Natural gas-fired power plants valuation and optimisation under Lévy copulas and regime-switching \author Nemat Safarov \\ Imperial College London\\ \\ Colin Atkinson\\ Imperial College London \\

Abstract

In this work we analyse a stochastic control problem for the valuation of a natural gas power station while taking into account operating characteristics. Both electricity and gas spot price processes exhibit mean-reverting spikes and Markov regime-switches. The Lévy regime-switching model incorporates the effects of demand-supply fluctuations in energy markets and abrupt economic disruptions or business cycles. We make use of skewed Lévy copulas to model the dependence risk of electricity and gas jumps. The corresponding HJB equation is the non-linear PIDE which is solved by an explicit finite difference method. The numerical approach gives us both the value of the plant and its optimal operating strategy depending on the gas and electricity prices, current temperature of the boiler and time. The surfaces of control strategies and contract values are obtained by implementing the numerical method for a particular example.

1 Introduction

The liberalisation of electricity and other energy markets, such as PJM in the United State, UKPX in the United Kingdom, Nord Pool in North Europe, and JEPX in Japan makes it necessary to incorporate highly volatile spot price dynamics into the optimisation problems for power generation.

During the traditional regulatory regime, the regulators used to set electricity prices based on cost of service. Investments in energy generating facilities were allowed to earn a fixed return through electricity tariffs upon approval by the regulators. The economic viability of such investments and value of power plants could be calculated via a discounted cash flow (DCF) method. But it has been shown that the DCF approach doesn’t give correct results as it ignores the opportunity costs (see Dixit and Pindyck [1994]). Meanwhile, the existence of competitive electricity markets necessitates the valuation of power plants by means of financial instruments. This kind of real option approach to electricity generation was proposed by Deng et al. [2001]. Deng and Oren [2003] further extend this work by including some physical operating constraints. Note that the omission of physical characteristics usually results in over-valuation.

The real options approach to power plant investment and optimisation problems has become an outstanding research area of different scientific groups. Pindyck [1993] applies this method to investigate the investment decisions to build a nuclear power plant. Tseng and Barz [2002] propose forward-moving Monte Carlo simulation with backward-moving dynamic programming technique to solve a multistage stochastic model used to evaluate a power plant with unit commitment constraints. Näsäkkälä and Fleten [2005] obtain a method to calculate thresholds for building a base load plant and upgrading it to a peak load plant when spark spread covers emission related costs. Takashima et al. [2007] investigate the investment problem for a power plant construction under the assumption that electricity prices are determined by the supply function and the equilibrium quantity.

Power generating assets can be classified as

-

•

Nuclear

-

•

Hydroelectric

-

•

Fossil

-

•

Renewable

In this work we will only consider fossil power stations. In general, a thermal power plant is a broader concept than fossil-fueled power generator. But we will use them interchangeably in this paper for simplicity purposes. Fossil power plants convert heat energy to electric power. More precisely, chemical energy in fossil fuels is first used to heat the water in the boiler. The resulting steam then spins the turbine which drives an electrical generator. The reader can refer to Wood and Wollenberg [2012] for more details regarding the operation of thermal power plants. Coal, natural gas and heating oil are the mostly used fuels for power generation. However, natural gas has become a primary fuel source for thermal power generators because of its low emissions and flexibility during peak hours. The main objective in operating a power plant is to maximise the profit by utilising the difference (or spread) between electricity and natural gas prices. So, the valuation of a gas-fired power plant is closely related to spark spread, which is the most important cross-commodity transaction in power markets and is presented by Deng et al. [2001] as

| (1) |

where and are electricity and gas spot prices, respectively. heat rate is the amount of gas required to generate 1 MWh of electricity which is defined by heat rate . It is a measure of efficiency. More precisely, the higher is the heat rate, the less efficient is the electricity generation. The heat rate has been usually assumed to be constant for convenience purposes (see Deng et al. [2001]; Benth and Kettler [2011]; Meyer-Brandis and Morgan [2014]).Deng and Oren [2003] generalise this approach by introducing an operating heat rate which changes depending on the discrete output levels. Thompson et al. [2004] consider the case where is the amount of natural gas that needs to be burned to maximise the total revenue from electricity generation. In this model depends continuously on time, boiler temperature, gas and electricity prices and is calculated via dynamic optimisation techniques.

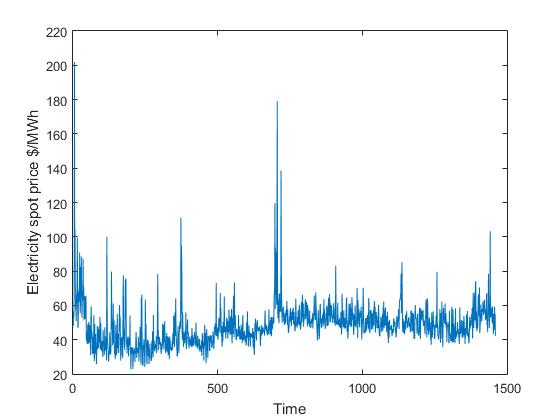

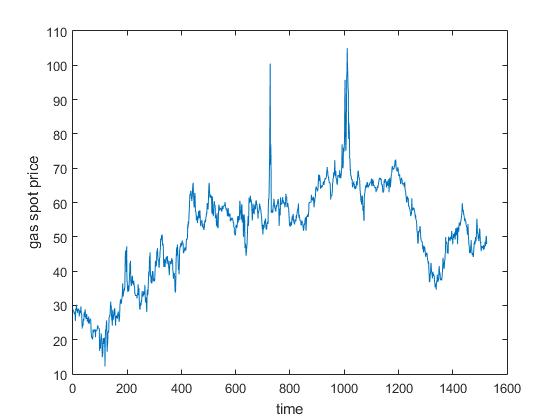

The evaluation of a power plant cannot deliver satisfactory results without realistic stochastic models for underlying spot prices (see Fig 1). The detailed discussion of the related literature was presented in Safarov and Atkinson [2016]. For completeness purposes we will briefly repeat them here.

A mean-reverting process is a common model for the energy spot price. For example, Schwartz [1997] presented three mean reverting models for commodity spot prices while assuming that stochastic convenience yield and interest rates also mean revert. Boogert and De Jong [2008] used the Least Square Monte Carlo method (initially proposed by Longstaff and Schwartz [2001] for American options) for gas storage valuation, while assuming the following one factor model for the spot price, which is calibrated to the initial futures curve:

| (2) |

where is a standard Brownian motion, is a time-dependent parameter, calibrated to the initial futures curve , provided by the market; the mean reversion parameter and the volatility are positive constants. One factor models are popular because of their simplicity. As is stated in Bjerksund et al. [2008]; Henaff et al. [2013], it’s unrealistic to assume that one factor models can capture all characteristics of highly volatile power or natural gas prices. Parsons [2013] extended eq. (2) to the two-factor mean-reverting model where the long-term mean is also a mean-reverting process. Boogert and de Jong [2011] extended the application of the Least Square Monte Carlo method to multi-factor spot processes.

The unstorability of electricity in large quantities and storage complexities of natural gas create frequent demand-supply fluctuations in the corresponding commodity markets. These disruptions lead to the spiky behavior of energy spot prices. Therefore, price spikes have to be included in our spot price models as they carry out significant arbitrage opportunities.

However, none of the models described above exhibit spiky instantaneous jumps of energy prices. Thompson et al. [2004, 2009] propose to model the risk adjusted power and natural spot prices, respectively by the following one dimensional continuous time Markov process:

| (3) |

where , and the ’s are any arbitrary functions and the ’s are arbitrary jump sizes with distributions . and ’s denote the standard Brownian motion and Poisson processes respectively. Eq. (3) covers a wide range of spot price models for natural gas and is tractable for numerical calculations. However, its jump component isn’t appropriate to represent instant and mean-reverting spikes.

Benth et al. [2007] propose a more realistic alternative by defining energy spot dynamics as a sum of Ornstein-Uhlenbeck (OU) processes with different mean-reverting speeds. The only sources of randomness of the spot prices are positive pure jump processes. The additive structure of the model makes it difficult to derive futures curves. Therefore, Benth [2011] considers a stochastic volatility model by Barndorff-Nielsen and Shephard [2001] for equity markets in the context of energy commodities. Benth et al. [2013] generalise this non-Gaussian approach to a multivariate case to model the dynamics of cross-commodity spot prices.

The volatile behaviour of energy prices can differ significantly between cold and warm months. Benth et al. [2008] make use of time-inhomogeneous jump processes to capture these seasonality effects by introducing geometric and arithmetic spot price dynamics in the following way:

| (4) | ||||

| and | ||||

| (5) | ||||

| where | ||||

| (6) | ||||

| (7) | ||||

for and . Here and are independent standard Brownian motions and independent time-inhomogeneous Lévy processes, respectively. is a deterministic, positive and continuously differentiable seasonality function, while the coefficients and are continuous functions of t.

In Safarov and Atkinson [2016] we investigated the optimal operation problem for gas storage based on the geometric model. But for the optimisation of gas-fired power plant we will follow the arithmetic dynamics based on the justification presented in Benth et al. [2008]; Meyer-Brandis and Morgan [2014].

