Abstract

A univariate Hawkes process is a simple point process that is self-exciting and has clustering effect. The intensity of this point process is given by the sum of a baseline intensity and another term that depends on the entire past history of the point process. Hawkes process has wide applications in finance, neuroscience, social networks, criminology, seismology, and many other fields. In this paper, we prove a functional central limit theorem for stationary Hawkes processes in the asymptotic regime where the baseline intensity is large. The limit is a non-Markovian Gaussian process with dependent increments. We use the resulting approximation to study an infinite-server queue with high-volume Hawkes traffic. We show that the queue length process can be approximated by a Gaussian process, for which we compute explicitly the covariance function and the steady-state distribution. We also extend our results to multivariate stationary Hawkes processes and establish limit theorems for infinite-server queues with multivariate Hawkes traffic.

Functional central limit theorems for stationary Hawkes processes and application to infinite–server queues

Xuefeng Gao 111Corresponding Author. Department of Systems Engineering and Engineering Management, The Chinese University of Hong Kong, Shatin, N.T. Hong Kong; xfgao@se.cuhk.edu.hk, Lingjiong Zhu 222Department of Mathematics, Florida State University, 1017 Academic Way, Tallahassee, FL-32306, United States of America; zhu@math.fsu.edu.

1 Introduction

A univariate linear Hawkes process is a simple point process whose (stochastic) intensity at time is given by

where are the occurrences of the points before time , and . See Section 2 for accurate definitions, multivariate extensions, and related properties. We use the notation to denote the number of points in the interval . When , the Hawkes process becomes a Poisson process with rate . In the literature, the parameter is called the baseline intensity, and is called the exciting function or sometimes referred to as the kernel function.

The linear Hawkes process was first introduced by A.G. Hawkes in 1971 [27, 28]. It exhibits both self–exciting (i.e., the occurrence of an event increases the probabilities of future events) and clustering properties. Hence it is very appealing in point process modeling and it has wide applications in various domains, including neuroscience [36, 47, 50], seismology [43], genome analysis [25, 49], social network [4, 12], finance (see the recent survey paper [2] and the references therein) and others.

This paper focuses on stationary Hawkes processes and their applications in specific queueing systems. A Hawkes process is stationary if its distribution does not change under time shift. See Section 2 for accurate definitions. In this paper, we develop approximations of a stationary Hawkes process with a large baseline intensity . Mathematically, under a mild assumption on the exciting function (Assumption 1), we establish a functional central limit theorem (FCLT) for a sequence of univariate stationary Hawkes processes indexed by the baseline intensity which goes to infinity (see Theorem 2). These Hawkes processes share a common fixed exciting function . The limit process turns out to be a Gaussian process which is non–Markovian unless . This limiting Gaussian process has stationary but dependent increments.

To illustrate the strength of the Gaussian approximation for the Hawkes processes, we study a specific queueing model with a stationary Hawkes traffic: an infinite–server queue with general service time distributions. The Hawkes process could be a potential traffic model especially for financial market data feeds333Market data feeds are typically composed of event messages that provide, in real time, the status of the market such as asset prices, reports of completed trades, and order activities. While some industry white paper [41] suggests that the market data traffic clearly exhibits clustering, we are not aware of academic studies or publicly available data on market data feeds. for several reasons. First, the Hawkes process naturally extends the classical Poisson process. Second, stock order flows and the occurrence of financial market events are known to exhibit clustering (in time) and self–exciting features, e.g., trades trigger other trades [2, 7, 11, 13, 30]. The standard Poisson process can not capture these features while the Hawkes process can adequately model such clustering and self–exciting behavior. Third, the Hawkes process is a highly versatile and flexible model which can exhibit a broad range of correlation structure, depending on the specification of how past events affect the occurrence of current and future events ([2]). Finally, the Hawkes process is amenable to statistical inference (see, e.g., [2, 14, 44]).

Infinite–server queues are interesting in their own right since they naturally arise in the study of many applications such as electric power consumption and insurance mathematics [3, 24]. In addition, as argued in [54], infinite–server queues often serve as useful approximations for multi–server queues which are classical models for large–scale service systems (e.g., server farms, call centers). In the financial context, such an infinite–server queue can serve as an approximate model for describing the market data feed sent from exchanges, processed by many parallel computer servers, and then delivered to consuming applications of end–users.

Since Hawkes processes are non–Markovian in general and the inter-arrival times are correlated, it is challenging to analyze the performance of an infinite-server queue with Hawkes traffic and general service time distributions, either analytically or numerically. Hence, we consider the regime that the baseline intensity of the Hawkes input is large. Such a regime could be relevant since the market data traffic is generated by many market participants and the market data volumes are huge in practice (e.g., in the range of gigabytes per second). Relying on [40], we develop heavy–traffic approximations for the performance of such an infinite–server queue fed by a univariate stationary Hawkes process with a large baseline intensity (Proposition 6). The limiting queue length process is a Gaussian process. We compute its covariance function as well as its steady–state distribution explicitly, both of which depend on the distribution of service times as well as the detailed form of the covariance density of the Hawkes traffic (Proposition 8 and Corollary 9). In the special case of exponential service time distributions, the limiting queue length process is an Ornstein-Uhlenbeck (OU) process driven by a Gaussian process. This Gaussian–driven OU process is non–Markovian in general. We illustrate through examples and numerical experiments that the Gaussian approximation for the steady–state queue length is effective.

We also extend our functional central limit theorem to multivariate stationary Hawkes processes (Theorem 12) and study infinite–server queues with multivariate Hawkes traffic and general service time distributions. Such a model can be viewed as a multi–class queueing model with correlated and mutually–exciting arrivals. We show that the limiting queue length process is a multivariate Gaussian process (Proposition 13). When the service times of each class of customers are independent exponentials, this limiting queue length process becomes a multi–dimensional Gaussian–driven OU process (Proposition 14).

To summarize, our paper is the first one that studies the large baseline intensity asymptotics for stationary Hawkes processes. Unlike the existing limit theorems for Hawkes process in the literature, our proof relies on the immigration-birth representation of the linear Hawkes processes [29], and the delicate analysis of the moments of the stationary Hawkes process. Our paper is also the first to study queues with stationary Hawkes traffic. We obtain new explicit results for the performance of infinite-server queueing systems which allows us to better understand the impact of self–exciting and mutually–exciting Hawkes traffic on the system performance.

Related Literature. Two streams of research that are closely related to our work are Hawkes processes and infinite-server queues. We now explain the difference between our study and the existing literature in these two areas.

Asymptotics of Hawkes processes. Note that most of the existing literature on limit theorems for Hawkes processes are for large–time asymptotics, where one scales both time and space. See [1, 6, 57] for large–time asymptotics of linear Hawkes processes, [38, 59] for large–time asymptotics for extensions of linear Hawkes processes, [34, 35] for the nearly unstable case where , [55] for the generalized Markovian Hawkes processes (or affine point processes), and [56] for large–time asymptotics of nonlinear Hawkes processes.

These large–time asymptotics are different from our large- asymptotics (no time-scaling is involved). We will see later, see e.g. Theorem 2, that the time-space and intensity-space scalings are not equivalent. For Poisson processes, these two scalings are equivalent and both lead to a Brownian limit. For Hawkes processes, for the time-space scaling, we obtain the Brownian limit, see e.g. [58]. On the other hand, if we consider large baseline intensity and scale down the space, we get a non-Markovian Gaussian limit (Theorem 2). The primary reason is that the Hawkes process with a baseline intensity , say is a positive integer, can be expressed as partial sums of i.i.d. copies of a Hawkes process which has baseline intensity one (see Sections 2 and 3). Thus for the intensity-space scaling we consider, the covariance structure of is still preserved in the limit, and the covariance structure of does not coincide with that of a Brownian motion since has dependent time increments, which leads to the non-Brownian Gaussian limit.

