Utility Indifference Pricing of Insurance Catastrophe Derivatives

Abstract

We propose a model for an insurance loss index

and the claims process of a single insurance company holding a fraction

of the total number of contracts

that captures both ordinary losses and losses due to catastrophes.

In this model we price a catastrophe derivative by the method of utility indifference pricing.

The associated stochastic optimization problem is treated by techniques for piecewise

deterministic Markov processes.

A numerical study illustrates our results.

Keywords: insurance mathematics, catastrophe derivatives, utility indifference pricing, modeling catastrophe losses, piecewise deterministic Markov process

Mathematics Subject Classification (2010): 91G20, 91B70, 91B16, 93E20, 60J75

JEL Classification: G13, G22

1 Introduction

Costly natural catastrophes in the recent past (hurricane Andrew in 1992, hurricane Katrina in 2005, the earthquake and tsunami in Japan 2011 resulting in the nuclear disaster at Fukushima, floods in Thailand 2011) all caused severe stress to the (re-)insurance industry. However, these losses are still small relative to losses of the US stock and bond markets. Therefore securitization (i.e. transferring part of the risk to the financial market) is an efficient alternative to reinsuring catastrophe (CAT) losses, cf. [5].

Contracts of this kind are insurance-linked derivatives.111Details on currently listed insurance-linked derivatives can be found at www.artemis.bm/deal_directory. They are usually written on insurance industry catastrophe loss indices, insurer-specific catastrophe losses, or parametric indices based on the physical characteristics of catastrophe events. We focus on the first kind of products; they involve more basis risk, but are less exposed to moral hazard than the others, cf. [4].

Derivatives written on insurance industry catastrophe loss indices were first issued in 1992 by the Chicago Board of Trade; these were futures and later also call- and put spread options written on aggregate CAT-loss indices, cf. [4].

A call spread option is a combination of a call option long and a call option short with a higher strike. Another popular type of catastrophe derivative is the CAT bond. This is a classical bond combined with an option that is triggered by a (predefined) catastrophe event. Note that the buyer of the bond thereby sells the embedded option. The issuer is typically a (re-)insurance company that wants to reinsure parts of its risk exposure on the financial market. In return the investor receives a coupon.

CAT derivatives are interesting for investors who seek to diversify their risk, since they are largely uncorrelated with classical financial instruments.

The challenges in pricing CAT derivatives are that the underlying index is not a traded asset,

that they are not liquidly traded themselves and, maybe most of all, the modeling of catastrophe events.

In the following we review the existing literature. For a more detailed literature overview we refer to Muermann [17].

Geman and Yor [12] study European vanilla call options written on an insurance loss index, which is modeled by a jump-diffusion. Cox et al. [3] model the aggregate loss of an insurance company by a Poisson process with constant arrival rate of catastrophe events and derive a pricing formula for CAT-puts. Jaimungal and Wang [14] model the aggregate loss by a compound Poisson process to describe the dynamic losses more accurately. Muermann [18] derives the market price of insurance risk from CAT derivative prices in a compound Poisson model. Leobacher and Ngare [15] use the method of utility indifference pricing to price CAT derivatives written on an insurance loss index modeled by a compound Poisson process.

For catastrophe events, the assumption that the resulting claims

occur at jump times of a Poisson process as adopted by most previous studies is

not beyond justifiable critique.

A generalization was proposed in Embrechts and Meister [9], who model an insurance loss index by a doubly stochastic Poisson process (Cox process), i.e. the arrival rate of claims is a stochastic process itself; they price CAT futures in this model. Lin et al. [16] also model the arrival of CAT events by a doubly stochastic Poisson process.

See also Fuita et al. [11] for no-arbitrage pricing of CAT bonds in this context.

Dassios and Jang [6] study the valuation of CAT derivatives by risk neutral valuation, where the underlying is modeled as a Cox process with shot noise intensity.

