Efficient Estimation in the Tails of Gaussian Copulas

Efficient Estimation in the Tails of Gaussian Copulas

Abstract

We consider the question of efficient estimation in the tails of Gaussian copulas. Our special focus is estimating expectations over multi-dimensional constrained sets that have a small implied measure under the Gaussian copula. We propose three estimators, all of which rely on a simple idea: identify certain dominating point(s) of the feasible set, and appropriately shift and scale an exponential distribution for subsequent use within an importance sampling measure. As we show, the efficiency of such estimators depends crucially on the local structure of the feasible set around the dominating points. The first of our proposed estimators is the “full-information" estimator that actively exploits such local structure to achieve bounded relative error in Gaussian settings. The second and third estimators , are “partial-information" estimators, for use when complete information about the constraint set is not available; they do not exhibit bounded relative error but are shown to achieve polynomial efficiency. We provide sharp asymptotics for all three estimators. For the NORTA setting where no ready information about the dominating points or the feasible set structure is assumed, we construct a multinomial mixture of the partial-information estimator resulting in a fourth estimator with polynomial efficiency, and implementable through the ecoNORTA algorithm. Numerical results on various example problems are remarkable, and consistent with theory.

1 INTRODUCTION

We investigate the question of efficiently estimating nonlinear expectations on constrained sets, that is, quantities that can be expressed as

| (1) |

where is a known polynomial, is a known constraint set, and has the NORTA (Gaussian copula) distribution (Nelson 2013, McNeil et al. 2005, Nelsen 2007). An important special case is the context of estimating the probability assigned to the set by a Gaussian copula, obtained by setting in (1). Since belongs to the NORTA family, we assume that random variates from the specific distribution of can be generated rapidly (Cario and Nelson 1997, 1998) on a digital computer. Also, when we say the function and the set are “known," we mean that they are both expressed in analytical form and that their structural properties, such as the curvature at a given point, can be deduced with some effort. Our particular interest is an estimator for that is effective when the set is assigned a small measure, as might happen in the context of studying the occurrence of rare events and calculating associated expectations in physical systems modeled using Monte Carlo simulation.

The question of estimating an expectation on a “small" constrained set is well motivated (Kroese et al. 2011, Asmussen and Glynn 2007), with examples arising in diverse fields such as production systems (Glasserman and Liu 1996), epidemics modeling (Eubank et al. 2004, Dimitrov and Meyers 2010), reliability settings (Barlow and Proschan 1987, Leemis 2009), financial applications (McNeil et al. 2005, Glasserman 2004), and confidence set construction within statistics (DasGupta 2008, 2011). The problem setting we consider in this paper is specific in that in (1) is assumed to be a NORTA random vector. We believe this special case is worthy of investigation since NORTA random vectors have recently become an important modeling paradigm (McNeil et al. 2005, Chapter 5) and, as we shall see, the knowledge that has a Gaussian copula can lead to highly efficient estimators of . Efficiency, as is usual, is considered here in a certain asymptotic sense, as the measure assigned to the set tends to zero.

1.1 Two Natural Estimators

An obvious consideration for estimating in (1) is the acceptance-rejection estimator, where independent and identically distributed (iid) copies of are generated and an estimator of is constructed using those random variates that fall within the set . To see why this estimator may not be efficient, consider estimating obtained by setting and in (1). (In what follows, we treat the quantity in (1) as a function of the parameter for reasons that will become clear.) The acceptance-rejection estimator is then given by . With some algebra, one can show that and that , giving the relative error

| (2) |

We see from (2) that the relative error as , and particularly that . (For two positive sequences converging to zero, we say to mean that .) Moreover, if has the Gaussian distribution with zero mean and unit variance, at an exponential rate (as ) suggesting that is a poor estimator of , especially for large values of .

A more sophisticated way of estimating is through exponential tilting or twisting (Glasserman 2004), where an estimator is obtained through importance sampling with a “shifted joint-normal" followed by an acceptance-rejection step. For the example considered above where , the exponential-twisting estimator

| (3) |

where has Gaussian density with mean and variance , and is the standard Gaussian density having mean zero and unit variance.

The estimator , like the estimator , is unbiased with respect to . Theorem 1 formally characterizes the asymptotic variances of and through a relative error calculation. A proof of Theorem 1 can be found in Appendix 6.

Theorem 1.

Let be the standard Gaussian random variable, , and . Then the following hold as .

-

(a)

-

(b)

with the minimum squared relative error

attained for the choice .

It is evident from Theorem 1 that if is chosen carefully, the estimator satisfies . While this suggests that is a much better estimator than , the fact remains that goes to as even in the one-dimensional context. By contrast, the estimator that we propose enjoys as ; in fact, we show that achieves bounded relative error for more general problems in an arbitrary (but finite) number of dimensions under certain conditions.

1.2 Summary and Key Insight

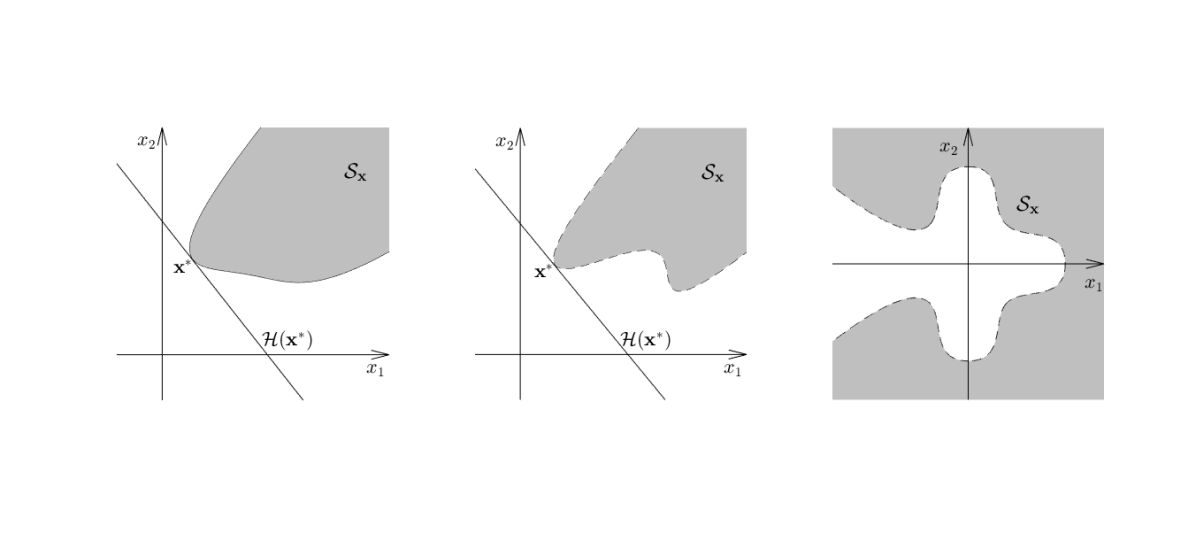

The central question underlying our investigation is whether there exist (Monte Carlo) estimators of whose relative error remains bounded as the set becomes rare in a certain sense. We answer in the affirmative but with some qualifications. We argue that highly efficient estimators of , particularly those with bounded relative error, can be constructed through the use of an appropriately shifted and scaled exponential importance sampling measure. The extent of such shifting and scaling, however, depends crucially on the following three structural properties of the set : (i) location of certain dominating points in defined (loosely) as the set of points that contribute maximally to the calculation of ; (ii) the local curvature of the set at the dominating points; and (iii) the existence (or lack) of a supporting hyperplane to the set at the dominating points. Considering (i) – (iii), we propose three alternate estimators , , that become applicable depending on the setting. The applicability of the estimators , , is summarized in Table 1 and illustrated through Figure 1.

