Physicists’ approach to studying socio-economic inequalities: Can humans be modelled as atoms?

Abstract

A brief overview of the models and data analyses of income, wealth, consumption distributions by the physicists, are presented here. It has been found empirically that the distributions of income and wealth possess fairly robust features, like the bulk of both the income and wealth distributions seem to reasonably fit both the log-normal and Gamma distributions, while the tail of the distribution fits well to a power law (as first observed by sociologist Pareto). We also present our recent studies of the unit-level expenditure on consumption across multiple countries and multiple years, where it was found that there exist invariant features of consumption distribution: the bulk is log-normally distributed, followed by a power law tail at the limit. The mechanisms leading to such inequalities and invariant features for the distributions of socio-economic variables are not well-understood. We also present some simple models from physics and demonstrate how they can be used to explain some of these findings and their consequences.

1 Introduction

Physicists have been always keen on exploring domains outside of physics, like biology, geology, astronomy, sociology, economics, etc., often giving birth to very successful interdisciplinary subjects like biophysics, astrophysics, geophysics, sociophysics, econophysics and so on Chakraborti2016 . The last two interdisciplinary fields: Sociophysics Sen2013 ; Chakrabarti2006 and Econophysics Sinha2010 ; Slanina2013 , have been only recent additions to the long list. However, the physicists’ interest in the social sciences (Economics and Sociology) is quite old, and they have been trying to approach economic and social problems using their experience of modelling physical systems and analysing data. The physicists’ ability to deal with complex dynamical systems have often inspired the central ideas and foundations of the modern axiomatic foundations of economics. No wonder, the first Nobel Prize winner in economics was Jan Tinbergen, a physicist by training (having completed his Ph.D. from the University of Leiden in 1929 on ‘Minimisation problems in Physics and Economics’) Samuelson2016 . The book of Paul Samuelson, the second Nobel Laureate in economics, entitled “Foundations of Economic Analysis” (1947) Samuelson1947 , which is considered as his magnum opus — derived from his doctoral dissertation at Harvard University, makes use of the classical thermodynamic methods of Willard Gibbs wikiGibbs , the American physicist and one of the founders of the area of statistical physics. On the other hand, the economic concept of the ‘invisible hand’ due to Adam Smith wikiSmith , cited as the father of modern economics and best known for his two classic works: The Theory of Moral Sentiments (1759) Smith1759 , and An Inquiry into the Nature and Causes of the Wealth of Nations (1776) Smith1776 , can be understood as an attempt to describe the influence of the market as a spontaneous order on people’s actions and self-organization, which has influenced many models of physical systems. Many such cross-fertilisation of ideas and concepts have been taking place for a long time, eventually leading to intense activities in the field and the coinage of the word:

Econophysics, a new interdisciplinary research field applying methods of statistical physics to problems in economics and finance, first introduced by the theoretical physicist H. Eugene Stanley in an international conference on statistical physics at Kolkata (India) in 1995.

In the field of statistical physics Mandl2002 ; Haar2006 ; Sethna2006 , one often encounters a system of many interacting dynamical units exhibiting a ‘collective behaviour’, which simply depends on a few basic (dynamical) properties of the individual constituents and the embedding dimension of the system. Since it is independent of other details, it thus displays a sort of ‘universality’. Often, socio-economic data also exhibit enough empirical evidences in support of such ‘universalities’, which prompt the physicists’ to propose simple, minimalistic models to understand them using the methods of statistical physics.

In sociology and economics, some of the major issues of concern have beeb inequalities in different forms: income, wealth, etc. It has been argued by certain social scientists that a society or country performs better where the resources are distributed more equitably or there exists less inequalities between the haves and the have-nots Wilkinson2009 . Most economists agree that fairness or equal chances of being involved in the economic activities promote growth Rodrik2003 . It would be impossible to find any society or country where e.g., income or wealth, is equally distributed among its people. The distribution of wealth, income, and consumption has never been uniform, and economists (and very recently physicists) have tried for years to understand the reasons for such inequalities. For a very long time, scholars have been working on the statistical descriptions and mechanisms leading to such inequalities (see e.g., Refs. Sen1992 ; BKChakrabarti2013 ; Deaton1992 ). We briefly mention a few of the empirical observations in the first section of the article. Based on these observations, many questions have been formulated by different scholars. In the following sections, we address from the perspective of the physicists, the questions below:

-

•

How are income, wealth, and consumption distributed and what are the statistical forms of their distributions?

-

•

Are there any robust or “universal” features of the statistical forms and how can they be modelled/reproduced in a mathematical/computational framework?

2 Empirical distributions of income and expenditure

Following several studies spanning more than a century, a few established regularities in income and wealth distributions have been observed. The most popular regularity was proposed by the Italian sociologist and economist, Vilfredo Pareto, who made extensive studies at the end of the 19th century and found that wealth distribution in Europe follows a power law for the very rich Pareto1897 . Later this came to be known as the Pareto law. Subsequent studies revealed that the distributions of income and wealth possess other fairly robust features, like the bulk of both the income and wealth distributions seem to reasonably fit both the log-normal and the Gamma distributions, also sometimes known as Gibrat’s law Gibrat1931 .

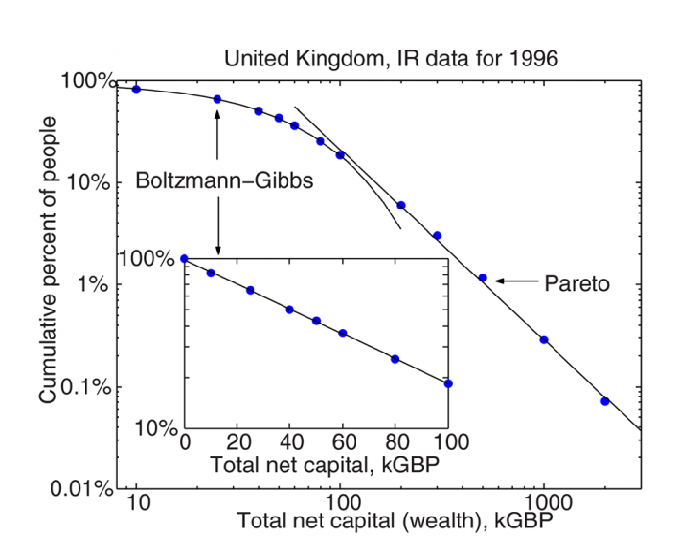

Pareto Law: In 1897, Pareto made extensive studies in Europe and found that wealth distribution follows a power law tail for richer sections of society. For about of the population, the distribution matches a Gibbs or Gamma (black curve), while the income for the top of the population decays much more slowly, following a power- law (red line). ![[Uncaptioned image]](/html/1606.06051/assets/p_tail.png)

