Inference in Regression Discontinuity Designs with a Discrete Running Variable††thanks: We thank Joshua Angrist, Tim Armstrong, Guido Imbens, Philip Oreopoulos, and Miguel Urquiola and seminar participants at Columbia University, Villanova University, and the 2017 SOLE Annual Meeting for helpful comments and discussions.

Abstract

We consider inference in regression discontinuity designs when the running variable only takes a moderate number of distinct values. In particular, we study the common practice of using confidence intervals (CIs) based on standard errors that are clustered by the running variable as a means to make inference robust to model misspecification (Lee and Card, 2008). We derive theoretical results and present simulation and empirical evidence showing that these CIs do not guard against model misspecification, and that they have poor coverage properties. We therefore recommend against using these CIs in practice. We instead propose two alternative CIs with guaranteed coverage properties under easily interpretable restrictions on the conditional expectation function.

1. Introduction

The regression discontinuity design (RDD) is a popular empirical strategy that exploits fixed cutoff rules present in many institutional settings to estimate treatment effects. In its basic version, the sharp RDD, units are treated if and only if an observed running variable falls above a known threshold. For example, students may be awarded a scholarship if their test score is above some pre-specified level. If unobserved confounders vary smoothly around the assignment threshold, the jump in the conditional expectation function (CEF) of the outcome given the running variable at the threshold identifies the average treatment effect (ATE) for units at the margin for being treated (Hahn et al., 2001).

A standard approach to estimate the ATE is local polynomial regression. In its simplest form, this amounts to fitting a linear specification separately on each side of the threshold by ordinary least squares, using only observations that fall within a prespecified window around the threshold. Since the true CEF is typically not exactly linear, the resulting estimator generally exhibits specification bias. If the chosen window is sufficiently narrow, however, the bias of the estimator is negligible relative to its standard deviation. One can then use a confidence interval (CI) based on the conventional Eicker-Huber-White (EHW) heteroskedasticity-robust standard error for inference.111Proceeding like this is known as “undersmoothing” in the nonparametric regression literature. See Calonico et al. (2014) for an alternative approach.

This approach can in principle be applied whether the running variable is continuous or discrete. However, as Lee and Card (2008, LC from hereon) point out, if the running variable only takes on a moderate number of distinct values, and the gaps between the values closest to the threshold are sufficiently large, there may be few or no observations close to the threshold. Researchers may then be forced to choose a window that is too wide for the bias of the ATE estimator to be negligible, which in turn means that the EHW CI undercovers the ATE, as it is not adequately centered. This concern applies to many empirical settings, as a wide range of treatments are triggered when quantities that inherently only take on a limited number of values exceed some threshold. Examples include the test score of a student, the enrollment number of a school, the number of employees of a company, or the year of birth of an individual.222This setting is conceptually different from a setting with a continuous latent running variable, of which only a discretized or rounded version is recorded in the data. See Dong (2015) for an analysis of RDDs with this type of measurement error.

Following LC’s suggestion, it has become common practice in the empirical literature to address these concerns by using standard errors that are clustered by the running variable (CRV). This means defining observations with the same realization of the running variable as members of the same “cluster”, and then using a cluster-robust procedure to estimate the variance of the ATE estimator. Recent papers published in leading economics journals that follow this methodology include Oreopoulos (2006), Card et al. (2008), Urquiola and Verhoogen (2009), Martorell and McFarlin (2011), Fredriksson et al. (2013), Chetty et al. (2013), Clark and Royer (2013), and Hinnerich and Pettersson-Lidbom (2014), among many others. The use of CRV standard errors is also recommended in survey papers (e.g. Lee and Lemieux, 2010) and government agency guidelines for carrying out RDD studies (e.g. Schochet et al., 2010).

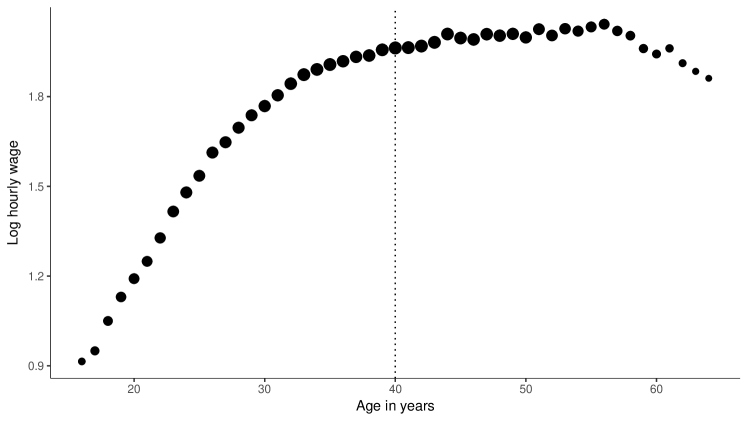

In this paper, we present theoretical, empirical and simulation evidence showing that clustering by the running variable is generally unable to resolve bias problems in discrete RDD settings. Furthermore, using the usual cluster-robust standard error formula can lead to CIs with substantially worse coverage properties than those based on the EHW standard errors. To motivate our analysis, and to demonstrate the quantitative importance of our findings, we first conduct a Monte Carlo study based on real data. Our exercise mimics the process of conducting an empirical study by drawing random samples from a large data set extracted from the Current Population Survey, and estimating the effect of a placebo treatment “received” by individuals over the age of 40 on their wages, using a discrete RDD with age in years as the running variable. By varying the width of the estimation window, we can vary the accuracy of the fitted specification from “very good” to “obviously incorrect”. For small and moderate window widths, CRV standard errors turn out to be smaller than EHW standard errors in most of the samples, and the actual coverage rate of CRV CIs with nominal level 95% is as low as 58%. At the same time, EHW CIs perform well and have coverage much closer to 95%. For large window widths (paired with large sample sizes), CRV CIs perform relatively better than EHW CIs, but both procedures undercover very severely.

To explain these findings, we derive novel results concerning the asymptotic properties of CRV standard errors and the corresponding CIs. In our analysis, the data are generated by sampling from a fixed population, and specification errors in the (local) polynomial approximation to the CEF are population quantities that do not vary across repeated samples. This is the standard framework used throughout the theoretical and empirical RDD literature. In contrast, LC motivate their approach by modeling the specification error as random, with mean zero conditional on the running variable, and independent across the “clusters” formed by its support points. As we explain in Section 3.3 however, their setup is best viewed as a heuristic device; viewing it as a literal description of the data generating process is unrealistic and has several undesirable implications.

Our results show that in large samples, the average difference between CRV and EHW variance estimators is the sum of two components. The first component is generally negative, does not depend on the true CEF, decreases in magnitude with the number of support points (that is, the number of “clusters”), and increases with the variance of the outcome. This component is an analog of the usual downward bias of the cluster-robust variance estimator in settings with a few clusters; see Cameron and Miller (2014) for a recent survey. The second component is non-negative, does not depend on the variance of the outcome, and is increasing in the average squared specification error. Heuristically, it arises because the CRV variance estimator treats the (deterministic) specification errors as cluster-specific random effects, and tries to estimate their variability. This component is equal to zero under correct specification.

This decomposition shows that CRV standard errors are on average larger than EHW standard errors if the degree of misspecification is sufficiently large relative to the sampling uncertainty and the number of support points in the estimation window. However, the coverage of CRV CIs may still be arbitrarily far below their nominal level, as the improvement in coverage over EHW CIs is typically not sufficient when the coverage of EHW CIs is poor to begin with. Moreover, when the running variable has many support points, a more effective way to control the specification bias is to choose a narrower estimation window. In the empirically relevant case in which the degree of misspecification is small to moderate (so that it is unclear from the data that the model is misspecified), clustering by the running variable generally amplifies rather than ameliorates the distortions of EHW CIs.

In addition to CRV CIs based on conventional clustered standard errors, we also consider CIs based on alternative standard error formulas suggested recently in the literature on inference with a few clusters (cf. Cameron and Miller, 2014, Section VI). We find that such CIs ameliorate the undercoverage of CRV CIs when the misspecification is mild at the expense of a substantial loss in power relative to EHW CIs (which already work well in such setups); and that their coverage is still unsatisfactory in settings where EHW CIs work poorly. This is because the second term in the decomposition does not adequately reflect the magnitude of the estimator’s bias.

