A Cross-Entropy-based Method to Perform Information-based Feature Selection

Abstract

From a machine learning point of view, identifying a subset of relevant features from a real data set can be useful to improve the results achieved by classification methods and to reduce their time and space complexity. To achieve this goal, feature selection methods are usually employed. These approaches assume that the data contains redundant or irrelevant attributes that can be eliminated. In this work, we propose a novel algorithm to manage the optimization problem that is at the foundation of the Mutual Information feature selection methods. Furthermore, our novel approach is able to estimate automatically the number of dimensions to retain. The quality of our method is confirmed by the promising results achieved on standard real data sets.

keywords:

Feature Selection; Mutual Information; Cross-Entropy Algorithm.1 Introduction

Since the 1960s, the rapid pace of technological advances allows to measure and record increasing amounts of data, producing real data sets comprising high-dimensional points. Unfortunately, due to the “curse of dimensionality” [1], high dimensional data are difficult to work with for several reasons. First, a high number of features can increase the noise, and hence the error; secondly, it is difficult to collect an amount of observations large enough to obtain reliable classifiers since several classifiers do not properly deal with classification problems where the number of observations is lower than, or comparable to, the data dimensionality (see [2, 3, 4]); finally, as the amount of available features increases, the space needed to store the data becomes high, while the speed of the employed algorithms could be too low.

For all the above mentioned reasons, feature selection algorithms are often employed as the first pre-processing step to improve classification performances. The aim of a feature selection technique is to identify a subset of relevant features to use in model construction. The main assumption when using a feature selection technique is that the data contains redundant or irrelevant attributes that can be omitted. Formally, given the input data matrix composed by samples and features (), and the target classification vector , the feature selection problem is to find a -dimensional subspace () by which we can characterize . Many interesting approaches have been proposed in literature [5] but most of them have a main drawback, they are not able to automatically estimate the value of .

In this work we present a novel algorithm to manage the optimization problem that is at the foundation of the Mutual Information (MI, [6, 7]) feature selection methods. Moreover, the proposed approach is able to estimate automatically the value of . We develop an algorithm based on the Cross-Entropy approach, to filter out the set of features among all those available. We perform this operation through a stochastic approach, which allows us to select efficiently the minimal feature set that minimizes the conditional entropy between and the class attribute . The quality of our method is confirmed by the promising results achieved on standard real data sets.

This paper is organized as follows: in Section 2 the related works are presented; in Section 3 the theoretical background underlying our approach is summarized; in Section 4 our algorithm is described; in Section 5 the experimental results are presented; finally, in Section 6 our conclusions are highlighted.

2 Related Works

From a machine learning point of view, if a classification algorithm uses irrelevant variables to generate the model, this model can be affected by poor generalization capabilities. To delete irrelevant features, a selection criterion is required. Once a feature selection criterion is selected, a procedure must be developed to find the subset of useful features. Directly evaluating all the subsets of features () for a given data is a NP-hard problem. For this reason, a suboptimal procedure must be employed to remove redundant data with tractable computations.

In [8], the feature selection methods are classified into filter and wrapper methods. Filter methods compute the rank of the features employing different criterion and select the highly ranked features that are applied to the predictor. In wrapper methods the feature selection criterion is the performance of the predictor; precisely, the classifier is wrapped on a search algorithm which will find a subset which gives the highest predictor performance.

Considering the filter feature selection approaches, one of the simplest criteria employed is the Pearson correlation coefficient [9] that is defined as follows:

| (1) |

where is the -th variable, is the output (class labels), is the covariance and the variance. It is important to notice that, this criteria can only detect linear dependencies between variable and target.

To overcame this limitation many approaches employ information theoretic ranking criteria to exploit the measure of dependency between variables. The MI between random variables is defined as follows:

| (2) | |||||

where is the entropy function, and or or both can be matrixes or vectors.

One of the simplest MI-based methods for feature selection is to find the MI between each feature and the output class labels and rank them based on this value. A threshold is set to select features. The results of this method can be poor (for further details see [10]) since inter-feature MI is not taken into account. Some approaches that improve the results of the aforementioned technique are proposed in [11], [12], and [13].

Another example of this kind of algorithm is given in [14], where the authors model the classification procedure through the probability that is the probability to have the class for the set of features . Under the assumption that there exists a subset of features such that the probability is close to , the authors evaluate minimizing the Kullback-Leibler’s (KL) divergence between the previous probabilities over all possible sets of features. Exploiting the theory of Markov Blanket for the set of features, the authors provide an approximate methodology for the feature selection, which relies on the following considerations: for each feature , let be the set of features for which the correlation between and has largest magnitude, the KL-Divergence is evaluated for each , the selected features are those one for which this quantity is minimal, then the set of selected feature is . This algorithm shows many weaknesses. First of all, due to the approximations adopted during the procedure (such as the Markov Blanket construction and KL-Divergence evaluation), the algorithm provides a suboptimal solution. Moreover, the algorithm needs as input the size of the set of the selected features, and evaluates the correlation between all the possible pairs of features, therefore it cannot be efficient for domains containing hundreds or even thousands of features.