Accurate valuation of power plants is impossible without the analysis of the multivariate dependence between electricity and gas prices. For Gaussian OU components it suffices to specify the appropriate covariance matrix. This approach is not useful when we consider non-Gaussian spot price models. Therefore Meyer-Brandis and Morgan [2014] proposed to make use of Lévy copulas to model the dependence between the non-Gaussian OU components of electricity and gas spot prices. Although Thompson et al. [2004] develop a comprehensive stochastic control model which incorporates all the necessary operational constraints, the dependence of non-Gaussian jump components is assumed to be independent. In the actual calculations the gas prices are even assumed to be constant which is unlikely to be true under unregulated markets.

An alternative approach is the regime-switching framework initially proposed by Hamilton [1990]. In a regime-switching model the price process can randomly shift between several regimes due to long-term demand-supply fluctuations, political instability, weather changes and other reasons. The spot price follows a distinct stochastic process within each regime. Carmona and Ludkovski [2010] and Chen† and Forsyth [2010] apply a regime-switching approach to investigate stochastic control problems related to natural gas storage and implement the numerical calculation via Monte Carlo and finite difference methods, respectively. However, there is a lack of research related to the valuation of a power plant or spark-spread option under regime-switching models.

In this paper we investigate the valuation and optimal operation of gas-fired power generating facilities and refer to Thompson et al. [2004]for the physical operational constraints. But we assume that the underlying electricity and gas spot prices follow the Lévy regime-switching model. More precisely, at each regime the spot dynamics is defined by a special case of an arithmetic model (7). For the dependence of gas and electricity spikes we make use of skewed Lévy copulas for the reasons stated in Meyer-Brandis and Morgan [2014]. Therefore, our approach not only incorporates the most important physical characteristics of a power plant but also takes into account short-term demand-supply variations and long-term economic disruptions.

We assume that the reader is familiar with fundamentals of the theory of Lévy processes, as presented for example in Cont and Tankov [2003], Schoutens [2003] and Kyprianou [2006].

To solve this stochastic control problem we employ the dynamic programming theory which gives us coupled Hamilton-Jacobi-Bellman (HJB) equations. We then solve this system of nonlinear partial integro-differential equations (PIDE) numerically.

2 Natural gas and electricity spot prices without regime-switching

Let be our complete filtered probability space. We assume that the underlying spot prices follow the arithmetic model defined by eqs. (5) to (7). For simplicity, we take . We also define the initial condition

Then we have the following dynamics for :

| (8) | ||||

| where | ||||

| (9) | ||||

| (10) | ||||

We further assume that the coefficients of eqs. (9) and(10) are constants such that and . Then the dynamics of electricity spot prices is given by

| (11) | ||||

| where | ||||

| (12) | ||||

| (13) | ||||

The underlying natural gas spot price follows the similar model:

| (14) | ||||

| where | ||||

| (15) | ||||

| (16) | ||||

Note that we could take unequal mean-reversion rates for normal variations and jumps in our spot price models following Safarov and Atkinson [2016]. But that would increase the dimension of our HJB equation which is derived in section 3. We keep them equal to reduce the computational time.

In general, and can be subordinator Lévy processes

where and are Poisson random measures with the corresponding Lévy intensity measures and (see Jacod and Shiryaev [2013]). These jump measures have positive supports because we only consider upward price spikes. Following Meyer-Brandis and Morgan [2014] we further assume that and are compound Poisson processes with intensities and and jump size distributions and , respectively. In other words,

The complete characterisation of the two-dimensional model requires the specification of the dependence risk between the spot prices and . We can separate this problem in defining the multivariate distributions of and . The former issue can be easily resolved by determining the correlation parameter between and

To specify the dependence between power and gas spot prices we will refer to Meyer-Brandis and Morgan [2014] for using positive Lévy copulas. This concept will be analysed in section 4.

Before moving to the optimisation problem of a power plant we can write the electricity and gas spot price models in a more convenient SDE form as follows:

| (17) |

where Similarly, we can derive the SDE for the gas spot price

| (18) |

Note that we can get the compensated compound Poisson processes and as follows:

3 Optimal control of power generation

The theoretical framework and physical constraints for the optimal operation of a gas-fired power generator will be based on Thompson et al. [2004]. Therefore, the following physical characteristics need to be incorporated in our optimisation model:

-

•

The minimum generation temperature: The plant cannot operate below a certain temperature.

-

•

Variable start-up times: The time required to heat the boiler to its minimum generation level depends on the heat rate of natural gas and the current temperature.

-

•

The variable output rates: The efficiency of the plant varies non-linearly with the amount of generated electricity.

-

•

The variable start-up and production costs. Increase of electricity output is achieved by raising the boiler temperature. The fuel used for this heat increase does not generate any additional power.

-

•

Control response time lags: Changing boiler temperature takes some time. Therefore, any decision to alter the power output will take effect after a reasonable amount of time.

-

•

The ramp rate limit: This is the minimum amount of time required for switching a unit on/off to avoid thermal stress and fatigue.

Following Thompson et al. [2004] we model the boiler temperature as a state variable and incorporate all these operational constraints in its mean-reverting equation

| (21) |

where is the variable controlling the amount of gas consumed per instant in time; is the equilibrium temperature of the generator depending on ; is a mean-reverting speed function specific to each power plant.

The non-linear dependence of the amount of produced electricity on the boiler temperature is given by the output function . We can now move to our stochastic control problem for the power plant.

The objective of the optimisation is to find a control variable that maximises the expected future cash flow up to maturity time and discounted at a rate

| (22) |

subject to

The minimum and maximum bounds on are necessary to avoid thermal stresses.

Rewriting (22) in a similar way to Thompson et al. [2004] will lead to the Bellman equation:

We can now apply the multidimensional Itô’s formula (see Cont and Tankov [2003]) to to expand it above in Taylor’s series:

| (23) |

where is a two-dimensional Poisson random measure with Lévy intensity measure and

We then denote

| and | ||||

for clarity purposes. After substituting eqs. (19) to (21) and (3) in eq. (23) we obtain

| (24) |

Elimination of all terms that go to zero faster than dt and some further simplifications similar to Safarov and Atkinson [2016] results in the following HJB equation

Note that the control variable only appears in the last two terms. We also need to introduce time to maturity . Then HJB equation above becomes

| (25) |

where

In other words, the maximisation problem reduces to

| (26) |

After the calculation of the optimal strategy we substitute it in eq. (25) to get

| (27) |

Thus, once the optimal control is known, the nonlinear HJB equation simplifies to linear PIDE. Before starting our numerical approach to solve eq. (27), we analyse the two-dimensional Lévy measure by means of Lévy copulas in the next section.

4 Lévy copula

Before starting the analysis of the dependence of we need to go through some brief introduction on Lévy copulas. We will refer to Cont and Tankov [2003]; Kallsen and Tankov [2006] for the detailed background on this concept. We will mainly use the following key results in our investigation:

Theorem 4.1

(Sklar’s Theorem for Lévy copulas) Let be a two-dimensional Lévy process with positive jumps that have tail integral and marginal tail integrals and . Then there exists a unique positive Lévy copula such that:

| (28) |

Conversely, if is a positive Lévy copula, and are one-dimensional Lévy processes with tail integrals , then there exists a two-dimensional Lévy process such that its tail integral is given by eq. (28).

An Archimedean Lévy copula is a popular parametric Lévy copula defined as

where is a strictly decreasing convex function with positive support such that and . In these models is always assumed to have the symmetry property . However Meyer-Brandis and Morgan [2014] argue that this symmetry property is not supported by the data. Therefore they introduce skewed Archimedean Lévy copulas as follows

where and are decreasing functions satisfying , while is the same as above. In our calculations we will use the skewed Clayton- Lévy copula where

for and . More precisely,

| (29) |

We can construct multivariate jump densities from univariate ones by using Lévy copulas. The following is the two-dimensional version of the Lemma proposed by Reich et al. [2010].

Lemma 4.2

Let be a bounded function vanishing on a neighbourhood of the origin. Moreover, let be a two-dimensional Lévy process with Lévy measure , Lévy copula , and marginal Lévy measures and . Then

| (30) |

We can now make use of this Lévy copula techniques to break the double integral term in eq. (27) into parts that can be calculated via standard numerical integration techniques. First of all, let’s denote the integrand as follows to reduce the size of calculations

| (31) |

for fixed and . The application of Lemma 4.2 to the integral term in eq. (27) results in

| (32) |

By taking the partial derivatives of in eq. (31) we obtain

| (33) | ||||

5 Boundary conditions

The terminal condition for our power plant valuation is assumed to be

| (36) |

where . Based on Thompson et al. [2004]; Safarov and Atkinson [2016] we choose the following limits as the boundary conditions:

| (37) |

The domain of the HJB equation (34) is But we need bounded domain for numerical calculations. So we need to restrict this unbounded domain to . Hence, for the case we apply and to simplify eq. (34) to

For the case we employ the first line of (37) again to get

We can obtain the boundary conditions for the limits and in a similar way. To conclude our analysis of boundary conditions we need to construct the equations corresponding to 4 corner points: , , and . For the first two corners we have

and

Similarly, we can derive the equations for the other two corners.