Physicists use the Gamma distribution for fitting the probability density or the Boltzmann-Gibbs/exponential distribution for the corresponding cumulative distribution. However, the tail of the distribution fits well to a power law (as first observed by Pareto), the exponent known as the Pareto exponent, usually ranging between and BKChakrabarti2013 . For India too, the wealthiest have been found to have their assets distributed along a power law tail Sinha2006 . The shape of the typical wealth distribution is thus, with Gibbs/Gamma behavior at lower and intermediate values of wealth , and a Pareto (power–law) tail at the larger values, where is a crossover value that depends on the numerical fitting of the data:

| (1) | |||||

where , the equilibrium distribution of wealth, is defined as follows: is the probability that in the steady state of the system, a randomly chosen agent will be found to have wealth between and . The exponent is known as the Pareto exponent, as mentioned earlier, is the average wealth (analogous to the temperature in a gas) of the economic system and is a numerical constant. Detailed empirical results in support of the above statistical form for both income and wealth in different countries, economic societies and over different periods of time, can be found in several research articles, monographs and books that are mentioned in the list of references. For an illustration, Fig. 2 shows the cumulative probability distribution of the net wealth, composed of assets (including cash, stocks, property, and household goods) and liabilities (including mortgages and other debts) in the United Kingdom for the year 1996.

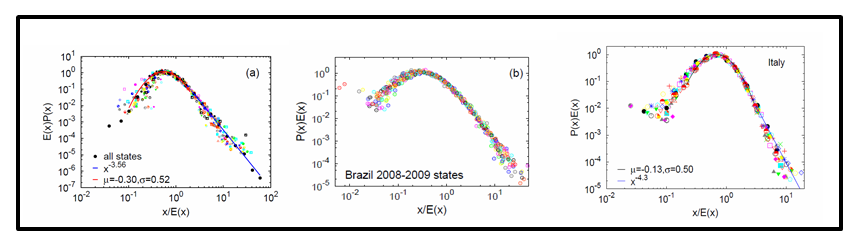

Although income and wealth distribution data are mainly used to quantify economic inequality for individuals or family/households, the distribution of consumer expenditure does also reflect certain aspects of disparity in the society. In a recent study, Chakrabarti et al. Chakrabarti analysed the unit-level expenditure on consumption across multiple countries and multiple years, and showed that certain invariant features of the consumption distribution could be extracted. Specifically, it was shown that the bulk of the distribution follows a log-normal, followed by a power law tail. As shown in Fig. 3, the distributions coincide with each other under normalization by mean expenditure and log scaling, even though the data was sampled across multiple dimensions including, e.g., time, social structure and locations across the globe. This observation seems to indicate that the dispersion in consumption expenditure across various social and economic groups are significantly similar (‘universal’), subject to suitable scaling and normalization. In another article, Chatterjee et al. Chatterjee2016 studied the distributional features and inequality of consumption expenditure, specifically across India – for different states, castes, religion and urban-rural divide. Once again they found that even though the aggregate measures of inequality are fairly diversified across the Indian states, the consumption distributions show near identical statistics after proper normalization. This feature was again seen to be robust with respect to variations in sociological and economic factors. They also showed that state-wise inequality seems to be positively correlated with growth, which is in agreement with the traditional idea of first part of the Kuznets’ curve Kuznets1955 .

Having discussed briefly the first question mentioned in the introduction, we now turn our attention to the modeling of the different robust features of the empirical distributions, by using a mathematical/computational framework that is inspired by some simple models of statistical physics of ideal gas.

3 Kinetic exchange models

The simple yet powerful framework of kinetic theory of ideal gases, first proposed in 1738 by Bernoulli, led eventually to the successful development of statistical physics towards the end of the 19th century Mandl2002 ; Haar2006 ; Sethna2006 . The aim of statistical physics is to study the physical properties of macroscopic systems consisting of a large number of constituent particles. In such large systems, the number of particles is of the order of Avogadro number and it is extremely difficult to have complete microscopic description of such a system.

The basic concept of kinetic exchange model is taken from the ‘Kinetic theory of gases’, which describes a gas as a large number of sub-microscopic particles (atoms and molecules), all of which are in constant, random motion. The rapidly moving “point-like” particles constantly collide with each other or with the walls of the container and exchange kinetic energy. Below we describe in details, how simple simulations can be used to demonstrate the results of the kinetic theory of ‘ideal gases’, which can be adapted to modelling simple closed economic systems for studying income/wealth distribution.

3.1 Kinetic energy exchange model (‘Ideal gas’)

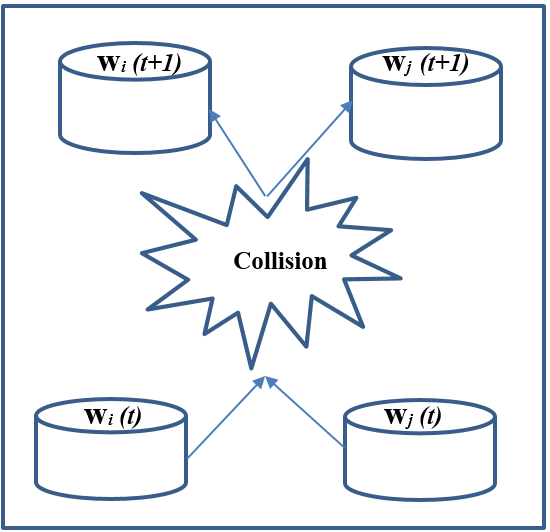

Kinetic exchange models are stochastic models, which are interpreted in terms of energy exchanges in gas molecules. The kinetic exchange model describes the dynamics at a microscopic level, based on pair-wise molecular collisions. Boltzmann wrote that ‘molecules are like so many individuals, having the most various states of motion’ Boltzmann1872 . Thus, for two particles and with energies and at time , the general dynamics can be described by the mathematical equations:

| (2) |

where time changes by one unit after each collision. A typical energy exchange process is shown schematically in Fig. 4.

