Hierarchical Marginal Models

with Latent Uncertainty

, , ,

1 Department of Management, Information and Production Engineering, University of Bergamo, Italy, e-mail: colombi@unibg.it

2 Department of Economics, Statistics and Finance, University of Calabria, Italy, e-mail: sabrina.giordano@unical.it

3 Department of Statistics, Computer Science, Applications, University of Florence, Italy, e-mail:gottard@disia.unifi.it

4 Department of Political Sciences, University of Naples Federico II, Italy, e-mail:maria.iannario@unina.it

Abstract

In responding to rating questions, an individual may give answers either according to his/her knowledge/awareness or to his/her level of indecision/uncertainty, typically driven by a response style. As ignoring this dual behaviour may lead to misleading results, we define a multivariate model for ordinal rating responses, by introducing, for every item, a binary latent variable that discriminates aware from uncertain responses. Some independence assumptions among latent and observable variables characterize the uncertain behaviour and make the model easier to interpret. Uncertain responses are modelled by specifying probability distributions that can depict different response styles characterizing the uncertain raters. A marginal parametrization allows a simple and direct interpretation of the parameters in terms of association among aware responses and their dependence on explanatory factors. The effectiveness of the proposed model is attested through an application to real data and supported by a Monte Carlo study.

Key words: Latent variables, Marginal models, Mixture models, Ordinal data, Response styles

1 Introduction

When people are invited to express their opinion about a set of items by choosing among ordinal categories, their answers can be either the exact expression of their opinion or can correspond to a response style ensued from indecision or uncertainty. The first type of answers is of interest when one is focused on the true perceived value of the items, the second type is investigated mainly in sociological and psychological studies on the uncertainty in the process of responding. Hence, we call awareness, the exact expression of personal opinion on an item, and uncertainty, the difficulty of choosing among the ordered alternatives due to response styles, careless, unconsciousness, indecision or randomness. Uncertain respondents may have particular response styles, using only a few of the given options: someone can have a tendency to select the end points, others the middle categories, or only the positive/negative side of the rating scale. Examples are described, among many, in Yates et al. (1997), Baumgartner and Steenkamp (2001), and Luchini and Watson (2013). Such response styles can potentially distort the reliability and validity of the data analysis.

To take into account the two possible behaviours in answering, for every observable variable , rating the item , , we introduce a binary latent variable such that the conditional distribution of given models uncertain responses while, given , it describes aware responses. The latent variables define latent classes, each one corresponding to a subset of the responses such that

-

i)

the observable variables belonging to are uncertain responses and the remaining ones are aware responses,

-

ii)

the observable variables in are mutually independent and independent of the variables not in ,

-

iii)

the distribution of the variables in is a marginal of the distribution in the latent class without any aware responses,

-

iv)

the distribution of the variables not in is a marginal of the distribution in the latent class with only aware responses,

-

v)

uncertain responses are modelled through probability functions that can depict different response styles in the process of answering.

As a consequence of points iii) and iv), the marginal distributions of uncertain and aware responses, respectively, are replicated in different latent classes. For this reason, it is convenient to parameterize the joint distribution of the observable and latent variables through marginal models (Bergsma and Rudas, 2002; Bartolucci et al., 2007). The marginal parametrization facilitates the interpretation of the results, defining directly the marginal distributions of the responses in case of awareness and uncertainty and their association structure. Moreover, this parametrization greatly simplifies the inclusion of explanatory variables and the maximum likelihood estimation.

We call this model Hierarchical Marginal Model with Latent Uncertainty components (HMMLU). It permits, for each item, to determine the probability of an uncertain response and to describe its dependence on individual characteristics and on the uncertainty in other items. An HMMLU enables to distinguish the distribution of responses dictated by the awareness from those dictated by a response style due to uncertainty.

A variety of non-model-based and model-based procedures have been provided to detect and control for the effect of response styles in rating data. Non-model-based approaches (e.g. Meade and Craig, 2012) include techniques aimed at detecting uncertain responses. For instance, they use indicators such as frequency accounts of endpoint responses or the computation of the standard deviation of item scores within a respondent. According to these methods, inattentive respondents are identified and usually excluded from the analysis. Therefore, this kind of procedures essentially ends up with a data cleaning process, whose results may be strongly influenced by the adopted indices for screening for unreliable responses.

Model-based procedures that present similarities with our proposal are item response theory (IRT) models for ordinal responses and latent class factor (LCF) models, which involve a latent variable that directly affects all the observable variables to account for uncertainty. In particular, such models assume that a multidimensional latent trait underlies item responses, and that the items are locally independent when the latent trait levels and the response style are controlled for. In this context, Jin and Wang (2014), Huang (2016) and Tutz et al. (2018), among others, propose random threshold IRT models for polytomous variables where the response style is included, in different ways, as a random effect. This random component reduces or increases the distance between thresholds so that the extreme (middle) categories are more likely to be endorsed. Böckenholt and Meiser (2017) (see also von Davier and Yamamoto, 2007) present an IRT model that allows for heterogeneity of thresholds across latent classes. Other authors (e.g. Morren et al., 2011) provide LCF models where the response style is a discrete ordinal latent variable.

The model we are proposing presents some advantages on the aforementioned approaches, that can be sketched in a few key points. Firstly, we assume that every observable variable is driven by its own binary latent variable to account for a item-specific uncertainty. Consequently, we identify subgroups of respondents who can exhibit different uncertainty/response styles for subsets of items. This is not possible when only one latent variable affects all the items. Defining latent with a univocal meaning permits to distinguish uncertain and aware responses for every subset of items. The other approaches based on mixture models need to select the number of latent classes and make a subjective interpretation of their meaning. In addition, our proposal replaces the local independence hypothesis with condition ii). That is to say, only the uncertain responses are assumed independent, while association among aware responses is modelled directly.

In addition, uncertain responses are in our paper explicitly modelled by probability functions with flexible (Uniform, bell and U) shape that can take into account both randomness and tendency to the extreme or middle categories. Subgroups of uncertain respondents can also have different response styles. In other approaches, these distributions are not directly modelled. Finally, a marginal modelling in our proposal allows a simpler and direct interpretation of the parameters in terms of marginal distributions of aware responses and in terms of their association. Other approaches deal with association only indirectly, assuming independence given the latent variables.

In our opinion, the here proposed model enriches the literature with new perspectives and useful advantages.

The rest of the paper is organized as follows. We firstly present the model in the bivariate case (Sec. 2) to exemplify our proposal in a simple setting. We discuss the general case in Sections 3, describing the main assumptions (Sec. 3.1, 3.2), the parameterization adopted and identifiability issues (Sec. 3.3, 3.4). The bias in the parameter estimates introduced by ignoring uncertainty in the answers is illustrated in Section 4 via a Monte Carlo study. An application and some concluding remarks are provided in Sections 5 and 6, respectively. Analytical technicalities are reported in the two Appendices.

2 A mixture model for two responses

For clarity, it is useful to introduce the main features of our model in the simple case of two items and delay the general presentation to the next section.

Let and be two ordinal variables with support and , respectively. We assume the existence of two binary latent variables, , , such that the respondent answers the question according to his/her awareness when or his/her uncertainty when .

The joint distribution of the observable variables is specified by the mixture

| (1) |

for every and where , , , are the joint probabilities of the latent variables. Specifically they are the probabilities that both the answers are given with awareness (), both with uncertainty () or one with uncertainty and the other one with awareness ( and ).

To adapt this general mixture to the particular task of allowing for individual uncertainty in responding, we introduce some further assumptions, also important to substantially simplifying model (1). These assumptions are consistent with the idea that uncertain responses are driven by randomness.