These results caution against clustering standard errors by the running variable in empirical applications, in spite of its great popularity.333Of course, clustering the standard errors at an appropriate level may still be justified if the data are not generated by independent sampling. For example, if the observational units are students, and one first collects a sample of schools and then samples students from those schools, clustering on schools would be appropriate. We therefore propose two alternative CIs that have guaranteed coverage properties under interpretable restrictions on the CEF. The first method relies on the assumption recently considered in Armstrong and Kolesár (2016) that the second derivative of the CEF is bounded by a constant, whereas the second method assumes that the magnitude of the approximation bias is no larger at the left limit of the threshold than at any point in the support of the running variable below the threshold, and similarly for the right limit. Both CIs are “honest” in the sense of Li (1989), which means they achieve asymptotically correct coverage uniformly over all CEFs satisfying the respective assumptions. Their implementation is straightforward using the software package RDHonest, available at https://github.com/kolesarm/RDHonest.

We illustrate our results in two empirical applications, using data from Oreopoulos (2006) and Lalive (2008). In both applications, we find that the CRV standard errors are smaller than EHW standard errors, up to an order of magnitude or more, with the exact amount depending on the specification. Clustering by the running variable thus understates the statistical uncertainty associated with the estimates, and in the Oreopoulos (2006) data, it also leads to incorrect claims about the statistical significance of the estimated effect. Honest CIs based on bounding the second derivative of the CEF are slightly wider than those based on EHW standard errors, while the second type of honest CI gives quite conservative results unless one restricts the estimation window.

The rest of the paper is organized as follows. The following section illustrates the distortion of CRV CIs using a simulation study based on data from the Current Population Survey. Section 3 reviews the standard sharp RDD, explains the issues caused by discreteness of the running variable, and discusses LC’s original motivation for clustering by the running variable. Section 4 contains the main results of our theoretical analysis, and Section 5 discusses the construction of honest CIs. Section 6 contains two empirical illustrations. Section 7 concludes. Technical arguments and proofs are collected in the appendix. The supplemental material contains some additional theoretical results, and also additional simulations that study the performance of CRV and EHW CIs as well as honest CIs from Section 5.

2. Evidence on Distortions of CRV Confidence Intervals

To illustrate that clustering by the running variable can lead to substantially distorted inference in empirically relevant settings, we investigate the performance of the method by applying it to wage data from the Current Population Survey.

2.1. Setup

Our exercise is based on wage data from the Outgoing Rotation Groups of the Current Population Survey (CPS) for the years 2003–2005. The data contain 170,693 observations of the natural logarithm of hourly earnings in US$ and the age in years for employed men aged 16 to 64. The data are augmented with an artificial treatment indicator that is equal to one for all men that are at least 40 years old, and equal to zero otherwise.444See Lemieux (2006), who uses the same dataset, for details on its construction. The artificial threshold of 40 years corresponds to the median of the observed age values. Considering other artificial thresholds leads to similar results. Figure 1 plots the average of the log hourly wages in the full CPS data by worker’s age, and shows that this relationship is smooth at the treatment threshold. This indicates that our artificial treatment is indeed a pure placebo, with the causal effect equal to zero.

For our exercise, we draw many small random samples from the full CPS data, and estimate the effect of the artificial treatment using an RDD, with log hourly wage as the outcome and age as the running variable, on each of them. Figure 1 therefore plots the true CEF of log hourly wages given age for the population from which our samples are taken. In particular, we draw random samples of size , from the set of individuals in the full CPS data whose age differs by no more than from the placebo cutoff of 40. In each sample, we use OLS to estimate the regression

| (2.1) |

for (a linear model with different intercept and slope on each side of the cutoff), and (a quadratic specification). The OLS estimate of is then the empirical estimate of the causal effect of the placebo treatment for workers at the threshold. The parameter is a window width (or bandwidth) that determines the range of the running variable over which the specification approximates the true CEF of log hourly wages given age. The regression coefficients in (2.1) are subscripted by because their value depends on the window width (the dependence on is left implicit). Running OLS on specification (2.1) is equivalent to local linear () or local quadratic () regression with a bandwidth and a uniform kernel function on a sample with individuals whose age differs by less than from the threshold.

Since we know the true CEF in the context of our exercise, we can compute the population values of the coefficients in the model (2.1) for the various values of and under consideration by estimating it on the full CPS data. Inspection of Figure 1 shows that the model (2.1) is misspecified to some degree for all values of and under consideration, as the dots representing the true CEF of log wages never lie exactly on a straight or quadratic line (Figures LABEL:fig_data1a and LABEL:fig_data1b in Appendix C show the resulting approximations to the CEF). As a result, the parameter , reported in the second column of Table 1, which approximates the true jump of the CEF at the placebo cutoff, is never exactly equal to zero. The degree of misspecification varies with and . In the linear case (), it is very small for , but increases substantially for larger values of . On the other hand, the quadratic model () is very close to being correctly specified for all values of that we consider.

To assess the accuracy of different methods for inference, in addition to the point estimate , we compute both the CRV and EHW standard error (using formulas that correspond to the default settings in STATA; see below for details) in each random sample. Because the OLS estimator is centered around , which due to misspecification of the model (2.1) differs from the true effect of zero, we expect that the 95% EHW CI, given by , contains the zero less than 95 percent of the time. However, when is close to zero relative to the standard deviation of we expect this distortion to be small. Moreover, if clustering by the running variable is a suitable way to correct the distortion, the CRV standard error of should generally be larger than the EHW standard error (to account for the incorrect centering), and the CRV CI, given by , should contain the true effect of zero in roughly 95 percent of the random samples across all specifications.