In this paper we introduce a novel model for an insurance loss index and for a single insurance portfolio that captures ordinary insurance losses as well as catastrophe losses. We model the ordinary claims in the loss index by a compound Poisson process with constant intensity and we model the arrival of catastrophes by a Poisson process with constant intensity, where a jump triggers another stochastic variable that determines the number of claims in case of a catastrophe.

The claims process of a single insurance company holding a fraction

of the total number of contracts is then a dynamic thinning of the process describing the index.

Our model has the advantage that the jump height distribution does not need to capture both many small claims and outliers caused by catastrophes, but these outliers are split into many smaller claims.

The dynamic thinning is reached in a very convenient way (by drawing from a uniform distribution on ) that we believe to be applicable in many other situations.

Using this model we present a pricing mechanism for CAT derivatives (like CAT spread options). Since the insurance loss index is not a tradable asset, and since the market for CAT derivatives is not liquid, risk neutral valuation is not applicable. Instead we use the method of utility indifference pricing. For this we need a hedging mechanism, which will be an active management of the risk portfolio. The pricing method requires solving an associated stochastic optimization problem.

Our paper extends [15] by a more realistic modeling approach for the insurance loss index and also for the thinning. In our paper a catastrophe event may partly hit the considered insurance company, whereas in [15] a catastrophe event always only affects one company. Their model for the claims process of a single insurance company is a thinning (a change of the intensity) of the Poisson process driving the number of claims, while ours is a dynamic thinning of the claims for each event and thus has a different distribution of the jumps.

The model presented here is technically harder to handle; we provide the mathematical toolkit in this paper. Using this new model instead of a simpler one is justified by our numerical results, which show that the new model has a significant impact on the price of a CAT derivative as it reflects catastrophes more accurately.

We also introduce a way to compute the utility indifference price of the derivative by Fourier techniques.

This method also allows to compute the residual risk and the profit-loss distribution and therefore to evaluate coherent risk measures.

The paper is organized as follows. In Section 2 we model the insurance loss index and the claims process of a single insurance company. The state process based on which the CAT derivative is priced, is identified as a piecewise deterministic Markov process (PDMP), see [7, 2]. In Section 3 we recall the general concept of utility indifference pricing and we solve the associated stochastic optimization problem. In Section 4 we show how the utility indifference price and also quantities relevant for risk management can be computed efficiently, and we present a numerical study.

2 The model

Let be a probability space carrying all stochastic variables appearing below.

Suppose we have a global claims process , which keeps track of all property insurance claims in a given country and we consider an insurance company in the same country, so that the index will contain the losses of that particular insurance company among others.

The portfolio income rate consisting of the premium revenues from the risk portfolio is given by a continuous function of the company’s market share .

The function is not necessarily linear in , since demand for insurance might depend on the premium the company charges.

The wealth process of the insurance company can

be controlled by managing the insured portfolio, i.e. by controlling the market share .

This allows for optimizing the management strategy for maximizing utility from terminal wealth.

Therefore, we can apply the method of utility indifference pricing for the valuation of CAT-derivatives.

The global claims process is given by

| (1) |

and where and are independent Poisson processes with intensities and jump times . The jump heights are iid random variables representing the damage of, e.g., single houses. The random variables , , describe the number of claims in case of a catastrophe. The process describes the occurrence of regular claims whereas a jump of indicates an accumulation of claims due to a catastrophe event.

If the insurance company holds the -th part of the whole risk, it is exposed to the -th part of the claims. We model this as

| (2) |

The random variables are iid and ; they determine whether the company is affected by the corresponding claim or not. For fixed this is a thinning of the original process, cf. [19, Section 3.12.1].

We assume independence of .

It is possible to write (1) as a single sum by adapting the jump intensity and the distribution of the , which we will do to ease the notation in the following. Note that the jump height distribution does not need to be adapted so that we do not loose the favourable properties for modeling catastrophe events. Let be a Poisson process with intensity and jump times and let the number of claims per jump of be denoted by with

| (3) |

We can write the insurance loss index as

| (4) |

Both and the distribution of are chosen such that (1) and (4) are equivalent.