We assume that each observable variable depends only on its latent variable , i.e.

| (2) |

and that the observable responses and are independent when at least one of them is given under uncertainty. Therefore,

| (3) |

Consequently, mixture (1) simplifies to

| (4) |

In (4), is the distribution of the aware responses, with and , , denotes the distribution of responses under uncertainty.

An important consequence of assumption (2) on the specification of model (4) is that it imposes coherence in the marginal distributions.

In fact, it ensures that marginalizing the distribution of the two responses in the last component of (4) over (or ), one get exactly the distributions of the aware responses, (or ), involved in the second (third) component of equation (4).

To facilitate the interpretation and the maximum likelihood estimation of the parameters, it is convenient to introduce a marginal parameterization (Bergsma and Rudas, 2002) for the mixture (4). The distribution of the latent variables , defined in (4) by the probabilities , , , is parameterized through a marginal logit for each latent variable, measuring the probability of being uncertain on each specific item, plus a log odds ratio. When this parameter is positive, respondents tend to have the same behaviour of uncertainty/awareness on the two items.

To parameterize the probabilities , and the probabilities , we define and logits, chosen from local, global, continuation, or reverse continuation logits. These logits, together with log odds ratios (local, global, continuation, reverse continuation), are used to parameterize the joint distribution .

Unfortunately, even when the uncertainty distributions , do not depend on unknown parameters, the model includes parameters. Therefore, identifiability constraints are necessary. For instance, under the constraint of uniform association that imposes identical log odds ratios, the number of parameters does not exceed , the number of independent observable frequencies, when . In addition, the presence of covariates may also help to make the model identifiable, as will be shown in Section 3.4.

Regarding the uncertainty distributions, the simplest choice not depending on unknown parameters is the discrete Uniform distribution, previously used by D’Elia and Piccolo (2005) to model uncertainty in the univariate case. Several more realistic distributions, not depending on any parameter, have been discussed by Gottard et al. (2016). A more flexible distribution with a shape parameter for describing different response styles will be proposed in Section 3.3.

3 A mixture model for more than two responses

In this section, we introduce the class of Hierarchical Marginal Models with Latent Uncertainty (HMMLU) that generalizes the model of Section 2 to the case of more than two responses.

Given ordinal variables , with categories , , the vector will denote one of their possible joint realizations. To model uncertainty in answering, we assume the existence of latent dichotomous variables , , whose joint realizations are called uncertainty configurations. In an uncertainty configuration, a in the position stands for an uncertain behaviour in answering the question. Hereafter, will denote the distribution of the observable variables given the latent ones and the joint distribution of the latent variables. Consequently, the joint distribution of the observable variables is the mixture

| (5) |

of components corresponding to the uncertainty configurations , analogous to (1) given in the bivariate case.

This model is well specified only by adding some assumptions, that will be introduced in Section 3.1. To this aim, further notation is required. Given the set of indices , let and denote the set of observable and latent variables, respectively. For every , we specify the subsets and . Specifically, for every uncertainty configuration , we will be interested in the subset of indices and the subset of variables observable under uncertainty. Moreover, it will be useful the configuration of no uncertain responses, i.e. Finally, for each , , we will denote with and the marginal configurations of the variables in and respectively. For the sake of simplicity, we will use the shorthand notation to indicate the marginal probabilities and to indicate the conditional probabilities

The proposed model will contemplate heterogeneity if and vary according to subject’s characteristics. We will clarify how to model the effect of covariates in Section 3.3, where respondents are grouped in strata identified by some covariate patterns. For simplicity, we will consider discrete explanatory variables only. Continuous covariates may be also taken into account.

3.1 Model assumptions

To characterize the awareness/uncertainty attitude in giving answers, we make the following assumptions that generalize those given in Section 2 to the case of , , responses. These assumptions formalize the idea that uncertainty implies randomness in responding, that a specific latent variable is needed for every item to account for uncertainty and that, for every respondent, an uncertain answer is independent of all the other (uncertain or aware) responses.

- Assumption A1:

-

Specific latent variables

For every ,

With respect to Section 2, A1 generalizes (2) and implies that every subset of observed variables depends on its corresponding subset of latent variables. Equivalently, for every , and .

- Assumption A2:

-

Context specific independence due to uncertainty

For every configuration and every ,

These independences are context specific (Hojsgaard, 2004) as they hold given a specific configuration , with the set of variables involved changing with . Assumption A2 generalizes (3). In particular, the first statement implies that, conditionally on , the variables in , describing uncertain responses, are mutually independent. The second statement says that, conditionally on , the variables in are independent of the remaining observable variables.

The next assumption is needed to facilitate the identifiability of the parameters of the model and their interpretation.

- Assumption A3:

-

Composition property

For every , , ,

is equivalent to for every and .

This assumption states that the probability function has to satisfy the composition property of conditional independence (Studeny, 2005, page 33). This property is not generally valid. By Lupparelli et al. (2009, Lemma 1) or Kauermann (1997, Lemma 1), it is equivalent to requiring that has all the Glonek-McCullagh interactions (Glonek and McCullagh, 1995) among more than two variables equal to zero. To understand the usefulness of this assumption, note that it makes sense only for . For it implies that three-way interactions are null in the joint distribution of the responses given that These restrictions, when allow for the introduction of the parameters needed to fully parameterize the joint distribution of the three binary latent variables. For or in the presence of covariates, Assumption A3 may be too restrictive or unnecessary and can be relaxed. However, it has the advantage of enhancing the interpretability of the model.

3.2 Consequences of model assumptions

The following theorems highlight some important features of the proposed model that are consequences of the assumptions in Section 3.1. In particular, Theorem 1 plays a key role in the model specification, showing how the components of mixture (5) simplify according to A1 and A2.

Theorem 1

Assumptions A1 and A2 imply that

| (6) |

where are the marginal probabilities of the uncertain responses, . Moreover, the joint distributions of aware responses are marginal distributions of .

Proof. Equation (6) derives from . The first factor of the last product simplifies to due to A1. For the second factor, it is according to A1 and the second statement of A2. The first part of the thesis follows since factorizes in the product of marginal probabilities as a consequence of the first statement of Assumption A2. The second part of the thesis is proved by noting that the equality is true according to Assumption A1 and because of

The following corollaries of Theorem 1 clarify the independence structure among observable variables implied by the proposed model.

In particular, the corollaries entail that independences among the observable variables, holding conditionally on the configuration of no uncertainty , are also valid conditionally on other configurations (Corollary 1) and, with further assumptions, unconditionally (Corollary 2).

Corollary 1

Suppose A1 and A2 hold.

-

If , with , and , then .

-

If , then for every such that .

Corollary 2

Suppose A1 and A2 hold. If and , with , and , then .

Proof. According to Corollary 1, it holds that . By Assumption A1, it results By the contraction property of conditional independence (Studeny, 2005), the previous two independences are equivalent to , which implies

| (7) |

Moreover, A1 ensures the following independences

| (8) |

Now, applying the contraction property to (7) and (8), we obtain

| (9) |

Similarly, from the hypothesis and (8), we get

| (10) |

The contraction property is further used to write the conditional independences (9) and (10) in an equivalent condition which implies .

3.3 A marginal parameterization

The mixture (5) and Theorem 1 characterize the probability function of the observable variables in terms of the uncertainty distributions , and the marginal distributions of . However, we need an explicit parameterization to tackle identifiability issues and parameter non-redundancy, to model covariate effects and to compute Maximum Likelihood (ML) estimates. The following theorem introduces a marginal parameterization (Bergsma and Rudas, 2002; Bartolucci et al., 2007; Colombi et al., 2014) which is extremely convenient to deal with these problems.