Which amongst the estimators , , is most appropriate for a given setting will be dictated by how much information we have about (i), (ii), and (iii). For instance, the estimator is the “full information" estimator designed for use in contexts where is Gaussian, and the set is well-behaved with known structural properties, that is, has a unique dominating point with identifiable local curvature that is encoded by certain structural constants, and has a supporting hyperplane at the dominating point. We argue later that the conditions on under which the full-information estimator becomes applicable are not onerous. Particularly, we show in Section 3.2.1 that for a large class of sets , the structural constants of are identifiable through a linear program that is easily solved. We provide sharp asymptotics of in Section 3.2, demonstrating that it enjoys bounded relative error leading to the remarkable numerical performance illustrated in Section 5.1.

![[Uncaptioned image]](/html/1607.01375/assets/x2.png)

The other two estimators and that we propose are “partial-information" estimators in that they are applicable in Gaussian settings where we have knowledge of the dominating point of but only limited to no curvature information. As we show in Section 3.3 where we provide the sharp asymptotics for and , such lack of full information hinders the optimal choice of importance-sampling parameters resulting in a loss of the bounded relative error property. The estimators and still achieve a weaker form of efficiency that we call polynomial efficiency.

For contexts where no information about (i) – (iii) is available, we first propose and analyze an (unimplementable) estimator that is obtained as a multinomial mixture of the partial-information estimator . The ecoNORTA algorithm that we propose then constructs a sequential form of by adaptively estimating the dominating points. ecoNORTA starts with an initial crude guess of the dominating points, and as random variates are generated during the estimation process, progressively updates the location of the dominating points within the estimator .

1.3 Paper Organization

The paper is organized into two main parts that appear in Section 3 and Section 4 respectively. Section 3 treats the Gaussian context in its entirety; we present the full-information estimator in Section 3.2 and the partial-information estimators in Section 3.3. Much of the theoretical machinery introduced in Section 3 is then co-opted into Section 4 where we treat the NORTA context. Section 5 provides numerical illustrations in the Gaussian and the NORTA contexts. In the ensuing section, we first introduce some important notions of asymptotic efficiency that will be used throughout the paper.

2 ASYMPTOTIC EFFICIENCY: NOTATION AND DEFINITIONS

As is usual in rare-event literature, we use the notion of relative error in assessing the efficiency of the estimators of . The relative error of the estimator (with respect to the quantity ) is given by

| (4) |

Since much of our analyses is in a “rare-event regime," we will assess by studying the behavior of as , where the latter limit is usually accomplished by sending a “rarity parameter" . Accordingly, we will be compelled to use the notation and to make explicit the dependence of and on the rarity parameter .

The following notions that quantify the asymptotic behavior of the relative error will be useful for assessing estimators.

Definition 1.

(Bounded Relative Error) The estimator is said to exhibit bounded relative error (BRE) if

That an estimator has BRE means that its root mean squared error tends to zero at a rate that is commensurate with the rate at which the quantity it estimates tends to zero. Estimators exhibiting BRE are generally difficult to find in the Monte Carlo context; those with are especially difficult to find.

Considering the difficulty of finding estimators exhibiting BRE, a weaker form of efficiency called logarithmic efficiency has become popular.

Definition 2.

(Logarithmic Efficiency) The estimator is said to exhibit logarithmic efficiency if Equivalently, logarithmic efficiency holds if

In this paper, we use a slightly more specific form of efficiency called polynomial efficiency to characterize the behavior of estimators that do not exhibit BRE.

Definition 3.

An estimator is said to exhibit Polynomial(), efficiency if

It is clear that if is Polynomial efficient, then it is Polynomial efficient for all . Hence, we will generally seek the smallest such that a given estimator is Polynomial() efficient. Also, it can be shown with some algebra that estimators that exhibit Polynomial() efficiency are also logarithmically efficient as long as converges to zero “faster" than , that is, as for any . See Asmussen and Glynn (2007) for more on measures of efficiency in the rare event simulation context.

3 THE CONSTRAINED GAUSSIAN CONTEXT

In this section, we treat the special context of estimation on low-probability sets driven by the Gaussian measure, that is, the question of estimating when has a Gaussian distribution. As we shall see, the constrained Gaussian context is special in that knowledge of the local structure of the set at the so-called dominating point can be used fruitfully in constructing highly efficient estimators of . Accordingly, in this section, we propose and analyze three different estimators depending on the extent of such available information. We first reformulate the problem statment for ease of exposition.

3.1 Problem Reformulation

For clarity, and since we are in the constrained Gaussian setting, we specialize the notation introduced earlier to write

| (5) |

where the feasible set , and is a polynomial in . The first subscript refers to the “rarity parameter" and will be explained in greater detail in Section 3.1.2. It has been introduced into notation to make explicit the dependence of the feasible set on a parameter that will be sent to infinity in our asymptotic analyses.

3.1.1 Key Assumptions

For the purposes of Section 3 alone, we assume that the random vector and in (5) are expressed in such a way that the following assumption holds.

Assumption 1.

-

(a)

is distributed as the standard Gaussian density

-

(b)

The “dominating point" exists, is unique, and known.

-

(c)

The “dominating point" is such that .

Assumption1(a) does not threaten generality — settings where has a multivariate Gaussian distribution with mean and positive-definite covariance matrix can be recast in the “standard Gaussian space" as the problem of estimating , where the lower-triangular matrix is such that , and the set .

Assumption1(b) holds often. For example, when the set is expressible through known convex constraints, that is, where the functions are convex, then is the solution to a convex optimization problem and can usually be identified simply. Even if one or more of the functions are not convex, could probably be identified, albeit with some effort, by solving a non-convex optimization problem. If is not expressed through the constraint functions but is instead expressed through a membership oracle, identifying could become a challenging proposition.

Assumption1(c), which stipulates that the second through the th coordinates of are zero, has been imposed for convenience and can be ensured through an appropriate rotation of the set . Specifically, suppose we wish to estimate where is a standard Gaussian random vector and suppose exists and is unique. Then, since the standard Gaussian distribution is spherically symmetric, we can transform the problem using an appropriate “rotation matrix" calculated such that satisfies . Such a rotation matrix always exists. The corresponding constraint set after such rotation becomes yielding the reformulated problem of needing to estimate . Furthermore, since the function is a polynomial, is also a polynomial and no generality is lost.

Considering the above discussion, reformulating the general Gaussian setting to satisfy Assumption1(b) and Assumption1(c) involves two steps in succession: (i) standardize the set to , and (ii) perform the rotation .

We emphasize that Assumption1 is a standing assumption in the Gaussian context, that is, all three estimators , , rely on it. By contrast, the following structural assumption is needed for constructing only and , and not .

Assumption 2.

The hyperplane is a supporting hyperplane to the set , that is, every point satisfies .

