Modelling the impact of financialization on agricultural commodity markets

Abstract

We propose a stylized model of production and exchange in which long-term investors set their production decision over a horizon , the “time to produce”, and are liquidity constrained, while financial investors trade over a much shorter horizon () and are therefore more duly informed on the exogenous shocks affecting the production output. The equilibrium solution proves that: (i) long-term producers modify their production decisions to anticipate the impact of short-term investors allocations on prices; (ii) short-term investments return a positive expected profit commensurate to the informational advantage. While the presence of financial investors improves the efficiency of risk allocation in the short-term and reduces price volatility, the model shows that the aggregate effect of commodity market financialization results in rising the volatility of both farms’ default risk and production output.

1 Introduction

The integration of agricultural commodity and financial markets has been largely criticized by both a growing body of economic literature (see e.g. [1]) and political consideration [2]. According to those critics the overflow of capital invested in the commodity markets feeds a destabilizing speculation, and a tightening of market regulation is then claimed. While the empirical evidence of international food price spikes and volatility driven by financial markets is robust (see [3] and references therein), its mechanisms and potential drawbacks for production risk management are unexplored.

This paper analyzes the effects of market integration on conventional production planning and farm liquidity risk management policies within a stylized equilibrium model of production, trade and consumption of an agricultural commodity where financial and agricultural commodity markets are partially integrated. We suggest that the “time to produce” is the fundamental parameter governing risk allocation and production dynamics and should be considered in designing more efficient production schemes and distribution policies aimed at improving liquidity risk-sharing.

The stylized model assumes that the production of an agricultural commodity is risky because farmers’ resources allocation and production decisions are irreversible and taken over a horizon , the “time to produce”. On the other hand financial investors trade over a much shorter horizon () and possess an information advantage contingent on the exogenous shocks affecting production of the commodity. In our model, investments on contingent contracts play a role similar to investments on physical storage and the zero net supply condition is assumed to hold on average.

Actually, as discussed by [4], any hedging policy, by requiring margin capital and liquidity, will in general have adverse effects on liquidity needs. In particular the inefficiency of long-term industry’s risk management are documented and discussed in [5], in [6], [7] and in [8].

Motivated by the above remarks, in the model at hand it is assumed that long-term investors face a liquidity constraint: at the end of the production cycle the farm goes bankrupt and its production is lost if the profit resulting from selling the production at market price is not sufficient to break even. Consequently, while price levels continue to depend on the joint allocation decisions of financial investors and producers, profits from financial hedging cannot be used to soften the liquidity constraint faced by long-term investors. In practice this constraint reproduces a segmentation of the capital market which is empirically well documented: most of the profits in commodity market trading remunerate professional investors while farm hedging investments are low.

In the model the commodity equilibrium price is thus set by the clearing of the market in an economy populated by an heterogeneous set of producers exposed to idiosyncratic and systematic shock components, by consumers described by an exogenously specified demand curve and by an extra demand or supply contribution generated by financial agents.

A comparative statics exercise proves that this model can reproduce many interesting stylized facts. First of all it is possible to prove that the long-term investors modify the production choice due to the effects of financial trading. In addition the financial investors make profit by exploiting their informational advantage. Finally, the model shows a progressive increase in the volatility of the produced quantity and a growth in default risk with an increasing market integration.

Our model highlights that the major issue in farm risk management is the necessity to alleviate the effects of credit constraints to reduce price pressure on producers and consumers. Correspondingly, public subsidization of agricultural investments can be interpreted as a necessary (possibly inefficient) response to restore the balance of capital flows from short-term to long-term investors. A rationalization for the farm policy actions similar to our has been discussed also in [9]. Our approach, however, is more focused on the description of farmers’ production planning decisions and our findings indicate that a rational production planning and liquidity risk management must classify different productions and financing opportunities considering the “time to produce” constraint faced by different participants.

The paper is organized as follows: in Section 2 we define the model and discuss its innovations with respect to the past literature. In Section 3 we present and discuss numerical results and their dependence on exogenous parameters. Section 4 is devoted to a discussion about the assumptions made within the model, while Section 5 to conclusions. A simplified (analytical solvable) version of the model is provided in the Appendix, together with some techinical aspects of the self consistent calculation procedure adopted.

2 Materials and Methods

2.1 Related literature

The model at hand is based on many simplifying assumptions in common with other rational expectations competitive storage models, [10], [11], [12, 13] and [14].

The intrinsic information asymmetry introduced in the model (discussed in Section 2.2) can be seen as a reduced form of the long-standing hedging pressure theory of commodity prices that dates back to [15], [16] and, more recently, to [17].

Market efficiency and its implications on commodity futures prices dynamics dates back to the seminal contribution of [18]. In presence of perfect (infinitely liquid and frictionless) capital markets, farmers could borrow sufficient capital to invest in the production and simultaneously take a position in the contingent contract markets to hedge the production risk.

The relation between liquidity constraints and productivity in farming and agricultural industries is grounded on a vast literature, see e.g. [19] and references therein. The influence of biological production lags on agricultural commodity price dynamics has been investigated in literature by means of the well known cobweb model, for example in the case of U.S. beef markets (see [20]). A thorough analysis of the relation between credit and liquidity constraints, farm investment policies and optimal subsidization policies could be found in [21].

