A probability-free and continuous-time explanation of the equity premium and CAPM

Abstract

This paper gives yet another definition of game-theoretic probability in the context of continuous-time idealized financial markets. Without making any probabilistic assumptions (but assuming positive and continuous price paths), we obtain a simple expression for the equity premium and derive a version of the capital asset pricing model.

The version of this paper at http://probabilityandfinance.com (Working Paper 44) is updated most often.

1 Introduction

This paper reviews and extends previous work in which we derived the existence of an equity premium and the validity of a Capital Asset Pricing Model (CAPM) from a purely game-theoretic hypothesis of market efficiency, without assuming the existence of probabilities for security prices.

For simplicity, we consider only two securities, a stock and a traded market index . We also make the following simplifying assumptions:

-

•

Trading in and continues indefinitely. (The time horizon is infinite.)

-

•

The prices of and are always positive and continuous.

-

•

The interest rate is zero.

All these assumptions can be relaxed.

Our mathematical results have a practical interpretation if one adopts the hypothesis that the index is efficient, in the sense that a strategy for trading in and will not multiply the capital it risks by a factor many times larger than what would be achieved by buying and holding . We call this the Efficient Index Hypothesis (EIH) for .

A typical mathematical result in this paper asserts the existence of a trading strategy that will multiply the capital it risks by a factor many times larger than what would be achieved by buying and holding unless the price trajectories of and have a particular property. Here are some properties we consider:

-

•

grows at a rate determined by its volatility. (This is the equity premium.)

-

•

has the properties of geometric Brownian motion when time is appropriately rescaled.

-

•

obeys a CAPM with respect to .

In each case, we prove the existence of a trading strategy that beats by a large factor if the property does not hold. If you subscribe to the EIH for , then you expect the property to hold.

Our EIH is explained more fully in Section 2, where we specify the trading strategies we consider, define an extended class of approximate capital processes (supermartingales), and state the associated definition of upper probability. An upper probability measures how little initial capital must be risked to obtain unit capital if an event happens and thus how unlikely that event is.

We study the index in Sections 3–5. In Section 3 we define ’s cumulative growth rate and relative quadratic variation; these exist in a strong sense under the EIH: the trader can become infinitely rich as soon as they cease to exist. In Sections 4 and 5 we consider strategies for trading in and show that under the EIH it grows at a rate determined by its relative quadratic variation. This growth is the equity premium.

Section 6 continues Section 3 by defining quantities involving both and . Section 7 then derives a CAPM that relates these quantities to each other and includes most of our results about the equity premium as special cases.

One purpose of this paper is to clarify the relation between two different methods that we used in previous work. We first established a probability-free CAPM fifteen years ago; essentially, our version was the conjunction of a probability-free version of the standard CAPM and a probability-free expression for the equity premium. We did this first in discrete time [18], and then we extended the argument to continuous time using nonstandard analysis [17]. The method used in those papers involved mixing, in a certain sense, the price paths of and (in the case of CAPM) or mixing and cash (in the case of the equity premium). Ten years later, without using nonstandard analysis, one of us derived a probability-free version of the Dubins–Schwarz theorem [14], effectively reducing the probability-free setting to the Bachelier model, which for positive prices becomes the Black–Scholes model after a time change. And the Black–Scholes model allows us to use standard probabilistic tools, including Girsanov’s theorem, to obtain a stronger form of our version of the CAPM [12, 11, 13].

In this paper we apply and compare the two methods, mixing [18, 17] and probabilistic [12, 11, 13], implementing them both without using nonstandard analysis. In Section 5, we study the equity premium using the mixing method, and in Section 4, we study it using the probabilistic method in combination with the probability-free Dubins–Schwarz theorem. The results from the probabilistic method are stronger than those from the mixing method, in the sense that they assert higher lower probabilities for the approximations formalizing the equity premium phenomenon, but the difference is not great. Since the probability-free Dubins–Schwarz theorem is only applicable to one security, we cannot apply the probabilistic method to the CAPM, which involves both and . Therefore, we use the mixing method to obtain our version of the CAPM in Section 7.