An improvement of the previous approach is based on the Mutual Information Maximization (MIM) as proposed in [7]. In this algorithm the features are ranked depending on the mutual information between each of them and the class attribute. MIM supposes that all the features are independent and its criterion is to maximize the mutual information between feature and class attribute .

In[15] authors propose an extension of MIM called Conditional Mutual Information Maximization (CMIM). This approach iteratively picks features which maximize their mutual information with the class to predict, conditionally to the response of any feature already picked. This Conditional Mutual Information Maximization criterion does not select a feature similar to already picked ones, even if it is individually powerful, as it does not carry additional information about the class to predict. This criterion ensures a good tradeoff between independence and discrimination.

It is important to notice that, MIM takes into account only the features that are relevant with the class variable (Maximal Relevance) but it does not consider any dependencies between these features. One desirable property is to have not features that are dependent since they produce redundant information. This is the main idea of the minimal-Redundancy-Maximal-Relevance criterion (mRMR) [16]. Precisely, this approach searches for the relevant features with the minimum redundancy.

In [17], the authors introduce a new information theoretic criterion: the Double Input Symmetrical Relevance (DISR). DISR measures the symmetrical relevance of two features in all the possible combinations of a subset and selects among a finite number of subsets the most significant one. One advantage of DISR is that a complementary feature of an already selected feature has higher probability to be chosen.

In [18], the authors measure the relationship between the candidate feature subsets and the class attribute exploiting the results on the Discrete Function Learning (DFS) algorithm jointly to the high-dimensional mutual information evaluation. The method proposed by the author uses the entropy of the class attribute as the criterion to choose the appropriate number of features, instead of subjectively assigning the number of features a priori. Again, the authors provide the following interesting result: if the mutual information between a feature set and the class attribute is equal to the entropy of , then is a Markov Blanket of .

Wrapper methods employ the predictor performance as the objective function to evaluate the variable subset. Since evaluating subsets is a NP-hard problem, suboptimal subsets are identified by employing heuristic search algorithms. The Branch and Bound method, proposed in [19], uses tree structures to evaluate different subsets for the given feature selection number. Nevertheless, the search would grow exponentially for higher number of features. For these reasons, simplified algorithms such as sequential search or evolutionary algorithms (Genetic Algorithm GA [20] or Particle Swarm Optimization PSO [21]) which yield local optimum results are employed. The PSO is a population-based search technique and is motivated by the social behavior of organisms. It is based on swarm intelligence and well suited for combinatorial optimization problems in which the optimization surface possesses many local optimal solutions. The underlying phenomenon of PSO is that knowledge is optimized by social interaction where the thinking is not only personal but also social. The particles in PSO resemble to the chromosomes in GA. However, PSO is usually easier to implement than the GA as there are neither crossover nor mutation operators in the PSO and the movement from one solution set to another is achieved through the velocity functions.These approaches can produce good results and are computationally feasible but are strongly related to the selected predictor.

Most of the filter methods stated above perform the feature selection basing their research on the maximization/minimization of the amount of information carried by the selected features about the class attribute. In this case Information Theory provides a solid mathematical framework to state the problem, that can be implemented through an algorithm based on many different optimization approaches, such as robust, genetic, or Bayesian-based. The main advantages offered by the algorithms based on Information Theory are that the features with redundant information are filtered out, and the performances of these algorithms do not degrade for high-dimensional sets of features. Moreover, the solid mathematical framework allows a rigorous performance evaluation of the developed techniques. Most of the the algorithms discussed above overcome many of the problems related to the feature selection: they have a sound theoretical foundation, they are effective in eliminating both irrelevant and redundant features, they are tolerant to inconsistencies in the training data, and finally, they are filter methods which do not suffer the high dimensionality of the space of features. The main shortcomings lie in: candidate feature is evaluated pairwise (step by step) with respect to every individual feature in the selected feature subset; the number of features needs to be specified a-priori. The motivation for the first shortcoming is that the feature is good only if it carries information about the class attribute and such information has not been caught by any of the features already picked. However, it is unknown whether the existing features as a vector have captured the information carried by or not. Due to the second shortcoming, the performances of most of the state-of-the-art algorithms can be affected by an imprecise selection of the value of .

Our algorithm overcomes all the weakness shown by these algorithms, in fact, all the estimated variables are evaluated through optimized algorithms and are not approximated; the candidate feature is not evaluated pairwise with respect to every individual feature in the selected feature subset; finally, the algorithm estimates autonomously the dimension of the set of selected features.