The Boltzmann-Gibbs distribution wikiBoltzmann , a fundamental law of equilibrium statistical mechanics, states that the probability of finding a physical system or subsystem in a state with energy is given by the exponential function: (3) where is the temperature (average kinetic energy) of the system, is a constant and the conserved quantity is the total energy of the system.

3.2 Simulation of the kinetic energy exchange model

Assume that the interacting units , with , are molecules of a gas with no interaction (potential) energy, and the variables represent their kinetic energies, such that . The time evolution of the system proceeds by a discrete stochastic dynamics Patriarca2013 . A series of updates of the kinetic energies are made at the discrete times . Each update takes into account the effect of a collision between two molecules (as shown in the schematic diagram, Fig. 4). The time step, which can be set to without loss of generality, represents the average time interval between two consecutive molecular collisions; i.e., on average, after each time step , two molecules and undergo a ‘scattering’ process and an update of their kinetic energies and is made. The evolution of the system is accomplished by the following steps at each time :

-

1.

Randomly choose a pair of molecules and and , with kinetic energies and , respectively; they represent the molecules undergoing a collision.

-

2.

Perform the energy exchange between molecules and by updating their kinetic energies,

(4) where is a stochastic variable drawn as a uniform random number between and , at time . The total kinetic energy is conserved during an interaction.

-

3.

Increment the time step, and go to first step (see the MATLAB code given in the appendix).

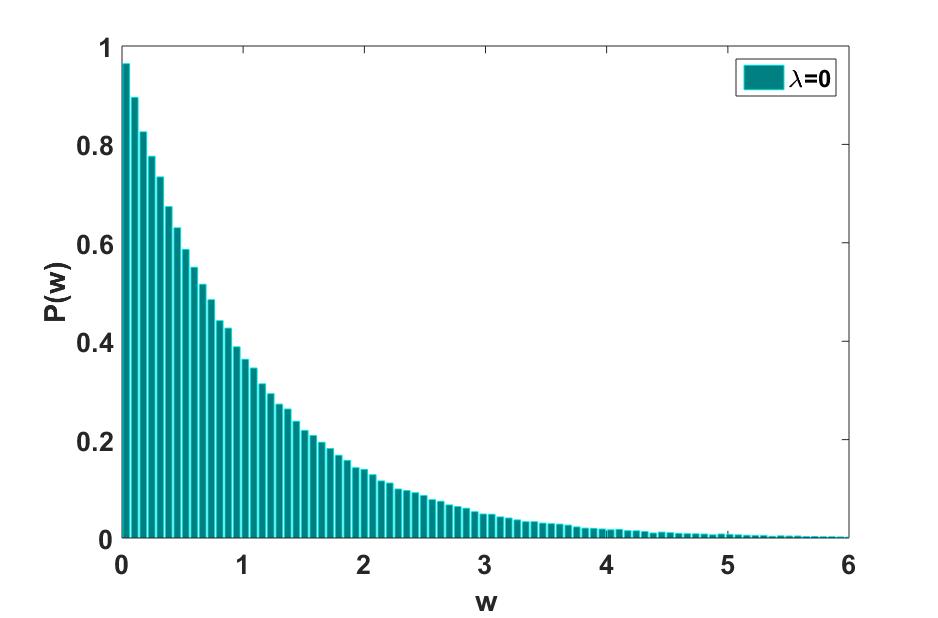

For a large number of molecules () and a sufficient number of time steps (), the system reaches an equilibrium (or steady-state) distribution Goswami2015 . The equilibrium distribution turns out to be the Boltzmann-Gibbs (exponential) distribution, as shown in Fig. 5, which can be derived analytically in several ways– probabilistic calculations Drăgulescu2000 , Master equation Chatterjee2005 , variational principle of maximum entropy Chakraborti2009 , etc. Interestingly, the most probable value of the exponential equilibrium distribution is zero (or very little) energy.

4 Kinetic wealth exchange models

As mentioned in the introduction, understanding the distributions of income and wealth in an economy has been a classic problem in economics for more than a hundred years BKChakrabarti2013 . Inspired from the kinetic theory of gases (mentioned in the last section), the kinetic wealth exchange models (KWEMs) were proposed, which tried to explain the robust and universal features of income/wealth distributions. These form a class of simple multi-agent models, where the actions and interactions of autonomous agents (representing individuals, organizations, societies, etc.), could be used to understand the behaviour of the system as a whole Yakovenko2009 ; Chatterjee2007 ; Chatterjee2010 ; Chakraborti2002 ; Hayes2002 ; Lallouache2010 ; Matthes2008-09 .

KWEMs owe their popularity to the fact that they can capture many of the robust features of realistic wealth distributions using a minimal set of exchange rules Patriarca2013 ; Chakraborti2002 ; Patriarca2004 . In KWEMs, the closed economy or society is described in terms of a simple model, in which agents randomly meet and exchange a part of their wealth Patriarca2013 , similarly to particle assemblies (e.g., a gas) in which from time to time, a pair of particles collide and exchange energy, as given by Eqs. 2. The core of the model dynamics are the simple linear relations in Eqs. 2, and the difficulty is actually in generalizing and adapting the models, and solving analytically the equations. In fact, the exchange of wealth between two agents parallels the exchange of energy between colliding particles to the point that the kinetic theory of a gas in dimensions can suggest the expressions for the equilibrium distributions.