Assumption2 states that the hyperplane passing through the dominating point and normal to the line joining the origin and the point is such that the set is on one side of it. The spirit of Assumption2 is that the region of integration governing the calculation of is a “tail region" that is a subset of an appropriate half-space. To aid reader’s intuition, we note that Assumption1 and Assumption2 together imply that the sets that we consider in Gaussian context have a dominating point and a “vertical" supporting hyperplane to at .

3.1.2 Asymptotic Regimes and a Word on Notation

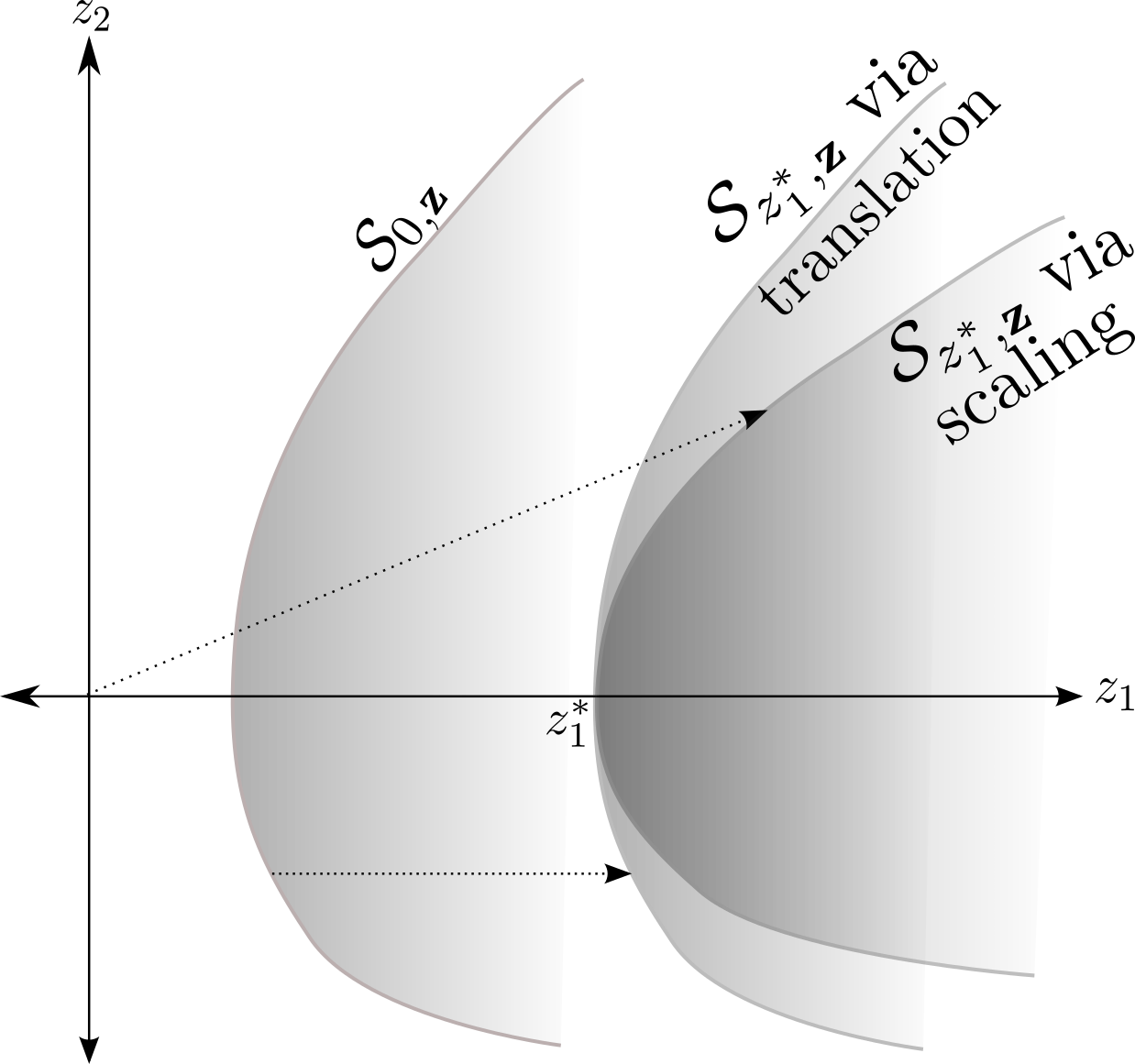

We will consider two types of asymptotic regimes when analyzing the effectiveness of a proposed estimator of . The first of these regimes, called the translation regime, refers to the sequence (in ) of sets obtained by “translating" a fixed set along the -axis. Formally, for a fixed set , we obtain the translation regime by defining and then considering the sequence of sets as .

The second asymptotic regime, called the scaling regime, refers to the sequence of sets obtained by “scaling" points in some fixed set using the scalar . Formally, for a fixed set , we obtain the scaling regime by defining and then considering the sequence of sets as .

Considering the reformulation due to Assumption1, under each regime the probability assigned to vanishes by simply sending . The translation and scaling regimes are depicted in Figure 2 where a fixed set is either translated or scaled to obtain the needed asymptotic regime.

The following comments are aimed at further clarifying notational issues.

-

(i)

The fixed set in the discussion above was introduced expressly for explaining the translation and scaling asymptotic regimes. We find no reason to refer to the set anywhere in the rest of the paper.

-

(ii)

Throughout the paper the scalar will serve as the rarity parameter that will be sent to infinity. In the translation regime, turns out to be the first-coordinate of the unique dominating point. In the scaling regime, has no such physical meaning.

-

(iii)

Unless mentioned explicitly, all analysis of the estimators we propose are performed in the translation regime. Particularly, all analysis in Section 3.2 and Section 3.3 is in the translation regime. We are forced to undertake analyses in the scaling regime in Section 4 in order to contend with the possibility of multiple dominating points.

3.2 The Full-Information Estimator

We now propose the full-information estimator for the constrained Gaussian context and in general high-dimensional space. As we shall see, knowledge of the local structure of the set at the dominating point is crucial for constructing efficient estimators of . Accordingly, our proposed estimator is a function of the local structure of the set around the point . Such local structure is encoded through the function in the following assumption, where quantifies the “cost-scaled content" of the set close to the point and “about" the line joining to the origin. When the cost function is identity, for instance, the function simply connotes the volume of the “cross-section" of the set when .

Assumption 3.

Let the cost function be a polynomial in , conveniently expressed as . Thus, is the term corresponding to the largest power of . Then, denoting and the cross-section set , the (d-1)-dimensional cost-scaled volume

satisfies the expansion as , and the constants are known. The argument in the constants and are often suppressed for convenience.

The assumption about the existence of a local polynomial expansion of is arguably mild; for example, it only precludes sets that are not “too sharp" around the point . The constants and appearing in the expansion of may or may not be easy to deduce depending on how the set is expressed. For example, when is expressed using constraint functions as and the functions are expressed analytically, the constants and can be identified easily. Such contexts seem typical and we provide a systematic way of identifying the structural constants for a large class of sets in Section 3.2.1.