3 Theoretical Background

In this section we introduce the theoretical background related to the feature selection approaches based on the information theoretic ranking. These concepts are exploited to explain the optimization problem related to the feature selection addressed in this paper. In Section 4 we provide a statistical interpretation of the optimization problem, and then, we propose a Cross-Entropy based method to find a solution for that.

We start recalling the meaning of Mutual Information (MI). Mutual information can be used to measure the amount of information obtained about a random variable , through another one . We remember that MI is a symmetric non-negative function. Furthermore, the MI is strictly related to the entropy of a random variable, which defines the amount of information held in . Note that, the entropy of grows if its outcomes have low probability to arise, otherwise the entropy decreases. Hence we can assert that the entropy measures the diversity of in terms of uncertainty of its outcomes. The MI between random variables is defined as in the equation (2).

In our case study, we are interested to the MI between the subset of features , and the class attribute :

| (3) |

where is the amount of information needed to describe conditioned by the information held in about . Hence, this quantity represents the dependence between and , precisely, the greater the information that can be obtained about through , the lowest the information needed about once that has been known. This means that the features in can fully determine the values of . In this case the features into the set are called essential attributes (EAs). This means that if the features in are EAs, then the equation (3) gets is maximum. The considerations discussed above have been summarized in the theorem that follows next, which has been proven in [22, 6].

Theorem 1.

If the MI between and is equal to the entropy of , then is function of .

The quantities in equation (3) can be evaluated trough a set of samples of both class attribute and subset of selected features, then, for , and . A powerful tool for the entropy and mutual information functions evaluation can be found in [23].

Now, we explain the information maximization criteria used for the information-based ranking. As stated above, the MI measures the amount of information obtained about a random variable , through . As proven in the papers [6, 22] the can be written as:

| (4) | |||

| (5) |

Equations (4-5) allow to select iteratively the features in , so that the MI can be maximized. Precisely, in the first step we select the j’-th feature that shares the largest MI with the class attribute , searching within the native set. During the other iterations, the feature is selected if it adds the maximum information to the already selected features , by searching into the native set minus the features already selected. An intuitive proof of equations (4-5) is given through the example in figure 1. In this example the circles are the entropies of the variables, and the gray regions are the MI between the feature that can be selected and the class attribute , given the already selected features . Hence, the feature to be selected is in this example. In figure 1, the sum of dashed and gray areas is the information shared between and the new feature or , respectively. Instead, the shared information between and is the sum of the dashed and dotted areas. Then, if we want to evaluate the information about carried by the new feature given the set , we need to take into account only the gray area, which is greater in the case of than in the case of . This means that contains most of the information carried by about , then is redundant and can be eliminated. In fact, the dashed area is greatest in the case of . On the opposite, the feature can be saved because carries new information about not yet contained in .

Hence, selecting iteratively the features of satisfying the equality , can be taken as complete subset for the prediction of (see theorem 1). Note that the equalities discussed above are obtained at the limit, hence, the problem of finding optimal feature subsets is equivalent to find the subset , over the native set, subject to , or equivalently subject to .

The results discussed above are very important, because they allow us to design our optimized algorithm for the selection of the optimal features. In the next section, we provide the mathematical framework, and then the new algorithm for the search of the subset of features that minimizes , avoiding the research of the solution on a set of elements, given that these are all possible set with cardinality for a native set with cardinality .

4 The Algorithm Formalization

In this section we present a novel and effective algorithm to find the solution for the feature selection problem based on the information theoretic ranking, presented in the previous section. As stated above, this search can be performed through our optimized procedure based on the mathematical framework described in the following.

The approach adopted in this work is based on the stochastic research of the solution. The main idea of this approach is to associate to each feature () a binary variable that can take value with probability . This is called Associated Stochastic Problem ASP [24]. Our algorithm finds which variables must have , so that the objective function given by is maximum. This means to find the optimal density distribution of the binary vector that has the entry to if the feature must be selected to maximize . Then, we can perform the search of the solution on a probability space through the ASP, and no longer on the initial space given by all the possible combinations of indexes of the features. Then, the combinatorial problem based on equations (4-5) has become a convex problem (for more details see Appendix A) through the ASP.

Hence, we start defining the ASP for our initial maximization problem. Let be a binary vector of cardinality , where if the feature belongs to and otherwise. Hence, we can rewrite the subset of the selected features as function of . In this case, the objective function for our is again a function of . Our goal is to forecast which entries of must be set to to maximize subject to . The last step to define our ASP is to assume that are independent Bernoulli random variables where the probabilities to get the value are , respectively. Then the evaluation problem of the distribution of entries equal to in , for which the objective function is maximum , can be formulated as in the following: to find the distribution of the values in , under a given parameter , which maximizes the probability for the objective function to be greater or equal to , i.e. .

Note that can be estimated through the following equation given the probability distribution function :

| (6) |

where is the indicator function of the event . The indicator function is equal to for all the possible configurations of that verify the event , and otherwise.

