Weighted Multilevel Langevin Simulation of Invariant Measures

Abstract

We investigate a weighted Multilevel Richardson-Romberg extrapolation for the ergodic approximation of invariant distributions of diffusions adapted from the one introduced in [LP13] for regular Monte Carlo simulation. In a first result, we prove under weak confluence assumptions on the diffusion, that for any integer , the procedure allows us to attain a rate whereas the original algorithm convergence is at a weak rate . Furthermore, this is achieved without any explosion of the asymptotic variance. In a second part, under stronger confluence assumptions and with the help of some second order expansions of the asymptotic error, we go deeper in the study by optimizing the choice of the parameters involved by the method. In particular, for a given , we exhibit some semi-explicit parameters for which the number of iterations of the Euler scheme required to attain a Mean-Squared Error lower than is about .

Finally, we numerically this Multilevel Langevin estimator on several examples including the simple one-dimensional Ornstein-Uhlenbeck process but also on a high dimensional diffusion motivated by a statistical problem. These examples confirm the theoretical efficiency of the method.

Keywords: Ergodic diffusion, Invariant measure, Multilevel, Richardson-Romberg, Monte Carlo.

AMS Classification: 60J60, 37M25, 65C05.

1 Introduction

Let be the unique strong solution to the stochastic differential equation ()

starting at where is a standard -valued standard Brownian motion, independent of , both defined on a probability space , where and are locally Lipschitz continuous functions with at most linear growth. The process is a Markov process and we denote by its distribution starting from . Let denote its infinitesimal generator, defined on twice differentiable functions by

As soon as there exists a continuously twice differentiable Lyapunov function such that

| (1.1) |

then there exists an invariant probability measure for the diffusion in the sense that is a stationary process under , so that for every t. Under appropriate (hypo-)ellipticity assumptions on or global confluence assumptions (on this topic, see [LPP15]), this invariant measure is unique, hence ergodic. In particular,

where denotes weak convergence of distributions on (see [Bil78] or [Kre85] for background). We will assume that this uniqueness holds throughout the paper. Under additional assumptions, one shows that the diffusion is stable in the sense that

This - convergence is ruled by Bhattacharya’s CLT (see [Bha82] for detailed assumptions), namely, if is such that the Poisson equation admits a solution, then

| (1.2) |

with where denotes the transpose matrix of .

In a series of papers (see [LP02, LP03, Lem07, PP09, PP14, Pan08]), the above properties have been exploited in order to compute by ergodic simulation integrals or, more generally, where is a (path-dependent) functional defined on the space (see also [Tal90] or [PS94] for other references on the topic or more recently [GT15]).

The starting idea is to mimic (1.2). First we replace the diffusion by a discretization scheme with decreasing step. To be more precise, we consider, for a given non-increasing sequence of steps , , the associated Euler scheme with decreasing step defined by

| (1.3) |

where , . Then we introduce (for technical matter to be explained further on) a weight sequence and the related -weighted empirical (or occupation) measures of the above Euler scheme, namely

The computation of can be performed recursively, once noted that that

| (1.4) |

It is clear that, in order to let the scheme explore the whole state space and to let the empirical measures take into account new values as grows, we must require the pair satisfies

| (1.5) |

When , the -empirical measure is the natural counterpart of and one expects that, under natural mean-reverting assumptions similar to (1.1) (or slightly more stringent), - taking advantage of the fact that the step . The major difference with the above continuous time pointwise Birkhoff’s ergodic theorem is that, provided , can be computed easily, these random measures taken against a function (computable as well) can in turn be simulated. This opens the way to simulation based ergodic methods to compute . Note that, though we will not go deeper in that direction, when is absolutely continuous such a method appears as a probabilistic numerical scheme for the resolution of the stationary Fokker-Planck equation by providing the values of as many integrals as required.

Let us first recall one simple convergence result for the weak convergence of the weighted empirical measures (see Theorem V.2 borrowed and slightly adapted from [Lem05]).

PROPOSITION 1.1.

Assume and satisfy the mean-reverting assumption

: There exists a positive -function and such that

and there exist some real constants , and such that:

Then ) admits at least one invariant distribution and for every and , .

Moreover, , for every - continuous functions with -polynomial growth,

| (1.7) |

REMARK 1.1.

By -polynomial growth we mean that at infinity for some .

The condition is stronger than (1.1). It implies that there exists and such that . In fact the conclusions of the above proposition are also true for the continuous time occupation measure of the diffusion itself.

The above result remains true under weaker Lyapunov assumptions of the following type: with . For the sake of simplicity, we choose in this paper to state the results under only but all what follows can be extended to the weaker setting owing to additional technicalities (involving the control of the moments of the diffusion or of the Euler scheme (1.3)).

In the above proposition, the condition can be relaxed into . For the sequel, the interest of this slightly reinforced assumption is to ensure that every function with polynomial growth has a -polynomial growth.

Examples. If and , then the pair is averaging as soon as and . In practice, we will extensively use that, furthermore, the pairs of the form are averaging for so that .

The rate of convergence of toward has also been elucidated and reads as follows (when and for the sake of simplicity, keeping in mind that even in that setting, various averaging systems are involved):

Set , . Assume the Poisson Equation has a smooth enough solution and that , then

| (1.8) | |||||

| (1.9) |

with and

When the unbiased () holds for , the biased for and the biased convergence in probability for .

On can interpret this result as follows: if decreases to fast enough (), the empirical measures behaves like the empirical measures of the diffusion. When goes to too slowly, there is a discretization effect which slows down the convergence of the empirical measure at rate . The convergence then holds (or at least in probability) which confirms that what slows down the convergence is a bias term whose rate of decay is lower than . The top rate of convergence is obtained with a biased .

We will see in Theorem 2.1 further on that, in fact, there are many of these bias terms which go to slower than the rate for slowly decreasing steps. So killing these terms is a major issue to speed up such ergodic simulations (or Langevin Monte Carlo method) compared to the regular Monte Carlo method.

The Multilevel paradigm has been introduced by M. Giles in the late 2000’s (2008, see [Gil08]). Ever since, it has been extensively adapted to various types of simulations (nested Monte Carlo, see [LP13], stochastic approximation [Fri16]) and dynamics (Lévy driven diffusion, random maps, etc) as a bias killer. The principle is the following: assume that a quantity of interest to be computed does have a representation as an expectation, say , but that the random variable cannot be simulated at a reasonable computational cost. Then one usually approximates by a family of random vectors that can be simulated with a low complexity, relying on discretization schemes of the underlying dynamics. The typical situation is the or where is a Brownian diffusion as above and or where is a discretization scheme, say an Euler or a Milstein scheme with step . A multilevel estimator with depth of is designed by implementing a non-homogeneous Multilevel Monte Carlo (MLMC) estimator of size of the form

where is a fixed coarse step, are independent copies of , , is a fixed integer and is an appropriate (optimized) allocation policy of the simulated paths across the levels such that (in practice, at a given level , only and have to be simulated). The level is the coarse level whereas the levels are the refined levels. Within a refined given level , denotes the coarse scheme and the refined scheme. For some fixed and , the random variables are “consistent” in the sense that they have been simulated from the same underlying Brownian motion . A quantitative translation of this consistency is that converges in (squared) quadratic norm to at a rate, namely , . The parameter depends on or in a diffusion framework. If or are locally Lipschitz continuous with polynomial growth (with respect to the sup norm as for ), . This parameter and the constant are key parameters to optimize the allocations of the paths to the various levels (see [Gil08, LP13]).

Among other results, M. Giles proved that if and – which is the standard situation in a diffusion discretized by its Euler scheme – when , (Euler scheme with step ), , , smooth enough (or uniformly elliptic if is simply Borel and bounded), the resulting complexity of the optimized Multilevel Monte Carlo estimator to attain a prescribed Mean Squared Error behaves like as . When (fast strong approximation like with the Milstein scheme), this rates attains the rate of a (virtual) unbiased simulation. The case provides even better improvements compared to a crude Monte Carlo simulation.

In a recent paper (see [LP13]) a weighted version of the above multilevel estimator has been devised to take advantage of a higher order expansion of the weak error (bias expansion) up to an order , namely

still under the above quadratic convergence rate assumption. Then, the so-called Multilevel Richardson-Romberg estimator (ML2R in short) is still based on the simulation of independent copies of and reads

where the -tuple of weights has a closed form entirely determined by , and and not on (that means on the specific form of , , in a diffusion framework). For this weighted estimator, the complexity is reduced mutatis mutandis to in the setting . When this estimator dramatically outperforms the above “regular” multilevel method since it only differs from a (virtual) unbiased simulation by a factor (when ) instead of with MLMC. The underlying idea for this weighted Multilevel method is to combine the multilevel paradigm with a multistep Richardson-Romberg extrapolation introduced in [Pag07], hence its name. We refer to [LP13] for more precise results and proofs.

