An Application of the EM-algorithm to Approximate Empirical Distributions of Financial Indices with the Gaussian Mixtures

Abstract

In this study I briefly illustrate application of the Gaussian mixtures to approximate empirical distributions of financial indices (DAX, Dow Jones, Nikkei, RTSI, SP 500). The resulting distributions illustrate very high quality of approximation as evaluated by Kolmogorov-Smirnov test. This implies further study of application of the Gaussian mixtures to approximate empirical distributions of financial indices.

financial indices, Gaussian distribution, mixtures of Gaussian distributions, Gaussian mixtures, EM-algorithm

1 Introduction

Approximation of empirical distributions of financial indices using mixture of Gaussian distributinos (Gaussian mixtures) (eq. (1)) has been recently discussed by Tarasenko and Artukhov [1]. Here I provide detailed explanation of steps and methods.

| (1) |

2 EM-algorithm for mixture separation

2.1 General Theory

The effective procedure for separation of mixtures was proposed by Day [2, 3] and Dempster et al. [4]. This procedure is based on maximization of logarithmic likelihood function under parameters ,,…, ,,,…, , where is number of mixture components:

| (2) |

In general, the algorithms of mixture separations based on (2) are called Estimation and Maximization (EM) algorithms. EM-algorithm consists of two steps: E - expectation and M-maximization. This section is focused scheme how to construct EM-algorithm.

Let is defined as posterior porbability of oservations to belong to -th mixture component (class):

| (3) |

Posterior probability is equal or greater then 0 and for any .

Let be a vector of parameters: = (,,…, ,,,…, ). Next, we deompose the logarithms likelihood function into three components:

| (4) | |||

| (5) | |||

| (6) | |||

| (7) |

For this algorithm to work, the initial value is used to calculate inital approximations for posterior probabilities . This is Expectation step. Then values of are used to calculate value of during the Maximization step.

Each of components (6) and (7) are maximized independently from each other. This is possible because component (6) depends only on (=1,…,), and component (7) depends only on (=1,…,).

As a solution of optimization task (8)

| (8) |

a value of for the iteration is calculated as:

| (9) |

where is iteration number, = 1,2, ,,,

A solution of optimization task (10)

| (10) |

depends on a particular type of function .

Next we consider solution of optimization task (10), when is Gaussian distribution.

2.2 Mixtures of Gaussian Distributions

Here we employ Guassian distributions:

| (11) |

Therefore, a specific formula to compute posterior probabilities in the case of Gaussian mixtures is

| (12) |

According to the EM-algorithm, the task is to find value of parameters = by solving maximization problem (14)

| (13) | |||

| (14) |

| (15) | |||

| (16) |

Having calculated optimal values for weights and paramaters (=1,…,) during a single iteration, we apply these optimal values to obtain estimates of posterior probabilities during the Expectation step of the next iteration.

As a stop criterion, we use difference between values of loglikelyhood on iteration and iteration :

| (17) |

where is infinitely small real value.