Theorem 2

Under A1, A2 and A3, the probability function can be parameterized by the following marginal interactions

-

i)

the Glonek-McCullagh interactions defined on the marginal distributions of

-

ii)

the vectors of logits of the probability functions , of the uncertain responses,

-

iii)

the vectors of log odds ratios , given by the difference between the vector of logits of and , ,

-

iv)

the vectors of log odds ratios computed on the bivariate distributions , .

Proof. The interactions and the logits parameterize the probabilities and , , respectively. The vector of logits

parametrizes the univariate marginal probability functions of and, together with the log odds ratios , parameterize the bivariate marginal probability functions.

Now, as a consequence of Assumption A3, all the Glonek-McCullagh interactions among more than two variables are set to zero. Therefore, the parameters and are sufficient to parameterize . Then, the proof follows

from (5) and Theorem 1.

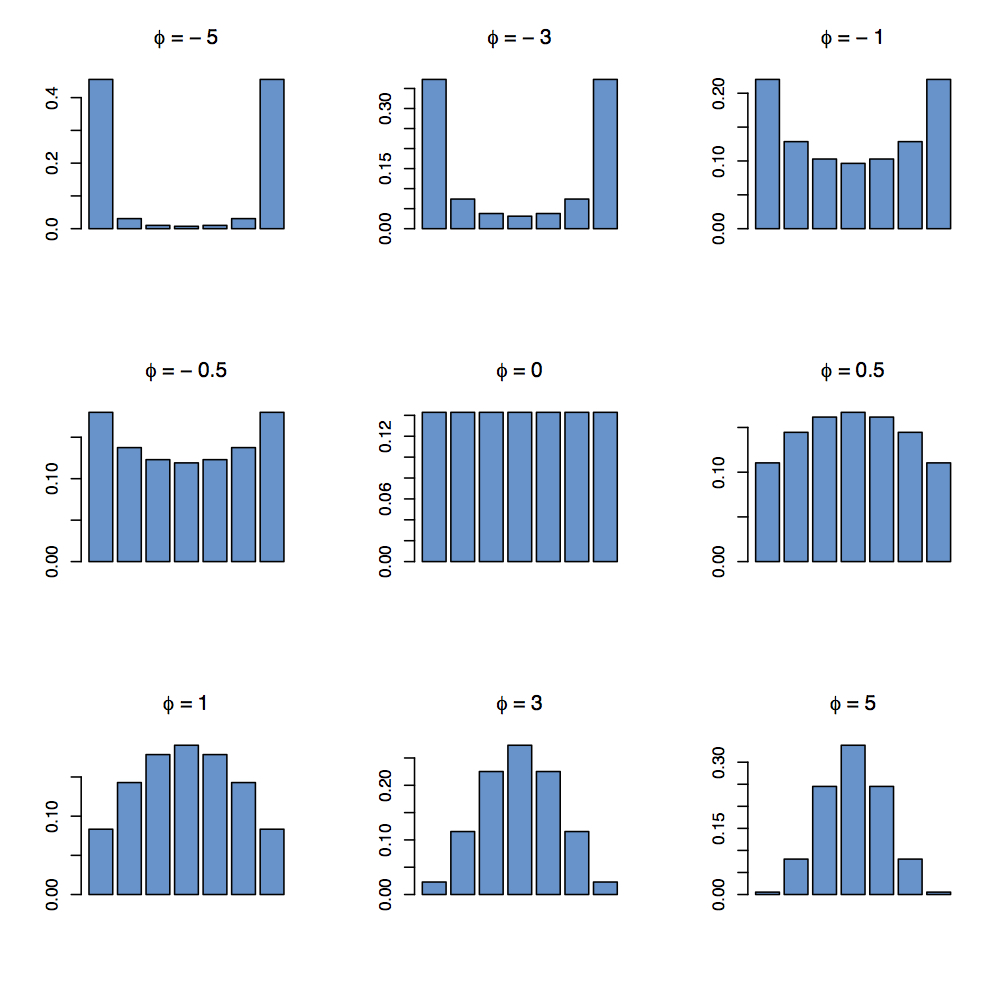

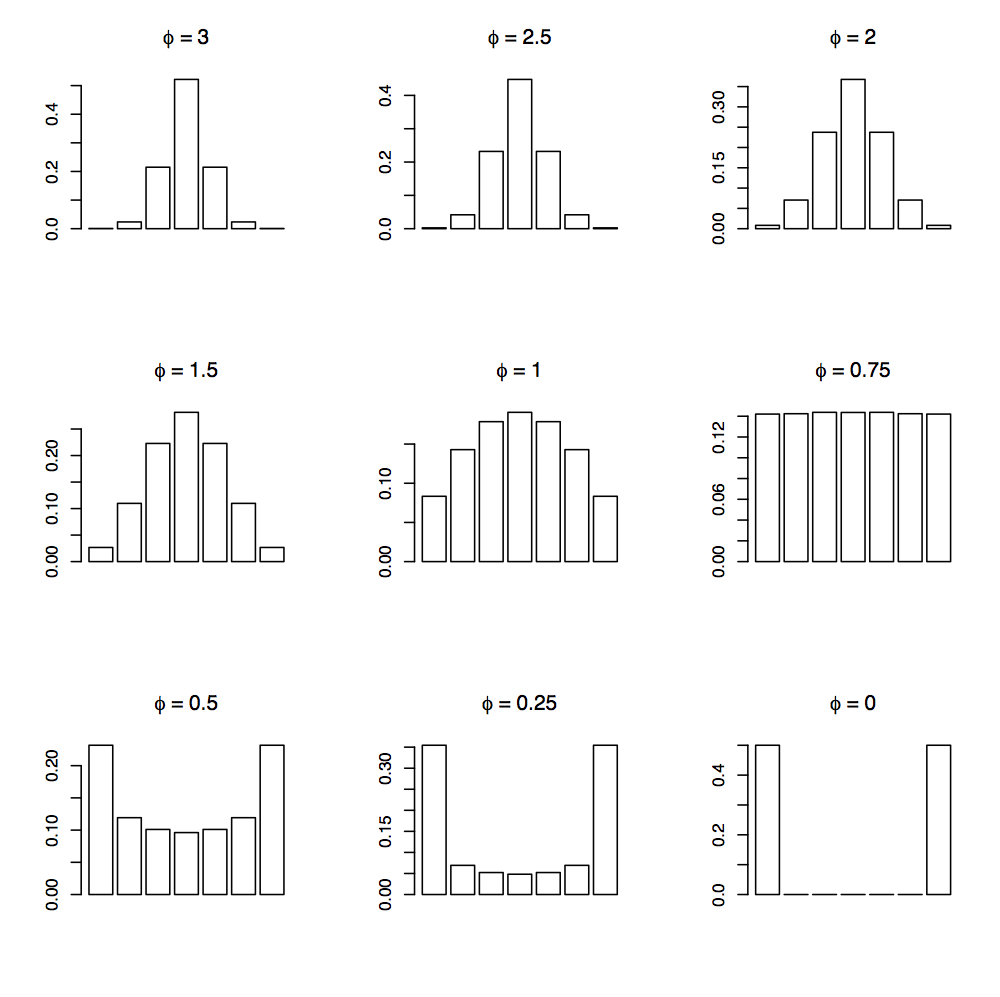

The uncertainty distributions , , mentioned at point ii) of Theorem 2 and in Section 2 for the bivariate case, can be chosen among distributions not depending on any unknown parameter. As an alternative, when possible, one can choose more flexible uncertainty distributions depending on few unknown parameters. As a possible choice, we propose the Local (Global) Reshaped Parabolic distribution. This is a function of the local (global) odds of a Parabolic distribution to the power of a parameter , which acts as a shape parameter. High values of the shape parameter correspond to the case where the uncertain response is focused on middle categories, while low values coincide with uncertainty focused on extreme categories. Consequently, the Reshaped Parabolic distribution can model different response styles as resoluteness in the extremes or middle responses (see Baumgartner and Steenkamp, 2001, among others) in the process of answering. Details are given in the Appendix B.