The aim of this paper is to transpose the weighted multilevel paradigm to the Langevin Monte Carlo simulation with decreasing step described above, with the issue that, in contrast with regular Monte Carlo simulation, canceling the bias terms directly impacts the rate of convergence of the method by enlarging the range of step parameters for which a holds at rate to coarser steps (so that goes faster to infinity where the stationary regime takes places). So we will adapt the ML2R estimator to the occupation measure introduced before. Like in the regular Monte Carlo setting, we introduce, for a function , a weighted estimator involving and some correcting terms denoted by , based on some pairs of coupled refined schemes (see (2.12) for details). Since the ergodic estimation of the invariant measure is based on only one path, the idea here is to replace the allocation policy of realizations of the ML2R method by a sizing policy of the length of the coarse path (involved in ) and those of the correcting sequences .

In order to asymptotically kill the successive terms of the bias induced by the estimator, we will need some asymptotic expansions of the and such as (2.13) and (2.14) below. These expansions, which require the invertibility of the infinitesimal generator (or equivalently the existence of solutions to the Poisson equation) can be viewed as the counterpart of the classical weak error/bias expansion in finite horizon. Concerning the strong convergence rate property which leads to the control of the variance of the corrective terms in the standard Multilevel method, its counterpart in our ergodic setting is the following mean confluence result which says that

It says that the -empirical measure of the couple concentrates on the diagonal of at rate . Such a property holds when the diffusion itself is exponentially confluent (typically a mean-reverting Ornstein-Uhlenbeck process) under an exponential confluence property which holds under .

Throughout the proofs, we will work in one dimension for notational convenience. The extension to the multidimensional case would only generate technicalities.

Outline. The paper is organized as follows. We begin by introducing precisely the weighted empirical sequence built for the estimation of the invariant measure, called ML2Rgodic and denoted by . Then, our main results are divided in three parts. In Theorem 2.1, we obtain some CLTs for : we show that the ML2Rgodic-Algorithm with levels of corrections and an appropriate sequence has an optimal rate of order with an asymptotic variance which is the same as the one of the original procedure. Then, in view of the optimization of the choices of the parameters, we exhibit in Theorem 2.2 some first and second order asymptotic expansions of the Mean-Squared Error. Based on this result, we proceed to the optimization in Theorem 2.3 and provide some choices of the parameters involved by the algorithm which lead to a complexity of order (instead of for the original procedure). The main tools for the establishment of Theorems 2.1 and 2.2 appear in Sections 3 and 4. Then, the proofs of Theorems 2.1, 2.2 and 2.3 are achieved in Section 5. Finally, we end this paper by some numerical computations in Section 6.

2 The Multilevel-Romberg Ergodic (ML2Rgodic) procedure

2.1 Design of the ML2Rgodic Langevin estimator

We aim at adapting the multilevel paradigm to devise an ergodic estimator for the approximation of the invariant distribution. For a given integer , the idea is to modify the original procedure with the aim to kill the first terms of the expansion of the discretization error without impacting too much the simulation cost of simulation.

Let be a sequence of steps, and and be two integers such that and . First we consider an Euler scheme with decreasing step associated to a standard Brownian motion . We associate to this scheme independent coupled schemes , , independent of where

-

•

is an Euler scheme with decreasing step (so that ) associated to a Brownian motion .

-

•

is a refined Euler scheme with decreasing step associated to the same Brownian motion where

(2.10)

Set, for every integers and ,

| (2.11) |

where . Note that .

Then, we define for every the sequence of difference of the empirical measures of the two schemes by

| (2.12) |

The expected weak limit of is as a difference of occupation measures of two Euler schemes with decreasing step. Thus, this empirical measure plays the role of a correcting term.

Now, let denote some positive real numbers, called re-sizers from now on, satisfying

and, for a given integer , set

Let be a smooth function, coboundary for the infinitesimal generator (existence of solutions to the Poisson equation . Under some appropriate assumptions (including weak confluence) we can prove in a sense made precise later on (see Propositions 3.2 and 3.3) that the sequences and satisfy the following asymptotic generic type-expansions:

| (2.13) | |||||

| (2.14) |

where is a martingale and is a sequence of functions made precise further on. At this stage, the reader can remark that there is no martingale term in the main part of the second expansion. This point, which is strongly linked with the weak confluence assumption introduced below, can be understood as follows: the martingale term induced by is asymptotically negligible against the one of . In a rough sense, this means that if we build an appropriate combination of and , , we will be able to kill the bias error without growing the asymptotic variance. But a numerical computation holds in a finite (non-asymptotic) setting so that this heuristic needs to be refined in practice. One of the objectives of the paper is thus to go deeper in the study of the expansion in order to be able to propose an efficient and potentially optimized method of approximation of the invariant distribution.

The ML2Rgodic-algorithm: As mentioned before, the first step toward our ML2Rgodic estimator is to design an appropriate combination of the formerly defined empirical measures in order to “kill” the bias. Furthermore, we require that this combination does not depend upon the size of the estimator. We thus define a sequence of empirical measures denoted by by:

| (2.15) |

where is a sequence of real numbers. For the sake of simplicity, we do not mention the dependency of in and . Also, let us remark that the weights clearly depend on and will sometimes be denoted in order to recall this dependence when necessary. Let us now specify . First, by (2.13) and (2.14), one remarks that it is necessary to assume that in order to ensure the convergence towards .

Let us now consider the construction of . To this end, we consider from now on step sequences with polynomial decay

| (2.16) |

Then by plugging the expansions of the bias resulting from (2.13) and (2.14) in the definition (2.15) of the ML2Rgodic estimator we derive that

where the notation is used to keep in mind that one implicitly assumes that is negligible (see further on the proof of Theorems 2.1 and 2.2). Then as soon as the weights are solutions to the linear system

| (2.17) |

the bias is “killed” up to order and reads

where we set, more generally,

| (2.18) |

The main difference at this stage with the regular weighted Multilevel estimator is that these weights depend on the re-sizers which will make a complete optimization of these allocation parameters out of reach.

In the following lemma the linear system (2.17) is solved. In short, it shows that the weights are uniquely defined provided the re-sizers satisfy , . Note that these weights depend on the exponent (and the ) but not on .

Another important point is that, by contrast with the regular weighted Multilevel Monte Carlo setting, this system in its general form is not a regular Vandermonde system though it shows some similarities. In fact it can be related to a sequence of -Vandermonde systems with closed solutions. A notable exception to this situation occurs in the very special of uniform re-sizers , where we retrieve exactly the weights of the regular Monte Carlo introduced in [LP13]. For a given depth , the closed form of (keeping in mind that ) is given by the following lemma.

LEMMA 2.1.

General re-sizers: If and satisfies , , then the above system (2.17) has a unique solution given by

| (2.19) |

Uniform re-sizers: If , , the following simpler closed form holds for the weights :

| (2.22) |

with

| (2.23) |

These weights , , are bounded . Furthermore

| (2.24) |

The proof is postponed to Appendix A.

Examples. : ,

:

When there is no ambiguity the superscript (R) will be dropped in the notations , and . In the sequel, will be always defined with satisfying (2.17) or (2.19).

Assumptions. We introduce below the assumptions for the first theorem. As recalled in the introduction, the study of the rate of convergence brings into play the Poisson equation related to the SDE. In this paper where we are going deeper in the expansion of the error, we will need to use it successively. For the sake of simplicity, we thus assume the following (strong) assumption:

For every function , there exists a unique (up to an additive constant) -function , such that . Furthermore, if is a function with polynomial growth, then also is.

For instance, it can be shown that, when is bounded and uniformly elliptic (in the sense that for some ), when Assumption is in force and , and are smooth have polynomial growth as well as their derivatives, then holds true. Actually, we first recall that under the ellipticity and Lyapunov assumptions, the semi-group converges exponentially fast towards (in total variation) so that is well-defined and it is classical background that is the unique (up to a constant) solution to the Poisson equation (see [PV01]). Then, by [GT83, Theorem 6.17], under uniform ellipticity, is in fact as soon as , and are. The polynomial growth of and has been proved in [PV01, Theorem 1]. The property is obtained through the a priori estimate, see Equation (9.40) in [GT83], which in fact also holds for . Then, we can establish by induction that all the partial derivatives of have a polynomial growth. Assume it is true up to order . First note that is a solution to where is a function which depends on , and and their first order partial derivatives and some derivatives of up to order . Hence, has polynomial growth and the a priori error bound (9.40) in [GT83] for the second order partial derivatives of yields the polynomial growth of the partial derivatives .

The second additional assumption has been introduced in [PP14] and deeply studied [LPP15]: it requires the diffusion to be weakly confluent, that two paths of the diffusion, with different initial values, but driven by the same Brownian motion, asymptotically cluster in a weak (or statistical) sense as follows: let be the duplicated diffusion (or two-point motion) associated with the diffusion () by

| (2.25) |

where are two starting values independent of . If is an invariant distribution for (), is trivially invariant for the couple . The diffusion ( is said weakly confluent if is the only invariant distribution for (which implies implicitly that itself is the unique invariant distribution of ()). In the sequel, this assumption is referred to as

: () is weakly confluent.