6 Discretisation scheme

and are finite activity Lévy processes where and . Therefore, we can rewrite the single integral terms of eq. (34) as

| (38) |

and

| (39) |

If we substitute eqs. (38) and (39) in eq. (34) the coefficients of partial derivatives and modify to

and the HJB equation (34) can be written as

| (40) |

where

| and | ||||

Note that we dropped the bar signs from our coefficients and for simplicity. We will apply the explicit finite difference scheme proposed in Cont and Voltchkova [2005a, b] to deal with the diffusion and single integral terms and . The discretisation of and optimisation terms requires further analysis.

First of all, we need to discretise the domain of the HJB equation by the following grid:

So, is the exact solution of the eq. (34) at the node , while stands for the approximate solution at the same node.

For the diffusion/PDE part we follow the steps discussed in Safarov and Atkinson [2016] use the explicit method discussed in Safarov and Atkinson [2016] and apply similar corrector term to get rid off the monotonicity issue. In other words,

| (41) |

assuming that and . We will use the downwind scheme for the cases and .

For the integral terms and we first need to restrict the unbounded integration domains by setting finite upper bounds and to truncate the larger jumps. We employ the trapezoidal quadrature method in order to get the numerical approximations for these integrals and take and . We also choose positive integers and such that and , respectively. By using the central difference discretisation for the partial derivatives and we get

| (42) |

and

| (43) |

where

We can now go through the numerical calculation of the double integral

First of all, denote for clarity purposes. Then apply the central difference formula to approximate the cross-derivative at the node :

By taking the double integral of both sides above we get

| (44) |

Thus, we need to integrate 4 terms over in eq. (44) in order to evaluate . For this purpose we will make use of two-dimensional trapezoidal rule explained below (see Davis and Rabinowitz [2007]).

Let be given over the rectangle . Assume that the intervals and are equally subdivided into and subintervals with widths and , respectively. The sample points and are defined as and where and . Then the two-dimensional trapezoidal rule can be formulated as follows

where

We apply this integration rule to approximate the four terms on the right hand side (RHS) of eq. (44). Let’s first consider the first term

This is a two-dimensional function depending on and . So, we can apply the 2d trapezoidal rule to get

We can similarly calculate the other three terms.

Hence, after denoting the approximate value of by our explicit scheme becomes

| (45) |

where and are discretisation operators corresponding to and , respectively. Note that when we will discretise by .

We know from the initial condition that . So, starting from time we first solve the maximization problem

then substitute this optimal strategy in (45) to get

| (46) |

where .

7 Hypothetical gas-fired power plant example

As we mentioned earlier, we want to model the power output as a function of heat . We specifically refer to Thompson et al. [2004] in assuming

Hence, the minimum and maximum operating temperatures for electricity generation are C and C, respectively which correspond to 150 MW and 400 MW output levels. As we are dealing with a dynamic model, we also need the equilibrium temperature for the boiler that depends on the amount of burned gas :

where . By assuming in eq. (21) we get the following dynamics for the temperature

| (47) |

where . We then impose a ramp rate restriction

proposed by Thompson et al. [2004]. If we combine this restriction with (47), we can update the lower and upper boundaries for the control variable in the following way

| where | ||||

Note the discontinuity of at causes some oscillation problems related to the discretisation of the partial derivative . with the smothness of solutions. We will follow Thompson et al. [2004] in making use of minmod slope limiters to get rid off this smoothness issue. The detailed explanation regarding slope or flux limiters is provided by LeVeque and Leveque [1992].

7.1 Slope limiter

The following calculations do not affect the diffusion and integration parts of the eq. (34). Therefore, we can omit them in order to simplify our PIDE to

| (48) |

If we denote in eq. (48) then we can see that

| (49) |

is an advection equation with variable speed . According to eq. (46), we find before applying explicit scheme to discretise (49). Therefore, we can extend the MUSCL scheme (Monotonic Upwind-Centered Scheme for Conservation Laws) for advection equations with constant speed to cover eq. (49) as well. So,

| (50) |

where and

is some slope that needs to be defined in order to reduce the numerical oscillations. The oscillations in a solution are measured by the total variation (TV) of :

The increase of TV leads to the development of oscillations in a solution. Therefore, a numerical method is total variation diminishing (TVD) if

We need to limit the slope of the MUSCL scheme to make it TVD. One of such ways is the minmod slope limiter:

| where | ||||

Thus, after improving the numerical algorithm (46) via the minmod slope limiter technique, we can get benefit from the accuracy of second order differencing scheme while avoiding numerical oscillations.

7.2 Numerical results

We first consider the framework similar to the one presented in Thompson et al. [2004]. More precisely, we assume that the natural gas spot price is constant and the input parameters are

Moreover, power spot price jump sizes are normally distributed, . The deterministic seasonality function is given as

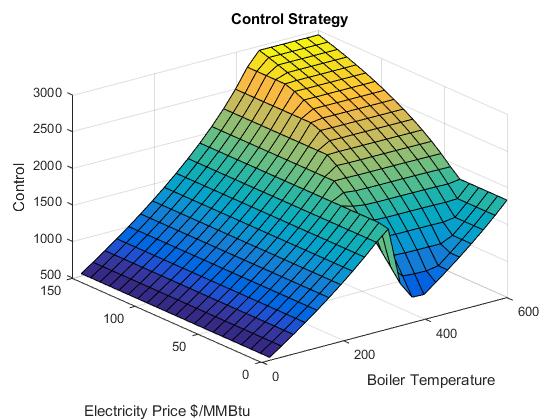

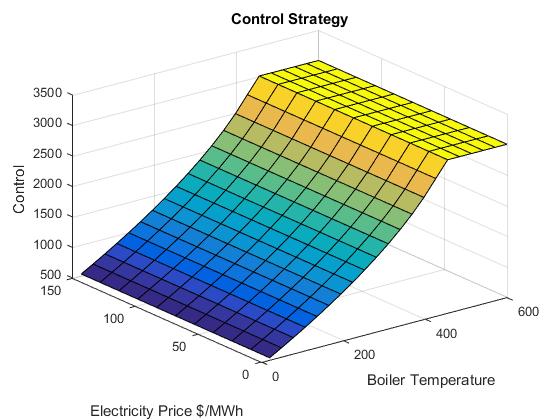

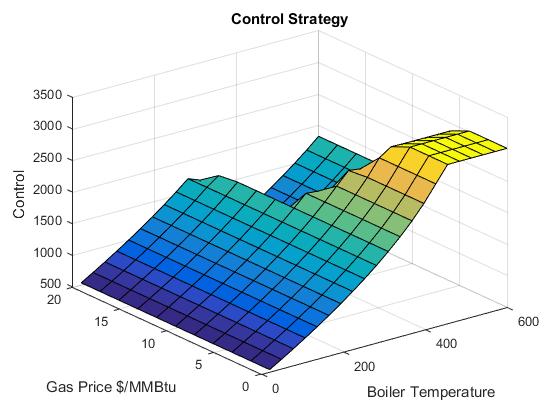

The optimal operating strategy surface for the gas-fired power plant is presented in Figure 2. For boiler temperatures below 300∘C the optimal strategy is to burn maximum amount of fuel within physical limitations in order to keep the plant on line. For low electricity spot prices gas consumption decreases when the temperature is above the minimum operation level to minimise the cost. But for higher power prices the optimal control of gas consumption increases nonlinearly w.r.t. spot prices and temperature. We can see from Figure 2 that in the case of low electricity spot prices the power plant burns more fuel for very high temperatures. This strategy is explained by the ramp rate restriction. In other words, we can’t shut down the plant immediately when the boiler is close to its maximum temperature limit. It will take some time for the unit to cool and we have to burn the required amount of gas during that time period.

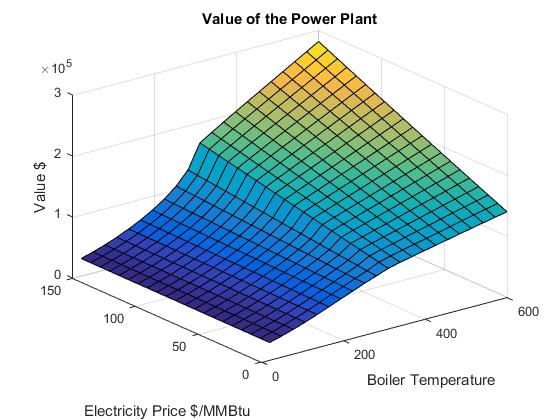

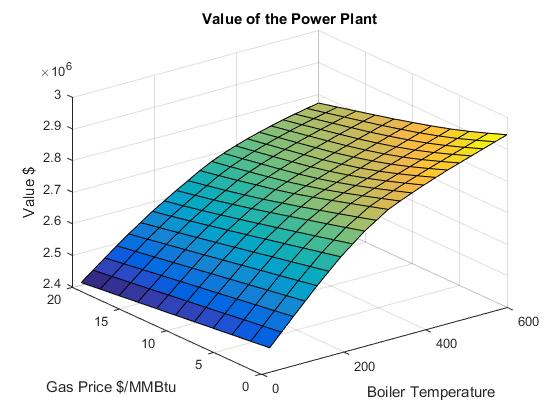

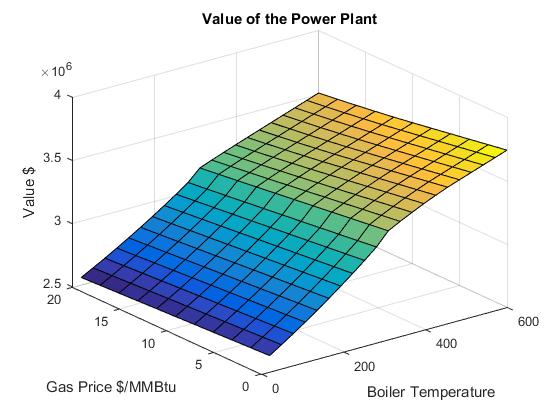

The Figure 3 shows the value or expected cash flow surface of power generating facility. We can see that the value surface does not depend on electricity spot prices when the boiler temperature is below the operating level. The plant is not reacting to spot price changes because there is no guarantee that by the time we increase the temperature to 300∘C spot prices will remain the same. Beyond 300∘C the plant starts to generate electricity which explains the non-smooth behaviour of the value surface at . Beyond this line both higher power prices and boiler temperatures contribute to larger values of the power generator.

