rate can be significantly slower than that of the full gradient methods [15]. Thus, a great deal of efforts have been made to devise modification to achieve the convergence rate of the full gradient while keeping low iteration cost [11, 22, 23, 27].

If is a positive definite matrix of containing the curvature information, this formulation leads us to second-order methods. It is well known that second order methods enjoy superior convergence rate in both theory and practice compared to first-order methods which only make use of the gradient information. The standard Newton Method, where , and , achieves a quadratic convergence rate for smooth-strongly convex objective functions. However, the Newton method takes cost per iteration, so it becomes extremely expensive when or are very large. As a result, one tries to construct an approximation of the Hessian in a way that the update is computationally feasible, and yet still provides sufficient second order information. One class of such methods are quasi-Newton methods, which are a generalization of the secant method to find the root of the first derivative for multidimensional problems. The celebrated Broyden-Fletcher-Goldfarb-Shanno (BFGS) and its limited memory version (L-BFGS) are the most popular and widely used [16]. They take cost per iteration.

Recently, when , a class of called sub-sampled Newton methods have been proposed, which define an approximate Hessian matrix on a small subset of samples. The most naive approach is to sample a subset of functions randomly [20, 3, 26] to construct a sub-sampled Hessian. Erdogdu and Montanari [9] proposed NewSamp which solves the problem that sampled Hessian may be ill-conditioned. When the Hessian can be written as where is an available matrix, Pilanci and Wainwright [17] then proposed to use sketching techniques to approximate the Hessian. Similarly, Xu et al. [26] proposed to sample rows of with non-uniform probability distribution. Agarwal et al. [1] proposed an algorithm called LiSSA to approximate the inversion of Hessian directly.

In the past few years, variants of sub-sampled Newton methods have been proposed. And the convergence properties have been analyzed. However, there are several important problems related to sub-sampled Newton methods are still open.

-

1.

Can sub-sampled Newton methods achieve superlinear even quadratic convergence rate without increasing sampling number?

-

2.

Is there a unifying framework to analyzing the convergence properties of sub-sampled Newton methods?

-

3.

Is Lipschitz continuity condition necessary for the convergence of sub-sampled Newton methods? If not, when is needed?

The first problem is important both in theory and application. An optimization algorithm with superlinear and quadratic convergence is appealing in most cases. The second problem is of great significance in analyzing the convergence properties sub-sampled Newton methods. Besides, a unifying framework can provide some potential inspirations for developing more efficient sub-sampled Newton methods. The third question is also of great importance both theory and application. Without the constrain of Lipschitz continuity condition, sub-sampled Newton methods can be widely used in optimization problems. In fact, Erdogdu and Montanari [9] found that NewSamp can be used in training SVM which did not meet the Lipschitz continuity condition. They concluded that NewSamp can be used in optimization problems where Lipschitz continuity condition is not satisfied empirically but without any theoretical analysis.

In this paper we will answer the above problems. And we summarize our contribution as follow.

-

1.

We propose the Refined Sub-sampled Newton (ReSubNewton) and Refined Sketch Newton (ReSkeNewton), which converge superlinearly in general case and quadratically with a little stronger assumption without increasing sampling number which answer the first problem. To the best of our knowledge, it is the first work to show that the sub-sampled Newton method can achieve quadratic convergence rate. To achieve superlinear convergence rate, the existing methods need to sample more and more samples as iteration goes, which may turn into the exact Newton method and lose the computational efficiency. Our methods do not need any additional samples but several matrix-vector multiplications and Hessian-vector multiplications which is cheap using a ‘Hessian-free’ technique. Especially, when Hessian-vector multiplication can be calculated very efficient, our methods have great advantage over other existing sub-sampled Newton methods.

-

2.

We observe that sub-sampled Newton methods can be viewed as an inexact Newton procedure [16, 7]. Theorem 7 gives a unifying framework to analyze variants of sub-sampled Newton methods which answer the second problem. The convergence properties of sub-sampled Newton methods can be analyzed easily and systematically. In Section 5, we analyze several important variants of sub-sampled Newton method. More importantly, Theorem 7 reveals the sufficient conditions to achieve different convergence rate.

-

3.

Theorem 7 also shows that Lipschitz continuity condition is not necessary for achieving linear and superlinear convergence. And it is needed to obtain quadratic convergence. Theorem 7 not only explains the phenomenon that NewSamp [9] can be used to train SVM which the Lipschitz continuity condition is not satisfied, but also shows that the convergence rate is linear. Hence, we clarify the third problem and greatly widen the range of applications of variants of sub-sampled Newton methods.

-

4.

We analyze the convergence properties of inexact sub-sampled Newnton method and provide a practical stop criterion to get the product of inverse of sub-sampled Hessian and gradient iteratively. We also give analysis to Newton method with sub-sampled Hessian and sub-sampled gradient and obtain new convergence properties which are preferable to previous work.