2 The Efficient Index Hypothesis

The sample space of this paper is the set of all pairs of positive continuous functions and . Each will be identified with the function defined by , . Intuitively, is the price path of an index and is that of a stock or another financial security. We assume, for simplicity, that .

We equip with the -algebra generated by the functions , (i.e., the smallest -algebra making them measurable). We often consider subsets of and functions on that are measurable with respect to . As shown in [15], the requirement of measurability is essential: without measurability, it is too easy to become infinitely rich infinitely quickly.

An event is an arbitrary subset of (we will add the qualifier “-measurable” when needed), a random vector is an -measurable function of the type for some , and an extended random variable is an -measurable function of the type . A stopping time is an extended random variable such that, for all and in ,

where stands for the restriction of to the intersection of and ’s domain. A random vector is said to be -measurable, where is a stopping time, if, for all and in ,

As customary in probability theory, we will often omit explicit mention of when it is clear from the context.

A simple trading strategy is a pair , where:

-

•

is a nondecreasing sequence of stopping times such that, for each , ;

-

•

for each , is a bounded -measurable -valued random vector.

A process is a function . The simple capital process corresponding to a simple trading strategy and initial capital is defined by

where “” stands for dot product and the zero terms in the sum are ignored (which makes the sum finite for each ).

The vector tells the trader how many units of and to hold between time and , and thus is his capital at time . Negative components for indicate short selling. Because and are continuous, a strategy can sell them short and yet produce a nonnegative simple capital process ; the and can be chosen so that the short selling always stops before gets below zero.

For and , we often let stand for and for ; since we often omit , this makes (resp. ) synonymous with (resp. ). We will often use the generic notation .

Let us say that a class of processes is -closed if the process

| (1) |

is in whenever each process is in . A nonnegative process is a test supermartingale if it belongs to the smallest -closed class of processes containing all nonnegative simple capital processes. Intuitively, test supermartingales are nonnegative capital processes (as they can be approximated by nonnegative simple capital processes; in fact, they can lose capital as the approximation is in the sense of ). We call processes of the type , where is a test supermartingale, test -supermartingales; they are like test supermartingales but use as the numéraire.

The initial value of a test supermartingale is always a constant. Given a subset of , we set

| (2) |

and

| (3) |

ranging in each case over the test supermartingales.111Here, as always in game-theoretic probability, upper probability is a special case of upper expected value. Upper expected values and , where , are defined by substituting the function for in (2) and (3), respectively. We do not use in this paper but do use on one occasion. We call ’s upper probability, and we call its -upper probability. The definition (3) can be rewritten as

| (4) |

ranging over the test -supermartingales.

Recalling that for all , we see from (3) that a value of close to zero indicates the existence of a trading strategy that beats the index by a large factor if happens. The EIH for says that we should not expect to beat by a large factor, and so we should not expect to happen. The EIH for has a lot of empirical support when is an index, such as the S&P500, which can be approximately traded with low transaction costs; see, e.g., [6, 7].

We do not interpret small values of in the same way. Saying that will not happen when is small would amount to adopting an efficiency hypothesis for cash or for a bank account (recall that the interest rate is zero)—i.e., to asserting that no trading strategy will beat holding cash by a large factor. We do not assert this. In fact, the EIH for nontrivial implies the opposite. It implies that we can expect holding to beat holding cash by an infinite factor as time goes to infinity; this is a consequence of our results for the equity premium in Sections 4 and 5. (The efficiency hypothesis for cash, in contrast, implies that the price of , or any other traded security, will tend to a constant. See Theorem 3.1 in [14].)

Remark 2.1.

An equivalent definition of the class of test supermartingales can be given using transfinite induction over the countable ordinals (see, e.g., [2], 0.8). Namely, define as follows:

-

•

is the class of all nonnegative simple capital processes;

-

•

for , if and only if there exists a sequence of processes in such that (1) holds.