Thus, our optimal control and value surfaces look similar to the figures given by Thompson et al. [2004]. Unfortunately, we can’t conduct more accurate comparison due to some missing parameter specifications in the original paper.

We can now investigate the numerical calculations for the underlying spot price models (11) and (14). The parameters for our single regime model are given in Table 1.

| Parameter | Value | Parameter | Value |

|---|---|---|---|

| .1 | .1 | ||

| .23 | .4 | ||

| .11 | 200 hours | ||

| .09 | .15 |

We assume that the risk-free interest rate is the same, . As the jump size distributions and we take inverse Gaussian distributions where and are mean and shape parameters, respectively. We can use the parameter values and for the corresponding distributions of power and gas price jumps.

Meanwhile, the deterministic seasonality terms and will be defined as follows

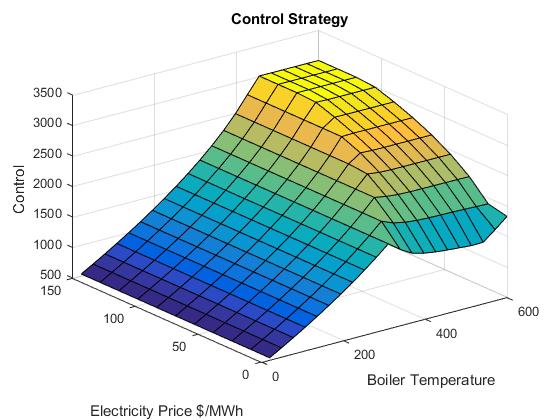

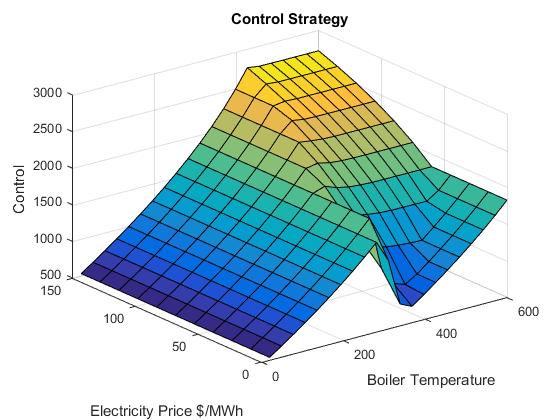

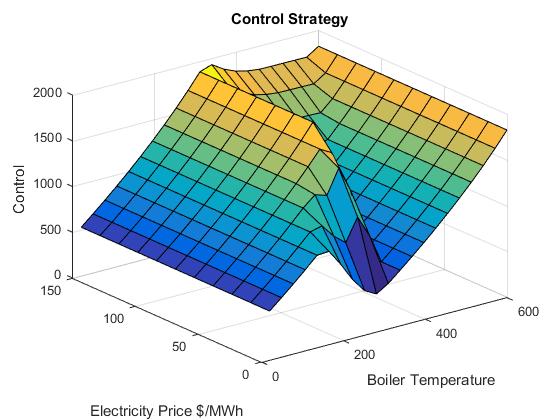

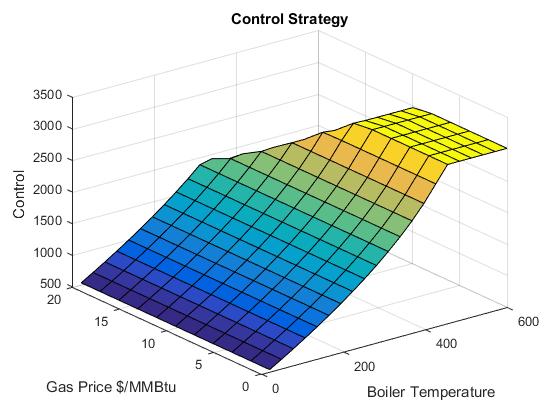

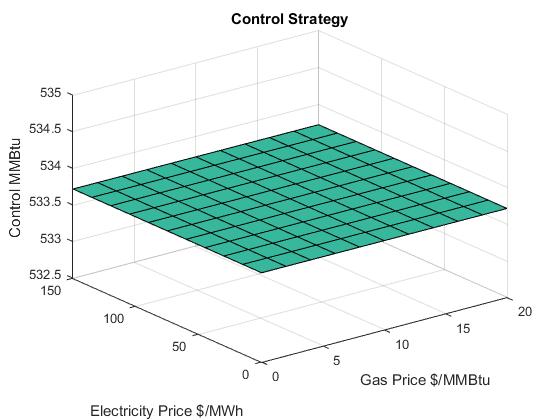

Figure 4 compares optimal operating surfaces w.r.t. power prices and boiler temperature for various gas spot prices. When , the generation costs are so small that the plant burns gas as much as possible at all levels of power prices and temperatures (Figure 4(a)). Figure 4(b) depicts the case when $/MMBtu. We can see that the surface looks more like in 2. For higher levels of natural gas spot prices the region of intensive fuel consumption diminishes (Figure 4(c) and 4(d)).

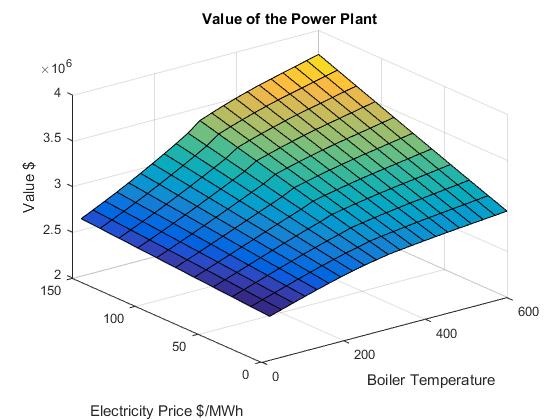

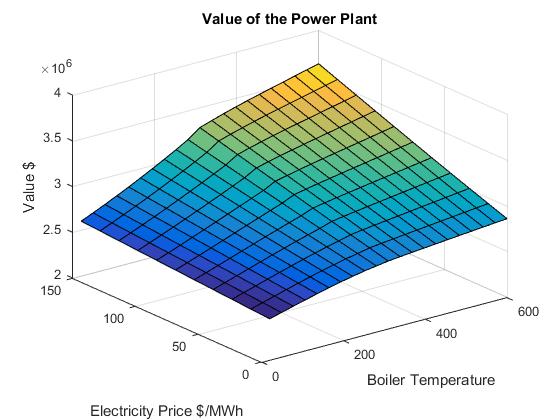

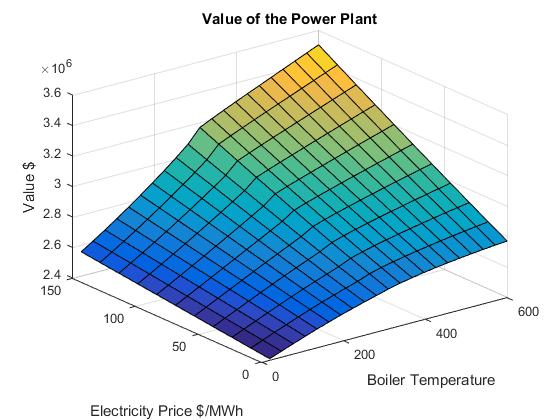

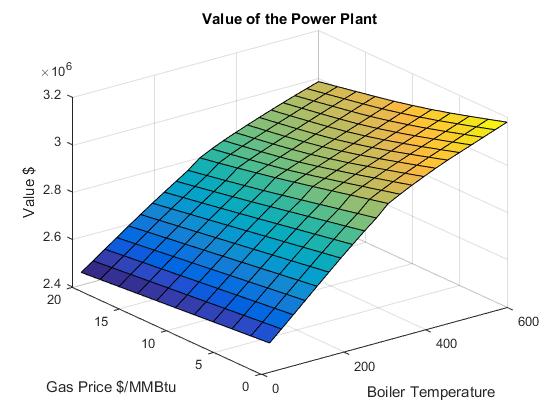

Value surfaces w.r.t. power spot price and boiler temperature for different gas prices are depicted in Figure 5. The shapes of these surfaces are almost the same. As gas prices increase, the surfaces shift downwards. But when is too high, the power plant value becomes dependant on power spot prices even for low temperature levels (Figure 5(c)).