REMARK 2.2.

Under slight additional assumptions on the stability of (), it can be shown (see [LPP15]) that, if holds, the diffusion is statistically confluent in the sense that

For the empirical measure , the role of is to ensure that the empirical measures , built with some differences of schemes and have a negligible asymptotic variance (with respect to that of ). This property will be made precise in Section 4.

We are now in position to state the first main theorem.

THEOREM 2.1 (CLT).

Assume , and . Let and let denote the -tuple of weights defined by (2.19). Let be an -tuple of re-sizers satisfying , . Let , , , be a discretization step sequence. Let be a -function and denote by the solution to . Let be defined by (2.19).

If , then

with

| (2.26) |

If , the holds at an optimal rate towards a biased Gaussian distribution, namely

with and where is given by (2.18) and , being a -function with polynomial growth (whose explicit expression in the one-dimensional case is given by (3.38)).

If , then

with

| (2.27) |

REMARK 2.3.

Note that the definitions of and in the above claims and are consistent since when .

From an asymptotic point of view, the above result says in particular that when grows, the optimal rate of convergence tends to without increasing the (asymptotic) variance. However, from a non-asymptotic point of view, one has certainly to go deeper in the result to try to optimize the choice of the parameters. This implies to take into account the effect of the choice of , and on the residual bias term, the variance and on the computational cost. This is the purpose of the next paragraph.

-expansions of the error. The aim of this part is to study the quadratic error to prepare the optimization of the parameter of the multilevel estimator () algorithm subject to a prescribed quadratic error . To this end, we will not only provide a re-formulation of Theorem 2.1 in quadratic norm, we will also go deeper in the study of the asymptotic error. In particular, in the previous result, the variance induced by the correcting terms does not appear and we would like to quantify it. We will also need to control the residual error terms not only in but also with respect to the depth , since this parameter is intended to go to in the optimization phase. This will lead us to carry out the expansion to the order and not or like in the above theorem and to introduce a second and more constraining confluence assumption denoted by :

There exists and a positive matrix such that for every ,

where and by stand for the inner product and norm on defined by and , and for , .

Furthermore to get closer to practical aspects, we only consider the optimal case which clearly provides the highest possible rate of convergence for a given complexity. Finally we will focus on the uniform re-sizing vector , . They turn out to be most likely rate optimal and, as emphasized in Remark B.11, in that case the first term of the bias of the ML2Rgodic estimator does vanish whereas for other choices of vectors a residual bias (at rate still remains. Though theoretically negligible, it turns out to have a strong numerical impact on simulations.

THEOREM 2.2 (Mean Squared Error for ).

Suppose that the assumptions of the previous theorem hold and let . Then,

2.2 Optimization procedure

It remains to optimize the parameters to minimize the complexity of the estimator for a given prescribed mean square error (). In view of the above Theorem 2.1, it is clear that the parameter should be settled at

We start from Theorem 2.2 with

Then the weights , and are given by (2.23) and (2.24) (those coming out in standard multilevel Monte Carlo in the case of the approximation of a diffusion by its Euler scheme).

We denote by the remaining set of free simulation parameters that we wish to optimize. With this specification for and the allocation vector , the reads

| (2.31) |

as goes to where, owing to (2.27), (2.30), (2.26) and (2.28),

On the other hand, the complexity of the multilevel Langevin estimator devised in (2.15) reads

where denotes the unitary computational cost of one iteration of an Euler scheme.

To calibrate the above parameter , we want to minimize the complexity subject to a prescribed , that is solving the constrained optimization problem:

To state the main result of this section, whose proof is postponed to Section 5, we need to introduce a function related to the weights and on the depth of the simulation. We know from Lemma 2.1 that . Consequently, being fixed, as (where is defined by (2.29)). This leads us to define

| (2.32) |

We refer to Table 2 for some numerical values of and .

THEOREM 2.3.

The above bound can be achieved by the (sub-)optimal given by , where is the unique solution to the equation and

Furthermore, as ,

and the (minimal) number of iterations necessary to attain an MSE lower than satisfies

| (2.34) |

REMARK 2.4.

Though difficult to check in practice, note that the assumptions on the sequence are satisfied as soon as

REMARK 2.5.

Note that the choice of does not depend on the parameters. In Table 1, we give the values of for several choices of and . As expected, one can check that increases very slowly when decreases.

| 2.08 | 2.79 | 3.38 | 3.89 | |

| 1.94 | 2.56 | 3.06 | 3.50 | |

| 1.87 | 2.44 | 2.90 | 3.30 |

REMARK 2.6.

A remarkable point to be noted is that we retrieve the same asymptotic rate as that obtained with the original ML2R Monte Carlo simulation at finite horizon, that is for the computation of expectations where is a standard diffusion discretized by its Euler scheme.

Practical aspects are investigated in the practitioners’ corner (see Section 6.1) especially how to calibrate the parameters which are involved in the definition of .

3 Expansion of the error

For the sake of simplicity, the proofs are detailed in dimension . In the following subsections, we begin by decomposing the quantity for a given smooth coboundary function ( such that the Poisson equation has a smooth enough solution) and for a general weight sequence . Then, in the next subsections, we successively propose some expansions of the error, for the original sequence (implemented on the coarse level) and for the sequences of correcting empirical measures for defined in (2.12) and corresponding to the successive refined levels of our estimator.

Note that by expansion, we mean an expansion of the bias of our estimators (level by level then globally) until we reach an order at which we reach a martingale term involved in the weak rate of convergence.

3.1 Higher order expansion of (coarse level)

For every integer , for every sequence , we set . We will also use the following notations:

| and , . |

LEMMA 3.2.

Let . Assume that where is a -function. Then, for every integer ,

| (3.35) |

where

As a consequence,

| (3.36) |

Proof.

By the Taylor formula with order , we have for every and in ,

where . Then, if with ,

The decomposition of easily follows by separating odd and even and by remarking that

Since

the second part of the lemma is a direct consequence. ∎

For notational convenience, we will denote by in what follows the solution of the Poisson equation satisfying . (Under Assumption , is well-defined).

DEFINITION 3.2.

Under Assumption , one may define a mapping from into itself defined for every by

| (3.37) |

where denotes the derivative of a function . Then, for every , one sets . To alleviate notations, we will often write instead of in what follows.

Still under Assumption , we define the mappings , ,

| (3.38) |

For example, note that

We have the following expansions of the error, depending on the averaging properties of the step sequence .

PROPOSITION 3.2 (Bias error expansion for the coarse level).

Assume , (and uniqueness of the invariant distribution ). Let , and let with polynomial growth and .

If is averaging for every ,

If, furthermore, the pair is averaging,

(c) The following sharper expansion also holds when is averaging

where and

with , the solution to .

REMARK 3.7.

The first expansion is adapted to the proof of Theorem 2.1, the second one to Theorem 2.1 and and Theorem 2.2. Statement is written in view of Theorem 2.2 where one needs to handle the second order term of the asymptotic expansion of the . Note that the bias term of order in will contribute to in Theorem 2.2. At this stage, it can be justified by the following remark: when ,

As concerns the contribution of the martingale correction , we refer to Proposition 4.4 for details. Finally, remark that all the negligible terms are given with the -norm. For Theorem 2.1, “” is enough.

Proof.

and : Let be an integer. Let us consider the decomposition given by (3.35) in Lemma 3.2. When , and , we get

| (3.39) | ||||

By Lemma 3.3 applied with ,

As well, by Lemma 3.3applied for different choices of , and , we have

Finally, Lemma 3.3 and are adapted to manage and respectively. This yields

The above terms are thus negligible in expansions and . As concerns , one can deduce from the polynomial growth of and from (3.41) that there exists such that

This means that this term is negligible in the expansion . In , is averaging so that by Proposition 1.1,

But using again (3.41), one checks that there is a such that is a bounded sequence. Thus, an uniform integrability argument yields that

But for any , is the component corresponding to in the definition (3.38) of . In , will thus contribute to . As well, the terms , exhibited in this first expansion will certainly contribute to , .

Now, we focus on the second bias term of the right-hand side of (3.39). More precisely, for each , we have to repeat the previous procedure: we apply the expansion (3.35) of Lemma 3.2 with , , and (defined above). After several transformations, this yields

| (3.40) | ||||

Applying again Lemma 3.3 allows us to control the -norm of the negligible terms:

and

Again, the penultimate term of the previous decomposition is negligible for expansion and satisfies the following convergence property when is averaging:

This brings a second “contribution” to .

Finally, it remains to consider for every each term of (3.40). Setting , , the sequel of the proof consists in repeating the procedure until . The result follows.

The proof is based on the same principle but is slightly more involved since we aim at keeping all the terms which are going to play a role in the second order expansion of Theorem 2.2. This implies to start the previous proof with (and in the second step with ). Furthermore, the main other difference comes from the martingale component. As a complement of , one also keeps whole the martingale terms whose -norm is not negligible with respect to . In short, this corresponds to the martingale increments with a factor or . This yields the two martingale increments and of the first expansion but also the dominating martingale increment of the second expansion above : . The result follows. ∎

LEMMA 3.3.