It is easy to check that the class of all test supermartingales is the union of the nested family over all countable ordinals . The class of a test supermartingale is defined to be the smallest such that ; in this case we will also say that is of class .

Remark 2.2.

Remark 2.3.

Our definition of upper probability is similar to the one given by Perkowski and Prömel [8] (who modified the definition given in [14]). The main differences are that Perkowski and Prömel define the upper probability (2) using the test supermartingales in the class rather than (in the notation of Remark 2.1) and that they consider a finite horizon (our time interval is instead of their ). The proofs of our results given below work for any , , in place of .

Remark 2.4.

The motivation for our terminology is the analogy with measure-theoretic probability. Namely, let us suppose that and are local martingales on a measure-theoretic probability space. Each simple capital process is a local martingale. Since each nonnegative local martingale is a supermartingale ([9], p. 123), nonnegative simple capital processes are supermartingales. By Fatou’s lemma, is a supermartingale whenever are nonnegative supermartingales:

where . Therefore, our definition gives a subset of the set of all nonnegative measure-theoretic supermartingales.

Remark 2.5.

Let us check that, in the measure-theoretic setting of Remark 2.4 (where and are local martingales), for each -measurable . (In this sense our definition (2) of is not too permissive, unlike the definition ignoring measurability in [15].) It suffices to establish the “maximal inequality” for nonnegative measure-theoretic supermartingales with a constant in the form

To check this, notice that, for each ,

Remark 2.6.

Let us say that is a class test -supermartingale, where is a countable ordinal, if is a class test supermartingale, as defined in Remark 2.1. For each countable ordinal and each class test -supermartingale we fix a sequence of test -supermartingales of smaller classes such that (as usual, we are using the axiom of choice freely).

The following lemma says that the definition (4) is robust in that the in it can be replaced by or even .

Lemma 2.7.

For any ,

| (5) |

ranging over the test -supermartingales.

Proof.

The only nontrivial part of the equality in (5) is the inequality “”, and it is clear that we can replace “” by “”. This is what we will be proving.

For each test -supermartingale with we will define another test -supermartingale , satisfying , as follows. If is a simple capital process, set

If is a class test -supermartingale, we set , where is the fixed sequence of -supermartingales of classes smaller than that of (see Remark 2.6).

It suffices to check that whenever . We will prove that whenever . Fix a . The proof is by transfinite induction. For nonnegative simple capital processes this is true by definition. Now let be a class test -supermartingale such that . Fix such that . Then for the fixed of smaller classes, and we have from some on. By the inductive assumption, from some on, which implies . ∎

We call a subset of a time-dependent property of the prices and . We say that a time-dependent property holds quasi-always (q.a.) if there exists a test supermartingale (or equivalently, a test -supermartingale) such that and, for all and ,

| (6) |

To put it differently, the trader can become infinitely rich as soon as such is violated. Many of the results in this paper involve showing that some time-dependent property (such as the existence of relative quadratic variation or growth rate up to time ) holds quasi-always and therefore can be expected to hold always under the EIH.

Remark 2.8.

In previous work on the topics of this paper (see for example [14]), we used only the very weak form of the EIH that states an event will not happen if it allows a trader to become infinitely rich infinitely quick. This weak hypothesis follows from the efficiency hypothesis for cash (which implies that an event with -probability zero will not happen) just as easily as from the EIH for (which implies that an event with -probability zero will not happen). Indeed, if we set

when is a time-dependent property, then holding quasi-always implies ; see (6). For this reason, we did not introduce in this previous work. Instead we discussed our results in terms of , which is easier to define.

3 Existence of some basic quantities (1)

In this section we do the preparatory work needed to state our results about the equity premium; namely, we show the existence of all the quantities required in their statements.

All quantities will be defined in terms of the sequences of stopping times and

| (7) |

for ; here is a positive integer, . The quadratic variation of on the log scale (or relative quadratic variation of ) can be measured by the sums of squares of the relative increments of ,

| (8) |

It follows from Theorem 3.1 in [14] and the properties of measure-theoretic Brownian motion that the limit of as exists quasi-always; however, we will also check this independently in Section 6. The limit will be denoted . Moreover, the convergence is uniform on compact intervals, so the limit is continuous quasi-always. (Formally, the property “ as uniformly over ” of and holds quasi-always.)

