Dimension Reduction in Statistical Estimation of Partially Observed Multiscale Processes

Abstract

We consider partially observed multiscale diffusion models that are specified up to an unknown vector parameter. We establish for a very general class of test functions that the filter of the original model converges to a filter of reduced dimension. Then, this result is used to justify statistical estimation for the unknown parameters of interest based on the model of reduced dimension but using the original available data. This allows to learn the unknown parameters of interest while working in lower dimensions, as opposed to working with the original high dimensional system. Simulation studies support and illustrate the theoretical results.

Keywords. data assimilation, filtering, parameter estimation, homogenization, multiscale diffusions, dimension reduction.

Subject classifications. 93E10 93E11 93C70 62M07 62M86

1 Introduction

This paper considers statistical inference for a general filtering problem with multiple time scales. On a probability space with , for positive integers we consider the -dimensional process , which satisfies a system of stochastic differential equations (SDEs) with ,

| (1) |

where , and are (unobserved) independent Wiener processes in , and , respectively.

One possible interpretation in the context of financial applications, is that the vector is part of a continuous stream of financial data, with the hidden processes and being factors in a stochastic model, see for example [Fouque et al., 2011]. A different possible interpretation is that is the signal of brain activity during a seizure, as in [Jirsa et al., 2014] where multiscale dynamical systems are exploited as models for seizure dynamics. Other applications include multiscale modeling in oceanography and climate modeling, see for example [Majda et al., 2008].

Initially, the model in (1) is left unspecified, and it is with the arrival of data that we can learn the parameter value . We let denote the -algebra generated by the data, , and a primary goal is to compute the maximum likelihood estimator (MLE). Given , we denote the log-likelihood function as , which we maximize to obtain the estimator

In financial applications for example and in particular in high-frequency trading, market and limit orders need to be executed at exact moments in time with accuracy that is of the order of nano seconds. Hence, an estimate such as the MLE may be very accurate, but it may also require computing time that is too long for the purposes of trading. In general, it is well known that standard Monte-Carlo particle filters can be quite slow even without the effect of multiple scales. However, in the small- limit there is a significant reduction in dimension because the process gets ‘averaged out’ by the ergodic theory, and this allows filtering for and inference for to have a faster algorithm.

The novel contribution of this paper is at two levels. At the first level, we prove that the nonlinear filter for (1) converges, for any parameter value of and under the measure parameterized by the true parameter value, with the limit being a filter of reduced dimension. We prove this result for test functions that can depend on both the slow and fast unknown components, and ; the test functions may be unbounded but we do impose moments bounds. This result extends previous works of [Imkeller et al., 2013] and [Papanicolaou and Spiliopoulos, 2014]. At the second level, we use the filters convergence result to prove that the MLE based on the model of reduced dimension produces both consistent and asymptotically normal estimators, and we identify the limiting variance of the estimator. We apply our methodology to examples where the reduction procedure allows to use classical Kalman-filter type of methods for a problem that is highly nonlinear without the small- asymptotics. Our examples demonstrate how statistical inference for a highly nonlinear problem is reduced to statistical inference for a problem that is both linear and of reduced dimension, and hence is significantly less demanding from a computational standpoint. Computations of filters in problems with nonlinearity in the reduced system are considerably more complicated to implement and usually require particle filers; we refer the reader to [Givon et al., 2009, Papavasiliou, 2007] for some related results in the multiscale setting. Another implementation issue is model learning/estimation, which is sometimes done with an expectation maximization (EM) algorithm (see [Elliott, 1993]). The results in this paper are directly applicable to learning of parametric models if the multiscale framework applies; the model is parameterized by and an MLE can be obtained using the reduced model as opposed to the original model.

The rest of the paper is organized as follows. In Section 2 we formulate the problem of interest in specific terms and present some preliminary well-known results that are useful throughout. In Section 3 we present the filtering equations of the original problem and we derive the filters associated to the problem of reduced dimensions. In Section 4 we present our first main result on filter convergence which is the main justification for doing inference using the original available data but based on the model of reduced dimension. In Section 5 we present our main results on parameter estimation. In particular, we prove that under appropriate conditions, the MLE for the problem of reduced dimension is both consistent and asymptotically normal as . In Section 6 we consider a few examples to illustrate and supplement the theoretical results for which classical Kalman filter techniques can be used. Simulation data are presented to support the theoretical claims.

2 Problem formulation and preliminary results

Let be an unknown parameter of interest which is to be estimated from data generated by (1). Assuming that we observe only the process, we develop a consistent and asymptotically normal MLE for . We consider the case , in which case is the fast component and is the slow component. We reduce the high dimensionality of the problem by looking at the limit and exploiting the statistical properties of the MLE based on the reduced likelihood.

For the model given in (1), we shall write and for the infinitesimal generators of the fast process, , and the process , respectively. Namely,

| (2) |

Next we pose the main condition of this paper on the growth and regularity of the coefficients of (1). Such conditions guarantee that (1) has a well defined strong solution, that the fast component is ergodic and that the slow component has a well-defined homogenization limit as in the appropriate sense. Assumptions to guarantee these properties are given by [Pardoux and Veretennikov, 2001] for homogenization and Chapter 3 of [Bain and Crisan, 2009] for filtering, and are stated as follows:

Condition 2.1.

-

i).

For ergodicity purposes we shall assume the recurrence condition

Under this assumption the Lyapunov-type condition for existence of an invariant measure associated to the fast dynamics of Hasminskii [Hasminskii, 1980] is satisfied.

-

ii).

To guarantee uniqueness of the invariant measure for , we assume that is non-degenerate uniformly in , i.e., there exists such that for all

-

iii).

The functions and are with , uniformly in . Namely, uniformly in , they have two bounded derivatives in and , with all partial derivatives being Hölder continuous, with exponent , with respect to , uniformly in .

-

iv).

We assume that and that there exist and such that

-

v).

For every there exists a constant such that for all and , the diffusion matrix satisfies

Moreover, there exists and such that

-

vi).

is bounded and globally Lipschitz in uniformly in .

-

vii).

The functions are Lipschitz continuous in and is bounded open set.

Under this assumption and non-degeneracy of the diffusion coefficient , for fixed with the process has a unique invariant measure which we shall denote by . For a given function , define its averaged version as

It is a well known result that converges in distribution in to the process (e.g. [Bensoussan et al., 1978, Pardoux and Veretennikov, 2003]), where

| (3) |

and where

| (4) |

Actually, due to the fact that the observation process has constant diffusion, Condition 2.1 and the ergodic theorem guarantee that a stronger result holds for any , i.e., for every

| (5) |

3 Filtering equations

The data is contained in the filtration

which is right continuous and contains all negligible sets. For any , we define a new measure on via the relationship

| (6) |

Under the proper assumptions is an exponential martingale and thus the probability measures and are absolutely continuous with respect to each other, and the distribution of is the same under both and . Furthermore, the process is a -Brownian motion and is independent of .

Next, for such that , we define the measure valued process acting on as

| (7) |

a process which, for is well-known to be the unique solution (see [Rozovsky, 1991]) to the following equation:

| (8) |

Equation (8) is the Zakai equation for nonlinear filtering. Furthermore, is actually an unnormalized probability measure which yields the normalized posterior expectations via the Kalianpour-Striebel formula,

| (9) |

If then we have the innovations process,

The process is a -Brownian motion under the filtration generated by the observed process, but will only be observable as Brownian motion if is equal to the true parameter value. For a suitable test function , the innovation process is used in the nonlinear Kushner-Stratonovich equation to describe the evolution of ,

| (10) |

Let us next consider the filtering equations of the approximating problem that is of reduced dimension. Consider the ‘averaged’ exponentials

| (11) | ||||

| (12) |

For , we define new posterior measures and which satisfy the stochastic evolution equations

| (13) | |||||

| (14) |

It is straightforward to verify with Itô’s lemma that the ‘average’ Zakai equations (13) and (14) have solutions

| (15) | |||||

| (16) |

where is a right continuous algebra and contains all negligible sets. We define the averaged filters as follows: and . It is easy to see that .

We conclude this section by mentioning that, under , equation (9) defines a measure-valued process , the conditional distribution, by the formula

Similarly, we define the probability measure-valued processes and by

The measure-valued process especially, will become handy in proving the consistency and asymptotic normality of the MLE based on the reduced estimator.

4 Convergence of the filters

Consider and define the following class of test functions

Then, we have the following result which is a generalization of the results of [Imkeller et al., 2013] and [Papanicolaou and Spiliopoulos, 2014].

Theorem 1.

Assume Conditions 2.1. For any , the following hold uniformly in

-

i).

Let . Then, for every

-

ii).

Assume that there is such that . Then, converges in -mean-square to , i.e.,

Additionally, we also have

For and for the case this is proven in [Imkeller et al., 2013]. Also, for the case and , i.e., when the model does not include the hidden slow process , Theorem 1 is proven in [Papanicolaou and Spiliopoulos, 2014]. Hence, Theorem 1 extends the results of [Imkeller et al., 2013, Papanicolaou and Spiliopoulos, 2014] to the case and under parameter mismatch. We emphasize here that since we are interested in the parameter estimation, we are naturally interested in making sure that the filters converge for any parameter value under the measure parameterized by the true parameter value. The proof of this theorem is in Appendix A.

5 On statistical inference based on reduced likelihood function

Theorem 1 suggests that for parameter estimation, we can approximate the conditional log-likelihood

| (17) |

by the ‘reduced’ log-likelihood

| (18) |

Note that by Lemma 3.29 in [Bain and Crisan, 2009] we have

| (19) |

The following condition is about regularity of as a function of .

Condition 5.1.

There are constants , and , such that for any ,

i.e., is Hölder continuous uniformly in .

Allowing arbitrary initial conditions, the set of processes , and are Markov-Feller processes in , and . Let , and be the corresponding transition functions. In order to have enough ergodicity of the averaged problem as we make the following assumption, see for example [Kushner, 1990]. The examples that will be considered in Section 6 satisfy Condition 5.2.

Condition 5.2.

There is a unique invariant measure for the transition function . In addition the set is tight and .

We also need the following identifiability condition.

Condition 5.3.

We assume that for any , any , and for every , one has

Let us define

| (20) |

Since we have assumed that is bounded, we get that with probability . We then have the following theorem:

Theorem 2.

Proof.

Under , we recall that the innovations process

is a -Brownian motion under the filtration generated from the observed process. Hence, under we have

where denotes the inner product over the coordinates in . Then, we have

| (21) |

where we used Condition 5.1. The constant might change from line to line, but we do not indicate this in the notation. By Theorem 1, we have that

| (22) |

Theorem 1, (21) and (22) imply by Theorem 12.3 in [Billingsley, 1968] that we have convergence in distribution of the process to that of in the uniform metric, where

| (23) |

Hence, similarly to the proof of Proposition 1.32 in page 61 of [Kutoyants, 2004], we have

At the same time for any we have

for some constant that does not depend on . Thus, we have in probability that

Let us define

and recalling Condition 5.2 we get that there is such that

Hence, we obtain

| (24) |

where the last computation used the identifiability Condition 5.3. With this, we conclude the proof of the theorem. ∎

Let us study next asymptotic normality of the maximum likelihood estimator that is based on the reduced likelihood function. We have that the maximizer will be solution to the equation for . Thus, the maximizer of that equation will satisfy the equation

| (25) |

We mention here that (20) and (25) are not equivalent; (20) contains all local minima and local maxima of which may be more than one. Also equation (25) may not even have a solution in with positive probability. For example, letting be a solution to (25) and assuming , then

Next we study asymptotic normality of the MLE corresponding to the reduced log-likelihood. We make the following assumption.

Condition 5.4.

There exists a strictly positive definite matrix such that we have in under the measure

| (26) |

It is clear that in the case that Condition 5.4 is satisfied with constant matrix . In Section 6 a more involved example will be examined where things can be also computed explicitly in closed form. Actually, is nothing else but the Fisher information matrix. By Theorem 2, based on smoothness of as a function of and under Condition 5.4, asymptotic normality of the MLE corresponding to the reduced log-likelihood holds. To be precise, we have the following theorem.

Theorem 3.

Proof.

We write for notational convenience. Based on (25) and for , we write for some such that

After some term rearrangement, we obtain

and by taking , ergodcity and Theorem 1 guarantee that

| (28) |

The latter statement and Condition 5.4 guarantee us that in -probability as first and then

| (29) |

For notational convenience, let us define the random matrix

Since under , the innovations process

is a -Brownian motion, for the stochastic integral we notice:

Since , Theorem 2 implies that

and hence by the almost sure continuity of as a function of and Condition 5.4, we obtain that in probability as and then

Then, Proposition 1.21 in [Kutoyants, 2004] and Slutsky’s theorem imply that in distribution, first as and then as ,

| (30) |

6 Examples

In this section we consider numerically several examples in order to illustrate the results of this paper. Even though the theory of this paper has been developed under the assumption that is bounded, the numerical results of this section indicate that there is some degree of flexibility to this assumption and that the results should be broader applicable. Let be a finite-dimensional parameter and consider the system of equations

| (31) |

where and , , and take values in . Without loss of generality and for presentation purposes the theory of the paper was developed for , but as we shall see here the same results hold with as long as is non-degenerate.

Let us further assume that we know the invariant measure for and that it is given by . Then, we know that the limit of (31) in probability as is

| (32) |

It is relatively easy to see that the diffusion coefficient can be viewed as a scaling factor. Under , the process defined by the equation

is a -Brownian motion under the filtration generated from the observed process. The maximizer satisfies

and the Fisher information turns out to be

The limiting system (32) uses the well-known Kalman-Bucy filter. The inference problem for the limiting linear system (32) was studied in [Kutoyants, 2004]. In [Kutoyants, 2004], the author develops MLE estimators for based on (32), i.e. using as data . However, the difference of our setup with the rest of the literature is that we want to estimate based on observations , which come from the multiscale model (31) and not from the limit model (32). Of course, the limit problem is used in order to derive properties of the estimators, but the actual inference is done based on observations from the multiscale model.

Let us write , . Notice that in the notation of Section 2 we have and . Let us compute the Fisher information matrix for this model and derive the conditions under which is strictly positive and the model is identifiable. Let us first denote . It is known that satisfies the equation

| (33) |

where solves the Ricatti equation

| (34) |

Next let us define

It is easy to see that if , then for all , which implies that is a stationary solution to (34). If on the other hand then converges exponentially fast to , see Section 3.1.1 of [Kutoyants, 2004]. Hence, in order to simplify things, let us assume that (33) and (34) are in the stationary regime. In this case, if the initial distribution of is then for all . In this case will satisfy the equation

| (35) |

Now notice that if (i.e., the true parameter value), then defined by is a Brownian motion. In the general case satisfies the averaged linear SDE (35), so when we have

from which it is clear that is Gaussian with invariant law .

Next, considering the derivative of with respect to , at we find that satisfies the SDE

| (36) |

and thus we obtain

| (37) |

from which Fubini’s theorem gives

| (38) |

Hence, by direct computation using (38) we can compute the asymptotic variance of the MLE. In particular, we obtain that in probability

| (39) |

Let us assume now that

Condition 6.1.

For any compact and for any

-

•

,

-

•

.

It is then proven in a related case in Section 3.1.1 of [Kutoyants, 2004], that in the specific example Condition 6.1 implies essentially Condition 5.3, i.e., we have identifiability of the model, and that the asymptotic variance is strictly positive, i.e. .

Let us next present some simulation studies based on the model problem (31). We consider three different examples. The examples lack the boundedness of assumption on indicating the broader applicability of the theoretical results of this paper.

6.1 Simulation Example 1

Let the processes be scalars , and consider the following example of the system in (31):

| (40) |

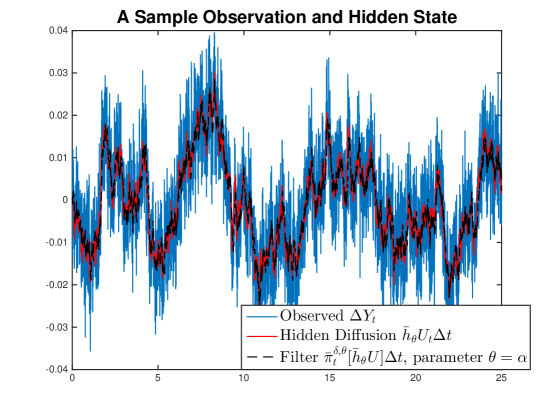

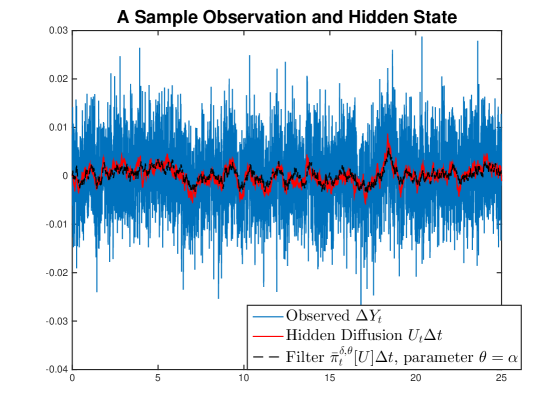

A key feature of this example is that the process behaves like a multiplicative noise factor. Figure 1 shows a realization of the system for a parameterization having , , , along with a true and discrete time step .

In this case the invariant measure of the process with is that corresponding to . Notice also that we can compute the Fisher information from (39) in closed form and obtain

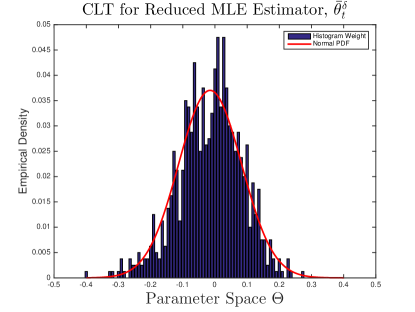

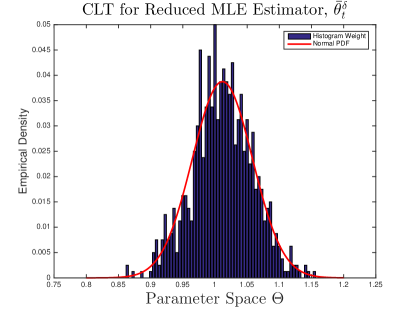

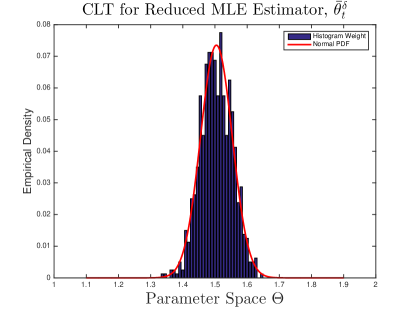

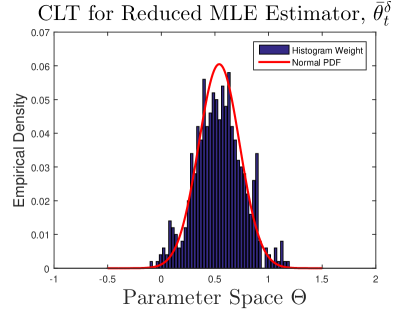

Table 1 presents the standard error for the empirical error for estimator alongside the predicted error from the Fisher information. The table shows a comparison for different values of the true parameter.

| Statistics for different values of the true parameter for . | |||

|---|---|---|---|

| estimator | empirical std-err. | theoretical std.err | |

| 0 | -0.0170 | 0.0982 | 0.0900 |

| 1 | 0.9844 | 0.0618 | 0.0542 |

| 1.5 | 1.4591 | 0.0503 | 0.0422 |

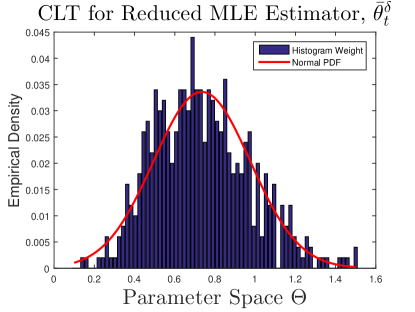

In Figure 2 we present the histograms for the three different cases of true value of the parameter, together with the fitted theoretical normal curve as this is given by Theorem 3.

|

|

|

|

6.2 Simulation Example 2

Let the processes be scalars , and consider the following example of the system in (31):

| (41) |

A key feature of this example is that the process affects the mean reversion rate of the process. Figure 3 shows a realization of the system for a parameterization having , , , along with a true and discrete time step .

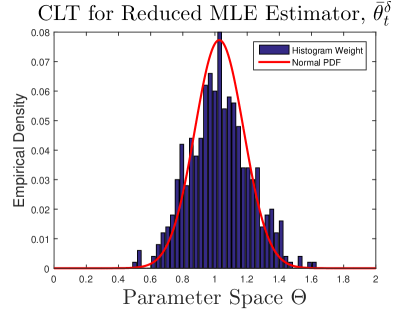

As in the case of Example 1, the invariant measure of the process with is that corresponding to . Notice also that we can compute the Fisher information from (39) in closed form and obtain

| Statistics for different values of the true parameter for . | |||

|---|---|---|---|

| estimator | empirical std-err. | theoretical std.err | |

| 0.5 | 0.5396 | 0.2385 | 0.2303 |

| 1 | 1.0268 | 0.1943 | 0.1917 |

| 1.5 | 1.5346 | 0.1815 | 0.1734 |

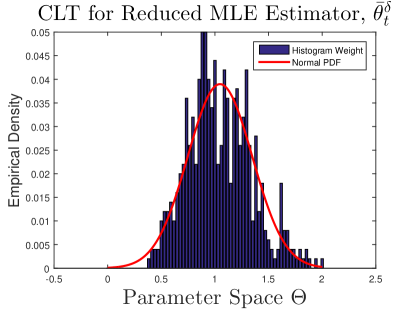

Table 2 shows the estimator’s standard deviation and the theoretical prediction for various values of the true parameter. In Figure 4 we present the histograms for the three different cases of true value of the parameter, together with the fitted theoretical normal curve as this is given by Theorem 3.

|

|

|

|

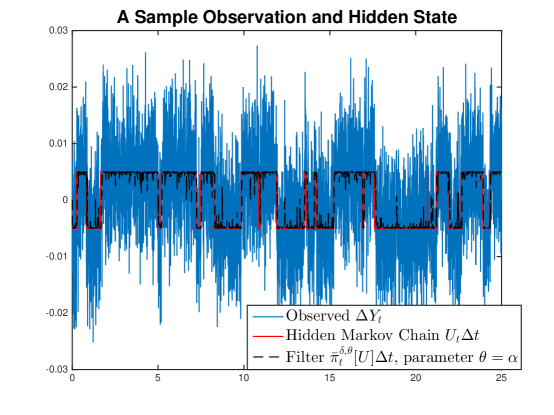

6.3 Simulation Example 3

Let the processes be scalars , and consider the following system:

| (42) |

where is a continuous time Markov chain taking values in with transition intensity , that is

This example is different from the system in (31) because the process is not a diffusion; it is comparable to the model considered in [Park et al., 2011]. Indeed, is a discrete space Markov chain and not a continuous diffusion, and so the theory of this paper does not apply, but we conjecture that things can be worked out to find analogous results. Figure 5 shows a realization and the filter for this example.

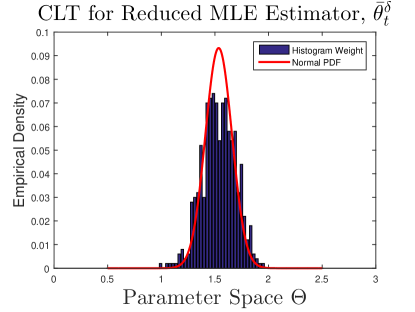

Table 3 shows the estimator’s standard deviation and the theoretical prediction for various values of the true parameter, but in this case we have no close-form expression for the Fisher information, so instead we have calculated it numerically.

| Statistics for different values of the true parameter for . | |||

|---|---|---|---|

| estimator | empirical std-err. | numerically calculated std.err | |

| 0.7 | 0.7349 | 0.2305 | 0.1917 |

| 1 | 1.0469 | 0.2697 | 0.2253 |

| 1.8 | 1.8990 | 0.3968 | 0.3058 |

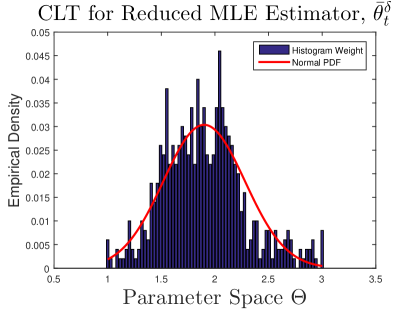

Then, in Figures 6 we present the histograms for the three different cases of true value of the parameter, together with the fitted empirical normal curve. Since, out theory does not cover this case, we cannot provide the theoretical variance of the estimator. However, as the numerical simulations indicate, a central limit theorem is expected to hold.

|

|

|

|

Appendix A Proof of Theorem 1

Versions of Theorem 1 in simpler settings have appeared in the literature in [Imkeller et al., 2013, Park et al., 2008, Park et al., 2011, Park et al., 2010]. The first main difference that Theorem 1 has when compared to the previous works is that under the measure parameterized by the true parameter value (i.e. the measure under which the observations are made) the filters will converge for any parameter value. Moreover, the second main difference is that we need to prove that the convergence of the filters is for test functions in the space the space , whereas the results in [Imkeller et al., 2013] use bounded and smooth test functions that depend only on the slow motion .

Lemma 4.

Assume Condition 2.1. Let us consider a copy of , which has the same law as , but which is independent of . Then, we have

and

Proof.

We will only prove the first statement as the proof of the second statement is the same. The convexity inequality is used to obtain

where we have defined the process

It remains to show that this term goes to zero. By the dominated convergence theorem and the independence of pairs and , the ergodic theory applies to the joint process , and in particular we see that the limit of is

This proves convergence in . Convergence in follows again from dominated convergence theorem, since , concluding the proof of the lemma. ∎

Lemma 5.

Let us consider bounded and assume Condition 2.1. For any , we have uniformly in

where defined as .

Proof.

Let us consider an independent copy of , which has the same law as , but which is independent of . We have

| (43) |

In the 2nd to last line of the above display, the term goes to zero by Lemma 4,

and the term in the last line of the display (43) goes to zero as follows,

where can be arbitrarily small. The limit is taken as , with the conditional expectation being handled in the following way:

The last convergence is due to the fact that as for any because of the ergodicity implied by Condition 2.1. Moreover, owing to Condition 2.1’s assumptions on

as by dominated convergence theorem. Hence, the remaining term is arbitrarily small, and we conclude that all terms converge to zero with . ∎

Lemma 6 (Lemma 6.7 in [Imkeller et al., 2013]).

Given that is bounded, then for any we have that

Lemma 7.

Proof.

Let us consider an independent copy of , which has the same law as , but which is independent of . We have

The first term of the last display goes to zero by Lemma 5. For the second term we have

| (44) |

The convergence in the last term is due to Lemma 4 proceeding as in the proof of Lemma 5. Then, we have convergence in probability, as for all .

Next, we notice that for such that and

where boundedness of was used. By combining Lemma 5 and (44) we get that

| (45) |

In addition, we have

| (46) |

Similarly, we can also obtain . Putting these statements together we obtain that

| (47) |

Then, by Cauchy-Schwartz inequality, we have

which goes to zero as by Lemma 6 and by (47). The third line, i.e.,

follows because both and are functionals of (and no other random variable), and is a Brownian motion under both measures and .

∎

Before moving on we should clarify the last step in the proof to Lemma 7. It should be made clear that is only observed to be Brownian motion when denotes the parameter value under the measure . In the proof we are always handling underneath an unconditional expectation operator , which is actually an expectation conditional on the ground truth of the true parameter value being . This notation can be made more explicitly in the following way: for any function of the path ,

where is a Brownian motion. Hence, we are able to say

Now the proof of Theorem 1 follows:

Proof of Theorem 1.

Let us prove just the second part of the theorem because the first part follows from a Chebyshev inequality and Lemma 5. We prove it first for . Then, we prove under the assumption that there exists such that . So, let us assume that . We start the proof by proving first that

Letting , Lemma 5 implies convergence in probability,

Now consider any , and again using a Cauchy-Schwartz inequality,

| (48) |

where finiteness of follows from Lemma 6, and follows as (47). This proves convergence in , and convergence in follows from dominated convergence because the test function was assumed bounded so that . This completes the proof for .

Let us complete the proof by assuming that there exists an such that . For , define

and set . Analogously define

Since is bounded, we already know that . So, it is enough to prove that

and

Both of these statements follow from the observation: for such that we have

and in particular, letting , so that and , then taking the following similar set of steps as in equation (48) we have

The equality in the fifth line above, i.e.,

follows because is a functional of (and no other random variable), and is a Brownian motion under both measures and .

The same limit can be shown for , but with and used instead. Due to ergodicity, the proof of

follows similarly and thus omitted. This concludes the proof of the theorem. ∎

References

- [Bain and Crisan, 2009] Bain, A. and Crisan, D. (2009). Fundamentals of Stochastic Filtering. Springer, New York, NY.

- [Bensoussan et al., 1978] Bensoussan, A., Lions, J., and Papanicolaou, G. (1978). Asymptotic Analysis for Periodic Structures, volume 5 of Studies in Mathematics and its Applications. North-Holland Publishing Co., Amsterdam.

- [Billingsley, 1968] Billingsley, P. (1968). Convergence of Probability Measures. New York, J. Willey.

- [Elliott, 1993] Elliott, R.J. (1993). New Finite-Dimensional Filters and Smoothers for Noisily Observed Markov Chains. IEEE Transactions on Information Theory, 39(1):265–271.

- [Fouque et al., 2011] Fouque, J.-P., Papanicolaou, G., Sircar, R., and Solna, K. (2011). Multiscale stochastic volatility for equity, interest rate, and credit derivatives, Cambridge University press, Cambridge, UK.

- [Givon et al., 2009] Givon, G., Stinis, P., and Weare, J. (2009). Variance reduction for particle filters of systems with time scale separation. IEEE Transactions on Signal Processing, 57(2):424–435.

- [Hasminskii, 1980] Hasminskii, R. (1980). Stochastic Stability of Differential Equations. Sijthoff and Noorhoff.

- [Imkeller et al., 2013] Imkeller, P., Namachchivaya, N. S., Perkowski, N., and Yeong, H. C. (2013). Dimensional reduction in nonlinear filtering: a homogenization approach. Annals of Applied Probability, 23(6):2290–2326.

- [Jirsa et al., 2014] Jirsa, V. K., Stacey, W. C., Quilichini, P. P., Ivanova, A. I., and Bernard, C. (2014). On the nature of seizure dynamics. Brain, 137(8):2210–2230.

- [Kushner, 1990] Kushner, H. J. (1990). Weak Convergence Methods and Singularly Perturbed Stochastic Control and Filtering Problems. Birkhäuser, Boston-Basel-Berlin.

- [Kutoyants, 2004] Kutoyants, Y. (2004). Statistical Inference for Ergodic Diffusion Processes. Springer, London.

- [Majda et al., 2008] Majda, A. J., Franzke, C., and Khouider, B. (2008). An applied mathematics perspective on stochastic modelling for climate. Philosophical Transactions of the Royal Society A, 366(1875):2429–2455.

- [Papanicolaou and Spiliopoulos, 2014] Papanicolaou, A. and Spiliopoulos, K. (2014). Filtering the maximum likelihood for multiscale problems. Siam journal on Multiscale Modeling and Simulation, 12(3):1193–1229.

- [Papavasiliou, 2007] Papavasiliou, A. (2007). Particle flters for multiscale diffusions. ESAIM Proceedings, 19:108–114.

- [Pardoux and Veretennikov, 2001] Pardoux, E. and Veretennikov, A. (2001). On Poisson equation and diffusion approximation i. Annals of Probability, 29(3):1061–1085.

- [Pardoux and Veretennikov, 2003] Pardoux, E. and Veretennikov, A. (2003). On Poisson equation and diffusion approximation ii. Annals of Probability, 31(3):1066–1092.

- [Park et al., 2011] Park, J., Rozovsky, B., and Sowers, R. (2011). Efficient nonlinear filtering of a singularly perturbed stochastic hybrid system. LMS J. Computational Mathematics, 14:254–270.

- [Park et al., 2008] Park, J., Sowers, R., and Namachchivaya, N. S. (2008). A problem in stochastic averaging of nonlinear filters. Stochastics and Dynamics, 8:543–560.

- [Park et al., 2010] Park, J., Sowers, R., and Namachchivaya, N. S. (2010). Dimensional reduction in nonlinear filtering. Nonlinearity, 23:305–324.

- [Rozovsky, 1991] Rozovsky, B. (1991). A simple proof of uniqueness for Kushner and Zakai equations. In Mayer-Wolf, E., editor, Stochastic analysis, pages 449–458. Boston: Academic Press.