Other than the large–time asymptotics, limit theorems for non-stationary Markovian Hawkes processes with a large initial intensity have been established in our recent studies [22, 23]. Large–dimension asymptotics have been studied in [16, 10, 15], in which the authors studied the asymptotics for the multivariate Hawkes process and its extensions where the number of dimension goes to infinity, and obtained a mean–field limit.

Infinite-server queues. In the setting of infinite–server queues, our work complements the stream of research on heavy–traffic approximations of such queues, see, e.g., [17, 32, 39, 42, 45, 46, 48, 53] and the references therein. In these studies, the heavy–traffic limit of the arrival process is typically a Brownian motion or a deterministic time–changed Brownian motion. With Hawkes traffic, we obtain a non–Markovian limit but the Gaussian structure still allows us to obtain elegant formulas for transient and steady–state performance measures. From the traffic modeling perspective, we also mention that certain Poisson cluster processes have been used to model tele–traffic arrivals (see, e.g., [20, 21, 31]). The linear Hawkes processes which can be seen as Poisson cluster processes (see e.g. [2, 14]) are not covered by these studies.

Organization of this paper. The rest of the paper is organized as follows. In Section 2, we formally introduce stationary linear Hawkes processes and review some of their properties. In Section 3, we state the main result on the functional central limit theorem for univariate stationary Hawkes processes with large baseline intensity and describe the properties of the limiting Gaussian process. In Section 4, we develop heavy–traffic approximations for infinite–server queues with univariate Hawkes traffic. We also discuss in detail the special case when service times are exponentially distributed. In Section 5, we extend our results to multivariate stationary Hawkes processes and study infinite–server queues with multivariate Hawkes traffic. The proofs of all the results are collected in the Appendix.

2 Introduction to Stationary Hawkes processes

In this section, we formally introduce stationary linear Hawkes processes and review some of their properties.

2.1 Definition and stationarity condition

Let be a simple point process on , that is, a family of random variables with values in indexed by the Borel -algebra of the real line , where and is a sequence of extended real-valued random variables so that almost surely , on for every . Let . The process is called the -intensity of if for all intervals , we have

| (2.1) |

The univariate linear Hawkes process with baseline intensity and exciting function is a simple point process admitting the -intensity

| (2.2) |

Due to (2.2), the univariate Hawkes process is sometimes also called the self–exciting point process in the literature.

A commonly used nontrivial example of the exciting function is an exponential function, i.e., for , where . In this special case, the process is Markovian, and the intensity process itself is also Markovian, see e.g. [18]. The power law function , where is also a popular choice for the exciting function in the literature, see e.g. [2].

The multivariate Hawkes process extends the univariate Hawkes process to dimensions as follows. Let , where are simple point processes on with no common points, and for each , has the intensity:

| (2.3) |

where and for . Due to (2.3), the multivariate Hawkes process is sometimes also called the mutually–exciting point process in the literature.

To facilitate the presentation, we summarize below the key properties of the linear stationary Hawkes processes that will be used in the paper. Write for a function .

-

(a)

(Stationarity). For a simple point process , stationarity of means its distribution does not change under time shift. More precisely, is stationary if the process has the same distribution as the process for any , where is a shift operator defined as for every . This directly implies that a stationary Hawkes process has stationary increments, and the intensity process is a stationary process where the distribution of does not depend on Similarly, we say a multivariate point process is stationary, if has the same distribution as for any .

Under the assumption , there is a unique stationary version of the Hawkes process with the intensity (2.2), see e.g. [8]. More generally, under the assumption that the spectral radius of the matrix is strictly less than , there is a unique stationary version of the multivariate Hawkes process with the intensity (2.3), see e.g. [8].

-

(b)

(Martingality). By the definition of the intensity in (2.1), we have for any simple point process with the intensity , is a martingale. Moreover, its predictable quadratic variation is given by so that is also a martingale. We will apply this martingale property to univariate stationary Hawkes processes and the marginal processes of multivariate stationary Hawkes processes in the proofs of Theorem 2 and 12.

- (c)

-

(d)

(Covariance density and variance function). For a stationary variate Hawkes process , the covariance density matrix , where which does not depend on , is given as follows, see e.g. [27, 28]. For ,

(2.5) and for every and , where is defined in (2.4). Here is the diagonal matrix with entries ’s on the diagonal, and with slight abuse of notations, . The variance function for the stationary variate Hawkes process, is given by

(2.6) -

(e)

(Association). Intuitively, since the Hawkes process has the self- and mutually-exciting properties, there are positive correlations between counts across time intervals. To make this statement rigorous, we will use the notion of association from probability theory, see e.g. [19]. Let and be complete and separable metric spaces, with closed orders and . A map is non-decreasing if implies . An -valued random variable is associated if for each pair of bounded, Borel measurable, non-decreasing functions , we have . Let be a locally compact, separable, metric space and denote by the space of Radon measures on equipped with the vague topology with a partial ordering which is closed by declaring that if for all Borel sets . A random measure is an -valued random variable. The linear variate Hawkes process is equivalent to a marked linear Hawkes process , which is a random measure defined on the space , via , for any Borel sets of and . The random measure is infinitely divisible since the variate linear Hawkes process is a special case of the Poisson cluster process (see e.g. [14, 37]), which is infinitely divisible. Theorem 1.1. in [19] (which first appears in [9]) says any infinitely divisible random measure on is associated. The association property of Hawkes processes implies that the covariance density (2.5) is non-negative and it will also be used to show the finiteness of the moment generating function of the stationary Hawkes process in the proof of Theorem 12.

Throughout the paper, we will always assume that we are working with the stationary version of a Hawkes process. More specifically, we will make the following assumption on the exciting function of dimensional Hawkes processes which guarantees the existence of the stationary version. This assumption is satisfied in most applications of Hawkes processes, see e.g. [2, 27, 56] and the references therein.

Assumption 1.

For all , the exciting function is non-negative, locally bounded, and Riemann integrable. In addition, the spectral radius of the matrix is strictly less than .

2.2 Immigration–birth representation

In this section, we review the well–known immigration birth representation of linear Hawkes processes (see, e.g., [29, 37]) which is the key to the proof of our results.

For the univariate stationary Hawkes process with intensity dynamics (2.2), we assume that immigrants arrive according to a homogeneous Poisson process with constant rate on the real line . Each immigrant would produce children and the number of children has a Poisson distribution with mean . Conditional on the number of the children of an immigrant, the children are born independently, and each child is born at a time with a probability density function . In other words, children are born according to an inhomogeneous Poisson process with intensity . Each child would produce children according to the same laws independent of other children. All the immigrants produce children independently. The number of points of a linear Hawkes process on a time interval equals the total number of immigrants and the descendants on the interval .

Note that the immigration–birth representation holds similarly for the multivariate Hawkes process, see e.g. [37]. For a –variate Hawkes process with the intensity (2.3) for , where , we consider immigrants of types, and the type- immigrants arrive according to a homogeneous Poisson process with intensity , and each type- immigrant produce children of type according to an inhomogeneous Poisson process with intensity . Each child of type would produce children of different types according to the same laws independent of other children. All the immigrants produce children independently. The number of points on a time interval equals to the total number of immigrants and the descendants of type on the interval .

Also note that the immigration–birth representation does not require the stationarity of the Hawkes process, or the monotonicity of the exciting function, see e.g. [57].

3 FCLT for univariate stationary Hawkes processes

In this section we develop approximations for a univariate stationary Hawkes process with a large baseline intensity .

Consider a univariate stationary Hawkes process with stochastic intensity in (2.2). We write to emphasize that the baseline intensity of this Hawkes process is . Our goal is to establish a functional central limit theorem for a sequence of stationary Hawkes processes in the asymptotic regime . Note that the exciting function is fixed, i.e., this sequence of Hawkes processes shares a common exciting function with .