2.2. Main results

| Average SE | Rate CRV SE [2pt] EHW SE | CI coverage rate | ||||||

| CRV | EHW | CRV | EHW | |||||

| Linear Specification () | ||||||||

| 5 | 100 | 0.239 | 0.166 | 0.234 | 0.14 | 0.773 | 0.938 | |

| 500 | 0.104 | 0.073 | 0.104 | 0.13 | 0.780 | 0.947 | ||

| 2000 | 0.052 | 0.036 | 0.052 | 0.13 | 0.773 | 0.949 | ||

| 10000 | 0.021 | 0.015 | 0.023 | 0.09 | 0.772 | 0.961 | ||

| 10 | 100 | 0.227 | 0.193 | 0.223 | 0.26 | 0.873 | 0.939 | |

| 500 | 0.099 | 0.086 | 0.099 | 0.25 | 0.876 | 0.944 | ||

| 2000 | 0.049 | 0.044 | 0.050 | 0.27 | 0.860 | 0.930 | ||

| 10000 | 0.021 | 0.021 | 0.022 | 0.39 | 0.781 | 0.829 | ||

| 15 | 100 | 0.222 | 0.197 | 0.216 | 0.31 | 0.884 | 0.927 | |

| 500 | 0.095 | 0.089 | 0.096 | 0.34 | 0.853 | 0.899 | ||

| 2000 | 0.048 | 0.047 | 0.048 | 0.45 | 0.712 | 0.730 | ||

| 10000 | 0.020 | 0.028 | 0.021 | 0.92 | 0.348 | 0.153 | ||

| 100 | 0.208 | 0.196 | 0.205 | 0.38 | 0.856 | 0.886 | ||

| 500 | 0.091 | 0.094 | 0.091 | 0.54 | 0.673 | 0.667 | ||

| 2000 | 0.045 | 0.058 | 0.046 | 0.93 | 0.292 | 0.134 | ||

| 10000 | 0.019 | 0.043 | 0.020 | 1.00 | 0.006 | 0.000 | ||

| Quadratic Specification () | ||||||||

| 5 | 100 | 0.438 | 0.206 | 0.427 | 0.03 | 0.607 | 0.932 | |

| 500 | 0.189 | 0.086 | 0.190 | 0.01 | 0.599 | 0.947 | ||

| 2000 | 0.093 | 0.042 | 0.095 | 0.01 | 0.587 | 0.951 | ||

| 10000 | 0.038 | 0.018 | 0.042 | 0.00 | 0.595 | 0.964 | ||

| 10 | 100 | 0.361 | 0.258 | 0.349 | 0.15 | 0.795 | 0.933 | |

| 500 | 0.157 | 0.110 | 0.156 | 0.12 | 0.790 | 0.948 | ||

| 2000 | 0.077 | 0.055 | 0.078 | 0.11 | 0.794 | 0.947 | ||

| 10000 | 0.033 | 0.025 | 0.035 | 0.13 | 0.808 | 0.956 | ||

| 15 | 100 | 0.349 | 0.270 | 0.329 | 0.20 | 0.836 | 0.923 | |

| 500 | 0.146 | 0.117 | 0.147 | 0.18 | 0.851 | 0.946 | ||

| 2000 | 0.073 | 0.058 | 0.073 | 0.17 | 0.839 | 0.946 | ||

| 10000 | 0.031 | 0.026 | 0.033 | 0.18 | 0.828 | 0.937 | ||

| 1 | 0.316 | 0.267 | 0.303 | 0.26 | 0.876 | 0.930 | ||

| 500 | 0.134 | 0.117 | 0.135 | 0.24 | 0.890 | 0.949 | ||

| 2000 | 0.068 | 0.058 | 0.067 | 0.23 | 0.887 | 0.947 | ||

| 10000 | 0.029 | 0.027 | 0.030 | 0.26 | 0.910 | 0.960 | ||

Note: Results are based on 10,000 simulation runs.

Table 1 reports the empirical standard deviation of across simulation runs, the average values of the EHW and CRV standard errors, the proportion of runs in which the CRV standard error was larger than the EHW standard error, and the empirical coverage probabilities of the EHW and CRV CI with nominal level 95%. These results are as expected regarding the properties of EHW standard errors and CIs. They also show, however, that the CRV standard error is a downward-biased estimator of the standard deviation of in almost all the specifications that we consider, and is thus typically smaller than the EHW standard error. Correspondingly, the CRV CI has coverage properties that are mostly worse than those of the EHW CI.

A closer inspection of Table 1 reveals further interesting patterns. Consider first the quadratic specification , which, as pointed out above, is close to correct for all bandwidth values. First, we see that when holding the value of constant, the coverage rate of the CRV CI is hardly affected by changes in the sample size, and always below the nominal level of 95%. The undercoverage for is very severe, about 35 percentage points, and decreases as the value of , and thus the number of “clusters” in the data, increases. However, it still amounts to 4–6 percentage points for , in which case there are, respectively, 24 and 25 “clusters” below and above the threshold. Third, the EHW CI has close to correct coverage for all bandwidth values since the degree of misspecification is small.

Next, consider the results for the linear model (), in which the degree of misspecification increases with the bandwidth. First, we see that when holding the sample size constant the value of the CRV standard error is increasing in . The CRV standard error is downward-biased for the standard deviation of when either or are small, and upward-biased if both are large (in the latter case, misspecification is substantial relative to sampling uncertainty). Second, even when the CRV standard error is larger than the EHW standard error, the corresponding CIs still undercover by large amounts.

In summary, our results suggest that if the specification (2.1) is close to correct, clustering by the running variable shrinks the estimated standard error, and thereby leads to a CI that is too narrow. This effect is particularly severe if the number of clusters is small. On the other hand, if misspecification is sufficiently severe relative to the sampling uncertainty, clustering by the running variable increases the standard error, but the resulting CIs often still remain too narrow. In the following sections, we derive theoretical results about the properties of CRV standard errors that shed further light on these findings.

Remark 1.

The results of our simulation exercise illustrate the potential severity of the issues caused by clustering standard errors at the level running variable in discrete RDDs. However, one might be concerned the results are driven by some specific feature of the CPS data. Another possible reservation is that by varying the bandwidth we vary both the degree of model misspecification and the number of “clusters”, and cluster-robust standard errors are well-known to have statistical issues in other settings with a few clusters. To address these potential concerns, we report the results of another simulation experiment in the supplemental material. In that simulation study, the data are fully computer generated, and we consider several data generating processes in which we vary the degree of misspecification and the number of support points of the running variable independently. These additional simulations confirm the qualitative results reported in this section.

Remark 2.

The clustered standard error used in our simulation exercise corresponds to the default setting in STATA. Although its formula, given in Section 3 below, involves a “few clusters” adjustment, this variance estimator is known to be biased when the number of clusters is small. One might therefore be concerned that the unsatisfactory performance of CRV CIs is driven by this issue, and that these CIs might work as envisioned by LC if one used one of the alternative variance estimators suggested in the literature on inference with few clusters. To address this concern, we repeat both the CPS placebo study and the simulation exercise described in Remark 1 using a bias-reduction modification of the STATA formula developed by Bell and McCaffrey (2002) that is analogous to the HC2 modification of the EHW standard error proposed by MacKinnon and White (1985). The results are reported in the supplemental material. The main findings are as follows. When combined with an additional critical value adjustment, also due to Bell and McCaffrey (2002), this fixes the undercoverage of CRV CIs in settings where the specification (2.1) is close to correct. However, this comes at a substantial loss in power relative to EHW CIs, which also have approximately correct coverage in this case (the CIs are more than twice as long in some specifications than EHW CIs). Under more severe misspecification, the adjustments tend to improve coverage relative to EHW CIs somewhat, but both types of CIs generally still perform poorly. Using bias-corrected standard errors does therefore not make CRV CIs robust to misspecification of the CEF.

3. Econometric Framework

In this section, we first review the sharp RDD,555While the issues that we study in this paper also arise in fuzzy RDDs and regression kink designs (Card et al., 2015), for ease of exposition we focus here on the sharp case. For ease of exposition, we also abstract from the presence of any additional covariates; their presence would not meaningfully affect our results. and formally define the treatment effect estimator and the corresponding standard errors and CIs. We then discuss LC’s motivation for clustering the standard errors by the running variable, and point out some conceptual shortcomings.

3.1. Model, Estimator and CIs

In a sharp RDD, we observe a random sample of units from some large population. Let and denote the potential outcome for the th unit with and without receiving treatment, respectively, and let be an indicator variable for the event that the unit receives treatment. The observed outcome is given by . A unit is treated if and only if a running variable crosses a known threshold, which we normalize to zero, so that . Let denote the conditional expectation of the observed outcome given the running variable. If the CEFs for the potential outcomes and are continuous at the threshold, then the discontinuity in at zero is equal to the average treatment effect (ATE) for units at the threshold,

A standard approach to estimate is to use local polynomial regression. In its simplest form, this estimation strategy involves fixing a window width, or a bandwidth, , and a polynomial order , with and being the most common choices in practice. One then discards all observations for which the running variable is outside the estimation window , keeping only the observations for which , and runs an OLS regression of the outcome on a vector of covariates consisting of an intercept, polynomial terms in the running variable, and their interactions with the treatment indicator.666Our setup also covers the global polynomial approach to estimating by choosing . While this estimation approach is used in a number of empirical studies, theoretical results suggest that it typically performs poorly relative to local linear or local quadratic regression (Gelman and Imbens, 2014). This is because the method often implicitly assigns very large weights to observations far away from the threshold.777For ease of exposition, we focus on case with uniform kernel. Analogous results can be obtained for more general kernel functions, at the expense of a slightly more cumbersome notation. Estimates based on a triangular kernel should be more efficient in finite samples (e.g. Armstrong and Kolesár, 2017). The ATE estimator of is then given by the resulting OLS estimate on the treatment indicator. Without loss of generality, we order the components of such that this treatment indicator is the first one, so

where denotes the first unit vector. When , for instance, is simply the difference between the intercepts from separate linear regressions of on to the left and to the right of the threshold. The conventional Eicker-Huber-White (EHW) or heteroskedasticity-robust standard error of is , where is the top-left element of the EHW estimator of the asymptotic variance of . That is,

An alternative standard error, proposed by LC for RDDs with a discrete running variable, is . Here is the top-left element of the “cluster-robust” estimator of the asymptotic variance of that clusters by the running variable (CRV). That is, the estimator treats units with the same realization of the running variable as belonging to the same cluster (Liang and Zeger, 1986). Denoting the support points inside the estimation window by , the estimator has the form888The STATA implementation of these standard errors multiplies by , where is the number of parameters that is being estimated. We use this alternative formula for the numerical results in Sections 2 and 6.