Under Assusmption1, the quantity of interest takes the form

| (6) |

where are constants appearing in Assumption3, is the univariate standard Gaussian density, and the cross-section set . (In (6) and throughout the paper, we have chosen to omit the tedious repitition of the elemental -dimensional volume in the integral.) The above form of inspires our proposed estimator which takes the following simple form:

| (7) |

where is the shifted-exponential density function, is a random variable having the density , and the constants are from Assumption 3. (Theorem 3 will establish that the choice is optimal in the sense of minimizing the relative error of .)

The basis of should be evident from the structure of in (6); the outer integral in (6) is approximated by the term after noting that

as by Assumption3, and the inner integral in (6) is estimated using a shifted-exponential importance sampling measure along the first dimension. There appears to be no strong physical justification for the use of the shifted exponential family but an algebraic explanation is evident by observing the respective exponents of the Gaussian and the exponential densities. The choice of support for the importance sampling measure is dictated by information contained in Assumption 2.

Towards establishing the bounded relative error property of , we first present a result on the asymptotic expansion of a certain class of integrals that we will repeatedly encounter.

Lemma 1.

Let as . Then, for and as , the following hold.

-

(i)

-

(ii)

Proof.

Proof. Notice that

| (8) |

where the last line is obtained after the variable substitution . Now, since Lebesgue’s dominated convergence theorem (Billingsley 1995) assures us that

we see from (3.2) that This concludes the proof of part (i) of the theorem. The proof of part (ii) follows similarly.

∎

As is usually done when analyzing estimators of the type , we next present a result that characterizes the rate at which the quantity of interest tends to zero in the asymptotic regime . This will be followed by a result that characterizes the behavior of .

Proof.

Proof. Write

| (9) |

where . The right-hand side of (3.2) is thus in a form that allows invoking part (i) of Lemma 1, if we can identify the expansion of around .

Towards identifying the expansion of around , we notice that

| (10) |

Next, we notice that and defined in Assumption3 have the same asymptotic expansion around . We thus invoke part (i) of Lemma1 to conclude that

∎

We are now ready to present the main result that characterizes the behavior of the proposed estimator . Since is a biased estimator, the result that follows characterizes both the second moment and the bias of in the translation asymptotic regime .

Theorem 3.

The assertion in implies that achieves bounded relative error for any choice of , although it is evident that the specific choice of can have an important effect on efficiency. It is clear from the expression for the relative mean squared error in that the best possible convergence rate for will be obtained by maximizing the function with respect to . The following theorem states this formally. A proof is not given here but follows from the basic calculus.

Theorem 4.

The asymptotic rate is minimized (with respect to ) at . The corresponding minimal rate is

Furthermore, the minimal rate satisfies

Theorem 4 has interesting consequences since it connects the local structure of the feasible set with the convergence rate, with “sharp" sets calling for lower intensities and “shallow" sets calling for higher intensities. We have attempted to depict this through Figure 3, where various sets with different structural constants are plotted on the left panel. As the second part of Theorem 3 notes, the asymptotic optimal rate diverges weakly with , as shown by the right panel in Figure 3.

3.2.1 Identifying the Structural Constants and .

The reader will recognize that the estimator crucially depends on the dominating point , the structural constants , , and the highest power appearing in the polynomial cost function . Of these, the constant is known since we have assumed that the cost function is given as part of the problem; and the dominating point can usually be identified in the Gaussian context. The identification of the structural constants and , on the other hand, might involve some effort. In what follows, we demonstrate how the structural constants and can be identified in a systematic way for a reasonably large class of problems. We first present an example that will lead to the more general approach.

Example 1.

Suppose where is the standard trivariate normal and the set is given by Suppose , we see then that

Let and substitute and to get the inner integral in the form

| (11) |

We see that and in the variable substitution above need to be chosen appropriately so that the integral in (1) remains bounded away from and as . Inspecting the powers in the integrand in (1) leads to the following linear program (LP) as a way of determinining , .

The optimal solution to the above LP is when and otherwise. We thus see that as , , for and for . The exact rate at which as can then be calculated by invoking Lemma1.

Now let us generalize Example1. Recall from Assumption3 that the (d-1)-dimensional cost-scaled volume

where we have suppressed notation to write in place of . Suppose the set takes the form where the function is a known -th degree polynomial given by Since we seek an expansion of as , we consider the change of variable and write

| (12) |

where It is evident from (12) that if the scaling variables are chosen so that as , then we would have identified the needed expansion of about . For identifying the scaling variables , as in Example1, we consider the following LP in the decision variables .

Notice that the coefficient vector of the objective function in Problem LP is the same as those appearing within the exponent of the variable in (12); similarly, the constraints in Problem LP come from the exponent of the variable in the definition of the set . Furthermore, the explicit connection between the structure of the constraints in Problem LP and the definition of the set dictates that the set converges to a set (as ) whose volume remains bounded away from zero. This implies that the structural constants are given by , , where is the solution to Problem LP.

The above method for identifying the structural constants applies when the function is a polynomial. We conjecture that the presented method can be applied even more generally, when is smooth in a neighborhood around the dominating point , admitting the application of Taylor’s theorem (Royden 1988) around the point .

3.3 The Partial-Information Estimators and

Recall that the estimator treated in the previous section is a “full-information" estimator that achieves bounded relative error through shifting and scaling operations that depend explicitly on (i) the knowledge of the dominating point ; (ii) the knowledge of the local curvature of at encoded through the structural constants ; and (iii) the knowledge of a supporting hyperplane to at . In this section we present two partial-information estimators, and , for use in the absence of (ii) or (iii). The partial-information estimator is applicable when (ii) is absent but (iii) is present; the partial-information estimator is applicable when both (ii) and (iii) are absent.

Suppose we have knowledge of a unique dominating point and of a supporting hyperplane to at . The partial-information estimator is then given by

| (12) |

where , is a random variable having the shifted-exponential density function with , and are iid standard Gaussian random variables.

For contexts where we have knowledge of a unique dominating point , but not of a supporting hyperplane to at , the estimator is given by

| (13) |

where , is a random variable having the Laplace (or double-exponential) density function with , and are iid standard Gaussian random variables.

Notice that the partial-information estimators and are identical except due to the manner in which the first dimension is generated. Since assumes knowledge of a supporting hyperplane at the dominating point, the first dimension in is generated using a shifted exponential that is supported on . Since the estimator makes no assumption about the existence of a supporting hyperplane, it uses a Laplace density having support to model the first dimension of the importance sampling measure. Such careful choice of domain ensures that both and are unbiased estimators of .

The partial-information estimators and differ from the full-information estimator in two respects. First, in both and , notice that the rate parameter is chosen to be ; this is as opposed to the choice in , where the curvature constant was assumed to be available. Second, in the full-information context, it was possible to approximate the outer integral in (6) by the expression again because the structural constants and were assumed to be known. In the current partial-information context, since the constants and are unknown, the inner integral (6) is estimated using an aceptance-rejection procedure that needs the generation of the Gaussian random variables .

These differences lead to an inferior relative error of and as compared to the optimal estimator . In Theorem 5 that follows, we characterize the relative errors of the estimators and in both the translation and the scaling asymptotic regimes (see Section 3.1.2 for formal definitions). The latter regime will become important in Section 4 where the NORTA vectors are considered. A proof of Theorem 5 follows from the application of Lemma1, and is provided in the Section 6.

Theorem 5.