In the equilibrium analysis described in [22] it is shown that the presence of producers’ liquidity constraints induces mean reversion in futures prices, while government price subsidies, if actively hedged by producers, lowers futures risk premia and reduces price volatility. Differently from that approach, here we explicitly model a multiplicity of producers which can default due to price dynamics. In this way we can analyze the equilibrium relations between liquidity restrictions, producers’ default and commodity prices. In this respect, our model bears some similarities with the model discussed in [23] where limits to arbitrage generate limits to hedging by producers.

2.2 The model

Production, trade and consumption of a real good are explicitly modeled. The price is set by the equilibrium between the supply and demand when the market clears. In particular, the equilibrium price is determined by the agents’ interaction, their operational timeline and market clearing conditions.

Hereafter agents are idealized to the extent that farmers can only produce real goods and financial investors can only trade goods whose payoff is contingent to the production outcome of the real one. The two types of agents are considered separated from one another in order to study the corresponding sector’s returns. However, a real agent could behave as a combination of the two idealized ones. As will be commented below considering a real agent (for example a farmer that can both produce and trade) does not alter the results of the model.

2.2.1 Agents

Supply and demand are regulated by the interaction of three types of agents: farmers, consumers and financial investors.

-

1.

Farmers are the producers of the commodity goods in the economy. We consider an ensemble of farmers, all producing the same food commodity, which only are allowed to sell the produced goods. A single farmer produces a quantity of this commodity investing an amount of capital . We consider that each farmer incurs in a fixed cost which do not depend on the quantity produced. For the sake of simplicity we assume to be the same for all the farmers.

The operational decision of the quantity to be produced is taken by the farmer at time . The quantity will be available on the market at a later time , corresponding to the “time to produce”, and sold at a price . Thus, the profit of a farmer will be:

(1) Producers are assumed to be risk neutral and, for the sake of simplicity, a zero rate discounting is applied. Extensions of the model to both fixed cost farmers’ dependency and to finite rate discounting are straightforward and will be discussed elsewhere. Within our framework the effect of individual risk aversion would be mitigated by the existence of a multitude of heterogeneous producers.

If the actual profit reaped by the farmer is negative the farmer defaults and the amount produced is distributed among lenders and does not contribute to the total quantity of goods brought to the market at time . Notice that in our model the liquidity constraint, that, as we will see is crucial in determining the production output volatility, is introduced by modeling the farmers’ default. The quantity is determined by the investment level , via a production function , that is generically assumed to be concave and with a positive derivative. We choose a simple form of :

(2) where is the “fitness” which induces uncertainty in the final amount specific to each farmer. models the exogenous stochastic uncertainty shocks and its realization at time is not predictable by farmers at the time of the production operational decision. However, its probability distribution (described in Section 2.2.2) is assumed to be known.

The time interval represents the lag between the farmers’ operational investment and the market clearing epoch (in short, the “time to produce”).

All the farmers enter the market at time in exactly the same conditions . Each farmer sets an investment level at time , maximizing the expected profit :

(3) where is the expected value of the price and the market fitness at the time conditional to the available information at time 0:

(4) The effective selling price is set by market equilibrium, while the variation of market fitness is determined by stochastic fitness. The investment level will be set consistently with market clearing by maximizing the expected profit given in Eq. (3) with respect to :

(5) Those quantities will determine the farmer’s effective profit.

-

2.

Consumers. We model the aggregate demand for food as given by:

(6) where is the demand elasticity. The demand curve indicates the quantity of the commodity which all consumers taken together would be willing to buy at each level of price. In the model, the value of is a constant parameter.

-

3.

Financial Investors are defined as agents that neither produce nor consume goods, entering the market at time very close to the market clearing (). They are informed of the fitness () and are allowed to trade on future contracts written on the produced good itself and contingent to the realization of . While several investment strategies are in principle possible, we assume that the investor trade contingent goods in a quantity that depends linearly on the differential of the newly available information :

(7) where measures the degree of integration between the financial and the commodity market. Importantly, we will show that its value can be determined self consistently if one assumes that the investment level is chosen in such a way that the average investment return is maximum.

In case of frictionless infinitely liquid capital markets and synchronous decisions, can be vanishing either because tends to zero (no market integration) or tends to zero (synchronous agents’ decisions, implying no information asymmetry). We will show that, when information asymmetry and market integration are present, the net demand of financial investors is zero on average. Consistently with this condition, we consider the expected capital gain of the financial investor as:

(8)

where is the average financial transaction cost, is set by the market equilibrium and . Consistently with the case of the farmer, in Eq. (8) we do not consider the cost of capital. However, since capital investments are more expensive for farmers than for financial investors. For this reason, considering the cost of capital in agents’ profits will eventually increase the profit of financial investors, with respect to that of producers.