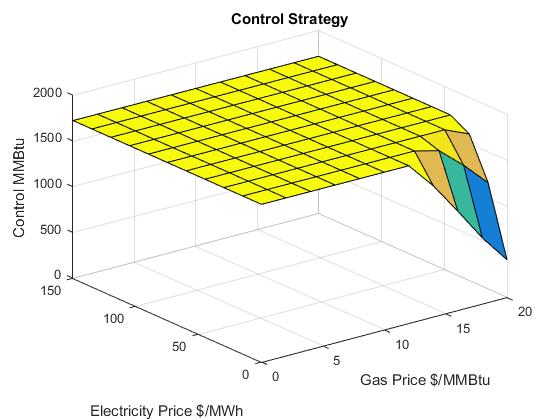

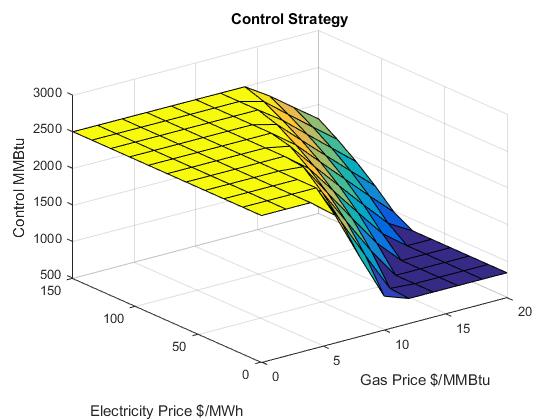

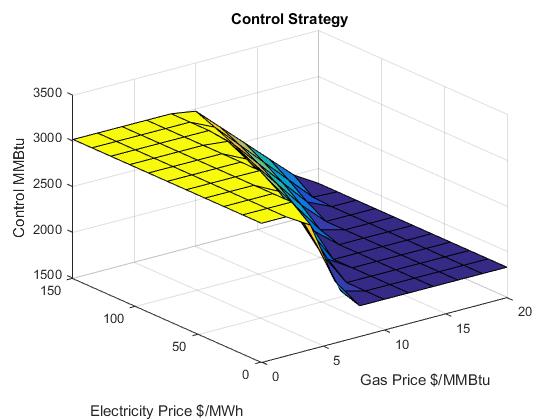

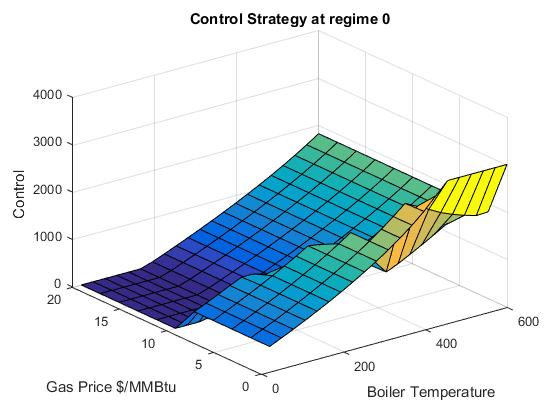

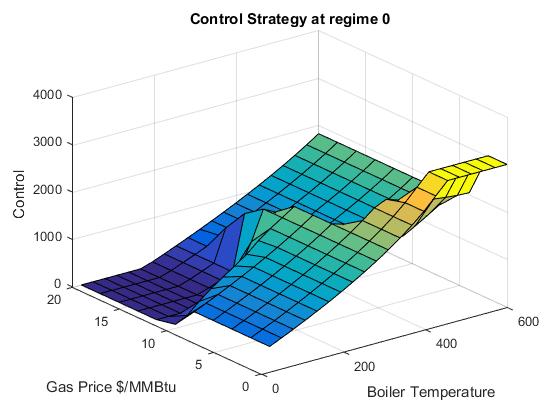

In Figure 6 we can observe optimal control and corresponding value surfaces w.r.t. gas spot price and boiler temperature for different electricity prices. Figures (a)-(c) imply that the higher is , the larger is the maximum consumption region. For very low values of electricity the plant minimises its fuel cost even before reaching 300∘C. But when the power prices are too high the plant can keep burning gas at full capacity beyond 300∘C as well. Running the plant in the presence of extremely expensive fuel prices when the boiler temperature is too high becomes unbearable. Therefore, the optimal strategy is to reduce gas consumption to minimum.

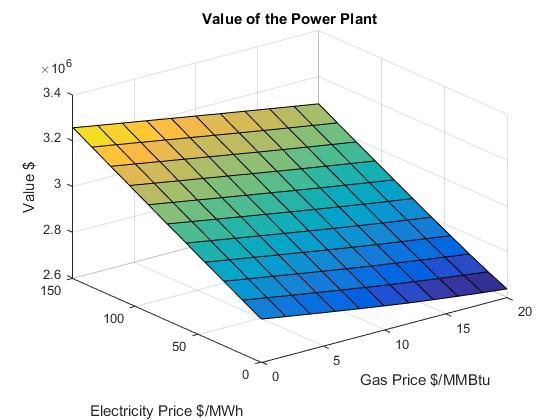

We can see from Figures 6(d)-(f) that value surfaces shift upwards when increases. Meanwhile, the value surface doesn’t exhibits a sharpe change in C when power prices are too low. In this case the surface becomes dependent on gas prices for boiler temperatures below the operating level. This dependence vanishes away for higher values of .