Assume . Let be a smooth function with polynomial growth. We know from Proposition 1.1 that, for every ,

| (3.41) |

Then,

(i) If is a non-increasing sequence of real numbers,

(ii) If is a sequence of centered random variables with finite variance, then for any deterministic sequence ,

(iii) For any sequence of real numbers,

(iv) For any sequence of real numbers and any , there exists a real constant such that

Proof.

Using that is a non-increasing sequence, we have

so that

This concludes the proof of . Items and are straightforward consequences of the fact that . For , the polynomial growth of implies that there exists and a constant such that for any ,

Using that and are sub-linear functions and Minkowski’s Inequality

The last statement follows using again Minkowski’s Inequality. ∎

3.2 Error expansion of the correcting levels

For a given sequence , let us denote by and the two Euler schemes of the diffusion driven by the same Brownian motion and with the step sequences and respectively. We then define a sequence of empirical measures by

By the definition (2.12), one first notes that for , built with the Euler schemes and (keep in mind that ). As a consequence, expanding will elucidate the behavior of the refined levels in the ML2Rgodic procedure.

In the proposition below, we thus state a result similar to Proposition 3.2 but for the sequence .

PROPOSITION 3.3 (Bias error expansion for the refined levels).

Assume , and uniqueness of the invariant distribution of the diffusion is unique. Let , and let with polynomial growth and let .

Assume that for every , the pair is averaging. Then,

where for a Borel function

If furthermore, the pair is averaging, then the following sharper expansion also holds:

The following sharper expansion also holds when is averaging :

where, for a Borel function ,

Proof.

With the notation introduced in (2.10). Set

One can check that for every ,

For and , it remains now to apply Proposition 3.2 and to both terms in the right-hand side of the above equation (with step for ). The result follows by concatenating martingale components and by noting that for any integer ,

For the proof of , the only difference with Proposition 3.2 is that one only keeps the martingale increment of the corrective term . More precisely, the terms of appearing with a factor are here viewed as negligible terms. Using Lemma 3.3, one easily check that these martingale corrections are bounded in by (which is ). ∎

REMARK 3.8.

The fact that we keep less martingale terms in Expansion can be understood as follows: in section (4.5), we will show that the apparently dominating martingale component is in fact negligible at the first order of the expansion under confluence assumptions. This implies that the covariance terms induced by the product of this martingale and the martingale corrections appearing with a factor in (see Proposition 3.2) will be also negligible at a second order.

4 Rate of convergence for the dominating martingales

In the continuity of Propositions 3.2 and 3.3, we now propose to elucidate the weak or rate of convergence of the dominating martingales , that is the martingales coming out in the above error expansions established in the former section.

4.1 The dominating martingale term involved in

We begin by stating some asymptotic results for the first and second order martingales and which appear in the expansions of Proposition 3.2. The associated statements describe the asymptotic martingale contributions of the first (dominating) term of the ML2Rgodic procedure. With the view to Theorem 2.1, the first statement concerns the convergence in distribution of the dominating martingale whereas the second and third ones are crucial steps in the proof of Theorem 2.2 and respectively.

PROPOSITION 4.4.

Assume and . Let .Then,

If is averaging,

where

| (4.42) |

where , the solution to .

REMARK 4.9.

Proof.

Using Proposition 1.1,

| (4.43) |

Furthermore, by Cauchy-Schwarz inequality and (3.41), we have for every ,

This second convergence implies that the so-called Lindeberg condition is fulfilled. Then, is a consequence of the CLT for martingale arrays (see [HH80, Corollary 3.1]).

By Jensen inequality, for a given function ,

and it follows again from Proposition 1.1 and from the fact that has (at most) polynomial growth that

| (4.44) |

owing to and (3.41). As a consequence, is a uniformly integrable sequence so that the convergence of toward also holds in . The second statement then follows from (4.43).

First, using that and that , one can check that

where

On the one hand, since is averaging, we deduce from Proposition 1.1 that

But using uniform integrability arguments similar to (4.44), the convergence also holds in . On the other hand, let us focus on . We set Using Proposition 3.2 (and the fact that ) with , we have

By (4.43), we deduce that

The last statement follows. ∎

4.2 The dominating martingale in the error expansion of

In this section, we focus on the behavior of the martingale terms involved by the refined levels of the ML2Rgodic procedure. Thus, this corresponds to the variance induced by this procedure. On a finite horizon, Euler schemes are pathwise close (in an -sense for instance) and this property implies one of the important features of multilevel procedures: reducing the bias without increasing significantly the variance. As mentioned before, on a long run scale, such a property is not true in general. More precisely, without additional assumptions, the martingale defined in Proposition 3.3 is a priori not negligible compared to the one induced by the first term of the ML2Rgodic procedure. However, this turns out to be true in presence of an asymptotic confluence assumption. This is the first statement of the next proposition. In the second one, we go deeper in the analysis of the martingale contribution of under a stronger confluence assumption. The second property will contribute only to Theorem 2.2.

PROPOSITION 4.5.

Assume and . Let and be locally Lipschitz functions with polynomial growth.

If holds, then converges to in .

) Assume holds and that is averaging. Assume that is and that and its derivatives have polynomial growth. Then, the martingales and are orthogonal and

In particular, when and (with ), this variance is denoted by which subsequently reads

| (4.45) |

Proof.

Set . First, using that and are built with the same Wiener increments,

so that

where and . With similar arguments as for the proof of Proposition 1.1, for every , converges to the unique invariant distribution of the duplicated diffusion (since Assumption holds). By uniform integrability arguments, one can check that the convergence holds along continuous functions with polynomial growth so that

Again with uniform integrability arguments (using that for every positive ), one can check that . It follows that

The proof of this statement is the purpose of the end of the section. First, remark that the orthogonality of and follows from independency of the increments of the Brownian motion and from the fact that for every , . Then, it remains to study these two martingales separately. In Lemma 4.4, we go deeper in the study of the long run behavior of the martingale under Assumption and in Lemma 4.5, we investigate the one of the martingale . ∎

4.2.1 Long run behavior of under strong confluence.

LEMMA 4.4.

Under the assumptions of Proposition 4.5,

Proof.

We temporarily write instead of .

Step 1: We decompose as the sum of terms involving the limiting diffusion process :

We first deal with whose predictable bracket given by

Let be the infinitesimal generator of the duplicated diffusion and let us denote by and the associated drift and diffusion coefficients. If we temporarily set , then

and reads, or equivalently .

Now, by mimicking the proof of (1.9) (where the result has been established for functions of the Euler scheme alone), we get that, as soon as , for every smooth function

where and is the image of on the diagonal of (which is the unique invariant distribution of the duplicated diffusion). Straightforward computations show that since , and , . Thus, taking advantage of the strong confluence, we derive that

Uniform integrability arguments imply that the above convergence also holds in . Thus,

The same method of proof shows a similar result for , (by considering the scheme and the filtration ). It follows that as .

Step 2: Now we deal with , . First we compute the predictable bracket

Then, we decompose

Let us deal first with . The function being with polynomial growth, there exists some positive and such that for every and in ,

Thus,

Using that , one easily checks that for every ,

so that with the help of the Cauchy-Schwarz inequality,

For we write

where

It is clear, owing to Doob’s Inequality, that

Then as above.

The last term of interest is again a martingale increment. We note that

The sequence being averaging,

Uniform integrability arguments imply that and one deduces that

The result then follows from the orthogonality of the martingales , (the fact that the martingales and are negligible also implies by Schwarz’s Inequality that so is their cross product). ∎

4.2.2 Long run behavior of .

We consider now the martingale

LEMMA 4.5.

Under Assumptions of Proposition 4.5,

Proof.

Like in the previous proof, we write instead of . We focus on the asymptotic behavior of .

First, noting that for a random variable , , we get since is averaging,

| (4.46) |

likewise one shows that for that

By uniform integrability arguments, the above convergence extends to the expectations. Second, we focus on the “slanted” brackets. Let us set . Using the chaining rule for conditional expectations, we note that, for every ,

so that .

Now, let us compute where and is viewed as a couple of -martingales. Writing the increment as follows:

and using some standard properties of the increments of the Brownian Motion, one can check that

Using second order Taylor expansions of between and for , combined with the fact that for every , one derives

where . Thus, the sequence of empirical measures associated to the duplicated diffusion (2.25) has a unique invariant distribution . By an adaptation of the proof of Proposition 1.1, it can thus be proved that

Once again, by a uniform integrability argument (and using what precedes), one obtains

As a conclusion of the previous convergences, one deduces that

∎

5 Proofs of the main theorems ( and optimization)

Owing to the results established in the previous sections, we are now in position to prove the three main results: Theorems 2.1, 2.2 and 2.3. First keep in mind that in these theorems the step sequence reads for some and .

5.1 Proof of Theorem 2.1.

We mainly detail the proof of Theorem 2.1 and we will only give some elements of the ones of and (which are based on the same principle) at the end of this section.