4.1 Model with no saving

The first model of this type was introduced by J. Angle in the context of social science (see Refs. Angle1986 ; Angle2006 ), already some years earlier than in physics or economics. In the 1960’s, Mandelbrot had suggested the possibility ‘. . . to consider the exchanges of money which occur in economic interaction as analogous to the exchanges of energy which occur in physical shocks between gas molecules …’ Mandelbrot1960 , but it was not until the works of E. Bennati Bennati1993 that such an analogy between statistical mechanics and the economics of wealth exchange was realized in terms of a quantitative Monte Carlo model, for which the corresponding numerical simulations demonstrated that the Boltzmann-Gibbs distribution was the equilibrium wealth distribution. Later, many physicists independently discovered such results by Monte Carlo simulations Drăgulescu2000 ; Ispolatov1998 . However, the introduction of ‘saving propensity’ (Chakraborti2000 ), as will be described next, brought forth the Gamma-like feature Patriarca2004 ; Chakraborti2008 of the distribution and such a kinetic exchange model with uniform saving propensity for all agents was subsequently shown to be equivalent to a commodity clearing market, where each agent maximizes his/her own utility Chakrabarti2010-4 .

4.2 Model with uniform saving

The concept of saving propensity was considered in this framework, first by Chakraborti and Chakrabarti Chakraborti2000 . In this model, the agents save a fixed fraction of their wealth, when interacting with another agent. Thus, two agents with initial wealth and at time interact such that they end up with wealth and given by

| (5) |

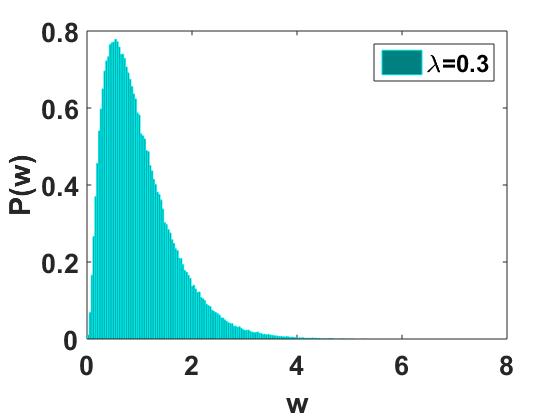

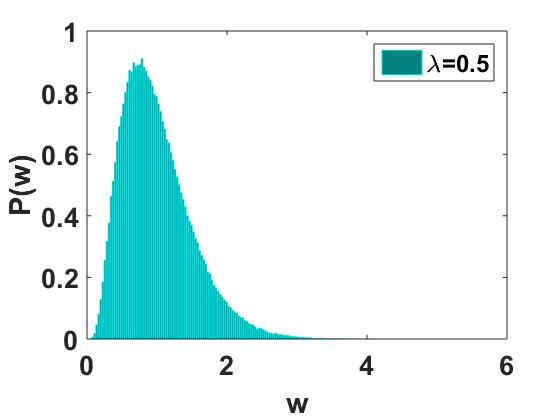

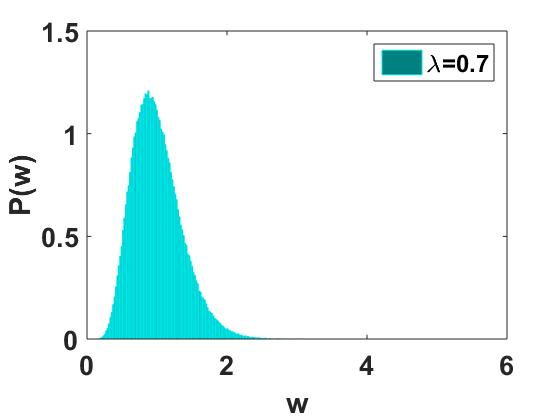

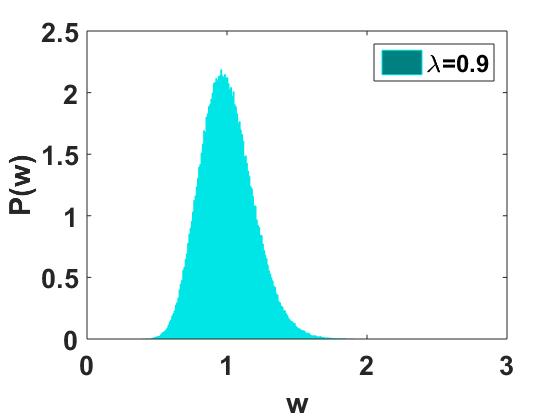

where is a stochastic fraction between and , drawn from an uniform random distribution at time . If , equivalent to Bennati model Bennati1993 , then the most probable wealth per agent is zero, and the market is ‘non-interacting’. The market dynamics freezes (no interactions occur) when . For the uniform saving propensity in between the two limits, (), the steady state distribution of money is a Gamma-like distribution Patriarca2004 ; Chakraborti2008 ; Lallouache2010 with exponentially decaying on both sides and the most-probable money per agent shifting away from (for ) to the average wealth of the system, , as (see Fig. 6). Note that there is no closed-form analytical solution of this exchange dynamics for the model with and the Gamma distribution is the one which fits closest/best the simulation results (the first three moments matching exactly and the fourth moment differing Lallouache2010 ). Here, the “self-organizing” feature of the market, simply induced by the “self-interest” of saving by each agent without any global perspective, is quite significant as the fraction of poor people (with very little or no money) decrease with saving propensity , and most people end up with some finite fraction of the average money in the market. The fact that savings can reduce inequality has been studied from a data science perspective in a recent article by Sharma et al. Sharma2018 . They also studied the empirical data of Gini indices and gross domestic savings (GDS) for several countries, and looked at the co-evolution of the countries in the inequality or savings spaces. Further, they sought an empirical linkage between the income inequality and savings, mainly for relatively small or closed economies, using linear regression model.

Note also that corresponds to the case where the economy is ideally ‘socialistic’ (inequality of wealth is almost zero), and this is achieved just with the people’s self-interest of saving. Although this fixed saving propensity does not give yet the Pareto-like power-law distribution, the Markovian nature of the scattering or trading processes is effectively lost. Indirectly through , the agents get to know (start ‘interacting’ with) each other and the system co-operatively self-organizes towards a non-zero most-probable distribution (see Fig. 6). Thus, for , the market is effectively ‘interacting’ Goswami2015 . The relaxation time to reach the steady state distribution is a complicated function of the saving propensity and the system size Patriarca2007 .