Notice that when the uncertainty distribution is a Local (Global) Reshaped Parabolic probability function and is a vector of local (global) logits, then , where are vectors of known constants, . This is a very useful property of this distribution, having the vector of logits linearly depending on a single parameter, for each variable.

Under multinomial sampling, the ML estimates of the parameters can be computed by maximizing the log-likelihood function via the Fisher scoring or BFGS algorithm and it is not necessary to resort to the slower EM algorithm, commonly used with mixture models. Details on ML estimates are reported in Appendix A. An R-function that maximizes the log-likelihood function and computes the ML estimates with their estimated standard errors is available from the authors. The function relies on the package hmmm (Colombi et al., 2014).

3.4 Identifiability conditions

In this section, we discuss some necessary conditions for the identifiability of the HMMLU, besides the basic requirement on the number of parameters, which is usually satisfied under Assumption A3.

Mixtures like (5) are unidentified when some parameter values make indistinguishable two components of the mixture (Früwirth Schnatter, 2006, Section 1.3). The next theorem shows that requiring is necessary to avoid this problem of non-identifiability.

Theorem 3

If there exists an such that then the HMMLU is not identifiable.

Proof. If , the vector of logits, defined on the marginal distributions of , given , is equal to which is the vector of logits of the distributions of , given In this case, the component , where is indistinguishable from the component related to the uncertain configuration where only is equal to one. Thus, there are infinite corresponding to the same marginal probability function .

Another identifiability issue is due to the case of a null that makes not depending on the parameters of the component with null weight. This problem is usually avoided by assuming that the weights of the mixture are strictly positive. The next theorem shows that in our case a less stringent condition is sufficient.

Theorem 4

Suppose A1, A2 and A3 hold. If for every couple of observable variables , there exists an uncertain configuration such that and and if for every there exists a such that and , then is a function of the parameters listed in , and of Theorem 2.

Proof. This follows because the parameters, listed in and of Theorem 2, are needed to parameterize the distributions of the responses in the configurations with . The second condition of the theorem assures the dependence of on the parameters , .

Notice that the condition when and is sufficient for the conclusion of Theorem 4. Moreover, remind that the condition that is a function of all the parameters listed in , and of Theorem 2 is only necessary for identifiability. In Appendix A, a local identifiability condition, based on the rank of the Fisher matrix, is discussed.

A further necessary condition for identifiability concerns the case of respondents grouped into strata, corresponding to distinct configurations of some discrete observable covariates. Notice that a suffix , , is added to the vectors of interactions listed in Theorem 2, , , , and to the shape parameters, , of the Reshaped Parabolic distributions, when these distributions are assumed for the uncertainty component. If Reshaped Parabolic distributions, or whatsoever distribution depending on a single parameter, model uncertain responses, the mixture components in (5) are parameterized by shape parameters , elements of the vectors and log odds ratios, entries of the vectors . Consequently, a necessary condition of identifiability is that the number of parameters is smaller than the number of free frequencies, that is it must be

Section 2 illustrates that in the bivariate case this condition is violated also when the shape parameters are null (Uniform distribution) or the uncertain distributions do not depend on unknown parameters. Therefore, restrictions on the dependence of and on covariates, defining H strata, are needed.

When , the above necessary condition of identifiability is usually satisfied but modelling parsimoniously the dependence of and on the covariates remains convenient, at least for simplifying the interpretability of the model. The shape parameters of the Rehaped Parabolic uncertain distributions may be assumed to be covariate-invariant () to reduce the number of parameters. In addition, linear models can be adopted for taking into account the dependence of on covariates. For example, if the strata are described by a categorical variable with categories, the model with parallel effect of the covariate, on the elements of the vectors

with , reduces the number of parameters from to A further simplification comes by assuming independence between the observable variables that corresponds to zero constraints on the log odds ratios .

4 A simulation study

To illustrate the performance of the proposed model and the consequences of ignoring uncertainty in the responses, we conducted a Monte Carlo simulation study from three different scenarios. For each scenario, we generated 100 random samples from the distribution (4) proposed in Section 2. On each sample, we fitted the correct model using the parameterization presented in Theorem 2, for the bivariate case. Moreover, we fitted the marginal model that ignores the existence of uncertainty in responding, wrongly assuming .

In each scenario, it is , for , and no covariate is included. The uncertainty distribution is assumed Uniform. The remaining parameter settings, specific for the three scenarios, are as follows.

Scenario A: We set the log odds ratio for the latent variables and at 2. The marginal distribution of is for . The association for the observable variables is modelled with all the local log odds ratios , for .

Scenario B: The setup is similar to Scenario A except that and are independent and the marginal distribution of is .

Scenario C: The same as in Scenario B, but the marginal distribution of is and of is .

| Scenario A | ||||||||||

|---|---|---|---|---|---|---|---|---|---|---|

| True | 0.69 | 0.41 | 0.29 | 0.69 | 0.41 | 0.29 | 3.00 | 0.85 | 0.85 | 2.00 |

| Correct model specification | ||||||||||

| MC Average | 0.74 | 0.40 | 0.29 | 0.72 | 0.41 | 0.29 | 3.09 | 0.86 | 0.88 | 2.19 |

| MC sd | 0.20 | 0.13 | 0.09 | 0.20 | 0.14 | 0.11 | 0.27 | 0.31 | 0.35 | 1.60 |

| Ignoring uncertainty | ||||||||||

| MC Average | 0.40 | 0.28 | 0.22 | 0.40 | 0.28 | 0.22 | 0.50 | |||

| MC sd | 0.11 | 0.08 | 0.07 | 0.11 | 0.09 | 0.08 | 0.04 | |||

| Scenario B | ||||||||||

| True | 0.69 | 0.41 | 0.29 | -0.29 | -0.41 | -0.69 | 3.00 | 0.85 | 0.85 | 0.00 |

| Correct model specification | ||||||||||

| MC Average | 0.72 | 0.39 | 0.30 | -0.30 | -0.40 | -0.68 | 2.59 | 0.85 | 0.90 | 0.34 |

| MC sd | 0.21 | 0.13 | 0.10 | 0.11 | 0.12 | 0.20 | 0.28 | 0.32 | 0.37 | 1.55 |

| Ignoring uncertainty | ||||||||||

| MC Average | 0.40 | 0.27 | 0.23 | -0.23 | -0.28 | -0.38 | 0.34 | |||

| MC sd | 0.11 | 0.09 | 0.08 | 0.08 | 0.08 | 0.10 | 0.04 | |||

| Scenario C | ||||||||||

| True | -1.39 | -0.00 | 1.39 | 1.39 | 0.00 | -1.39 | 3.00 | 0.85 | 0.85 | 0.00 |

| Correct model specification | ||||||||||

| MC Average | -1.37 | 0.01 | 1.37 | 1.43 | 0.01 | -1.40 | 3.19 | 0.95 | 0.85 | 0.16 |