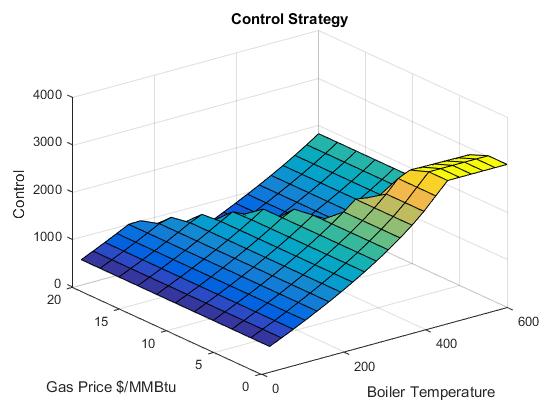

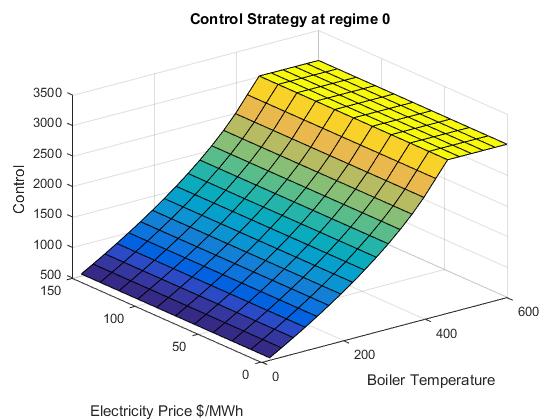

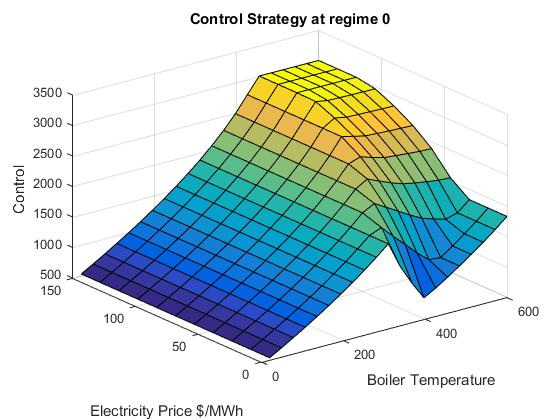

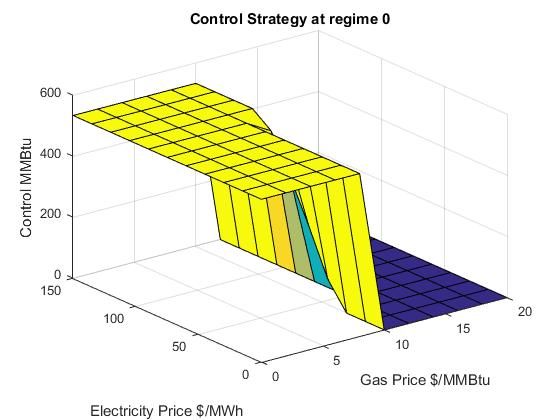

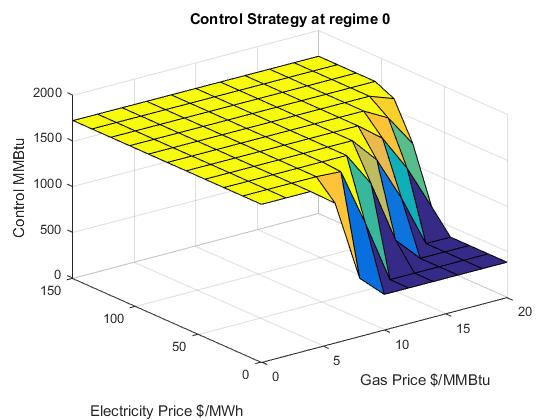

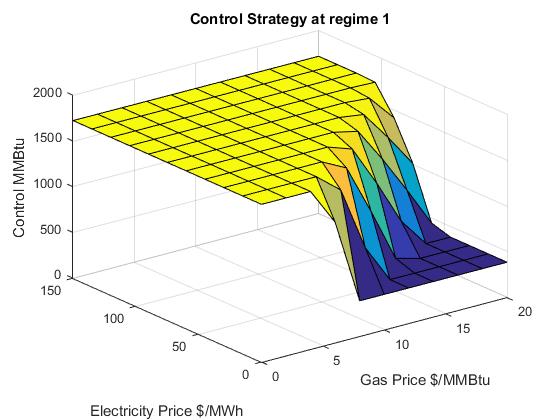

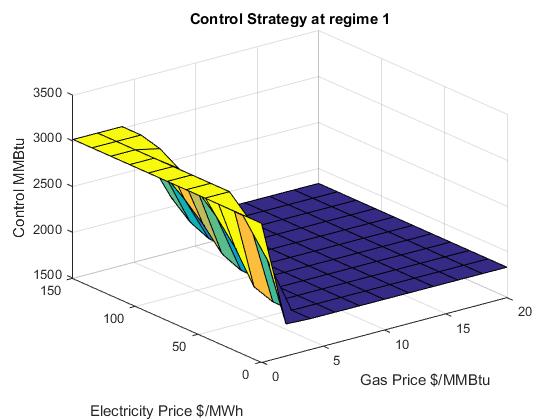

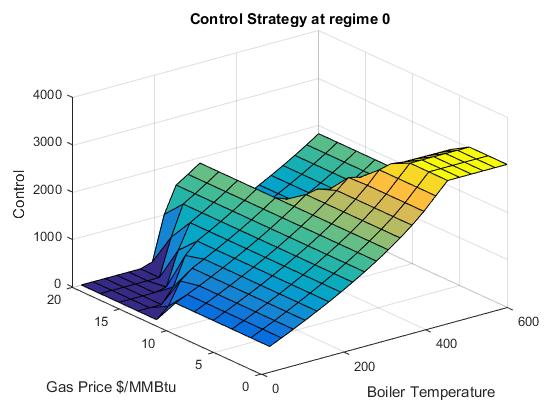

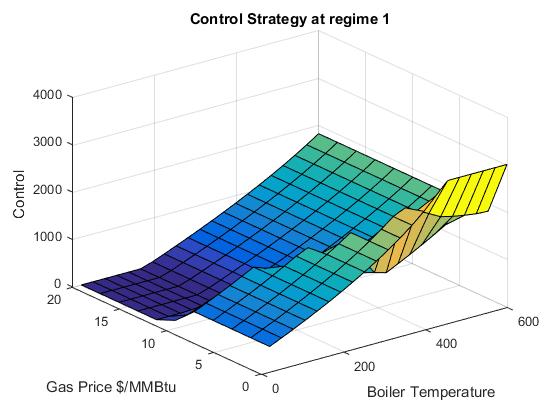

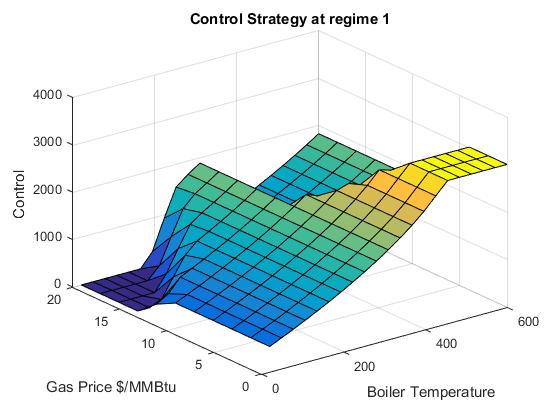

The operating strategies w.r.t. electricity and gas spot prices for different boiler temperatures are depicted in Figure 7. For very low boiler temperatures the control strategy surface is flat. In other words, it doesn’t change depending on underlying spot prices. Starting from the case C we notice a small region of dependence on power and gas spot prices. For higher temperature levels we can see that dependence more clearly (Figures 7(c) and 7(d)).

We can differentiate 3 different regions here: (dark blue), (yellow), and (in between).

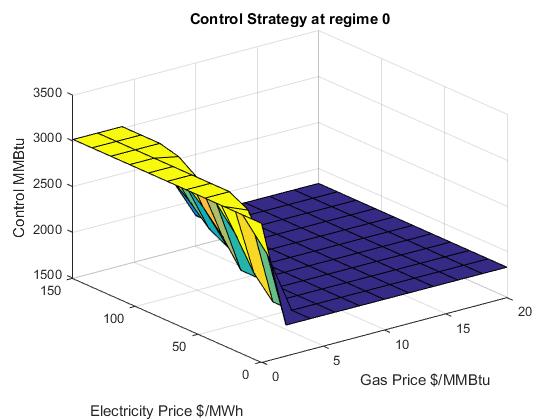

Figure 8 describes the power generator value surface w.r.t. electricity and gas spot prices when C. The value surface exhibits increasing and decreasing dependence on power and natural gas spot prices, respectively. The overall shape of the surface is the same for other temperature levels as well.

8 Regime-switching

Let’s assume the economy has two phases/regimes (0 and 1) and the switch has some finite probabilities: and . We will model this regime switching by the following two state continuous-time Markov chain presented by Chen† and Forsyth [2010]:

| (51) |

where is the time infinitesimally before , and are independent Poisson processes with intensities and ,respectively. So, within a regime the underlying electricity and gas spot prices follow:

| (52) | ||||

| where | ||||

and

| (53) | ||||

| where | ||||

where and are Lévy processes with intensity measures and , respectively. In our compound Poisson case we have

We can rewrite our power plant optimisation objective (22) for each regime as follows

| (54) |

subject to

The application of previously used techniques, such as Bellman’s Principle of Optimality and Itô’s Lemma will give us the following coupled HJB equations

| (55) |

with the terminal condition

The boundary conditions at each regime will be the same as in Section 5.

8.1 Numerical results

We first need to define our input parameters for the regime switching model. We adopt the parameter values introduced in Section 7.2 for regime 0. Analogously, we make the following assumptions for regime 1 (see Table 2).

| Parameter | Value | Parameter | Value |

|---|---|---|---|

| .6 | .2 | ||

| 1 | .6 | ||

| .2 | 200 hours | ||

| .3 | .15 |

We assume that the risk-free interest rate is the same, . As the jump size distributions and we again take inverse Gaussian distributions with parameters and , respectively.