3 An Application of the EM-algorithm to Approximate Empirical Distributions of Financial Indices with Guassian Mixtures

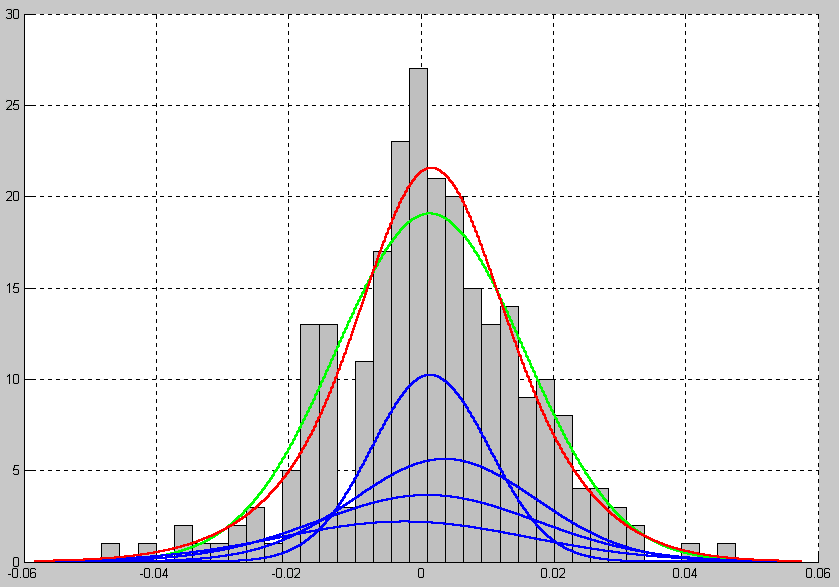

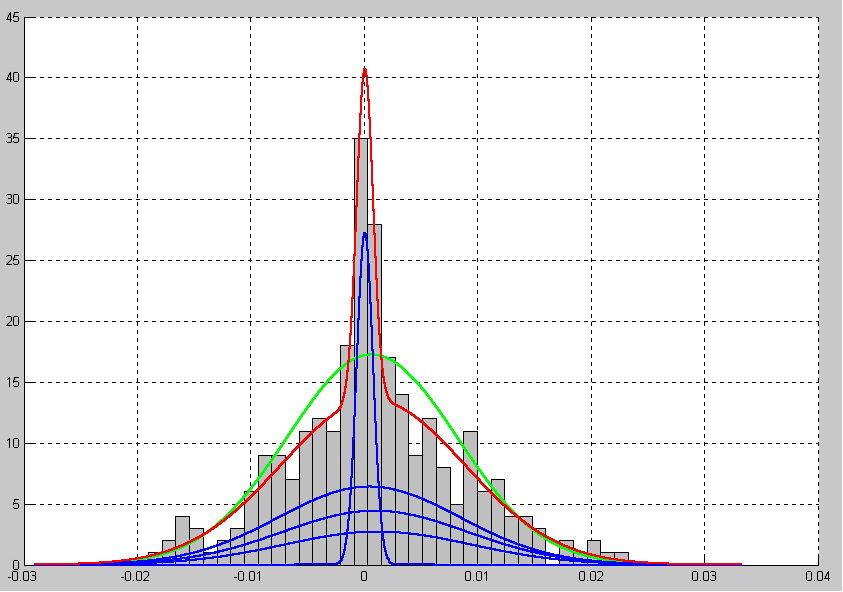

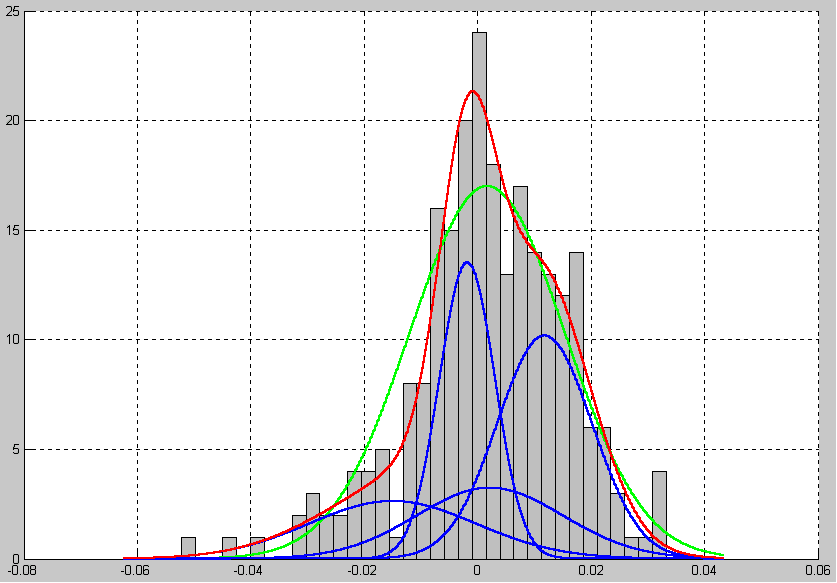

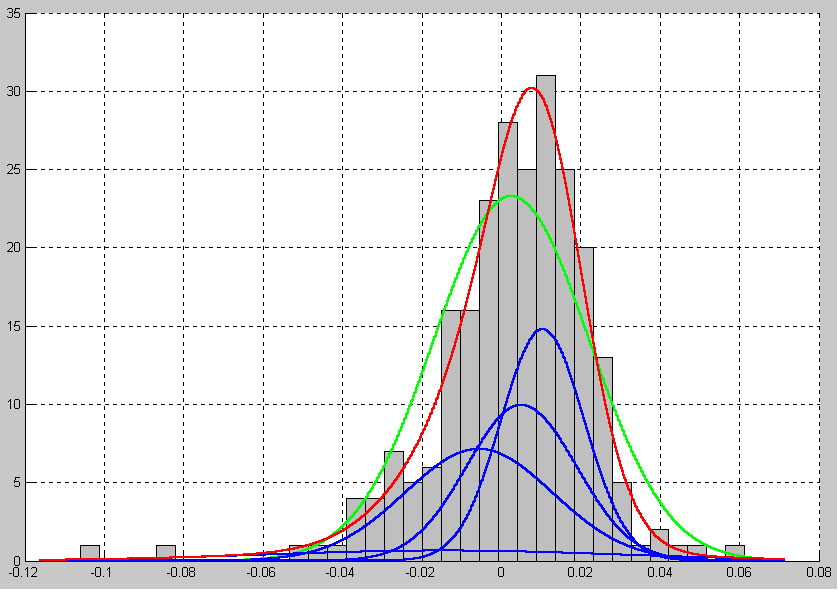

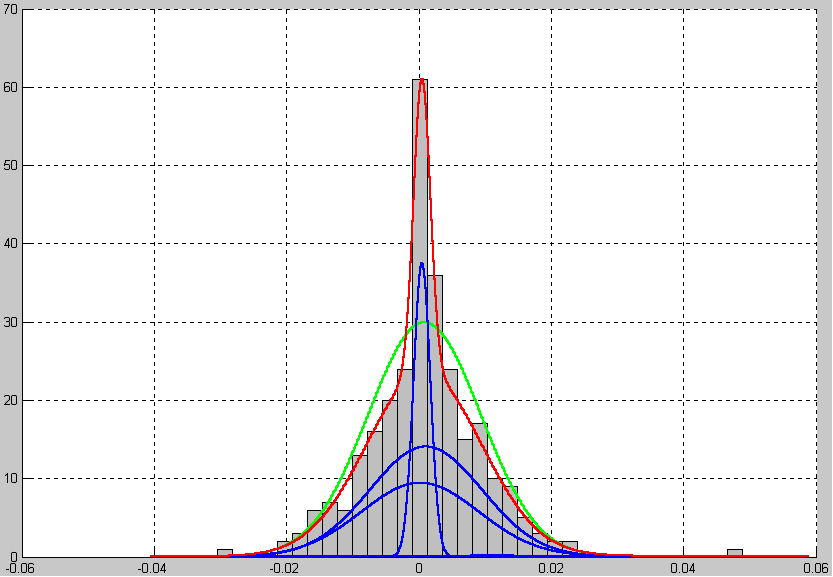

In this section, I provide several examples of EM-algorithm applications to approximate empirical distributions of financial indices with Gaussian mixtures. I consider the following indices: DAX, Dow Jones Industrial, Nikkei, RTSI, and SP 500.

In Figs. 1-5, the green line corresponds to the Gaussian distribution, the red line illustrates a Gaussian mixture and the blue lines represent components of the Gaussian mixture.

| Weight | Mean | Standard | |

|---|---|---|---|

| Diviation | |||

| Component 1 | 0.152 | -0.002 | 0.018 |

| Component 2 | 0.223 | 0.001 | 0.017 |

| Component 3 | 0.287 | 0.004 | 0.014 |

| Component 4 | 0.337 | 0.001 | 0.009 |

| Weight | Mean | Standard | |

|---|---|---|---|

| Diviation | |||

| Component 1 | 0.173 | 0.001 | 0.008 |

| Component 2 | 0.279 | 0.001 | 0.008 |

| Component 3 | 0.396 | 0.001 | 0.008 |

| Component 4 | 0.152 | 0.000 | 0.001 |

| Weight | Mean | Standard | |

|---|---|---|---|

| Diviation | |||

| Component 1 | 0.167 | -0.014 | 0.014 |

| Component 2 | 0.180 | 0.002 | 0.013 |

| Component 3 | 0.367 | 0.011 | 0.008 |

| Component 4 | 0.286 | -0.002 | 0.005 |

| Weight | Mean | Standard | |

|---|---|---|---|

| Diviation | |||

| Component 1 | 0.062 | -0.014 | 0.044 |