The EHW and CRV CIs for with nominal level based on these standard errors are then given by

respectively, where the critical value is the quantile of the standard normal distribution. In particular, for a CI with 95% nominal coverage we use .

3.2. Potential issues due to discreteness of the running variable

Whether the EHW CI is valid for inference on largely depends on the bias properties of the ATE estimator . It follows from basic regression theory that in finite samples, is approximately unbiased for its population counterpart , given by

(for simplicity, we leave the dependence of on implicit). However, is generally a biased estimator of . The magnitude of the bias, , is determined by how well is approximated by a th order polynomial within the estimation window . If was a th order polynomial function, then , but imposing this assumption is typically too restrictive in applications.

The EHW CI is generally valid for inference on since, if is fixed, the -statistic based on the EHW standard error has a standard normal distribution in large samples. That is, as , under mild regularity conditions,

| (3.1) |

Using the EHW CI for inference on is therefore formally justified if the bias is asymptotically negligible relative to the standard error, in these sense that their ratio converges in probability to zero,

| (3.2) |

Choosing a window width such that condition (3.2) is satisfied is called “undersmoothing” in the nonparametric regression literature. If the distribution of the running variable is continuous, then (3.2) holds under regularity conditions provided that sufficiently quickly as the sample size grows, and that is sufficiently smooth (e.g. Hahn et al., 2001, Theorem 4). This result justifies the use of the EHW standard errors for inference on when has rich support and is chosen sufficiently small.

In principle, the EHW CI is also valid for inference on when the distribution of is discrete, as long as there is some justification for treating the bias as negligible in the sense of condition (3.2).999While most results in the recent literature on local polynomial regression are formulated for settings with a continuous running variable, early contributions such as that of Sacks and Ylvisaker (1978) show that it is not necessary to distinguish between the discrete and the continuous case in order to conduct inference. This justification becomes problematic, however, if the gaps between the support points closest to the threshold are sufficiently wide. This is because, to ensure that is large enough to control the sampling variability of and to ensure that the normality approximation (3.1) is accurate, a researcher may be forced to choose a window width that is “too large”, in the sense that the bias-standard error ratio is likely to be large. When the running variable is discrete, the EHW CI might therefore not be appropriately centered, and thus undercover in finite samples.

3.3. Motivation for clustering by the running variable

To address the problems associated EHW standard errors discussed above, LC proposed using CRV standard errors when the running variable is discrete. This approach has since found widespread use in empirical economics. The rationale provided by LC is as follows. Let denote the specification bias of the (local) polynomial approximation to the true CEF, and write . Then, for observations inside the estimation window, we can write

| (3.3) |

where is the deviation of the observed outcome from its conditional expectation, and the value of is identical for all units that share the same realization of the running variable. LC then treat as a random effect, rather than a specification error that is non-random conditional on the running variable. That is, they consider a model that has the same form as (3.3), but where , with a mean-zero random vector with elements that are mutually independent and independent of . Under this assumption, equation (3.3) is a correctly specified regression model in which the error term exhibits within-group correlation at the level of the running variable. That is, for , we have that and . LC then argue that due to this group structure, the variance estimator is appropriate.

This rationale is unusual in several respects. First, it is not compatible with the standard assumption that the data are generated by i.i.d. sampling from a fixed population, with a non-random CEF. Under i.i.d. sampling, is not random conditional on , as the function depends only on the population distribution of observable quantities, and does not change across repeated samples. Assuming that is random implies that the CEF changes across repeated samples, since in each sample one observes a different realization of , and thus different deviations of the CEF from its “average value” .

Second, the randomness of the CEF in the LC model implies that the ATE , which is a function of the CEF, is also random. This makes it unclear what the population object is that the RDD identifies, and the CRV CIs provide inference for. One might try to resolve this problem by defining the parameter of interest to be , the magnitude of the discontinuity of the “average” CEF , where the average is taken over the specification errors. But it is unclear in what sense measures a causal effect, as it does not correspond to an ATE for any particular set of units. Furthermore, proceeding like this amounts to assuming that the chosen polynomial specification is correct after all, which seems to contradict the original purpose of clustering by running variable. Alternatively, one could consider inference on the conditional expectation of the (random) ATE given specification errors, . But once we condition on , the data are i.i.d., the LC model becomes equivalent to the standard setup described in Section 3.1, and all the concerns outlined in Section 3.2 apply.

Third, the LC model effectively rules out smooth CEFs. To see this, note that if the CEF were smooth, then units with similar values of the running variable should also have a similar value of the specification error . In the LC model, the random specification errors are independent for any two values of the running variable, even if the values are very similar. Since in most empirical applications, one expects a smooth relationship between the outcome and the running variable, this is an important downside.

Due to these issues, we argue that the LC model should not be viewed as a literal description of the DGP, but rather as a heuristic device to motivate using CRV standard errors. Their performance should be evaluated under the standard framework outlined in Section 3.1, in which the data are generated by i.i.d. sampling from a fixed population distribution.

4. Theoretical properties of CRV confidence intervals

In this section, we study the properties of under the standard setup introduced in Section 3.1, which then directly leads to statements about the coverage properties of the corresponding CIs. The results reported here summarize the main insights from a more formal analysis in Appendix A. To capture the notion that is “close” to a polynomial specification, our asymptotic analysis uses a sequence of data generating processes (DGPs) under which the CEF changes with the sample size, so that it lies within an neighborhood of the polynomial specification uniformly over the estimation window . Changing the DGP with the sample size is a widely used technical device that helps preserve important finite-sample issues in the asymptotic approximation. In our setting, it allows us capture the fact that it may be unclear in finite samples whether the chosen polynomial specification is correct.101010If the CEF , and thus the magnitude of the specification errors , did not change with the sample size, the asymptotic coverage probability of CRV CIs would be equal to either zero or one, depending on the magnitude of the bias . This would clearly not be a very useful approximation of the finite-sample properties of these CIs.

This setup implies that there are constants and such that, as the sample size increases,

for each support point in the estimation window. Lemma 1 in Appendix A then shows that in large samples, is normally distributed with mean zero and asymptotic variance

where denotes the conditional variance of the outcome given the running variable, and is the probability that the value of the running variable for a unit within the estimation window equals , the th support point. The asymptotic variance is a weighted sum of the conditional variances of the outcome given the running variable, with the weights reflecting the influence of observations with on the estimate . It follows that in large samples, is normally distributed with asymptotic bias and variance . Lemma 1 also shows that the EHW variance estimator is consistent for .

As discussed in Section 3.1, CIs based on EHW standard errors generally undercover , as they are not correctly centered unless . A CI based on the CRV standard error is centered at the same point estimate. In order for a CRV CI to have correct coverage, the CRV standard error thus has to be larger than the EHW standard error by a suitable amount, at least on average. In the remainder of this section, we show that this is not the case, and that CIs based on CRV standard errors (i) undercover the ATE under correct specification and (ii) can either over- or undercover the ATE under misspecification by essentially arbitrary amounts. The asymptotic behavior of differs depending on whether the number of support points inside the estimation window is treated as fixed or as increasing with the sample size. We examine each of these two cases in turn now.

4.1. Fixed number of support points

In Theorem 1 in Appendix A, we study the properties of when is held fixed as the sample size increases. This should deliver useful approximations for settings with a small to moderate number of support points within the estimation window . We show that in this case does not converge to a constant, but to a non-degenerate limit denoted by . This means that it remains stochastic even in large samples.111111In general, clustered standard errors converge to a non-degenerate limiting distribution unless the number of clusters increases with the sample size at a suitable rate (see for example, Hansen, 2007). It follows from Theorem 1 that we can decompose the expected difference between and as

| (4.1) |

The first term on the right-hand side of (4.1) is positive, and its magnitude depends on the degree of misspecification. The second term does not depend on the degree of misspecification and vanishes if we replace the estimated regression residuals in the CRV formula with the true error . Its sign is difficult to determine in general. It is therefore helpful to consider the case in which the conditional variance of the outcomes is homoskedastic, , so that . The expected difference between and , relative to , can then be written as,

| (4.2) |

This decomposition is key to understanding the properties of in settings with a few support points . Since the EHW variance estimator is consistent for , the notation introduced in (4.2) implies that average magnitude of is about times that of . In order for the CRV CI to have correct coverage, the terms have to be positive, with a magnitude that suitably reflects the degree of misspecification. That is generally not the case.