(a)

(b)

(b)

(c)

(c)

(d)

(d)

Most interestingly for the physicists, the KWEMs in the regime , seem to reproduce the energy dynamics of a -dimensional system, with the additional remarkable feature that the corresponding dimension can assume any real value Chakraborti2009 ; Goswami2015 ; Patriarca2004 , and also establishes interesting links with a generalized -dimensional kinetic theory with real spatial dimension Patriarca2015 ; Patriarca2017 . Numerical simulations suggest that at equilibrium, the system has a Gamma-distribution of order , coinciding with the Boltzmann–Gibbs energy distribution for a -dimensional gas with . The relation between the dimension (or the order ) is: . For , the purely exponential shape is regained.

4.3 Model with distributed savings

In a real society or economy, the interest of saving varies from person to person, which implies that may be a heterogeneous parameter. To mimic this situation, the saving factor may be assumed to be widely distributed within the population Chatterjee2004 ; Chatterjee2003 .

As before, starting with an arbitrary initial (uniform or random) distribution of wealth among the agents, the market evolves with the trading. At each time, two agents are randomly selected and the wealth exchange among them occurs, following the above mentioned scheme. One checks for the steady state, by looking at the stability of the money distribution in successive Monte Carlo steps (one Monte Carlo time step is defined as pairwise exchanges). Eventually, after a typical relaxation time the wealth distribution becomes stationary. This relaxation time is dependent on system size and the distribution of (e.g., for and uniformly distributed ). After this, one averages the money distribution over time steps. Finally, one takes the configurational average over realizations of the distribution to get the money distribution . Interestingly, this non-ergodic model has a power-law decay similar to the decay of the Pareto law (see Eq. 1) with . One may note, for finite size of the market, the distribution has a narrow initial growth up to a most-probable value, after which it decays as a power-law tail for several decades, and then there is a finite cut-off. This Pareto law (with ) covers almost the entire range in wealth of the distribution in the limit . This result can be derived analytically too Mohanty2006 ; Chakraborti2009 .

5 Discussions

There have been several works and extensions done on these simple KWEMs and lot of interesting features were extracted Chakraborti2002 . Recently, a ‘bi-directional exchange model‘ was introduced for mimicking more realistically a wealth exchange Heinsalu2014 ; Heinsalu2015 :

| (6) |

where and are two independent random numbers () and the sum of the variables before and after the collision is conserved, . In the same paper Heinsalu2014 , a generalized microscopic version of the model was also introduced, in which, instead of saving propensity parameters, a few parameters regulated probabilistically the microscopic negotiation dynamics between the two agents. For this model, the numerical fitting of the equilibrium distributions suggested an effective dimension which is just half of the dimension of the saving propensity model of Ref. Chakraborti2000 , i.e., ). This result, as well as the analogous ones based on the numerical fittings of the results of other versions of KWEMs, had remained more a conjecture for some years Lallouache2010 ; Patriarca2004 ; Repetowicz2005 . However, this bi-directional exchange model being more tractable analytically, Katriel Katriel2015 recently managed to show with the help of a Boltzmann equation approach that the relation between the dimension and the saving parameter is exact, thus confirming the deep link between KWEMs and statistical physics. The study of this physics-related aspect of the models has now re-entered a challenging active phase in which the theoretical picture of the relaxation and equilibrium in KWEMs is under investigation.

The kinetic exchange framework can suitably be adapted to other areas in economics as well, e.g., the study of the firm size distributions. The size of a firm is measured by the strength of its workers. A firm grows when one worker joins it after leaving another firm. The rate at which a firm gains or loses workers is called the ‘turnover rate’ in economics literature. Thus, there is a redistribution of workers and the corresponding dynamics can be studied using these exchange models. In the models of firm dynamics, one assumes that: (i) Any formal unemployment is avoided in the model. Thus one does not have to keep track of the mass of workers who are moving in and out of the employed workers pool. (ii) The number of workers is treated as a continuous variable. (iii) The size of a firm is just the number of workers working in the firm. In firm dynamics models, one makes an analogy with the previous subsections that firms are agents and the number of workers in the firm is its wealth. Assuming no migration, birth and death of workers, the economy thus remains conserved. As the ‘turnover rate’ dictates both the inflow and outflow of workers, we need another parameter to describe only the outflow. That parameter may be termed as ‘retention rate’, which describes the fraction of workers who decide to stay back in their firm. This is identical to saving propensity in wealth exchange models, as discussed earlier. Some interesting results using this framework have been produced by Chakrabarti Chakrabarti2012 ; Chakrabarti2013 .

Emergence of consensus is another important issue in sociophysics problems, where the people interact to select an option among different options of a subject like vote, language, culture, opinion, etc. Castellano2009 ; Galam2012 ; Stauffer2013 ; Sen2013 . When each person chooses an option, often a state of consensus is reached. In opinion formation, consensus is analogous to an ‘ordered phase’ in statistical physics, where most of the people have a particular opinion. Several models have been proposed to mimic the dynamics of opinion spreading, and the opinions are usually modelled as discrete or continuous variables and are subject to either spontaneous changes or changes due to binary interactions, global feedback and external factors (see Castellano2009 for a general review). Lallouache et al. LallouacheI2010 ; LallouacheII2010 proposed a minimal multi-agent model for the collective dynamics of opinion formation in the society, by modifying kinetic exchange dynamics studied in the context of wealth distribution in a society. The model presented an intriguing spontaneous symmetry-breaking transition to polarized opinion state starting from non-polarized opinion state LallouacheII2010 , and many other features of interest to the statistical physicists studying phase transitions.