First, by (2.15), one reminds that is a linear combination of and of with , , . For and , we will make use of the expansions given in Propositions 3.2 and 3.3 respectively. For , , as defined by (2.14), we apply Proposition 3.3 with step sequence . More precisely, by (2.11),

so that by Proposition 3.3, we have for every ,

where is defined similarly to but with the step sequence In particular, is now a couple of Euler schemes with step sequences and respectively.

It follows from the expansions of order of each term of established in Propositions 3.2 and 3.3 respectively that

| (5.47) |

where is defined in Lemma B.9 and

By Lemma B.9

| (5.48) |

5.2 Proof of Theorem 2.2.

is an -version of Theorem 2.1 so that it relies on the same decomposition. More precisely, it is a direct consequence of (5.47) and (5.48) combined with Propositions 4.4 and 4.5.

Claim is based on the (sharper) second expansions of Propositions 3.2 and 3.3 up to order . More precisely, using the same strategy as in (5.47), one obtains

where is defined by (2.18) (and explicitly given by (2.21)), is given by

and (resp. ) denotes a remainder term induced by the coarse level (resp. by the levels ). By Propositions 3.2 and 3.3, one obtains when ,

where is a centered random variable independent of and and such that (In fact, for , one is slightly more precise than in Proposition 3.3 by separating the martingale component and the bias component in the ).

On the other hand, we obtain similarly to (5.48):

With the help of these properties (and from the independence of the strata), we deduce that

The result is then a consequence of Propositions 4.4 and 4.5 combined with the following expansion available for any : (see (B.66)). In particular, it is worth noting that when ,

which induces the rectangular term .

5.3 Proof of Theorem 2.3

Step 1(Optimization of the step parameter ): This step is devoted to the optimization of the starting step , in order to equalize the impact of the bias and of the variance in the first term of the expansion of the in (2.31). It amounts to solving the elementary minimization problem

We rely on the following elementary lemma (whose proof is left to the reader).

LEMMA 5.6.

Let . Then,

and

Consequently,

attained at given by

| (5.49) |

Step 2 (Optimization of the size of the coarse level): We introduce an auxiliary allocation parameter to dispatch the target global so that the contribution of the first and the second term in the right hand side of (2.31) are and respectively. The first of these two equalities reads

where the step parameter is given by (5.49). One straightforwardly derives that

| (5.50) |

where

Step 3 (Calibrating the depth ): To calibrate , we will now deal with the second term of the expansion (2.31). Since we have no clue on the sign of the residual bias term , we will replace it by its absolute value. Moreover, we can plug in its formula the above expression (5.49) of the optimal step size which yields

Consequently, using the function introduced in (2.32) and the obvious fact that , this second term will be upper-bounded by as soon as

| (5.51) |

where as owing to the assumption made on the sequence .

Given the expression obtained for , this inequality is satisfied in turn as soon as

or equivalently

| (5.52) |

where

Note that under the assumptions made on the sequence , , In order to ensure the above condition, we begin by rewriting the left-hand side as follows:

| (5.53) |

and will apply the next lemma with and :

LEMMA 5.7.

Let . Then, for every , there exists a unique solution to

The function is increasing and satisfies

| (5.54) |

and

| (5.55) |

where , .

Proof. The function defined on is continuous, increasing in both and , and which ensures the existence of a unique solution to the equation . The monotony of follows from that of . Its limit at infinity follows from the fact that and the inequality in (5.54) is a consequence of the fact that as . For the expansion, we first note that satisfies the second order equation

with where so that

| (5.56) |

We derive from the inequality in Equation (5.54) that, for small enough ,

Consequently, we derive from (5.56) that

| (5.57) |

so that . Plugging this back into (5.57) yields

Now let be the solution of the above equation where . We have

Now, we set

We derive from the above lemma the following useful estimates for :

Now, it follows from the very definitions of and that

where is defined in the proof of the previous lemma. Plugging these inequalities into (5.53) yields

| (5.58) |

The above inequality on the right implies that (6.59) will be true as soon as satisfies

In fact, one will try to saturate the above condition, to choose such that

As the function is a decreasing homeomorphism from onto this equation always has a solution . Unfortunately it turns out to be of little interest in its present form for practical implementation since both are unknown.

However, as as , and as , we derive that

Step 4 (MSE, number of iterations and resulting complexity):

Resulting : From what precedes, we deduce that after iterations, the MSE is lower than .

Size: it follows from Equation (5.50) in Step 1 combined with the left inequality in Equation (5.58) that

Complexity: Set . The asymptotic resulting complexity satisfies

so that

Initialization of the step: it follows from (5.49), the assumption made on and the convergence of that

where we used that . Finally using the expression of , we get

6 Numerical experiments

6.1 Practitioner’s corner

In this section, we want to provide some helpful informations for some practical use of the optimized algorithm given in Theorem 2.3. Let denote the prescribed RMSE and let be an integer greater than . In what follows we aim at computing for a given function such that is supposed to be a smooth enough coboundary.

The weights

Computation of .

We recall that where is the unique solution to . For the computation of , we use the classical (one-dimensional) zero search Newton algorithm. For standard values of and , the reader may use Table 1. Finally, note that, “though” , one has .

Values for and choice of .

The quantity appears in the size parameter (and in the complexity parameter given by (2.33)). Going back to the optimization procedure of the previous section, one remarks that for some fixed and , one can replace by . This strategy leads to sharper bounds on the size parameter for a given RMSE . We refer to the first paragraph of Section 6.2 for further investigations on this topic (see (6.60) below and what precedes). Consequently, in Table 2, we give some values of , but also of , corresponding to some standard specifications encountered in practical simulations. This also allows to check how varies for such low values of compared to . The conclusion is that is an acceptable proxy of .

| 2.133 | 2.591 | 2.674 | 2.674 | |

| 1.200 | 1.278 | 1.245 | 1.278 | |

| 0.948 | 1.021 | 1.024 | 1.024 |

Computation of .

The specification of the size of the coarse level and, which is less important, the a priori estimation of the global complexity, denoted , both require to estimate, at least theoretically, the parameters , and . We will focus on their calibration in the next paragraph. To some extent, the estimation of is less important and any way out of reach at a reasonable cost.

But even at this stage, it is inserting to analyze their impact on in order to optimize the choice of the root . To this end, we assume for a moment that is known. Going back to the sharper upper-bound of at our disposal, namely (2.33), it suggests to minimize, for fixed , the function

Without going further, let us just note that so that for any since so that it seems that is always a better choice than . But as emphasized in the next section 6.2 (first paragraph devoted to a “toy” Ornstein-Uhlenbeck setting), a sharper study of the complexity involving leads to temper the answer.

Calibration of the parameters

This calibration can be performed as a pre-processing phase based on a preliminary short Monte Carlo simulation, having in mind that only rough estimates are needed.

– Estimation of and . First, let us consider . Through an -version of (1.8), one deduces that for a family of independent random empirical measures , namely

where with (say in practice to get rid of the bias effect even for small values of ) and .

As , it remains to provide an estimator of . To do so we take advantage of the fact that is the (normalized) asymptotic variance of . We thus may use the same strategy as above. More precisely, under Assumption , we deduce from Propositions 3.3 and 4.5 that

if with (say in practice to get rid of the bias effect even for small values of ) with .

– About and . The coefficient will probably always remain mysterious. On the other hand in practice what we really need is rather . However, under the assumption made on in Theorem 2.3, one can make the guess from its very definition that its value is not too far from or is at least of order a few units. In particular, if the coefficients have a polynomial growth or even , , . If they have an exponential growth it remains finite (but possibly large). The point of interest is that, anyway, this value is much more stable than the first coefficient itself which would come out in a standard MLMC Langevin simulation framework (not investigated here).

The parameter seems to be unaccessible as well, but for another reason: it is the variance induced by a second order martingale. However as noticed in Section 6.2 (first paragraph), is the ratio of two variance terms so that it seems not so much dependent on the magnitude of the diffusion coefficient (in fact it can be noted that the same property holds for ).

REMARK 6.10.

The numerical investigations of the next section show that the algorithm is very robust to the choice of the parameters. For simple practice, we thus recommend to get a rough estimation of and possibly of and to set .

6.2 Numerical tests

We propose in this section to provide some numerical tests of our algorithm.

Orstein-Uhlenbeck process: oracle and blind simulation.

We begin with the Ornstein-Uhlenbeck process in dimension solution to

with . We recall that this case is a toy example since whole the computations can be made explicit. In particular, so that . Furthermore, is the unique solution (up to a constant) to the Poisson equation and it follows that

The reader can remark that in this case, the ratios and do not depend on . Even though this property can not be really generalized, it however emphasizes a stability of these parameters with respect to the variance of the model. The bias terms can also be computed: using that and that for , we get (so that ).

We want in this part to get a sharp estimate of the complexity for several choices of couples . Following the optimization procedure, we go back to the definition of given in (5.50):

and for each value of and , we solve by a Newton method the following equation for :

| (6.59) |

where the values of for are given in Table 2.