Remark 3.1.

Of course, we could have defined as the limit of

as .

The quantity measures the accumulated volatility of the index by time . It can be interpreted as the intrinsic time that elapsed by the moment of physical time; unlike physical time, intrinsic time flows faster during intensive trading.

We will simplify our exposition by requiring that Reality ensure that the function exists and . (Essentially, that the market exists forever and trading in it never dies out.)

The cumulative relative growth of the index by time is

| (9) |

(where is the capital version of the Greek letter ). The existence of the limit of as and a simple expression for it are provided by the following lemma.

Lemma 3.2.

The limit exists and satisfies, quasi-always,

Proof.

Let us show that the limit exists and is uniform over compact time intervals quasi-always. Applying

to

| (10) |

we obtain

and it remains to notice that the last added, , is since the denominator in it can be ignored (remember that is positive). ∎

4 Equity premium (1): reduction to the Black–Scholes model

In this section we will state two forms of our equity premium result: as a central limit theorem (which is trivial in the context of Brownian motion) and as a law of the iterated logarithm. Remember that we assume that .

Lemma 4.1.

Set for each . As function of , is Brownian motion with respect to .

Remark 4.2.

Proof of Lemma 4.1.

Let be a Borel set in . The set is time-superinvariant (as defined in [14], Section 3). According to Theorem 3.1 in [14], coincides with the standard Wiener measure of . This measure is concentrated on the positive functions whose quadratic variation is the identity. Applying the time transformation , where to those functions, we obtain a probability measure (the pushforward of under ) concentrated on the functions whose relative quadratic variation is the identity; we know that . By the standard measure-theoretic Dubins–Schwarz theorem, will coincide with the distribution of the measure-theoretic martingale

| (11) |

being the standard Brownian motion (started at ). (Notice that (11) is a special case of geometric Brownian motion, i.e., the Black–Scholes model.) Therefore,

Remark 4.3.

Corollary 4.4.

As function of , is Brownian motion with respect to .

Proof.

According to Lemma 4.1, is standard Brownian motion w.r. to . To change the numéraire we apply Girsanov’s theorem (see, e.g., [4], Corollary 3.5.2; this version, unlike Theorem 3.5.1 in [4], does not require the usual conditions). It suffices to show, for each , that , , is Brownian motion over with respect to . Fix such a . By Girsanov’s theorem, is standard Brownian motion w.r. to the measure on whose density with respect to (as defined in the proof of Lemma 4.1 but restricted to ) is

Let map each to the path ; we will continue to use the notation for the function that maps each to the path . Let us check that is the pushforward of under : for each Borel , by the definition (3) and Remark 4.3,

Let us first derive a central limit theorem for the index from Corollary 4.4. Let be the upper -quantile of the standard Gaussian distribution ; i.e., is defined by the requirement that , where .

Corollary 4.5.

If and are positive constants,

| (12) |

We can interpret (12) by saying that there is a prudent trading strategy that beats the index by a factor of nearly unless is close to in the sense

In other words, the efficient index can be expected to outperform cash -fold. The case in Corollary 4.5 is trivial, but we do not exclude it to simplify its statement; the upper quantile is understood to be when .

If we are only interested in a lower or upper bound on , we can use the following corollary.

Corollary 4.6.

Let and be as before. Then

and

Corollaries 4.5 and 4.6 follow immediately from Corollary 4.4. Corollary 4.4 also immediately implies the following law of the iterated logarithm for the equity premium:

Corollary 4.7.

It is -almost certain that

and

5 Equity-premium (2): mixing method

In this section we will discuss an alternative approach to the equity premium phenomenon, which will also be used to derive a probability-free CAPM in Section 7. The test -supermartingale whose existence is implicitly asserted in (12) is, in a sense, reckless: it beats the index -fold if the event in the curly braces fails to happen but can (and does) lose everything if it happens. In this section we will discuss safer (more conservative) trading strategies instead of “all-or-nothing” trading strategies fine-tuned to the event of interest (such as the one in (12)).