The most interesting aspect of KWEMs is related to their heterogeneous generalizations. In fact, KWEMs owe their popularity to the fact that they can predict realistic wealth distributions using a minimal set of exchange rules Patriarca2013 ; Chakraborti2002 but this cannot be achieved in the framework of homogeneous versions of the models, that (as mentioned earlier) usually lead to the exponential or Gamma-like equilibrium wealth distributions. Instead, the simple addition of a suitable level of heterogeneity, either in the saving propensities of the agents of the KWEM of Ref. Chakraborti2000 , or in the negotiation parameters of the model in Ref. Heinsalu2014 directly leads to the Pareto power-law. In other words, KWEMs suggest that heterogeneity is a key factor in producing the power-law observed in the wealth distributions Patriarca2005 ; Patriarca2010 ; Patriarca2015 ; Patriarca2017b , a fact related to the general interest toward the effects of diversity in ‘Complex Systems’ Patriarca2015 . Also, the dynamics of kinetic exchange models are often criticized for being based on an approach that is far from an actual economic or sociological foundation. However, it has been recently shown, for example, that such a economical dynamics of wealth exchange can also be derived from microeconomic theory Chakrabarti2010-4 ; Chakrabarti2009 . Although standard economics theory assumes that the activities of individual agents are driven solely by the utility maximization principle, the alternative picture that was presented, is that the agents can also be viewed as particles exchanging ‘wealth’, instead of energy, and trading in wealth (energy) conserving two-body scattering, as in entropy maximization based on the kinetic theory of gases. This qualitative analogy between the two maximization principles has thus been firmly established only recently.

6 Final remarks

Human beings are much more complex than particles!! The diverse types of interactions among the heterogeneous human beings make the society even more complex. However, in a certain idealised and simple closed economy (as mentioned in this article), we may ignore many complexities or “degrees of freedom” of the system, and model the system simply as an assembly of atoms or gas particles, in order to reproduce some of the statistical features of the empirical distributions. Definitely the real economy or society is much more complex, but this is perhaps one baby step of the econophysicists towards modelling the reality!

In this article, we could give an exposure to only a few models in one particular area. However, the field of Econophysics has had many many contributions from physicists, economists, mathematicians, financial engineers and others in the last two decades. Important directions and new areas in Econophysics have emerged in the last two decades, and one could get further information from the following Refs.:

-

•

Empirical characterization, analyses and modelling of financial markets and limit order books ChakrabortiI2011 ; ChakrabortiII2011 ; Abergel2011 ; ChakrabortiI2016 .

-

•

Network models and characterization of market correlations among different stocks/sectors Abergel2012 ; Sharma2017a ; Sharma2018b ; Sharma2018c .

-

•

Determination of the income or wealth distribution in societies, and the development of statistical physics models Chakrabarti2005 ; BKChakrabarti2013 .

-

•

Development of behavioural models, and analyses of market bubbles and crashes Abergel2013 ; Abergel2015 ; Pharasi2018 .

-

•

Learning in multi-agent game models and the development of Minority Game models Chakraborti2015 ; ChakrabortiI2015 ; Sharma2018d .

7 Acknowledgment

This manuscript was based on the lectures given by AC at International Christian University-Mitaka, Japan, the Indian Institute of Advanced Study (IIAS)-Shimla, India and the International Conference on ‘Social Statistics in India’ at Asian Development Research Institute-Patna, India. AC and KS heartily thank all the collaborators whose works have been represented here. They also acknowledge the hospitality of IIAS-Shimla where the manuscript was initiated. KS thanks University Grants Commission (Ministry of Human Research Development, Govt. of India) for her senior research fellowship. AC acknowledges financial support from the grant number BT/BI/03/004/2003(C) of Govt. of India, Ministry of Science and Technology, Department of Biotechnology, Bioinformatics division; University of Potential Excellence-II grant (Project ID-47) of the Jawaharlal Nehru University, New Delhi; the DST-PURSE grant given to Jawaharlal Nehru University, New Delhi.

8 Appendix

Code in MATLAB for generating the equilibrium distributions represented in Fig. 5:

![[Uncaptioned image]](/html/1606.06051/assets/matlab_code.png)

References

- (1) A. Chakraborti, D. Raina, K. Sharma, “Can an interdisciplinary field contribute to one of the parent disciplines from which it emerged?”, European Physical Journal Special Topics 225 (17-18), 3127-3135 (2016).

- (2) P. Sen and B.K. Chakrabarti, Sociophysics: An Introduction (Oxford University Press, Oxford, 2013).

- (3) Eds. B.K. Chakrabarti, A. Chakraborti and A. Chatterjee, Econophysics and Sociophysics (Wiley-VCH, Berlin, 2006).

- (4) S. Sinha, A. Chatterjee, A. Chakraborti and B.K. Chakrabarti, Econophysics: An Introduction (Wiley-VCH, Berlin, 2010).

- (5) F. Slanina Essentials of econophysics modelling (Oxford University Press, Oxford, 2013).

- (6) https://en.wikipedia.org/wiki/Jan_Tinbergen (Retrieved on March 13, 2016).

- (7) P. A. Samuelson, Foundations of Economic Analysis (Harvard University Press, Massachusetts, 1947).

- (8) https://en.wikipedia.org/wiki/Josiah_Willard_Gibbs(Retrieved on March 13, 2016).

- (9) https://en.wikipedia.org/wiki/Adam_Smith (Retrieved on March 13, 2016).

- (10) A. Smith, The Theory of Moral Sentiments (A. Kincaid and J. Bell, Edinburgh, 1759).

- (11) A. Smith, The Wealth of Nations (W. Strahan and T. Cadell, London, 1776).

- (12) F. Mandl, Statistical Physics (2nd Ed.) (John Wiley, New York, 2002).

- (13) D. ter Haar, Elements of Statistical Mechanics (Butterworth-Heinemann, Oxford, 1995).

- (14) J.P. Sethna, Statistical Mechanics (Oxford University Press, Oxford, 2006).

- (15) R. G. Wilkinson and K. Pickett, The Spirit Level: Why More Equal Societies Almost Always Do Better (Bloomsbury Press, US, 2009).

- (16) Ed. D. Rodrik, In Search of Prosperity: Analytic Narratives on Economic Growth (Princeton University Press, 2003).

- (17) A. Sen, Inequality Re-examined (Harvard University Press, Massachusetts, 1992).

- (18) B.K. Chakrabarti, A. Chakraborti, S.R. Chakravarty and A. Chatterjee, Econophysics of Income and Wealth Distributions (Cambridge University Press, Cambridge, 2013).

- (19) A. Deaton, Understanding Consumption. Clarendon Lectures in Economics (Clarendon Press, Oxford, 1992).

- (20) V. Pareto, Cours d’economie Politique (F. Rouge, Lausanne, 1897).

- (21) R. Gibrat, Les inégalités économiques, Sirey, Paris (1931).