A well known approach to estimate the probability in the equation (6) is to use the Likelihood Ratio (LR) estimator with reference parameter . From the theory of LR estimator [24] the best value , such that the samples drawn from provide the maximum value for our objective function , can be calculated through the following equation:

| (7) |

where is a set of possible samples drawn by the distribution and .

As stated above is a vector of independent Bernoulli random variables where takes value equal to with probability and with probability . Then for the assumptions stated above, the probability distribution of the ones in can be rewritten with parameter as in the following:

| (8) |

Given that for equation (7) it holds the convexity property, its solution can be found in a closed form through derivation w.r.t. and imposing the derivative to be equal to .

| (9) |

The equation (9) allows us to evaluate the vector , where its entries closer to correspond to the entries of that with high probability take the value .

The derivation of equations 7-9 is shown in the Appendix A where the optimality of the probability distribution function is also proven.

Summarizing, we found the density distribution of the entries in that take the value , these entities provide the set of the indexes of the features that maximize the objective function that is the mutual information .

The solution for the probability can be calculated through an iterative algorithm as showed in the following (see Algorithm 1).

The Algorithm 1 estimates iteratively the value , and hence it helps to evaluate the vector of the indexes of the selected features that maximize the function . The algorithm finds the optimal value of the probability vector after steps, starting from the uniform distribution at step . The distribution probability at each step is refreshed trough the samples drawn from the distribution and the equation (9). Precisely, the events are verified over the samples , and then, in the equation (9) are used only those samples belonging to the -quantile that verifies the inequality . This means that the maximum of the objective function is refreshed with its -quantile step by step. The stopping criteria for the algorithm is stated as follows: if the max value of the objective function does not change by at least after steps, the optimal distribution probability is found. Assuming that the algorithm finds after steps, then entries of will be very close to and entries will be very close to .

The parameters and can be statically set as in the Algorithm 1, or, they can be dynamically computed at each step. In the first case the tuning of these parameters can be found in [24]. In the last case (which is ours), the parameter can be evaluated generating multiple sequences of samples at each step , by ranging their length between and . The value is set to the cardinality of the unknown parameters ( in our case) and the value is set to the empirical value . For each sequence of length , the event is verified, then the length adopted at the step is the largest which generates the -quantile . At the same time, the quantile parameter at the step is evaluated through the empirical formula . Finally, the threshold parameter is set to the empirical value of (for further details about the tuning parameters see [24], chapter 5).

Through we can evaluate the distribution of the ones in , i.e. the best set of features for our maximization problem. Moreover, through we are able to study the behavior of the error of the classification model, for different size of the set of the selected features (for more details see [24]).

5 Experimental Results

The performance evaluation of our algorithm has been performed on six data sets from UCI Machine Learning Repository [25]. All experiments have been performed on an iMAC endowed with a 2,4 GHz Intel Core 2 Duo, and 4 GB of SDRAM at 667 MHz. All the involved algorithms have been implemented in MATLAB.

The chosen data have integer and real values for the class attributes, and they can have single or multi-label class attributes. Considering the feature values, they can take integer and real values, and the cardinality of features set ranges between medium to wide size.

| Advertisements | Blog Feedback | Cancer Breast | |

| num. samples | 3279 | 52397 | 569 |

| num features | 1558 | 280 | 32 |

| feature type | Binary/Real | Real/Integer | Real |

| attribute type | Binary | Integer | Binary |

| Connect-4 | Forest Fires | Gesture Phase | |

| num. samples | 67557 | 517 | 1444 |

| num features | 42 | 12 | 32 |

| feature type | Integer | Real | Real |

| attribute type | Integer | Real | Integer |

Precisely, the Advertisements dataset represents a set of possible advertisements on Internet pages. The features encode the geometry of the image, if available, the phrases occurring in the URL, the image’s URL, the alt text, the anchor text, and words occurring near the anchor text. The task is to predict whether an image is an advertisement ‘1’ or not ‘0’.

The Blog Feedback data set contains the data originated from blog posts. The raw HTML-documents of the blog posts were crawled and processed. The prediction task associated with the data is to identify the number of comments in the upcoming 24 hours. Precisely, the features represent the average, standard deviation, min, max and median of the parameters, and others parameters which characterize the number of comments in the time, such as number of comments in the first 24 hours after the publication of the blog post, and the length of the blog post. The class attribute is the number of comments in the following 24 hours.

The Cancer Breast data are computed from a digitized image of a fine needle aspirate of a breast mass. They describe characteristics of the cell nuclei present in the image. The features are real values and represent the image characteristics of the nuclei, such as radius, texture, smoothness. The class attribute is a binary value that is the diagnosis malignant ‘1’ or not ‘0’.