2.2.2 The probabilistic description of fitness uncertainty

Even if all the farmers enter the market with the same fitness , their fitness will be different at time due to unpredictable changes in the global production condition of the commodity, affecting independently each individual farmer. Denoting by the fitness at time of farmer , we write it as the sum of normal distributed aggregate and idiosyncratic innovations:

| (9) |

where and , are statistically independent Wiener processes, with denoting the number of farmers. and are positive parameters that determine the typical size of the variation in the average fitness and the difference between this average and the fitness of a single farmer.

Hereafter, we will assume that the number of farmers is very large, and denote by the average value between all the farmers of a function of :

| (10) |

where and is a normal distribution of average and variance

We will also denote by the average value of a function of over the realizations of :

| (11) |

2.2.3 The time line

-

1.

At time , the farmers decide the amount of capital to invest in the production. In order to take this decision, they can access all the information on the past time course of and of the price. Based on this information, they know exactly the probability distribution of the fitness at time . Moreover, they know the equations regulating the commodity market they participate in and anticipate their investment decision conditional on the realization of the fitness.

-

2.

At time , , the approximate value of the aggregate fitness is observed by financial investors who set their strategy according to Eq. (7).

-

3.

At time the market for the food commodity clears and the equilibrium price is determined, production of non defaulted farmers is allocated to consumers and profits are distributed to farmers. For , due to commodity and financial market integration, financial investors with long (short) positions maturing at also contribute to an extra demand (supply).

Farmers’ production decision. The quantity brought to the market at time is conditional on the production decision taken at time and on the realization of the fitness (aggregate plus idiosyncratic). From Eq. (5) and (2), we have

| (12) |

where the primed sum runs over the farmers who are able to make a positive profit (namely, that do not default). Assuming the number of farmers is very large, we have:

| (13) |

where is the characteristic function of the interval and is defined as the minimum value of corresponding to a non negative profit for the farmers, i.e. . The value of entering in is estimated by Eq. (4) as:

| (14) |

where is a function of determined by the marked clearing (see below) and we have assumed, under rational expectation, that .

The farmers’ total return is computed in a static form as a statistical average over the farmers and over different realizations of the fitness. The average farmers’ total return, also determined by market clearing prices, is evaluated considering the average profit per unit of invested capital :

| (15) |

where has been estimated using Eq. (5). The expected farmers’ profit is estimated as:

| (16) |

where, putting together Eqs. (1), (2) and (5), if and otherwise.

Similarly, the expected fraction of defaulting farmers at time is given by:

| (17) |

Financial investors’ allocation decision. In this model the quantity of contingent goods, given in Eq. (7), is decided by the financial investor at time , under the condition of zero average net supply. This condition is automatically verified, since . In fact on a single trade the investor can reduce or increase the amount of production available for consumption, but this deviation has zero expectation under the farmer information set. Following the same reasoning used to compute the farmer total return, we interpret this static condition as a weak form of the dynamic constraint that financial investors are zero net suppliers of the traded commodity. Notice that by construction the position held by the financial investor in the long run will play a role similar to virtual storage with zero contents in average, with the possibility of both negative and positive inventory fluctuations.

The financial investor may produce a capital gain , given in the last term of Eq. (8), by extracting the informational rent generated by the possibility to select an optimal strategy based on the observation of the realized level of fitness. Since the feasible strategies are market neutral, i.e. on average the capital invested in the long and short position adds up to zero, the investment return per unit of dollar long is quantified by:

| (18) |

where is determined by the average capital gain accumulated by the investor over different outcomes of the fitness :

| (19) |

and, abstracting from margin requirements to short sell the commodity,

is the expected amount of capital required for the investment

in the long positions:

| (20) |

where is given by Eq. (7) and is the average trading transaction cost.

2.2.4 Commodity Market clearing

The selling price and the allocation of resources among agents are determined by the clearing of the market, namely by the total supply equaling the total demand, conditioned to the realization of the fitness uncertainty . For , in case of an adverse (favorable) realization, (), the production supply (consumer demand) is augmented by the extra supply (demand) generated by the financial agents investing on contingent goods maturing at .

| (21) |

where is the quantity of goods produced at time by farmers that have not defaulted and is given by Eq. (13), and is the extra financial investors’ demand or supply defined in Eq. (7). This equation must be solved iteratively together with Eq. (14), since in this equation the selling price as a function of enters explicitly. The existence of a unique solution for the equilibrium price and the procedure for solving numerically Eq. (21) together with (13) is discussed in the Appendix.

3 Calculation

The equilibrium of the model is characterized by solving the market clearing in Eq. (21). In this manner the consumer prices , the equilibrium production (given in Eq. (13)) and the returns on investments and (defined in Eqs. (18,15)), as well as other derivative quantities, can be determined for different values of market integration .

The model’s solution depends on the determination of the farmers’ expectation (given in Eq. (14)), which is calculated using the price schedule as obtained by solving Eq. (21). The system of Eq. (14) and Eq. (21) cannot be solved analitically due to the presence of the liquidity constraint present in the lower extreme of the definite integral appearing in Eq. (17). The system is then solved through the numerical self-consistent iterative procedure is described in the Appendix. Numerical results will of course depend on the choice of the scenario parameters, in particular , fixing the market elasticity, and determining fitness volatility. Thus, a comparative statics of an analytic approximation of the model for the case of a single farmer has been used to facilitate the setting of the parameters’ values used in the complete model simulation. The analytic approximation of the model is also given in the Appendix.