First, the term is indeed positive and increasing in the “average” misspecification, as measured by the average squared local specification error, , weighted by the cluster size and . Heuristically, this term arises because the CRV variance estimator treats the specification errors as random effects, and tries to account for their “variance”. The magnitude of depends on the magnitude of the average misspecification, relative to . Second, the term is negative under homoskedasticity because both the weights and are positive. We thus also expect the term to be negative for small and moderate levels of heteroskedasticity. Third, the magnitude of depends only on the marginal distribution of the running variable, and not on . It is therefore the dominant term in the decomposition (4.2) if the variance of the error terms is large. Fourth, the term is increasing in the polynomial order . To see this, observe that . The term can thus be written as a weighted average of terms whose unweighted average is equal to . Heuristically, this means that the expected difference between and should be increasing with the order of the polynomial. For example, it is generally larger for local quadratic regression () than for local linear regression (). Fifth, the term is analogous to the downward bias of cluster-robust variance estimators in settings with a few clusters (e.g. Cameron and Miller, 2014). While the existence of such biases is well-known in principle, in the current setting the distortion can be substantial even for moderate values of , as shown by our simulations in Section 2 and the supplemental material.

In summary, our theoretical results show if the degree of misspecification relative to the variance of the residuals and the number of clusters are both small to moderate, the CRV standard error is on average smaller than the EHW standard error. Clustering the standard error by the running variable will then amplify, rather than solve, the problems for inference caused by specification bias. This problem is particularly severe under correct specification. These results are exactly in line with the evidence presented in Section 2.

4.2. Increasing number of support points

In Theorem 2 in Appendix A, we study the properties of when increases with the sample size. This should deliver a useful approximation when there are many support points within the estimation window . We show that if as , the variance of vanishes, and we obtain that

The right-hand side coincides with the first term in Equation (4.1); the second term vanishes. This means that if the number of support points is large, the CRV standard error indeed tends to be larger than the EHW standard error, so that clustering by the running variable improves coverage of the corresponding CI.121212A similar result could be obtained for the alternative clustered variance estimators described in Remark 2, which involve a “few clusters” bias correction. Such corrections would shrink the second term in Equation (4.1), and possibly remove it under additional assumptions on the error term.

This fact alone does not imply that CRV confidence intervals have correct coverage for all possible CEFs , but only that there exist a set of CEFs over the estimation window for which correct asymptotic coverage is delivered. While is strictly larger than the set of all th order polynomial functions, this property by itself is not a sufficient argument for justifying the use of CRV CIs. This is because any inference method that leads to CIs wider than those based on EHW standard errors—including undesirable approaches such as simply adding an arbitrary constant to the EHW standard errors—gives an improvement in coverage, and delivers correct inference if the true CEF lies in some set that is strictly larger than the set of all th order polynomial functions.

Whether CRV standard errors provide a meaningful degree of robustness to misspecification depends on whether contains CEFs that are empirically relevant and easy to interpret, so that it is clear in practice what types of restrictions on the researcher is imposing. In this respect, the set has the undesirable feature that it depends on the distribution of the running variable through the weights and the relative cluster sizes . This makes the set difficult to characterize. Furthermore, it implies that two researchers studying the same RDD may arrive to different conclusions if, say, one of them oversampled observations closer to the cutoff (so that the relative cluster size for those observations is larger). Finally, simulation results in the supplemental material show that the set does not include mild departures from a polynomial specification, which is in line with the intuition given in Section 3.3 that the model that motivates the CRV approach implicitly rules out smooth CEFs.

For these reasons, when the number of support points within the estimation window is large, and the researcher is worried that is biased, a better alternative to using CRV CIs is to choose a smaller bandwidth. Alternatively, one can use one of the honest inference procedures that we outline in Section 5, which guarantee proper coverage under easily interpretable restrictions on .

5. Honest Confidence Intervals

If the CEF is allowed to vary arbitrarily between the two support points of the running variable closest to the threshold, no method for inference on the ATE can be both valid and informative: without any restrictions on , even in large samples, any point on the real line would remain a feasible candidate for the value of . To make progress, we need to place constraints on . Formally, we impose the assumption that for some class of functions , and then seek to construct CIs that satisfy

| (5.1) |

where the notation makes explicit that the coverage probability depends on the CEF. Following the terminology in Li (1989), we refer to such CIs as honest with respect to . Honesty with respect to a meaningful and interpretable function class is desirable for a CI, as it guarantees good coverage properties even when facing the “the worst possible” CEF that still satisfies the postulated constraints. In the following subsections, we present honest CIs with respect to two different function classes, which correspond to two different formalizations of the notion that can be well-approximated by a polynomial. The implementation of these CIs is straightforward using the software package RDHonest, available at https://github.com/kolesarm/RDHonest. Proofs are relegated to Appendix B.

5.1. Bound on the second derivative

The first restriction on that we consider is based on bounding the magnitude of its second derivative, which is perhaps the most natural way of imposing smoothness. Specifically, we assume that is twice differentiable on either side of the cutoff, with a second derivative that is bounded in absolute value by a known constant . By choosing a value of close to zero, the researcher can thus formalize the notion that is close to being linear, whereas choosing a large value of allows for less smooth CEFs. For technical reasons we only require to be twice differentiable almost everywhere, which leads to the second-order Hölder class

A local version of this assumption is used in Cheng et al. (1997), whose results formally justify using local polynomial regression to estimate the ATE parameter when the running variable is continuous. Our goal is inference: we seek to construct CIs that are honest with respect to , and based on a local linear estimator as defined in Section 3 (with ). This can be accomplished using results in Armstrong and Kolesár (2016), who study the construction of honest CIs in general nonparametric regression problems.131313The related problem of honest testing for a jump in the density of the running variable at the threshold has been considered in Frandsen (2016), who uses a bound on the second derivative of the density that yields a class of densities similar to .

It turns out that it is easier to construct CIs that are honest conditional on the realizations of the running variable, which is a slightly stronger condition than (5.1). To explain the construction, let denote conditional expectation of the treatment effect estimator, and let denote the nearest-neighbor estimator (Abadie and Imbens, 2006; Abadie et al., 2014) of , the conditional variance of . With discrete running variable, this estimator can be written as

where is the number of observations with , and is an unbiased estimator of the conditional variance , with .141414Abadie et al. (2014) show that the EHW variance estimator overestimates the conditional variance of , while the nearest-neighbor estimator is consistent under mild regularity conditions, in the sense that . One could nevertheless use the EHW standard error for the construction of the CI described in this subsection, but the resulting CI would be conservative. We can decompose the -statistic based on this variance estimator as

Under mild regularity conditions, a Central Limit Theorem ensures that the first term has standard normal distribution in large samples, and the second term is bounded in absolute value by

In Appendix B, we show that the supremum on the right-hand side of the last equation is attained by the function that equals for and for . This yields the explicit expression

| (5.2) |

for the upper bound on the second component of the -statistic. This approach of bounding the second derivative (BSD) thus leads to the following CI:

Proposition 1.

Let denote the quantile of the distribution (the distribution of the absolute value of a normal random variable with mean and variance 1). Then, under regularity conditions stated in Appendix B, the CI

| (5.3) |

is honest with respect to .

This CI has several attractive features. First, since the CI is valid conditional on the realizations of the running variable, it is not necessary to distinguish between the cases of a discrete and a continuous distribution of the running variable. The CI is valid in both cases. Second, takes into account the exact finite-sample bias of the estimator, and is thus valid for any choice of bandwidth. In particular, it does not rely on asymptotic promises about what the bandwidth would have been had the sample size been larger, and remains valid even if the bandwidth is treated as fixed. In contrast, the usual methods of inference in RDDs rely on the assumption that the bandwidth shrinks to zero sufficiently quickly relative to the sample size, which can be hard to evaluate in practice. Third, to achieve the tightest possible CI, one can simply choose a bandwidth that minimizes its length . Since this quantity depends on the outcome data only through the variance estimate , which does not depend on , and which can be shown to be consistent under mild regularity conditions, doing so does not invalidate the honesty of the resulting CI.