- (22) S. Sinha, ‘Evidence for Power–law tail of the Wealth Distribution in India’, Physica A 359, pp 555-562 (2006).

- (23) A. A. Dragulescu and V. M. Yakovenko, “Exponential and power-law probability distributions of wealth and income in the United Kingdom and the United States,” Physica A 299, 213–221 (2001).

- (24) A. S. Chakrabarti, A. Chatterjee, T. K. Nandi, A. Ghosh, A. Chakraborti, ‘Quantifying Invariant Features of Within-Group Inequality in Consumption Across Groups’, http://papers.ssrn.com/sol3/papers.cfm?abstract_id=2727616.

- (25) A. Chatterjee, A. S. Chakrabarti, A. Ghosh, A. Chakraborti, T. K. Nandi, ‘Invariant features of spatial inequality in consumption: the case of India’, Physica A 442, pp 169-181 (2016).

- (26) S. Kuznets, ‘Economic Growth and Income Inequality’, American Economic Review 45, pp 1–28 (1955).

- (27) L. Boltzmann, ‘Weitere Studien über das Wärmegleichegewicht unter Gasmolekulen’, Akad. Wiss. Wein 66, 275–370 (1872).

- (28) https://en.wikipedia.org/wiki/Boltzmann_distribution (Retrieved on March 13, 2016).

- (29) M. Patriarca and A. Chakraborti, Am. J. Phys. 81, 618 (2013).

- (30) S. Goswami and A. Chakraborti , ‘Kinetic Exchange Models in Economics and Sociology’, in Eds. R. Lopez-Ruiz, D. Fournier–Prunaret, Y. Nishio, C. Gracio, Nonlinear Maps and their Applications, Springer Proceedings in Mathematics & Statistics (Springer International Publishing, Switzerland, 2015).

- (31) A. A. Drăgulescu and V. M. Yakovenko, Eur. Phys. J. B 17, 723 (2000).

- (32) A. Chatterjee, B. K. Chakrabarti and R.B. Stinchcombe, Phys. Rev. E 72, 026126 (2005).

- (33) A. Chakraborti and M. Patriarca, Phys. Rev. Lett. 103, 228701 (2009).

- (34) V. M. Yakovenko and J. Barkley Rosser, Jr., Rev. Mod. Phys. 81, 1703 (2009).

- (35) A. Chatterjee and B.K. Chakrabarti, Eur. Phys. J. B 60, 135 (2007); A. Chatterjee, S. Sinha and B. K. Chakrabarti, Curr. Sci. 92, 1383 (2007).

- (36) A. Chatterjee, in Eds. G. Naldi et. al., Mathematical Modeling of Collective Behavior in Socio-Economic and Life Sciences (Birkhaüser, Boston, 2010), p. 31.

- (37) A. Chakraborti, Int. J. Mod. Phys. C 13, 1315 (2002).

- (38) B. Hayes, American Scientist 90, 400 (2002).

- (39) M. Patriarca, A. Chakraborti, and K. Kaski, “Statistical model with a standard gamma distribution”, Phys. Rev. E, 70, 016104 (2004).

- (40) M. Lallouache, A. Jedidi and A. Chakraborti, Science and Culture 76, 478 (2010).

- (41) D. Matthes and G. Toscani, J. Stat. Phys. 130, 1087 (2008); D. Matthes and G. Toscani, Kinetic and related Models 1, 1 (2008); V. Comincioli, L. Della Croce and G. Toscani, Kinetic and Related Models 2, 135 (2009).

- (42) J. Angle, Social Forces 65, 293 (1986).

- (43) J. Angle, Physica A 367, 388 (2006).

- (44) B. Mandelbrot, ‘The Pareto-Levy law and the distribution of income’, Int. Econ. Rev. 1, 79 (1960).

- (45) E. Bennati, La Simulazione Statistica Nell’ analisi Della Distribuzione del Reddito: Modelli Realistici e Metodo di Monte Carlo (ETS Editrice, Pisa, 1988); ‘Un metodo di simulazione statistica nell’analisi della distribuzione del reddito’, Rivista Internazionale di Scienze Economiche e Commerciali 35, pp 735–756 (1988); ‘Il metodo Monte Carlo nell’analisi economica’, Rassegna di lavori dell’ISCO 10, pp 31–79 (1993).

- (46) S. Ispolatov, P.L. Krapivsky and S. Redner, Eur. Phys. J. B 2, 267 (1998).

- (47) A. Chakraborti and B. K. Chakrabarti, Eur. Phys. J. B 17, 167 (2000).

- (48) A. Chakraborti and M. Patriarca, Pramana J. Phys. 71, 233 (2008).

- (49) A.S. Chakrabarti and B.K. Chakrabarti, Economics E-journal 4 (2010); available at http://www.economics-ejournal.org/economics/journalarticles/2010-4.

- (50) K. Sharma, S. Das and A. Chakraborti, “Global Income Inequality and Savings: A Data Science Perspective”, accepted in the proceedings of 5th IEEE International Conference on Data Science and Advanced Analytics (DSAA), 2018; available at arXiv:1801.00253 (2018).

- (51) M. Patriarca, E. Heinsalu, A. Chakraborti, and G. Germano, “Relaxation in Statistical Many-agent Economy Models”, Eur. Phys. J. B 57, 219 (2007).

- (52) M. Patriarca, E. Heinsalu, L. Marzola, A. Chakraborti, and K. Kaski. Power laws as statistical mixtures, in S. Battiston, F. de Pellegrini, G. Caldarelli, and E. Merelli, editors, Special Issues - Proceedings ECCS14 – European Conference on Complex Systems, 2014 September 22-26, Lucca, Italy, Berlin, 2015. Springer-Verlag, pp 271-282.

- (53) M. Patriarca, E. Heinsalu, A. Singh and A. Chakraborti, “Kinetic Exchange Models as Dimensional Systems: A Comparison of Different Approaches”, in Eds. F. Abergel et al., Econophysics and Sociophysics: Recent Progress and Future Directions (Springer, Milan, 2017), pp 147-158.

- (54) A. Chatterjee, B.K. Chakrabarti and S.S. Manna, Physica A 335, 155 (2004).