The equilibrium solution discussed below has been found for the parameter set listed in Table 1. In the following we also discuss the robustness of the results for different choices of the scenario parameters.

4 Results and economic implications

4.1 Equilibrium prices

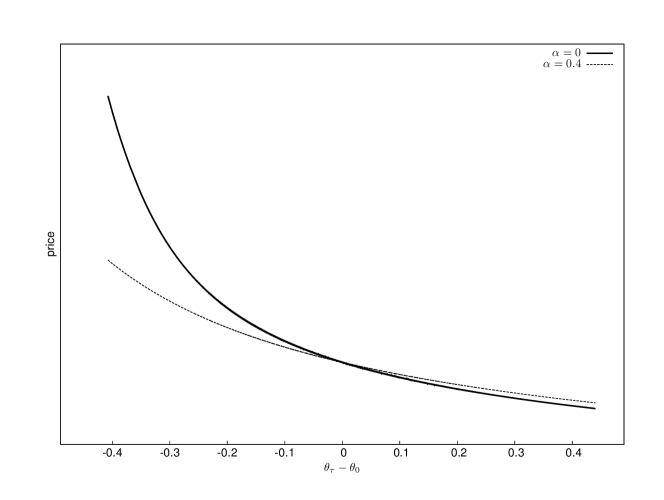

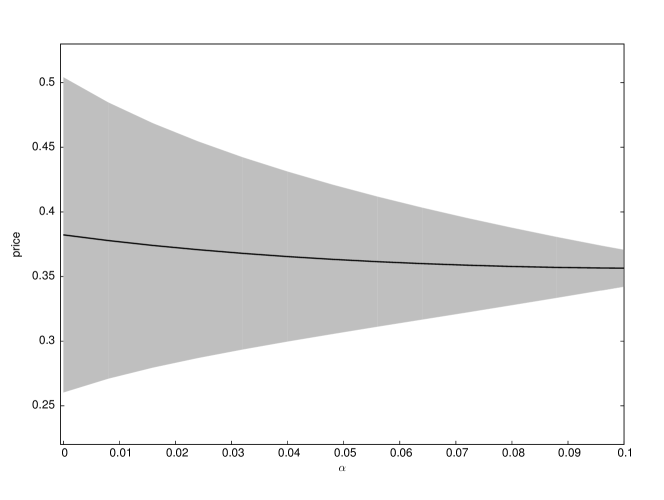

Figure 1 shows the price function solving Eq. (21), for the choice of the scenario parameters given in Table 1, as a function of the difference , for (representing the scenario with no markets integration) and for a finite value of . As expected financial trading has the effect of stabilizing the equilibrium price by smoothing the price dependence on exogenous shocks. Consistently with traditional perfect market models, the commodity price volatility is also reduced as an effect of trading (see Figure 2). According to the model an increased trading efficiency will reduce price volatility in any analyzed scenario parameter. We argue that this is probably related to our choice of using statistically independent Wiener processes to characterize the evolution of the farmers’ fitness appearing in Eq. (9).