| MC sd | 0.26 | 0.23 | 0.23 | 0.21 | 0.10 | 0.18 | 0.97 | 0.41 | 0.29 | 1.35 |

| Ignoring uncertainty | ||||||||||

| MC Average | -0.89 | 0.00 | 0.89 | 0.91 | 0.00 | -0.89 | 0.38 | |||

| MC sd | 0.09 | 0.12 | 0.10 | 0.11 | 0.08 | 0.10 | 0.04 | |||

| Scenario A | ||||||||||

|---|---|---|---|---|---|---|---|---|---|---|

| True | 0.69 | 0.41 | 0.29 | 0.69 | 0.41 | 0.29 | 3.00 | 0.85 | 0.85 | 2.00 |

| Correct model specification | ||||||||||

| MC Average | 0.69 | 0.40 | 0.29 | 0.69 | 0.40 | 0.29 | 3.00 | 0.88 | 0.88 | 1.83 |

| MC sd | 0.06 | 0.04 | 0.03 | 0.05 | 0.04 | 0.03 | 0.12 | 0.10 | 0.09 | 0.52 |

| Ignoring uncertainty | ||||||||||

| MC Average | 0.39 | 0.28 | 0.22 | 0.40 | 0.28 | 0.22 | 0.49 | |||

| MC sd | 0.03 | 0.03 | 0.03 | 0.03 | 0.03 | 0.03 | 0.01 | |||

| Scenario B | ||||||||||

| True | 0.69 | 0.41 | 0.29 | -0.29 | -0.41 | -0.69 | 3.00 | 0.85 | 0.85 | 0.00 |

| Correct model specification | ||||||||||

| MC Average | 0.69 | 0.41 | 0.29 | -0.28 | -0.40 | -0.70 | 2.94 | 0.84 | 0.85 | 0.08 |

| MC sd | 0.06 | 0.04 | 0.04 | 0.03 | 0.04 | 0.06 | 0.17 | 0.11 | 0.10 | 0.43 |

| Ignoring uncertainty | ||||||||||

| MC Average | 0.39 | 0.28 | 0.22 | -0.22 | -0.28 | -0.40 | 0.34 | |||

| MC sd | 0.04 | 0.03 | 0.03 | 0.02 | 0.03 | 0.03 | 0.01 | |||

| Scenario C | ||||||||||

| True | -1.39 | -0.00 | 1.39 | 1.39 | 0.00 | -1.39 | 3.00 | 0.85 | 0.85 | 0.00 |

| Correct model specification | ||||||||||

| MC Average | -1.39 | -0.00 | 1.39 | 1.39 | -0.00 | -1.40 | 3.12 | 0.88 | 0.84 | -0.00 |

| MC sd | 0.11 | 0.08 | 0.10 | 0.07 | 0.03 | 0.06 | 0.63 | 0.17 | 0.09 | 0.32 |

| Ignoring uncertainty | ||||||||||

| MC Average | -0.90 | -0.00 | 0.90 | 0.90 | -0.00 | -0.90 | 0.37 | |||

| MC sd | 0.03 | 0.04 | 0.03 | 0.03 | 0.02 | 0.03 | 0.01 | |||

| Scenario A | ||

|

|

|

| Scenario B | ||

|

|

|

| Scenario C | ||

|

|

|

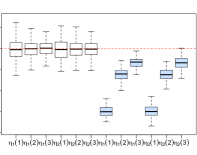

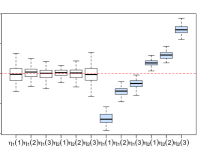

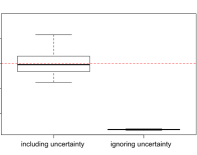

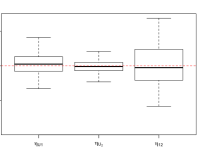

The Monte Carlo experiment was repeated for sample size and to evaluate the asymptotic behaviour of the estimates. Summaries of the simulation results are reported in Tables 1 and 2. In these tables, the local logits and log odds ratios parameters corresponding to the three scenarios are reported in the lines labelled as True. Moreover, the last three columns concern the Gloneck-McCullagh interactions defined at point of Theorem 2. As can be seen along the tables, the proposed estimation procedure is able to capture quite well the model parameters concerning the rating of the two items in the aware component (). On the other hand, the estimates for the model parameters obtained ignoring uncertainty, well illustrate the consequences of model misspecification. These consequences are better detectable in Figure 1 that presents the box plots for the Monte Carlo errors under the proposal models (white) and ignoring uncertainty (coloured).

Estimates from the model ignoring uncertainty differ substantially from the true values and underestimate or overestimate the true parameters. As a matter of fact, ignoring uncertainty corresponds to estimating logits and log odds ratios of the mixture of four components (4), when actually we are interested in the parameters of the fourth component of this mixture. In particular, in Scenario A the local logits, all positive, are underestimated. On the contrary, in Scenario B the negative local logits of are overestimated. A similar pattern can be detected in Scenario C for the positive and negative logits of the probability functions and . This is explained by the fact that in the marginal distribution of the observable variables, the logits shrink in absolute values because of the Uniform component. Analogously, in all the considered scenarios, the positive uniform association in the fourth component of the mixture (4) is underestimated if uncertainty is not taken into account.

5 Illustrative example

This example concerns the perception of the quality of working life, using data from the 5th European Working Conditions Survey (EWCS). The survey has been carried out by the European Foundation for the Improvement of Living and Working Conditions (Eurofound). We focus on respondents’ agreement on three statements: Losejob (I might lose my job in the next 6 months), Wellpaid (I am well paid for the work I do) and Career (My job offers good prospects for career advancement). The responses are recoded on a 3-point scale: disagree, neither agree nor disagree, agree. In addition, we consider two explanatory variables, Gender (0 = Male, 1 = Female) and Country (0 = Northern and 1 = Southern EU regions according to the geographic scheme in use by the United Nations). Table 3 reports the data of a sample of workers derived from those available on the Eurofound website https://www.eurofound.europa.eu.

| Gender | Male | Female | ||||||||

| Career | disagree | n. agree | agree | disagree | n. agree | agree | ||||

| n. disagree | n. disagree | |||||||||

| Country | Losejob | Wellpaid | ||||||||

| Northern | disagree | disagree | 136 | 41 | 26 | 179 | 62 | 34 | ||

| regions | n. agree n. disagree | 121 | 94 | 84 | 129 | 76 | 62 | |||

| of EU | agree | 116 | 87 | 227 | 89 | 57 | 173 | |||

| n. agree n. disagree | disagree | 45 | 10 | 7 | 30 | 14 | 6 | |||

| n. agree n. disagree | 21 | 40 | 30 | 32 | 20 | 15 | ||||

| agree | 13 | 19 | 25 | 5 | 8 | 25 | ||||

| agree | disagree | 76 | 7 | 11 | 60 | 9 | 13 | |||

| n. agree n. disagree | 36 | 21 | 4 | 13 | 9 | 6 | ||||

| agree | 18 | 9 | 12 | 10 | 10 | 18 | ||||

| Southern | disagree | disagree | 30 | 7 | 17 | 39 | 11 | 19 | ||

| regions | n. agree n. disagree | 33 | 31 | 26 | 24 | 20 | 22 | |||

| of EU | agree | 49 | 64 | 137 | 41 | 36 | 97 | |||

| n. agree n. disagree | disagree | 9 | 3 | 2 | 7 | 4 | 3 | |||

| n. agree n. disagree | 11 | 10 | 4 | 5 | 3 | 2 | ||||

| agree | 6 | 14 | 22 | 8 | 8 | 12 | ||||

| agree | disagree | 15 | 1 | 6 | 18 | 2 | 5 | |||

| n. agree n. disagree | 8 | 15 | 4 | 10 | 10 | 5 | ||||

| agree | 12 | 10 | 21 | 9 | 7 | 6 |

It is reasonable to assume that not all the respondents have been able to allocate their perceptions exactly into a category when requested to evaluate personal satisfactions and worries on their work. Hence, the observed responses could have been contaminated by a certain amount of uncertain answers. The aim of this illustrative example is to show how an HMMLU adequately takes into account for uncertainty in the responses, detects which one is perceived with more/less uncertainty, and if the proportion of uncertain answers changes with the individual characteristics. The model can also describe the association between the aware responses and their dependence on the respondent’s features, separately from the uncertain answers.