The claims process of the insurance company holding the -th part of the risk becomes

| (5) |

Denote by . For all the generating function of is given by , where

Assumption 2.1.

We assume that

-

-

;

-

-

.

Assumption 2.1 implies that the convergence radius of the generating function is greater than and hence

Note that if , also by Jensen’s inequality.

In contrast to a model where the claims process is a simple compound Poisson process,

here assuming the existence of exponential moments of the claim size distribution is not a great restriction,

since we model catastrophes as an accumulation of small claims rather than one big claim.

The dynamics of the wealth process of the insurance company with initial wealth is given by:

| (6) |

PDMP characterization

The two-dimensional process is a PDMP in the sense of [7]. We also refer to [2, Chapter 8] or [1] for a presentation of the theory. Our PDMP has the following characteristics:

-

-

state space ;

-

-

control space ;

-

-

deterministic flow between jumps;

-

-

jump intensity ;

-

-

jump kernel ,

where

and where we use the notation ;

-

-

zero running reward rate;

-

-

zero discount rate.

Denoting by the time of a jump of the PDMP and by the state immediately after that jump, we define the set of bounded Markov controls as the set of all measurable functions assigning to given input data a control until the next jump, i.e.

3 Utility indifference pricing

The method of utility indifference pricing for the valuation of derivatives in incomplete markets has been introduced in [13]. It relies on the fact that even if the derivative cannot be replicated, it may still be the case that much of its variation can be hedged.

In [8] utility indifference pricing is used to price structured catastrophe bonds. However, there is a difference in modeling the hedging possibility. In our setup this is done via managing the insured portfolio. The main idea is that the loss in the portfolio of a single insurance company is necessarily correlated with the insurance loss index. The introduction of the derivative has therefore an influence on the pricing policy of the insurance company.

We will first explain the notion of utility indifference pricing and then apply it to our problem.

Assume the investor has a utility function and

initial wealth . Define

, where the supremum is taken over

all possible wealths that can be generated

from . The random variable is the payment from a European claim with

expiry , and is the number of claims that are bought.

The utility indifference bid price is the price at which the investor has the same utility whether she pays nothing and does not receive the claim , or she pays now and receives units of the claim at time . Therefore, is the largest amount of money the investor is willing to pay for buying units of the claim ; it solves .

The utility indifference ask price is the smallest amount of money the investor is willing to accept for selling units of the claim ; it solves .

The two prices are related via . With this in mind we can define the utility indifference price .

Assumption 3.1.

-

-

The insurance company has exponential utility , .

-

-

is of the form for some control and does not depend on the initial wealth .

In that case

| (7) |

(provided that the arguments in the logarithms are finite), and hence does not depend on the initial wealth .

Note that exponential utility is a natural choice for insurance companies as often such a utility function is used to calculate insurance premia. As an example where exponential utility is used in a stochastic optimal control framework in an insurance context, see [10].

3.1 The stochastic optimization problem

We apply the concept of utility indifference pricing to the model presented in Section 2. Our aim is to price a derivative written on the total claims process with payoff , where is a continuous and bounded function on .

Example 3.1.

We are specifically interested in CAT (spread) options, i.e.

with cap and strike . The option is in the money, if exceeds , and the payoff is bounded by .

Note that the main task in pricing CAT bonds also lies in pricing the embedded spread option, since for exponential utility the price of a CAT bond is the sum of a spread option price and a bond price.

We maximize the expected utility from terminal wealth. The corresponding value function is defined by

| (8) |

Since is bounded we have that

for ,

for all ,

and hence .

is bounded from above since is bounded.

Therefore, is well-defined.

For bounded and measurable the generator of the jump process is defined by

The Hamilton-Jacobi-Bellman (HJB) equation corresponding to optimization problem (8) is

| (9) | ||||

We make the ansatz to obtain a backward equation which is independent of the initial wealth . This yields

Defining

| (10) |

and using that is negative, we obtain the backward equation for :

| (11) | ||||

Lemma 3.2.

Let be such that . Then is bounded by .