An important implementation aspect of is that it requires the researcher to choose a value for . This choice reflects the researcher’s beliefs of what constitutes a plausible level of fluctuation in the function in the particular empirical context. In practice, we recommend reporting results for a range of values in order to illustrate the sensitivity of empirical conclusions to this choice. We find the following heuristic useful to get an intuition for the restrictions implied by particular choices of . Consider the function over some interval . One can show by simple algebra that if , then it differs by at most from a straight line between and . Thus, if a researcher believes, for example, that the CEF differs by no more than from a straight line between the CEF values at the endpoints of any interval of length one in the support of the running variable, a reasonable choice for the bound on the second derivative is .

The use of subject knowledge for choosing is necessary, as it is not possible to use a data-driven method without additional assumptions. In particular, it follows from the results in Low (1997) and Armstrong and Kolesár (2017) that it is not possible to form honest CIs that are tighter than those in Proposition 1 by using data-dependent tuning parameters, and at the same time maintain coverage over the whole function class , for some conservative upper bound . This is related to the fact that it is not possible to upper bound from the data. It is possible, however, to lower bound from the data. In the supplemental material, we construct an estimate and a left-sided CI for this lower bound by adapting the construction from Armstrong and Kolesár (2017) to our setup. We apply this method to the two empirical applications in Section 6 below. The left-sided CI can be used as a specification test to check if the chosen value of is too low to be compatible with the data.

5.2. Bounds on specification errors at the threshold

The second restriction on that we consider formalizes the intuitive notion that the chosen model fits no worse at the cutoff than anywhere else in the support of the running variable within the estimation window . In particular, we assume that the left limit of the specification bias at the threshold, , is no larger than the specification bias at any point in the support of the running variable below the threshold, and similarly for the right limit. This leads to the class

where we assume that the support points are ordered so that the first points are below the cutoff, and is the specification bias. Note that the specification bias depends on the function directly, but also indirectly as the definition of the best polynomial predictor depends on . We refer to this class as the bounded misspecification error (BME) class.

The assumption that contains the true CEF implies that we can bound the bias as follows:

It will be convenient to rewrite the bias bound in a way that avoids using the absolute value operator as

| (5.4) |

where , and the maximum is taken over the set .

As a first step towards constructing a two-sided CI, consider first the slightly simpler problem of constructing an honest right-sided CI for . Suppose we knew that (5.4) was maximized at . Then we could estimate the bias bound by

Here is an estimator of , where is simply the average outcome for the observations whose realization of the running variable is equal to . Since is asymptotically normal, we could then construct a right-sided CI for with confidence level as

where is a consistent estimator of the asymptotic variance of given in Equation (B.1) in Appendix B, and denotes the quantile of the standard normal distribution.

Although we do not know which maximizes (5.4), we do know that the union of CIs,

contains the CI corresponding to that value of that maximizes (5.4). Hence, is a valid CI for . This type of construction is called the union-intersection principle (Casella and Berger, 2002, Chapter 8.2.3), and produces CIs with correct asymptotic coverage. By analogous reasoning, a left-sided CI for can be constructed as

An intersection of the right- and left-sided CIs with a Bonferroni adjustment for their confidence levels then yields a two-sided CI for with confidence level :

Proposition 2.

In contrast to the CI described in the previous subsection, which is valid regardless of whether the running variable is discrete or continuous, is explicitly tailored to settings in which the running variable is discrete. It also requires many observations to be available for every support point within the estimation window. This is needed to justify joint asymptotic normality of the estimators , which is in turn needed to ensure that is asymptotically normal. We do not recommend using the BME CI when the variance of is large relative to the absolute magnitude of , or when there are many support points within the estimation window.

Remark 3.

In the supplemental material, we evaluate the performance of the honest CIs described in this section in the CPS placebo study from Section 2, and also in an additional simulation study. BSD CIs are shown to have excellent coverage properties given an appropriate choice of the constant . BME CIs perform well in designs with a few support points when many observations are available at each of them; they are conservative otherwise.

6. Empirical Applications

In this section, we use data from Oreopoulos (2006) and Lalive (2008) to illustrate the performance of CRV CIs and honest CIs from Section 5 in empirical settings.

6.1. Oreopoulos (2006)

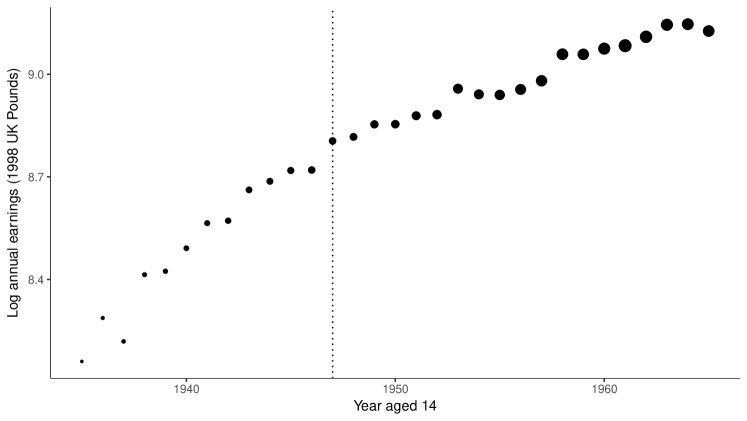

Oreopoulos (2006) studies the effect of a change in the minimum school-leaving age in the United Kingdom from 14 to 15 on schooling attainment and workers’ earnings. The change occurred in 1947 in Great Britain (England, Scotland and Wales), and in 1957 in Northern Ireland. The data are a sample of UK workers who turned 14 between 1935 and 1965, obtained by combining the 1984–2006 waves of the U.K. General Household Survey; see Oreopoulos (2006, 2008) for details.

For simplicity, we focus on the sub-sample of British workers, and restrict attention to the effect of facing a higher minimum school-leaving age on (the natural logarithm of) annual earnings measured in 1998 U.K. Pounds. Oreopoulos uses a sharp RDD to estimate this parameter. The running variable is the year in which the worker turned 14, and the treatment threshold is 1947. The running variable thus has support points, of which are above the threshold, and ones are below. Oreopoulos (2006, 2008) uses the global specification

| (6.1) |

Table LABEL:tab:results4 reports the resulting treatment effect estimate along with CRV and conventional EHW standard errors and CIs for this specification (column (1)). In addition, we consider linear and quadratic specifications fitted separately on each side of the threshold using either the full data set (columns (2)–(3)), or with the estimation window restricted to years around the threshold (columns (4)–(5)), or years (columns (6)–(7)).151515 Our analysis is based on the data distributed together with the online corrigendum Oreopoulos (2008), which fixes some coding errors in the original paper and includes data from additional waves of the U.K. General Household Survey. The results in column (1) therefore differ from those reported Oreopoulos (2006), but they are identical to those given in Oreopoulos (2008).161616We consider different specifications in order to illustrate how these affect the relative magnitude of CRV and EHW standard errors. Whether the estimated effect is significantly different from zero is secondary for our purposes. See e.g. Devereux and Hart (2010) for a discussion of the sensitivity of the point estimates in Oreopoulos (2006) with respect to model specification.

For Oreopoulos’ original specification in column (1), the EHW standard error is twice as large as CRV standard error. The corresponding 95% EHW CI covers zero, whereas the 95% CRV CI does not. For the linear specification using the full data in column (2), the point estimate is negative, and EHW standard errors are slightly smaller than CRV ones. Figure 2 suggests that this may be due to substantial misspecification of a global linear model below the threshold. For the remaining specifications in Table LABEL:tab:results4, all EHW standard errors are larger than the CRV standard errors, by a factor between 1.6 and 28.9. For both the linear and the quadratic specifications, the factor generally increases as the bandwidth (and thus the number of support points used for estimation) decreases. Moreover, the factor is larger for quadratic specifications than it is for the linear specifications. This is in line with the theoretical results presented in Section 4. While our analysis does not imply that EHW CIs have correct coverage in this setting, it does imply that any CI with correct coverage must be at least as wide as the EHW CI. As a result, since none of the EHW CIs in Table LABEL:tab:results4 exclude zero, for the specifications in columns (1), (3) and (5)–(7), LC’s approach leads to incorrect claims about the statistical significance of the estimated treatment effect.