To facilitate the presentation, let us define

| (3.1) |

where satisfies the integral equation:

| (3.2) |

and for . The function and are just the covariance density and variance functions for the univariate stationary Hawkes process with baseline intensity , respectively. See Equations (2.5) and (2.6). Note that the covariance density is non-negative since the linear Hawkes process is associated. When , the linear Hawkes process reduces to the Poisson process with independent increments and thus . On the other hand, when , from (3.2), it is clear that . Hence, if and only if .

We now present a result on the functional central limit theorem for such univariate stationary Hawkes processes. Write as the space of càdlàg processes on that are equipped with Skorohod topology (see, e.g., Billingsley [5]), and write for convergence in distribution. Recall from (2.4) that

Theorem 2.

Under Assumption 1, we have as ,

in , where is a mean-zero almost surely continuous Gaussian process with the covariance function, for ,

| (3.3) |

The proof of this result is given in Appendix A.1.

We now briefly explain the intuition behind this result. Without loss of generality, we assume takes integer values. By the immigration–birth representation of Hawkes processes, one can deduce that for a stationary univariate Hawkes process with a baseline intensity and an exciting function , we can decompose it as the sum of i.i.d stationary Hawkes processes, each having a baseline intensity one and an exciting function . Then one expecte by central limit theorem type of arguments that will be asymptotically Gaussian when we send to infinity.

We next discuss the covariance function of in (3.3). In general, the covariance function of in (3.3) is semi-explicit and we can compute it by first numerically solving via the integral equation (3.2). In the special case when where , the covariance function of is explicit. To see this, we first deduce from (3.2) that

which yields that

| (3.4) |

Plugging this into (3.1), we find that

| (3.5) |

and for ,

In this special case, we notice that , the variance function of , is nonlinear in in general. This is very different from the case when is a Poisson process (i.e., ) where becomes a standard Brownian motion. In addition, we find from (3) that when is a single exponential function, the variance function have the following properties: is Lipschitz continuous, convex, and asymptotically linear as .

For a general exciting function we next summarize important properties of defined in (3.1) and defined in (3.2) in the following result. These properties provide us a better understanding about the variance of the limit Gaussian process .

Proposition 3.

Under Assumption 1, the following hold:

-

(a)

-

(b)

, and the variance function is convex and Lipschitz continuous on .

-

(c)

If in addition , then

where is given by

The proof of this result is given in Appendix A.2.

Part (a) of this result is known in the literature, and we include it here mainly for completeness. The results in other parts appear to be new.

Having characterized the covariance and variance functions of , we can now elaborate further properties of the Gaussian process . We summarize them in the following result. The proof is given in Appendix A.3.

Proposition 4.

Under Assumption 1, the Gaussian process in Theorem 2 has stationary increments. In addition, the Gaussian process is not Markovian unless . Furthermore, the paths of are Hölder continuous of order for every .

Remark 5.

The increments of the Gaussian process are positively correlated and dependent in general. This is clear from (3.3) since for

which is nonzero and positive.

4 Infinite–server queues with self-exciting traffic

In this section we study infinite–server queues with high-volume self-exciting traffic, i.e., the arrival process is modeled by a univariate stationary Hawkes process. We establish limit theorems for such queues in Section 4.1, characterize the limit process in Section 4.2, and discuss in detail the special case of exponential service time distributions in Section 4.3.

4.1 Limit theorems for queues with self–exciting Hawkes traffic

In this section, we follow [40] to establish the limit theorems for queues with self–exciting Hawkes traffic.

We consider a sequence of infinite-server queueing models indexed by and let . For each fixed , the customers arrive to the th system according to a stationary univariate Hawkes process with a baseline intensity and an exciting function . Hence, the average arrival rate is . Write as the number of customers in the th system at time .

We assume given an i.i.d. sequence of nonnegative random variables with a cumulative distribution function and another i.i.d. sequence of nonnegative random variables with a cumulative distribution function . Assume for simplicity. The customers initially present in the infinite–server queueing system have remaining service times ; the new arriving customers have service times All these service times, , and the arrival process are assumed to be mutually independent. Then we have (see, e.g., [40, 46])

where is the arrival time of the -th new customer.

It follows from Theorem 3 in [40] and our Theorem 2 that the following result holds. The proof is omitted.

Proposition 6.

Suppose Assumption 1 holds. Assume that for some constant and random variable

| (4.1) |

Then the sequence of processes defined by

| (4.2) |

as converges in distribution in to the process where

| (4.3) |

Here, is a Brownian bridge, is the mean-zero Gaussian process given in Theorem 2, is a mean-zero Gaussian process with covariance function given by

| (4.4) |

The random elements are mutually independent.

Remark 7.

The integral in (4.3) is defined in a pathwise sense and is understood as the result of integration by parts. See Theorem 3 in [40]. In addition, it is known in the literature (see, e.g., [40, 46]) that one can represent the Gaussian process as an integral with respect to a random field, that is,

where the Kiefer process is a two-parameter continuous centered Gaussian process on with covariance function

As is independent of the other three Gaussian processes , so for given we obtain that the limit process in Proposition 6 is Gaussian. We next discuss the properties of this Gaussian limit with a given initial condition

4.2 Properties of the Gaussian process in (4.3)

In this section, we characterize the Gaussian limit process in Proposition 6 by computing the mean, covariance function, and long-term behavior of with a given initial condition

It is clear from Proposition 6 that for each fixed the mean of is given by:

To compute the covariance of , we can obtain from Proposition 6 that for ,

| (4.5) |

By using the property of Brownian bridge, for , we have

In addition, is already given in (4.4). Hence, it suffices to compute the last term in (4.5).

Proposition 8 (Covariance function of the Gaussian process in (4.3)).

An immediate observation from this result is that the covariance density of the traffic input Hawkes process, together with the service time distributions, leads to a delicate correlation structure of the limiting scaled queue length process .

From Proposition 8, we can immediately find that given

| (4.6) |

Note that converges to 0 almost surely as . In view of (4.3) and by letting in (4.6), we get the following result about the long-term behavior of the limiting process .

Corollary 9.

As the sequence of random variables in (4.3) converges in distribution to which is a Gaussian random variable with mean zero and variance

4.3 A special case: exponential service times

In this section, we discuss in detail the special case that service times of each customer are mutually independent and exponentially distributed. Without loss of generality, we consider service time distribution with mean one.

Then we have the following result.

Proposition 10.

Suppose Assumption 1 holds. Assume (5.5) and

| (4.7) |

Then as the sequence of processes in (4.2) converges in distribution to the process with continuous sample paths in and

or equivalently,

| (4.8) |

where is the mean-zero Gaussian process given in Theorem 2, is a standard Brownian motion, and are mutually independent. In addition, the Gaussian process is non–Markovian unless .

The proof of the weak convergence in this result immediately follows from Proposition 6 and Part II of Theorem 3 in [40]. The non-Markovian property of is also evident given the non-Markovian property of in Proposition 4. We omit the proof.

Note under the assumptions in (4.7), one can readily verify from (4.2) that

| (4.9) |

In the classical case where the traffic is Poisson, i.e., , it is well known that reduces to a standard Brownian motion, and the sequence converges in distribution to the limit process where is an Ornstein–Uhlenbeck (OU) diffusion process (driven by a Brownian motion) which is Markovian. When the traffic model is a Hawkes process and the exciting function is nonzero, Equation (4.8) suggests that the limit process can be viewed as an Ornstein-Uhlenbeck (OU) process driven by the centered Gaussian process where

We explore additional properties of the process in the next section.