We denote by the solution of this equation. Then, the complexity (where we assume that ) is given by

| (6.60) |

This yields the following results for :

| R=3 | R=4 | ||

|---|---|---|---|

| R=3 | R=4 | ||

|---|---|---|---|

On this example, we retrieve the property which says that is a good choice when is small whereas can be greater when this quantity increases. However, as expected, the main parameter is the level of the method which increases when .

Taking only the first term of the expansion of the MSE for the crude procedure, the optimized complexity (with ) for a MSE lower than is equal to and if or respectively.

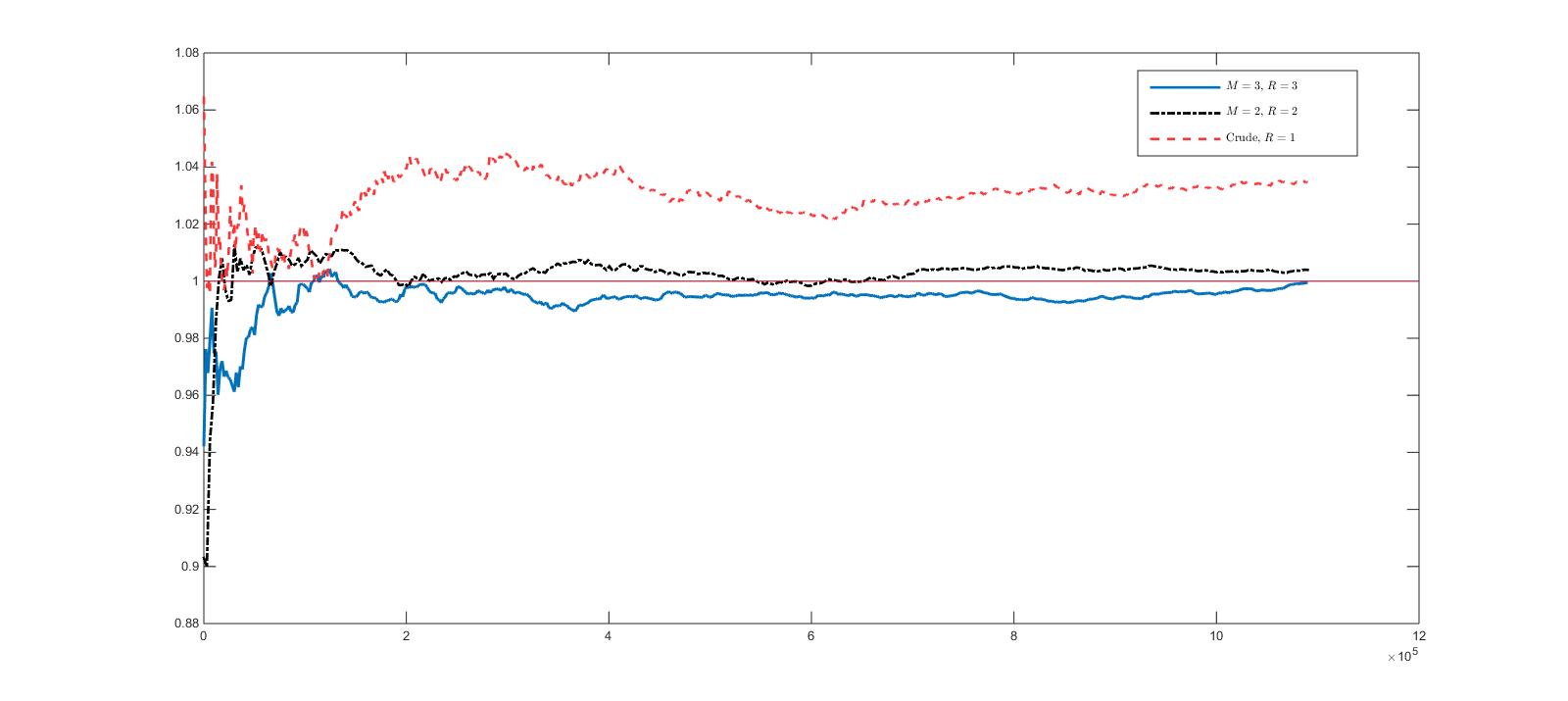

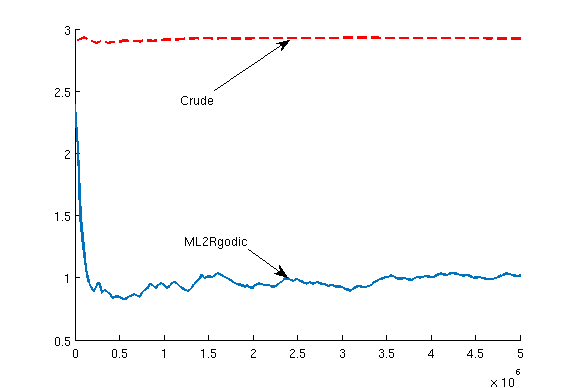

In Figure 1, we compare numerically the evolution of ML2Rgodic with the crude algorithm for and . Note that to obtain a rigorous comparison, the graphs are drawn in terms of the complexity, that once again with a slight abuse of language, is the number of iterations of the Euler scheme involved by procedure.

One remarks that the effect of the Multilevel-RR procedure is increased in the case where the bias is larger. One also remarks in this case that, even though the algorithm is robust to the choice and , the best choice seems to be the one given in Table 3.

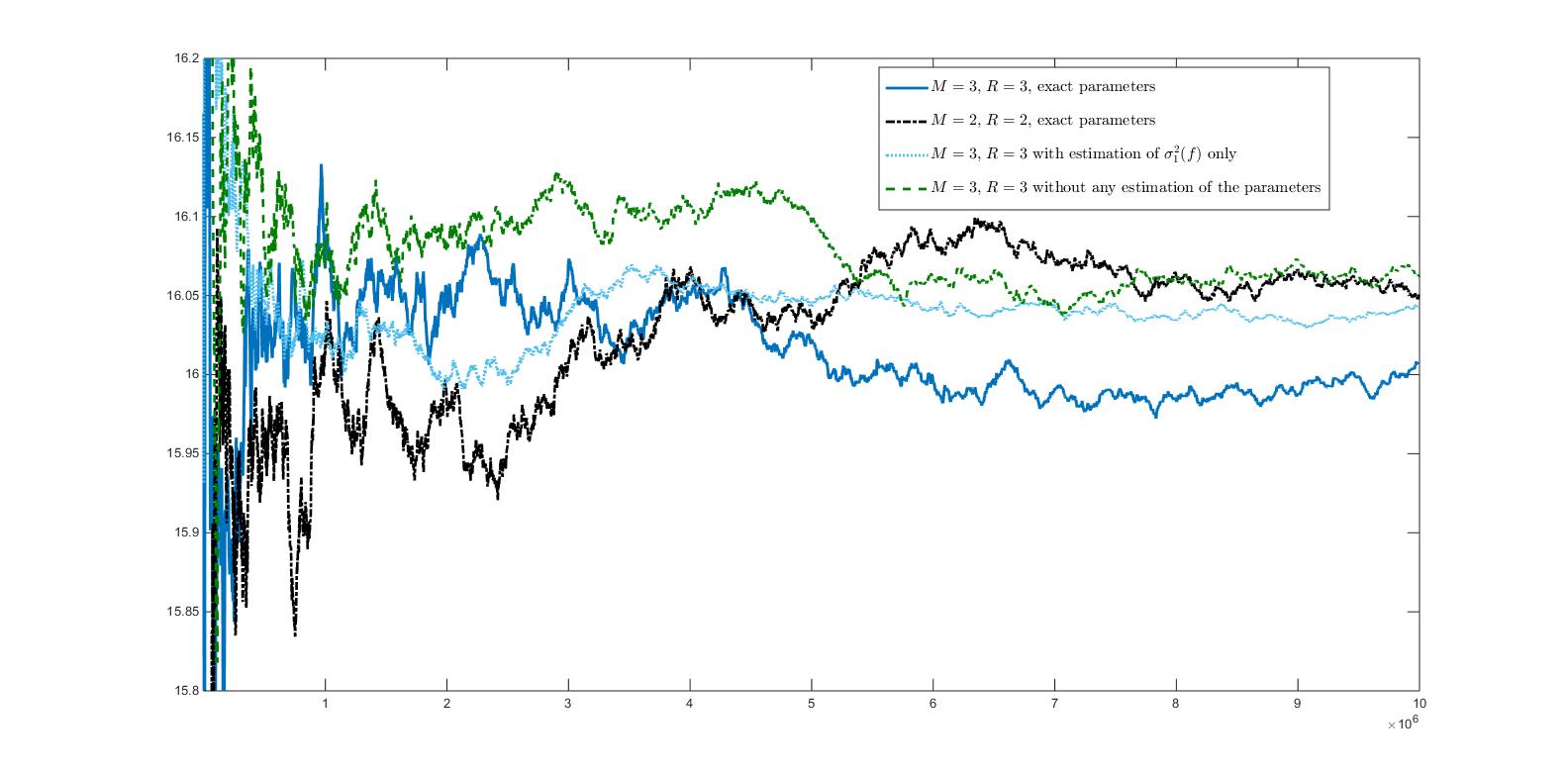

Of course, in practice, one can not make use of the exact parameters. As explained in Section 6.1, it is possible to get a rough estimation of and using the CLTS induced by the procedure. The coefficient can also be estimated but for this coefficient, this requires to use a Multistep method or the procedure ML2Rgodic itself with one more stratum than in the algorithm that we will implement after. Finally, the coefficient seems to be impossible to estimate. This implies that the natural question that the practitioner may ask is: is it possible to get rid of the estimation of the above parameters ?