Lemma 5.1.

For each , the process

| (13) |

is a test -supermartingale q.a.

In other words, the lemma says that the process (13) coincides with a test -supermartingale quasi-always.

Proof.

The value of the index at time is (where is defined by (10)). Let us consider the simple capital process whose value at time is (which should be stopped as soon as the capital hits 0). Intuitively, we are mixing the returns of and the returns of cash (and this is a convex mixture when ); when is small (which case is important for limit theorems such as the law of the iterated logarithm in Corollary 5.5), the new simple capital process can be regarded as a perturbation of .

We can see that

is the value at time of the log of a test -supermartingale (of class 0). In combination with Taylor’s expansion, this implies that

is the value at time of the log of a test -supermartingale. Passing to the limit as (and remembering that the variation index of over compact intervals does not exceed 2 quasi-always [14]), we obtain that

is the log of a test -supermartingale (of class 1) q.a. ∎

Corollary 5.2.

For any and ,

Proof.

The following corollary is in the spirit of Corollary 4.5.

Corollary 5.3.

If , , and for some constant ,

| (14) |

It is natural to optimize the in (14) given and ,

| (15) |

which gives our final corollary in this direction.

Corollary 5.4.

It is instructive to compare (16) and (12), which are obtained using two very different methods (especially that for the more general CAPM-type results of the following sections we will be able to use only the second, more conservative, method). The difference between the two inequalities for asserted with lower probability of (at least) boils down to the difference between the functions

in the notation of Hastings [3], who considers . Hastings gives two approximations to (pp. 191–192, reproduced in [1], 26.2.22 and 26.2.23) as the optimal, in a minimax sense, product of and a rational function of (the two approximations correspond to different degrees of the polynomials in the numerator and denominator of the rational function).

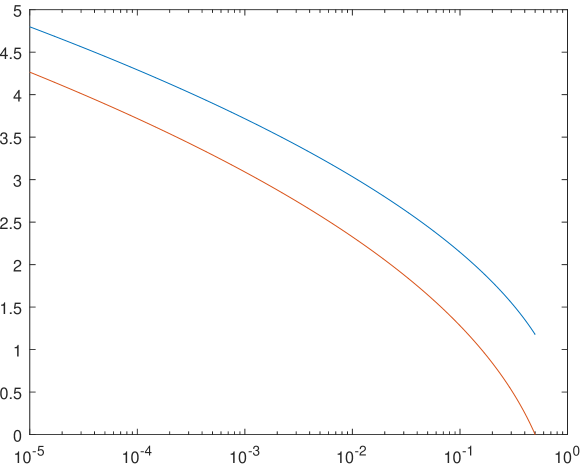

It is easy to check that as . Figure 1 compares the two functions over the range ( corresponding to the trivial value ).

It is easy to prove the validity part of a LIL for the equity premium using Ville’s [10] method.

Corollary 5.5.

Almost surely w.r. to ,

Proof.

This is part of Corollary 4.7 (combined with Lemma 3.2), so there is nothing to prove. But alternatively, we could mix the processes (which quasi-always coincide with test -supermartingales: cf. Lemma 5.1)

and

over of the form , , with weights (so that slowly while still ) for small and . For details, see Section 7, where we will prove a more general statement. ∎

Intuitively, our new method still allows us to derive the upper LIL since as , and the LIL is about almost sure convergence and so corresponds to small .

6 Existence of some basic quantities (2)

This section continues the series of definitions that we started in Section 3. Now we consider another traded security . Since it is a traded security, we can define and analogously to and ; however, this would involve stopping times defined in terms of rather than . It is more convenient to have just one family of stopping times. Therefore, we now define the sequence of stopping times , , inductively by and

| (17) |

for . We let stand for the th partition, i.e., the set

under our new definition, the partitions are not necessarily nested, (as was the case for our old definition (7)).