4.3.1 Properties of the Gaussian-driven OU process

From the results in Section 4.2, we can immediately obtain the mean, the covariance function and the long-term behavior of the Gaussian-driven OU process .

Proposition 11.

One can obtain an explicit formula for the covariance function and long-term limit of in the special case where . Recall when , we have given in (3.4). Therefore, from Proposition 11 we can compute that for :

In addition,

| (4.11) |

When is not a single exponential function, let us discuss how to compute the Laplace transform of in (4.10) in general. It is proved in Lemma 11 of [60] that if is positive, continuous and integrable, can be approximated by a sum of exponentials in both and norms, that is there exist and so that for every and in both and norms. For such a general exciting function , let us write . Thus, for any ,

where for and a given function . Thus, by taking Laplace transform on both sides of (3.2), we get

| (4.12) |

By letting , , we get

Let denote the vector with , and be the vector with and be the matrix with entries , and finally be the identity matrix. Thus, we have

| (4.13) |

which implies that provided that is invertible, which holds if for example the spectral radius of is strictly less than . In practice, if we consider , for some finite , where , and for every , then one can readily obtain and , and hence and can be easily solved. Once the values of are determined, so is the Laplace transform of given in (4.12). An example to illustrate this procedure will be provided in the next section (Example 2).

4.3.2 Gaussian approximations and numerical experiments

Note that Proposition 10 and (4.9) suggest that when the baseline intensity of the Hawkes arrival process is large, we can heuristically approximate the steady-state distribution of the number of customers in the queue as follows:

| (4.14) |

where the random variable follows a normal distribution with mean zero, and variance where is given in (4.10). A more precise statement of the approximation in (4.14) is

| (4.15) |

where , and is the probability density function of a standard normal distribution.

We now present numerical experiments to demonstrate that the Gaussian approximation in (4.15) is effective by making comparisons with simulations of the queue. We consider two examples.

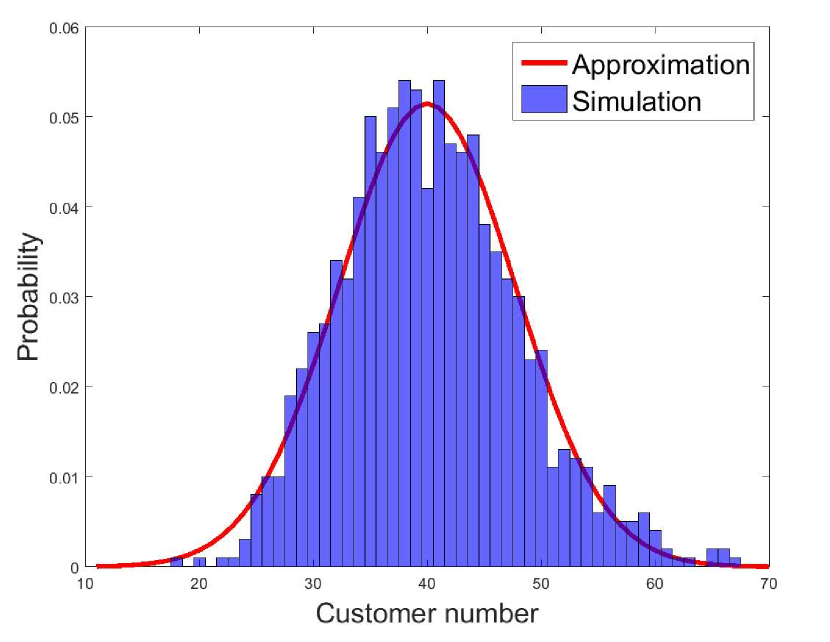

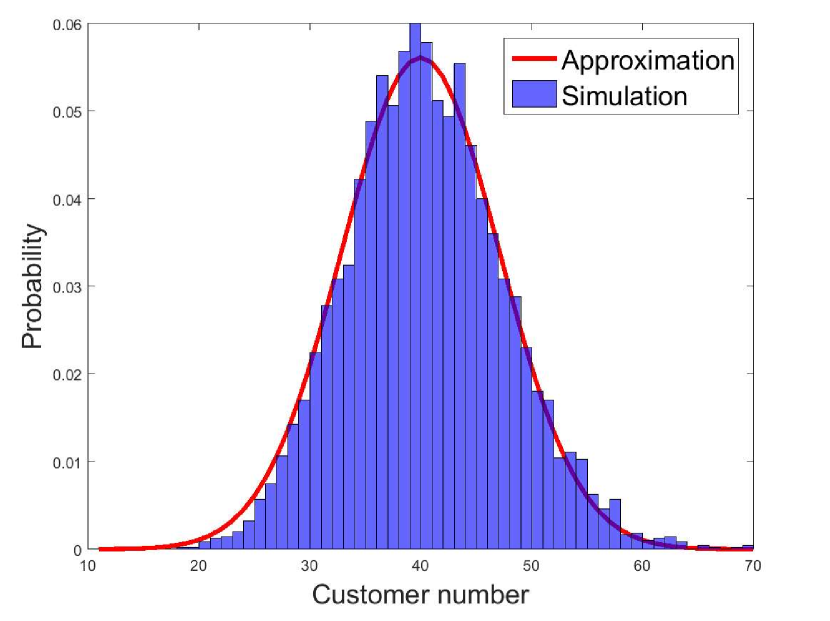

Example 1. We first consider the Hawkes input process with a single exponential function:

It is clear that . Suppose the stationary Hawkes input process has a baseline intensity . Then we can infer from (4.11) that the Gaussian random variable has mean and variance , where we have used (4.11) to find that

We now compare the Gaussian approximation in (4.15) with simulations in Figure 1. We observe that the approximation agrees with the simulation results well, even for moderately large such as twenty.