Next, Table LABEL:tab:results4 reports results for a bias-reduced version of the CRV estimator developed by Bell and McCaffrey (2002), which we term CRV2, and results for CIs that combine this bias-reduction with an adjusted critical value, also due to Bell and McCaffrey (2002), which we term CRV-BM.171717We also considered the Imbens and Kolesár (2016) version of the critical value adjustment. The results, not reported here, are virtually identical to the CRV-BM results. See the supplemental material for formal definitions, and Remark 2 in Section 2 for a discussion of the performance of these CIs in simulations. While these adjustments lead to larger CIs relative to CRV, CRV-BM CIs are still smaller than EHW CIs for specifications (1) and (7), and the effect in Oreopoulos’ original specification (1) is still significant. CRV2 standard errors remain smaller than EHW standard errors in all specifications except (2).

Finally, Table LABEL:tab:results4 reports the values of the honest CIs proposed in the Section 5. It shows that the BME procedure leads to CIs that are wider than the EHW CIs. The difference is most pronounced for Oreopoulos’ original specification in column (1) and the specifications that use the full data in columns (2) and (3), due a large number of support points within the estimation window. For the estimation windows and , the BME CI is only slightly wider than the EHW CIs.

We also report BSD CIs for . We use the heuristic described in Section 5.1 that fixing a value of corresponds to assuming that the true CEF does not deviate from a straight line by more than over a one-year interval. Given that a typical increase in log earnings per extra year in age is about 0.02, we consider and to be reasonable choices, with the other values corresponding to a very optimistic and a very conservative view, respectively. We check these choices by estimating the lower bound for using the method described in the supplemental material, which yields a point estimate equal to , with a 95% CI given by . Except for , for which the implied maximum bias is as large as (reflecting that this choice of is very conservative), the resulting CIs, reported in columns (8)–(11) of Table LABEL:tab:results4, are reasonably tight, and in line with the results based on EHW and BME CIs.

6.2. Lalive (2008)

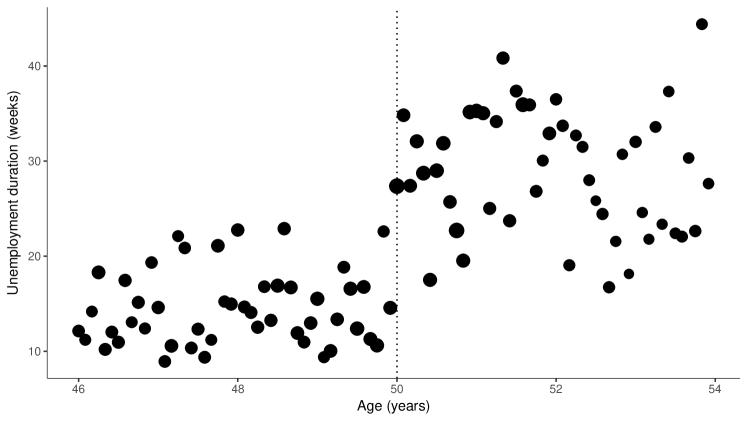

Lalive (2008) exploits a sharp discontinuity in Austria’s Regional Extended Benefit Program that was in place in 1989–1991 to study how changes in unemployment benefits affect the duration of unemployment. To mitigate labor market problems in the steel sector that was undergoing restructuring, the program extended the potential duration of unemployment benefits from 30 weeks to 209 weeks for job seekers aged 50 or older, living in one of 28 labor market districts of Austria with high steel industry concentrations. The sharp age and location cutoffs in eligibility for this program allow Lalive (2008) to exploit two separate regression discontinuity designs.

We focus here on the design with age in months as the running variable, with 50 as the treatment threshold, and focus on the effect on unemployment duration for men aged 46–54, previously employed in non-steel sectors, living in the treated districts.181818 As discussed in Lalive (2008), there may be a concern about the validity of this design if firms wait to lay off employees until they just satisfy the age requirement. If such manipulation was happening in the data, it may call into question the causal interpretation of the RD estimand. This concern about validity is secondary here, as our focus is on whether CRV CIs provide adequate coverage of the RDD estimand irrespective of whether it has causal interpretation. See Gerard et al. (2016) for bounds on causal parameters in RDDs with manipulation. Because the data used in Lalive (2008) record age only up to a precision of one month, there are support points, 48 above, and 48 below the cutoff. Figure 3 plots the data. Lalive (2008) uses the global polynomial regression

| (6.2) |

with or , as well as a local linear regression with bandwidth and the Epanechnikov kernel, to estimate the parameter of interest. Lalive also reports CRV standard errors. Table LABEL:tab:lalive reproduces these estimates and standard errors, and also reports conventional EHW standard errors for these specifications (columns (1)–(4)), except in column (4) we use the uniform rather than the Epanechnikov kernel for simplicity. Columns (5)–(7) report estimates for local linear and local cubic regressions with bandwidth and . Like in Section 6.1, we also report results for CRV-BM, and CRV2 that correspond to the bias-reduction modification of the CRV estimator developed by Bell and McCaffrey (2002), with and without an additional critical value adjustment.

The point estimate is relatively insensitive to changes of the specification, indicating that men stay unemployed for about 13 additional weeks in response to receiving up to 179 extra weeks of unemployment benefits. For all specifications, the EHW standard errors are bigger than CRV standard errors, by a factor of 1.1 to 2.0 that is increasing in the order of the polynomial and decreasing in the bandwidth. This is in spite of the moderate number of support points on either side of the threshold. Although the results remain significant, the CRV standard errors overestimate the precision of the results. The CRV2 adjustment does not change this conclusion. Similarly, the CRV-BM CIs are shorter than EHW CIs in all specifications considered except (5) and (7).

Table LABEL:tab:lalive also reports honest CIs proposed in Section 5. BME CIs turn out to be very wide for all specifications, and are essentially uninformative. As discussed after Proposition 2, this is because there is substantial uncertainty here about the magnitudes of the specification errors (only few observations are available for each support points, and the number of support points is relatively large). This is an instance of a setup where BME CIs are very conservative. For BSD CIs, using the heuristic from Section 5.1 that the CEF should not deviate by more than over a one-year interval, we set and as reasonable choices. We also consider and as a robustness check. The specification test described in the supplemental material cannot reject linear CEF (). Again, this is due to a relatively small number of observations available for each support point. The resulting CIs for these choices of , reported in columns (8)-(11) of Table LABEL:tab:lalive, are much tighter than those based on the BME method, and quite close to the EHW CIs based local linear regression and bandwidth .

7. Conclusions

RDDs with a discrete running variable are ubiquitous in empirical practice. In this paper, we show that the commonly used confidence intervals based on standard errors that are clustered by the running variable have poor coverage properties. We therefore recommend that they should not be used in practice, and that one should instead proceed as follows. First, there is no need to distinguish sharply between the case of a discrete and a continuous running variable. In particular, if the discrete running variable has rich support, one can make the bandwidth smaller to reduce the bias of the treatment effect estimate, and use EHW standard errors for inference. Discreteness of the running variable only causes problems if the number of support points close to the cutoff is so small that using a smaller bandwidth to make the bias of the estimator negligible relative to its standard deviation is not feasible. Second, if one wants to deal with bias issues explicitly, one can use one of the two honest CIs described in this paper. The BSD approach works whether the running variable is discrete or continuous, whereas the BME approach is tailored to settings in which the running variable only takes on a few distinct values.

Appendix A Proofs of results in Section 4

The claims in Section 4 follow directly from general results on the properties of that are given in the following subsection. The proofs of these results are given in turn in Sections A.2–A.4. To state these results, we use the notation to denote a diagonal matrix with diagonal elements given by , and .

A.1. Properties of under General Conditions

In this subsection, we consider a setup that is slightly more general than that in Section 3, in that it also allows the bandwidth to change with the sample size. For convenience, the following assumption summarizes this more general setup.

Assumption 1 (Model).

For each , the data are i.i.d., distributed according to a law . Under , the marginal distribution of is discrete with support points denoted . Let denote the CEF under . Let , and let denote its conditional variance. Let denote a non-random bandwidth sequence, and let denote the indices for which , with and denoting the number of elements in above and below zero. Let , , and . For a fixed integer , define

, and . Let and . Let , and denote its first element my . Let , and denote its first element by . Define , and . Define , where .