| Component 2 | 0.294 | -0.005 | 0.019 |

| Component 3 | 0.303 | 0.005 | 0.014 |

| Component 4 | 0.341 | 0.011 | 0.011 |

| Weight | Mean | Standard | |

|---|---|---|---|

| Diviation | |||

| Component 1 | 0.014 | 0.011 | 0.027 |

| Component 2 | 0.331 | 0.000 | 0.009 |

| Component 3 | 0.470 | 0.001 | 0.009 |

| Component 4 | 0.186 | 0.000 | 0.001 |

4 Discussion and Conclusion

The results presented in this study illustrate that EM-algrothim can be effectively used to approximate empiral distributions of log daily differences of financial indices. Throughout the data for five selected indices, EM-algorithm provided very good approximation of empoiral distirbution with Gaussian mixtures.

The approximations based on Gaussian mixtures can be used to improve application of Value-at-Risk and other methods for financial risk analysis.

This implies further explorations in applying Gaussian mixtures and the EM-algorithm for the purpose of approximation of empirial distirbutions of financial indices.

References

- [1] Tarasenko, S., and Artukhov, S. (2004) Stock market pricing models. In the Proceedings of International Conference of Young Scientists Lomonosov 2004, p. 248-250.

- [2] Day, N.E. (1969) Divisive cluster analysis and test for multivariate normality. Session of the ISI, London, 1969.

- [3] Day, N.E. (1969) Estimating the components of a mixture of normal distributions., Biometrika, 56, N3.

- [4] Dempster, A., Laird, G. and Rubin, J. (1977) Maximum likelihood from incomplete data via EM algorithm. Journal of Royal Statistical Society, B, 39.