1.1 Related Work

Byrd et al. [3] proposed a sub-sampled Newton method which is similar to Sub-sampled Newton (SubNewton Algorithm 1) and approximates the product of inverse of sub-sampled Hessian and gradient by conjugate gradient. The asymptotic convergence of the method was established but without quantitative bounds in [3]. Erdogdu and Montanari [9] then gave local convergence analysis of sub-sampled Newton method and proposed Newsamp (Algorithm 7 in Appendix). Pilanci and Wainwright [17] first used ‘sketching’ within the context of Newton-like methods. The authors proposed a randomized second-order method which is based on performing an approximate Newton’s step using randomly sketched Hessian and gave the detailed analysis of convergence properties. The algorithm is referred as Sketch Newton (SkeNewton Algorithm 2) in this paper. Similarly, Xu et al. [26] proposed to sketching Hessian matrix with non-uniform probability distribution. Agarwal et al. [1] proposed an algorithm called LiSSA to approximate the inversion of Hessian directly.

Roosta-Khorasani and Mahoney analyzed the global and local convergence rates of variants of sub-sampled Newton methods in detail [21, 20]. The work of [21, 20] focused on constrained optimization problem. Our work focuses on unconstrained optimization problem and proposes a proof framework that the analysis of [20] can also be fitted into. Though our work focuses on unconstrained optimization problems, we can use project iteration onto the constrained set for the constrained optimization problem.

2 Notation and Preliminaries

In this section, we introduce the notation and preliminaries that will be used in this paper.

2.1 Notation

Given a matrix of rank , its SVD is given as , where and contain the left singular vectors of , and contain the right singular vectors of , and with are the nonzero singular values of . If is positive semidefinite, then and the square root of can be defined as .

Additionally, is the Frobenius norm of and is the spectral norm. If is a positive definite matrix, is called -norm. The condtion number of is defined as .

Throughout this paper, we use notions of linear convergence rate, superlinear convergence rate and quadratic convergence rate. In our paper, the convergence rates we will use are defined in a little different way from standard ones. A sequence of vectors is said to converge linearly to a limit point , if for some ,

where the function we want to optimize. Similarly, superlinear convergence and quadratic convergence are respectively defined as

We call it as linear-quadratic convergence rate shown as below

where . Besides, we assume that each is convex and twice differentiable. And the Lipschitz continuity condition for Hessian is defined as follows:

where is the Lipschitz constant.

We also assume that each and have the following properties:

| (3) | |||

| (4) |

2.2 Randomized sketching matrices

We first give an -subspace embedding property which will be used in ReSkeNewton . Then we list some useful different types of randomized sketching matrices.

Definition 1

is an -subspace embedding matrix for any fixed matrix . Then, for all , .

Gaussian sketching matrix: The most classical sketching matrix is Gaussian sketching matrix with i.i.d normal random variables with variance . Because of well-known concentration properties of Gaussian random matrices [25], gaussian random matrices are very attractive. Besides, is enough to guarantee -subspace embedding property any fixed matrix . is the tightest bound in known types of sketching matrices. However, Gaussian random matrices are dense matrices. It is costly to compute .

Random sampling sketching matrix: Let be column orthonormal basis for with , and denote the -th row of . Let and be an integer with . Then the ’s are leverage scores for . Given a distribution with and , where , we construct a sampling matrix and a rescaling matrix as follows. For every , independently and with replacement, pick an index from the set with probability and set and . The random sampling sketching matrix for is then defined as . To achieve an -subspace embedding property for , is needed. When we sample by the distribution with leverage sores, i.e. , we just need samples. There are several methods to approximate the leverage score of which are of computational efficiency [8, 12].

Sparse embedding matrix: Sparse embedding matrix is of the form that there is only one non-zero entry uniformly sampling from in each column [5]. Hence the it is very efficient to compute , especially when is a sparse matrix. To achieve an -subspace embedding property for , is sufficient [14, 25].

For random sampling, -Coherence is an important concept which is closely relatd to leverage scores.

Definition 2

Let be column orthonormal basis for with , and denote the -th row of . Then the -Coherence of is

Other types of sketching matrices like Subsampled Randomized Hadamard Transformation and detailed properties of sketching matrices and subspace embedding matrices can be found in the survey [25].

2.3 Computation cost of matrix operations

We will give the computation cost of basic matrix operations, the cost can be found in Matrix Computation [10].

For matrix multiplication, given dense matrices and , the basic cost of the matrix product is flops. It costs flops for the matrix product when is sparse, where denotes the number of nonzero entries of . If is a sparse subspace embedding matrix [25], then the product costs .

For SVD and QR-decomposition of a matrix , it costs about flops if [10]. To get the inverse of a positive-definite matrix , it costs flops by Cholesky decomposition.

3 Inexact Newton

The basic Newton step is to calculate a direction vector by solving the following symmetric linear system

| (5) |

An inexact Newton method tries to find an approximation to . We define the residual with as follows

| (6) |

Usually, inexact Newton methods should satisfy the following condition

| (7) |

where the sequence (with for all ) is called the forcing sequence.

We give a new form of convergence properties of inexact Newton method. The convergence properties can be found in [16, 7].

Theorem 3

Suppose that exists and is continuous in a neighborhood of a minimizer , with being positive definite. Consider the iteration where satisfies (7). If the starting point is sufficiently near , then the sequence converges to and satisfies

| (8) |

where and are constant.

Besides, if is Lipschitz continuous for near , then sequence converges to and satisfies

| (9) |

where is the Lipschitz constant.