- (55) A. Chatterjee, B.K. Chakrabarti and S.S. Manna, Phys. Scr. T 106, 36 (2003).

- (56) P. K. Mohanty, Phys. Rev. E 74, 011117 (2006).

- (57) E. Heinsalu and M. Patriarca, “Kinetic models of immediate exchange”, Eur. Phys. J. B 87, 170 (2014).

- (58) E. Heinsalu and M. Patriarca, “Uni- versus bi-directional kinetic exchange models”, Int. J. Comp. Economics and Econometrics 50, 213 (2015).

- (59) P. Repetowicz, S. Hutzler and P. Richmond, Physica A 356, 641 (2005).

- (60) G. Katriel, Directed Random Market: the equilibrium distribution. Eur. Phys. J. B, 88:19, 2015.

- (61) A. S. Chakrabarti, Physica A 391, 6039 (2012).

- (62) A. S. Chakrabarti, Eur. Phys. J. B 86, 255 (2013).

- (63) C. Castellano, S. Fortunato and V. Loreto, Rev. Mod. Phys. 81, 591 (2009).

- (64) S. Galam, Sociophysics: A Physicist’s Modeling of Psycho-Political Phenomena (Understanding Complex Systems) (Springer, Heidelberg, 2012).

- (65) D. Stauffer, J. Stat. Phys. 151, 9 (2013).

- (66) M. Lallouache, A. Chakraborti and B.K. Chakrabarti, Science and Culture 76, 485 (2010).

- (67) M. Lallouache, A.S. Chakrabarti, A. Chakraborti and B.K. Chakrabarti, Phys. Rev. E 82, 056112 (2010).

- (68) M. Patriarca, A. Chakraborti, K. Kaski, and G. Germano. Kinetic theory models for the distribution of wealth: Power law from overlap of exponentials, in Eds. A. Chatterjee, S.Yarlagadda, and B. K. Chakrabarti, Econophysics of Wealth Distributions, page 93. Springer, 2005.

- (69) M. Patriarca, E. Heinsalu, and A. Chakraborti. Basic kinetic wealth-exchange models: common features and open problems. Eur. Phys. J. B, 73:145–153, 2010.

- (70) M. Patriarca, E. Heinsalu, A. Chakraborti and K. Kaski. “The Microscopic Origin of the Pareto Law and Other Power-Law Distributions”, in Eds. F. Abergel et al., Econophysics and Sociophysics: Recent Progress and Future Directions (Springer, Milan, 2017), pp 159-176.

- (71) A.S. Chakrabarti and B.K. Chakrabarti, Physica A 388, 4151 (2009).

- (72) A. Chakraborti, I. Muni Toke, M. Patriarca and F. Abergel, ‘Econophysics review: I. Empirical Facts’, Quantitative Finance 11, 991-1012 (2011).

- (73) A. Chakraborti, I. Muni Toke, M. Patriarca and F. Abergel, ‘Econophysics review: II. Agent-based models’, Quantitative Finance 11, 1013-1041 (2011).

- (74) Eds. F. Abergel, B.K. Chakrabarti, A. Chakraborti and M. Mitra, Econophysics of order-driven markets (Springer- Verlag (Italia), Milan, 2011).

- (75) A. Abergel, M. Anane, A. Chakraborti, A. Jedidi, I. Muni Toke, Limit Order Books (Cambridge University Press, 2016).

- (76) Eds. F. Abergel, B.K. Chakrabarti, A. Chakraborti and A. Ghosh, Econophysics of systemic risk and network dynamics (Springer-Verlag (Italia), Milan, 2012).

- (77) K. Sharma, B. Gopalakrishnan, A.S. Chakrabarti, A. Chakraborti, “Financial fluctuations anchored to economic fundamentals: A mesoscopic network approach”, Scientific Reports 7, 8055 (2017).

- (78) K. Sharma, A.S. Chakrabarti and A Chakraborti, “Multi-layered network structure: Relationship between financial and macroeconomic dynamics”, to be published in Eds. F. Abergel et al., New Perspectives and Challenges in Econophysics and Sociophysics (Springer, Milan); available at arXiv:1805.06829 (2018).

- (79) A. Chakraborti, K. Sharma, H.K. Pharasi, S. Das, R. Chatterjee, T.H. Seligman, “Characterization of catastrophic instabilities: Market crashes as paradigm”, available at arXiv:1801.07213 (2018).

- (80) Eds. A. Chatterjee, S.Yarlagadda, and B. K. Chakrabarti, Econophysics of Wealth Distributions (Springer, Milan, 2005).

- (81) Eds. F. Abergel, H. Aoyama, B.K. Chakrabarti, A. Chakraborti and A. Ghosh, Econophysics of Agent-based models (Springer-Verlag (Italia), Milan, 2013).

- (82) Eds. F. Abergel, H. Aoyama, B. K. Chakrabarti, A. Chakraborti and A. Ghosh, Econophysics and Data Driven Modelling of Market Dynamics (Springer, Milan, 2015).

- (83) H.K. Pharasi, K. Sharma, A Chakraborti and T.H. Seligman, “Complex market dynamics in the light of random matrix theory”, to be published in Eds. F. Abergel et al., New Perspectives and Challenges in Econophysics and Sociophysics (Springer, Milan) (2018).

- (84) A. Chakraborti, Y. Fujiwara, A. Ghosh, J.-I. Inoue and S. Sinha, “Physicists’ Approaches to a Few Economic Problems”, in Eds. F. Abergel, H. Aoyama, B. K. Chakrabarti, A. Chakraborti and A. Ghosh, Econophysics and Data Driven Modelling of Market Dynamics (Springer, Milan, 2015).

- (85) A. Chakraborti, D. Challet, A. Chatterjee, M. Marsili, Y.-C. Zhang, B.K. Chakrabarti, “Statistical mechanics of competitive resource allocation using agent-based models”, Physics Reports 552, pp 1-25 (2015).

- (86) K. Sharma, Anamika, A.S. Chakrabarti, A. Chakraborti, S. Chakravarty, “The Saga of KPR: Theoretical and Experimental developments”, Science and Culture Kolkata 84, 31 (2018); available at arXiv:1712.06358.