The Connect-4 data set contains all legal 8-ply positions in the game of connect-4 game, in which neither player has won yet, and in which the next move is not forced. The features are integer values and represent the positions taken by one of the two players on a matrix with six rows and seven columns. Precisely, if the player 1 takes the position of the matrix , if the position is taken by the player 2 , if it is blank . The class attribute is an integer value that is the result of the game: ‘1’ or ‘0’ if one of the two players won, or ‘2’ if it was a draw.

The Forest Fires data set contains information about all the parameters that can be involved in the forest fires. The features are real values and represent the spatial coordinates of the forest, the date, the parameters of the most famous forest fire danger rating systems, and the weather parameters. The class attribute is a real value that is the burned area of the forest.

The data set Gesture Phase contains the data about the temporal segmentation of gestures, performed by gesture researchers in order to pre-process videos for further analysis. The data set is composed by the data that come from videos recorded using Microsoft Kinect sensor. The collected features represent an image of each frame identified by a timestamp, the text file containing positions coordinates , , of six articulation points: left hand, right hand, left wrist, right wrist, head and spine, with each line in the file corresponding to a frame and identified by a timestamp. The class attribute is an integer value that is the gesture phase: Rest ‘1’, Preparation ‘2’, Stroke ‘3’, Hold ‘4’, Retraction ‘5’. Table 1 summarizes the data sets used during the performance evaluation.

| Advertisements | Blog Feedback | Cancer Breast | ||

| Our | 0.1055 | 0.3837 | 0.0371 | |

| 0.0037 | 0.0018 | 0.01 | ||

| 0.002 | 0.2965 | 25.0797 | ||

| 176.29 | 178.12 | 162.54 | ||

| DISR | 0.21 | 0.5071 | 0.0726 | |

| 0.1459 | 0.3888 | 0.01 | ||

| 0.1038 | 0.3414 | 24.7977 | ||

| 167.46 | 184.62 | 184.43 | ||

| CMIM | 0.1169 | 0.4364 | 0.0856 | |

| 0.0065 | 0.22 | 0.01 | ||

| 0.0096 | 0.2945 | 23.1734 | ||

| 174.17 | 164.44 | 172.63 | ||

| mRMR | // | 0.4979 | 0.0705 | |

| 0.0103 | 0.1568 | 0.01 | ||

| 0.0181 | 0.3725 | 23.9602 | ||

| 184.43 | 184.76 | 180.51 | ||

| Cardinality | 39 | 93 | 20 | |

| Connect-4 | Forest Fires | Gesture Phase | ||

| Our | 0.3904 | 0.0775 | 0.2888 | |

| 0.00067 | 0.052 | 0.01 | ||

| 0.0011 | 0.0115 | 0.0244 | ||

| 178.27 | 172.65 | 161.95 | ||

| DISR | 0.4361 | 0.0789 | 0.2915 | |

| 0.1457 | 0.068 | 0.01 | ||

| 0.3648 | 0.0532 | 0.0241 | ||

| 164.05 | 180.31 | 161.39 | ||

| CMIM | 0.4267 | 0.0789 | 0.5591 | |

| 0.0228 | 0.063 | 0.01 | ||

| 0.0396 | 0.0532 | 0.0241 | ||

| 171.04 | 184.49 | 181.73 | ||

| mRMR | 0.4406 | 0.0899 | 0.3099 | |

| 0.1691 | 0.0797 | 0.01 | ||

| 0.4591 | 0.0455 | 0.0306 | ||

| 183.39 | 176.89 | 183.85 | ||

| Cardinality | 32 | 5 | 29 |

To assess the performance of our algorithm we have generated independent training and validation sets from the aforementioned data sets. The training and test sets are independent for the Blog Feedback data set, instead, for the others data set the training and test sets have been evaluated through the partition and , respectively. As stated in Section 4, parameters and are dynamically computed at each step of the algorithm. Instead, entries of the initial probability vector have been set all to , and the exit condition for the algorithm has been set to with , as suggested in [24].

The performances of our algorithm have been compared with those achieved by the following Information-based feature selection algorithms: DISR, CMIM, and mRMR. For the performance evaluation the parameters taken into account are: the misclassification error (MCE), the relative difference of information (), and the execution time () in seconds. The MCE is the number of misclassified observations divided by the number of observations on the test set as a function of the number of features; the is the ratio between the difference and the Mutual Information ; and the is merely the time spent to get the set of selected features. Through the MCE we can study the accuracy of the given classification model, using the selected features. Instead, through the we can study how well the class attribute can be represented as function of the set of selected features. Precisely, the class attribute is function of the selected features for close to zero.

For the evaluation of the MCE we have taken into account a classification model that fits the multivariate normal density to each group, with a pooled estimate of covariance or with a diagonal covariance matrix estimate through Naive Bayes classifiers. Moreover, we have also employed the KNN classifier (with ) thus to use a different predictor to fully evaluate the proposed method.