The following lemma says that we can redefine as (8) using the new partitions.

Lemma 6.1.

Proof.

As shown in [16], the limit of (8) as exists and is uniform on compact intervals quasi-always if we ignore the denominator; namely, the sequence

converges to a function uniformly on compact intervals quasi-always. The function is the same (quasi-always) for the sequences of partitions (7) and (17): to check this, apply the argument given in Section 5 of [16] to the th partitions in (7) and (17) rather than to the th and th partitions in the same sequence. It is clear that is the Riemann–Stiltjes integral

and that the statement of uniform convergence carries over to . ∎

Next we state the analogue of Lemma 6.1 for .

Lemma 6.2.

Proof.

The existence of the limit quasi-always is shown in [16], Section 4 (and the earlier work [8] by Perkowski and Prömel); the limit is nothing else than the Itô integral

The coincidence of the functions quasi-always for the sequences of partitions (7) and (17) follows from the argument given in Section 4 of [16] applied to the th partitions in (7) and (17) rather than to the th and th partitions in the same sequence. ∎

Using in place of , we obtain the definitions of and . The analogues of Lemmas 6.1 and 6.2 still hold.

As we are also interested in the covariance between (the returns of) and , we define

| (18) |

and then set to the limit as . The existence of the limit quasi-always is asserted in our next lemma.

Lemma 6.3.

The limit of (18) as exists quasi-always uniformly on compact intervals.

Proof.

The last quantity that we will need quantifies the difference between the returns of and :

| (19) |

we then set to the limit as . The final lemma of this section shows that the limit as exists quasi-always and is closely related to the other quantities introduced in this section.

Lemma 6.4.

The limit of (19) as exists uniformly on compact intervals quasi-always and satisfies

Proof.

It suffices to notice that, using the notation and for the returns of and ( is defined by (10) and is defined in the same way using in place of ),

and pass to the limit as . ∎

7 Capital Asset Pricing Model

Let us use the same mixing method as in Section 5, except that now we will apply it to and rather than to and cash.

Lemma 7.1.

For each , the process

| (20) |

is a test -supermartingale q.a.

Proof.

The value of the index at time is , and the value of the security at time is , where as before we use for the analogue of for . Let us consider the simple capital process whose value at time is (except that it is stopped if and when it hits ); it can be considered to be a mixture (convex mixture when ) of and . We can see that

is the log of a test -supermartingale at time for all , which implies the analogous statement for

Passing to the limit as , we obtain that

is the log of a test -supermartingale q.a. ∎

Corollary 7.2.

For any and ,

Proof.

The following corollary is in the spirit of Corollaries 4.5 and 5.3; however, now we wait until and become sufficiently different.

Corollary 7.3.

If , , and for some constant ,

| (22) |

Our convention is that the event in the curly braces in (22) happens when (i.e., when the security essentially coincides with the index).

It is natural to optimize the in (22) given and , as we did in (15), which gives us the following corollary.

Corollary 7.4.

If and for some constant ,

| (23) |

We will now give a complete proof of the validity part of a LIL for the CAPM; the following proposition generalizes Corollary 5.5 (we obtain the latter by taking cash as ).

Proposition 7.5.

Almost surely w.r. to ,

| (24) |

Proof.

We will implement in detail the idea mentioned in the proof of Corollary 5.5, namely, we will mix the processes, which quasi-always are test -supermartingales (see Lemma 7.1),

| (25) |

and

over of the form , , with weights . We will only prove (24) with the operation of taking the absolute value omitted (the proof for the case where it is replaced by negation is analogous), and so we will only consider (25).