The seasonality terms and will be assumed to be

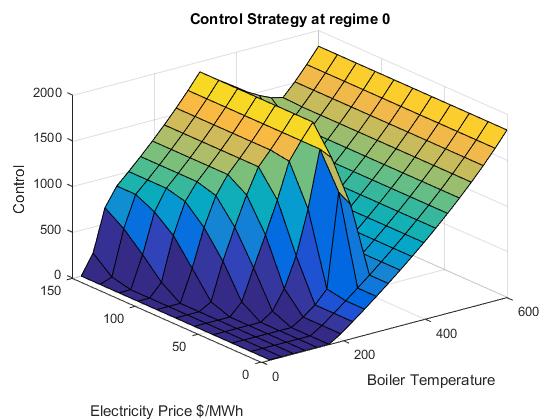

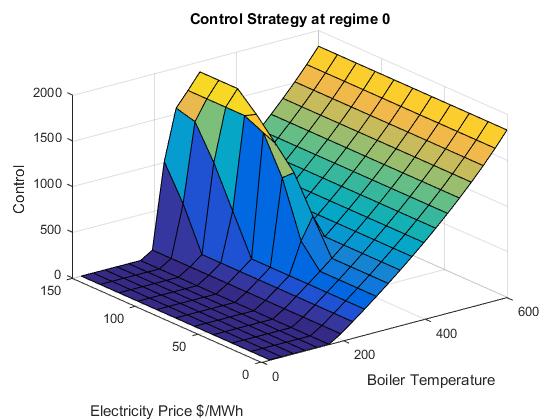

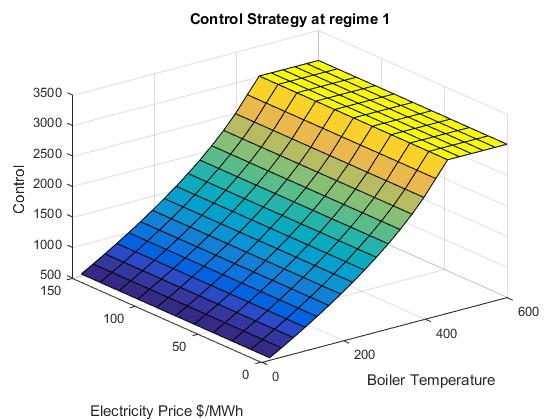

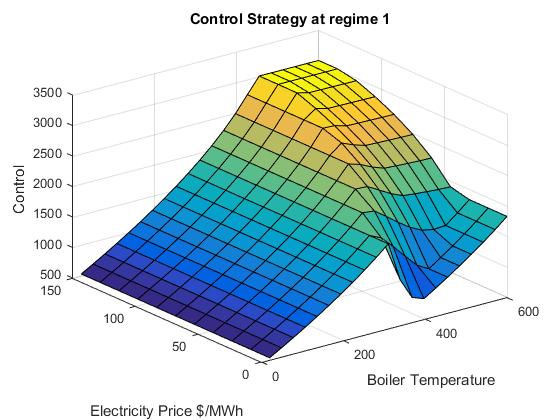

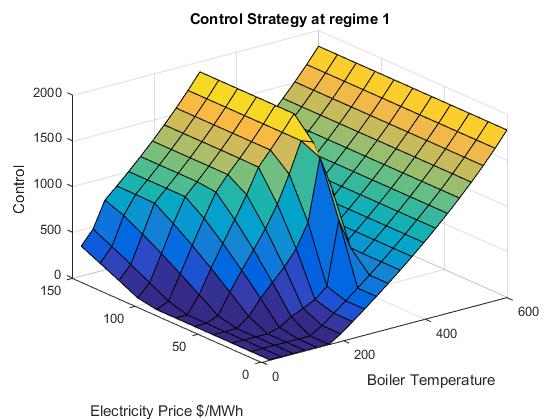

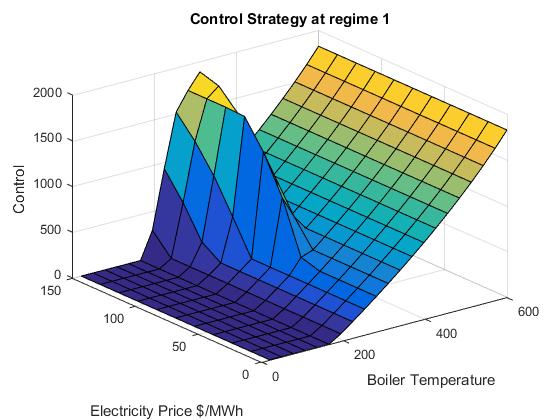

Figures 9 and 10 compare operating strategies for the regimes 0 and 1, respectively w.r.t. power prices and boiler temperature for different gas spot prices. We can see that under both of these regimes the optimal strategy for is to burn maximum amount of gas all the time. However, for all other non-zero natural gas prices the region of maximum fuel consumption is larger for the regime 0 than for the regime 1. When gas prices are too high the plant no longer consumes fuel when electricity prices are low and C. In other words, the plant manager becomes more pessimistic (or risk-averse) under the regime-switching model.

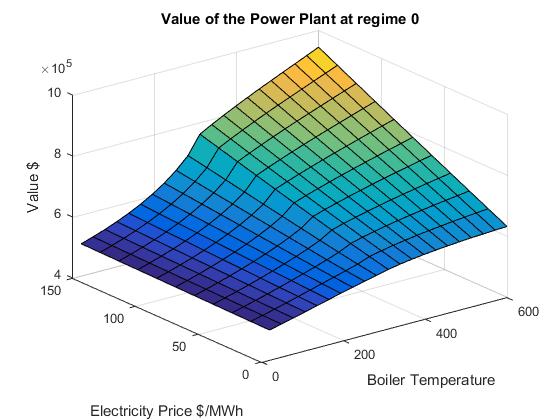

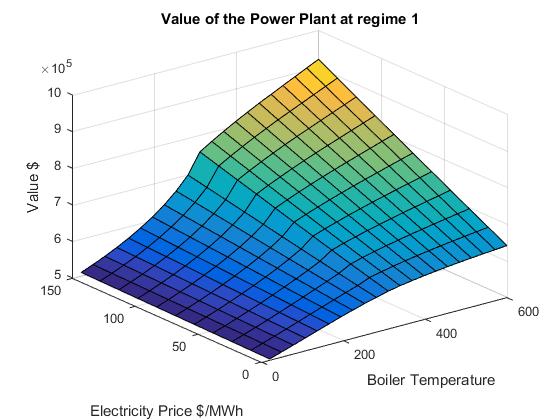

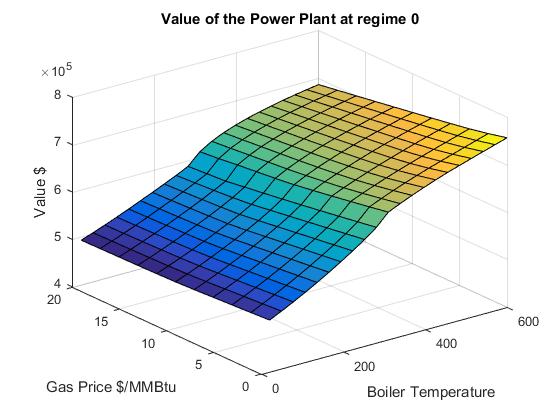

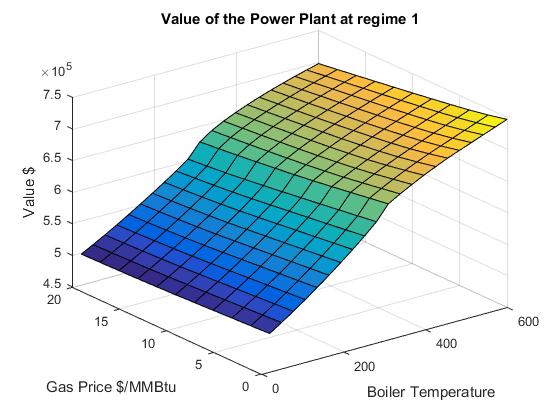

Value surfaces for the regime-switching model w.r.t. power prices and boiler temperature for the fixed gas price are depicted in Figure 11. The surfaces look similar in their shapes but in regime 1 we have a downside shift which reflects an unfavorable economic situation.

Control strategies for regime-switching model w.r.t. power and gas spot prices for different boiler temperatures are presented in Figure 12. When the temperature is above the operating level C, optimal operation surfaces are more risk-averse in regime 1. As the plant doesn’t produce electricity below C, the change in power spot prices does not affect our decision making. Hence, in regime 1 the optimal control surface for C is more optimistic than in regime 0 due to fall in fas spot prices (see Figures 12(a) and 12(d)). Moreover, in contrast to Figure 7, the surface isn’t flat when the temperature is close to its minimum.

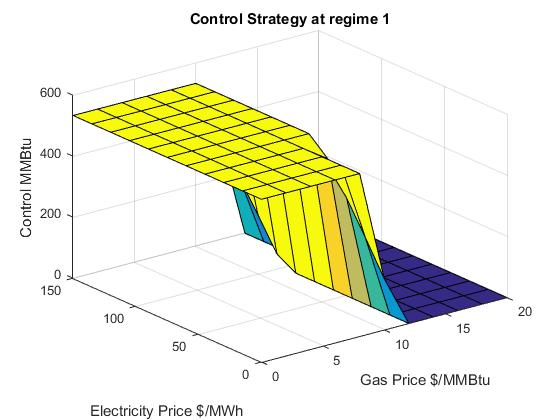

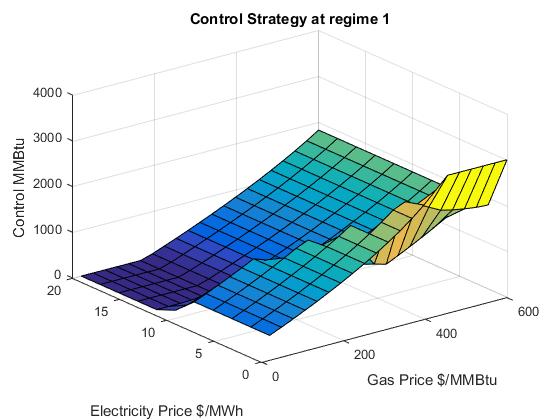

In Figure 13 we can observe operating strategy for regime-switching model w.r.t. gas spot prices and boiler temperature for different electricity spot prices. In general, these figures show less appealing results than in single regime case (see Figure 6). When the power prices are extremely low or high, the surfaces in regimes 0 and 1 look almost the same. However, for moderate electricity prices we have a larger region of minimal fuel consumption in regime 1.

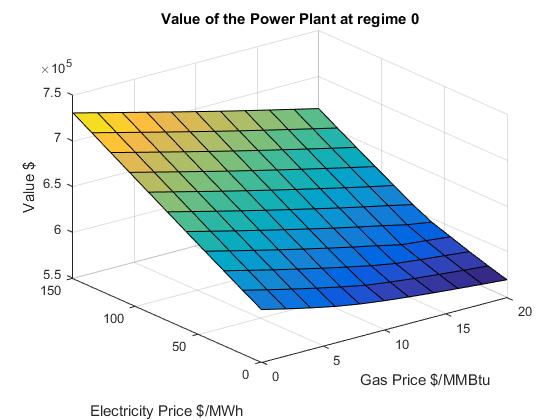

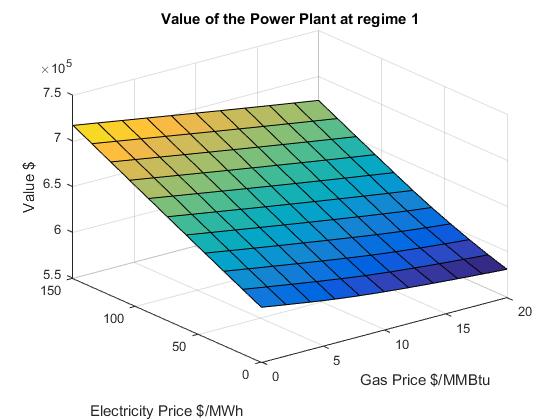

Value surfaces for the regime-switching case w.r.t. gas spot prices and boiler temperature for fixed electricity price are provided in Figure 14, while the corresponding surfaces w.r.t. electricity and gas spot prices are given in Figure 15. We can infer from these figures that the value surfaces are shifted down in regime 1 due to economic disruptions.