To answer to this question, we propose in the case to look at the dynamics of the procedure when we choose to fix

-

•

and to estimate and ,

-

•

.

With these two choices of parameters and with , we follow the procedure described in the previous section to estimate , , and . Note that we again obtain and as an optimal choice. In Figure 2, we thus compare the evolution of the previous method (with semi-estimated or not estimated) parameters and we can remark on this example that the algorithm seems to be very robust to the choice of the parameters.

Double-well potential.

We consider a second example in dimension

where which is a non-convex potential (with two local minima in and ) so that Assumption is not fulfilled. However, Assumption is true (see [LPP15], Theorem 2.1). Let us also recall that the invariant distribution satisfies

where .

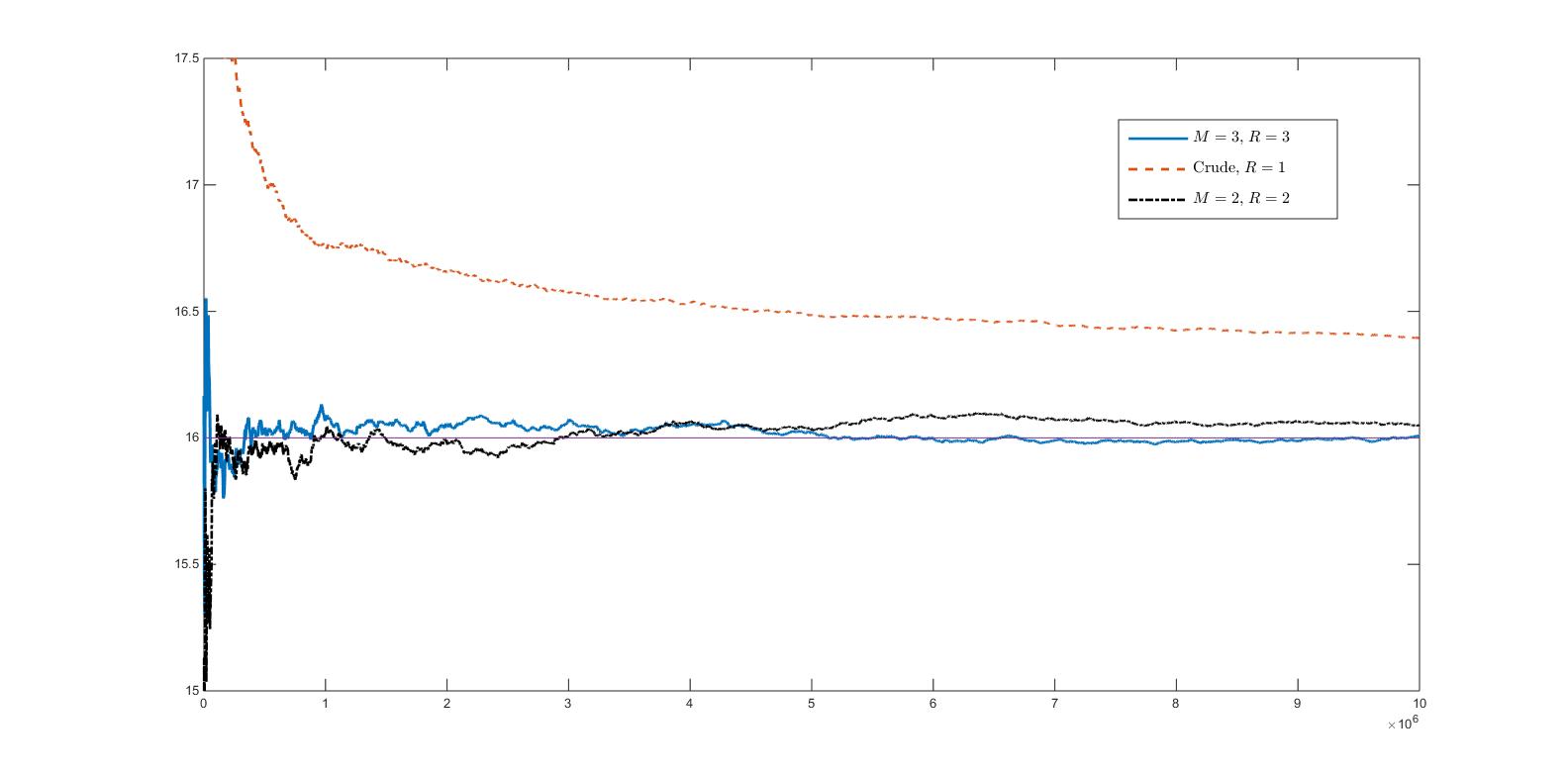

We test the algorithm in this setting with and . Figure 3 shows that ML2Rgodic is still efficient in this setting. The results are obtained using a rough estimation of and and the other parameters are fixed to . Once again, the evolution is compared with the crude algorithm with an optimized choice of and the evolution is drawn as a function of the complexity.

Statistical example (Sparse Regression Learning).

In [DT12], the authors consider the problem of Sparse Regression Learning by Aggregation. For the sake of simplicity, we only recall here the case of linear regression: let denote the number of variables and the number of observations and suppose we are given couples of observations , …, where the vector is the predictor and the scalar is the response. Suppose that there exists such that

where denotes a sequence of random variables with distribution for a given (generally unknown) . Then, the classical question is: how to estimate ? When , the classical methods (such as the least-square method) do not work and it is necessary to introduce some alternative procedures. The estimator of proposed by Dalalyan and Tsybakov – called EWA (for Exponentially Weighted Aggregate) – is designed as follows:

where is the Gibbs probability measure defined by

and is a normalizing coefficient and is the potential defined for some given positive numbers , and by

with .

As mentioned (and already numerically tested) in [DT12], is but the expectation related to the invariant distribution of the following SDE

It can subsequently be estimated through a Langevin Monte-Carlo procedure. The difficulty in this context is the fact that is potentially large so that the numerical computation needs some adaptations. More precisely, in order to avoid an explosion of the Euler scheme, we need to impose the step to be not to large for small values of . We thus assume in what follows that :