Theorem 5 demonstrates that the etimators and exhibit polynomial efficiency, with the latter’s relative error being twice that of the former. While this means that neither of the two estimators achieve bounded relative error, it is evident from the definition in Section 2 that both and achieve logarithmic efficiency. It so happens that the exponential-twisting estimator also achieves polynomial efficiency but is inferior to that of and . Specifically, for both the translation and scaling regime, as . Sharp asymptotics of are given in the electronic companion, in Section 6.1.

We conclude this section with two examples that are meant to illustrate the performance of the estimators and . The first example illustrates the performance of and on a feasible set that is a polyhedral cone opening outward from the vertex and the second example illustrates the performance of and on a feasible set defined by a general smooth boundary.

Example 2.

Suppose and the set is a polyhedral cone (Boyd 2004) “opening outward" along the -axis and having vertex at . Formally, the set can be defined as , where are some fixed points in d and each of whose -coordinate exceeds . Recalling the cross-sectional set and using the variable substitution in the expression for the cost-scaled volume we get

| (14) |

We now read-off the structural constants from (14) as and . We can then invoke Theorem 5 to see that and have relative errors that diverge polynomially as for the translation regime and for the scaling regime.

Example 3.

Let’s now consider the more general context of estimating on a feasible set with cross-sectional set such that the function is a known -th degree polynomial. Recall from Section 3.2.1 that the polynomial rate in the volume expansion for sets that have a smooth polynomial boundary at is obtained as the optimal value of the linear program Problem LP. Thus, , where the is the optimal solution to Problem LP. If represents the optimal solution to the Problem LP with cost , then we have that

| (15) |

The term in parenthesis on the right-hand side of (15) is non-negative; it is zero if the solution to Problem LP with cost vector is also optimal to the Problem LP with cost vector . Also, the second term on the right-hand side of (15) is strictly positive given the constraints of Problem LP. We conclude from Theorem 5 that and have relative errors that diverge polynomially with exponents given by the right-hand side of (15).

4 THE CONSTRAINED NORTA-VECTOR CONTEXT

Recall our problem statement of having to estimate

| (16) |

where the set has a small implied measure under the distribution of . In Section 3, we assumed that the random variable belonged to the Gaussian family, leading to the reformulated problem in (5). In this section, we generalize to the important setting where is a NORTA vector, that is, has a distribution whose dependence structure is specified through the Gaussian copula (Nelson 2013, McNeil et al. 2005, Nelsen 2007, Ghosh and Henderson 2003). Since such generalization renders the estimators inapplicable (particularly due to possible violation of Assumption 1(b)), we present a fourth estimator that is derived from and achieves polynomial efficiency under certain conditions.

For easing exposition of , let us now reformulate the problem in (16) for the context where is a NORTA random vector. If is a NORTA random vector, it is well-known (Nelson 2013, Ghosh and Henderson 2003) that the components of can be expressed through the NORTA map as for , , , where is the standard normal distribution function, is the marginal distribution of with inverse , and is a standard Gaussian random vector, and the matrix defines a Gaussian random vector with mean and positive-definite covariance matrix . The NORTA inverse map allows to reformulate the problem in (16) into the Gaussian space as follows.

| (17) |

We limit our attention to continuous marginal distributions such that their density function exists and is strictly positive everywhere. (Note that continuous may have “flat” regions, e.g. where the density is zero, and hence and may have jump discontinuities.)

Notice that the problem in (4) has been recast in the Gaussian space implying that one of the estimators , , or could be applicable as an estimator. The complication, however, is that the transformed feasible set may not be well-behaved even if the set is well behaved. For example, properties such as convexity are generally not preserved in the sense that even if is convex, may not be convex. More importantly, the dominating point that was assumed to be known (and unique) throughout Section 3 is neither easily identified nor unique, rendering the estimators , , inapplicable for the current context.

Remark 1.

It so happens that the image of the set of boundary points of remains on the boundary of . One may thus reasonably expect that the pre-image of the dominating set is “close" to the dominating set in the space. This and some other properties are summarized in Section 6.2 appearing in the appendix.

4.1 The ecoNORTA Estimator

Considering that the set in the NORTA context (4) can be poorly behaved, in what follows, we assume only that the dominating set exists. Specifically, we make no assumptions about the cardinality of the set except that , nor about the local curvature of at the dominating set (as embodied in Assumption 3).

The ecoNORTA estimator is a mixture of estimators, each of which is centered at the elements of . Formally, we write

| (18) |

where the random variable , is a random variable having the shifted-Laplace density function defined in Section 3.3, and are iid standard Gaussian random variables. The mixing random variable has a multinomial distribution supported on with probability mass function .

As can be seen in (18), the estimator co-opts the estimator for a context where the set may have multiple dominating points. The multinomial random variable in (18) samples one such dominating point, and the rotation matrix reverses alignment with the axis to generate a random variate near the -th dominating point . The unbiasedness of in estimating follows from the absolute continuity of the Laplace density with respect to the standard normal density . As we will demonstrate shortly through Theorem 6, under certain structural conditions, the estimator achieves the same slow polynomially growing relative error as . This compares favourably with the exponential rates of the naïve estimator , and also the exponential-twisting estimator which is analyzed in Section 6.1. For showing the polynomial efficiency of the estimator , we make the following regularity assumption on .

Assumption 4.

-

(a)

At each , the set locally satisfies Assumption3 with parameters for cost exponents .

-

(b)

The half-spaces for all are such that .

[1,r,![[Uncaptioned image]](/html/1607.01375/assets/nortaSet.png) ,

An illustration of the conditions needed

for Theorem 6]

In Figure 4, the example set plotted in bold has

five dominating points in the set . The set locally satisfies

Assumption3 at each dominating point as required in

Assumption4(a). Assumption4(b) states

that the set as a whole lies inside the union of the half-spaces

defined by the tangent hyperplanes at each of the dominating points, as

shown by the light-shaded region. Also plotted is an example set

that satisfies Assumption4(a) but not

Assumption4(b) in the dark-shaded regions. So, the

requirement Assumption4(b) may be violated in practice

by sets like , but the regions where these happen are far from

the dominating points, and so it is reasonable to expect that the

relative error does not degrade too much. Thus, the uniqueness of

the dominating point (Assumption1) as well as the assumption about the separating hyperplane (Assumption2) are relaxed. Assumption4 is inspired by a similar assumption in Juneja and Shahabuddin (2006).

,

An illustration of the conditions needed

for Theorem 6]

In Figure 4, the example set plotted in bold has

five dominating points in the set . The set locally satisfies

Assumption3 at each dominating point as required in

Assumption4(a). Assumption4(b) states

that the set as a whole lies inside the union of the half-spaces

defined by the tangent hyperplanes at each of the dominating points, as

shown by the light-shaded region. Also plotted is an example set

that satisfies Assumption4(a) but not

Assumption4(b) in the dark-shaded regions. So, the

requirement Assumption4(b) may be violated in practice

by sets like , but the regions where these happen are far from

the dominating points, and so it is reasonable to expect that the

relative error does not degrade too much. Thus, the uniqueness of

the dominating point (Assumption1) as well as the assumption about the separating hyperplane (Assumption2) are relaxed. Assumption4 is inspired by a similar assumption in Juneja and Shahabuddin (2006).

Theorem 6.