With this intent, we specify several models, with different hypotheses about the association and/or the dependence on covariates Gender and Country. In each model, we adopt Local Reshaped Parabolic distributions with shape parameters independent of the explanatory variables for the uncertain responses and we use local logits and local odds ratios to parameterize the components in (5). Table 4 summarizes the fitting of some of these models.

| Model | Hypotheses on | Hypotheses on | n.par. | Compared | -value | ||

|---|---|---|---|---|---|---|---|

| obs. responses | latent var. | models | |||||

| Unrestricted ass. | Unrestricted ass. | -9849.839 | 103 | ||||

| with covariates | with covariates | ||||||

| unrestricted eff. | unrestricted eff. | ||||||

| Homogeneous ass. | Unrestricted ass. | -9866.294 | 67 | vs | 0.6164 | ||

| with covariates | with covariates | ||||||

| unrestricted eff. | unrestricted eff. | ||||||

| Uniform ass. | Unrestricted ass. | -9906.695 | 67 | vs | 0.0000 | ||

| with covariates | with covariates | ||||||

| unrestricted eff. | unrestricted eff. | ||||||

| Homogeneous ass. | Unrestricted ass. | -9883.178 | 55 | vs | 0.0384 | ||

| with covariates | with covariates | ||||||

| additive-parallel eff. | unrestricted eff. | ||||||

| Homogeneous ass. | Unrestricted ass. | -9944.525 | 49 | vs | 0.0000 | ||

| no covariates | with covariates | ||||||

| - | unrestricted eff. | ||||||

| Homogeneous ass. | Independence | -9884.186 | 36 | vs | 0.4198 | ||

| with covariates | with covariates | ||||||

| additive-parallel eff. | additive-parallel eff. | vs | |||||

| Homogeneous ass. | Independence | -9900.109 | 30 | vs | 0.0000 | ||

| with covariates | no covariates | ||||||

| additive-parallel eff. | - |

Among the analysed models, shows the best fit on the base of the likelihood ratio test (LRT). According to this model the latent variables are independent and the association among the aware responses is homogeneous (see Kateri, 2014, Section 6.7.2). The effect of Gender and Country is modelled in by the linear models with parallel and additive effect of the covariates on the parameters and the logits for the latent variables

| (11) | ||||

| (12) |

where .

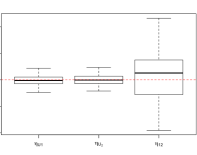

To provide an insight on the goodness-of-fit of model , in Figure 2 we show the standardized residuals, computed on joint sample frequencies and estimated probabilities, by the covariate strata. Most of the residuals are small as over do not exceed the threshold 4 in absolute value showing a satisfactory fit. A more careful inspection reveals that highest residuals correspond to the stratum of Southern workers. In marginal modelling, the fitting of the univariate marginal distributions is often the main interest and association parameters are regarded as nuisance parameters. From this point of view, the standardized marginal residuals, based on univariate sample frequencies and estimated probabilities, are relevant. Here, the marginal residuals highlight that the marginal distributions are well fitted, except for the distribution related to Career in Southern EU regions (see Table 5).

| Male North | Female North | Male South | Female South | |

|---|---|---|---|---|

| Losejob | ||||

| disagree | -0.510 | 0.331 | -0.519 | 1.533 |

| n. agree n. disagree | 1.020 | -0.759 | 0.871 | -2.073 |

| agree | -0.510 | 0.427 | -0.352 | 0.540 |

| Wellpaid | ||||

| disagree | -0.861 | 0.903 | -1.256 | 2.336 |

| n. agree n. disagree | 2.500 | -2.545 | 1.047 | -1.678 |

| agree | -1.639 | 1.642 | 0.209 | -0.658 |

| Career | ||||

| disagree | 0.222 | 1.468 | -7.875 | 5.705 |

| n. agree n. disagree | 1.065 | -1.600 | 7.082 | -7.877 |

| agree | -1.287 | 0.133 | 0.794 | 2.173 |

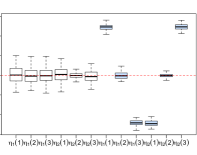

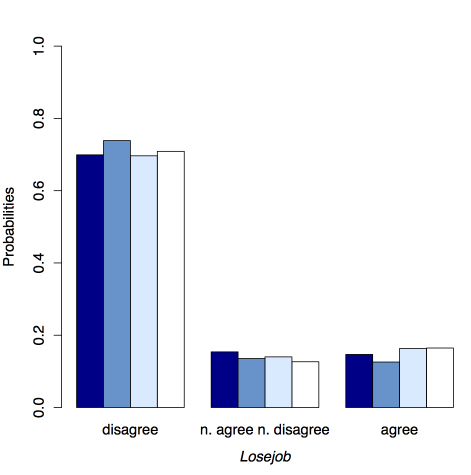

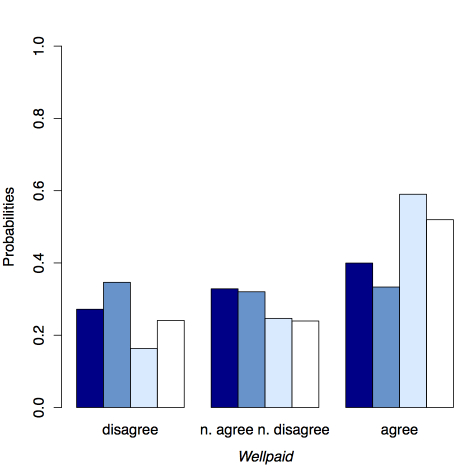

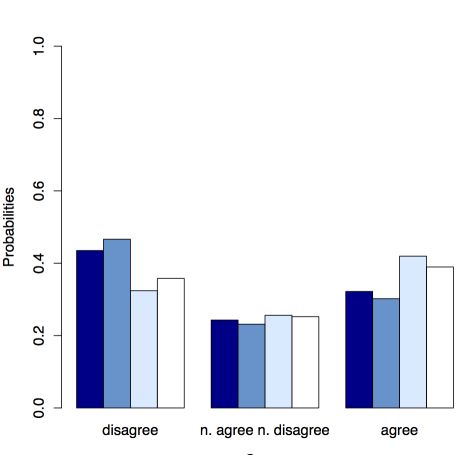

The estimated parameters of model are reported in Tables 6 and 7. In particular in Table 6, the estimates of the parameters in equation (11) highlight how workers’ perceptions of the three aspects of their job vary according to Gender and Country. Gender has the same impact on the responses, whereas logits decrease for Southern workers when the question is Losejob and increase for Wellpaid and Career. The corresponding fitted distributions are illustrated in Figure 3 (top and bottom-left).