Proof.

We have , i.e.

Denote by the process with . Then

and

Thus . ∎

3.2 Verification result

We show that the solution of the HJB equation (9) solves the optimization problem (8). For this we apply results from stochastic control theory for PDMPs; more precisely, a slight variation of the verification theorem [2, Theorem 8.2.8]. For this we recall two definitions from [1].

Definition 3.3.

A measurable function is called a bounding function for our piecewise deterministic Markov decision model, if there exist constants such that for all

-

i.

;

-

ii.

for all , ;

-

iii.

for all .

Here is the space of relaxed policies, i.e. of measurable maps , where is the space of all probability measures on the Borel -algebra on .

Definition 3.4.

Let be a bounding function and fixed. Define the Banach space with the norm

Theorem 3.5 (Verification Theorem).

Let be a bounding function for our piecewise deterministic Markov decision model with for all . Let be a solution of the HJB equation (9) and let be a maximizer for (9), leading to the state process .

Then and is an optimal feedback-type Markov policy.

Remark 3.6.

For proving Theorem 3.5, we first need to prove existence of a bounding function.

Lemma 3.7.

The function defined by is a bounding function for our piecewise deterministic Markov decision model.

Proof.

Now we need to show that the backward equation (11) has a solution and hence also (9) has a solution.

Define on by

| (12) |

We show that if , then and that is locally Lipschitz. For this we write and show that are locally Lipschitz and is -valued.

Lemma 3.8.

For the mapping is a power series in . Its coefficients are of the form for non-negative random variables with that do not dependent on and . The power series converges uniformly on .

Proof.

Let be the distribution function of . Then

Expanding the above expression yields the first and the second claim of the lemma. Setting , we get . Setting gives

The right-hand side is finite by Assumption 2.1 and by the assumption of the lemma. ∎

Define the function-space

and let be defined by

, with

as in Lemma 3.8. Hence, for

any ,

for every .

Lemma 3.9.

The function is a bounded linear operator.

Proof.

We need to prove that for every the mapping is a bounded linear operator .

Let . We show that the mapping is continuous and bounded on . Let in . Then for all . The sequence is dominated by , which is integrable. Hence, by the dominated convergence theorem. Thus is continuous. Moreover, is bounded, since .

For it holds that . Thus is bounded by Lemma 3.8. ∎

For a sequence in define the function by

| (13) |

Lemma 3.10.

Let be defined as in (13). Then

-

1.

is defined on and it is bounded on every norm-bounded subset of ;

-

2.

is convex;

-

3.

is Lipschitz on every norm-bounded subset of .

Proof.

For and we have . The function , is well-defined and continuous as a uniform limit of continuous functions on . Since is also continuous, the first statement follows.

The proof of the second statement is straightforward.

Following [20] we use the convexity of to show that is Lipschitz on . Let and define . It holds that and hence . By the definition of we have that , where . Since is convex, and hence for some constant , since is bounded on . ∎

For let and define the function by .

Lemma 3.11.

The function is -valued and locally Lipschitz.

Proof.

Let . Let in and let . There exists such that , and for large enough . Thus, .

The claim that is locally Lipschitz follows from Lemma 3.10: let and let with and . is Lipschitz on the ball with radius in . Denote the corresponding Lipschitz constant by . Then lie in the ball with radius in . Hence, . ∎

Finally, define , and note that is locally Lipschitz.

Lemma 3.12.

Let be defined as in (12). If , then and is locally Lipschitz.

Proof.

Now we prove that (11) has a unique maximal local solution.

Lemma 3.13.

Let . Then the backward equation (11) has a unique maximal local solution.

Proof.

The backward equation (11) is an initial value problem with -valued solution:

| (14) |

By Lemma 3.12, is -valued and locally Lipschitz. In particular, is Lipschitz on the ball with radius . From the Picard-Lindelöf theorem on existence and uniqueness of solutions of ordinary differential equations we get existence and uniqueness of a maximal local solution of (14), i.e. there exists and a solution of (14) on with for all . We may choose maximal such that or .