4.2 Return on financial and farm investments

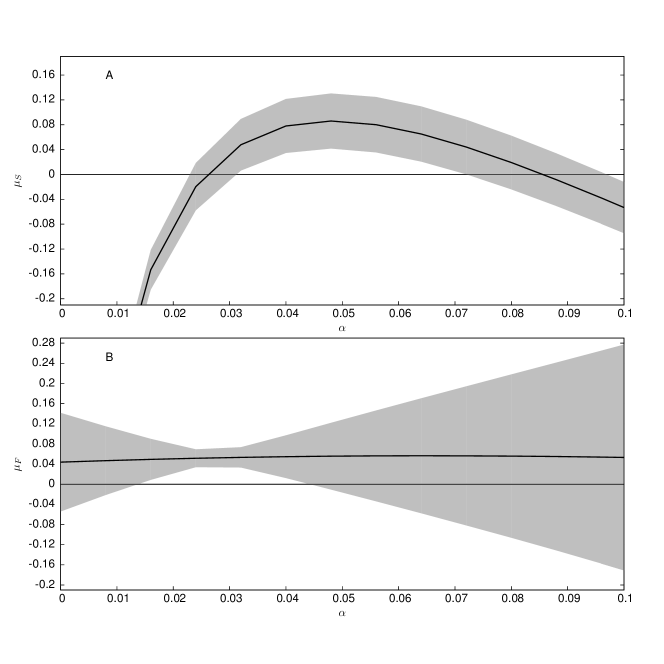

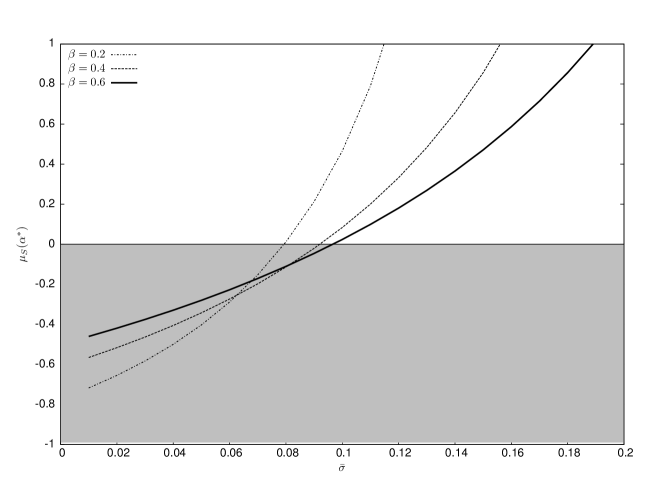

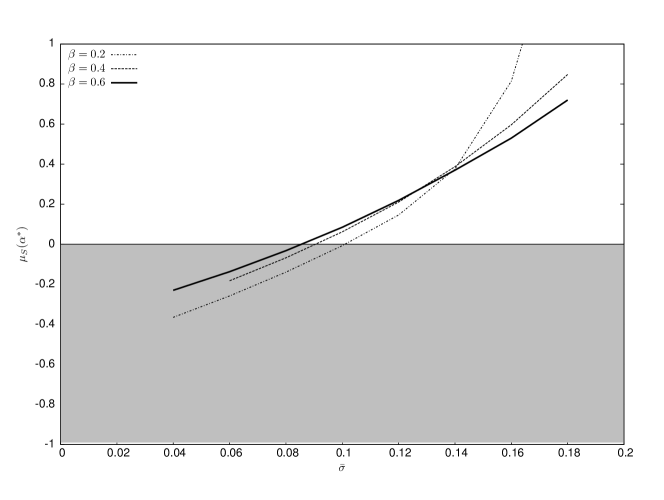

Expected speculator’s and farmer’s returns and are shown in Figure 3 as a function of the market integration parameter . For values of market integration smaller than a critical value , the financial investor’s expected return is negative, mainly due to the finite transaction cost considered in the model. We can interpret this result by observing that for market integration does not lead to an advantage for financial investors: i.e. for the financial transaction costs does not allow financial investors to extract their information rent. However, for larger values of financial integration the financial investors can exploit their superior information (see Figure 3, top panel). We also observe that the variance of the financial investor return is almost constant in , consistently with the neutral hypothesis for financial investors’ strategies. Notice that in the model it exists an which maximizes the expected returns for the financial investors . The financial investor’s return depends on the choice of scenario parameters, whose explicit dependence has been found in the simplified analytic model of a single farmer (described in the Appendix). Within the simplified model its dependence on the volatility of fitness and the market elasticity is shown in Figure 4 (top). It can be observed that financial investors’ expected return is higher for highly risky (high value of ) and inelastic markets (low value of ). The numerical solution for is also shown in Figure 4 (bottom). We observe that numerical and analytic solutions are qualitatively in agreement in reconstructing this observable.

Farmer’s investment return is fairly constant and positive showing a slight maximum in correspondence to (see bottom panel in Figure 3). In the long run farmer investment is productive, thus in the absence of liquidity constraints production is a profitable investment and, using land as a collateral would guarantee credit availability.

The variance of the farmers’ return is low in the region where is not far from , while for larger values of it grows sharply. The variance is a good indicator of the level of risk faced by a farmer in producing the real commodity, and the model is able to reproduce the counterintuitive evidence that the financialization amplifies the variability of returns on commodity production.

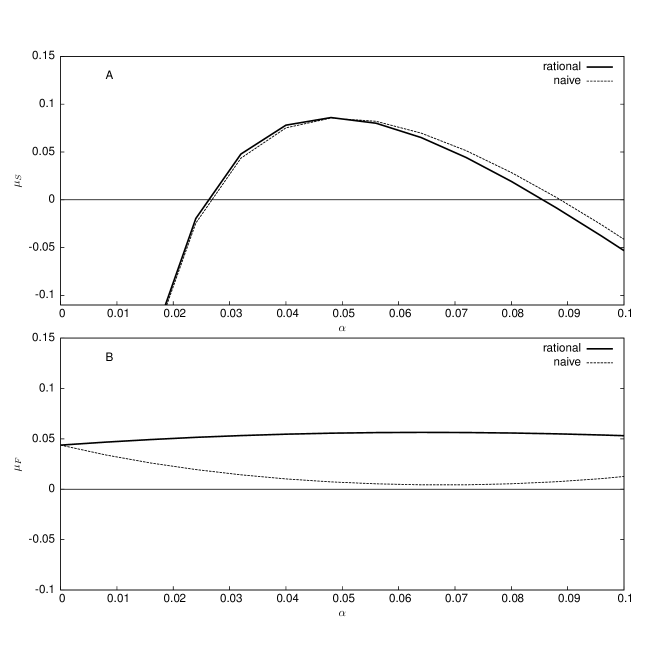

Figure 5 quantifies the impact of the farmer’s rational production planning on investment returns and by comparing the outcome of a rational farmer which sets the level of production taking into account the effect of market integration level , with the outcome of a naive farmer’s decision setting production level while ignoring the effect of market integration () on the expectation value of (see Eq. (14)). The financial investor’s return does not change significantly, while the farmer’s return , not surprisingly, shows a sharp reduction of return as an effect of a suboptimal production planning: naive farmers pay the maximum rent to financial investors which are better informed.