| Losejob | Wellpaid | Career | |||||||||

| Parameters | MLE | s.e. | -value | MLE | s.e. | -value | MLE | s.e. | -value | ||

| -1.5571 | 0.0655 | 0.0000 | 0.2503 | 0.0619 | 0.0001 | -0.3579 | 0.1470 | 0.0149 | |||

| -0.2918 | 0.1440 | 0.0427 | 0.1569 | 0.0476 | 0.0010 | -0.0586 | 0.1462 | 0.6885 | |||

| -0.2243 | 0.0455 | 0.0000 | -0.2252 | 0.0271 | 0.0000 | -0.1088 | 0.0267 | 0.0000 | |||

| -0.1893 | 0.0646 | 0.0034 | 0.6288 | 0.0371 | 0.0000 | 0.3732 | 0.0327 | 0.0000 | |||

| Losejob,Wellpaid | Losejob,Career | Wellpaid,Career | |||||||||

| 0.0826 | 0.0898 | 0.3572 | 0.3370 | 0.1034 | 0.0011 | 1.3550 | 0.1444 | 0.0000 | |||

| -1.2757 | 0.2092 | 0.0000 | -1.4139 | 0.2787 | 0.0000 | 0.3530 | 0.1180 | 0.0028 | |||

| -0.8518 | 0.1046 | 0.0000 | -0.6649 | 0.1207 | 0.0000 | 7.0451 | 2E+02 | 0.9799 | |||

| -0.5245 | 0.4309 | 0.2234 | -8.1503 | 1E+03 | 0.9960 | 1.5291 | 0.1256 | 0.0000 | |||

|

|

|

|

| Parameters | MLE | s.e. | -value | MLE | s.e. | -value | MLE | s.e. | -value | ||

|---|---|---|---|---|---|---|---|---|---|---|---|

| 2.1636 | 0.4410 | 0.0000 | 3.2589 | 0.5784 | 0.0000 | 1.2839 | 0.2995 | 0.0000 | |||

| -0.3103 | 0.1847 | 0.0930 | -0.8157 | 0.1575 | 0.0000 | -0.1601 | 0.1236 | 0.1953 | |||

| -0.9766 | 0.2147 | 0.0000 | -1.3943 | 0.4931 | 0.0047 | 0.3109 | 0.2113 | 0.1411 | |||

The estimated log odds ratios in the last rows of Table 6 suggest that aware responses on Wellpaid and Career are quite positively associated. On the contrary, as reasonably expected, Losejob, is mainly negatively associated with the other responses. This result seems reasonable since workers who are worried about the loss of their job, probably do not meet good opportunities in their career or satisfaction in their remuneration.

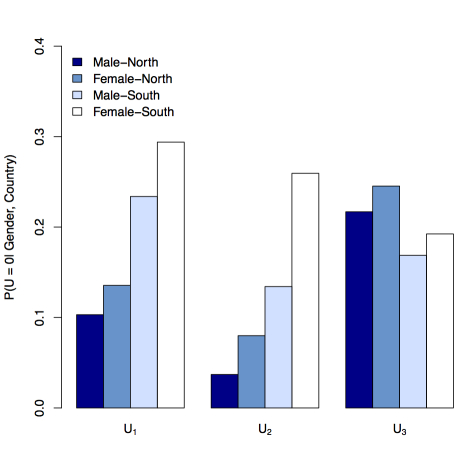

The estimates of the parameters in equation (12), reported in Table 7, and the corresponding probabilities in Figure 3 (bottom-right) show how the propensity to giving uncertain responses on Losejob and Wellpaid differs between male and female and among countries. The question on Career advancements has high proportion of uncertain responses, but women living in the South of EU tend to give uncertain answer more than the others when evaluating how plausible is losing their job.

The estimated shape parameters of the Local Reshaped Parabolic distributions that model conditionally on , are all negative (, , ), corresponding to U-shaped distributions. This suggests that people giving uncertain answers tend to split into optimistic and pessimistic behaviours. As for the comparison between model and the analogous estimated under the constraints the test results , the hypothesis of Uniform distribution for the uncertain responses has to be rejected.

6 Concluding remarks

The proposed mixture model, HMMLU, is able to distinguish two kinds (awareness and uncertainty) of behaviour that people may adopt, even unconsciously, when faced with rating questions. It allows to study the distribution of the aware responses and their dependence on covariate and to model the association among responses given without uncertainty. Moreover, the HMMLU enables to specify different association structures among the binary latent variables governing the aware/uncertain behaviours and their dependence on covariates. As shown in Section 4, ignoring uncertainty can result in erroneous estimates both of the rating distribution and the association parameters.

To model the uncertain responses, we introduce a class of distributions with a shape parameter that models different response styles and admits the Uniform distribution as a special case. Nonetheless, the problem of selecting an adequate distribution of uncertainty is still an open problem and deserves further research.

A second critical aspect is that general results on identifiability are lacking for HMMLU as for many other latent variable models. The issue is discussed in Sections 3.3, 3.4 and Appendix A, where we provided some necessary conditions. Empirical evidence on local identifiability, at least in a neighbourhood of the maximum likelihood estimate, is based on the fact that the Fisher matrix was never singular in the numerical examples and simulations we performed. Moreover, a data independent assessment of local identifiability is provided by the numerical algorithm described by Forcina (2008).

Another point not considered in this paper is to test if uncertainty/awareness rules only some or none of the responses. Testing such hypotheses represents a non-standard problem as, under the null hypothesis, some parameters are on the boundary of their parametric space. For this reason, a comparison among HMMLU and models which do not contemplate uncertainty is not immediate. This problem can be solved, when the uncertain distribution is supposed to be Uniform, along the lines of Colombi and Giordano (2016) who dealt with the problem of testing uncertainty in a different multivariate model. However, the presence of shape parameters in the uncertainty distributions make the issue more complicated, since testing a no uncertainty hypothesis produces non-identifiability of these parameters. Such an issue deserves an in-depth study.

Acknowledgments

The authors are grateful to Alan Agresti for his thoughtful and suggestive comments.

Appendix A: Inference on marginal parameters

Analytical details to make inference on the marginal parameters of HMMLU models are here provided.

Let be the vector of the joint probabilities of the configurations of the observable variables and the configurations of the latent ones in the covariate stratum, .

A marginal parameterization of in terms of a vector of generalized marginal interactions is defined by the one-to-one mapping (Lang and Agresti, 1994). Here is a matrix of row contrasts and a matrix of and values to determine the marginal probabilities of interest (Bartolucci et al., 2007). Specifically, the marginal interactions in are contrasts of logarithms of sums of probabilities in (logits, log odds ratios, of any type, and contrasts of them).

Calculations are mainly based on the key result by Bartolucci et al. (2007) that the transformation is a diffeomorphism from the parameters of the saturated log-linear model for

to the interactions . Here is the design matrix.

For every non-empty subset of , let be the sub-vector of of the generalized interactions involving only variables in the set . In the proposed parameterization, every , , is a vector of interactions defined in the marginal distribution of the variables belonging to . These are Glonek-McCullagh interactions that parameterize the vector of the joint probabilities of the latent variables. Moreover, to assure the smoothness of the parameterization (Bergsma and Rudas, 2002), every vector of interactions , , is defined in the marginal distribution of the variables in the set . These interactions parameterize the vector of the probabilities of the responses given the latent variables. All the previous interactions are defined by taking as the reference or base-line category of the logits of the latent variables (see Colombi et al. (2014) for a description of how interactions are built starting from the logit types assigned to the variables).

Assumptions A1-A3 make some interactions null. Interactions defined in the joint distribution of the variables in the sets and , , , and those , , defined in the marginal distribution of the variables belonging to , are the only ones not constrained to be zero and correspond to the parameters involved in of Theorem 2.