The function defined by is the unique maximal local solution of (11). ∎

Proof of Theorem 3.5.

Since for every and the function is continuous on by Lemma 3.8, there exists a maximizer for (9). By Lemma 3.7 and Lemma 3.13 the assumptions of Theorem 3.5 are satisfied on , where is as in the proof of Lemma 3.13. Along the lines of the proof of [2, Theorem 8.2.8] it can be shown that with solves the optimization problem (8) for , i.e. for .

3.3 Utility indifference price

With the solution of (11) we can compute the utility indifference price of a derivative with payoff . Given the value of the index and the amount of wealth at time , the maximum expected utility of terminal wealth can be written as

The corresponding value with no derivative bought is given by

where is the solution of equation (11) with . Therefore (7) simplifies to

| (15) |

In particular, does not depend on and we omit that parameter from henceforth. The function does not depend on . So is the solution of an ordinary differential equation.

Lemma 3.14.

Let solve (11) with terminal condition . Then

Proof.

From (15) we can derive a backward equation for . Since does not depend on the second variable, we have

and it holds that , where

Hence

| (17) |

4 Computations

In this section we present a convenient numerical method for computing the expected value in (17) for the case where the distribution of has a smooth density. Denote by the k-fold convolution of a function with itself, i.e. and . Let denote the Fourier transform. It holds that . The following lemma gives an efficient method for computing .

Lemma 4.1.

Assume that the distribution of has a piecewise continuous density . Denote by . Let be measurable and bounded.

Then it holds that

where .

Proof.

Denote . We have

where we used that , which can be seen by induction. The first claim now follows by linearity of the convolution. Further,

With this,

Since is piecewise continuous, is continuous for and hence is piecewise continuous.

Thus a.e. on . ∎

4.1 Numerical experiments

Our aim is to price a CAT (spread) option, i.e. .

The function governing the company’s market share is chosen as in [15]. We assume that there are clients in the market who potentially contribute to the claims process. Let be the fair annual premium for one client, i.e. . The annual premium for one contract therefore has to be greater or equal than , since otherwise the insurance company will make an almost sure loss in the long run. The premium the insurance company charges for a claim is with . Furthermore, the company faces an exogenously given demand curve for insurance. It is continuous, decreasing in , and satisfies for and for , i.e. the company gets to insure the whole risk, if it does not charge any risk loading () and it gets contracts, if the risk-loading exceeds some fixed number . With this , where . For our numerical example we choose

The model parameters in our example are given

by , , , , year.

The number of jumps in case of a catastrophe is Poisson distributed, ; the distribution of then follows from (3).

The claim size distribution is a Gamma distribution, .

We want to study two effects: the effect that holding a derivative has on the risk loading (which depends on the optimal market share ) and its change over time, and the effect of our model (the clustered claims (CC) model) on the utility indifference price of the derivative and on the risk loading in comparison to the model where the claims process is a simple compound Poisson process as, e.g., in [15] (the single claim (SC) model).

For the SC-model we choose .

In order to be able to compare the two models we adapt such that the expected annual claim size per contract stays constant, yielding .

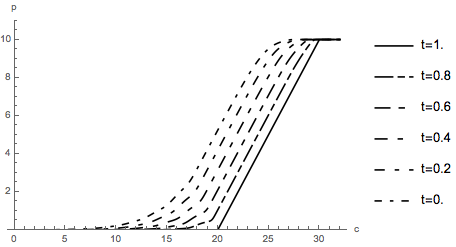

Figure 1 shows the utility indifference price of the CAT spread option in dependence of the value of the claims process.

We see that the price increases in .

As time increases the expected number of claims within the remaining time decreases, and hence also the price decreases;

for the prices converges to the payoff.

Further, we observe that in the SC-model the price is always lower than in the

CC-model, since the latter more accurately accounts for a clustering of claims.