Note that the setup allows various quantities that depend on and to change with , such as the number of support points , their locations , the conditional expectation function , or the specification errors .

Assumption 2 (Regularity conditions).

(i) , for some that does not depend on , where , , and the limit exists. (ii) ; and the limit exists.

The assumption ensures that that bandwidth shrinks to zero slowly enough so that the number of effective observations increases to infinity, and that the number of effective support points is large enough so that the parameter and the asymptotic variance of remain well-defined with well-defined limits. We normalize and by the inverse of since if , their elements converge at different rates.

Our first result is an asymptotic approximation in which and are fixed as the sample size increases. Let be a collection of random vectors such that , with

Note that if , then and , and that the limiting distribution of the statistic coincides with the distribution of . Finally, define

With this notation, we obtain the following generic result.

Theorem 1.

Our second result is an asymptotic approximation in which the number of support points of the running variable (or, equivalently, the number of “clusters”) that are less than away from the threshold increases with the sample size.

The assumption that ensures that each “cluster” comprises a vanishing fraction of the effective sample size.

A.2. Auxiliary Lemma

Here we state an intermediate result that is used in the proofs of Theorem 1 and 2 below, and that shows that is consistent for the asymptotic variance of .

Lemma 1.

Proof.

We have . Therefore, by Markov’s inequality, implies , which proves (A.1). Secondly, since elements of are bounded by , the second moment of any element of is bounded by , which converges to zero by assumption. Thus, by Markov’s inequality, . Combining this result with (A.1) and the fact that is bounded then yields (A.2).

Next note that since , , and that by the central limit theorem, . Therefore,

as claimed. Next, we prove (A.4). Let . Then by (A.1), the cluster-robust variance estimator can be written as

The expression in parentheses can be decomposed as

which yields the result.

It remains to prove consistency of . To this end, using (A.1), decompose

where , , and . Since elements of are bounded by , variance of is bounded by , so that by Markov’s inequality, . Similarly, all elements of are bounded, by (A.1)–(A.3). Finally, by Cauchy-Schwarz inequality. Thus,

| (A.5) |

and consistency of then follows by combining this result with (A.2). ∎

A.3. Proof of Theorem 1

Let , and define , , and as in the statement of Lemma 1. By Lemma 1, , and by Markov’s inequality and Equation (A.1), for . Combining these results with Equation (A.4), it follows that the cluster-robust variance estimator satisfies

To prove the theorem, it therefore suffices to show that

| (A.6) |

This follows from Slutsky’s lemma and the fact that by the central limit theorem,

| (A.7) |

A.4. Proof of Theorem 2

Throughout the proof, write to denote for some constant that does not depend on . By Equation (A.4) in Lemma 1, we can write the cluster-robust estimator as , with

where , and and are defined in the statement of the Lemma.

We first show that . Since by Lemma 1, it suffices to show that

To this end, note that since elements of are bounded by , for any , by Cauchy-Schwarz inequality, , where denotes the Euclidean norm of a vector . By Lemma 1, and so that

Now, since , and ,

Therefore, by Markov’s inequality, , so that as claimed.

Next, consider . Let . We have

where

We have

and

Next, , and

The expectations for the remaining terms satisfy , and

The variances of are all of smaller order than this expectation:

and

It therefore follows that

Finally, the cross-term is by Cauchy-Schwarz inequality, so that , which yields the result.

Appendix B Proofs of results in Section 5

For the proof of Propositions 1, we suppose that Assumptions 1 and 2 (i) hold. We denote the conditional variance of by , where , and . We assume that is bounded and bounded away from zero. To ensure that , as defined in Section 5.1, is consistent, we assume that as , , so that in large samples there are at least two observations available for each support point. We put if . For simplicity, we also assume that ; otherwise will diverge with the sample size.

For the proof of Proposition 2, we suppose that Assumptions 1 and 2 hold. For simplicity, we also assume that as , and are fixed, and that is bounded away from zero. We also assume that the asymptotic variance of is bounded away from zero for some .

B.1. Proof of Proposition 1

We first derive the expression for , following the arguments in Theorem B.1 in Armstrong and Kolesár (2016). Note first that the local linear estimator can be written as a linear estimator, , with the weights given in (5.2). Put , and , and put and , with the convention that . Since and , the conditional bias has the form

By assumption, the first derivatives of the functions and are Lipschitz, and hence absolutely continuous, so that, by the Fundamental Theorem of Calculus and Fubini’s theorem, we can write, for , , and for , , where . Since the weights satisfy , and , it follows that

where the second line uses Fubini’s theorem to change the order of summation and integration. Next, note that is negative for all , because , for , and is monotone on with . Similarly, is positive for all . Therefore, the expression in the preceding display is maximized by setting , and minimized by setting . Plugging these expressions into the preceding display then gives , with , which yields (5.2).

Let denote a term that’s asymptotically negligible, uniformly over . To complete the proof, we need to show that (i) , (ii) , (iii) , and (iv) , where and are non-random, and by an argument analogous to that in the preceding paragraph, satisfy . It then follows from uniform continuity of that

where , from which honesty follows.

To show (i), note that by (A.1), (A.2), and the law of large numbers, it suffices to show that . Note that , where (so that ). This yields the decomposition

Since elements of are bounded by , the first term on the right-hand side of the preceding display is of the order by the law of large numbers. Conditional on , the second term has mean zero and variance bounded by , which implies that unconditionally, it also has mean zero, and variance that converges to zero. Therefore, by Markov’s inequality, it is also of the order . Finally, by assumption of the proposition, the probability that the third term is zero converges to one. Thus, as required.

B.2. Proof of Proposition 2

It suffices to show that for each , the left- and right-sided CIs and are asymptotically valid CIs for , for any sequence of probability laws satisfying the assumptions stated at the beginning of Appendix B, and satisfying . Honesty will then follow by the union-intersection principle and the definition of .

Note first that by the central limit theorem and the delta method,

Applying the delta method again, along with Lemma 1, yields

where the variance matrix is given by

and is a matrix with element equal to .

Fix , and let denote a vector with the th element equal to , th element equal to , the last element equal to one, and the remaining elements equal to zero. It follows that is asymptotically normal with variance . To construct the left- and right-sided CIs, we use the variance estimator

| (B.1) |

where is a plug-in estimator of that replaces by , by , by , and by (given in Section 5.1). Since by standard arguments , and , it follows from (A.2) and (A.5) that , which, together with the asymptotic normality of , implies asymptotic validity of and , as required.

Appendix C Additional Figures

This appendix shows the fit of the specifications considered in Section 2. Specifically, Figure LABEL:fig_data1a shows the fit of a linear specification () for the four values of the bandwidth considered; Figure LABEL:fig_data1b shows the analogous results for a quadratic fit (). In each case, the value of the parameter is equal to height of the jump in the fitted line at the 40-year cutoff.

References

- Abadie and Imbens (2006) Abadie, A. and G. W. Imbens (2006): “Large Sample Properties of Matching Estimators for Average Treatment Effects,” Econometrica, 74, 235–267.

- Abadie et al. (2014) Abadie, A., G. W. Imbens, and F. Zheng (2014): “Inference for Misspecified Models with Fixed Regressors,” Journal of the American Statistical Association, 109, 1601–1614.

- Armstrong and Kolesár (2016) Armstrong, T. B. and M. Kolesár (2016): “Simple and honest confidence intervals in nonparametric regression,” ArXiv:1606.01200.

- Armstrong and Kolesár (2017) ——— (2017): “Optimal inference in a class of regression models,” ArXiv:1511.06028.

- Bell and McCaffrey (2002) Bell, R. M. and D. F. McCaffrey (2002): “Bias Reduction in Standard Errors for Linear Regression with Multi-Stage Smples,” Survey Methodology, 28, 169–181.

- Calonico et al. (2014) Calonico, S., M. D. Cattaneo, and R. Titiunik (2014): “Robust Nonparametric Confidence Intervals for Regression-Discontinuity Designs,” Econometrica, 82, 2295–2326.

- Cameron and Miller (2014) Cameron, C. A. and D. L. Miller (2014): “A Practitioner’s Guide to Cluster-Robust Inference,” Journal of Human Resources, 50, 317–372.