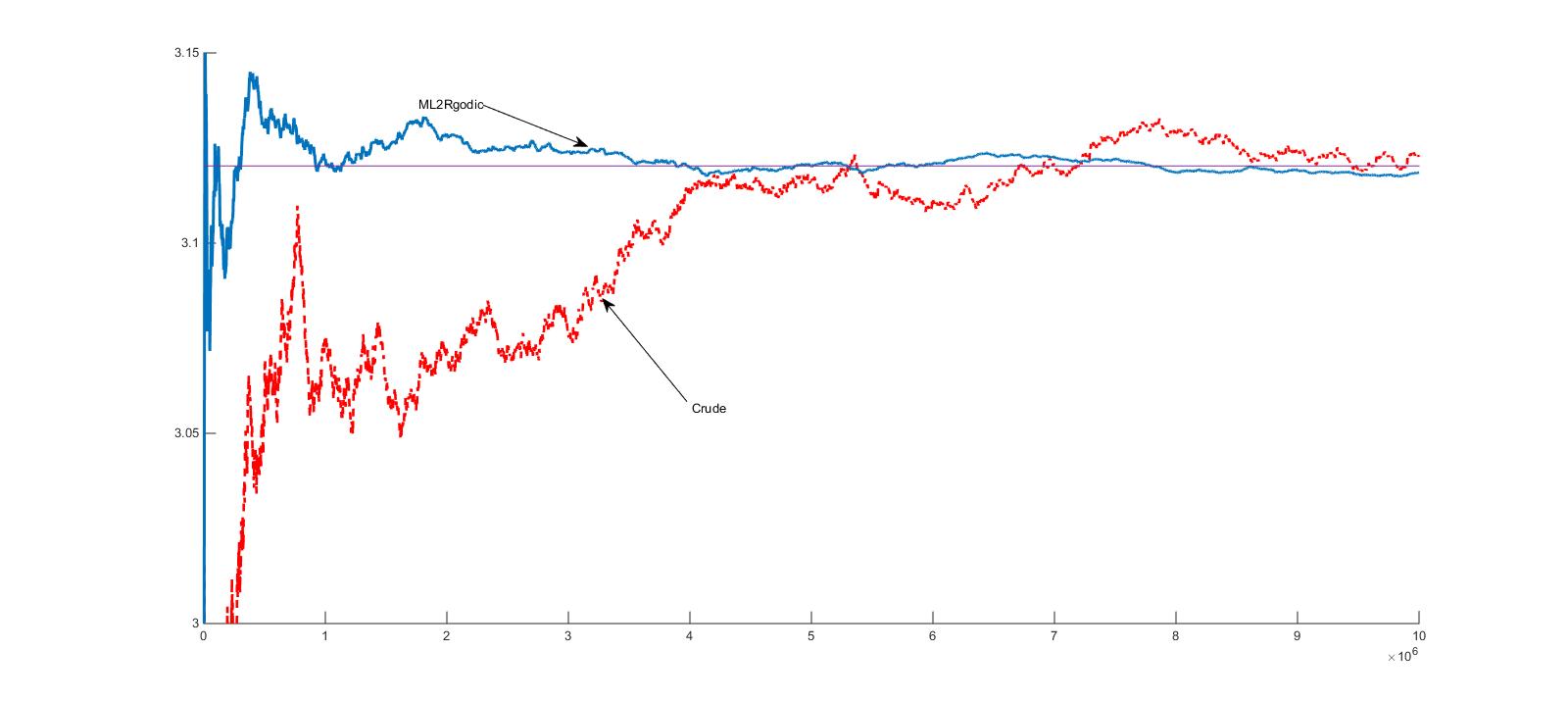

Below, we test our ML2Rgodic estimator on a compressed sensing example given [DT12] (see Example 1) with the parameters given in this paper. We fix (111From a theoretical point of view, should be a positive number such that .)

and the computations are achieved with , and where denotes the sparsity parameter, the number of non-zero components of (of course we do not know which ones). Then, the matrices and are generated from simulated data as follows: in this compressed sensing setting, the matrix has independent Rademacher entries with parameter . The unknown is defined simply by , for every . Finally, following again the parameters given in [DT12], we set .

Denoting by the approximation of obtained after iterations of the scheme, we depict in Figure 4 the evolution of . Note that converges to (which is not equal to ). We compare it with the crude procedure (taken with whereas for the ML2Rgodic procedure, as usual). We can remark that the correction on the bias involved by the weighted Multilevel Langevin procedure strongly improves the estimation of . This remark is emphasized if we compare with the results of [DT12] based on an Euler scheme with constant step where the corresponding quantity is equal to (in this case, the constant step is about ).

References

- [Bha82] R. N. Bhattacharya. On the functional central limit theorem and the law of the iterated logarithm for Markov processes. Z. Wahrsch. Verw. Gebiete, 60(2):185–201, 1982.

- [Bil78] Patrick Billingsley. Ergodic theory and information. Robert E. Krieger Publishing Co., Huntington, N.Y., 1978. Reprint of the 1965 original.

- [DT12] A. S. Dalalyan and A. B. Tsybakov. Sparse regression learning by aggregation and Langevin Monte-Carlo. J. Comput. System Sci., 78(5):1423–1443, 2012.

- [Fri16] N. Frikha. Multi-level stochastic approximation algorithms. Ann. Appl. Probab., 26(2):933–985, 2016.

- [Gil08] M. B. Giles. Multilevel Monte Carlo path simulation. Oper. Res., 56(3):607–617, 2008.

- [GT83] David Gilbarg and Neil S. Trudinger. Elliptic partial differential equations of second order, volume 224 of Grundlehren der Mathematischen Wissenschaften [Fundamental Principles of Mathematical Sciences]. Springer-Verlag, Berlin, second edition, 1983.

- [GT15] C. A. García Trillos. A decreasing step method for strongly oscillating stochastic models. Ann. Appl. Probab., 25(2):986–1029, 2015.

- [HH80] P. Hall and C. C. Heyde. Martingale limit theory and its application. Academic Press, Inc. [Harcourt Brace Jovanovich, Publishers], New York-London, 1980. Probability and Mathematical Statistics.

- [Kre85] U. Krengel. Ergodic theorems, volume 6 of de Gruyter Studies in Mathematics. Walter de Gruyter & Co., Berlin, 1985. With a supplement by Antoine Brunel.

- [Lem05] V. Lemaire. Estimation récursive de la mesure invariante d’un processus de diffusion. Thèse de doctorat, Université de Marne-la-Vallée (France), 2005.

- [Lem07] V. Lemaire. Behavior of the Euler scheme with decreasing step in a degenerate situation. ESAIM Probab. Stat., 11:236–247, 2007.

- [LP02] D. Lamberton and G. Pagès. Recursive computation of the invariant distribution of a diffusion. Bernoulli, 8(3):367–405, 2002.

- [LP03] D. Lamberton and G. Pagès. Recursive computation of the invariant distribution of a diffusion: the case of a weakly mean reverting drift. Stoch. Dyn., 3(4):435–451, 2003.

- [LP13] V. Lemaire and G. Pagès. Multilevel Richardson-Romberg extrapolation. Bernoulli (to appear in), 2013.

- [LPP15] V. Lemaire, G. Pagès, and F. Panloup. Invariant measure of duplicated diffusions and application to Richardson-Romberg extrapolation. Ann. Inst. Henri Poincaré Probab. Stat., 51(4):1562–1596, 2015.

- [Pag07] G. Pagès. Multi-step Richardson-Romberg extrapolation: remarks on variance control and complexity. Monte Carlo Methods Appl., 13(1):37–70, 2007.

- [Pan08] F. Panloup. Recursive computation of the invariant measure of a stochastic differential equation driven by a Lévy process. Annals of Applied Probability, 18(2):379–426, 2008.

- [PP09] G. Pagès and F. Panloup. Approximation of the distribution of a stationary Markov process with application to option pricing. Bernoulli, 15(1):146–177, 2009.

- [PP14] G. Pagès and F. Panloup. A mixed-step algorithm for the approximation of the stationary regime of a diffusion. Stochastic Process. Appl., 124(1):522–565, 2014.

- [PS94] M. Piccioni and S. Scarlatti. An iterative Monte Carlo scheme for generating Lie group-valued random variables. Adv. in Appl. Probab., 26(3):616–628, 1994.

- [PV01] E. Pardoux and A. Yu. Veretennikov. On the Poisson equation and diffusion approximation. I. Ann. Probab., 29(3):1061–1085, 2001.

- [Tal90] D. Talay. Second order discretization schemes of stochastic differential systems for the computation of the invariant law. Stoch. Stoch. Rep., 29(1):13–36, 1990.

Appendix A Proof of Lemma 2.1

Prior to the proof of Lemma 2.1, we need to prove this first technical lemma which will be used to estimate in a precise way the coefficients and involved in the asymptotic mean square error of the ML2Rgodic estimator in Theorems 2.1 and 2.2.

LEMMA A.8.

Let be an integer.and let be pairwise distinct real numbers. Then the unique solution to the solution to the -Vandermonde system

| (A.61) | |||||

| (A.62) | |||||

| (A.63) |

Proof.

The above Vandermonde system can be explicitly solved by the Cramer formulas since its right hand side is of the form for some . Namely

(the column vector replaces the column of the original Vandermonde matrix). Then, elementary computations show that it yields the announced solutions.

To compute the next two sums, we start from the following canonical decomposition of the rational fraction

Setting yields after elementary computations

Now, using that solves the above Vandermonde system, we get

so that

The second identity follows likewise by differentiating the above rational fraction with respect to and then setting again. ∎

Proof of Lemma 2.1. We introduce the auxiliary variables and parameters

| (A.64) |

Then is solution to the system (2.17) if and only if is solution to

Expanding yields by linearity of the above system that it suffices to solve the sequence of -Vandermonde systems.

As the are pairwise distinct, has a unique solutions given by

with the usual convention Consequently, for every ,

Coming back to the weights of interest finally yields the expected formula.

One derives from the definition (2.18) of , using the auxiliary variables, that

and the are given by (A.64). Following the lines of , we derive that

where the identity (A.62) established in the above lemma A.8 yields

Finally

Noting that completes the proof this claim. The computation of follows likewise, starting from the identity (A.63).

In the the starting system (2.17) for the weights no longer depends on and can be cancelled in each equation. This leads to the system

After a standard Abel transform, we get that where the are solution to the Vandermonde system

Note that these weights corresponds to those coming out when dealing with for regular Monte Carlo (see [LP13]) under a weak error expansion condition at rate .

As for the boundedness, first note that the “small” weights read , , with

One straightforwardly checks that and . As a consequence

Appendix B An additional bias term

In this part of the appendix, we focus the bias induced by the approximation

that we use to build some universal weights (by universal, we mean that they do not depend on ). We have the following lemma:

LEMMA B.9.

Assume that with .

Let and such that . Then, for every ,

| (B.65) | |||||

Set

where . We have:

where

with and .

Furthermore, if , then .

REMARK B.11.

Proof.

First, we derive by a comparison argument with integrals and that

| (B.66) |

Elementary computations then show that, for every , , and every , every integer

Using that is -Hölder, we derive from the left inequality in (B.66) that so that, for every ,

| (B.67) | |||||