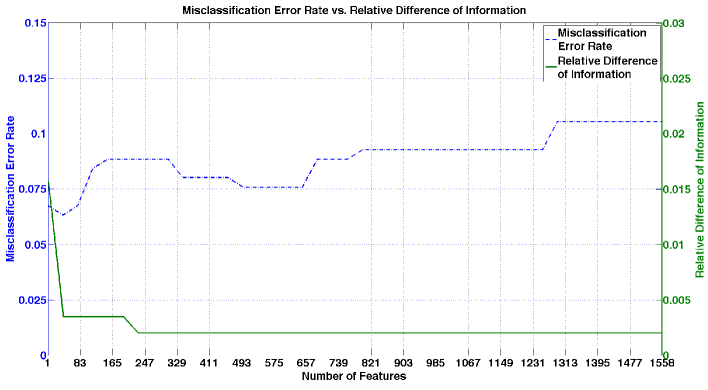

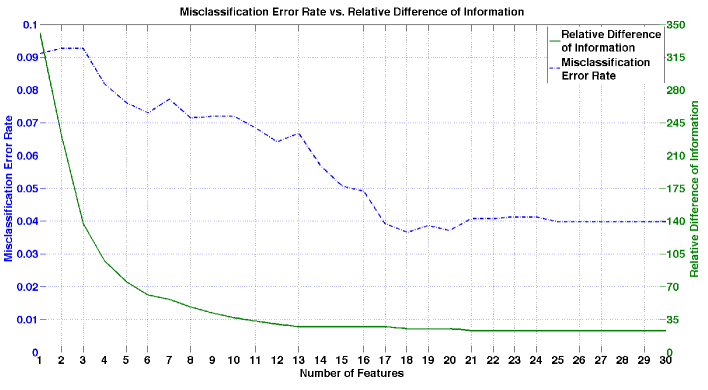

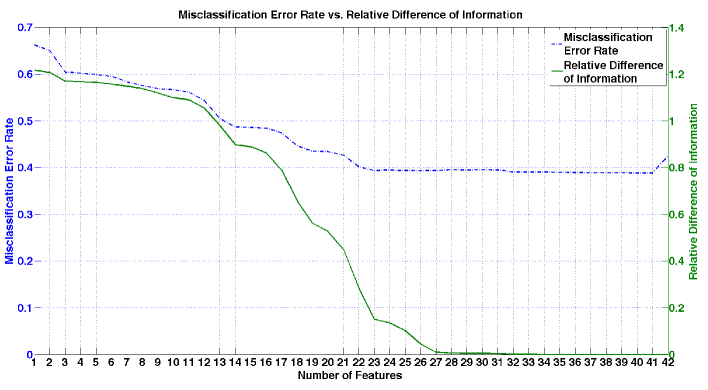

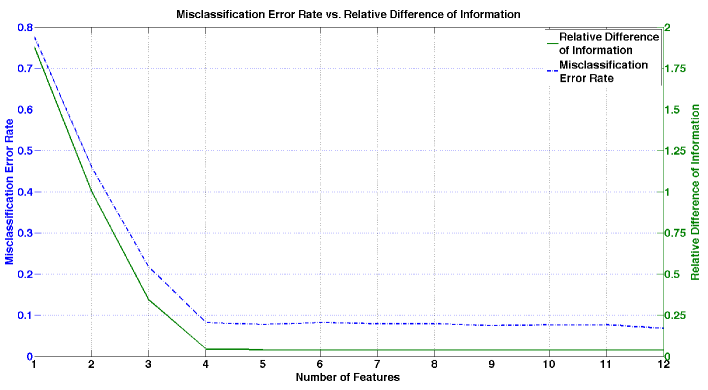

Table 2 summarizes the performance results in terms of MCE (both employing Naive Bayes, , and KNN, ), , and , where the bold entries are the best results obtained. These results show how our algorithm, in all the data set analyzed, is able to find the optimal set of features which minimizes . Note that our method in some cases provides one order of accuracy more than other techniques. Moreover, in the cases where this does not happen, it is due to the fact that our algorithm minimizes also the MCE for the optimal set of selected features. The rows labelled as Cardinality shows the cardinality of the feature set automatically selected through our approach111This cardinality is used to evaluate the set of features selected by the other algorithms taken into account in this work.. Considering , our approach always shows a comparable time cost222Notice that, the implementation of our approach is not fully optimize whilst for the other algorithms we have used optimized toolbox implementations..