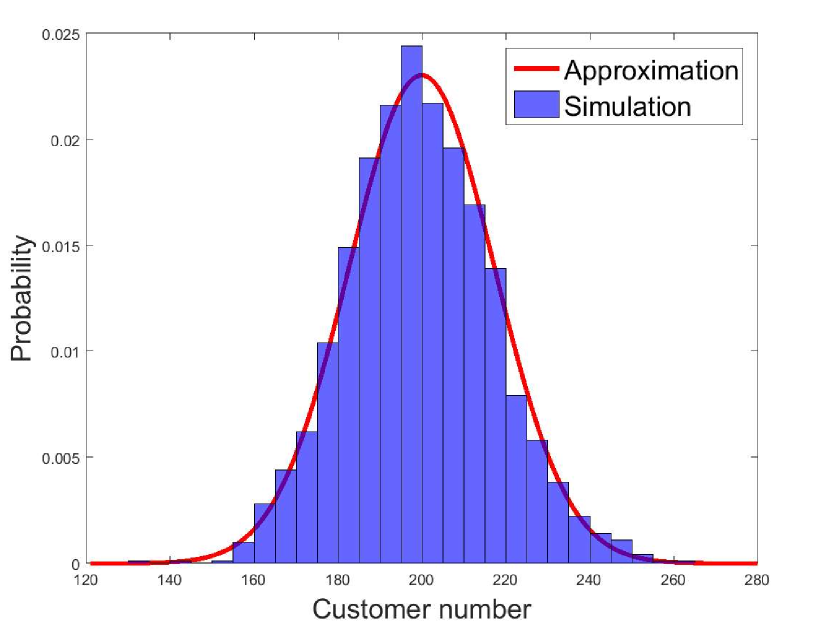

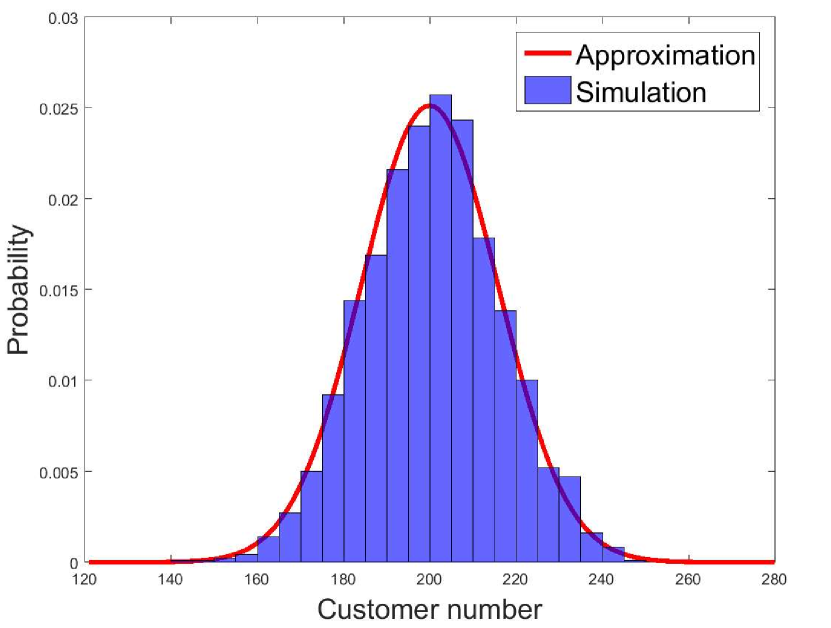

Example 2: We next consider a Hawkes input process with an exciting function which is a sum of exponentials:

It is also clear that . In this case, when the baseline intensity of the Hawkes process is , we have the Gaussian random variable has mean and variance .

To see this, we compute using (4.10) and Equations (4.12) and (4.13). Note that , and hence

| (4.16) |

One can readily verify from the expression of that

This yields

On combining (4.16) and (4.10) we deduce that when the traffic is a Hawkes process with an exciting function , then we have

We next demonstrate in Figure 2 that the Gaussian approximation in (4.15) is effective by comparing with simulations of the infinite–server queue with Hawkes input where the exciting function is . We also observe that the Gaussian approximation for the steady–state customer number agrees with the simulation results very well.

5 Infinite-server queues with mutually–exciting traffic

In this section we extend Theorem 2 to multivariate stationary Hawkes processes, and establish limit theorems for infinite–server queues with multivariate Hawkes traffic.

5.1 FCLT for multivariate stationary Hawkes processes

In this section, we establish an FCLT for multivariate stationary Hawkes processes.

We consider a -dimensional stationary Hawkes process , where has the intensity:

| (5.1) |

where for , and the exciting kernel satisfies Assumption 1. With slight abuse of notations, we still use as a scaling parameter, and study the limit of as we send . Note that for each fixed , we can obtain from (2.4) that for each

where is the average arrival rate and the vector is given by

| (5.2) |

with , and .

Similar as in the univariate case, we can infer from the immigration-birth representation of multivariate Hawkes processes, when is a positive integer, that the multivariate stationary Hawkes process can be written as the sum of i.i.d. copies of , see e.g. [37]. The covariance density of , which we still use the notation as in (2.5), is given by

| (5.3) |

and for every and . Here is the diagonal matrix with entries ’s on the diagonal, and . The variance function of , which we still use the notation as in (2.6), is given by

| (5.4) |

5.2 Limit theorem for queues with multivariate Hawkes traffic

In this section, we rely on Theorem 12 to develop approximations for infinite–server queues with high-volume multivariate stationary Hawkes traffic. Such a queueing model can be viewed as a multi-class queueing model with correlated arrivals as mutually–exciting Hawkes processes.

We first establish limit theorems for such queues. Similar as in Section 4.1, we consider a sequence of infinite-server queueing models indexed by and let . For each fixed , there are classes of customers arriving to the th system according to a stationary dimensional Hawkes process with a baseline intensity vector and an exciting kernel . That is, the arrival process of customer class is the th component of the multivariate stationary Hawkes process .

In addition, for , each customer class may have different service requirements. For each , we assume given an i.i.d. sequence of nonnegative random variables with a cumulative distribution function and another i.i.d. sequence of nonnegative random variables with a cumulative distribution function . Assume for all for simplicity. The customers of class initially present in the infinite–server queueing system have remaining service times ; the new arriving customers of class have service times All these service times, the random initial numbers of customers of each class denoted by , and the multivariate Hawkes arrival process are assumed to be mutually independent.

Denote as the number of customers of class in the th system at time , and write the vector . Given Theorem 12, we can then obtain the following result. Recall the vector given in (5.2).

Proposition 13.

Suppose Assumption 1 holds. Assume that for some vector constant and random vector

| (5.5) |

Then the sequence of dimensional processes with its th component defined by

| (5.6) |

as converges in distribution in to the process where

Here, is a Brownian bridge, is the th component of the dimensional Gaussian process given in Theorem 12, is a Kiefer process which is a two-parameter continuous centered Gaussian process on with covariance function

For all , all the random elements are mutually independent, and they are independent of .

Note that in the above result, the weak convergence of the component process to for each fixed follows directly from our Theorem 12 and Theorem 3 in [40]. However, we still need to show the joint weak convergence of the sequence as . We provide a proof in Appendix B.2.

One can also readily see that the limit process in Proposition 13 is a -dimensional Gaussian process given its initial state. The covariance function of can be computed in a similar manner as we have done in Section 4.2 in the one–dimensional case. For notational simplicity and illustration purposes, we study this limiting Gaussian process in detail for the special case of exponential service times in the following section.

5.3 An example: exponential service times

In this section, we consider the special case that class customers have the mean service requirement with , and the service time distributions are independent exponentials for all . That is,

| (5.7) |

Then we immediately obtain the following result from Proposition 13 and Part II of Theorem 3 in [40]. The proof is omitted.

Proposition 14.

Suppose Assumption 1 and (5.7) holds. Assume (5.5) with for . Then as the sequence of processes in (5.6) converges in distribution to the process with continuous sample paths in and for ,

| (5.8) |

where is the mean-zero Gaussian process given in Theorem 12, is a standard dimensional Brownian motion, and , and are mutually independent.

Proposition 14 suggests that given , the limit process can be viewed as a -dimensional Gaussian–driven OU process. We next provide a characterization of this multi–dimensional Gaussian–driven OU process by computing its covariance function and steady–state distribution explicitly.

Given , for , we write

To compute this covariance function, we note from (5.8) that for each

Therefore, we can compute that

We can compute that

and similar as in the univariate Hawkes process case,

by using the definition of in (5.4).

Hence, we conclude that for and

| (5.9) | ||||

In addition, it readily follows from (5.9) that

where is given in (5.3). As , the sequence of random vectors converges in distribution to a limiting dimensional Gaussian random vector which has mean zero and covariance

Hence, we have obtained the covariance function and the steady–state distribution of the multi–dimensional Gaussian–driven OU process in (5.8).

Acknowledgements

We are grateful to two anonymous referees, and the Associate Editor for very careful readings of the manuscript, and helpful suggestions, that greatly improve the quality of the paper. We also thank Jim Dai for helpful comments and Junfei Huang for many useful discussions. Xuefeng Gao acknowledges support from Hong Kong RGC ECS Grant 24207015 and CUHK Direct Grants for Research with project codes 4055035 and 4055054. Lingjiong Zhu is grateful to the support from NSF Grant DMS-1613164.

Appendix A Proofs of results in Section 3

This section collects the proofs of results in Section 3.

A.1 Proof of Theorem 2

Proof of Theorem 2.

The proof relies on Hahn’s theorem (see Theorem 2 in [26] or Theorem 7.2.1. in [53]), and delicate estimates of moments of stationary Hawkes processes.