4 Refined Sub-sampled Newton Methods

We propose ReSubNewton and ReSkeNewton which can both achieve superlinear and quadratic convergence rate without more and more sampling as iteration goes. The key advantage of our algorithms is to get accurate approximation to without any additional samples.

4.1 Algorithms Description

In ReSubNewton, we first select a sample set to construct such that

| (10) |

Then, is a good approximation to . Furthermore, if is bigger than a prespecified tolerance , where , we can refine as follows

After refine iterations above, will decrease to , where is the residual before refine iterations. If we choose properly, will decrease to very fast. Finally, we update with refined just as

The detailed algorithm is depicted in Algorithm 3.

In machine learning, it is common that the Hessian matrix is of the form and is an explicitly available , e.g., SVM, generalized linear models, etc.. Hence, we propose Refined Sketch Newton (Algorithm 4) where refine iterations are used similar to ReSubNewton. Different types of sketching matrices have the same algorithms structure of ReSkeNewton. But, the computational cost of ReSkeNewton will be different if different types of sketching matrices used in algorithm. The most popular two kinds of sketching matrices are leverage-score sketching matrix and sparse embedding matrix because they can achieve sketching in input sparsity.

We give the properties of ReSubNewton and ReSkeNewton in the following theorems.

Theorem 4

Let Assumptions. (3) and Eqn. (4) hold, and and be given. If the sample size is set as , then Algorithm 3 has the following convergence properties:

-

1.

If , then the sequence converges superlinearly.

-

2.

If and is Lipschitz continuous, then the sequence converges quadratically.

Besides, iterations of the inner loop of Algorithm 3 are at most .

Theorem 5

Let Assumptions (3) and Eqn. (4) hold, and and be given. If is an -subspace embedding matrix for , then Algorithm 4 has the following convergence properties:

-

1.

If , then the sequence converges superlinearly.

-

2.

If and is Lipschitz continuous, then the sequence converges quadratically.

Besides, iterations of the inner loop are at most .

When , where and , ReSubNewton can be viewed as a special case of ReSkeNewton. And random sampling sketching matrix can be constructed just as described in Subsection 2.2.

Corollary 6

4.2 Algorithm Analysis

We conduct comparison between ReSubNewton and ReSkeNewton. First, they have different application scenarios. ReSubNewton is suitable for problems of the form (1) and ReSkeNewton applies to the problem where Hessian is of the form and () is explicitly available. Furthermore, ReSkeNewton has a better theoretical property; that is, to achieve (10), the sampled size of ReSubNewton depends on linearly, where is commonly referred to as the condition number, and sketched dimension of ReSkeNewton is independent on , i.e., condition number independent. Hence, the sketched dimension can be small even Hessian matrix is ill-conditioned which is very attractive in practice.

In our algorithms, is refined to approximate more accurately within the inner loop. The main calculation cost of the inner loop is matrix multiplications and . Note that can be calculated cheaply without explicit Hessian by a ‘Hessian-free’ technique [3, 16]. Especially, in many machine learning problems the loss functions take the following linearly-parameterized form: , where is the label of the -th input data , thus can be computed in input sparsity of the data matrix which is very efficient when the data matrix is sparse. Besides, iterations of the inner loop are at most by Theorems 4 and 5, hence, the number of iterations of the inner loop is small if we choose a moderate small .

What’s more, our algorithms are very robust because is satisfied in each iteration. We can extend our method to other sub-sampled Newton methods, the failure probability of algorithms can be reduced to by checking the defined in (6) with little additional cost.

4.3 Application Range

ReSubNewton and ReSkeNewton both need to compute the inverse of sub-sampled or sketched Hessian which cost arithmetic operations by Cholesky decomposition in general case which is similar to SubNewton and SkeNewton. Hence, ReSubNewton and ReSkeNewton are more suitable for the cases where is moderate or small.

In fact, our algorithms still have advantages in real applications even when is large. Without loss of generality, we conduct comparison between ReSkeNewton with other existing algorithms and we assume that . Similar result also holds for ReSubNewton. When is large, the Byrd et al. [3] proposed to use sub-sampled Newton method with conjugate gradient to approximate . The convergence rate of conjugate gradient linearly depends on i.e. because . It costs to approximate , when is a dense matrix. As to our algorithm, it requires to compute and to compute the inner loop. Therefore, our algorithm has comparable or better performance when is large. The running time of LiSSA [1] also depends on condition number. Hence, even when is large, our algorithms are competitive because is commonly ill-conditioned in machine learning application.

When is sparse which is also common in machine learning problems, we sketch to get using leverage-score sampling. Then we conduct QR decomposition to get with Givens operations in a proper order. This decomposition is fast and is a sparse matrix because is a sparse matrix. For similar reason, is sparse and can be computed efficiently. Besides, in the inner loop can be computed efficiently in the manner . Combining Hessian-free technique, the inner loop is very efficient when is sparse.

Hence, our algorithms have good performance in real machine learning problem.

4.4 Comparison with previous work

Next, we compare our main algorithms with other main variants of sub-sampled Newton methods.

First, our algorithms are both condition number independent when Hessian matrix is of the form . The previous variants of sub-sampled Newton methods are all condition number dependent. Hence, our algorithms need much less samples than previous samples which means faster speed.

Before our work, several sub-sampled Newton methods with superlinear convergence rate have been proposed. Roosta-Khorasani and Mahoney [20] and Pilanci and Wainwright [17] proposed to reduce the value of in NaSubNewton and SkeNewton to as iteration goes. Though these methods can achieve superlinear convergence rate, the sub-sampled size or the sketched dimension will go beyond which will become the exact Newton method and lose computational efficiency. Furthermore, for suggested in [17], it will not accelerate convergence much in real applications though it converges superlinearly. Thus, our algorithms are the first practical sub-sample Newton method with superlinear convergence rate.

Finally, our algorithms can achieve quadratic convergence rate when is Lipschitz continuous. It is the first time that variant of sub-sampled Newton achieve quadratic convergence rate.

We summarize our comparisons in Table 1.

| -independent |

|

|

|||||

|---|---|---|---|---|---|---|---|

| SubNewton[3, 20] | No | No | No | ||||

| SkeNewton[17] | No | No | No | ||||

| Newsamp[9] | Ye | No | No | ||||

| LiSSA[1] | No | No | No | ||||

| ReSubNewton | Yes, when | Yes | Yes | ||||

| ReSkeNewton | Yes | Yes | Yes |

5 Beyond Refined Sub-sampled Newton Methods

In this section, we bring in the perspective of inexact Newton to analyze variants of sub-sampled Newton Methods and propose a unifying framework.

5.1 Unifying Framework

The existing variants of sub-sampled Newton methods have close relationship. For example, if we let be big enough, ReSubNewton and ReSkeNewton will reduce to SubNewton and SkeNewton, respectively. In fact, NewSamp [9], LiSSA [1], sub-sampled Newton with conjugate gradient [3] and sub-sampled Newton with non-uniformly sampling [26], they all can be cast into inexact Newton. We give Theorem 7 which is a framework of analyzing convergence properties of variants of sub-sampled Newton methods and the basis of designing new sub-sampled Newton type algorithms.

Theorem 7

Suppose that exists and is continuous in a neighborhood of a minimizer , with being positive definite. Assuming that is the sub-sampled Hessian and . Then defined in (6) satisfies the following property:

For sub-sampled newton update , we have the following convergence properties:

-

1.

If for all , then the sequence converges to optimal linearly with rate .

-

2.

If for all and , then the sequence converges to optimal superlinearly.

-

3.

If for all , and is Lipschitz continuous for near , the sequence has linear-quadratic convergence rate

where is a constant and is the Lipschitz constant. Hence, sequence starts with a quadratic rate of convergence which will transform to linear rate later to optimal .

-

4.

If for all , is Lipschitz continuous for near and , then the sequence converges to optimal quadratically.

From Theorem 7, we can find something important insights.

First, Lipschitz continuity of is not necessary for linear convergence and superlinear convergence rate of sub-sampled Newton methods. This reveals the reason for NewSamp can be used in training SVM where Lipschitz continuity is not satisfied. Lipschitz continuity condition is only needed to get a quadratic convergence or linear-quadratic convergence. This explains the phenomena that LiSSA[1], NewSamp [9], sub-sampled Newton with non-uniformly sampling [26], Sketched Newton [17] etc. all have linear-quadratic convergence rate because they all assume that Hessian is Lipschitz continuous.

Second, Theorem 7 provide sufficient conditions to get superlinear and quadratic convergence rate, the sufficient condition relies on . Hence, any method which decreases can achieve the better convergence property.

5.2 Regularized Subsampled Newton

When the Hessian matrix is ill-conditioned, we need to a lot of samples to guarantee sub-sampled Newton methods work since the sample size is dependent on condition number. Similarly, sketched Newton methods have to sketch to a higher dimension. To reduce the influence of condition number, regularized sub-sampled Newton methods are proposed. The main two algorithms are depicted in Algorithm 7 and Algorithm 8.

Theorem 8

Assumption (3) holds, and is the -th eigenvalue of defined in Algorithm 7. Then defined in Theorem 7 has the following bound:

If (by choosing and properly), then Algorithm 7 has the following convergence properties:

-

1.

The sequence converges linearly with probability .

-

2.

If is Lipschitz continuous, then the sequence has a linear-quadratic convergence rate with probability .

Theorem 8 explains the empirical results that Newsamp is applicable in training SVM which the Lipschitz continuity condition is not satisfied [9]. It is worth pointing out that the result about the linear convergence rate without Lipschitz continuity is unknown before.

Theorem 9

Assumption (3) holds, and is the -th eigenvalue of . Then defined in Theorem 7 has the following bound:

If (by choosing properly), then Algorithm 8 has the following convergence properties:

-

1.

The sequence converges linearly with probability .

-

2.

If is Lipschitz continuous, then the sequence has a linear-quadratic convergence rate with probability .

We conduct comparison between Theorem 8 and Theorem 9. If we set in Theorem 8 and set to satisfy in Theorem 9, then we can see that the convergence properties of Theorem 8 and Thereom 9 are the same. Algorithm 8 do not need to perform SVD comparing to Algorithm 7. In fact, Algorithm 7 proposes a method to choose in Algorithm 8.

5.3 Inexact Subsampled Newton

In light of inexact Newton method, can also be computed inexactly by optimizing the following problem

| (11) |

This scheme has been used in several work [3, 21, 26]. Conjugate gradient is the most popuplar method to solve above problem [3, 26]. When optimization problem (11) solved inexactly, we have the following property.

Theorem 10

We assume that is the sub-sampled Hessian and is an approximate solution satisfying , where . We define and . If , for update , we have the following convergence properties:

-

1.

The sequence converges linearly.

-

2.

If is Lipschitz continuous, then the sequence has a linear-quadratic convergence rate.

Lemma 7 in [26] gives a similar convergence result to Theorem 10. However, Theorem 10 are preferable due to two advantages. The first one is that the condition can be easily checked in optimization procedure. The condition is in [26]. This condition is very hard to check in the procedure of solving (11), hence, it has to stop the optimization iteration by experience. The second one is that Theorem 10 does not need Lipschitz continuity condition to get a linear convergence rate.

5.4 Subsampled Hessian and Gradient

In fact, we can also subsample gradient to accelerate sub-sampled Newton method depicted in Algorithm 6 [3, 20].

Theorem 11

We assume that is the sub-sampled Hessian and is a sub-sampled gradient constructed in Algorithm 6 satisfying . We define and . If , for update , where , Algorithm 6 have the following convergence properties:

-

1.

The sequence converges linearly.

-

2.

If is Lipschitz continuous, then the sequence has a linear-quadratic convergence rate.

Theorem 13 in [20] got an R-linear convergence rate which is , where and is a constant. To get R-linear convergence with rate , it needs and , where is a constant. This means that it has to increase sampling gradients quickly as iteration goes. As a contrast, Theorem 11 need to increase the number of sampled gradients much slower to achieve linear since convergence since is a constant. Hence, our result is more attractive.

In common case, sub-sampled gradient needs to subsample over percents samples to guarantee as iteration goes. Roosta-Khorasani and Mahoney [20] showed that it needs , where for . When is close to , is large in common cases. This is the reason why Newton method and variants of sub-sampled Newton methods are very sensitive to the accuracy of sub-sampled gradient.

5.5 Discussion

In fact, the perspective of inexact Newton procedure may provide potential inspirations for developing more efficient sub-sampled Newton methods. For example, Byrd et al. [3] proposed use to conjugate method to solve approximately, where and are sub-sampled Hessian and sub-sampled gradient respectively. This is a method combining inexact Subsampled Newton with sub-sampled gradient.

6 Empirical Study

In this section we present experimental evaluation for our algorithms. We perform the experiments for binary classification problems. We use the following popular and standard Ridge Logistic Regression

where is the -th input vector, is the -th label and is the number of training samples. A small value of often means a hard optimization problem of Ridge Logistic Regression for sub-sampled Newton methods. We perform optimization over Ridge Logistic Regression on four data sets: Nomao, Covertype, a9a, and w8a. We give the detailed description of the datasets in Table 2.

| Dataset | sparsity | source | ||

|---|---|---|---|---|

| Nomao | dense | [4] | ||

| Covertype | dense | [2] | ||

| a9a | [18] | |||

| w8a | [18] |

We set in ReSubNewton and Newton-CG. Subsampled Newton with conjuate gradient(SNCG) will obtain a satisfying . In our experiment, we implement ReSubNewton as Algorithm 5. Besides, the first sevral iterations of ReSubNewton are implemented in Subsampled Newton with conjugate gradient to achieve faster speed. This scheme is reasonable for ReSubNewton because it will reduce to SubNewton if we set big enough in Algorithm 3.

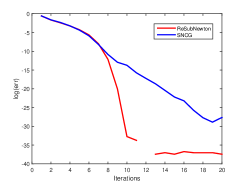

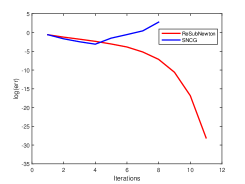

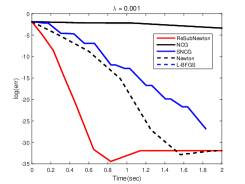

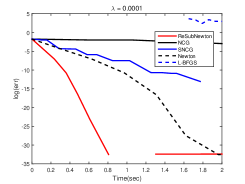

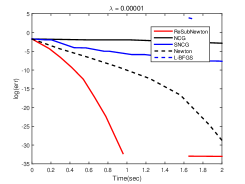

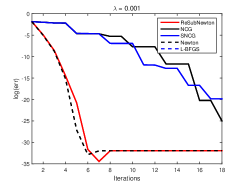

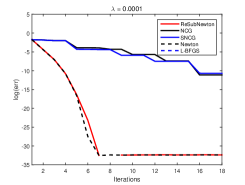

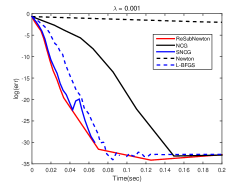

First, we compare ReSubNewton with Subsampled Newton with conjugate gradient. In the experiment, ReSubNewton and SNCG will subsample the same number of samples. We will change the sampling number and compare their convergence properties. We conduct our experiment on ’w8a’ and set . The result is shown in Figure 1. As we can see, ReSubNewton is very robust. It converges superlinearly even when there are only percents of samples. In contrast, SNCG converges linearly only when sampling percents. This is because ReSubNewton is independent of condition number just as Corollary 6 shows. However, the sampling number of SubSampled Newton and Sketched Newton both depends on condition number [20, 17]. That is the reason why ReSubNewton is much robust than Subsampled Newton. Similarly, ReSkeNewton is also independent of condition number.

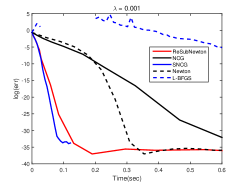

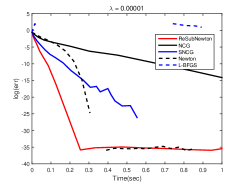

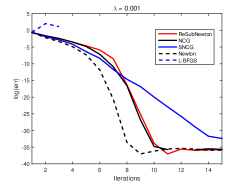

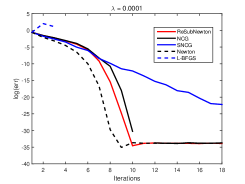

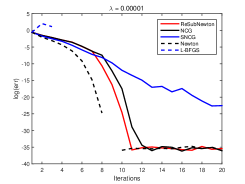

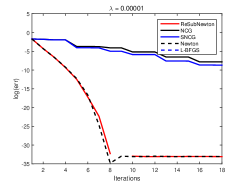

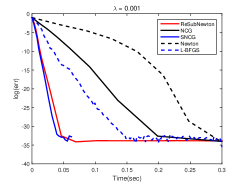

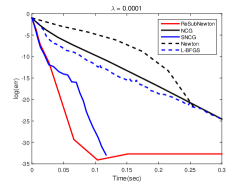

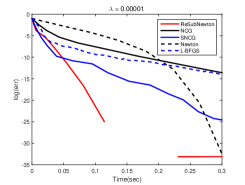

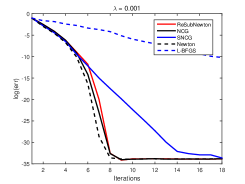

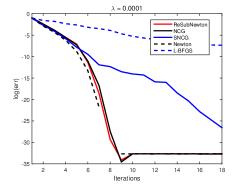

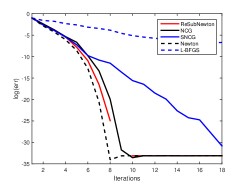

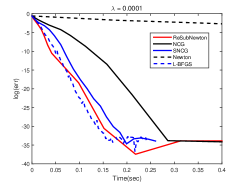

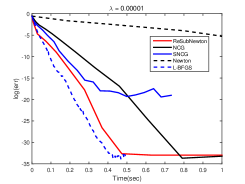

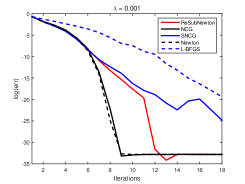

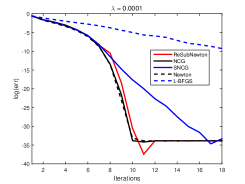

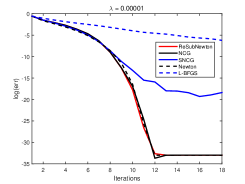

Then, we compare ReSubNewton with BFGS and several important algorithms, including the standard Newton method, Newton-CG(NCG), sub-sampled Newton with conjuate gradient(SNCG). In this paper, we do not compare with SkeNewton and ReSkeNewton because the Hessian of Ridge Logistic Regression if of the form . And Corollary 6 implies that SubNewton and ReSubNewton is a special case of SkeNewton and ReSkeNewton respectively in this case with some tranformation. In the experiment, we set different value to to compare the performance of algorithms in different condition number.

We report results in Figure 2, 3, 4 and 5. As we can see, ReSubNewton achieves superlinear convergence rates on all datasets which are even close to quadratic convergence rates on all datasets. SNCG starts with quadratic convergence rate and transform into linear convergence rate. Furthermore, we can find that ReSubNewton is very robust to the value of and datasets from experiments. When , other algorithms all perform poorly, ReSubNewton still keeps a superlinear convergence rate and fast speed. Besides, SNCG, NCG and BFGS all show poor performance on ’covertype’, however, ReSubNewton convergence very fast and has great advantages on running time. In our experiments, SNCG, NCG and BFGS all show sensitivity to the value of and dataset. They have good performance, when is big which means a well-conditioned Hessian matrix. However, when is small which leads to ill-conditioned Hessian matrix in our experiments, they obtain poor performance. Hence, ReSubNewton is more robust and efficient than SNCG, NCG and BFGS.

7 Conclusion

In this paper we have proposed two novel sub-sampled Newton methods called ReSubNewton and ReSkeNewton. They are the first practical sub-sampled Newton method which can achieve superlinear and quadratic convergence rate. We have developed a more general proof framework from a perspective of inexact Newton, which unifies several existing sub-sampled Newton methods. The framework is a fundamental of convergence analysis of sub-sampled Newton methods. Accordingly, we have shown several new convergence properties of sub-sampled Newton methods, which are important both in theory and real application. The empirical studies have validated the efficiency of our algorithms. Our work would be potentially useful for sub-sampled Newton methods.

A Some Important Lemmas

Lemma 12

Proof Consider i.i.d random matrces such that for all . Then, we have for all . By (3) and the positive semi-definite property of , we have and . By Matrix Chernoff bound, we have that if , holds with probability at least .

We define random maxtrices for all . We have , and . By Matrix Bernstein, we have

When , holds with probability at least .

Lemma 13 ([24])

If are symmetric nonsingular matrix, and , where , then for the optimization problem , we have

where and . Besides, if we set , and , then .

B Proof of Theorem 3

Proof of Theorem 3 Since is positive definite at , it has

| (12) |

where

Because is continuous near , it holds that

| (13) |

| (14) |

and

if , where and . The equation (B) is equivalent to

| (15) |

since .

By (13), we can assume that

| (16) |

for all sufficiently close to . Therefore, we have from (6) that the inexact Newton step satisfies

| (17) |

where the second inequality is because and . Combining Taylor’s theorem and the continuity of , we obtain

| (18) | ||||

| (19) | ||||

Inequality (19) follows the definition of and (16). And inequality (18) is because is continuous near . If , we have

We define . Therefore, we have

| (20) | ||||

| (21) | ||||

| (22) | ||||

| (23) |

Equation (20) and (21) follow from (15) and inequality (22) is because of (12). Equation (23) just omits since .

Hence, we obtain

The proof is similar when is Lipschitz continous near with parameter . We have

| (24) |

and

| (25) |

when is sufficiently close to .

C Proofs of theorems of Section 5

Proof of Theorem 7

We have

For convergence rate analysis, the first convergence rate result can derived directly from Equation (8). The second one follows from Equation (8) and when , and . For the third convergence result, Equation (9) leads to the convergence rate and shows that when is big enough that holds, sequence will start with a quadratic rate of convergence. However, when will decrease to a small value, and will not hold any more which leads to a linear convergence rate. The forth one is because when by Equation (9).

Proof of Theorem 8

We have

By Lemma 12 with and , with probability at least , it holds that

Besises, we have

Hence, has the following upper bound:

The convergence rate can be derived directly from Theorem 7.

Proof of Theorem 9

We have

By Lemma 12 and , with probability at least , it holds that

Besises, we have

Hence, has the following upper bound:

The convergence rate can be derived directly from Theorem 7.

D Convergence Analysis of ReSubNewton and ReSkeNewton

Proof of Theorem 4

By Lemma 12, when , in Algorithm 3 has the following property:

Above property implies the following:

By Lemma 13, after iterations of inner loop of Algorithm 3, we have

| (28) |

We also have

| (29) | |||

| (30) |

Hence, to satisfy the condition , it needs

| (31) |

Combining (28), (29), (30) and (31), we reach the result that if

then .

The convergence properties can be derived directly from Theorem 7.

Proof of Theorem 5 If is an -subspace embedding matrix for , then we have

| (32) |

By simple transformation and omitting , (32) can be transformed into

The rest of proof is the same to that of Theorem 4.

Proof of Corollary 6 We first define . We sample rows of uniformly and construct random sampling sketching matrix as in Subsection 2.2. Then, we have . In the construction of , we need that for all , where is the -th leverage score of , hence, . So, when , we have

The last Equation is because and . The rest of proof is the same to that of Theorem 4.

E Examples of Analyzing Convergence Properties of some variants of Sub-sampled Newton methods

Theorem 14

If Eqn. (3) and Eqn. (4) hold and let and be given. is set as Algorithm 1 and is constructed as in Algorithm 1. Then for , we have the following convergence properties:

-

1.

If , sequence converges linearly with probability .

-

2.

If as grows, then sequence converges superlinearly with probability .

-

3.

If is a constant, and is Lipschitz continuous, then sequence has a linear-quadratic convergence rate with probability .

Proof of Theorem 14 By Lemma 12 with , we have

By above result and the definition of in Theorem 7, we obtain

The convergence rate can be derived directly from Theorem 7.

For Sketch Newton method [17], a similar result can be reached.

Theorem 15

If Eqn. (3) and Eqn. (4) hold and let and be given. Assume Hessian matrix is of the form and is available, where is a matrix of dimension , is an -subspace embedding matrix for with probability at least . Then for , Algorithm 2 has the following convergence properties:

-

1.

If , sequence converges linearly with probability .

-

2.

If as grows, then sequence converges superlinearly with probability .

-

3.

If is a constant, and is Lipschitz continuous, then sequence has a linear-quadratic convergence rate with probability .

Proof We give the SVD decomposition of as follow:

We give the bound of as follow:

where the inequality follows from the property of -subspace embedding.

For , we have

Hence, can be bounded as follow:

The convergence rate can be derived directly from Theorem 7.

References

- Agarwal et al. [2016] Naman Agarwal, Brian Bullins, and Elad Hazan. Second order stochastic optimization in linear time. arXiv preprint arXiv:1602.03943, 2016.

- Blackard and Dean [1999] Jock A Blackard and Denis J Dean. Comparative accuracies of artificial neural networks and discriminant analysis in predicting forest cover types from cartographic variables. Computers and electronics in agriculture, 24(3):131–151, 1999.

- Byrd et al. [2011] Richard H Byrd, Gillian M Chin, Will Neveitt, and Jorge Nocedal. On the use of stochastic hessian information in optimization methods for machine learning. SIAM Journal on Optimization, 21(3):977–995, 2011.