Suppose the set exists, and Let the -dimensional cost-scaled volume around (as defined in Assumption3) satisfy the expansion as . Further, let Assumption4 hold and let the form a probability mass function such that . Then, in the scaling regime, as ,

where the , the constants defined in Theorem 5, are calculated at each dominating point using the corresponding constants and .

Proof of Theorem 6:

Theorem 5(ii) will be applied to show the relative error result. Let represent, for each , an estimator centered at the dominating point to estimate . The ecoNORTA estimator is a mixture of estimators with mixing probabilities . Scaling the original set as preserves the key geometric requirements of Assumption 2 and 3. Denote by the likelihood ratio of the dimensional and the distribution of , and likewise as the likelihood ratio of the estimator restricted to the set . Split the second-moment of as (with )

Each set in the partition is non-empty given the structure of in Assumption 4(b). For any set in the partition, for any . The tightest bound for the th set in the partition is obtained by using the term. Thus, we get that

The final inequality follows by noting that . The penultimate inequality follows from Theorem 5(ii), which we can apply as per Assumption 4(a).

It can be shown that for the polynomial growth of relative error to be preserved for polynomial cost functions in the NORTA context, the implied cost function should be regularly varying (Resnick 1987). This can be expected to hold when the marginal distributions exhibit exponential tails, such as the exponential, gamma and phase-type distributions. Consider, for example, a NORTA vector having exponential marginals with rate for the -th component. Then, as , where and using the asymptotic as (Johnson et al. 1994). Thus, is regularly varying in .

This is however not the case for marginals with heavier than exponential tails. Consider a Pareto distribution , where the shape parameter . Then, as where again . Here, is super-exponential in .

We end this section by speculating that the estimator in could be replaced with the estimator , and or even the estimator , if it is (somehow) known that the needed structural conditions for and hold locally. For incorporating the estimator within , we will of course need to know the curvature information at each dominating point .

4.2 The ecoNORTA Algorithm for Implementing

The estimator proposed in Section 4.1 is usually unimplementable simply because the set of dominating points is unknown. A natural idea, however, is to estimate the set sequentially and use it within the expression (18), resulting in an “implementable" version of . The ecoNORTA algorithm, listed as Algorithm 1, provides details on the construction of such a sequential version of . The ecoNORTA algorithm, while simple in principle, has a number of heuristic steps introduced for enhanced and stable implementation. In what follows, we describe these steps.

The ecoNORTA algorithm is an iterative algorithm which, during each iteration , maintains an estimate of the dominating set , and a set that is best described as the set of “candidate" dominating points. The candidate set is chosen as the collection of a fixed number () of “nearest points" from amongst those feasible points generated by iteration . The ecoNORTA algorithm then repeats Steps 5 and 6 in Algorithm 1 a total of times during each iteration . In Step 5, mimicking the estimator given in (18), the current estimate of the dominating set is used to generate an observation from a multinomial mixture of Laplace distributions each of which is centered on the elements of . The random variate generated in Step 5 is then used to update the candidate set in Step 6. In Step 7, a clustering algorithm, e.g., Lloyd (1982), is used to identify at most clusters of points in the candidate set ; clusters that are too close in the sense that their centroids are within distance are merged into a single cluster. The maximum number of clusters and the minimum distance between clusters are both algorithm parameters. Points closest to the origin from each of the identified clusters in Step 7 are deemed dominating point estimates and added to the set in Step 8. As noted, the two steps 5 and 6 are repeated times during the -th iteration of ecoNORTA towards constructing a sequence of dominating set estimators . An initial estimate of can be obtained via Lemma 3, and the algorithm parameter is usually set to a convenient constant during implementation.

While the procedure in Algorithm 1 is expected to consistently estimate all the optimal solutions to , as a practical matter, the updating of the set stops when successive sets , change very little. The resulting dominating set estimate upon such termination is used in place of in (18) for constructing the ecoNORTA estimator.

![[Uncaptioned image]](/html/1607.01375/assets/x5.png)

It is important to note that Algorithm 1 is essentially a mechanism to make implementable, since the dominating set appearing in (18) is unknown. The problem of identifying the set of all points nearest to the origin, that is, all solutions to , is a deterministic global optimization problem. An extensive literature (Pardalos and Romeijn 2002) exists on solution approaches to such formulations, and any reasonable procedure, e.g., Gramacy et al. (2016), to seek all global optima can be used within Algorithm 1. A fuller analysis of this question takes us beyond the scope of this paper.

5 Numerical Experiments

In this section, we present a sampling of our fairly extensive numerical experience with the estimators presented in this paper. In Section 5.1 we present an example in the Gaussian context aimed at showcasing the power of the full-information estimator . The experiment in Section 5.1 is designed so as to allow the numerical computation of the exact value of in any number of dimensions. In Section 5.1, we compare against the partial-information estimator , the exponential-twisting estimator , and the acceptance-rejection estimator .

Section 5.2, which follows Section 5.1, illustrates the power of the ecoNORTA estimator throug a configure-to-order manufacturing system example. Since none of the other estimators are applicable in this context, the ecoNORTA estimator (as implemented via the ecoNORTA algorithm) is compared against the acceptance-rejection estimator

5.1 A Constrained Gaussian Experiment

Suppose that where is the standard Gaussian vector and where the positive-definite matrix for a strictly positive diagonal . Denote and . Setting and , we get

Let , where is the identity matrix. From (7), the optimal estimator for this example is

where is a shifted-exponential random variable with density , and following Theorem 4, the optimal intensity . The estimators , and follow the definitions (12), (3) and (2).

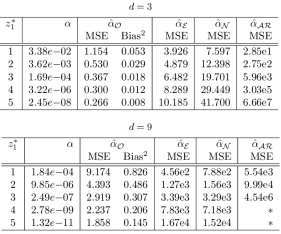

Table 2(a) displays numerically computed relative mean squared errors of the estimators , , , and for problem dimensions and , and for increasing values of the distance of the dominating point of from the origin. Recall that since the estimators , , and are unbiased, the relative mean squared error for each of these estimators is . Since the full-information estimator is biased, its relative mean squared error . Each cell in the table was computed with a sample size of . Although computing is generally intractable, the quadratic form of in this particular problem lets us numerically evaluate from a recursion, details of which are provided in Section 6.3.

As predicted by theory, and as can be seen in Table 2(a), the performance of the full-information estimator is dramatically better than the partial-information estimator and the exponential-twisting estimator . The difference becomes particularly pronounced for “harder" problems, e.g., in higher dimensions and for larger values of . As an example, in dimension and for , the mean squared error of the exponential-twisting estimator is about times larger than that of the full-information estimator . While we have reported results only for dimensions and , the performance of the full-infomration estimator appears to remain quite stable for much larger values, even though the corresponding calculation of values becomes numerically unstable.

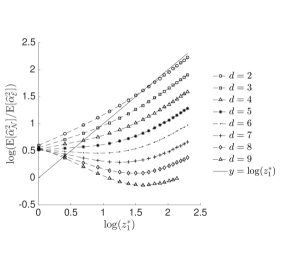

As can be seen from Table 2(a), the partial-information estimator does not perform nearly as well as although it seems to generally perform better than the exponential-twisting estimator and the acceptance-rejection estimator . Such performance is consistent with our asymptotic theory, as demonstrated by Figure 2(b) which plots the ratio of the mean squared error of the and estimators as grows. In each case, the ratio is seen to grow as , as predicted by Theorem 5 and Lemma 2. The asymptotics seem to take longer to “kick-in" as becomes larger.

5.2 A Constrained NORTA Experiment

Consider a CTO (Configure To Order) manufacturer that produces three products with uncertain demands for period , where is a NORTA-generated random vector i.i.d. over . Product 1 has a net margin much higher than those of products 2 and 3. These products share one critical component, which is procured only in a two-month replenishment cycle for reasons of economic scaling. Taking this into account, sales in the first period are managed to limit fulfilling and/or demand, so that the more profitable demand can be satisfied in the next period. In particular, the demand in set defined by these constraints are unmet:

| (19) | |||||

| (20) |

Inequality (19) arises from the per-unit consumption of the critical common component by the products. Constraints in (20) present upper bounds on and .

Demand is revealed at the beginning of each period, after which fulfillment decisions are taken. All demand for product 1 is filled, i.e. . In the first period, are optimally chosen to minimize the lost sales:

| (21) |

where and are the prices of products 2 and 3, respectively. Suppose . It is then straightforward to derive the optimal solution leading to

The sales department wishes to estimate the expected lost sales in the first period. Suppose and . The rareness of the set is then controlled by varying . The NORTA vector has marginal distributions . Two scenarios of correlations among are considered: (i) positive correlation with , and and (ii) negative correlation with , and .

For the above example, it seems clear that the structure of the image of the set in the Gaussian space is not easily deducible. Furthermore, neither the dominating set , nor its cardinality , are known. Such lack of adequate information leaves only the ecoNORTA estimator (via the ecoNORTA algorithm) and the acceptance-rejection estimator directly applicable. Accordingly, in what follows, we compare only these two estimators.

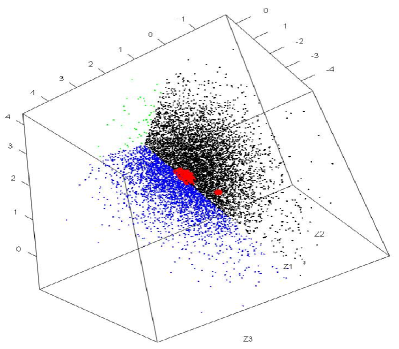

The set has one unique point closest to the origin, obtained by solving the quadratic program subject to constraints (19) and (20). The dominating set of estimated using Algorithm 1 starting from the -image of , illustrated in the Figures 4, is observed to cluster around a unique point, though far from the starting point. We set for all . Because of the stochastic nature of Algorithm 1, we repeat the experiment 1,000 times. Figures 4(c) and 4(d) illustrate the boundaries of the feasible region by plotting samples close to or on the boundaries. The green dots are samples close to or on the boundary specified by the constraint on the total consumption of the common component (19). The blue and black dots show the samples close to boundaries corresponding to the upper bounds on products 2 and 3 (20). The red dots correspond to the estimated dominating set found by Algorithm 1. We also mark the origin of the space using a single red dot. We observe that Algorithm 1 produced quite reliable estimates of . We also observe that samples are sparse in areas further away from the set . There is a rapid increase in the density of points close to the estimated dominating set , reflecting that Algorithm 1 converges quickly.

Figure 4 demonstrates how correlation patterns affect the locations of and the curvature of around . For the positive correlation case depicted in Figure 4(c), seems to be located at the corner where all three constrain surfaces intersect. In comparison, the negative correlation between product 1’s demand and the demands for products 2 and 3 shift away from the corner to a point on the ridge formed by the two constraint surfaces specifying the upper limits on product 2 and product 3. This is because the negative correlations mean that when demands for product 2 and 3 are higher than average in the first period, demand for product 1 is more likely to be lower than average. Consequently, it is more likely for the total consumption of the common components by products 2 and 3 to exceed the consumption by product 1, and thus satisfy constraint (19).

Using the estimated set , we compare the performance of against the acceptance-rejection estimator in Table 3. We experimented with four values that make range from to for the positive correlation scenario. As discussed previously, the negative correlation case has higher probabilities for these values. The estimator outperforms as expected. The performance of is affected by the curvature of at the dominating point. For instance, compare the negative correlation case with to the positive correlation case with . While the former has a smaller probability, the relative error is actually much smaller, due to the different curvature at the dominating point.

| Positive Correlation | Negative Correlation | |||||||

| 1.6300 | 1.7300 | 1.7607 | 1.771 | 1.6300 | 1.7300 | 1.7607 | 1.771 | |

| 1.00e-3 | 1.01e-4 | 1.02e-5 | 1.08e-6 | 9.81e-3 | 1.31e-3 | 2.01e-4 | 3.43e-5 | |

| 7.92e-4 | 8.75e-5 | 1.07e-5 | 1.23e-6 | 1.01e-2 | 1.56e-3 | 3.00e-4 | 6.38e-5 | |

| 986 | 9.81e3 | 1.17e5 | 1.37e6 | 1.01e2 | 7.74e2 | 5.04e3 | 2.86e4 | |

| 12.6 | 13.2 | 13.9 | 18.4 | 3.44 | 2.74 | 2.25 | 2.07 | |

| 1.56e3 | 1.56e4 | 1.89e5 | 3.27e6 | 1.56e2 | 1.11e3 | 6.67e3 | 3.53e4 | |

| 17.3 | 20.3 | 19.6 | 29.3 | 4.70 | 3.77 | 2.90 | 2.45 | |

References

- Asmussen and Glynn [2007] S. Asmussen and P. W. Glynn. Stochastic Simulation: Algorithms and Analysis. Springer, New York, NY., 2007.

- Barlow and Proschan [1987] R. E. Barlow and F. Proschan. Mathematical Theory of Reliability. Society for Industrial and Applied Mathematics, New York, NY., 1987.

- Billingsley [1995] P. Billingsley. Probability and Measure. Wiley, New York, NY., 1995.

- Boyd [2004] S. Boyd. Convex Optimization. Cambridge University Press, Cambridge, U.K., 2004.

- Cario and Nelson [1997] M. C. Cario and B. L. Nelson. Modeling and generating random vectors with arbitrary marginal distributions and correlation matrix. Technical report, Department of Industrial Engineering and Management Sciences, Northwestern University, Evanston, IL, 1997.

- Cario and Nelson [1998] M. C. Cario and B. L. Nelson. Numerical methods for fitting and simulating autoregressive-to-anything processes. INFORMS Journal on Computing, 10:72–81, 1998.

- DasGupta [2008] A. DasGupta. Asymptotic Theory of Statistics and Probability. Springer, New York, NY., 2008.

- DasGupta [2011] A. DasGupta. Probability for Statistics and Machine Learning. Springer, 2011.

- Dimitrov and Meyers [2010] N. B. Dimitrov and L. A. Meyers. Mathematical approaches to infectious disease prediction and control. INFORMS TutORials on Operations Research. INFORMS, 2010.

- Eubank et al. [2004] S. Eubank, H. Guclu, V. S. A. Kumar, M. V. Marathe, A. Srinivasan, Z Toroczkai, and N. Wang. Modelling disease outbreaks in realistic urban social networks. Nature, 429:180–184, 2004.

- Ghosh and Henderson [2003] S. Ghosh and S. G. Henderson. Behavior of the NORTA method for correlated random vector generation as the dimension increases. ACM TOMACS, 13(3):276–294, 2003.

- Glasserman [2004] P. Glasserman. Monte Carlo Methods in Financial Engineering. Springer, New York, NY., 2004.

- Glasserman and Liu [1996] P. Glasserman and T. -W. Liu. Rare-event simulation for multistage production-inventory systems. Management Science, 42(9):1292–1307, 1996.

- Gramacy et al. [2016] R. B. Gramacy, G. A. Gray, S. Le Digabel, H. K. H. Lee, P. Ranjan, G. Wells, and S. M. Wild. Modeling an augmented lagrangian for blackbox constrained optimization. Technometrics, 58(1):1–11, 2016.

- Johnson et al. [1994] N. L. Johnson, S. Kotz, and N. Balakrishnan. Continuous Univariate Distributions, volume 1. John Wiley & Sons, Inc., New York, NY., 1994.

- Juneja and Shahabuddin [2006] S. Juneja and P. Shahabuddin. Rare-event simulation techniques: An introduction and recent advances. In S. G. Henderson and B. L. Nelson, editors, Simulation, volume 13 of Handbooks in Operations Research and Management Science, pages 291–350. Elsevier, 2006.

- Kroese et al. [2011] D. P. Kroese, T. Taimre, and Z. I. Botev. Handbook of Monte Carlo Methods. Wiley, first edition, 2011.

- Leemis [2009] L. M. Leemis. Reliability: Probabilistic Models and Statistical Methods. Prentice Hall, United Kingdom, second edition, 2009.

- Lloyd [1982] S. Lloyd. Least squares quantization in PCM. IEEE Transactions on Information Theory, 28(2):129–137, Mar 1982.

- McNeil et al. [2005] A. J. McNeil, R. Frey, and P. Embrechts. Quantitative Risk Management: Concepts, Techniques and Tools. Princeton University Press, Princeton, NJ, 2005.

- Nelsen [2007] R. B. Nelsen. An Introduction to Copulas. Springer, New York, NY., 2007.

- Nelson [2013] B. L. Nelson. Foundations and Methods of Stochastic Simulation: A First Course. Springer, New York, NY., 2013.

- Pardalos and Romeijn [2002] P. M. Pardalos and H. E. Romeijn, editors. volume 2 of Handbook of Global Optimization. Kluwer Academic Publishers, 2002.

- Resnick [1987] S. Resnick. Extreme Values, Regular Variation, and Point Processes. Springer, New York, NY, 1987.

- Royden [1988] H. Royden. Real Analysis. Prentice Hall, New York, NY., 1988.

6 Appendix

Proof of Theorem 1: We first notice that satisfies the well-known asymptotic

| (22) |

as . The assertion in (a) follows upon noticing that and that as argued in Section 1.1.

To obtain the result in (b), write

| (23) |

and use the expression in (22). Finally, it is easily seen that the relative error is minimized by setting in the expression for . ∎

Proof of Theorem 3: Since is a random variable having the density and , we can write

| (24) |

where the last line follows from the application of Lebesgue’s dominated convergence theorem [Billingsley, 1995] and the definition of the gamma function.

To prove , we first see that

| (25) | ||||

| (26) |

where the last asymptotic equivalence (as ) follows from Lemma 1. We also recall, using the notation from (3.2), that

| (27) |

where as

| (28) |

We see that (28) implies that for given , there exists (not dependent on such that for all ,

| (29) |

Combining (25) and (27), we see that

| (30) |

Towards bounding appearing in (6), we use (29) to write for large enough that

| (31) |

where the last step follows from the application of Lemma1 and from the assertion of Theorem 2. To bound the second integral in (6), we note that

| (32) |

where the last step again follows from the application of Lemma1 and from the assertion of Theorem 2. From arguments in the proof of Theorem 2, we know that each summand in the expression for is giving us that as . This last observation along with (6) and (6), and observing that is arbitrary, proves the assertion in .

To prove , we notice after some algebra that

| (33) |

We know from the assertion in that the last term in (33) is . We also know from the assertion in and Theorem 2 that the first term in (33) converges to We conclude from these arguments that the assertion in holds. ∎

Proof of Lemma 5: The point represents the nearest point of the set to the origin along the axis. Recall the volume expansion defined in Assumption 3:

| (34) |

where , , the cross-section set , and the argument has been included for emphasis.

Part (i): For the translation regime , the set remains the same as , and the volume expansion follows 34. Theorem 2 gives us that

| (35) |

The second moment of is

Use the substitution , and apply Lemma1 (i) to get

Comparing against from (35) gives us the desired growth rate of the relative error of as:

Part (ii): The key step, as in the analysis above, is in characterizing the volume expansion for the scaled set . Using the observation that the cross-sectional set , substitute for , to get

where and are the parameters of the volume expansion of the original set as defined in 34. Thus, in this case follows from 35 as

| (37) |

The second moment on the other hand uses and so is

| (38) |

6.1 The Exponential-Twisting Estimator

How does the performance of the partial information estimators and compare to the exponential-twisting estimator ? The following result provides the answer.

Lemma 2.

Let estimate , where

and all . Let Then

Thus, for both the translation and scaling regime, the RE()/RE() with .

Proof of Lemma 2: We shall show (i), and the proof of (ii) follows similarly as in the proof of Lemma 3. The for the translation regime is given by 35, so we need to calculate the second moment of . Starting from the step 6 above:

where the second equality substitutes , the third substitutes , the fourth follows from applying the dominated convergence theorem and the last uses the gamma function definition. Comparing this with the gives us the desired result.

6.2 Properties of the NORTA Transformation

This section provides some structural properties of the set given as the pre-image of the feasible set under the NORTA transformation .

Lemma 3.

Suppose the constrained sets are defined as and , where each constraint is continuous in . Further, suppose the set is compact. Then:

-

(i)

is compact.

-

(ii)

The boundary of set maps to points on the boundary of .

-

(iii)

has an interior if is full-dimensional.

-

(iv)

Further, if is connected, then so is .

Proof of Lemma 3: Property (i) follows from the continuity and one-to-one onto nature of the maps and its inverse . For (ii), note that since is closed, there exist sequences in its complement that converge to , which map to sequences in . Further, these converge to and hence

For (iii), consider any point in the strict interior of . For any vector , there exists an such that For any vector , taking a Taylor approximation, the point satisfies for a sufficiently small , where has components , where the derivative exists and is non-zero everywhere because is continuous, strictly increasing and has a non-zero density.

In (iv), for any two points , there exists at least one path between them. By definition, the pre-image of points in are in . Further, since each point on a path is a limit of a sequence of points on the path, the image of the path is itself a path, giving us (iv).

6.3 Additional Examples

This section provides two examples. The first shows how the parameters can be estimated for sets with polynomial boundaries. The parameter is guessed based on the polynomial terms involved. The second example continues the Gaussian numerical experiment presented in Section 5.1 and provides additional details for the results presented.

Example 4.

Suppose that where is the standard trivariate normal and the set is given by Denoting , we see then that

| (39) |

where

upon making the substitution , . We thus see that as ,

Then, to calculate the exact rate at which as , we invoke Lemma 1 to obtain