The first clear advantage given by our algorithm is the ability to find the best minimum set of features that maximize . Moreover, our algorithm finds the set of features that minimizes at the same time the MCE and the as shown in the figures 2-6. Each figure shows the MCE and the as functions of different values of retained features. These figures show that the chosen set of features as well as their cardinality are the best for the addressed problem, indeed, for the chosen cardinality the MCE and the have the global minimum.

| Advertisements | Blog Feedback | Cancer Breast | ||

| Our | MCE | 0.1055 | 0.3837 | 0.0371 |

| 0.002 | 0.2965 | 25.0797 | ||

| 176.29 | 178.12 | 162.54 | ||

| PSO | MCE | 0.1441 | 0.4851 | 0.0523 |

| 0.0084 | 0.3345 | 23.6741 | ||

| 302.67 | 289.32 | 198.78 | ||

| Cardinality CE/PSO | 39/42 | 93/87 | 20/18 | |

| Connect-4 | Forest Fires | Gesture Phase | ||

| Our | MCE | 0.3904 | 0.0775 | 0.2888 |

| 0.0011 | 0.0115 | 0.0244 | ||

| 178.27 | 172.65 | 161.95 | ||

| PSO | MCE | 0.4345 | 0.0878 | 0.266 |

| 0.0525 | 0.0492 | 0.0287 | ||

| 174.32 | 201.02 | 196.21 | ||

| Cardinality CE/PSO | 32/27 | 5/ 5 | 29/35 |

We have also compared our algorithm with the Particle Swarm Optimization method (PSO, [26]), which is one of the most representative heuristic methods, since the heuristic approaches can be suitable to address this kind of problem. The comparison results are shown in table 3, where the bold entries are again the best results obtained.

The results show that our algorithm has better performance especially in terms of . In fact, the PSO algorithm selects the subset of features by a random proportional rule, and even if the algorithm analyzes the research history (see [26]), its convergence is slower with respect to our algorithm. The main advantage given by our approach is that we refresh the joint occurrence probability of the features step by step, which provides faster and more accurate convergence compared with the proportional rule.

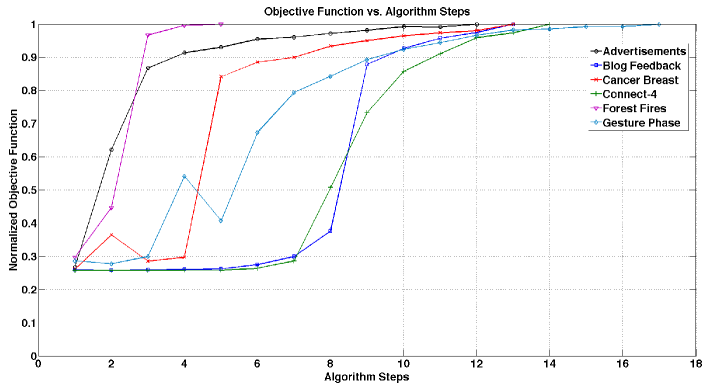

We have investigated also the ability of our algorithm to converge rapidly towards the solution, for all the datasets taken into account in this paper. Precisely, figure 7 shows the number of steps required by our algorithm to maximize the normalized objective function, i.e. the mutual information. For all the datasets taken into account, the figure shows that in steps in the average, our algorithm is able to find the optimal subset of features. Moreover, the algorithm converges toward the solution stably, with power law.

6 Conclusions

In this work, we have presented a novel algorithm to manage the optimization problem that is at the foundation of the Mutual Information feature selection methods. A peculiarity of this novel approach consists in the ability to estimate automatically the dimensions to retain. The proposed methodology is based on a Cross-Entropy approach that filters out the set of features among all those available. The numerical results obtained on standard real data sets have confirmed that our method is promising.

References

- [1] I. Jollife, Adaptive Control Processes: A Guided Tour, Princeton University Press, 1961.

- [2] J. Friedman, Regularized discriminant analysis, Journal of the American Statistical Association 84 (1989) 165–175.

- [3] L. Chen, H. Liao, M. Ko, J. Lin, G. Yu, A new LDA-based face recognition system which can solve the small sample size problem, Pattern Recognition 30 (2000) 1713–1726.

- [4] A. Rozza, G. Lombardi, E. Casiraghi, P. Campadelli, Novel Fisher Discriminant Classifiers, Elsevier, Pattern Recognition 45 (2012) 3725–3737.

- [5] G. Chandrashekar, F. Sahin, A survey on feature selection methods, Computers and Electrical Engineering 40 (1) (2014) 16 – 28.

- [6] T. Cover, J. Thomas, Elements of Information Theory, John Wiley and Sons, Inc, New York, NY, USA, 1991.

- [7] G. Brown, A new perspective for information theoretic feature selection, in: Int. Conf. on Artificial Intelligence and Statistics, Clearwater Beach, Fl, USA, 2009.

- [8] R. Kohavi, G. John, Wrappers for feature subset selection, Artificial Intelligence 97 (1-2) (1997) 273–324.

- [9] I. Guyon, An introduction to variable and feature selection, Journal of Machine Learning Research 3 (2003) 1157–1182.

- [10] G. Forman, An extensive empirical study of feature selection metrics for text classification, J. Mach. Learn. Res. 3 (2003) 1289–1305.