We can express therefore the parameter constraints through the linear model , , where is the vector of unknown parameters, including the shape parameters of the Reshaped Parabolic distributions. This linear model accounts for the dependence structure of both latent and observed variables and the effects of covariates.

We now provide the analytical details for the ML estimation of . To this regard, we utilize some results by Forcina (2008), as the HMMLU of Section 3 can be viewed as a special case of his Extended Latent Class Model.

We start from the mentioned diffeomorphism to obtain

with .

Moreover, denote the saturated log-linear model for the vector of the joint probabilities of the responses in the stratum by

where is the marginalization matrix with respect to the latent variables, is the design matrix of the log-linear model and is a vector of contrasts of logarithms of the elements of , with . By the chain rule of matrix differential calculus (Magnus and Neudecker, 2007), we get where It also follows that which is the main result needed for calculating the Fisher matrix.

Let indicate the observed joint frequencies of the responses in the stratum of size and be the total sample size. Under multinomial sampling within every stratum, the log-likelihood function is and the row vector of the score functions is From the previous results, the averaged Fisher matrix easily follows If then

Since is non singular, is non singular if and only if the matrix , obtained by row-binding the matrices , is of full column rank. Thus implies that the vector of parameters , at which is computed, is locally identifiable (Rothenberg, 1971; Forcina, 2008).

Hence, denotes the vector of the true parameters and , and the other just introduced matrices, will be computed at this value. If , from the standard MLE theory, it follows that has an asymptotic Normal distribution with null expected value and variance matrix .

Appendix B: Reshaped Parabolic distributions

Given an ordinal categorical variable with categories, the Reshaped Parabolic distribution is defined by the powers of the local odds or by the powers of the global odds, , of the discrete Parabolic probability function

with distribution function

Local and global odds lead to two different Reshaped Parabolic probability functions which will be called Local and Global Reshaped, respectively. The Local Reshaped Parabolic distribution family contains, as a special case with , the Uniform distribution, for positive it is bell shaped and for negative it is U-shaped. The Global Reshaped Parabolic distribution is defined only for and assigns probability to the two extreme categories when . For it is bell shaped and U-shaped for . Both Local and Global Reshaped Parabolic are symmetric, have expected value independent of and variance which is a decreasing function of . Figure 4 shows some examples.

|

|

Distributions similar to the Reshaped Parabolic can be obtained from the powers of logits of other symmetric probability functions which do not depend on unknown parameters such as, for example, the Triangular probability function

where is the Dirac measure.

References

- Bartolucci et al. (2007) Bartolucci, F., R. Colombi, and A. Forcina (2007). An extended class of marginal link functions for modelling contingency tables by equality and inequality constraints. Statistica Sinica 17, 691–711.

- Baumgartner and Steenkamp (2001) Baumgartner, H. and J. B. E. Steenkamp (2001). Response styles in marketing research: a cross-national investigation. Journal of Marketing Research 38(2), 143–156.

- Bergsma and Rudas (2002) Bergsma, W. P. and T. Rudas (2002). Marginal models for categorical data. Annals of Statistics 30(1), 140–159.

- Böckenholt and Meiser (2017) Böckenholt, U. and T. Meiser (2017). Response style analysis with threshold and multi-process IRT models: a review and tutorial. British Journal of Mathematical and Statistical Psychology 70(1), 159–181.

- Colombi and Giordano (2016) Colombi, R. and S. Giordano (2016). A class of mixture models for multidimensional ordinal data. Statistical Modelling 16(4), 322–340.

- Colombi et al. (2014) Colombi, R., S. Giordano, and M. Cazzaro (2014). hmmm: an R package for hierarchical multinomial marginal models. Journal of Statistical Software 59(11), 1–25.

- D’Elia and Piccolo (2005) D’Elia, A. and D. Piccolo (2005). A mixture model for preferences data analysis. Computational Statistics & Data Analysis 49(3), 917–934.

- Forcina (2008) Forcina, A. (2008). Identifiability of extended latent class models with individual covariates. Computational Statistics & Data Analysis 52(12), 5263–5268.

- Früwirth Schnatter (2006) Früwirth Schnatter, S. (2006). Finite Mixture and Markov Switching Models. Springer, New York, USA.

- Glonek and McCullagh (1995) Glonek, G. F. and P. McCullagh (1995). Multivariate logistic models. Journal of the Royal Statistical Society. Series B (Methodological) 57(3), 533–546.

- Gottard et al. (2016) Gottard, A., M. Iannario, and D. Piccolo (2016). Varying uncertainty in CUB models. Advances in Data Analysis and Classification 10(2), 225–244.

- Hojsgaard (2004) Hojsgaard, S. (2004). Statistical inference in context specific interaction models for contingency tables. Scandinavian Journal of Statistics 31(1), 143–158.

- Huang (2016) Huang, H. Y. (2016). Mixture random-effect IRT models for controlling extreme response style on rating scales. Frontiers in Psychology 7, 1706.

- Jin and Wang (2014) Jin, K. Y. and W. C. Wang (2014). Generalized IRT models for extreme response style. Educational and Psychological Measurement 74(1), 116–138.

- Kateri (2014) Kateri, M. (2014). Contingency Table Analysis: Methods and Implementation Using R. Springer.

- Kauermann (1997) Kauermann, G. (1997). A note on multivariate logistic models for contingency tables. Australian & New Zealand Journal of Statistics 39(3), 261–276.

- Lang and Agresti (1994) Lang, J. B. and A. Agresti (1994). Simultaneously modeling joint and marginal distributions of multivariate categorical responses. Journal of the American Statistical Association 89(426), 625–632.

- Luchini and Watson (2013) Luchini, S. and V. Watson (2013). Uncertainty and framing in a valuation task. Journal of Economic Psychology 39, 204–214.

- Lupparelli et al. (2009) Lupparelli, M., G. M. Marchetti, and W. P. Bergsma (2009). Parameterization and fitting of bi-directed graph models to categorical data. Scandinavian Journal of Statistics 36(3), 559–576.

- Magnus and Neudecker (2007) Magnus, J. R. and H. Neudecker (2007). Matrix Differential Calculus with Applications in Statistics and Econometrics. Third edition. John Wiley & Sons.

- Meade and Craig (2012) Meade, A. W. and S. B. Craig (2012). Identifying careless responses in survey data. Psychological methods 17(3), 437–455.

- Morren et al. (2011) Morren, M., J. P. Gelissen, and J. K. Vermunt (2011). Dealing with extreme response style in cross-cultural research: a restricted latent class factor analysis approach. Sociological Methodology 41(1), 13–47.

- Rothenberg (1971) Rothenberg, T. (1971). Identification in parametric models. Econometrica 39, 577–591.

- Studeny (2005) Studeny, M. (2005). Probabilistic Conditional Independence Structures. London, Springer.

- Tutz et al. (2018) Tutz, G., G. Schauberger, and M. Berger (2018). Response styles in the partial credit model. Applied Psychological Measurement, OnlineFirst, doi.org/10.1177/0146621617748322.

- von Davier and Yamamoto (2007) von Davier, M. and K. Yamamoto (2007). Mixture-distribution and hybrid rasch models. In M. von Davier and C. H. Carstensen (Eds.), Multivariate and Mixture Distribution Rasch Models, pp. 99–115. Springer.

- Yates et al. (1997) Yates, J. F., J. W. Lee, and J. G. Bush (1997). General knowledge overconfidence: cross-national variations, response style, and “reality”. Organizational Behavior and Human Decision Processes 70(2), 87–94.