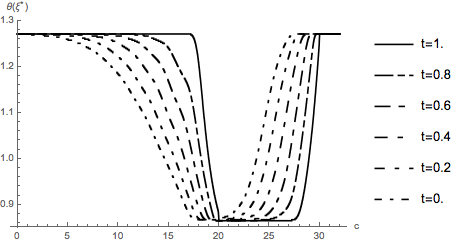

Figure 2 shows the risk loading corresponding to the optimal market share in dependence of the value of the claims process. For small the risk loading is the same as in the case of no derivative held, since the probability that the derivative has a positive payoff is small. For a further increase of does not change the payoff and hence the situation is the same as for holding no derivative.

As time increases the probability that the payoff of the derivative grows in and hence compensates losses during the remaining time decreases, but also the expected number of claims before decreases. An interesting observation is that for small the first effect dominates and hence the risk loading increases, whereas for large the latter effect dominates and hence the risk loading decreases.

In the CC-model the risk loading is in general higher than in the SC-model, since we imposed risk aversion.

The risk loading decreases significantly when a derivative is bought.

The effect of holding a derivative is higher in the CC-model; the optimal average risk loading decreases by approximately (compared to in the SC-model).

We observe the same effects when comparing our CC-model to the SC-model for the example of [15], where a bounded claim size distribution was used.

Concluding remarks

The introduction of a derivative serves as an effective alternative to classical reinsurance and leads to significantly smaller insurance premia. The CC-model introduced in this paper has a significant impact on the price of a CAT derivative as well as on the optimal average risk loading. It reflects catastrophes more accurately.

4.2 Risk management

In this section we compute the profit-loss distribution and the residual risk of an insurance company holding a CAT derivative. The former is useful for the derivation of coherent risk measures, the latter quantifies the efficiency of the hedge.

Profit-loss distribution

The profit-loss distribution is the distribution of the (optimally controlled) wealth in case the company holds a CAT derivative.

Let be the optimal control. For define

| (18) |

The right-hand side in (18) can be interpreted as (two-sided) Laplace transform of the profit-loss distribution at , . We can compute by making the ansatz , where solves the backward equation

| (19) | ||||

with corresponding . By solving (19) for different values of , we get the density of the profit-loss distribution by inverting the Laplace transform:

Residual risk

The numerical experiments in Section 4.1 showed that the optimal market share of an insurance company that holds a CAT derivative is higher than for a company that does not (). The change in the strategy when an insurance company buys a CAT derivative, is also the strategy used for hedging the derivative itself.

The (buyer’s) risk of derivative is ; the residual risk, i.e. the remaining risk after hedging is given by

| (20) |

The density of (20) can be computed in the same way as the density of the profit-loss distribution above.

Acknowledgements

A. Eichler is supported by the Austrian Science Fund (FWF): Project P21196.

G. Leobacher is supported by the Austrian Science Fund (FWF): Project F5508-N26, which is part of the Special Research Program ”Quasi-Monte Carlo Methods: Theory and Applications” and by the Austrian Science Fund (FWF): Project P21196. This paper was written while G. Leobacher was member of the Department of Financial Methematics and Applied Number Theory, Johannes Kepler University Linz, Altenbergerstraße 69, 4040 Linz, Austria.

M. Szölgyenyi is supported by the Vienna Science and Technology Fund (WWTF): Project MA14-031.

References

- Bäuerle and Rieder [2010] N. Bäuerle and U. Rieder. Optimal control of piecewise deterministic markov processes with finite time horizon. In A. Piunovskiy, editor, Modern trends in controlled stochastic processes: theory and applications, pages 123–143. Luniver Press, 2010.

- Bäuerle and Rieder [2011] N. Bäuerle and U. Rieder. Markov Decision Processes with Applications in Finance. Universitext. Springer, Berlin, Heidelberg, 2011.

- Cox et al. [2004] S. H. Cox, J. R. Fairchild, and H. W. Pedersen. Valuation of structured risk management products. Insurance: Mathematics & Economics, 34(2):259–272, 2004.

- Cummins [2006] J. D. Cummins. Should the government provide insurance for catastrophes? Federal Reserve Bank of St. Louis Review, 88(4), 2006.