For the sake of simplicity, we first consider that is a positive integer. By the immigration-birth representation, we can decompose as the sum of independent and identically distributed (i.i.d) Hawkes processes , each distributed as a stationary Hawkes process with baseline intensity (the superscript 1 in ) and the exciting function . For notational simplicity, we use for . Therefore, we have

Let . Then, are i.i.d. random elements of with (see e.g. Equation (9) in [27]) and for any (see e.g. Lemma 2 in [58]444In Lemma 2 in [58], it was proved that . By the stationarity of and the Cauchy-Schwarz inequality, for every positive integer , .).

By Hahn’s theorem, since are i.i.d., as we have

weakly in , where is a mean-zero almost surely continuous Gaussian process with the covariance function of provided that the following condition is satisfied: For every , there exist continuous nondecreasing real-valued functions and on with numbers and such that

| (A.1) |

and

| (A.2) |

for all with .

Let us prove (A.1) and (A.2). For notational simplicity, we use to stand for (equivalently, ) which records the number of points of the process in the interval . We also use to denote the intensity process of the stationary Hawkes process with baseline intensity 1. We now present a lemma which is the key to the proofs of (A.1) and (A.2). The proof is given at the end of this section.

Lemma 15.

We have

| (A.3) |

As a result, for all and , there are some constants independent of such that

| (A.4) | |||||

| (A.5) |

With Lemma 15, we are ready to prove (A.1) and (A.2). First, let us prove (A.1). It is clear from the definition of that

Using (A.4) in Lemma 15 and the fact that , we immediately obtain that (A.1) is satisfied with and

Next, let us prove (A.2). Note that

| (A.6) | ||||

Since and , we can then infer from Lemma 15 and (A.6) that (A.2) is satisfied with for some positive constant (independent of ) and .

Now we have proved Theorem 2 by assuming is a positive integer in our discussions. The same result holds when for . Note that for , by the immigration-birth representation, the process can be decomposed as the sum of two independent stationary Hawkes processes and , where the superscripts represent the baseline intensities, respectively. Hence, to show the result holds for with , it suffices to show that for any ,

in probability as . This can be easily verified since for any , for sufficiently large , we have , and

as . Here denotes a stationary Hawkes process with a baseline intensity one and an exciting function .

Finally, let us compute the covariance function of , or equivalently (from Hahn’s Theorem), the covariance function of . Since and have mean zero, we can compute that, for any ,

| (A.7) | ||||

It is clear that

In addition, we can verify that

Hence, we get

| (A.8) | ||||

The proof is therefore complete. ∎

Proof of Lemma 15.

We first prove (A.3). Using the definition of the intensity and the simple inequality , we obtain that for sufficiently small ,

| (A.9) | |||||

Note here that under Assumption 1, we know is locally bounded and Riemann integrable, hence for sufficiently small ,

| (A.10) |

Applying the Jensen’s inequality to (A.9), we get

| (A.11) | ||||

where we have used the stationarity of , (A.10) and the fact that for sufficiently small , see e.g. [58].

We next prove (A.4). We can directly compute that

| (A.12) | ||||

for some positive constant . Here, the second line follows from the martingale property, see Section 2; the third line follows from the stationarity of the intensity process and ; the fourth line follows from the Cauchy-Schwarz inequality so that ; the fifth line is due to the fact that is a stationary process; and the last inequality is due to (A.3) and the fact that .

Finally, we prove (A.5). We can directly compute that

| (A.13) | ||||

where we use the fact that is -measurable and is a martingale with predictable quadratic variation so that is also a martingale (see Section 2) and the Cauchy-Schwarz inequality so that . From here, we can further estimate that

| (A.14) | ||||

where we applied Cauchy-Schwarz inequality to the first term in the last line in (A.13) so that , and the simple inequality to the second term in the last line in (A.13). From here, we can continue that

| (A.15) | ||||

where we used Cauchy-Schwartz inequality , and the stationarity of the Hawkes processes, see Section 2.

Hence, to bound , we need to estimate . We can compute that (explanations follow below)

| (A.16) | ||||

The first inequality in (A.16) uses the inequality . The second inequality in (A.16) uses the martingality of with the predictable quadratic variation and the Burkholder-Davis-Gundy inequality, where is a constant from the Burkholder-Davis-Gundy inequality 555The Burkholder-Davis-Gundy inequality reads that for a local martingale starting at at , and , we have , for some constant depending on only and is the (predictable) quadratic variation of . As a corollary, we have . In our application, and , so that is a martingale with and the predictable quadratic variation .. The third inequality in (A.16) uses Jensen’s inequality so that

and

Finally, the last equality in (A.16) is due to stationarity of the intensity process, see Section 2.

A.2 Proof of Proposition 3

Proof of Proposition 3.

We first prove Part (b), then prove Parts (a) and (c).

To prove Part (b), we recall that

| (A.17) |

Denote . By integrating Equation (A.17) at both sides, we get

Since , there exists some so that . In addition, note that is decreasing in to as . Hence, for sufficiently large we have . This implies

Note that (See e.g. Lemma 2 in [58]) and hence

| (A.18) |

Moreover, is non-decreasing in , and for every . It implies that for every . Thus, . Hence, it follows that

| (A.19) |

To establish the second part of Part (b), we first note from the definition of in (3.1) that

The differentiability of is due to the integrability of as given in (A.19). Since is nonnegative, it follows that is non-decreasing. Hence, is convex. In addition, we note that for all . Thus is Lipschitz continuous.

We next provide a proof of Part (a) which will be useful in proving Part (c). Write for a stationary Hawkes process with baseline intensity . From the Bartlett spectrum for the stationary Hawkes process (see [27] or [14]), we know that

where . Note that

and

We can compute that

Therefore,

| (A.20) |

Notice that for any ,

and . Thus, , which is integrable. On the other hand, for every , . Therefore, by dominated convergence theorem, we obtain

We now prove Part (c). This requires a more delicate analysis of the Bartlett spectrum. Write for the complex conjugate of a complex number . We can obtain from (A.20) and that

| (A.21) | ||||

where

We claim that , i.e., is integrable on the real line. To see this, notice first that

and thus for any . Moreover, by L’Hôpital’s rule, we can check that

Since

we apply the L’Hôpital’s rule again and get

Note that the first and second derivatives of and are well defined due to the assumption and are given by

We deduce from the above that , and then Riemann-Lebesgue theorem gives

which implies that the limit of the real part is also zero:

Hence, we conclude from (A.21) that

where the fact that this constant is negative follows from the observation that for each

Hence we complete the proof of Part (c). ∎

A.3 Proof of Proposition 4

Proof of Proposition 4.

We first prove that has stationary increments. One can directly verify this fact by noting that for is a mean zero Gaussian random variable, with variance given by

Using (3.1) and (3.3), it is easily checked that , which is independent of .

We next show that the Gaussian process is not Markovian unless . To see this, recall (see, e.g., Revuz and Yor [51, p.86]) that a centered Gaussian process with covariance function is Markovian if and only if

| (A.22) |

for every . Given the covariance function of in (3.3), one can directly check that (A.22) does not hold for any nonzero exciting function .

Finally, we prove that the paths of are Hölder continuous of order for every . To see this, note that is a mean zero Gaussian random variable with variance , which implies that for ,

where and follows a standard normal distribution. By the Lipschitz property of in Proposition 3, we infer from the Kolmogorov-Chentsov theorem that the sample paths of are Hölder continuous with order less than . ∎

Appendix B Proof of results in Section 5

B.1 Proof of Theorem 12

Proof of Theorem 12.

For notational simplicity, we write for each ,

to stand for a dimensional stationary Hawkes processes where the intensity is given in (5.1) with . It should be self-evident that here the notation stands for the th process (in Appendix A we used this notation to represent a univariate Hawkes process with baseline intensity ). Let us define

| (B.1) |

and let be independent copies of where for each . We obtain from the immigration–birth representation of multivariate Hawkes processes that

| (B.2) |

where as in the proof of Theorem 2, it suffices to establish the weak convergence of the sequence for positive integer valued .