Since converges,

is also a test -supermartingale with finite initial capital; therefore, it is bounded -a.s., and so we have

i.e.,

The value of that minimizes the right-hand side (let’s forget for a minute that is a function of and ignore the ) is

Let us choose such that this is approximately true, namely,

| (26) |

it is easy to check that such exist when is sufficiently large. This gives us

| (27) |

The right-hand inequality in (26) can be rewritten as

(for large ), and plugging this into (27) gives

It remains to mix over sequences of and . ∎

Theoretical performance deficit

Using Lemma 3.2 we can rewrite (23) as

And using Lemma 6.4 we can rewrite the last inequality as

Therefore, for large the EIH for implies

(the assumes that , , and grow linearly in , and so can be regarded as small). The subtrahend can be interpreted as measuring the lack of diversification in as compared with ; we call it the theoretical performance deficit.

Acknowledgments

This research was supported by the Air Force Office of Scientific Research (grant FA9550-14-1-0043).

References

- [1] Milton Abramowitz and Irene A. Stegun, editors. Handbook of Mathematical Functions: with Formulas, Graphs, and Mathematical Tables, volume 55 of National Bureau of Standards Applied Mathematics Series. US Government Printing Office, Washington, DC, 1964. Republished many times by Dover, New York, starting from 1965.

- [2] Claude Dellacherie and Paul-André Meyer. Probabilities and Potential. North-Holland, Amsterdam, 1978. Chapters I–IV. French original: 1975; reprinted in 2008.

- [3] Cecil Hastings, Jr. Approximations for Digital Computers. Princeton University Press, Princeton, NJ, 1955.

- [4] Ioannis Karatzas and Steven E. Shreve. Brownian Motion and Stochastic Calculus. Springer, New York, second edition, 1991.

- [5] Alexander S. Kechris. Classical Descriptive Set Theory. Springer, New York, 1995.

- [6] Burton G. Malkiel. Returns from investing in equity mutual funds 1971 to 1991. Journal of Finance, 50:549–572, 1995.

- [7] Burton G. Malkiel. A Random Walk Down Wall Street. New York, Norton, eleventh revised edition, 2016.

- [8] Nicolas Perkowski and David J. Prömel. Pathwise stochastic integrals for model free finance. Bernoulli, 22:2486–2520, 2016. arXiv:1311.6187 [math.PR].

- [9] Daniel Revuz and Marc Yor. Continuous Martingales and Brownian Motion. Springer, Berlin, third edition, 1999.

- [10] Jean Ville. Étude critique de la notion de collectif. Gauthier-Villars, Paris, 1939. This differs from Ville’s dissertation, which was defended in March 1939, only in that a one-page introduction was replaced by a 17-page introductory chapter.

- [11] Vladimir Vovk. The Capital Asset Pricing Model as a corollary of the Black–Scholes model, September 2011. GTP Working Paper 39. arXiv:1109.5144v1 [q-fin.PM].

- [12] Vladimir Vovk. The efficient index hypothesis and its implications in the BSM model, October 2011. GTP Working Paper 38. First posted in September 2011. arXiv:1109.2327v1 [q-fin.GN].

- [13] Vladimir Vovk. A simplified Capital Asset Pricing Model. Technical Report arXiv:1111.2846v1 [q-fin.PM], arXiv.org e-Print archive, November 2011.

- [14] Vladimir Vovk. Continuous-time trading and the emergence of probability, May 2015. GTP Working Paper 28. First posted in April 2009. Journal version: Finance and Stochastics, 16:561–609, 2012. arXiv:0904.4364v4 [math.PR].

- [15] Vladimir Vovk. Getting rich quick with the Axiom of Choice, May 2016. GTP Working Paper 43. arXiv:1604.00596v2 [q-fin.MF].

- [16] Vladimir Vovk. Purely pathwise probability-free Itô integral, June 2016. GTP Working Paper 42. First posted in December 2015. arXiv:1512.01698v5.

- [17] Vladimir Vovk and Glenn Shafer. Game-theoretic capital asset pricing in continuous time, December 2001. GTP Working Paper 2.

- [18] Vladimir Vovk and Glenn Shafer. The Game-Theoretic Capital Asset Pricing Model, March 2002. GTP Working Paper 1. First posted in November 2001. Journal version: International Journal of Approximate Reasoning, 49:175–197, 2008.