Weak convergence of a pseudo maximum likelihood estimator for the extremal index

Abstract.

The extremes of a stationary time series typically occur in clusters. A primary measure for this phenomenon is the extremal index, representing the reciprocal of the expected cluster size. Both a disjoint and a sliding blocks estimator for the extremal index are analyzed in detail. In contrast to many competitors, the estimators only depend on the choice of one parameter sequence. We derive an asymptotic expansion, prove asymptotic normality and show consistency of an estimator for the asymptotic variance. Explicit calculations in certain models and a finite-sample Monte Carlo simulation study reveal that the sliding blocks estimator outperforms other blocks estimators, and that it is competitive to runs- and inter-exceedance estimators in various models. The methods are applied to a variety of financial time series.

Key words. Clusters of extremes, extremal index, stationary time series, mixing coefficients, block maxima.

Abstract.

Appendices A and B contain the proofs of the auxiliary lemmas in Section 9 and 10 from the main paper, respectively. The proof of Theorem 3.1 is given in Appendix C, and additional results from the main paper are proven in Appendix D. Finally, additional simulation results are presented in Appendix E.

1. Introduction

An adequate description of the extremal behavior of a time series is important in many applications, such as in hydrology, finance or actuarial science (see, e.g., Section 1.3 in the monograph Beirlant et al., 2004). The extremal behavior can be characterized by the tail of the marginal law of the time series and by the serial dependence; that is, by the tendency that extremal observations tend to occur in clusters. A primary measure of extremal serial dependence is given by the extremal index , which can be interpreted as being equal to the reciprocal of the mean cluster size. The underlying theory was worked out in Leadbetter (1983); Leadbetter et al. (1983); O’Brien (1987); Hsing et al. (1988); Leadbetter and Rootzén (1988).

Estimating the extremal index based on a finite stretch from the time series has been extensively studied in the literature. Common approaches are based on the blocks method, the runs method and the inter-exceedance times method (see Beirlant et al., 2004, Section 10.3.4, for an overview). The first two methods usually depend on two parameters to be chosen by the statistician: a threshold sequence and a cluster identification scheme parameter (such as a block length). In contrast, inter-exceedance type-estimators are attractive since they only depend on a threshold sequence. Some references are Hsing (1993); Smith and Weissman (1994); Weissman and Novak (1998); Ferro and Segers (2003); Süveges (2007); Robert (2009); Robert et al. (2009); Süveges et al. (2010), among others. The present paper is on a blocks estimator (and a slightly modified version) due to Northrop (2015), which, remarkably, only depends on a cluster identification parameter. This makes the estimator practically appealing in comparison to other blocks methods.

In many papers on estimating the extremal index, either no asymptotic theory is given (such as in Süveges, 2007; Northrop, 2015), or the asymptotic theory is incomplete in the sense that theory is developed for a non-random threshold sequence, while in practice a random sequence must be used (as, e.g., in Weissman and Novak, 1998; Robert et al., 2009). As pointed out in the latter paper, “the mathematical treatment of such random threshold sequences requires complicated empirical process theory”. In the present paper, the mathematical treatment is comprehensive, working out all the arguments needed from empirical process theory.

Let us proceed by motivating and defining the estimator: throughout, denotes a stationary sequence of real-valued random variables with stationary cumulative distribution function (cdf) . The sequence is assumed to have an extremal index : for any , there exists a sequence such that and such that

Here, and .

For simplicity, we assume that is continuous (c.f. Remark 3.6 below) and define a sequence of standard uniform random variables by . For , let and , where denotes the generalized, left-continuous inverse of the cdf . Then, and as , whence

| (1.1) | ||||

| (1.2) |

where . In other words, both and asymptotically follow an exponential distribution with parameter . The result concerning inspired Northrop (2015) to estimate by the maximum likelihood estimator for the exponential distribution, based on a sample of estimated block maxima.

More precisely, suppose that we observe a stretch of length from the time series . Divide the sample into blocks of length , and for simplicity assume that (otherwise, the final block would consist of less than observations and should be omitted). For , let

denote the maximum over the from the th block. Also, let and . If is sufficiently large, then, by (1.2), the (unobservable) random variables form an approximate sample from the Exponential-distribution. Moreover, as common when working with block maxima of a time series, they may be considered as asymptotically independent, which prompted Northrop (2015) to estimate by the maximum-likelihood estimator for the Exponential distribution:

Note that should not be considered an estimator, as it is based on the unknown cdf . Subsequently, we call an oracle for .

In practice, the are not observable, whence they need to be replaced by their observable counterparts giving rise to the definitions

where denotes the empirical cdf of . We obtain, up to a bias correction discussed below, Northrop’s estimator

| (1.3) |

In Northrop (2015), no asymptotic theory on given. While deriving the asymptotic distribution of the oracle may appear tractable (see also Robert, 2009: essentially, a central limit theorem for rowwise dependent triangular arrays is to be shown, followed by an argument using the delta method), asymptotic theory on the estimator is substantially more difficult due to the additional serial dependence induced by the rank transformation (which on top of that operates between blocks instead of within blocks).

A central contribution of the present paper is the derivation of the asymptotic distribution of . It will further turn out that the impact of the rank transformation is non-negligible, resulting in different asymptotic variances of and the corresponding oracle . For that purpose, it will be convenient to consider the following (mathematically simpler) variant of Northrop’s estimator,

| (1.4) |

This estimator can either be motivated following the above lines, but using (1.1) rather than (1.2) as a starting point, or by consulting Robert (2009) and writing

| (1.5) |

with denoting Robert’s estimator for (page 275 in Robert, 2009, with ‘’ replaced by ‘’ in his definition of ). We will show below (Theorem 3.1) that and are in fact asymptotically equivalent. We also present asymptotic theory for modifications of and based on sliding block maxima, which is the second main contribution of the paper. Finally, the asymptotic expansions for suggest estimators for the asymptotic variance of and (and its sliding blocks variants); proving their consistency is the third main contribution.

The remaining parts of this paper are organized as follows: in Section 2, we present mathematical preliminaries needed to formulate and derive the asymptotic distributions of the estimators for . Asymptotic equivalence, consistency and asymptotic normality is then shown in Section 3. Estimators of the asymptotic variance are handled in Section 4. In Section 5, we propose a simple device to reduce the bias of the estimator and relate it to the ad-hoc approach in Northrop (2015). Examples are worked out in detail in Section 6, while finite-sample results and a case study are presented in Sections 7 and 8, respectively. Sections 9 and 10 contain a sequence of auxiliary lemmas needed for the proof of the main results. Their proofs, as well as additional proofs are postponed to the supplementary material (Appendices A, B, C and D). The supplementary material also contains additional simulation results (Appendix E).

2. Mathematical preliminaries

The serial dependence of the time series will be controlled via mixing coefficients. For two sigma-fields on a probability space , let

In time series extremes, one usually imposes assumptions on the decay of the mixing coefficients between sigma-fields generated by and , where is some sequence reflecting the fact that only the dependence in the tail needs to be restricted (see, e.g., Rootzén, 2009). For our purposes, we need slightly more to control even the dependence between the smallest of all block maxima (see also Condition 2.1(v) below). More precisely, for and , let denote the sigma algebra generated by with and define, for ,

Note that the coefficients are increasing in , whence they are bounded by the standard alpha-mixing coefficients of the sequence , which can be retrieved for . In Condition 2.1(iii) below, we will impose a condition on the decay of the mixing coefficients for small values of .

The extremes of a time series may be conveniently described by the point process of normalized exceedances. The latter is defined, for a Borel set and a number , by

Note that iff ; the probability of that event converging to under the assumption of the existence of extremal index .

Fix and . For , let denote the sigma-algebra generated by the events for and . For , define

The condition is said to hold if there exists a sequence with such that as . A sequence with is said to be -separating if there exists a sequence with such that as . If is met, then such a sequence always exists, simply take

By Theorems 4.1 and 4.2 in Hsing et al. (1988), if the extremal index exists and the -condition is met (), then a necessary and sufficient condition for weak convergence of is convergence of the conditional distribution of with given that there is at least one exceedance of in to a probability distribution on , that is,

where is some -separating sequence. Moreover, in that case, the convergence in the last display holds for any -separating sequence . If the -condition holds for any , then does not depend on (Hsing et al., 1988, Theorem 5.1).

A multivariate version of the latter results is stated in Perfekt (1994), see also the summary in Robert (2009), page 278, and the thesis Hsing (1984). Suppose that the extremal index exists and that the -condition is met for any . Moreover assume that there exists a family of probability measures on such that, for all ,

where is some -separating sequence. In that case, the two-level point process converges in distribution to a point process with characterizing Laplace transform explicitly stated in Robert (2009) on top of page 278. Note that

The following set of conditions will be imposed to establish asymptotic normality of the estimators.

Condition 2.1.

-

(i)

Extremal index and the point process of exceedances. The extremal index exists and the above assumptions guaranteeing convergence of the one- and two-level point process of exceedances are satisfied.

-

(ii)

Moment assumption on the point process. There exists such that, for any , there exists a constant such that

-

(iii)

Asymptotic independence in the big-block/small-block heuristics. There exists and such that

for some with and with from Condition (ii). The block size is chosen in such a way that

(2.1) and such that there exists a sequence (to be thought of as the length of small blocks which are to be clipped-of at the end of each block of size ) satisfying and all convergences being for .

-

(iv)

Bound on the variance of the empirical process. There exist some constants such that, for all and all ,

-

(v)

All standardized block maxima of size converge to . For all , we have

where , for , denote consecutive standardized block maxima of (approximate) size .

-

(vi)

Existence of moments of maxima. With from Condition (ii), we have

-

(vii)

Bias. As ,

Assumptions (i)–(iii) are suitable adaptations of Conditions (C1) and (C2) in Robert (2009); in fact, they can be seen to imply the latter. Among other things, these conditions are needed to apply his central result, Theorem 4.1, on the weak convergence of the tail empirical process on . Note that the assumptions are satisfied for solutions of stochastic difference equations, see Example 3.1 in Robert (2009). The Assumption in (2.1) is a growth condition that is needed in the proof of Lemma 9.1. As argued in Robert et al. (2009), it is actually a weak requirement, as in many time series models it is a necessary condition for the bias condition in (vii) to be true (see Section 6 below). Finally, a positive extremal index can be guaranteed by assuming that

| (2.2) |

for any , see Beirlant et al. (2004), formula (10.8). We will additionally need this assumption for the calculation of the asymptotic variance of the estimators.

In a slightly different form concerning only the tail, Assumption (iv) has also been made in Condition (C3) in Drees (2000) for proving weak convergence of the tail empirical process. In comparison to there, the extra factor allows for additional flexibility, in that it allows for -non-negligible covariances, as long as their contribution is at most . In Section 6, we show that the assumption holds for solutions of stochastic difference equations, such as the squared ARCH-model, and for max-autoregressive models.

Recall that is approximately Beta-distributed. As a consequence, every standardized block maximum must converge to as the sample size grows to infinity. Still, out of the sample of block maxima, the smallest one could possibly be smaller than one, especially when the number of blocks is large. Assumption (v) prevents this from happening; note that a similar assumption has also been made in Bücher and Segers (2015), Condition 3.2. Imposing the assumption even for block maxima of size guarantees that also the minimum over all big sub-block maxima (needed in the proof for the disjoint blocks estimator) and the minimum over all sliding block maxima of size (needed in the proof for the sliding blocks estimator) converges to .

Assumption (vi) is needed to deduce uniform integrability of the sequence . It implies convergence of the variance of to that of an exponential distribution with parameter . Finally, (vii) requires the approximation of the first moment of by that of an exponential distribution to be sufficiently accurate.

3. Main results

In this section we prove consistency and asymptotic normality of the disjoint blocks estimators and defined in (1.3) and (1.4), respectively, as well as of variants which are based on sliding blocks and which we will denote by and , respectively. We begin by defining the latter estimators.

Divide the sample into blocks of length , i.e., for , let

Analogously to the notation used in the definition of the estimators for disjoint blocks, we will write , and and define their empirical counterparts and , where is the empirical cdf of . Just as for the disjoint blocks estimators, the (pseudo-)observations and are approximately exponentially distributed with mean , which suggests to estimate by the reciprocal of their empirical mean:

Up to a bias correction discussed below, is the sliding blocks estimator proposed in Northrop (2015). Note that, for both estimators, no data has to be discarded if is not a divisor of the sample size .

The first central result is on first order asymptotic equivalence between the proposed estimators, proven in Section C in the supplementary material.

As a consequence of this theorem, we may concentrate on the mathematically simpler estimators and in the following asymptotic analysis. We will shortly write and , respectively. Note that, while is based on a substantially larger number of blocks than the disjoint blocks estimator, the blocks are heavily correlated. The following theorem is the central result of this paper and shows that both estimators are consistent and converge at the same rate to a normal distribution. The disjoint blocks estimator has a larger asymptotic variance than the sliding blocks estimator (see also Robert et al., 2009).

It is interesting to note that the asymptotic variance of the disjoint blocks estimator is substantially more complicated than if one would naively treat the (or the ) as an iid sample from the exponential distribution with parameter (as is done in Northrop, 2015; the variance would then simply be ). A heuristic explanation can be found in Remark 3.4 below. A formal proof is given at the end of this section, with several auxiliary lemmas postponed to Section 9 (for the disjoint blocks estimator) and to Section 10 (for the sliding blocks estimator). Explicit calculations are possible for instance for a max-autoregressive process, see Section 6.1, or for the iid case.

Example 3.3.

If the time series is serially independent, a simple calculation shows that and . This implies

and therefore and . It is worthwhile to mention that these values are smaller than the variances of any of the disjoint and sliding blocks estimators considered in Robert et al. (2009), respectively. Moreover, note that asymptotic variance of the oracle is equal to , which is twice as large as when the marginal cdf is estimated. Finally, it can be seen that the same formulas are valid whenever : the fact that implies that . By (A.9) in the supplementary material, we then obtain .

Remark 3.4 (Main idea for the proof).

Define and

| (3.1) | ||||||

| (3.2) |

In the following, we only consider the disjoint blocks estimator, the argumentation for the sliding blocks estimator is similar. For the ease of notation, we will skip the upper index and just write instead of , etc. Asympotic normality of may be deduced from the delta method and weak convergence of . The roadmap to handle the latter is as follows: decompose

| (3.3) |

Using a big-block/small-block type argument, the asymptotics of the second summand on the right-hand side can be deduced from a central limit theorem for rowwise independent triangular arrays. Depending on the choice of the block sizes, an asymptotic bias term may appear, which we control by Condition 2.1(vii). The first summand is more involved, and also contributes to the limiting distribution: first, for , let

| (3.4) |

denote the tail empirical process of and let

| (3.5) |

be the empirical distribution function of . Then

| (3.6) | ||||

Since is approximately exponentially distributed with parameter , one may expect that converges to in probability, for and for any . Moreover, on an appropriate domain, for some Gaussian process (Drees, 2000, 2002; Rootzén, 2009; Robert, 2009; Drees and Rootzén, 2010), whence a candidate limit for the expression on the left-hand side of the previous display is given by The latter distribution is normal, and joint convergence of both terms on the right-hand side of (3.3) will finally allow for the derivation of the asymptotic distribution of . These heuristic arguments have to be made rigorous.

Remark 3.5 (Disjoint blocks: alternative proof).

As pointed out by a referee, the asymptotic distribution of the disjoint blocks estimator may alternatively be derived by completely relying on results in Robert (2009). The idea is as follows. First, recall (1.5), where for . Since if and only if , this expression coincides with the definition of used in Robert (2009), middle of page 275, up to a ‘’-sign replaced by a ‘’-sign in his definition of . Hence, by Theorem 4.2 in that reference, assuming the latter replacement to be asymptotically negligible, we have in some appropriate metric space, where is a Gaussian process. The continuous mapping theorem implies

again on some appropriate metric space. Some tedious, but straightforward calculations show that the random variable has the same law as the limit that we obtained with the approach stated in Remark 3.4. We do not give any further details on this approach as it is limited to the case of disjoint blocks.

Remark 3.6 (On continuity of ).

In the introduction, we assumed for simplicity that is continuous. Some thoughts reveal that the main limit relations motivating the estimators, that is (1.1) and (1.2), continue to hold under the weaker assumption that

where denotes the right endpoint of the support of . By Theorem 1.7.13 in Leadbetter et al. (1983), this condition is also necessary for the extremal index to exist. However, the proofs of our theoretical results do not easily generalize to this weaker assumption, the reason being that we heavily rely on the asymptotic equivalence of in (3.4) and on page 281 in Robert (2009) (to apply his Theorem 4.1 on weak convergence of ) and on centredness of on (to show negligibility of certain terms in Lemma 9.1 and 10.1). A further discussion is beyond the scope of this paper.

Proof of Theorem 3.2 (Disjoint blocks).

Write and . Recall the definitions of and in (3.4) and (3.5), respectively. For , let

where . Also, let and let be defined as in Lemma 9.3. Suppose we have shown that

-

(i)

For all : ;

-

(ii)

For all : as ;

-

(iii)

as .

It then follows from (3.6) and Wichura’s theorem (Billingsley, 1979, Theorem 25.5) that

By Condition 2.1(vii), we obtain that The theorem then follows from the delta-method.

The assertion in (i) is proved in Lemma 9.1. The assertion in (ii) is proved in Lemma 9.5 (it is a consequence of the continuous mapping theorem and Lemmas 9.2 and 9.4), The assertion in (iii) follows from the fact that is normally distributed with variance as specified in Lemma 9.5, and the fact that by Lemma 9.6 for . ∎

4. Variance estimation

For statistical inference on , estimators for the asymptotic variance formulas in Theorem 3.2 are needed. Unfortunately, the formulas themselves are too complicated to base such estimators on a simple plug-in principle. Rather than that, we rely on an asymptotic expansion of the disjoint blocks estimator resulting from a careful inspection of the proofs. Note that, since , an estimator for the variance of the disjoint blocks estimator can immediately be transferred into one for the sliding blocks estimator. This is particularly useful since a straightforward extension of our proposed estimator for to the sliding blocks estimator is not possible and would require the choice of an additional tuning parameter.

The proof of Theorem 3.2, in particular the central decomposition in (3.3) and the calculations in (3.6), allows to write as

where

and where denotes the th block of indices. The proof of Theorem 3.2 shows that are asymptotically independent (big block/small block heuristics) and centred, and that their empirical mean multiplied by converges to a centred normal distribution with variance . Hence, their second empirical moment should be a consistent estimator for . As the sample depends on unknown quantities, we must replace these objects by empirical counterparts, leading us to define

where . The following proposition shows that

are in fact consistent estimators for and , respectively, provided that moments of order slightly larger than exist. To simplify the proofs, we assume beta-mixing of the times series, since it allows for stronger coupling results than alpha-mixing. We also impose a further growth condition on the block size, which allows for a further simplification within the proof (which is given in in the supplementary material).

Proposition 4.1 (Consistency of variance estimators).

5. Bias reduction

While the previous sections were concerned with the -asymptotics, we will now have a heuristic look at the -asymptotics, in particular in terms of expectations. As a result, we will obtain a bias reduction scheme. Let denote any of the quantities defined in (3.1), (3.2) or Theorem 3.2. A Taylor expansion allows to write

Let . The second component is inherent to the time series itself. In many examples, it can be seen to be of the order , see for instance Section 6 or similar calculations made in (Robert et al., 2009, Section 6). Since , it seems plausible that the third component satisfies , though we will not give a precise proof. Finally, consider the first component , which is essentially due to the use of the empirical distribution function in the definition of the estimator. The following lemma gives a first-order asymptotic expansion, which turns out to be the same for the disjoint and sliding blocks estimator.

Lemma 5.1.

The proof is given in Section D. As a consequence, we have . Now, plugging-in and as a consistent estimator for and , we can estimate and by and , respectively. Subtracting these expression from , we obtain the bias-reduced estimator

The -asymptotics will not be affected, but shows a better finite-sample performance and is therefore used in Section 7.

Note that if we are additionally willing to assume that as (cf. Condition 2.1(vii)), we obtain that and are in fact the dominating bias-components. In common models, the assumption is satisfied as soon as (see Section 6). In comparison to the assumption in Condition 2.1(iii) larger block sizes are required. Similar assumptions have also been made for the bias reductions in Robert et al. (2009).

Finally, note that the bias reduction based on can actually be alternatively motivated by the fact that is equal to , where with being the empirical cdf of . The idea of using rather than has been used in Northrop (2015) as a bias reduction scheme.

6. Examples

Two examples are worked out in this section. For the max-autoregressive processes, considered in Section 6.1, explicit calculations for the asymptotic variance formulas in Theorem 3.2 are possible. These allow for a theoretical comparison with the blocks estimators from Robert (2009) and Robert et al. (2009). All assumptions imposed in Condition 2.1 are shown to hold. In Section 6.2, we consider solutions of stochastic difference equations such as ARCH-processes. Complementing results from Robert (2009) we show that Condition 2.1(iv) is satisfied.

6.1. Max-autoregressive processes

Consider the max-autoregressive process of order one, ARMAX(1) in short, defined by the recursion

where and where denotes an i.i.d. sequence of standard Fréchet random variables. A stationary solution of this recursion is given by

which shows that the stationary distribution is standard Fréchet as well. The sequence has extremal index and its cluster size distribution is geometric, i.e., for (see, e.g., Chapter 10 in Beirlant et al., 2004). Moreover, it follows from Proposition 5.3.7 in Hsing (1984) and some simple calculations that

for , where . The formula in Proposition 5.3.7 in Hsing (1984) is wrong for , but can be corrected to

for . Based on these formulas, some straightforward calculations yield

and

Note that, for , we obtain and , which corresponds to the iid scenario. The latter two displays imply

and hence

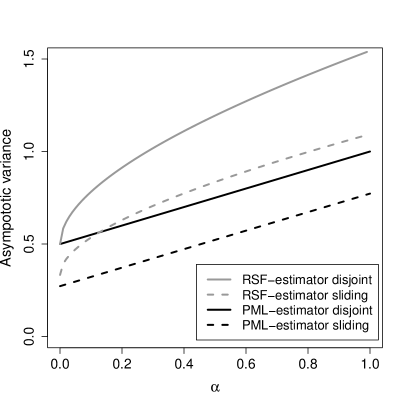

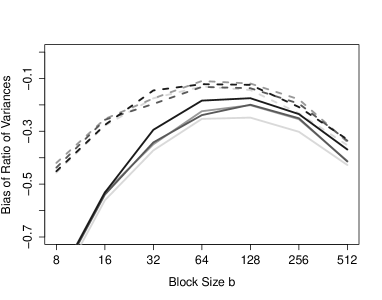

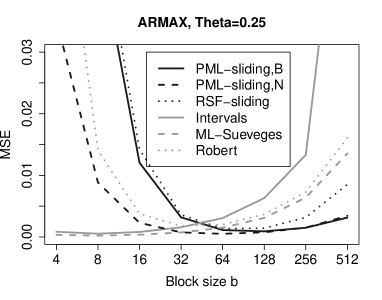

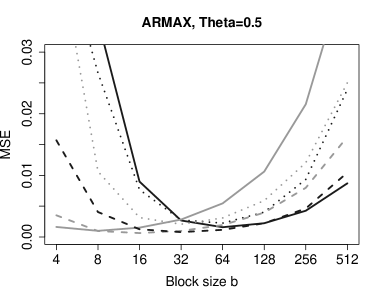

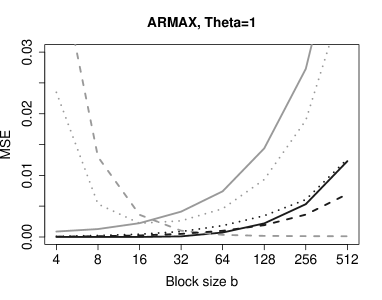

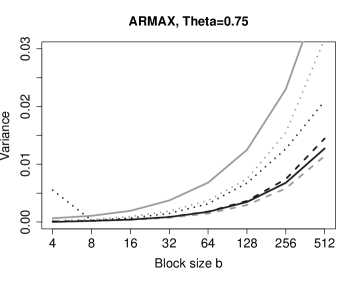

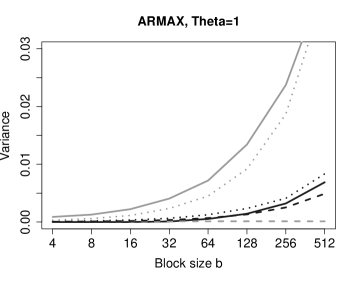

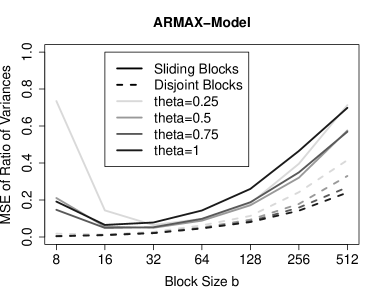

Since , the asymptotic variances of simply reduce to the affine linear functions and for the disjoint and the sliding blocks estimator, respectively. These functions can be compared with the asymptotic variance formulas in (Robert et al., 2009, Formula 5.1) and in (Robert, 2009, Page 285, variance of ). Note that the variance of in Robert (2009) is exactly the same as the one of the disjoint blocks estimator in Robert et al. (2009). The asymptotic variance formulas depend on an additional parameter to be chosen by the statistician. Assuming we would have access to the optimal value (which can be calculated numerically, but must be estimated in practice), we obtain the variance curves depicted in Figure 1. We observe that, for the ARMAX-model, the PML-estimators analyzed in this paper have a smaller asymptotic variance than the (theoretically optimal) estimators in Robert et al. (2009) and Robert (2009).

Regarding the additional assumptions in Condition 2.1, some tedious calculations show that Condition 2.1(ii) is satisfied for . can further be shown to be a geometrically ergodic Markov chain, see Formula (3.5) in Bradley (2005). As a consequence of Theorem 3.7 in that reference, is geometrically -mixing, whence Condition 2.1(iii) is satisfied (and also the condition on beta-mixing imposed in Proposition 4.1). It can be further be shown that, with , we have for all , that is, Condition 2.1(iv) is met. Moreover, a simple calculation shows that provided that . Hence, Condition 2.1(v). Based on an explicit calculation of the distribution of , it can also be seen that Condition 2.1(vi) is satisfied for any , and that . The latter implies that Condition 2.1(vii) is satisfied if , see (2.1). It can easily be seen that (2.2) is met.

6.2. Stochastic Difference Equations

Consider the equation

| (6.1) |

where are i.i.d. -valued random vectors. If and for some and some i.i.d. real-valued sequence , the above equation defines the popular (squared) ARCH(1)-time series model. For simplicity, we assume that the distribution of is absolutely continuous.

The existence of a stationary solution of (6.1) as well as the tail behavior of the stationary distribution of has been studied in Kesten (1973), Theorem 5. More precisely, consider the condition

-

(S)

There exists some such that

Under this assumption, there exists a unique stationary solution of (6.1) and the cdf of satisfies as for some constant . Moreover, is continuous (Vervaat, 1979, Theorem 3.2) and, in particular, in the max-domain of attraction of , the generalized extreme value distribution with extreme-value index .

Explicit calculations for the (two-level) cluster size distribution have been carried out in (Perfekt, 1994, Example 4.2). Unfortunately, the formulas are complicated and do not allow for simple expressions of the asymptotic variances in Theorem 3.2.

Slight adaptations of Assumptions (i)–(iii) of Condition 2.1 have been checked in (Robert, 2009, Example 3.1). We complement those results by showing that also (iv) is satisfied. The result is inspired by Section 4 in Drees (2000) and is in fact a modification of Lemma 4.1 in that paper to the present needs. Its proof is given in Section D in the supplement material.

7. Finite-sample performance

A simulation study is performed to illustrate the finite-sample performance of the proposed estimators and methods. Results are presented for four time series models:

-

•

The ARMAX-model from Section 6.1:

where and where is an i.i.d. sequence of standard Fréchet random variables. We consider resulting in .

- •

-

•

The ARCH-model:

where and where denotes an i.i.d. sequence of standard normal random variables. We consider which implies , respectively (Table 3.2 in de Haan et al., 1989).

-

•

The Markovian Copula-model (Darsow et al., 1992):

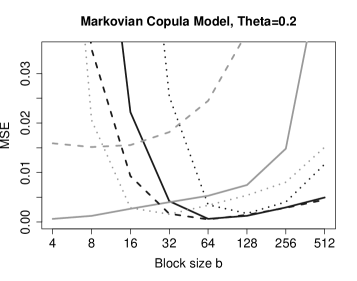

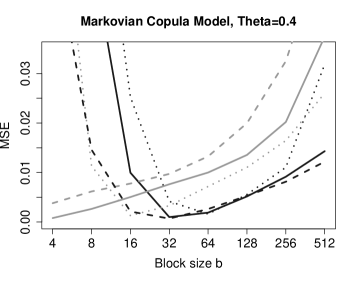

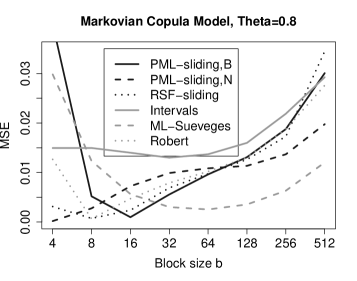

Here, is the left-continuous quantile function of some arbitrary continuous cdf , is a stationary Markovian time series of order 1 and denotes the Survival Clayton Copula with parameter . For this model, where are independent, is standard uniform and has cdf , , see Perfekt (1994) or Beirlant et al. (2004), Section 10.4.2. We consider choices such that (approximately) and fix as the standard uniform cdf (the results are independent of this choice, as the estimators are rank-based). Algorithm 2 in Rémillard et al. (2012) allows to simulate from this model.

Additional simulation results for the AR-model and the doubly stochastic process from Smith and Weissman (1994) turned out to be quite similar to the ARMAX-model and are not presented for the sake of brevity. In all scenarios under consideration, the sample size is fixed to and the block size for the blocks estimators is chosen from the set .

7.1. Comparison with other estimators for the extremal index

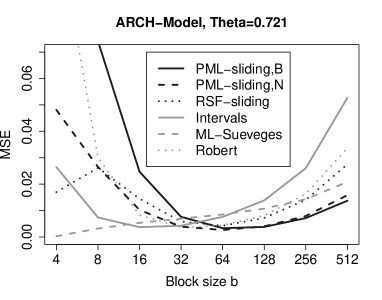

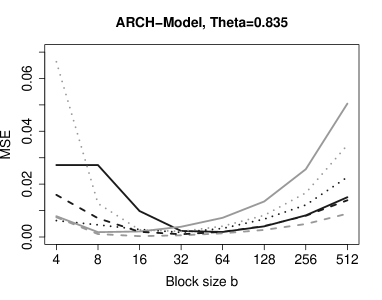

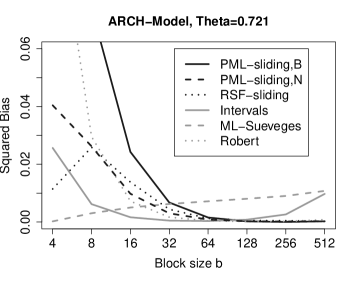

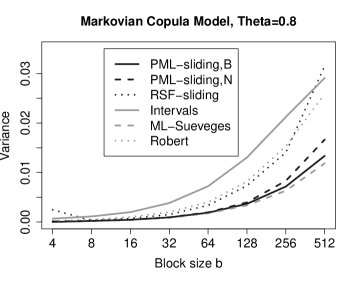

We present results for six different estimators: the bias-reduced sliding blocks estimator , the sliding blocks estimator from Northrop (2015) (i.e., , but with replaced by in the th block), the bias-reduced sliding blocks estimator from Robert et al. (2009) (with a data-driven choice of the threshold as outlined in Section 7.1 of that paper), the integrated version of the blocks estimator from Robert (2009), the intervals estimator from Ferro and Segers (2003) and the ML-estimator from Süveges (2007). Results for other versions of these estimators (e.g., the disjoint blocks versions or the versions based on a fixed threshold) are not presented as their performance was dominated by the above versions in almost all scenarios under consideration. The parameters and for the Robert-estimator (last display on page 276 of Robert, 2009) are chosen as and . The intervals estimator and the Süveges-estimator require the choice of a threshold , which we choose as the empirical quantile of the observed data. All estimators are constrained to the interval , except for Table 1 where we also report results for the unconstrained versions.

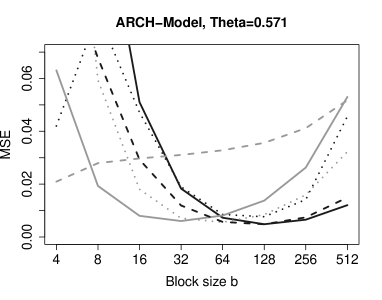

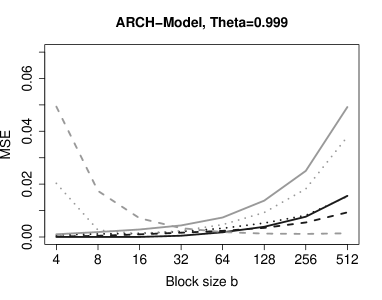

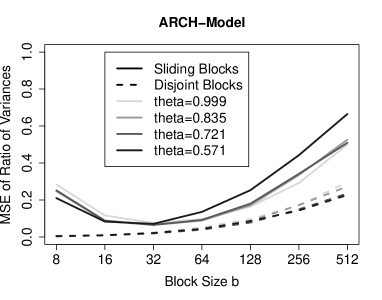

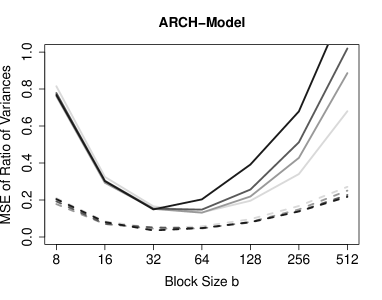

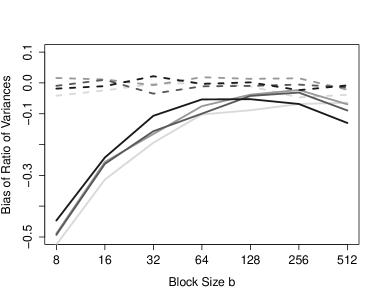

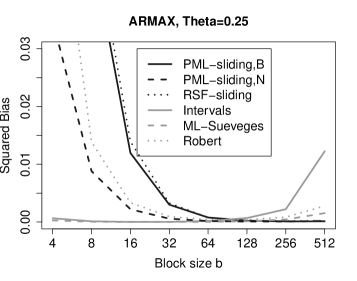

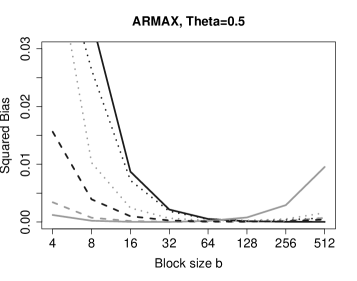

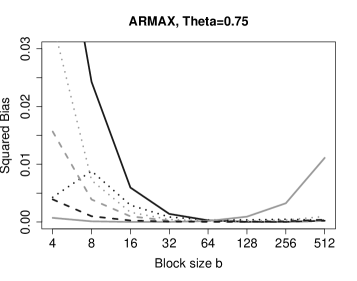

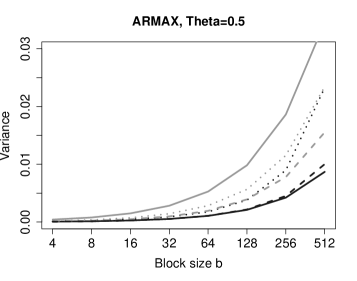

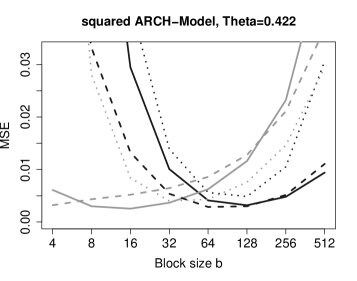

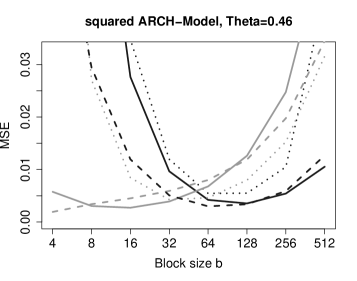

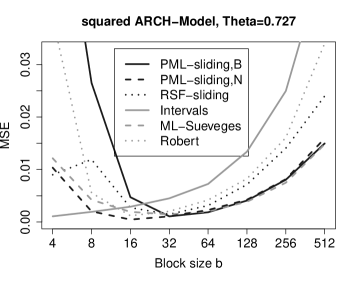

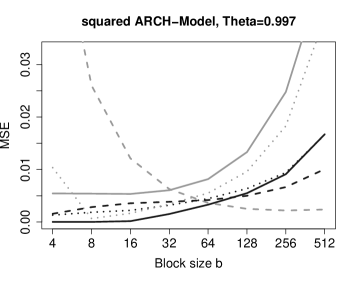

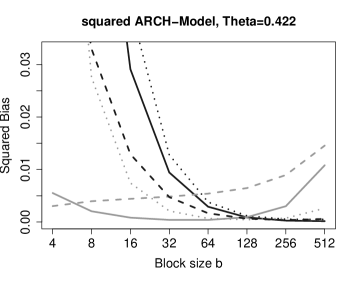

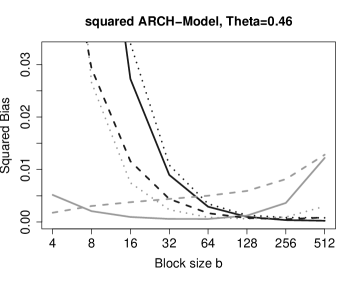

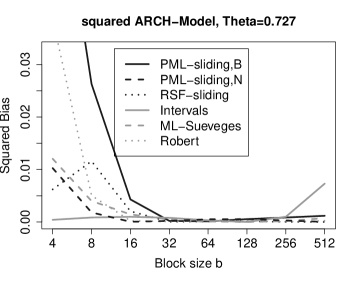

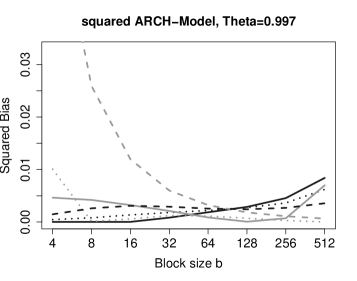

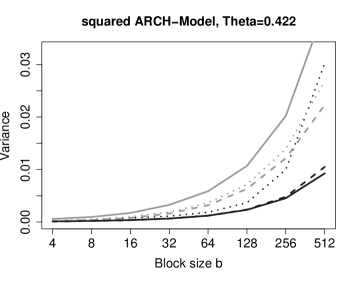

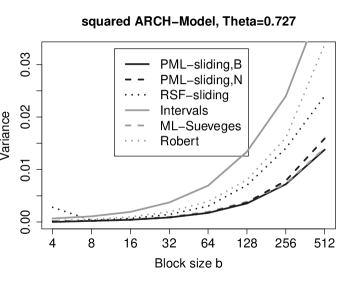

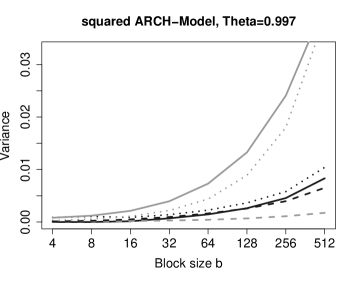

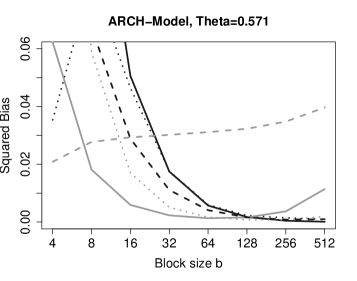

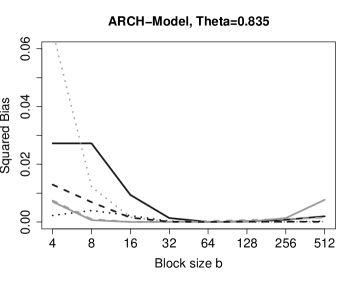

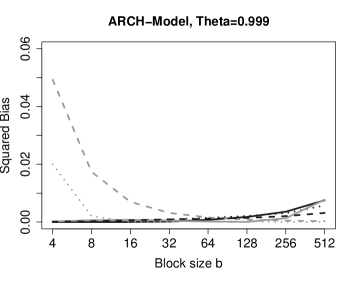

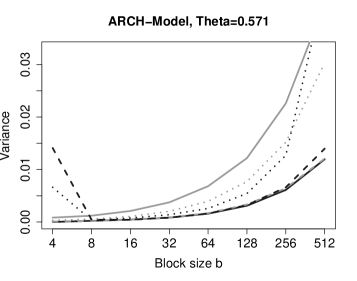

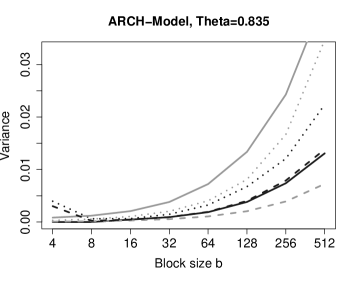

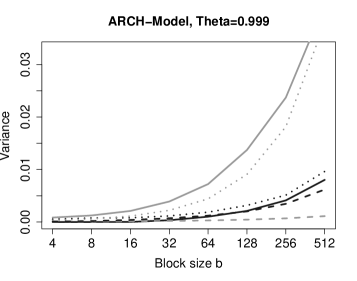

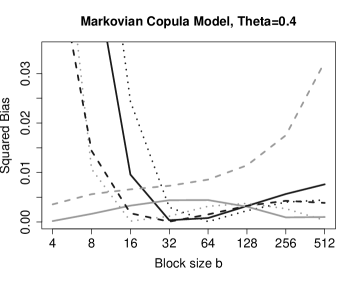

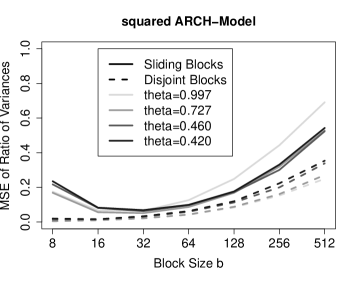

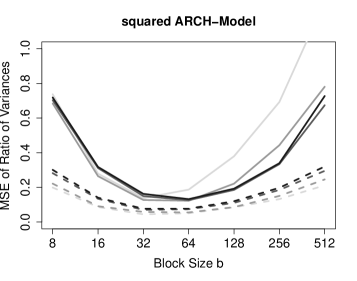

In Figure 3 (ARCH), as well as in Section E of the supplement material (ARMAX, squared ARCH and Markovian Copula), we depict the mean-squared error as a function of the block size parameter , estimated on the basis of simulation runs. For most models and estimators, the MSE-curves are U-shaped, representing the usual bias-variance tradeoff in extreme value theory (an exception being the Süveges-estimator within the ARCH-model for , a possible reason being its high bias due to fact that his central assumption is not satisfied in this model). Explicit pictures of the squared bias and variance can be found in Section E of the supplement. For the blocks estimators considered in this paper, the bias is decreasing in (the asymptotics for the exponential distribution kick in), while the variance is increasing (the convergence rate of the estimators being ). In terms of the bias, is clearly superior to for small block sizes.

The minimal values of the curves in Figure 3 are of particular interest, and are summarized in Table 1. We observe that the sliding blocks estimators and outperform the other two blocks estimators in most scenarios. For the ARMAX-model, this is in agreement with the theoretical findings presented in Figure 1. Comparing and , we see that seems to be preferable in most scenarios. In general, there is no clear best estimator in terms of the MSE: wins six times, the Süveges-estimator six times, four times, and the intervals estimator is best in one scenario.

| RSF-sliding | Intervals | ML-Süveges | Robert | |||

| 0.25 | 0.91 | 0.51 | 1.35 | 0.53 | 0.22 | 1.77 |

| 0.50 | 1.58 | 0.78 | 2.24 | 0.99 | 0.63 | 2.07 |

| 0.75 | 2.03 | 0.67 | 2.34 | 1.17 | 0.96 | 2.31 |

| 1.00 | 0.00 (1.78) | 0.05 (0.11) | 0.10 (0.12) | 0.88 | 0.11 | 2.22 |

| 0.422 | 3.18 | 2.86 | 4.85 | 2.53 | 3.19 | 4.00 |

| 0.460 | 3.53 | 2.98 | 5.45 | 2.71 | 1.92 | 4.26 |

| 0.727 | 1.07 | 0.46 | 1.46 | 1.08 | 1.44 | 1.19 |

| 0.997 | 0.01 (0.50) | 1.56 | 1.31 (1.33) | 5.34 | 2.19 | 0.65 |

| 0.571 | 4.82 | 4.81 | 7.65 | 6.02 | 20.94 | 5.58 |

| 0.721 | 3.32 | 2.63 | 4.22 | 3.70 | 0.28 | 3.65 |

| 0.835 | 1.89 | 1.02 | 1.74 | 1.83 | 0.31 | 2.09 |

| 0.999 | 0.00 (0.98) | 0.16 (0.17) | 0.73 (0.76) | 1.01 | 1.15 | 1.13 |

| 0.20 | 0.63 | 0.52 | 1.72 | 0.63 | 15.14 | 1.56 |

| 0.40 | 0.99 | 0.68 | 1.61 | 0.79 | 3.80 | 1.29 |

| 0.60 | 1.65 | 0.92 | 1.72 | 4.77 | 0.43 | 1.65 |

| 0.80 | 0.97 | 0.18 | 0.72 | 13.00 | 2.53 | 0.63 |

| 0.95 | 0.82 (0.94) | 4.60 | 2.87 | 12.05 (12.50) | 4.32 | 1.65 (2.06) |

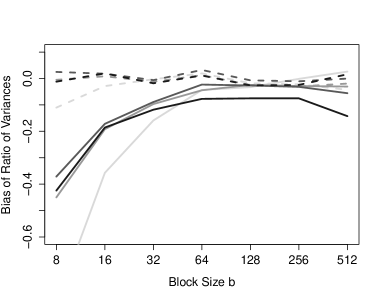

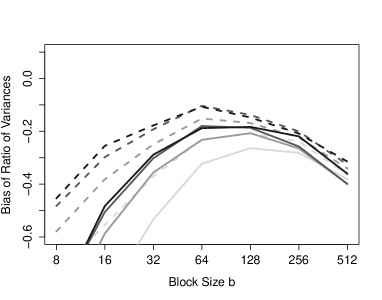

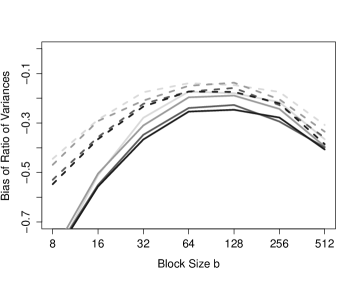

7.2. Estimation of the asymptotic variance and coverage of confidence bands

We consider the ARMAX-, squared ARCH-, and ARCH-model as described above. We are interested in the performance of

as estimators for the variances of and , respectively, where . Results can be found in Figure 3 (as well as in Figures 16 and 17 of the supplement), where we depict the curves

, estimated on the basis of 10,000 simulation runs. Here, is approximated by the empirical variance of over additional 10,000 simulations. Qualitatively, we observe a similar behaviour as for the estimation of depicted in Figure 3: the curves are U-shaped and possess a minimum at some intermediate values of . Due to the fact that estimator is based on an additional estimation step (which is potentially biased, if is small), the approximation works better for the disjoint blocks estimator. Also, the approximation is far better for than for (in particular for the bias), which may be explained by the fact that is based on an explicit expansion for . In particular, the fact that the bias of is eventually increasing for larger block sizes may be explained by the -approximation of by (Theorem 3.1).

We are also interested in the coverage probabilities of the confidence sets

for , where denotes the -quantile of the standard normal distribution. Empirical coverage probabilities for based on simulation runs are presented in Tables 2 (-versions) and 3 (-versions), with coverage probabilities above in boldface. Since the variance approximation is worse for , the coverage probabilities are worse as well. Moreover, it can be seen that the probabilities strongly depend on the block size , with, for , at least one reasonable choice for every model, usually close to the MSE-minimal choice in Figure 3 (and Figure 6 in the supplement). The larger width of the confidence sets for the disjoint blocks estimator (not presented here; it is due to the larger variance) results in a slightly better performance compared to the sliding blocks estimator.

| ARMAX-model | ARCH-model | ||||||||

|---|---|---|---|---|---|---|---|---|---|

| 0.25 | 0.5 | 0.75 | 1 | 0.571 | 0.721 | 0.835 | 0.999 | ||

| disjoint | 16 | 0 | 0 | 0.13 | 1.0 | 0.00 | 0.00 | 0.04 | 1.00 |

| 32 | 0.03 | 0.63 | 0.85 | 0.99 | 0.01 | 0.42 | 0.87 | 0.97 | |

| 64 | 0.80 | 0.93 | 0.95 | 0.98 | 0.68 | 0.91 | 0.94 | 0.93 | |

| 128 | 0.94 | 0.94 | 0.94 | 0.95 | 0.93 | 0.94 | 0.92 | 0.91 | |

| 256 | 0.93 | 0.92 | 0.91 | 0.92 | 0.93 | 0.92 | 0.90 | 0.89 | |

| 512 | 0.91 | 0.90 | 0.88 | 0.87 | 0.90 | 0.88 | 0.86 | 0.84 | |

| sliding | 16 | 0 | 0 | 0.02 | 1.00 | 0.00 | 0.00 | 0.00 | 1.00 |

| 32 | 0.01 | 0.46 | 0.75 | 1.00 | 0.00 | 0.20 | 0.76 | 0.95 | |

| 64 | 0.71 | 0.90 | 0.93 | 0.96 | 0.53 | 0.86 | 0.92 | 0.89 | |

| 128 | 0.92 | 0.93 | 0.92 | 0.92 | 0.89 | 0.92 | 0.88 | 0.85 | |

| 256 | 0.91 | 0.89 | 0.87 | 0.86 | 0.90 | 0.88 | 0.84 | 0.81 | |

| 512 | 0.88 | 0.85 | 0.81 | 0.76 | 0.85 | 0.81 | 0.77 | 0.73 | |

| ARMAX-model | ARCH-model | ||||||||

|---|---|---|---|---|---|---|---|---|---|

| 0.25 | 0.5 | 0.75 | 1 | 0.422 | 0.46 | 0.727 | 0.997 | ||

| disjoint | 16 | 0.00 | 0.47 | 0.84 | 0.95 | 0.00 | 0.01 | 0.62 | 0.82 |

| 32 | 0.50 | 0.87 | 0.92 | 0.96 | 0.07 | 0.64 | 0.91 | 0.88 | |

| 64 | 0.88 | 0.93 | 0.93 | 0.97 | 0.69 | 0.90 | 0.92 | 0.92 | |

| 128 | 0.91 | 0.92 | 0.92 | 0.96 | 0.89 | 0.92 | 0.92 | 0.94 | |

| 256 | 0.90 | 0.90 | 0.91 | 0.96 | 0.90 | 0.91 | 0.94 | 0.94 | |

| 512 | 0.87 | 0.87 | 0.91 | 0.94 | 0.86 | 0.89 | 0.92 | 0.93 | |

| sliding | 16 | 0.00 | 0.22 | 0.70 | 0.91 | 0.00 | 0.00 | 0.32 | 0.62 |

| 32 | 0.31 | 0.80 | 0.88 | 0.94 | 0.01 | 0.42 | 0.87 | 0.77 | |

| 64 | 0.82 | 0.89 | 0.90 | 0.94 | 0.54 | 0.84 | 0.88 | 0.85 | |

| 128 | 0.87 | 0.88 | 0.88 | 0.92 | 0.83 | 0.88 | 0.86 | 0.84 | |

| 256 | 0.85 | 0.84 | 0.81 | 0.86 | 0.83 | 0.83 | 0.80 | 0.76 | |

| 512 | 0.75 | 0.72 | 0.69 | 0.76 | 0.73 | 0.69 | 0.67 | 0.62 | |

8. Case study

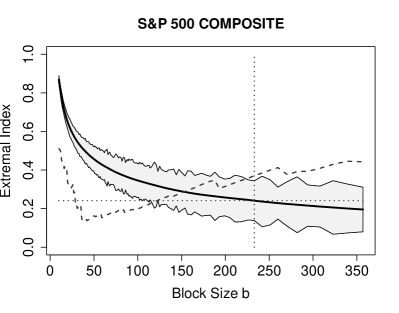

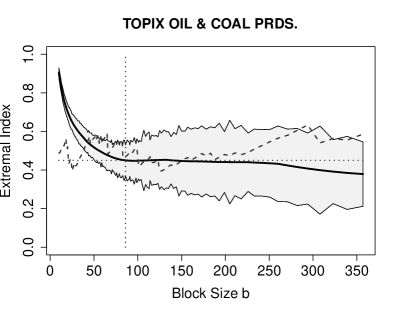

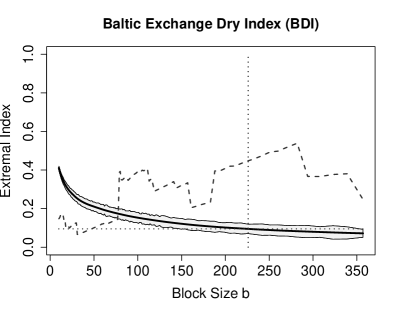

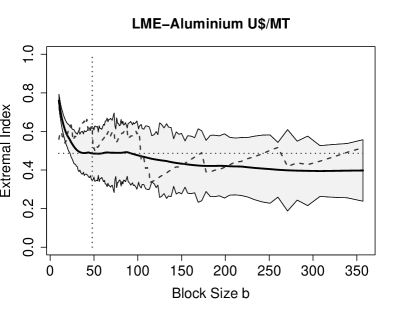

The use of the PML-estimators and the corresponding confidence sets is illustrated on negative daily log returns of a variety of financial market indices and prices including equity (e.g., S&P 500 Composite, MSCI World), commodities (e.g., TOPIX Oil & Coal, Gold Bullion LBM, Raw Sugar) and U.S. treasury bonds between 04 January 1990 and 30 December 2015 ( observations for each index). Clusters of large negative returns can be financially damaging and are hence of interest for risk management.

In Figure 4, we depict estimates of the extremal index for four typical time series as a function of the block length parameter, ranging from to . The solid curves correspond to the bias corrected sliding blocks estimator , alongside with a 95%-confidence band based on the variance estimator from Section 4 and the normal approximation. Interestingly, the curves appear to be quite smooth, which is a typical and nice property of the sliding blocks estimator. For comparison, the (far rougher) dashed lines correspond to the intervals estimator from Ferro and Segers (2003). As highlighted by many other authors, there is no simple optimal solution for the choice of the best block length parameter and a unique estimate for the extremal index. The dotted lines in Figure 4 correspond to case-by-case visual choices, trying to capture plateaus in the respective plots.

For the ease of comparison, this procedure has been repeated for all 20 time series under consideration (despite the fact that the entire curves provide a more detailed picture of the extremal dependence). In Table 4, we state the resulting estimates of the extremal index and the width of the corresponding confidence intervals. Interestingly, the estimates of the extremal index lie around 0.3 for most of the equity indexes (S&P 500 Composite, MSCI World, etc.), while they are around 0.45 for many of the commodity prices (Coffee, Cotton, Aluminium). The smallest value of 0.12 is attained for the Baltic Exchange Dry Index, an index measuring the price of moving the major raw materials by sea and usually regarded as an efficient economic indicator of future economic growth and production.

| Index / Prices | Extremal Index | Width of C-Interval |

|---|---|---|

| Raw Sugar Cents/lb | 0.54 | 0.17 |

| Coffee-Brazilian Cents/lb | 0.49 | 0.13 |

| LME-Aluminium U$/MT | 0.49 | 0.14 |

| Palladium U$/Troy Ounce | 0.46 | 0.11 |

| TOPIX OIL & COAL PRDS. | 0.45 | 0.08 |

| US T-Bill 10 YEAR | 0.44 | 0.12 |

| Cotton Cents/lb | 0.42 | 0.12 |

| S&P GSCI Precious Metal | 0.42 | 0.12 |

| MSCI WORLD EX US | 0.36 | 0.11 |

| Crude Oil-Brent Cur. Month | 0.35 | 0.10 |

| Gold Bullion LBM | 0.33 | 0.10 |

| RUSSELL 2000 | 0.31 | 0.09 |

| S&P GSCI Commodity Total Return | 0.30 | 0.09 |

| S&P 500 COMPOSITE | 0.29 | 0.10 |

| LMEX Index | 0.27 | 0.10 |

| G12-DS Banks | 0.26 | 0.09 |

| G7-DS Banks | 0.26 | 0.10 |

| EU-DS Banks | 0.26 | 0.08 |

| S&P500 BANKS | 0.22 | 0.08 |

| Baltic Exchange Dry Index (BDI) | 0.12 | 0.02 |

9. Auxiliary Lemmas for proving Theorem 3.2 (disjoint blocks)

Lemma 9.1 (Approximation by an integral with bounded support).

Under Condition 2.1, for all ,

Lemma 9.2 (Approximation by a Lebesgue integral).

Suppose that Condition 2.1 is met. Then, as ,

Lemma 9.3 (Joint convergence of fidis).

Under Condition 2.1, for any , as ,

the random vector on the right-hand side being -distributed with

Here, and, for with ,

where, for ,

with independent of iid random vectors .

Lemma 9.4.

Lemma 9.5.

10. Auxiliary Lemmas for proving Theorem 3.2 (sliding blocks)

Lemma 10.1 (Approximation by an integral with bounded support – sliding blocks).

Under Condition 2.1, for all ,

Lemma 10.2 (Approximation by a Lebesgue integral – sliding blocks).

Suppose Condition 2.1 is met. Then, as ,

Acknowledgments

The authors would like to thank two anonymous referees and an Associate Editor for their constructive comments on an earlier version of this manuscript. Moreover, they would like to thank Johan Segers (for providing the R-implementations of several estimators for the extremal index), Gregor Weiß (for providing the financial market data) and Daniel Ullmann and Peter Posch for fruitful discussions.

This research has been supported by the Collaborative Research Center “Statistical modeling of nonlinear dynamic processes” (SFB 823) of the German Research Foundation, which is gratefully acknowledged. Parts of this paper were written when A. Bücher was a visiting professor at TU Dortmund University.

References

- Beirlant et al. (2004) Beirlant, J., Y. Goegebeur, J. Segers, and J. Teugels (2004). Statistics of extremes: Theory and Applications. Wiley Series in Probability and Statistics. Chichester: John Wiley & Sons Ltd.

- Berbee (1979) Berbee, H. C. P. (1979). Random walks with stationary increments and renewal theory, Volume 112 of Mathematical Centre Tracts. Amsterdam: Mathematisch Centrum.

- Berghaus and Bücher (2017) Berghaus, B. and A. Bücher (2017, 004). Goodness-of-fit tests for multivariate copula-based time series models. Econometric Theory 33(2), 292–330.

- Billingsley (1979) Billingsley, P. (1979). Probability and measure. John Wiley & Sons, New York-Chichester-Brisbane. Wiley Series in Probability and Mathematical Statistics.

- Bingham et al. (1987) Bingham, N. H., C. M. Goldie, and J. L. Teugels (1987). Regular Variation. Cambridge: Cambridge University Press.

- Bradley (1983) Bradley, R. C. (1983). Approximation theorems for strongly mixing random variables. Michigan Math. J. 30(1), 69–81.

- Bradley (2005) Bradley, R. C. (2005). Basic properties of strong mixing conditions. A survey and some open questions. Probab. Surv. 2, 107–144. Update of, and a supplement to, the 1986 original.

- Bücher and Segers (2015) Bücher, A. and J. Segers (2015). Maximum likelihood estimation for the Fréchet distribution based on block maxima extracted from a time series. ArXiv e-prints.

- Darsow et al. (1992) Darsow, W. F., B. Nguyen, and E. T. Olsen (1992). Copulas and Markov processes. Illinois J. Math. 36(4), 600–642.

- de Haan et al. (1989) de Haan, L., S. I. Resnick, H. Rootzén, and C. G. de Vries (1989). Extremal behaviour of solutions to a stochastic difference equation with applications to ARCH processes. Stochastic Process. Appl. 32(2), 213–224.

- Dehling and Philipp (2002) Dehling, H. and W. Philipp (2002). Empirical process techniques for dependent data. In Empirical process techniques for dependent data, pp. 3–113. Boston, MA: Birkhäuser Boston.

- Drees (2000) Drees, H. (2000). Weighted approximations of tail processes for -mixing random variables. Ann. Appl. Probab. 10(4), 1274–1301.

- Drees (2002) Drees, H. (2002). Tail empirical processes under mixing conditions. In Empirical process techniques for dependent data, pp. 325–342. Birkhäuser Boston, Boston, MA.

- Drees and Rootzén (2010) Drees, H. and H. Rootzén (2010). Limit theorems for empirical processes of cluster functionals. Ann. Statist. 38(4), 2145–2186.

- Ferro and Segers (2003) Ferro, C. A. T. and J. Segers (2003). Inference for clusters of extreme values. J. R. Stat. Soc. Ser. B Stat. Methodol. 65(2), 545–556.

- Hsing (1984) Hsing, T. (1984). Point Processes Associated with Extreme Value Theory. ProQuest LLC, Ann Arbor, MI. Thesis (Ph.D.)–The University of North Carolina at Chapel Hill.

- Hsing (1993) Hsing, T. (1993). Extremal index estimation for a weakly dependent stationary sequence. Ann. Statist. 21(4), 2043–2071.

- Hsing et al. (1988) Hsing, T., J. Hüsler, and M. R. Leadbetter (1988). On the exceedance point process for a stationary sequence. Probab. Theory Related Fields 78(1), 97–112.

- Kesten (1973) Kesten, H. (1973). Random difference equations and renewal theory for products of random matrices. Acta Math. 131, 207–248.

- Kosorok (2008) Kosorok, M. R. (2008). Introduction to empirical processes and semiparametric inference. Springer Series in Statistics. New York: Springer.

- Leadbetter (1983) Leadbetter, M. R. (1983). Extremes and local dependence in stationary sequences. Z. Wahrsch. Verw. Gebiete 65(2), 291–306.

- Leadbetter et al. (1983) Leadbetter, M. R., G. Lindgren, and H. Rootzén (1983). Extremes and related properties of random sequences and processes. Springer Series in Statistics. Springer-Verlag, New York-Berlin.

- Leadbetter and Rootzén (1988) Leadbetter, M. R. and H. Rootzén (1988). Extremal theory for stochastic processes. Ann. Probab. 16(2), 431–478.

- Northrop (2015) Northrop, P. J. (2015). An efficient semiparametric maxima estimator of the extremal index. Extremes 18(4), 585–603.

- O’Brien (1987) O’Brien, G. L. (1987). Extreme values for stationary and Markov sequences. Ann. Probab. 15(1), 281–291.

- Perfekt (1994) Perfekt, R. (1994). Extremal behaviour of stationary Markov chains with applications. Ann. Appl. Probab. 4(2), 529–548.

- Rémillard et al. (2012) Rémillard, B., N. Papageorgiou, and F. Soustra (2012). Copula-based semiparametric models for multivariate time series. J. Multivariate Anal. 110, 30–42.

- Resnick (1987) Resnick, S. I. (1987). Extreme values, regular variation, and point processes, Volume 4 of Applied Probability. A Series of the Applied Probability Trust. Springer-Verlag, New York.

- Robert (2009) Robert, C. Y. (2009). Inference for the limiting cluster size distribution of extreme values. Ann. Statist. 37(1), 271–310.

- Robert et al. (2009) Robert, C. Y., J. Segers, and C. A. T. Ferro (2009). A sliding blocks estimator for the extremal index. Electron. J. Stat. 3, 993–1020.

- Rootzén (2009) Rootzén, H. (2009). Weak convergence of the tail empirical process for dependent sequences. Stochastic Process. Appl. 119(2), 468–490.

- Segers (2005) Segers, J. (2005). Approximate distributions of clusters of extremes. Statist. Probab. Lett. 74(4), 330–336.

- Smith and Weissman (1994) Smith, R. L. and I. Weissman (1994). Estimating the extremal index. J. Roy. Statist. Soc. Ser. B 56(3), 515–528.

- Süveges (2007) Süveges, M. (2007). Likelihood estimation of the extremal index. Extremes 10(1-2), 41–55.

- Süveges et al. (2010) Süveges, M., A. C. Davison, et al. (2010). Model misspecification in peaks over threshold analysis. The Annals of Applied Statistics 4(1), 203–221.

- van der Vaart (1998) van der Vaart, A. W. (1998). Asymptotic statistics, Volume 3 of Cambridge Series in Statistical and Probabilistic Mathematics. Cambridge: Cambridge University Press.

- Vervaat (1979) Vervaat, W. (1979). On a stochastic difference equation and a representation of nonnegative infinitely divisible random variables. Adv. in Appl. Probab. 11(4), 750–783.

- Weissman and Novak (1998) Weissman, I. and S. Y. Novak (1998). On blocks and runs estimators of the extremal index. J. Statist. Plann. Inference 66(2), 281–288.

SUPPLEMENTARY MATERIAL ON

“WEAK CONVERGENCE OF A PSEUDO MAXIMUM LIKELIHOOD

ESTIMATOR FOR THE EXTREMAL INDEX”

BETINA BERGHAUS AND AXEL BÜCHER

Throughout this supplement, and denote generic constants whose values may change from line to line. The notation always refers to , if not mentioned otherwise.

Appendix A Remaining steps for the proof of Theorem 3.2 – disjoint blocks

Proof of Lemma 9.1.

For some , let denote the event . By Condition 2.1(v), we have as . We may write

as , where, with for (and else),

and

Now, decompose according to whether the second sum over is such that or , respectively. It suffices to show that and as , and that

| (A.1) |

for all .

Second, we can write , where

whence it suffices to show that . For that purpose, define

| (A.2) |

Note that is measurable, whence the mixing coefficients become available. On the event , we have , where is defined exactly as , but with and replaced by and , respectively. By stationarity, we obtain

Recall Theorem 3 in Bradley (1983) (coupling for strongly mixing random variables): if and are two random variables in some Borel space and , respectively, if is uniform on and independent of and if and are such that , then there exists measurable function such that has the same distribution as , is independent of and satisfies

| (A.3) |

Apply this theorem with , , and to obtain that

where is independent of and has the same distribution as . Note that . Since , it follows that

which converges to by Conditions 2.1(iii) and (vi). To conclude, .

The sum can be treated analogously so that it remains to show (A.1). Decompose where

and where is defined analogously with the second sum ranging from to . We will only treat in the following, as can be treated analogously. Recall (A.2) and note that, on the event , we have . Therefore, again on the event ,

where, for , , and ,

We will show that (A.1) is met with replaced by , and for that purpose we consider the first central moment of .

Note that and that, for all with for some , we have

as can be shown by a case-by-case study and monotonicity arguments. The previous two inequalities, together with (A.3) with , , and , imply that is bounded above by

where is independent of and has the same distribution as . The second sum on the right-hand side is of the order (note that )

which converges to by Condition (2.1).

Since converges to for followed by , it remains to consider the sums over

We only treat the sum involving the plus-sign. After conditioning on we are left with bounding for (note that implies that for sufficiently large ). Decompose where and denote the sum over the even and the odd blocks, respectively. It suffices to treat both sums separately, and we give the details for the sum over the even blocks. Let

such that Note that . Repeatedly applying the coupling construction from (A.3) above (with , and, in the th step, and ), together with Theorem 5.1 in Bradley (2005), we can inductively construct an iid sequence such that has the same distribution as for any and such that

where . Note that, since , we have by Condition 2.1(iv). Now

Since is a centered iid sequence, we have the bound

By the Cauchy-Schwarz-inequality, we further have

As a consequence,

for any , where by Condition 2.1(iv). A similar bound for the sum over the odd blocks finally implies that

after conditioning on . Note that the limes superior for of the moment on the right-hand side can be made arbitrary small by increasing . To finalize the treatment of we are hence left with bounding the expression

Since , we obtain that , which converges to zero under the assumption that . ∎

Proof of Lemma 9.2.

Recall that . We have to show that

which follows from Lemma C.8 in Berghaus and Bücher (2017), provided we can show that

The last display in turn follows from pointwise convergence (in probability) of to by a standard Gilvenko-Cantelli-type argument. For the pointwise convergence, note that by (1.1). By similar arguments as in the proof of Proposition 3.1 in Robert et al. (2009) (but under slightly different assumptions) it can be shown that

This implies pointwise convergence in probability and hence the Lemma. ∎

Proof of Lemma 9.3.

Note that weak convergence of the first components of the vector follows from Theorem 4.1 in Robert (2009). Regarding joint convergence with the st component, we only consider the case and set ; the general case can be treated analogously.

Recall the definition of in Condition 2.1(iii). Decompose blocks , where

and let

As a consequence of Lemma 6.6 in Robert (2009), . Let us show the same for . Denote and . For , let and note that by Condition 2.1(v). It then suffices to show that . We can write , where

Now, implies that , where the latter variable is defined in terms of the instead of the . Hence, , where

is -measurable. As a consequence, by stationarity

| (A.4) |

Let us first show that as , which would follow, if we show that, for any , in (the inequality follows by studying the cases and ). Since we have, for any ,

| (A.5) | ||||

which can be made arbitrary small by increasing . Hence, . Since for any by Condition 2.1(vi), we can conclude that in .

It remains to treat the sum over the covariances on the right-hand side of (A). By Lemma 3.11 in Dehling and Philipp (2002) (which is a slightly more general version of Lemma 6.3 in Robert, 2009), for any ,

(note that is -measurable). Now, for , by monotonicity of . The sum over the covariances in (A) can thus be bounded by a multiple of

The series converges and the moment converges to by arguments as given above.

Now, since and , it suffices to show that converges weakly to the claimed normal distribution. This in turn follows from the Cramér-Wold device, provided we show that for any

The left-hand side can be written as , where and

Note that is -measurable. A standard argument based on characteristic functions (see, e.g., the proof of Lemma 6.7 in Robert, 2009) shows that the weak limit of is the same as if the were considered as iid. Now,

By Minkowski’s inequality, for any , by Condition 2.1(vi) and (ii). As a consequence, provided exists, Ljapunov’s condition is satisfied (Billingsley, 1979, Theorem 27.3) and converges to a normal distribution with variance equal to

The latter limit is equal to , whence it remains to be shown that

which in turn follows, observing the expressions for the limiting covariances in Theorem 4.1 in Robert (2009), from

Repeating arguments from above, we may replace the set by in the preceding display, whence it is in fact sufficient to show that

By an application of Theorem 2.20 in van der Vaart (1998), the second assertion follows directly from and Condition 2.1(vi). For the first convergence, abbreviate and note that

see Perfekt (1994); Robert (2009), that is, converges jointly. By uniform integrability, we may deduce that

The lemma finally follows from and . ∎

Proof of Lemma 9.4.

This follows from a slight extension of Theorem 4.1 in Robert (2009), with in his notation. Indeed, a careful look at his proof shows that one may set everywhere (whenever the last coordinate of his vector of processes is concerned). ∎

Proof of Lemma 9.5.

Proof of Lemma 9.6.

Since

| (A.6) | ||||

we only have to show, that . First of all, note that, for ,

where . Using this representation and substituting we obtain

which is exactly the first summand in .

Consider the second integral in . By the definition of in Lemma 9.3 we have

where is independent of iid random vectors . With the identity , which we will show later, the latter expectation can further be rewritten as

| (A.7) |

Hence, substituting ,

| (A.8) |

and therefore

which corresponds to the remaining summands in .

Appendix B Remaining steps for the proof of Theorem 3.2 – sliding blocks

Proof of Lemma 10.1.

The proof is similar to the proof of Lemma 9.1, whence we only give a sketch proof. For some let denote the event . Note that by Condition 2.1(v). Recalling the definition of from the beginning of the proof of Lemma 9.1, we may then write where

Now, decompose according to whether the second sum over is such that or , respectively. Similar as in the proof of Lemma 9.1, it can be shown that and that . ∎

Proof of Lemma 10.2.

Proof of Lemma 10.3.

For notational convenience, we will only show the joint weak convergence of for some fixed ; the general case can be shown analogously. Let , where and note that as . Due to the Cramér-Wold device it suffices to prove that, for any ,

We may write

where the is due to omitting summands from the last block. Choose some integer sequence such that and as , where is defined in Condition 2.1(ii). Moreover, set . For , define

i.e., we combine consecutive -blocks in one big block of size and each of the big blocks is separated by a small block of size , formed by merging two consecutive -blocks. With this notation we obtain

where, for ,

First, we will show that . As in the proof of Lemma 9.3 we have , where is defined exactly as , but with replaced by

with . By an inequality similar to (A) and the argumentation subsequent to that inequality, it suffices to show that for some and that The first assertion follows from

by Condition 2.1(ii) and (vi) and the definition of . For the second assertion, note that is -measurable, whence

By Condition 2.1(iii) the sum converges to 0, which implies the assertion.

It remains to be shown converges to a normal distribution with the claimed covariance. As in the proof of Lemma 9.3, we can write

For , the observations and are separated by at least one block of size and measurable with respect to the -sigma fields. Further, by Condition 2.1(iii), . A standard argument for the characteristic function then shows that the weak limit of is the same as if the sample was independent, which we will assume subsequently. By arguments as before, we can then pass back to an independent sample , and weak convergence follows from the classical central limit theorem for rowwise iid triangular arrays.

By Condition 2.1(ii) and (vi) and Minkowski’s inequality, we have that . Hence,

by the definition of , provided that exists (which we will show below). Therefore, Ljapunov’s condition is satisfied and converges weakly to a normal distribution with variance . Hence, it remains to be shown that

and this in turn follows from the proof of Theorem 4.1 in Robert (2009) (for the first summand in the latter display) and Lemma B.1, B.2 and B.3 below (note that, with , we can write and that all assumptions in Condition 2.1 are satisfied if and are replaced by and ). ∎

Lemma B.1.

Proof of Lemma B.1.

For the sake of a clear exposition, we will assume that both and are measurable with respect to the -sigma fields; the general case follows by multiplication with suitable indicator functions as in the previous proofs. Introduce the notation and . We can write

The second sum on the right hand-side is negligible, since both and by Condition 2.1(ii) and (vi). Regarding the first sum, by stationarity, we can write

Split the right-hand side according to whether is such that either , or or . Up to negligible terms, this allows to write the right-hand side of the previous display as , where , and

Both sums in converge to : first, and . Second, the variables defining and are at least -observations apart, while the variables defining and are at least -observations apart. As a consequence, by Lemma 3.11 in Dehling and Philipp (2002),

The term is also negligible: we have

The covariance on the right-hand side can be bounded by a multiple of . The remaining sum over the mixing-coefficients converges, such that . The covariance can be treated similarly.

It remains to be shown that

converges to . To this end, define functions by

With this notation, we obtain

By uniform integrability of we have , as . Furthermore, for any , and are uniformly bounded by , which again is uniformly bounded in by Condition 2.1(ii) and (vi), i.e., . Hence, by dominated convergence, the lemma follows if we show that, for any ,

| (B.1) |

We only do this for , as can be treated similarly. Fix and note that

Let us first show joint weak convergence of the two variables inside this expectation, and for that purpose consider

For , we can write where

Let us show that we can manipulate any sum inside this probability by adding or subtracting summands, where is some integer sequence with . Indeed, for any fixed and sufficiently large :

Now, by omitting the last summands of the first sum inside the probability defining , this sum becomes asymptotically independent of the remaining sums in the probability (at the cost of an additive -error). The same can be done for the last sum and we obtain

This expression converges to by Theorem 4.1 in Robert (2009). As a consequence,

In the case similar arguments imply that

Since both and are in , weak convergence implies convergence of moments, whence

Calculating the integral on the right-hand side explicitly yields (B.1). ∎

Proof of Lemma B.2.

As in proof of Lemma B.1 we will assume that the are measurable with respect to the -sigma fields. Similar as in the beginning of the proof of Lemma B.1, one can show that

where is defined as

Condition 2.1(vi) implies . The limit of the integral over can deduced from pointwise convergence and the dominated convergence theorem. To see this, note that , due to Condition 2.1(vi). Regarding the pointwise convergence, suppose we have shown that, for any , there exists some random vector with dirtybution function depending on , such that

| (B.2) |

In that case, converges to by Condition 2.1(vi). Let us show (B.2). Fix and write

Now, if is an integer sequence such that , then, for sufficiently large ,

which is why we can omit or add observations in the maximum without changing the limit of its distribution. Similar as in the proof of Lemma B.1 this gives

which, by (1.1), converges to

This implies (B.2), with being defined by its joint survival function . Now, it is easy to see that

Finally, putting everything together, we obtain

as asserted. ∎

Lemma B.3.

Proof of Lemma B.3.

By the definition of and in Lemma B.1 and Lemma 9.3 we obtain that

with independent random variables , , and . For this reason, we can write

By Wald’s identity, we have . Independence of and , further implies

where we used that , see (A.9). Finally, (A) implies that

Altogether, we obtain

Now, noting that , we can rewrite as follows

From (A.8) we finally obtain that . ∎

Appendix C Equivalence of estimators – Proof of Theorem 3.1

Proof of Theorem 3.1.

We will only give the proof for the disjoint blocks version of the theorem as the sliding blocks can be treated analogously. For notational reasons we will omit the upper index . Define

and note that

The fraction on the right-hand side is . Indeed, the elementary inequality for implies that , and converges to in probability by Theorem 3.2. Now, we further decompose

By Lemma C.2, we immediately obtain . Furthermore, from Lemma C.1 and (3.6), we have, for any ,

with and . Hence, is if we can show that, for any , we have and that , for any fixed . The first part can be done by similar arguments as in the proof of Lemma 9.1. To see this, note that for and that as by Condition 2.1(v). Furthermore, by Proposition 7.27 in Kosorok (2008). ∎

Proof.

We will only give the proof for the disjoint blocks version of the theorem as the sliding blocks can be treated analogously. For notational reasons we will omit the upper index . By a Taylor expansion and a similar calculation as in (3.6), we have

where, for some ,

and where . Let . By Condition 2.1(v), we have . Note that, by Condition 2.1(iii), the sequence is -mixing with polynomial mixing rate and with stationary cdf satisfying for . For this reason, its empirical process converges weakly in and hence we obtain that

is of the order . Thus, for sufficiently large ,

as . As a consequence,

as . ∎

Proof.

We will only give the proof for the disjoint blocks version of the theorem as the sliding blocks can be treated analogously. For notational reasons we will omit the upper index . By Condition 2.1(v) and since we are only concerned with convergence in probability, it suffices to work on the event , where . It then suffices to show convergence in , and for that purpose note that

By a Taylor expansion, we have

Hence, by Condition 2.1(vi), we immediately obtain

and the proof is finished. ∎

Appendix D Additional proofs

Proof of Proposition 4.1.

Let

where the last supremum is over all finite partitions and of . Decompose

where

and where

By the Cauchy-Schwarz inequality, it suffices to show that and that .

Let us first show that . Note that iff , almost surely. As a consequence, by a similar calculation as in (3.6), we can write

almost surely, where the -term is uniformly in . We may further write

where denotes the usual empirical process. By weak convergence of that process (a consequence of the assumption on beta-mixing) we can conclude that . Hence,

Repeating arguments from the proof of Theorem 3.2 (Wichura’s theorem), it can be seen that the dominating term on the right-hand side of this display is of the order which converges to by assumption.

It remains to be shown that . For that purpose, write , where

From the proof of Lemma 9.6 we know that , where is defined in (A.6). Therefore, it suffices to show that

The first convergence can be shown by considering expectations and variances: first, by Condition 2.1(vi) and weak convergence of . Second,

which is of the order by a standard inequality for covariances of strongly mixing time series and by finiteness of moments of of order larger than 4.

Consider . For integer , let

where . Using similar arguments as in the proof of Lemma 9.1 it can be shown that, for any , converges to 0 for . Therefore, by Wichura’s theorem (Billingsley, 1979, Theorem 25.5), it is sufficient to show that

holds for any . For that purpose, we will show that and that as .

Recall Berbee’s coupling Lemma (Berbee, 1979): if and are two random variables in some Borel spaces and , respectively, then there exists a random variable independent of and a measurable function such that has the same distribution as , is independent of and satisfies . Apply this lemma with and (with ) to construct a random variable ( denoting the cdf of ) independent of satisfying . Write

| (D.1) | ||||

By Hölder’s and Minkowski’s inequality, the second expectation on the right-hand side of this display can be bounded in absolute value by

This bound converges to , since and since the assumptions imply that and that .

As a consequence, rewriting the first summand on the right-hand side of (D.1), we obtain that

where . By Condition 2.1(ii) and (vi) is uniformly integrable. Hence, to obtain that we only have to show that with being exponentially distributed with parameter . This in turn follows from the extended continuous mapping theorem, since and for any sequence . To see the latter, note that, for and large enough, Minkowski’s inequality and Condition 2.1(ii) and (vi) imply that

Consider the variance of . By the Cauchy-Schwarz inequality, up to negligible terms, it can be written as

| (D.2) |

where denote the set of all such that any two of the indexes are at distance larger than 2. We have to show that all covariances in this sum converge to , uniformly in the indexes.

First, consider the case where either or . Recall Lemma 3.11 in Dehling and Philipp (2002): for real-valued random variables and real numbers such that , we have

| (D.3) |

Therefore, for some , the covariances inside the sum in (D.2) are bounded by

which can be seen to be by Minkowski’s inequality and the Cauchy-Schwarz inequality.

The other cases are slightly more difficult. Consider the case . Apply Berbee’s coupling Lemma with and . Then the mixed moment inside the covariance can be written as

where the remainder term has been handled by Hölder’s and Minkowski’s inequality just as in (D.1). A second application of Berbee’s coupling Lemma (with and ) allows to rewrite the dominating term in the last display as

where the latter equality follows from (D.3). Since

we finally obtain that

All other cases can be treated similarly by a successive application of Berbee’s coupling Lemma. Also, can be treated similarly. ∎

Proof of Lemma 5.1.

We begin with the disjoint blocks estimator and write . Recalling (3.6), we can write where

Note that , as , by Condition 2.1 (vi). Hence, it remains to be shown that , and vanish as .

Consider . Choose some integer and let be sufficiently large such that . Write , where

The absolute value of can be bounded by

which goes to as for any fixed by Condition 2.1 (vi) and similar reasons as in the proof of Lemma 9.3, see (A.5). For the treatment of fix such that . Then, for sufficiently large , we can use the coupling construction leading to (A.3) (with and ) to find a random variable that has the same distribution as , is in dependent of and satisfies

By a monotonicity argument, we have

Furthermore, since is independent of ,

Combining everything we obtain

As a consequence, since by Condition 2.1 (iii),

This bound in turn can be made arbitrarily small by first choosing sufficiently small and then choosing sufficiently large. Hence, . Along the same lines, we obtain that .

The term can also be treated by a coupling construction. Here, we choose for some . By similar arguments as before, we obtain that

by Condition 2.1 (iii) and by the choice of . The proof for the disjoint blocks estimator is finished.

Sliding Blocks. By the definition of and we can write

as , where

and are negligible by the same reasons as for the treatment of and above, respectively. Regarding , we can write

The first summand on the right-hand side vanishes by similar arguments as we used to show the negligibility of above. Furthermore, the second sum on the right-hand side converges to for , by Condition 2.1(vi). Hence, . Similarly, , which finishes the proof. ∎

Proof of Lemma 6.1..

A function is slowly varying with index , notationally , if for any . Recall the Potter bounds (Bingham et al., 1987, Theorem 1.5.6): if , then, for any , there exists some constant such that, for any and with :

Let . Since , the function is regularly varying with index . We obtain that by, e.g., Proposition 0.8 (v) in Resnick (1987),

For non-negative integers define

Then and is independent of . We obtain that

where

Consider . By independence of and , we get the bound

The last inequality follows from the Potter bounds applied to (): we may choose sufficiently small such that

Now consider . By Markov’s inequality and a change of variable, for any ,

By the Potter bounds applied to , with and , we have, for all sufficiently large and for all ,

With and we obtain, after decreasing if necessary,

As a consequence, .

The derived bounds on and directly yield the bound

The assertion follows from the fact that by condition (S). ∎

Appendix E Additional Simulation results

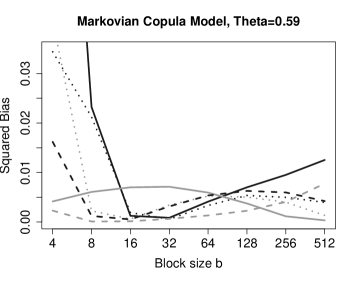

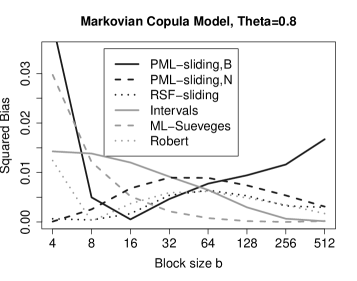

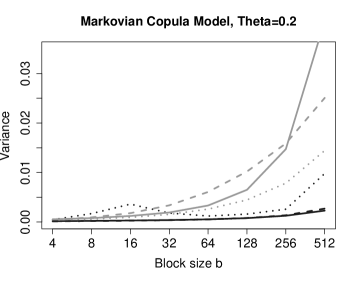

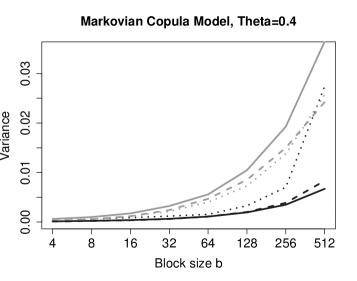

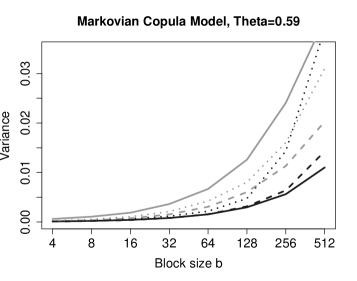

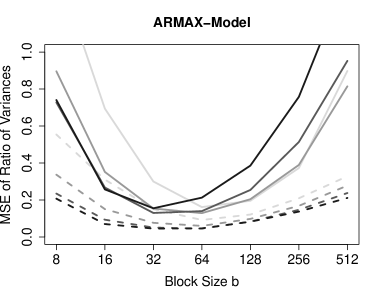

In this section, we present additional results of the simulation study (see also Section 7). Figures 6, 8 and 14 depict the mean squared error as a function of the block size parameter for the ARMAX, the squared ARCH and the Markovian Copula-model, respectively. The curves behave similar as for the ARCH-model (see Figure 3). Additionally, in Figures 6, 8, 10, 10, 12, 12, 14 and 16 we depict the corresponding squared biases and variances for all of the four considered models as a function of the block size . Finally, Figures 16 and 17 compare the performances of the estimator of the asymptotic variance for the estimators and in the ARMAX and the squared ARCH model. We observe the same behavior as in the simulations for the ARCH model (see Figure 3): the approximation for is better than for .

References

- Beirlant et al. (2004) Beirlant, J., Y. Goegebeur, J. Segers, and J. Teugels (2004). Statistics of extremes: Theory and Applications. Wiley Series in Probability and Statistics. Chichester: John Wiley & Sons Ltd.

- Berbee (1979) Berbee, H. C. P. (1979). Random walks with stationary increments and renewal theory, Volume 112 of Mathematical Centre Tracts. Amsterdam: Mathematisch Centrum.

- Berghaus and Bücher (2017) Berghaus, B. and A. Bücher (2017, 004). Goodness-of-fit tests for multivariate copula-based time series models. Econometric Theory 33(2), 292–330.

- Billingsley (1979) Billingsley, P. (1979). Probability and measure. John Wiley & Sons, New York-Chichester-Brisbane. Wiley Series in Probability and Mathematical Statistics.

- Bingham et al. (1987) Bingham, N. H., C. M. Goldie, and J. L. Teugels (1987). Regular Variation. Cambridge: Cambridge University Press.

- Bradley (1983) Bradley, R. C. (1983). Approximation theorems for strongly mixing random variables. Michigan Math. J. 30(1), 69–81.

- Bradley (2005) Bradley, R. C. (2005). Basic properties of strong mixing conditions. A survey and some open questions. Probab. Surv. 2, 107–144. Update of, and a supplement to, the 1986 original.

- Bücher and Segers (2015) Bücher, A. and J. Segers (2015). Maximum likelihood estimation for the Fréchet distribution based on block maxima extracted from a time series. ArXiv e-prints.

- Darsow et al. (1992) Darsow, W. F., B. Nguyen, and E. T. Olsen (1992). Copulas and Markov processes. Illinois J. Math. 36(4), 600–642.

- de Haan et al. (1989) de Haan, L., S. I. Resnick, H. Rootzén, and C. G. de Vries (1989). Extremal behaviour of solutions to a stochastic difference equation with applications to ARCH processes. Stochastic Process. Appl. 32(2), 213–224.

- Dehling and Philipp (2002) Dehling, H. and W. Philipp (2002). Empirical process techniques for dependent data. In Empirical process techniques for dependent data, pp. 3–113. Boston, MA: Birkhäuser Boston.

- Drees (2000) Drees, H. (2000). Weighted approximations of tail processes for -mixing random variables. Ann. Appl. Probab. 10(4), 1274–1301.

- Drees (2002) Drees, H. (2002). Tail empirical processes under mixing conditions. In Empirical process techniques for dependent data, pp. 325–342. Birkhäuser Boston, Boston, MA.

- Drees and Rootzén (2010) Drees, H. and H. Rootzén (2010). Limit theorems for empirical processes of cluster functionals. Ann. Statist. 38(4), 2145–2186.

- Ferro and Segers (2003) Ferro, C. A. T. and J. Segers (2003). Inference for clusters of extreme values. J. R. Stat. Soc. Ser. B Stat. Methodol. 65(2), 545–556.

- Hsing (1984) Hsing, T. (1984). Point Processes Associated with Extreme Value Theory. ProQuest LLC, Ann Arbor, MI. Thesis (Ph.D.)–The University of North Carolina at Chapel Hill.

- Hsing (1993) Hsing, T. (1993). Extremal index estimation for a weakly dependent stationary sequence. Ann. Statist. 21(4), 2043–2071.