We first establish the tightness of the sequence of processes . We use the tightness criteria in [33, Chapter VI. Theorem 4.1] and verify the three conditions there. Condition (i) trivially holds. To verify Condition (ii) and (iii), it suffices to check the following two conditions: for every , there exist some positive constants so that

| (B.3) |

and

| (B.4) |

for all with , where the notation stands for the usual Euclidean norm of a vector in To see this, first notice that using Markov inequality, it is straightforward to verify that (B.3) implies Condition (ii) in [33, Chapter VI. Theorem 4.1]. In addition, following the proof of Theorem 2 in [26] (the processes considered there are real–valued, but the argument in that proof also works for -valued processes), one can immediately deduce that (B.4) implies Condition (iii) in [33, Chapter VI. Theorem 4.1].

We now prove (B.3) and (B.4). As the dimension of the multivariate Hawkes process is finite, in order to prove (B.3) and (B.4), it suffices to check that for every , there exist some positive constants so that for all with and every ,

| (B.5) |

and

| (B.6) |

We next prove (B.5) and (B.6). Similar as (A.12), we can compute that

for some positive constant , provided that .

Moreover, similar as the derivations in (A.13), (A.14) and (A.15), we have

Similar as (A.16) in the proof of Theorem 2, we have

Hence, we obtain

for some positive constant , provided that for .

It remains to prove that for , as it implies . Similar as the derivations in (A.9)–(A.11) in the proof of Theorem 2, since are locally bounded and Riemann integrable by Assumption 1, for sufficiently small , we obtain

for some positive constant Thus, it remains to show that for every , . It suffices to show that there exists some constant so that . Let us define as the expectation under which the process (with slight abuse of notations) is a multivariate Hawkes process starting from empty history, that is, . For any , is a martingale (see e.g. [52]), and thus

which implies that

| (B.7) |

Since the spectral radius of the matrix is strictly less than , we know that exists and . Thus for any fixed positive column vector , we have for every , where is the -th component of the vector . Let , where is sufficiently small so that we can find some constant that depends on such that

Hence, we deduce from (B.7) that there exists so that

In particular, for every , we have

Since the linear Hawkes process (either with empty history or the stationary version) is associated, we then deduce that for positive integer ,

Hence, by the ergodicity of the Hawkes processes with empty history where the exciting function satisfies Assumption 1, see e.g. [8], we obtain

where we recall is the expectation under which the Hawkes process is stationary. Hence, we have proved that there exists some constant so that for each .

Now we have proved the tightness of the sequence , we next show that the finite dimensional distributions of the sequence of processes converges in distribution to that of the limiting process as . To this end, we note that one can readily compute the covariance function of as in the univariate case (see Equations. (A.7)-(A.8)), and find that for ,

Hence, in view of (B.2) and (B.3), the weak convergence of the finite dimensional distributions of this sequence immediately follows from the central limit theorem for sum of i.i.d. random vectors and the Cramér-Wold device (see e.g. Section 4.3.2 in [53]).

B.2 Proof of Proposition 13

Proof of Proposition 13.

To prove Proposition 13, we rely on [40]. For notational simplicity, we prove the joint weak convergence of as for the case The general case follows similarly.

First, as in the proof of Theorem 3 in [40], we obtain that for ,

where for

Here are all independent and uniformly distributed random variables on and the service times , where . For each fixed , it was proved in [40] (see (6.1)–(6.3) there) that the following weak convergence of processes hold:

| (B.8) | |||

| (B.9) | |||

| (B.10) |

In addition, there is clearly a joint weak convergence of the left-hand sides of (B.8)–(B.10) to the right-hand sides [40]. Now, by the hypothesis, the number of customers in the system at time zero, for , as well as their respective service requirements for are mutually independent. Moreover, the arrivals of new customers and the service requirements of those new customers are independent of the initial number of customers and their service times. Hence, in order to prove the joint weak convergence of , it suffices to prove the weak convergence of as

To this end, let us define

Note that by Theorem 12, we have the sequence of processes converges in distribution to a deterministic limit process where for each As has continuous paths and the Skorohod topology relativized to the space of continuous functions coincides with the uniform topology there ([5, p.124]), we obtain that for each , as ,

Then using a similar argument as in the proof of Lemma 5.3 in [40], we can establish that for each and ,

| (B.11) |

In addition, using integration by parts, we can write , where for each , is defined by

and is continuous at points . See the proof of Lemma 3.3 in [40]. Now in Theorem 12 we have established that converges in distribution to the Gaussian process under the Skorohod topology where the limiting Gaussian process has continuous paths, it then immediately follows that

| (B.12) |

where

Furthermore, as the service processes of each class customers are independent, we deduce that the two processes and are independent for each , which further implies that and are two independent processes. By Lemma 3.1 of [40], we have in for each as . Hence, we deduce from Lemma 5.3 of [40] that

| (B.13) |

where

Then we can obtain from (B.12), (B.13) and the independence of the service processes and the arrival processes of each class of customers that

Together with (B.11) which implies that , we infer that the process converges in distribution to as . Therefore, we obtain the weak convergence of to the desired limit process . The proof is completed. ∎

References

- [1] Bacry, E., Delattre, S., Hoffmann, M., Muzy, J. F.: Scaling limits for Hawkes processes and application to financial statistics. Stochastic Processes and their Applications 123, 2475-2499 (2013)

- [2] Bacry, E., Mastromatteo, I., Muzy, J. F.: Hawkes processes in finance. Market Microstructure and Liquidity. 01, 1550005 (2015).

- [3] Blanchet, J., Chen, X., Lam, H.: Two-parameter sample path large deviations for infinite-server queues. Stochastic Systems. 4(1), pp.206-249. (2014)

- [4] Blundell, C., Beck, J., Heller, K. A.: Modelling reciprocating relationships with Hawkes processes. In Advances in Neural Information Processing Systems. 2600-2608. (2012)

- [5] Billingsley, P.: Convergence of Probability Measures, 2nd edition. Wiley–Interscience, New York. (1999)

- [6] Bordenave, C., Torrisi, G. L.: Large deviations of Poisson cluster processes. Stochastic Models, 23, 593-625. (2007)

- [7] Bowsher, C. G.: Modelling security market events in continuous time: Intensity based, multivariate point process models. Journal of Econometrics. 141(2), 876-912. (2007)

- [8] Brémaud, P., Massoulié, L.: Stability of nonlinear Hawkes processes. Ann. Probab.. 24, 1563-1588. (1996)

- [9] Burton, R., Waymire, E.: The central limit problem for infinitely divisible random measures. In : Taqqu, M., Eberlein, E. (eds.) Dependence in probability and statistics. Boston: Birkhauser. (1986)

- [10] Chevallier, J.: Mean-field limit of generalized Hawkes processes. to appear in Stochastic Processes and their Applications. (2017)

- [11] Cont, R., De Larrard, A.: Order book dynamics in liquid markets: limit theorems and diffusion approximations. Available at SSRN 1757861. (2012)

- [12] Crane, R., Sornette, D.: Robust dynamic classes revealed by measuring the response function of a social system. Proc. Nat. Acad. Sci. USA. 105, 15649. (2008)

- [13] Da Fonseca, J., Zaatour, R.: Hawkes process: Fast calibration, application to trade clustering, and diffusive limit. Journal of Futures Markets. 34(6), 548-579. (2014)

- [14] Daley, D. J., Vere-Jones, D.: An Introduction to the Theory of Point Processes, Volume I and II, 2nd edition. Springer-Verlag, New York. (2003)