- Cummins et al. [2004] J. D. Cummins, D. Lalonde, and R. D. Phillips. The basis risk of catastrophic-loss index securities. Journal of Financial Economics, 71(1):77–111, 2004.

- Dassios and Jang [2003] A. Dassios and J.-W. Jang. Pricing of Catastrophe Reinsurance and Derivatives using the Cox Process with Shot Noise Intensity. Finance & Stochastics, 7:73–95, 2003.

- Davis [1993] M. H. A. Davis. Markov Models and Optimization. Monographs on Statistics and Applied Probability. Chapman & Hall, London, 1993.

- Egami and Young [2008] M. Egami and V. R. Young. Indifference prices of structured catastrophe (CAT) bonds. Insurance: Mathematics & Economics, 42(2):771–778, 2008.

- Embrechts and Meister [1997] P. Embrechts and S. Meister. Pricing Insurance Derivatives: The Case of CAT Futures. In Securization of Insurance Risk: The 1995 Bowles Symposium, pages 16–26, 1997.

- Fernández et al. [2008] B. Fernández, D. Hernández-Hernández, A. Meda, and P. Saavedra. An Optimal Investment Strategy with Maximal Risk Aversion and its Ruin Probability. Mathematical Methods in Operations Research, 68:159–179, 2008.

- Fuita et al. [2008] T. Fuita, N. Ishimura, and D. Tanake. An arbitrage approach to the pricing of catastrophe options involving the cox process. Hitotsubashi Journal of Economics, 49:67–74, 2008.

- Geman and Yor [1997] H. Geman and M. Yor. Stochastic time changes in catastrophe option pricing. Insurance: Mathematics & Economics, 21(3):185–193, 1997.

- Hodges and Neuberger [1989] S. Hodges and A. Neuberger. Optimal replication of contingent claim under transaction costs. Rev. Futures Markets, 8:222–239, 1989.

- Jaimungal and Wang [2006] S. Jaimungal and T. Wang. Catastrophe options with stochastic interest rates and compound poisson losses. Insurance: Mathematics & Economics, 38(3):469–483, 2006.

- Leobacher and Ngare [2016] G. Leobacher and P. Ngare. Utility indifference pricing of derivatives written on industrial loss indexes. Journal of Computational and Applied Mathematics, 300:68–82, 2016.

- Lin et al. [2009] S. Lin, C. Chang, and M. R. Powers. The valuation of contingent capital with catastrophe risks. Insurance: Mathematics & Economics, 45(1):65–73, 2009.

- Muermann [2004] A. Muermann. Catastrophe Derivatives. In J. L. Teugels and B. Sundt, editors, Encyclopedia Of Actuarial Science, volume 1, pages 231–236. John Wiley & Sons, Ltd, Chichester, 2004.

- Muermann [2008] A. Muermann. Market Price of Risk Implied by Catastrophe Derivatives. North American Actuarial Journal, 12(3):221–227, 2008.

- Olofsson and Andersson [2012] Peter Olofsson and Mikael Andersson. Probability, statistics, and stochastic processes. John Wiley & Sons, Hoboken, NJ, 2nd ed. edition, 2012.

- Roberts and Varberg [1974] A. W. Roberts and D. E. Varberg. Another proof that convex functions are locally Lipschitz. The American Mathematical Monthly, 81:1014–1016, 1974.

Andreas Eichler

University of Applied Sciences Upper Austria – Campus Wels, Stelzhamerstraße 23, 4600 Wels, Austria

andreas.eichler@fh-wels.at

Gunther Leobacher

Department of Mathematics and Scientific Computing, University of Graz, Heinrichstraße 36, 8010 Graz, Austria

gunther.leobacher@jku.at

Michaela Szölgyenyi 🖂

Institute for Statistics and Mathematics, WU Vienna University of Economics and Business, Welthandelsplatz 1, 1020 Vienna, Austria

michaela.szoelgyenyi@wu.ac.at