9 Conclusion and future research plans

In this research we analysed a stochastic control problem for gas-fired power generators while taking into account operating characteristics. The optimisation method introduced by Thompson et al. [2004] was elaborated by incorporating electricity and natural gas spot prices that exhibit regime-switching and interdependent spikes. The dependence of the price jumps has been modeled by means of skewed Lévy copulas. We combined different numerical techniques to solve the resulting coupled non-linear HJB equations. We also used a minmod slope limiter to eliminate numerical oscillations from the optimal solution. The numerical approach gives us both the value of the power plant and optimal control strategy depending on the electricity and gas price, boiler temperature and time. The numerical approach was implemented in MATLAB for a single regime and regime-switching cases. We investigated the differences in those models by observing the surfaces of optimal operation and value surfaces.

As the next step, we plan to extend our numerical examples to the cases when underlying power and natural gas spot prices follow interdependent generalised hyperbolic (see Eberlein [2001] and Eberlein and Prause [2002]) and variance-gamma (see Madan et al. [1998] or Brody et al. [2012]) Lévy models.The application of this optimisation approach into more complicated power generating assets could also be investigated.

References

- Barndorff-Nielsen and Shephard [2001] Ole E Barndorff-Nielsen and Neil Shephard. Non-Gaussian Ornstein–Uhlenbeck-based models and some of their uses in financial economics. Journal of the Royal Statistical Society: Series B (Statistical Methodology), 63(2):167–241, 2001.

- Benth [2011] Fred Espen Benth. The stochastic volatility model of Barndorff-Nielsen and Shephard in commodity markets. Mathematical Finance, 21(4):595–625, 2011.

- Benth and Kettler [2011] Fred Espen Benth and Paul C Kettler. Dynamic copula models for the spark spread. Quantitative Finance, 11(3):407–421, 2011.

- Benth et al. [2007] Fred Espen Benth, Jan Kallsen, and Thilo Meyer-Brandis. A non-Gaussian Ornstein–Uhlenbeck process for electricity spot price modeling and derivatives pricing. Applied Mathematical Finance, 14(2):153–169, 2007.

- Benth et al. [2008] Fred Espen Benth, Jurate Saltyte Benth, and Steen Koekebakker. Stochastic modelling of electricity and related markets, volume 11. World Scientific, 2008.

- Benth et al. [2013] Fred Espen Benth, Linda Vos, et al. Pricing of forwards and options in a multivariate non-Gaussian stochastic volatility model for energy markets. Advances in Applied Probability, 45(2):572–594, 2013.

- Bjerksund et al. [2008] Petter Bjerksund, Gunnar Stensland, and Frank Vagstad. Gas storage valuation: Price modelling v. optimization methods. 2008.

- Boogert and De Jong [2008] Alexander Boogert and Cyriel De Jong. Gas storage valuation using a Monte Carlo method. The journal of derivatives, 15(3):81–98, 2008.

- Boogert and de Jong [2011] Alexander Boogert and Cyriel de Jong. Gas storage valuation using a multifactor price process. The Journal of Energy Markets, 4(4):29–52, 2011.

- Brody et al. [2012] Dorje C Brody, Lane P Hughston, and Ewan Mackie. General theory of geometric Lévy models for dynamic asset pricing. In Proc. R. Soc. A, page rspa20110670. The Royal Society, 2012.

- Carmona and Ludkovski [2010] René Carmona and Michael Ludkovski. Valuation of energy storage: An optimal switching approach. Quantitative Finance, 10(4):359–374, 2010.

- Chen† and Forsyth [2010] Zhuliang Chen† and Peter A Forsyth. Implications of a regime-switching model on natural gas storage valuation and optimal operation. Quantitative Finance, 10(2):159–176, 2010.

- Cont and Tankov [2003] Rama Cont and Peter Tankov. Financial modelling with jump processes. CRC press, 2003.

- Cont and Voltchkova [2005a] Rama Cont and Ekaterina Voltchkova. A finite difference scheme for option pricing in jump diffusion and exponential Lévy models. SIAM Journal on Numerical Analysis, 43(4):1596–1626, 2005a.

- Cont and Voltchkova [2005b] Rama Cont and Ekaterina Voltchkova. Integro-differential equations for option prices in exponential Lévy models. Finance and Stochastics, 9(3):299–325, 2005b.

- Davis and Rabinowitz [2007] Philip J Davis and Philip Rabinowitz. Methods of numerical integration. Courier Corporation, 2007.

- Deng and Oren [2003] Shi-Jie Deng and Shmuel S Oren. Incorporating operational characteristics and start-up costs in option-based valuation of power generation capacity. Probability in the Engineering and Informational Sciences, 17(02):155–181, 2003.

- Deng et al. [2001] Shi-Jie Deng, Blake Johnson, and Aram Sogomonian. Exotic electricity options and the valuation of electricity generation and transmission assets. Decision Support Systems, 30(3):383–392, 2001.

- Dixit and Pindyck [1994] Avinash K Dixit and Robert S Pindyck. Investment under uncertainty. Princeton university press, 1994.

- Eberlein [2001] Ernst Eberlein. Application of generalized hyperbolic Lévy motions to finance. In Lévy processes, pages 319–336. Springer, 2001.

- Eberlein and Prause [2002] Ernst Eberlein and Karsten Prause. The generalized hyperbolic model: financial derivatives and risk measures. In Mathematical Finance—Bachelier Congress 2000, pages 245–267. Springer, 2002.

- Hamilton [1990] James D Hamilton. Analysis of time series subject to changes in regime. Journal of econometrics, 45(1):39–70, 1990.

- Henaff et al. [2013] Patrick Henaff, Ismail Laachir, and Francesco Russo. Gas storage valuation and hedging. A quantification of the model risk. arXiv preprint arXiv:1312.3789, 2013.

- Jacod and Shiryaev [2013] Jean Jacod and Albert Shiryaev. Limit theorems for stochastic processes, volume 288. Springer Science & Business Media, 2013.

- Kallsen and Tankov [2006] Jan Kallsen and Peter Tankov. Characterization of dependence of multidimensional Lévy processes using Lévy copulas. Journal of Multivariate Analysis, 97(7):1551–1572, 2006.

- Kyprianou [2006] Andreas Kyprianou. Introductory lectures on fluctuations of Lévy processes with applications. Springer Science & Business Media, 2006.

- LeVeque and Leveque [1992] Randall J LeVeque and Randall J Leveque. Numerical methods for conservation laws, volume 132. Springer, 1992.

- Longstaff and Schwartz [2001] Francis A Longstaff and Eduardo S Schwartz. Valuing American options by simulation: A simple least-squares approach. Review of Financial studies, 14(1):113–147, 2001.

- Madan et al. [1998] Dilip B Madan, Peter P Carr, and Eric C Chang. The variance gamma process and option pricing. European finance review, 2(1):79–105, 1998.

- Meyer-Brandis and Morgan [2014] Thilo Meyer-Brandis and Michael Morgan. A dynamic Lévy copula model for the spark spread. In Quantitative Energy Finance, pages 237–257. Springer, 2014.

- Näsäkkälä and Fleten [2005] Erkka Näsäkkälä and Stein-Erik Fleten. Flexibility and technology choice in gas fired power plant investments. Review of Financial Economics, 14(3):371–393, 2005.

- Parsons [2013] Cliff Parsons. Quantifying natural gas storage optionality: a two-factor tree model. Journal of Energy Markets, 6(1):95–124, 2013.

- Pindyck [1993] Robert S Pindyck. Investments of uncertain cost. Journal of financial Economics, 34(1):53–76, 1993.

- Reich et al. [2010] Nils Reich, Christoph Schwab, and Christoph Winter. On Kolmogorov equations for anisotropic multivariate Lévy processes. Finance and Stochastics, 14(4):527–567, 2010.

- Safarov and Atkinson [2016] Nemat Safarov and Colin Atkinson. Natural gas storage valuation and optimization under time-inhomogeneous exponential Lévy processes. International Journal of Computer Mathematics, pages 1–19, 2016.

- Schoutens [2003] Wim Schoutens. Lévy processes in finance pricing financial derivatives, 2003.

- Schwartz [1997] Eduardo S Schwartz. The stochastic behavior of commodity prices: Implications for valuation and hedging. The Journal of Finance, 52(3):923–973, 1997.

- Takashima et al. [2007] Ryuta Takashima, Yuta Naito, Hiroshi Kimura, and Haruki Madarame. Investment in electricity markets: equilibrium price and supply function. In 11th Annual Real Options Conference, Berkeley, CA, USA, June, pages 6–9. Citeseer, 2007.

- Thompson et al. [2004] Matt Thompson, Matt Davison, and Henning Rasmussen. Valuation and optimal operation of electric power plants in competitive markets. Operations Research, 52(4):546–562, 2004.

- Thompson et al. [2009] Matt Thompson, Matt Davison, and Henning Rasmussen. Natural gas storage valuation and optimization: A real options application. Naval Research Logistics (NRL), 56(3):226–238, 2009.

- Tseng and Barz [2002] Chung-Li Tseng and Graydon Barz. Short-term generation asset valuation: a real options approach. Operations Research, 50(2):297–310, 2002.

- Wood and Wollenberg [2012] Allen J Wood and Bruce F Wollenberg. Power generation, operation, and control. John Wiley & Sons, 2012.