- [11] R. Battiti, Using mutual information for selecting features in supervised neural net learning, IEEE Transactions on Neural Networks 5 (1994) 537–550.

- [12] P. Comon, Independent component analysis, a new concept?, Signal Processing 36 (3) (1994) 287–314.

- [13] K. Torkkola, Feature extraction by non-parametric mutual information maximization, Journal of Machine Learning Research 3 (2003) 1415–1438.

- [14] D. Koller, M. Sahami, Toward optimal feature selection, in: Int. Conf. on Machine Learning, Bari, Italy, 1996.

- [15] F. Fleuret, I. Guyon, Fast binary feature selection with conditional mutual information, Journal of Machine Learning Research 5 (2004) 1531–1555.

- [16] H. Peng, F. Long, C. Ding, Feature selection based on mutual information criteria of max-dependency, max-relevance, and min-redundancy, IEEE Transactions on Pattern Analysis and Machine Intelligence 27 (8) (2005) 1226–1238.

- [17] P. E. Meyer, G. Bontempi, On the use of variable complementarity for feature selection in cancer classification, Springer Applications of Evolutionary Computing 3907 (2006) 91–102.

- [18] Y. Zheng, C. K. Kwoh, A feature subset selection method based on high-dimensional mutual information, MDPI Entropy 13 (4) (2011) 860–901.

- [19] P. M. Narendra, K. Fukunaga, Branch and bound algorithm for feature subset selection., IEEE Transactions on Computers C-26 (9) (1977) 917–922.

- [20] D. E. Goldberg, Genetic Algorithms in Search, Optimization and Machine Learning, 1st Edition, Addison-Wesley Longman Publishing Co., Inc., Boston, MA, USA, 1989.

- [21] J. Kennedy, R. Eberrhart, Particle swarm optimization, in: IEEE Int. Conf. on Neural Network, Perth, WA,USA, 1995, pp. 1942–1948.

- [22] R. McEliece, In The Theory of Information and Coding: A Mathematical Framework for Communication, Vol. Vol. 3 of Encyclopedia of Mathematics and Its Applications, Addison-Wesley Publishing Company: Reading, MA, USA, 1977.

- [23] [online][link].

- [24] R. Y. Rubinstein, D. P. Kroese, The cross-entropy method: a unified approach to combinatorial optimization, Monte-Carlo simulation and machine learning, Springer, 2004.

-

[25]

M. Lichman, UCI machine learning

repository (2013).

URL http://archive.ics.uci.edu/ml - [26] J. Kennedy, R. Eberhart, A discrete binary version of the particle swarm algorithm, in: IEEE Int. Conf. on Systems, Man and Cybernetics, Orlando, FL, USA, 1997, pp. 4104–4108.

Appendix A Derivation of Equations 12 and 13

Consider the following general maximization problem. Let be a finite set of states, and let be a real-valued performance function on . The issue is to find the maximum of over , and the corresponding state(s) at which this maximum is attained. Let us denote the maximum by thus to obtain:

| (10) |

This equation represents the associate estimation problem related to the starting optimization problem.

To find the solution through the Cross-Entropy Theory, we define a collection of indicator functions on for various thresholds . Next, let be a family of probability distribution functions (pdf) on , parameterized by a real-valued parameter (vector) . Given we associate with equation 10 the problem of estimating the following quantity:

| (11) |

where is the probability measure under which the random state has pdf , and denotes the corresponding expectation operator. The estimation problem in equation 11 is called the associated stochastic problem (ASP). To indicate how (11) is associated with (10), suppose for example that is equal to and that is the uniform density on . Note that, the way to evaluate is through its occurrence rate, hence , where denotes the number of elements in . Thus, for a natural way to estimate would be to use an estimator based on the Kulback-Leibler distance and with optimal reference parameter , as shown in the following.

The expectation operator can be written by the Lebesgue-integral as:

| (12) |

A straightforward way to estimate this integral is to use crude Monte-Carlo simulation drawing a random sample from , but this approach is inefficient because a large simulation effort is required in order to estimate accurately the expectation, i.e., with small relative error or a narrow confidence interval. An alternative, based on importance sampling, takes a random sample from an importance sampling density on , and evaluates the expectation using this new estimator:

| (13) |

It is well known (see [24]) that one of the best ways to estimate the expectation is to use the change of measure with density:

| (14) |

Note that (called optimal Importance Sampling distribution) depends on the unknown value , so this probability distribution function is hard to evaluate.

For this kind of problem the Cross-Entropy method provides an iterative method to evaluate the optimal density . In brief, the method evaluates , minimizing the Kulback-Leibler distance between the optimal densities and :

| (15) |

The minimization of the equation (15) is equivalent to the maximization of the following quantity:

| (16) |

Hence, substituting with the optimal solution in equation 14 we obtain the maximization program: