A Principal–Agent Model of Trading Under Market Impact111The research leading to these results has received funding from the ERC (grant agreement 249415-RMAC), from the Swiss Finance Institute project Systemic Risk and Dynamic Contract Theory, as well as the SFB 649 Economic Risk, and it is gratefully acknowledged.

-Crossing networks interacting with dealer markets-

Jana Bielagk222Department of Mathematics, Humboldt-University Berlin, Unter den Linden 6, 10099 Berlin, Germany.

bielagk@math.hu-berlin.de,

Ulrich Horst333Department of Mathematics, Humboldt-University Berlin, Unter den Linden 6, 10099 Berlin, Germany.

horst@math.hu-berlin.de &

Santiago Moreno–Bromberg444 Center for Finance and Insurance, Department of Banking and Finance, University of Zurich, Plattenstr. 14, 8032 Zurich, Switzerland. santiago.moreno@bf.uzh.ch

Abstract

We use a principal–agent model to analyze the structure of a book–driven dealer market when the dealer faces competition from a crossing network or dark pool. The agents are privately informed about their types (e.g. their portfolios), which is something that the dealer must take into account when engaging his counterparties. Instead of trading with the dealer, the agents may chose to trade in a crossing network. We show that the presence of such a network results in more types being serviced by the dealer and that, under certain conditions and due to reduced adverse selection effects, the book’s spread shrinks. We allow for the pricing on the dealer market to determine the structure of the crossing network and show that the same conditions that lead to a reduction of the spread imply the existence of an equilibrium book/crossing network pair.

AMS Classification: 49K30; 65K10; 91A13; 91B24.

Keywords: Asymmetric information; crossing networks; dealer markets; non–linear pricing; principal–agent games.

1 Introduction

Recently, the analysis of optimal trading under market impact has received considerable attention. Starting with the contribution of Almgren and Chriss (2001), the existence of optimal trading strategies under illiquidity has been established by many authors, including Forsyth et al. (2012), Gatheral and Schied (2011), Kratz and Schöneborn (2013) and Schied et al. (2010), just to name a few. The literature on trading under illiquidity typically assumes that block trading takes place under some (exogenous) pricing schedule, which describes the liquidity available for trading at different price levels. This article studies the impact of a CN on a DM within the scope of principal–agent models under hidden information (adverse selection). This asymmetric–information approach is a significant departure from the settings of the articles mentioned above. Specifically, we consider a one–period model where block trading is modeled via a risk–neutral dealer or market–maker who provides liquidity to a heterogeneous (in terms of idiosyncratic characteristics or “types”) group of privately–informed investors or traders. Extending the seminal work on asset pricing under asymmetric information in Biais et al. (2000), we assume that each investor has an outside option that provides him with a type–dependent reservation utility that the dealer may not be able to match without making a loss. We allow the dealer to abstain from trading with investors whose outside options would be too costly to match. The fact that the dealer may choose between excluding agents, matching their outside options (which in some cases yields him strictly positive profits) or offering them contracts that result in utilities that strictly dominate their reservation ones, implies that a rich structure (in terms of the partition of the type space) may emerge in equilibrium. For instance, in Example 4.9 we analyze a scenario where the type space is partitioned into two intervals where the agents’ outside options are matched, one where they are excluded and three where they earn positive rents. In more mundane terms, within a portfolio–liquidation framework, we may think of traders who need to unwind portfolios whose sizes are private information and who can either trade in a DM or a CN, the latter providing some of them with trading options that the dealer may be unable improve upon without suffering losses. To the best of our knowledge, such adverse–selection models have thus far only been considered by Jullien (2003) and Page Jr. (1992). The latter analyzes, in quite a general setting where the set of consumer types is a Polish space and the contract space an arbitrary compact metric space, the problem of a monopolist who faces both an adverse-selection problem (as in the work at hand) as well as a moral-hazard one relative to contract performance. Jullien (2003), on the other hand, only studies the adverse-selection problem in a finite-dimensional setting. This allows him to find a quasi-explicit representation of the optimal contract using Lagrange-multiplier techniques. He identifies conditions for the optimal contract to be separating, to be non–stochastic and to induce full participation. Furthermore, he also discusses the nature of the solution when bunching occurs. He does not, however, analyze the case where the dealer’s choices may have an impact on the structure of the reservation–utility function, which in turn would influence his decisions. Our study of such a feedback loop is novel and it is a crucial component in our analysis of the interactions between DMs and CNs, which is typically not unidirectional. To account for the fact that many off–exchange venues settle trades at prices taken from primary venues, we state sufficient conditions for the existence of an equilibrium pricing schedule. By this we mean that there exists a pricing schedule in the DM such that, if trades in the CN are settled at the best bid and ask prices from the DM, then the dealer’s optimal pricing schedule is precisely that schedule.

In order to study the impact of a type–dependent outside option, we first analyze the benchmark case where the said option is trivial, i.e. all traders may abstain from engaging the dealer and in turn earn (or lose) nothing. In such a setting the dealer is able to match the traders’ outside options by offering “nothing in exchange for nothing”, which is costless. This analysis follows Biais et al. (2000). Next we look at the general case where the traders’ reservation utilities are type dependent and the dealer need not be able to match them without incurring losses. It is well known that asymmetric information results, in equilibrium, in some traders being kept to their reservation utilities. This is due to the adverse–selection costs. Intuitively, these costs increase with the profitability of trading with high–type traders (e.g. investors with large portfolios). This suggests that when mostly high–type traders benefit from the outside option in terms of the latter strictly dominating what the dealer would have offered them in the benchmark case, then more low–type traders will be serviced in equilibrium. As a consequence of the reduced adverse–selection costs, more investors engage in trading, either in the DM or the CN. Our analysis further suggests that the presence of the CN is welfare improving even for investors for whom trading in the CN is not beneficial. We also provide sufficient conditions that guarantee that the competition from the CN results in a narrower spread in the DM. Overall, we propose a benchmark model of optimal block trading of privately–informed traders with an endogenous pricing schedule, analyze the impact of a CN on pricing schedules in DMs and prove an existence result of equilibria of best bid and ask prices in our trading game.

Related literature

Horst and Naujokat (2014) and Kratz and Schöneborn (2013) were the first to allow orders to be simultaneously submitted both to a dealer market (DM) and to an off–exchange venue such as a crossing network (CN) or a dark pool (DP). These are alternative trading facilities that allow investors to reduce their market impact by submitting liquidity that is shielded from the public view. The downside is that trade execution is uncertain: trades take place only when the matching liquidity is or becomes available. In such a case, trades are typically settled at prices prevailing in an associated primary venue, which significantly reduces the cost of large trades if settled in a CN or in a DP. The aforementioned articles on optimal, simultaneous trading in DMs and CNs do not allow for an impact of off–exchange trading on the dynamics of the associated DM. Equilibrium models analyzing the impact of alternative trading venues on DMs and trading behavior have been extensively analyzed in the financial–economics literature; see, e.g. Glosten (1994) and Parlour and Seppi (2003) and the references therein. To simplify the analysis of market impact, this literature typically assumes that the market participants trade only a single unit of the stock. For instance, in their seminal work, Hendershott and Mendelson (2002) derives conditions for the viability of the alternative trading institutions in a modeling framework where a random number of informed and liquidity traders, each buying or selling a single unit, chooses between a DM and a CN. In their model, dealers receive multiple single–unit orders and cannot distinguish between the informed and the liquidity orders. Hence, their bid–ask spread corresponds to each order’s market impact. Daniëls et al. (2013) consider the allocation of order flow between a CN and a DM when trading in both markets takes place at exogenously given prices. They show that small differences in the traders’ preferences generate a unique equilibrium, in which patient traders use the CN whereas impatient traders submit orders directly to the DM. Due to the fact that prices are exogenous, the equilibrium market share of the CN is fully determined by the price differential between the markets, together with the distribution of the traders’ liquidity preferences. In contrast with the two preceding works, where interactions between DMs and CNs are studied, Buti et al. (2016) take an alternative approach and analyze a dynamic model with single–unit traders who may place market or limit orders in a limit–order book (LOB). Alternatively, should they have access to it, the agents may place an immediate–or–cancel order in a dark pool (DP). Agents differ in their valuation of the asset and their access to the DP. The authors find that, whenever the LOB is illiquid, the presence of a DP leads to widening spreads and to a decline in the book’s depth; thus, to a deterioration of market quality and welfare. This, in spite of the fact that, on average, trade volume increases. These negative effects are generally decreasing in the depth of the LOB. The take–home message offered is that, when studying interacting LOBs and DPs, there is a trade–off between trade and volume creation on the one hand, and book depth and spread on the other one.

In terms of the aforementioned effects of the presence of the CN, whereas increases in the number of participating agents and welfare are generic, the narrowing of the spread does not seem to be so. For instance in Buti et al. (2016), the presence of a DP results in a migration of liquidity and hence an increasing spread — an effect that cannot appear in our setting where all traders are liquidity takers. Contrastingly, Buti et al. (2011), provide empirical evidence that high DP activity is associated with narrower spreads, but no causality is concluded. In Zhu (2014), asymmetric information divides agents into informed and (uninformed) liquidity traders. When a CN complements an existing DM, the spread widens because the liquidity traders move to the CN, whereas the informed ones, who tend to be on one side of the market, prefer the DM. In our setting, agent heterogeneity corresponds to different endowments or preferences, but there is no distinction at the level of access to information. Hence, the spread originates due to the adverse–selection problem faced by the dealer.

The remainder of this article is structured as follows. Our model and main results are presented in Section 2. Existence of a solution to the dealer’s optimization problem is established in Section 3. Section 4 studies the impact of a CN on the spread. Section 5 establishes our result regarding the existence of equilibrium price schedules. A specific application to a portfolio–liquidation problem with dark–pool trading is analyzed in Section 6 and Section 7 concludes.

2 Model and main results

We consider a quote–driven market for an asset, in which a risk–neutral dealer engages a group of privately–informed traders555Our dealer is called the principal in the contract–theory jargon and the traders are usually referred to as the agents.. The dealer market (DM for short) is described by a pricing schedule In other words, units of the asset are offered to be traded, on a take–it–or–leave–it basis, for the amount . For we refer to the pair as a contract. We assume that and that is absolutely continuous. Thus, we may write

and analogously for negative values of Here is the marginal price at which the –th unit is traded. As we shall see below, pricing schedules are, in general, not differentiable at zero. Hence, for a particular schedule the spread is

where and are the best–bid and best–ask prices, respectively. We denote by the dealer’s inventory or risk costs associated with a position , e.g. the impact costs of unwinding a portfolio of size in a limit order book. We assume that the mapping is strictly convex, coercive and that it satisfies

The traders’ idiosyncratic characteristics are represented by the index that runs over a closed interval called the set of types. We assume that zero belongs to the interior of Saying that a trader’s type is means that if he trades shares for dollars his utility is where

and are smooth functions that satisfy is strictly increasing and holds for all . Thus far, with our choice of preferences the traders enjoy a type–independent reservation utility of zero, should they decide to abstain from trading in the DM. Such an action is commonly referred to agents choosing their outside option. As , providing is costless to the dealer and, since yields all agents their reservation utility, in the absence of any other trading opportunity, we may equate the contract to the traders’ outside option.

Besides participating in the DM, each trader has the possibility to submit an order to a crossing network (CN). The latter is an alternative trading venue where trades take place at fixed bid/ask prices , but where execution might not be guaranteed.666In other words, the crossing network presents agents with possibly better prices at the cost of an uncertain execution. CN trading often benefits agents who intend to unwind large positions, which might result in a price impact. The possibility of trading in the crossing network modifies the traders’ outside option to the extent that now they may choose between abstaining from all trading and earning zero or participating in the CN if the corresponding expected utility is non–negative. For a specific the quantity represents the expected utility of the –type investor who decides to take his (now extended) outside option. In the sequel we indulge in a slight abuse of the language and also refer to as the agents’ outside option(s). Following Daniëls et al. (2013); Hendershott and Mendelson (2002) we focus on the case where a trader chooses exclusively between his outside option and trading in the DM, i.e. we do not allow for simultaneous participation in the DM and the CN. Initially we take as given, but later we analyze the case where it is endogenously determined through the interaction between the DM and the CN via the feedback of the spread in the former into the pricing in the latter. We work under the following assumption:777Once an assumption has been made, we consider it to be standing for the remainder of the paper.

Assumption 2.1.

There is a fixed cost of accessing the outside option such that, for all the function can be written as where

Trading over the DM is anonymous; the dealer is unable to determine a trader’s type before he engages the latter. The only ex–ante information the dealer has is the distribution of the individual types over which is described by a density In the sequel we specify the traders’ and the dealer’s optimization problems and analyze the impact of the CN on the DM, especially on its spread.

2.1 The traders’ problem

Until further notice we consider to be fixed. The problem of a trader of type is to determine, for a given pricing schedule

and then choose, for between his indirect–utility from trading in the DM and his outside option As the supremum of affine functions, the indirect utility function is convex.

The choice of a pricing schedule induces a partition of the type space. We say that a trader of type participates in the DM if assuming that ties are broken in the dealer’s favor. Conversely, we say that a trader of type is excluded from trading in the DM if For a given schedule we denote the set of excluded types by Observe that, in the absence of a CN, there is no loss of generality in assuming that all traders participate. We say that a trader of type is fully serviced if he earns strictly positive profits from interacting with the dealer.

2.2 The dealer’s problem

The Revelation Principle (see, e.g. Meyerson Meyerson (1991)) says that, when studying Nash–equilibrium outcomes in adverse-selection games such as ours, there is no loss of generality in focusing on direct–revelation mechanisms, i.e. those mechanisms where the set of types indexes the contracts. Furthermore, from the Taxation Principle (see, e.g. Rochet Rochet (1985)) there is also no loss of generality in writing instead of where is an absolutely continuous function. From this point on we shall, therefore, study our principal–agent game through books of the form and drop from the specification of the indirect–utility functions. We also write instead of for the set of excluded types.

At the onset, a trader of type could misrepresent his type by choosing a contract with The dealer strives to avoid this situation, since he wants to exploit the information contained in the density of types. This requires that he offers incentive–compatible books, i.e. those that satisfy

In the presence of an incentive–compatible book, the contract that yields a trader of type his indirect utility is precisely the one the dealer has designed for him.

Since the dealer is risk neutral, his goal is to maximize his expected income from engaging the traders. Taking into account the impact of the CN on the traders’ optimal actions, his problem is to devise so as to solve the problem

Due to the Envelope Theorem, if a contract is incentive compatible, then belongs to the subdifferential . Since for almost all it holds that and is strictly increasing, we have for almost all that

| (1) |

Therefore, starting from a convex indirect–utility function we can recover, for almost all types, the quantities in the incentive–compatible book that generated it. Furthermore, the indirect utility function may be written as

| (2) |

where It follows from Eqs. (1) and (2) that the traders’ indirect utility function contains all the information about the quantities and the pricing schedule, which allows us to write instead of In particular, introducing the functions

and denoting by the cone of all real–valued convex functions over , we can restate the dealer’s problem as

We prove in Theorem 2.4 below that, under suitable assumptions, Problem admits a solution. The latter is, in fact, quasi–unique in the sense that on the set of participating types the solution is indeed unique. However, agents are excluded by offering their types any incentive–compatible, indirect–utility function that lies below In other words, there is no uniqueness on the set of excluded types. From the agents’ point of view there is no ambiguity: they either trade with the specialist or they take their outside option. The non–uniqueness is also a non–issue for the specialist, since it it only appears in subdomains of the type space that he does not access. With this in mind, in the sequel we denote by “the” solution to Problem .

Assumption 2.2.

The functions and are such that is strictly convex, coercive, continuously differentiable and it satisfies

Determining the set of types who do participate but who earn zero profits is essential to our analysis, since it is precisely at the boundary types where and are determined. We prove in Lemma 4.7 that, by virtue of Assumption 2.1, these limits are always well defined. For any , we shall refer to

as the set of reserved traders. Whenever we refer to the reserved set corresponding to the solution to we write We prove in Proposition 3.2 that there is no loss of generality in assuming that any feasible satisfies thus,

Remark 2.3.

A well defined spread requires to be a proper interval which will follow from Assumption 2.1, and that there exists such that and belong to the set of fully–serviced traders. The existence of such an is proved in Lemma 4.7. Economically, this conditions means that the CN is not beneficial for low–type traders. We shall encounter several instances where the proofs of our results concern conditions on points to the left of or to the right of that are analogous. So as to streamline the said proofs, whenever we find ourselves in one of these “either–or” situations, we deal only with the positive case.

We are now ready to state the first main result of this paper, whose proof is given in Section 3 below.

Theorem 2.4.

Problem admits a solution, which is unique on the set of participating types.

Our second main result concerns the effect of the CN on the spread and the set of participating traders if, disregarding negative expected unwinding costs, the dealer can match the CN.

Assumption 2.5.

There exists an incentive compatible book such that for almost all it holds that

Assumption 2.5 implies that is also a convex function. The case where is concave is somewhat simpler, since it boils down to exclusion without matching.

The following theorem analyzes the impact of the CN on the DM and the traders’ welfare.

Theorem 2.6.

For a given price let and be the spreads with and without the presence of the crossing network and and the corresponding indirect–utility functions, respectively. In the presence of the crossing network

-

1.

less types are reserved, i.e. Furthermore, the inclusion is strict if there exists such that

-

2.

if the types are uniformly distributed () the spread narrows, i.e.

-

3.

the typewise welfare increases, i.e. for all

In the sequel we use the subindexes and to distinguish structures or quantities with and without a CN, respectively.

2.3 Equilibrium

It is natural to assume that pricing in the DM has an impact on the pricing schedule For example, the CN could be a dark pool, where trading takes place at the best–bid and best–ask prices of the primary market. We analyze such an example, within a portfolio–liquidation framework, in Section 6. The pecuniary interaction between the DM and the CN, however, is not unidirectional if the dealer anticipates the effect that his choice of book structure has on the CN. Our main focus is the impact of the CN on the spread in the DM. Specifically, if we denote by the best bid–ask prices in the DM for a given CN price schedule then we call an equilibrium price if

We make the following natural assumption on the impact of on the traders’ outside option.

Assumption 2.7.

Let where “” is the lexicographic order in then for all it holds that Furthermore, we assume that there exists such that for all such that and

The following is our main result on the existence of an equilibrium price.

Theorem 2.8.

If types are uniformly distributed, then the mapping has a fixed point.

Summarizing, we have that the dealer can correctly anticipate the movements in prices in the CN when he designs the optimal pricing schedule for the DM. Furthermore, the presence of the CN is beneficial in terms of liquidity, market participation and the traders’ welfare.

3 Existence of a solution to Problem

In this section we prove the existence of a solution to the dealer’s problem in the presence of a CN. Even though, strictly speaking, this result is a particular case of Theorem 4.4 in Page Jr. (1992), for the reader’s convenience we present a proof in our simpler setting. Some of the arguments are somewhat standard, but we include them for completeness. The first important result that we require is that the dealer’s optimal choices will lead to him never losing money on types that participate.

Proposition 3.1.

If is an optimal allocation, then for all participating types it holds that

Proof. Assume the contrary, i.e. that the set

where has positive measure. Define a new pricing schedule via

The incentives for types in do not change, since their prices remain unchanged, whereas prices for others have increased. Profits corresponding to trading with types in increase to zero. As a consequence the dealer’s welfare strictly increases, which violates the optimality of

A consequence of Proposition 3.1 is that, together with Assumption 2.2, it allows us to restrict the feasible set of the dealer’s problem to a compact one. We prove this in several steps,

Lemma 3.2.

If is a non–negative, convex function that solves then

Proof. Assume that solves and This implies that Since, from Assumption 2.1, a trader of type has no access to a profitable outside option, then he participates. From Proposition 3.1 it must then hold that which in turn implies that This relation, however, can only hold for which implies that

Lemma 3.3.

There exists such that if is feasible, then

Proof. From Assumption 2.2 and the compactness of we have that the mapping tends to as uniformly on for From Proposition 3.1 must be non–negative for all participating types, which concludes the proof.

From Lemmas 3.2 and 3.3 we have that the quantity is an upper bound for any feasible choice of which yields the following

Corollary 3.4.

The feasible set of Problem is uniformly bounded and uniformly equicontinuous.

Proof. A uniform bound is Lemma 3.3 guarantees that for any it holds that In other words, is composed of convex functions whose subdifferentials are uniformly bounded, hence is uniformly equicontinuous.

Notice that, when it comes to determining quantities and prices for trader types who do participate, Proposition 3.1 results in the dealer having to solve the problem

The last auxiliary result that we need is the following proposition, whose proof is a direct consequence of Fatou’s Lemma, together with Lemmas 3.2 and 3.3.

Proposition 3.5.

The mapping is upper semi–continuous in with respect to uniform convergence.

We are now ready to prove our first main result:

Proof of Theorem 2.4: Assume that is non–empty and consider a maximizing sequence of Problem From Corollary 3.4 we have that, passing to a subsequence if necessary, there exists such that uniformly. A direct application of Proposition 3.5 yields that is a solution to To finalize the proof we must construct from a solution to Problem To this end, let us define the sets

It is well known that if a sequence of convex functions converges uniformly (to a convex function), then there is also uniform convergence of the derivatives wherever they exist, which is almost everywhere. This fact, together with the continuity of the mappings and implies that is the union of a disjoint set of open intervals:

Define, for each

and consider the support lines to at and given by

respectively. Let be, for each the unique solution to the equation and define on

Finally define

then is a solution to Problem and which concludes the proof.

Remark 3.6.

If the specialist can profitably match all agents’ outside option, then the quasi–uniqueness of a solution to Problem is in fact uniqueness and it follows directly from Assumption 2.2. Indeed, in such a case

nd problem is one of maximizing a strictly concave, coercive functional over a convex set that is closed with respect to uniform convergence. In the general case, we construct the quasi–unique solution in Section 4.2. Assumption 2.2 remains crucial, since it guarantees that the maximization problems through which we define the optimal quantities have unique maximizers.

4 The impact of a crossing network

In this section we look at the impact that a CN has on the spread, on participation and on the traders’ welfare. In order to do so, we provide a characterization of the solution to Problem It should be noted that, given the restriction of candidate solutions to we cannot simply make use of the Euler–Lagrange equations to solve the variational problem, since the said equations are only satisfied when the constraints do not bind.

4.1 A benchmark without a CN

We first analyze the benchmark case where the traders do not have access to a CN. The corresponding dealer’s problem is denoted by Recall that all trader types have a zero reservation utility, which the dealer is able to match costlessly by offering the contract The point of making this normalization is to simplify the constraints in the dealer’s optimization problem. This will not be possible in the presence of a CN since, even if the dealer were able to match the utility that investors enjoy if they trade in the CN, this would be in general not costless.

We take a Lagrange–multiplier approach to provide a characterization of the solution to Problem To this end, let us introduce the following definition:

Let be the space of non–negative functions of bounded variation which we place in duality with the space of real–valued, continuous functions on via the standard pairing

for where is the distributional derivative of Furthermore, it follows from Pontryagin’s Maximum Principle and the fact that is a probability density function that there is no loss of generality in assuming that is absolutely continuous and that The Lagrangian for the dealer’s problem is

with corresponding Karush–Kuhn–Tucker conditions

| (3) |

The next result is the formalization of the vox populi saying that “quality does not jump”. Regularity properties of the solutions to variational problems subject to convexity constraints were studied by Carlier and Lachand–Robert in Carlier and Lachand-Robert (2001), and their methodology can be directly adapted to prove the following result.

Proposition 4.1.

If is a stationary point of then

The fact that, at the optimum, the mapping is continuous, implies that is also a continuous function of the types. This will prove to be extremely useful, specially in the presence of a crossing network. If we integrate by parts, then can be transformed into

where as described above, and The idea now is to maximize the mapping

pointwise, for a given fixed (in the sequel we use whenever we are dealing with an arbitrary but fixed value of ). From Assumption 2.2 it follows that we can write down the unique maximizer as

where For each and the quantity is a candidate for the optimal and convexity (or incentive compatibility) is verified if the mapping is increasing. The crux is then to determine the Lagrange multiplier In the sequel we denote where solves Problem In other words, if , then

From Lemma 3.2 we have that, unless the quantity and the complementary–slackness condition imply that for for some The left endpoint of is then determined by solving the equation

Furthermore, since must be convex, once then for all This implies that the right endpoint of is determined by solving the equation

The quantities and are know as the hazard rates, and sufficient conditions for the mapping to be non–decreasing are

see, e.g. Biais et al. Biais et al. (2000) for a discussion on this condition.

Let us assume that we have determined . What remains is then to connect the participation constraint with the spread. Differentiating Eq. (2) and noting that we have that

Observe that and are in fact and since by construction If we define and , then we have that the spread is given by the expressions

| (4) |

Our objective in Section 4.2 is to compare the values above to those obtained in the presence of a crossing network.

Before we proceed we present two examples so as to illustrate the use of the methodology described hitherto. The first revisits Mussa & Rosen Mussa and Rosen (1978). The second is slightly more advanced. We shall use it below to illustrate the complex structure of equilibrium pricing schedules and utilities in the presence of CNs.

Example 4.2.

Let us assume that for some , that types are uniformly distributed and that

We also set By direct computation we find that and Since a trader of type is brought down to reservation utility and hence trades the expression

implies that the Lagrange multiplier is

In particular, and hence and . Thus, the spread increases linearly in the highest/lowest type.

Example 4.3.

Let us assume that the distribution of types over is given by for and for ; that and that It is straightforward to show that the conditions on the Hazard rates are satisfied and that

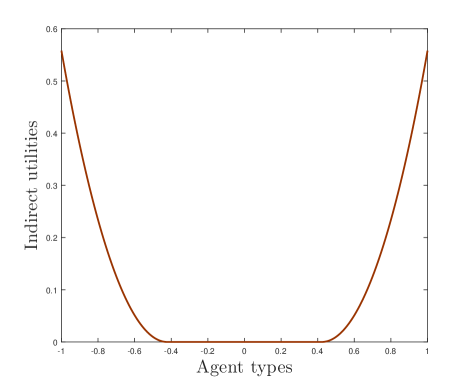

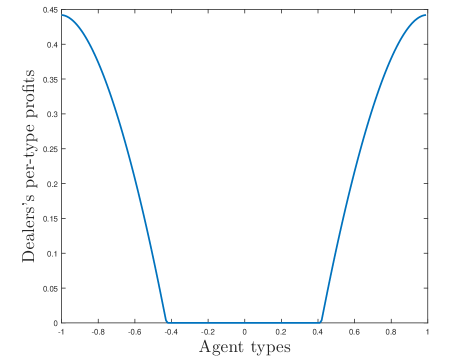

Furthermore, For the spread, we have that and In order to obtain we integrate (since ) and take into account that over We plot graph in Figure 1, as well as the per–type profits of the dealer.

4.2 Introducing a crossing network

Let us now analyze the dealer’s problem when the market participants have access to a CN that yields a trader of type the expected utility In this setting it is no longer without loss of generality to assume that all traders participate in the DM, given that enforcing participation (which can be done thanks to Assumption 2.5) may result in losses to the dealer. The latter may, as a consequence, choose to abstain from trading with a set of types by offering an incentive–compatible book whose corresponding indirect–utility function lies strictly under for . The resulting problem for the dealer would be

Dealing with the presence of the zero–one indicator function is quite cumbersome (see, e.g. Horst & Moreno–Bromberg Horst and Moreno-Bromberg (2011)), since its domain of definition may change with different book choices. In contrast to the setting studied in Horst and Moreno-Bromberg (2011), however, here the CN is passive. This lack of non–cooperative–games component allows for an alternative way to proceed. To this end, we make use of the following accounting trick, which was introduced by Jullien Jullien (2003): Let us assume that the dealer had access to a fictitious market such that the unwinding costs from trading in it, denoted in the sequel by satisfy for almost all In this way, we may again assume that the dealer trades with all market participants, but now his costs of unwinding are given by the function defined as

In terms of incentives, nothing is distorted by introducing the cost function but we must identify the points where there is switching from using to using and vice versa. These switching points will determine the regions of market segmentation.

If we define, for any traded quantity the function then we may re–use the machinery from Section 4.1 with minor modifications;888Observe that Assumptions 2.1 and 2.5 imply that satisfies Assumption 2.2. namely, denoting by the energy corresponding to the cost function we may write the Lagrangian of the dealer’s problem as

with the corresponding complementary–slackness conditions. From here we may proceed as in Section 4.1 to find the quantities that the dealer will choose to offer. Strictly speaking we should find the pointwise maximizer in of the expression

| (5) |

where This may fortunately be avoided, given that whenever , the participation constraint binds and Before proceeding to the proof of Theorem 2.6, we study the mechanism used by the dealer to choose between excluding types, matching the CN and trading with them while offering strictly positive rents.

Whenever the participation constraint does not bind, the dealer selects the quantity to be chosen via the pointwise maximization of the mapping What makes the current problem trickier than the case without a CN is that now we must pay more attention to the evolution of the multiplier If we compare and to we may pinpoint the set where the participation constraint may bind. Observe that and are the sets of the lowest and highest quantities the dealer may offer in an individually–rational way. Hence, as long as there is the possibility of profitable matching.

There might be instances where the participation constraint is binding for some type , i.e. and In such cases and for the corresponding indirect utility function, and we say there is exclusion.

Remark 4.4.

It is at this point that the quasi–uniqueness mentioned in Remark 3.6 can be addressed. The principal’s problem using the cost function results in the condition

being trivially satisfied. As a consequence, problem admits a unique solution. The latter coincides, by construction, with the solution to whenever . The caveat is that the solution to problem is blind towards what is offered to excluded types, since here their outside option is costlessly matched (they are effectively reserved). Constructing incentive compatible contracts for the excluded types is, thanks to the convexity of the indirect utility function, relatively simple. For instance if an interval of types were excluded (but and participated) one could consider any two supporting lines to at and . From the resulting indirect–utility function on one could extract the corresponding quantities and prices. The resulting global convexity of the indirect–utility function offered by the principal would imply that all incentives would remain unchanged. Whether the principal would suffer losses from the contracts offered to types on would be irrelevant, since the corresponding agents do not participate.

As mentioned above, here it is not necessary to determine in order to do likewise with On the other hand, however, if we interpret as the shadow cost of satisfying the participation constraint, we may wish to identify the multiplier so as to have a measure of the impact of the CN on the dealer’s profits. The following result, which deals with points where there is switching between matching and fully servicing, extends Proposition 4.1.

Proposition 4.5.

For given, let be such that there exists such that on and on . Furthermore, assume that

where implements In other words, there is profitable matching on and the dealer fully services types on Then is a singleton. The result also holds if the order of the matching and full-servicing intervals is switched.

The rationale behind Proposition 4.5 is that, as long as the dealer is able to match the traders’ outside option without incurring in a loss, it is possible to normalize the latter to zero and directly apply Proposition 4.1. This is, naturally, not the case when matching results in losses. We put Proposition 4.5 to work in Example 4.9.

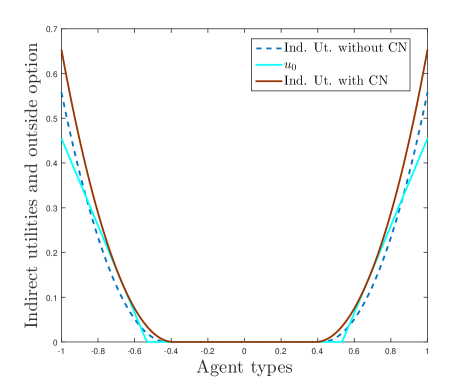

Before moving on, we present below a modification to Example 4.3 that shows how even agents without access to a non–trivial outside option benefit from the presence of the CN and that the optimal Lagrange multiplier need not be continuous.

Example 4.6.

Let and be as in Example 4.3 and assume that the CN offers the traders the following expected profits:

Matching this outside option would require the dealer to offer the contracts . This is profitable, hence the indirect utility never lies below . To illustrate this, we have plotted the indirect–utility function in Figure 2(a). It strictly dominates the one plotted in Figure 1(a) for all types who earn positive profits. The smooth pasting condition ( where touches , i.e. in ) determines the optimal Lagrange multiplier, namely and on . For positive types we obtain symmetrically and on . The new spread, given by , is strictly smaller than in the case without a CN.

The following result will prove to be essential for the results in Section 5. It guarantees,by virtue of Assumption 2.1, our notion of the spread is well defined in the presence of a CN and could be loosely summarized by saying that the first (in terms of moving away from ) types to earn positive utility trade in the DM.

Lemma 4.7.

There exists such that the types that belong to are fully serviced.

Proof. Let us denote by the positive solution to the equation If there exists such that types on can be matched profitably, then the result follows either because or because and the types on for some are fully serviced. Let us now assume that such an does not exist, we claim then that must hold. Proceeding by the way of contradiction, let us assume that (which is equivalent to ) and that there exists such that This configuration can be improved upon as follows: let be such that By construction Let us fix for where the solution to on if it exists or otherwise, given that we denote by the indirect–utility function corresponding to . In particular and for .

We now have that types are fully serviced. By Assumption 2.1, therefore, there exists such that for all it holds that If we could show that there exists such that the principal could offer types in the quantities at a profit, we would contradict the optimality of and the proof would be finalized, since incentives above would not be distorted and the principal’s profits would strictly increase. In order to do so, observe that the principal’s typewise profit when offering is

In particular, and

The step from the second to the third equality follows, because by construction by assumption and, from Assumption 2.2, Furthermore, since is strictly increasing and then Therefore, there exists such that if As a consequence, if is small enough, then for as required.

We are now in the position to present the proof of our second main result.

Proof of Theorem 2.6. (1) Observe that if is such that then the result follows immediately from Lemma 4.7. If we revert the inclusion, two situations are possible, since the addition of the CN–constraint to Problem may or may not bind for some types. The latter case being trivial, let us look at the case where there is a point on which it holds that and such that for and vice versa for The Lagrange multiplier is active on which implies that We know from Jullien (2003), p. 9, that for all such that the latter is decreasing in As a consequence, the root of the equation

is strictly smaller than that of which yields the desired result.

(2) Let us denote by and the best bid and ask prices without the presence of a CN and by and the corresponding marginal prices with one; thus,

and

From Part (1) we know that (both negative) and (both positive) and, since and do not depend on the presence of the CN, all we have left to do is show that

Using the well–known relation we have that

where we have used the fact that is constant on for some We may proceed analogously for the other three quantities. We have to show that

| (6) | ||||

which hold with equality under the assumption that

(3) If follows from Part (1) that, if participates in the presence of the CN, then Assume now that the inequality holds for all in a non–empty interval and and By the convexity of and this would imply the existence of such that holds almost surely in However and is strictly increasing; hence, this would imply that for almost all which is a contradiction.

We finalize this section with two examples that showcase the results obtained thus far. Example 4.8 showcases that, in the simple case where the outside option is such that the dealer will (only) exclude all high–enough (in absolute value) types, then the results of Theorem 2.6 follow trivially.

Example 4.8.

Let us revisit Example 4.2 with an extremely steep outside option that will warrant exclusion, namely, for let

Recall that, for a given value of the Lagrange multiplier, the corresponding quantity is

In Example 4.2 the participation constraint does not bind for high types. In particular, on and to find the left–hand endpoint of the reserved set we set and solve In the current setting, the participation constraint must bind for and the multiplier will be constant on where

By construction, the choice of will bear no weight on the trader types that will be serviced to the left of but only on how many additional low types benefit from the presence of the outside option. By integrating and noting that the corresponding indirect–utility function must satisfy we have, for

Since the indirect–utility function also satisfies we have that the dealer market on is described by the quantity–price pairs As a consequence, the per–type profit is

where the third term on the right–hand side is positive and dominates the first two. Finally, we have that each choice of will result in the dealer obtaining the aggregate profits from negative types

The mapping is strictly concave and the first–order conditions yield that it is maximized at As a result and which correspond to the boundary of the reserved set and the indirect–utility function for negative trader types in the problem without a CN on

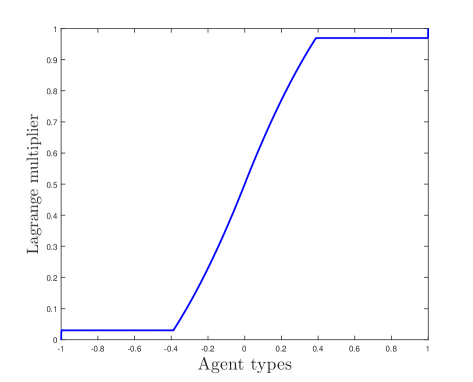

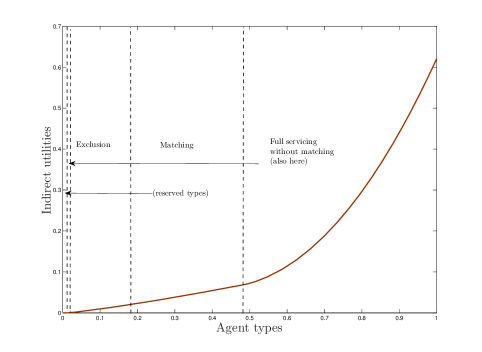

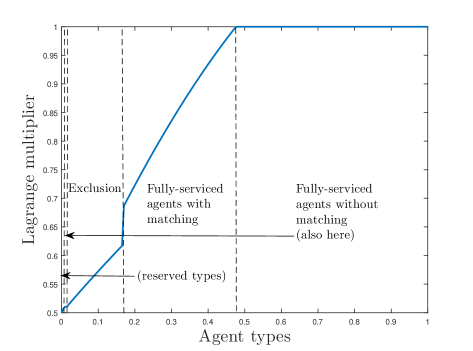

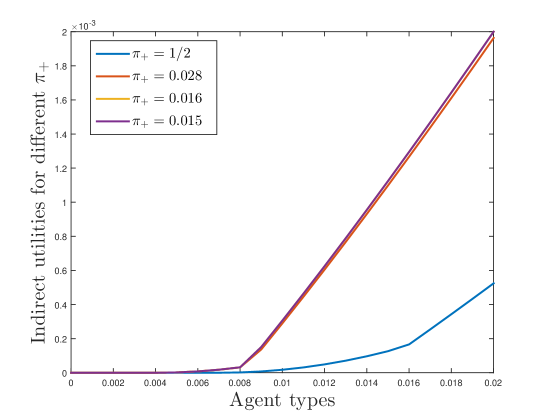

Example 4.9.

We stay with the basic setup of Examples 4.3 and 4.6, but now assume that for and otherwise. For any type such that it holds that

We assume The first thing to notice is that the dealer’s per-type profit for offering , i.e. , is negative for types . On the other hand, the inequality only holds for Combining both arguments we see that Next we observe that the inequality

holds for all Hence profitable matching may occur on the interval over which and Furthermore, Proposition 4.5 implies that the corresponding indirect utility function will be differentiable at In order to obtain for we integrate and determine the corresponding integration constant by equating

We know from the example without a CN that for On the multiplier must satisfy

which results in on the said interval. What remains to be determined is and To this end, we define the family of functions such that whenever this quantity is positive and for where is the solution to the equation Since we have that 999Pasting when passing from servicing to excluding need not be smooth. In fact, and the intersection of and occurs at

Summarizing, the types on are fully serviced, those on are reserved and the ones that lie on are excluded. The left–hand side of the spread is the same as in the example without a CN, whereas the right–hand side is This is significantly smaller than in Example 4.3.

Determining on is relatively simple, as we again must solve which results in . Finally, in order to determine on we must rewrite the virtual surplus using which results in The pointwise maximization of the resulting virtual surplus must equal After some lengthy arithmetic that we choose to spare the reader from, we obtain

Finally, in the profitable–matching region we solve so as to find the multiplier, which yields

or

Observe that, in contrast with Example 4.6, here for types that are strictly smaller than one. This means that the rightmost types do not profit from introduction of CN via changes in the quantities they are offered, but rather from changes in the corresponding prices. Intuitively speaking this has to do with how steep the outside option is for large types and, as a consequence, whether or not it will be matched over a non-trivial interval.

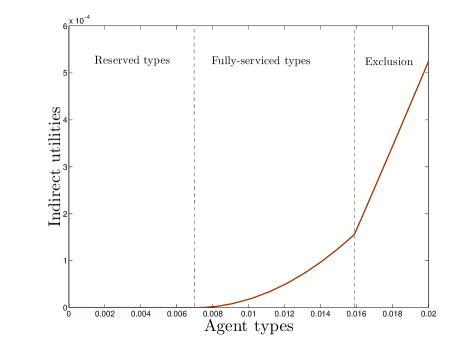

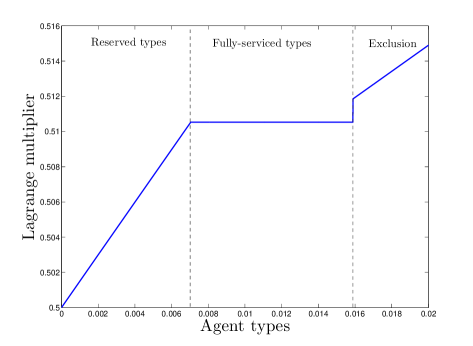

We present in Figure 3(a) the indirect utilities for positive types (the ones for negative ones being the same as in Figure 1(a)). The values of have been plotted in Figure 3(b). In Figure 4 we provide a magnification around small values of so as to highlight the switching between reservation, full servicing and exclusion. Observe the jump of the Lagrange multiplier at the boundary between fully–serviced and excluded types (Figure 4(b)) and between excluded and matched ones (Figure 3(b)).

We shall revisit this example in the upcoming section, where we look into the existence of equilibrium prices in the CN.

5 An equilibrium price in the crossing network

In this section we prove the existence of an equilibrium price We first observe that, from Assumption 2.7, there is no loss of generality in assuming that belongs to some closed and bounded subset of which we denote by As a consequence we have that The restriction of possible equilibrium prices to together with Assumptions 2.1 and 2.7, yields the next result.

Lemma 5.1.

There exists a non–empty interval such that

-

1.

-

2.

for all and all

In the sequel we make use of the results obtained in Section 4.2 to show that the mapping has the required monotonicity properties so as to use the following result (see, e.g. Aliprantis & Border Aliprantis and Border (2007)):

Theorem 5.2.

(Tarski’s Fixed Point Theorem) Let be a non–empty, complete lattice. If is order preserving, then the set of fixed points of is also a non–empty, complete lattice.

We are now ready to give the proof of our third main result.

Proof of Theorem 2.8. Lemmas 4.7 and 5.1 guarantee that we have a well–defined spread; thus, we may decompose the analysis of the mapping into that of the mappings and In other words, for a given price the dealer’s optimal response to is, modulo a normalization of equivalent to the combination of his actions towards negative and positive types separately. We shall concentrate on the existence of a fixed point of the mapping

From Assumption 2.7 we have that if , then for all If for it holds that for all , then on the same domain and Next assume that on a subset of for Given that for all then and the first point such that holds satisfies where the latter is the analogous to in the presence of The existence of and is guaranteed by the fact that in both cases the indirect–utility functions intersect the corresponding outside options. Arguing as in the proof of Theorem 2.6, Part (2), this also implies that hence In other words, the mapping is order–preserving and, using Tarski’s Fixed Point Theorem, we may conclude it has a fixed point.

Remark 5.3.

The requirement of uniformly distributed types can be relaxed to the extent that if and are such that Conditions (6) are satisfied, then the required monotonicity properties still apply. Unfortunately, these conditions cannot be verified ex–ante, since they include the end points of the set of reserved traders.

Example 5.4.

Let us go back to our example with exclusion, but introduce the feedback loop between the DM and the CN through the iteration We initialize the recursion by setting and , which are the parameters in the aforementioned example.

We observe a very swift convergence. Indeed, it takes only four iterations to reach and the indirect–utility functions in the third and fourth iteration are almost indistinguishable. The equilibrium price is . We present in Figure 5 the plots of the first four iterates. It is evident that each iteration results in a smaller set of reserved traders and in a higher indirect utility for all types. The spreads, the right endpoints of the reserved regions, the Lagrange multipliers at the right endpoint of the reserved regions and the exclusion regions are provided in Table 1. It is interesting to observe that, as the spread decreases to its equilibrium level, the number of trader types that are reserved decreases and the sets of excluded types grow (in terms of inclusions). This last fact obeys the fact that, when the traders have a more attractive outside option, it is harder for the dealer to match it profitably.

| [-0.423,0.0070] | 0.5105 | [0.0159, 0.1667] | |

| [-0.423,0.0040] | 0.5061 | [0.0083, 0.4872] | |

| [-0.423,0.0040] | 0.5060 | [0.0082, 0.4954] | |

| [-0.423,0.0040] | 0.5060 | [0.0082, 0.4955] |

6 Portfolio liquidation and dark–pool trading

In this section we present an application of our methodology to portfolio liquidation. We assume that the market participants’ aim is to liquidate their current holdings on some traded asset. The sizes of the traders’ portfolios are heterogeneous and saying that a trader’s type is means that he holds shares of the asset prior to trading. We set and If a trader of type trades shares for dollars, his utility is

where denotes the traders’ (homogeneous) sensitivity towards inventory holdings. Notice that is the type–dependent reservation utility of a trader of type If we “normalize” the said utility to zero, we may write

In this example the crossing network takes the form of a dark pool (DP). Choosing to trade in the latter entails two kinds of costs for the traders: On the one hand, there is a direct, fixed cost of engaging in dark–pool trading. On the other hand, execution in the DP is not guaranteed. We denote by the probability that an order is executed where we assume for simplicity that the probability of order execution is independent of the order size. Pricing in the DP is linear. Namely, for a given execution price , the utility that a trader of type extracts from submitting an order of shares to be traded in the DP is

where again we have normalized reservation utilities to zero. The problem of optimal submission to the DP for a –type trader is

which yields the optimal submission level

We obtain that opting for the DP results in a trader of type enjoying the expected utility

We assume that so as to keep the DP unattractive for small types.

We assume that the dealer’s costs/profits of unwinding a portfolio of size are where and is non–negative. Observe that, since does not satisfy Assumption 2.1, some restrictions must be imposed on the problem’s parameters so as to still have Lemma 5.1. Namely, it must hold that

| (7) |

Condition (7) imposes a hard upper bound on possible equilibrium DP prices. It should be noted that Assumption 2.7 is not satisfied by which, together with the way in which we shall define the pricing feedback loop from the DM to the DP, implies that our equilibrium result does not apply “as is” to the current setting.

6.1 The dealer market without a dark pool

In the absence of a dark pool, the dealer’s optimal choices of quantities are, for negative types

and for positive types

where the boundary of is given by

In order to guarantee that the condition must be imposed on the corresponding parameters. From the relation we have that the indirect–utility function is

where

When it comes to the spread, observe that and which yields

Below we analyze how the spread changes with the introduction of the DP.

6.2 The impact of a dark pool

We first take an exogenous execution price and determine, for each what is the quantity–price pair that the dealer must offer so as to match a DP with execution price Using the relation we obtain

| (8) | ||||

From the Envelope Theorem and the structure of we have that the traders’ indirect utility function satisfies

| (9) |

In order to determine the spread in the presence of the DP we must determine and together with and For an arbitrary we have

Indexed by the candidates for are then given by

Since it must hold that , then Integrating Expression (9) we have that, on the interval the traders’ indirect utility is given by

| (10) |

where is the first intersection to the left of of and and is determined by the equation

Unless the inequality is tight, in which case the types below are excluded, Proposition 4.5 implies that must be chosen so as to satisfy the smooth–pasting condition which is equivalent to

Observe that, besides the requirement the strategy to determine is exactly the same as for Summarizing, from Eq. (10) we observe that, if and correspond to the optimal choices for the negative and positive endpoints of then

The spread is then

i.e. the presence of a dark pool strictly narrows the spread in the dealer’s market.

6.3 An equilibrium price

A standard (but not unique) way in which dark–pool prices are generated is by computing the average of some publicly available best–bid and best–ask prices. In the case of the US, this is usually the mid–quote of the National Best Bid and Offer (NBBO). Borrowing from this idea we define the price–iteration in the DP as follows:

where are the best bid and ask prices in the DM in the presence of a DP with execution price We know from the previous section that the sequence hence, by the Bolzano–Weierstrass Theorem it has at least one convergent subsequence. The limit of each of the said subsequences will be an equilibrium price. The (possible) non–uniqueness of these prices is due to the fact that by virtue of its definition, the sequence of dark–pool prices need not be monotonic. The problem of non-uniqueness of equilibria in models of competing DMs and CNs has been observed before. We refer to Daniëls et al. (2013) for a detailed discussion.

7 Conclusions

We have presented an adverse–selection model to study the structure of the limit–order book of a dealer who provides liquidity to traders of unknown preferences. Furthermore, we have established a link between the traders’ indirect–utility function and the bid–ask spread in the DM. Making use of the aforementioned link, we have studied how the presence of a type–dependent outside option impacts the spread of the DM, as well as the set of trader types who participate in the DM and their welfare. In particular, we have shown, in a portfolio–liquidation setting, that the presence of a dark pool results in a shrinkage of the spread in the DM. Finally, we have established that, under certain conditions, the feedback loop introduced by the impact that the spread has on the structure of the outside option leads to an equilibrium price.

References

- Aliprantis and Border (2007) Aliprantis, C. D., Border, K. C., 2007. Infinite Dimensional Analysis: A Hitchhiker’s Guide. Springer Science & Business Media.

- Almgren and Chriss (2001) Almgren, R., Chriss, N., 2001. Optimal execution of portfolio transactions. J. Risk 3 (2), 5–39.

- Biais et al. (2000) Biais, B., Martimort, D., Rochet, J.-C., July 2000. Competing mechanisms in a common value environment. Econometrica 68 (4), 799–838.

- Buti et al. (2011) Buti, S., Rindi, B., Werner, I. M., 2011. Diving into dark pools. Working Paper 2010-10, Charles A. Dice Center.

- Buti et al. (2016) Buti, S., Rindi, B., Werner, I. M., 2016. Dark pool trading strategies, market quality and welfare. Journal of Financial Economics, (to appear).

- Carlier and Lachand-Robert (2001) Carlier, G., Lachand-Robert, T., 2001. Regularity of solutions for some variational problems subject to a convexity constraint. Communications on Pure and Applied Mathematics 54 (5), 583–594.

- Daniëls et al. (2013) Daniëls, T. R., Dönges, J., Heinemann, F., 2013. A crossing network versus dealer market: Unique equilibrium in the allocation of order flow. European Economic Review 62, 41–53.

- Forsyth et al. (2012) Forsyth, P., Kennedy, J., Tse, S., Windcliff, H., 2012. Optimal trade execution: A mean quadratic variation approach. J. Econom. Dynam. Control 36 (12), 1971–1991.

- Gatheral and Schied (2011) Gatheral, J., Schied, A., 2011. Optimal trade execution under geometric Brownian motion in the Almgren and Chriss framework. Int. J. Theor. Appl. Finance 14 (3), 353–368.

- Glosten (1994) Glosten, L., 1994. Is the electronic order book inevitable? The Journal of Finance 49, 1127–1161.

- Hendershott and Mendelson (2002) Hendershott, T., Mendelson, H., 2002. Crossing networks and dealer markets: competition and performance. The Journal of Finance 55, 2071–2115.

- Horst and Moreno-Bromberg (2011) Horst, U., Moreno-Bromberg, S., 2011. Efficiency and equilibria in games of optimal derivative design. Mathematics and Financial Economics 5 (4), 269–297.

- Horst and Naujokat (2014) Horst, U., Naujokat, F., 2014. When to cross the spread? trading in two-sided limit order books. SIAM J. Financial Math. 5 (1), 278–315.

- Jullien (2003) Jullien, B., 2003. Participation under adverse selection. Journal of Economic Theory 93, 1–47.

- Kratz and Schöneborn (2013) Kratz, P., Schöneborn, T., 2013. Portfolio liquidation in dark pools in continuous time. Math. Finance 25 (3), 496––544.

- Meyerson (1991) Meyerson, 1991. Game Theory: Analysis of Conflict. Harvard University Press, United States of America.

- Mussa and Rosen (1978) Mussa, M., Rosen, S., 1978. Monopoly and product quality. Journal of Economic Theory 18, 301–317.

- Page Jr. (1992) Page Jr., F. H., 1992. Mechanism design for general screening problems with moral hazard. Economic Theory 2 (2), 265–281.

- Parlour and Seppi (2003) Parlour, C.-A., Seppi, D. J., 2003. Liquidity-based competition for order flow. Review of Financial Studies 16, 301–343.

- Rochet (1985) Rochet, J.-C., 1985. The taxation principle and multi–time Hamitlon–Jacobi equations. Journal of Mathematical Economics 14, 113–128.

- Schied et al. (2010) Schied, A., Schöneborn, T., Tehranchi, M., 2010. Optimal basket liquidation for CARA investors is deterministic. Appl. Math. Finance 17 (6), 471–489.

- Zhu (2014) Zhu, H., 2014. Do dark pools harm price discovery? Review of Financial Studies 27 (3), 747–789.