- Candillier and Lemaire [2012] Laurent Candillier and Vincent Lemaire. Design and analysis of the nomao challenge active learning in the real-world. In Proceedings of the ALRA: Active Learning in Real-world Applications, Workshop ECML-PKDD, 2012.

- Clarkson and Woodruff [2013] Kenneth L Clarkson and David P Woodruff. Low rank approximation and regression in input sparsity time. In Proceedings of the forty-fifth annual ACM symposium on Theory of computing, pages 81–90. ACM, 2013.

- Cotter et al. [2011] Andrew Cotter, Ohad Shamir, Nati Srebro, and Karthik Sridharan. Better mini-batch algorithms via accelerated gradient methods. In Advances in neural information processing systems, pages 1647–1655, 2011.

- Dembo et al. [1982] Ron S Dembo, Stanley C Eisenstat, and Trond Steihaug. Inexact newton methods. SIAM Journal on Numerical analysis, 19(2):400–408, 1982.

- Drineas et al. [2012] Petros Drineas, Malik Magdon-Ismail, Michael W Mahoney, and David P Woodruff. Fast approximation of matrix coherence and statistical leverage. Journal of Machine Learning Research, 13(Dec):3475–3506, 2012.

- Erdogdu and Montanari [2015] Murat A Erdogdu and Andrea Montanari. Convergence rates of sub-sampled newton methods. In Advances in Neural Information Processing Systems, pages 3034–3042, 2015.

- Golub and Van Loan [2012] Gene H Golub and Charles F Van Loan. Matrix computations, volume 3. JHU Press, 2012.

- Johnson and Zhang [2013] Rie Johnson and Tong Zhang. Accelerating stochastic gradient descent using predictive variance reduction. In Advances in Neural Information Processing Systems, pages 315–323, 2013.

- Li et al. [2013] Mu Li, Gary L Miller, and Richard Peng. Iterative row sampling. In Foundations of Computer Science (FOCS), 2013 IEEE 54th Annual Symposium on, pages 127–136. IEEE, 2013.

- Li et al. [2014] Mu Li, Tong Zhang, Yuqiang Chen, and Alexander J Smola. Efficient mini-batch training for stochastic optimization. In Proceedings of the 20th ACM SIGKDD international conference on Knowledge discovery and data mining, pages 661–670. ACM, 2014.

- Meng and Mahoney [2013] Xiangrui Meng and Michael W Mahoney. Low-distortion subspace embeddings in input-sparsity time and applications to robust linear regression. In Proceedings of the forty-fifth annual ACM symposium on Theory of computing, pages 91–100. ACM, 2013.

- Nemirovski et al. [2009] Arkadi Nemirovski, Anatoli Juditsky, Guanghui Lan, and Alexander Shapiro. Robust stochastic approximation approach to stochastic programming. SIAM Journal on Optimization, 19(4):1574–1609, 2009.

- Nocedal and Wright [2006] Jorge Nocedal and Stephen Wright. Numerical optimization. Springer Science & Business Media, 2006.

- Pilanci and Wainwright [2015] Mert Pilanci and Martin J Wainwright. Newton sketch: A linear-time optimization algorithm with linear-quadratic convergence. arXiv preprint arXiv:1505.02250, 2015.

- Platt [1999] John C Platt. 12 fast training of support vector machines using sequential minimal optimization. Advances in kernel methods, pages 185–208, 1999.

- Robbins and Monro [1951] Herbert Robbins and Sutton Monro. A stochastic approximation method. The annals of mathematical statistics, pages 400–407, 1951.

- Roosta-Khorasani and Mahoney [2016a] Farbod Roosta-Khorasani and Michael W Mahoney. Sub-sampled newton methods ii: Local convergence rates. arXiv preprint arXiv:1601.04738, 2016a.

- Roosta-Khorasani and Mahoney [2016b] Farbod Roosta-Khorasani and Michael W Mahoney. Sub-sampled newton methods i: globally convergent algorithms. arXiv preprint arXiv:1601.04737, 2016b.

- Roux et al. [2012] Nicolas L Roux, Mark Schmidt, and Francis R Bach. A stochastic gradient method with an exponential convergence _rate for finite training sets. In Advances in Neural Information Processing Systems, pages 2663–2671, 2012.

- Schmidt et al. [2013] Mark Schmidt, Nicolas Le Roux, and Francis Bach. Minimizing finite sums with the stochastic average gradient. arXiv preprint arXiv:1309.2388, 2013.

- Spielman [2015] Daniel A. Spielman. Spectral graph theory. University Lecture, 2015.

- Woodruff [2014] David P Woodruff. Sketching as a tool for numerical linear algebra. arXiv preprint arXiv:1411.4357, 2014.

- Xu et al. [2016] Peng Xu, Jiyan Yang, Farbod Roosta-Khorasani, Christopher Ré, and Michael W Mahoney. Sub-sampled newton methods with non-uniform sampling. arXiv preprint arXiv:1607.00559, 2016.

- Zhang et al. [2013] Lijun Zhang, Mehrdad Mahdavi, and Rong Jin. Linear convergence with condition number independent access of full gradients. In Advance in Neural Information Processing Systems 26 (NIPS), pages 980–988, 2013.