- [15] Delattre, S., Fournier, N.: Statistical inference versus mean field limit for Hawkes processes. Electronic Journal of Statistics. 10(1), pp.1223-1295. (2016)

- [16] Delattre, S., Fournier, N., M. Hoffmann, M.: Hawkes processes on large networks. Annals of Applied Probability. 26, 216-261. (2016)

- [17] Eick, S.G., Massey, W.A., Whitt, W.: The physics of the queue. Operations Research. 41(4), pp.731-742. (1993)

- [18] Errais, E., Giesecke, K., Goldberg, L.: Affine point processes and portfolio credit risk. SIAM J. Financial Math. 1, 642-665. (2010)

- [19] Evans, S. N.: Association and random measures. Probability Theory and Related Fields 86, 1-19. (1990)

- [20] Fasen, V.: Modeling network traffic by a cluster Poisson input process with heavy and light-tailed file sizes. Queueing Systems. 66(4), 313-350. (2010)

- [21] Fay, G., Gonzalez-Arevalo, B., Mikosch, T., Samorodnitsky, G.: Modeling teletraffic arrivals by a Poisson cluster process. Queueing Systems. 54(2), 121-140. (2006)

- [22] Gao, X., Zhu, L.: Limit theorems for linear Markovian Hawkes processes with large initial intensity. arXiv:1512.02155. (2015)

- [23] Gao, X., Zhu, L.: Large deviations and applications for Markovian Hawkes processes with a large initial intensity. to appear in Bernoulli.

- [24] Glynn, P.W., Szechtman, R.: Rare-Event Simulation for Infinite Server Queues. Proceedings of the 2002 Winter Simulation Conference, 416-423. (2002).

- [25] Gusto, G., Schbath, S.: FADO: a statistical method to detect favored or avoided distances between occurrences of motifs using the Hawkes’ model. Statistical Applications in Genetics and Molecular Biology. 4(1). (2005)

- [26] Hahn, M.G.: Central limit theorems in D [0, 1]. Probability Theory and Related Fields, 44(2), pp.89-101. (1978)

- [27] Hawkes, A. G.: Spectra of some self-exciting and mutually exciting point processes. Biometrika 58, 83-90. (1971)

- [28] Hawkes, A.G.: Point spectra of some mutually exciting point processes. Journal of the Royal Statistical Society. Series B (Methodological). pp.438-443. (1971)

- [29] Hawkes, A. G., Oakes, D.: A cluster process representation of a self-exciting process. J. Appl. Prob. 11, 493-503. (1974)

- [30] Hewlett, P.: Clustering of order arrivals, price impact and trade path optimisation. In Workshop on Financial Modeling with Jump processes, Ecole Polytechnique. 6-8. (2006)

- [31] Hohn, N., Veitch, D., Abry, P.: Cluster processes: a natural language for network traffic. IEEE Transactions on Signal Processing. 51(8), 2229-2244. (2003)

- [32] Iglehart, D. L.: Limiting diffusion approximations for the many server queue and the repairman problem. Journal of Applied Probability. 2(2), pp.429-441. (1965)

- [33] Jacod, J., Shiryaev, A.N.: Limit theorems for stochastic processes (Vol. 288). Springer Science & Business Media. (2013)

- [34] Jaisson, T., Rosenbaum, M.: Limit theorems for nearly unstable Hawkes processes. Annals of Applied Probability. 25, 600-631. (2015)

- [35] Jaisson, T., Rosenbaum, M.: Rough fractional diffusions as scaling limits of nearly unstable heavy tailed Hawkes processes. Annals of Applied Probability. 26, 2860-2882. (2016)

- [36] Johnson, D. H.: Point process models of single-neuron discharges. Journal of computational neuroscience. 3(4), 275-299. (1996)

- [37] Jovanović, S., Hertz, J., S. Rotter.: Cumulants of Hawkes point processes. Physical Review E. 91, 042802. (2015)

- [38] Karabash, D., Zhu, L.: Limit theorems for marked Hawkes processes with application to a risk model. Stochastic Models. 31, 433-451. (2015)

- [39] Ko, Y. M., Pender, J.: Strong Approximations for Time Varying Infinite-Server Queues with Non-Renewal Arrival and Service Processes. Preprint. (2016)

- [40] Krichagina, E.V., Puhalskii, A.A.: A heavy-traffic analysis of a closed queueing system with a service center. Queueing Systems. 25(1), pp.235-280. (1997)

- [41] Low Latency market data. Corvil white paper. Available at www.cisco.com/c/dam/en_us/solutions/industries/docs/finance/corvil_Latency_mkt_data.pdf.

- [42] Lu, H., Pang, G., Mandjes, M.: A functional central limit theorem for Markov additive arrival process and its applications to queueing systems. Queueing Systems. To appear. (2016)

- [43] Ogata, Y.: Statistical models for earthquake occurrences and residual analysis for point processes. Journal of the American Statistical Association. 83(401), 9-27. (1988)

- [44] Ozaki, T.: Maximum likelihood estimation of Hawkes’ self-exciting point processes. Annals of the Institute of Statistical Mathematics,. 31(1), pp.145-155. (1979)

- [45] Pang, G., Talreja, R., Whitt, W.: Martingale proofs of many-server heavy-traffic limits for Markovian queues. Probability Surveys 4, no. 193-267. (2007)

- [46] Pang, G., Whitt, W.: Two-parameter heavy-traffic limits for infinite-server queues. Queueing Systems. 65(4), pp.325-364. (2010)

- [47] Pernice, V., Staude B., Carndanobile, S., S. Rotter, S.: How structure determines correlations in neuronal networks. PLoS Computational Biology. 85:031916. (2012)

- [48] Reed, J., Talreja, R.: Distribution-valued heavy-traffic limits for the queue. The Annals of Applied Probability. 25(3), pp.1420-1474. (2015)

- [49] Reynaud-Bouret, P., Schbath, S.: Adaptive estimation for Hawkes processes; application to genome analysis. The Annals of Statistics. 38(5), 2781-2822. (2010)

- [50] Reynaud-Bouret, P., Rivoirard, V., Tuleau-Malot, C.: Inference of functional connectivity in neurosciences via Hawkes processes. In 1st IEEE Global Conference on Signal and Information Processing. (2013)

- [51] Revuz, D., Yor, M.: Continuous Martingales and Brownian Motion. Springer, 3rd Edition. (1998)

- [52] Sokol, A., Hansen, N. R.: Exponential martingales and changes of measure for counting processes. Stochastic Analysis and Applications. 33, 823-843. (2015)

- [53] Whitt, W.: Stochastic-process limits: an introduction to stochastic-process limits and their application to queues. Springer Science and Business Media. (2002)

- [54] Whitt, W.: The infinite-server queueing model: the center of the many-server Queueing Universe (i.e., More Relevant Than It Might Seem), http://www.columbia.edu/~ww2040/8100S12/ISqueue021412.pdf (2012)

- [55] Zhang, X., Blanchet, J., Giesecke, K., Glynn, P. W.: Affine point processes: Approximation and efficient simulation. Mathematics of Operations Research. 40, 797-819. (2015)

- [56] Zhu, L.: Nonlinear Hawkes Processes. PhD thesis, New York University. (2013)

- [57] Zhu, L.: Moderate deviations for Hawkes processes. Statistics & Probability Letters. 83, 885-890. (2013)

- [58] Zhu, L.: Central limit theorem for nonlinear Hawkes processes. Journal of Applied Probability. 50 760-771. (2013)

- [59] Zhu, L.: Limit theorems for a Cox-Ingersoll-Ross process with Hawkes jumps. Journal of Applied Probability. 51, 699-712. (2014)

- [60] Zhu, L.: Large deviations for Markovian nonlinear Hawkes Processes. Annals of Applied Probability. 25, 548-581. (2015)