Within our model financialization of trade is driven by the asymmetric impact of market integration. On the one hand the financial investor increases the investment opportunity and raises the expected return on investment, while on the other the liquidity constraint which limits the aggregate investment capacity of the farmer implies that their return volatility grows sharply with . In other terms the improved efficiency of production risk sharing exacerbates the effect of the liquidity constraints which worsen the financing conditions of real investment and raise the default rates. This is best understood by analyzing equilibrium production.

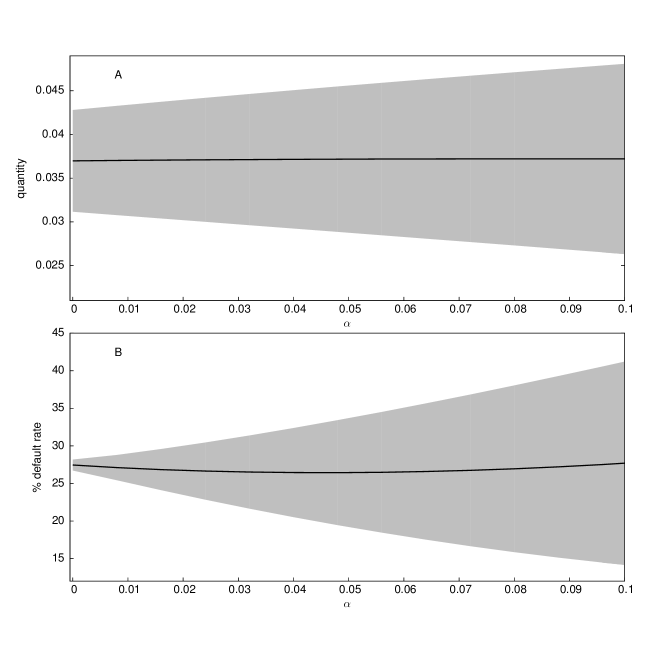

4.3 Equilibrium production risk and the effect of market integration on production planning

As the degree of market integration increases, the production quantity (shown in Figure 6) remains fairly constant, while its volatility increases with . The default rate in this market is approximately and almost constant with market integration, while the default rate variance increases with as a combined effect of the increase in the return volatility and the fitness fluctuation, . Note that the longer the time to produce the larger the fluctuations in returns from real investment, thus an efficient subsidization approach should consider a redistribution of wealth which accounts for the differential levels of liquidity stress suffered by producers, intermediaries and last minute-traders with differential “time to produce”.

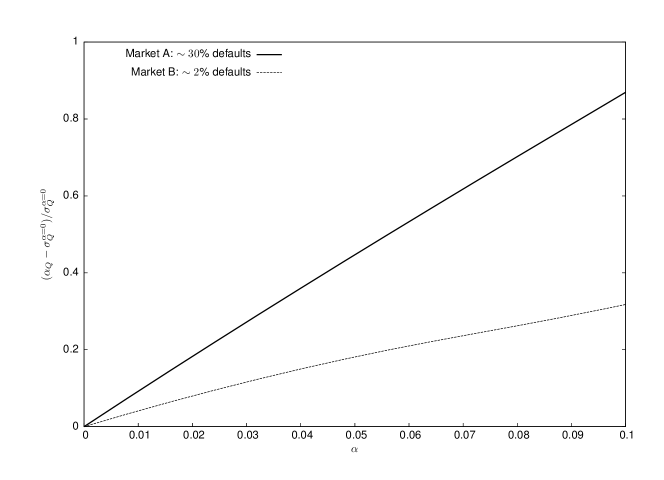

To better identify the relation between farmers default and production volatility , in Figure 7 we compare two different market conditions corresponding to different levels of exogenous parameters (details reported in the figure caption): one characterized by a large default rate , the other characterized by a smaller , in which subsidization effects are simulated by artificially raising the level of consumers’ demand (which is equivalent to a softening of the liquidity constraint). As can be seen the financialization effect, i.e. the relative increase in production volatility with increasing market integration is much larger in the market with higher default rates.

Notice that within our model the main channel of propagation of instability induced by financialization is the lack of an efficient hedging channel able to transfer the liquidity risk. Thus, the most dangerous fluctuations are not price fluctuations but rather those induced by fluctuations in default rates.

A thorough analysis of the policy implications under similar assumptions is discussed in [9], where it is suggested that subsidies are determined by the necessity to reduce default rates to improve welfare. Within our equilibrium solution all those conclusions continue to hold. It is however important to point out an important distinction: in our model defaults are driven by liquidity rather than credit risk. This is consistent with the well known observation that in most of case subsides are given to land owners which are well collateralized and have a reduced exposure to credit risk.

4.4 Can farmers’ hedging be effective? Some basic risk management policy considerations

In our model farmers are not allowed to invest in the financial market and financial investors do not invest in real production. It is important to notice, however, that this restriction does not impose any limit in the diversification opportunities of liquidity risk affecting production. The farmer can reduce the default probability only by reducing the amount of capital invested in the production of the real commodity. However, this farmer decision will not have any consequence on aggregate sector quantities.

Assume that a representative investor is allowed to invest both in real and financial activities by maximizing the risk return trade-off on those activities. The asymmetric impact of market integration on the returns of real production and financial trading would imply that the optimal allocation in financial investment would increase with and the investment in production would be depleted. Changing the identity of the investors would not modify the clearing equation (21). For this reason the global relations of quantity, price and farmers’ survival fraction (and their volatility) would remain unaffected by any farmer hedging policy. The key condition is that the liquidity constraint applies only to real investment and generates capital market segmentation which is not mitigated by financial hedging.

Despite our model does not address the welfare implications of the market imperfections, it suggests that an improvement in the liquidity risk management should be one of the main goals of optimal market regulations, taxation schemes and public subsidization programs and correspondingly that such policies should enhance liquidity risk sharing between producers, intermediaries and traders investing in commodity markets. Stated that the longer is the investment horizon, in presence of large fitness uncertainty, the larger is the liquidity risk, optimal intervention schemes could be introduced to classify different agents according to their time to produce.

5 Conclusions

In this paper we have shown that, at least in principle, in commodity markets dominated by uncertainty and characterized by a “time to produce” , at a certain critical level of market integration a financial trader operating with a deterministic strategy can take advantage of his “on time” action to realize a profit. Upon the introduction of a diffusive market stochastic fitness, we demonstrate that this is the consequence of a competitive equilibrium generated by the asynchronous decisions of the two agents participating in market clearing: producers are forced by their production cycle to anticipate market decisions when programming their production strategy, while financial investors can instantaneously react to current prices. In fact, the long production cycle operates as a credit and liquidity risk multiplier on farmers, which, along with liquidity constraints on production, makes the long-term (production) investments much riskier than short-term (financial) investments: due to the presence of liquidity constraints on long-term producers, the integrated spot commodity and financial market is inefficient in sharing the risk between market participants.

The model shows that more elastic markets tolerate larger values of market integration. On the contrary negative effects of market financialization are more pronounced on those markets characterized by long production cycles andor large market fitness volatility. Among negative effects we point out that the combined effect of liquidity constraints and market financialization amplifies producers’ risk and production volatility. This fact may result in markets which are unprotected by price turbulence if investors move suddenly elsewhere their financial activity towards different investment targets. The model presented here can be developed and improved along many directions: first the above model implications can be tested on real data and an empirical analysis would certainly improve our understanding of market imperfections, second our analysis does not take into account the relevant sustainability issues which are generated by the complex interaction between commodity production, food quality health programs and standards of living of consumers. As for the first issue we note that if spot commodity and financial market integration is proxied by the relative size of short and long-term allocations, our model predicts that for a specific commodity this quantity should positively correlate with production volatility of that commodity.

Appendix A Supplementary information

A.1 The producers’ expectation

The model solution discussed in Section 2 depends on the determination of the farmers’ expectation , which is calculated as given in Eq. (14) and using the price schedule obtained by solving Eq. (21). The Eq. (14) is a non-linear self consistent equation of the form , where the expectation value is also present in the second member through the price schedule . The Eq. (14) is solved with respect to using a numerical iterative algorithm based on the secant method. The algorithm starts from a guess and find the value that satisfy the convergence criteria , after iterations.

At each iteration the second member is calculated by computing the integral numerically using a grid of points over the range of possible . Even though the distribution of has an unbounded support, in practice we truncate the distribution at four standard deviation from the mean . The number of grid points has been chosen in such a way that the integral does not change more than between two consecutive grid points. The integrand is evaluated at each value of on the grid and a constant interpolation between the grid points is used for values of not on the grid. The integrand evaluation is obtained by solving numerically the clearing equation Eq. (21) in the form:

| (22) |

where is given in Eq. (13) and is a function , while is given in Eq. (7) and is a function of only. The numerical iterative algorithm starts from a guess value and finds the equilibrium price when the convergence criteria over iterations is satisfied. In practice convergence is achieved after iterations, where is typically between and , and between and depending on the initial guess values for .

The clearing equation Eq. (21) has a single solution as demonstrated in Section A.2 . The existence of a single solution for the expectation can be analytically demonstrated in the case of a single farmer (see Section A.3). In the more general case, we checked that the algorithm described above converges always to the same value by starting the solution search from different initial guess values for , distributed at random between and .

A.2 Existence condition for the equilibrium price

For a given realization of the fitness uncertainty , the demand curve in Eq. (21) is a monotonic decreasing function of , while, due to the price dependence of through (see Eq. (13)), the supply curve is monotonic increasing in . For this reason the price forms, i.e. it exists the equilibrium solution of Eq. (21), if . Since is limited from above the existence condition becomes:

| (23) |

that also depends on the financial investor’s strategy. For the solution always exists. When this condition is satisfied the clearing equation always has a single positive solution .

A.3 Simplified equilibrium solution for a single farmer

In this section we provide the analytic solution of a simplified formulation of the commodity market model described in this paper. We consider a single farmer case. Thus, Eq. (21) becomes:

| (24) |

Under the hypothesis that, in order to make hisher production decision, the producer takes the price schedule solving the clearing equation (24) with :

| (25) |

the expected value solving Eq. (14) reduces to:

| (26) |

Developing the probability distribution of in cumulants, Eq. (26) can be solved with respect to and we obtain the single solution:

| (27) |

where .

Expanding into a power series with center , the constant (), 1st-order () and 2nd-order () approximation are respectively:

The approximate analytic form of the financial investor’s return (Eq. (18)) is then:

| (28) |

where:

| (29) |

and is the financial transaction cost.

References

- [1] O. Orhangazi, Financialisation and capital accumulation in the non-financial corporate sector: A theoretical and empirical investigation on the US economy: , Cambridge Journal of Economics 32 (6) (2008) 863–886.

- [2] G. Soros, Testimony at the Senate Hearing On Energy Market Manipulation and Federal Enforcement Regimes. URL: http://www.gpo.gov/fdsys/pkg/CHRG-110shrg80428/html/CHRG-110shrg80428.htm (2008).

-

[3]

G. Tadesse, B. Algieri, M. Kalkuhl, J. von Braun,

Drivers and triggers

of international food price spikes and volatility , Food Policy 47 (2014)

117–128.

URL http://dx.doi.org/10.1016/j.foodpol.2013.08.014 - [4] A. S. Mello, J. E. Parsons, Margins, Liquidity, and the Cost of Hedging, Journal of Applied Corporate Finance 25 (1) (2013) 34–43.

- [5] J. E. Parsons, A. S. Mello, Rising food prices: What hedging can and cannot do, Blog: Betting the Business Financial risk management for non-financial corporations. URL: http://bettingthebusiness.com/ 2011/06/27/rising-food-prices-what-hedging-can-and-cannot-do/ (2011) [cited 2013].

- [6] I. A. Cooper, A. S. Mello, Corporate Hedging: the Relevance of Contract Specifications and Banking Relationships, European Finance Review 2 (1999) 195–223.

- [7] G. Allayannis, Comment on ”Corporate Hedging: The Relevance of Contracts Specifications and Banking Relationships”, European Finance Review 2 (1999) 225–228.

- [8] A. S. Mello, J. E. Parsons, Hedging and Liquidity, Review of Financial Studies 13 (1) (2000) 127–153.

- [9] H. D. Leathers, J.-P. Chavas, Farm debt, default, and foreclosure: An economic rationale for policy action, American Journal of Agricultural Economics 68 (4) (1986) 828–837. arXiv:http://ajae.oxfordjournals.org/content/68/4/828.full.pdf+html, doi:10.2307/1242129.

- [10] M. J. Brennan, The supply of storage, American Economic Review 48 (1958) 50–72.

- [11] J. C. Williams, B. D. Wright, Storage and Commodity Markets, Cambridge: Cambridge University Press, 1991.

- [12] A. Deaton, G. Laroque, On the Behavior of Commodity Prices, Review of Economic Studies 59 (1992) 1–23.

- [13] A. Deaton, G. Laroque, Competitive storage and commodity price dynamics, Journal of Political Economy 104 (5) (1996) 896–923.

- [14] B. R. Routledge, D. J. Seppi, C. S. Spatt, Equilibrium forward curves for commodities, Journal of Finance 60 (2000) 1297–1338.

- [15] J. M. Keynes, A Treatise on Money: The Applied Theory of Money, Vol. 2, London: Macmillan, 1930.

- [16] C. Hicks, Value and Capital, New York: Oxford University Press, 1939.

- [17] D. Hirshleifer, Residual Risk, Trading Costs, and Commodity Futures Risk Premia, Review of Financial Studies 1 (2) (1988) 173–193.

- [18] P. A. Samuelson, Stochastic speculative price, Proceedings of the National Academy of Science 68 (1971) 335–337.

-

[19]

B. C. Briggeman, C. A. Towe, M. J. Morehart,

Credit

Constraints: Their Existence, Determinants, and Implications for U.S. Farm

and Nonfarm Sole Proprietorships, American Journal of Agricultural

Economics 91 (1) (2009) 275–289.

URL http://ideas.repec.org/a/oup/ajagec/v91y2009i1p275-289.%html - [20] J.-P. Chavas, On information and market dynamics: The case of the U.S. beef market, Journal of Economic Dynamics & Control 24 (2000) 833–853.

- [21] J. Vercammen, Farm bankruptcy risk as a link between direct payments and agricultural investment, European Review of Agricultural Economics 34 (4) (2007) 479–500.

- [22] Z. Zhou, An Equilibrium Analysis of Hedging with Liquidity Constraints, Speculation, and Government Price Subsidy in a Commodity Market, The Journal of Finance 53 (5) (1998) 1705–1736.

- [23] V. Acharya, L. Lochstoer, T. Ramadorai, Limits to Arbitrage and Hedging: Evidence from Commodity Markets, Working paper, New York University.

| 0.6 | 0.02 | 0.1 | 0.2 | 0.5 | 0.6 | 0.0002 |