Bayesian estimation of incompletely observed diffusions

Abstract

. We present a general framework for Bayesian estimation of incompletely observed multivariate diffusion processes. Observations are assumed to be discrete in time, noisy and incomplete. We assume the drift and diffusion coefficient depend on an unknown parameter. A data-augmentation algorithm for drawing from the posterior distribution is presented which is based on simulating diffusion bridges conditional on a noisy incomplete observation at an intermediate time. The dynamics of such filtered bridges are derived and it is shown how these can be simulated using a generalised version of the guided proposals introduced in Schauer et al. (2016).

Keywords: data augmentation; enlargement of filtration; guided proposal; filtered bridge; smoothing diffusion processes; innovation scheme; Metropolis-Hastings; multidimensional diffusion bridge; partially observed diffusion

keywords:

[class=MSC]journalname

1 Introduction

We consider Bayesian estimation for incompletely, discretely observed multivariate diffusion processes. Suppose is a multidimensional diffusion with time dependent drift and time dependent dispersion coefficient governed by the stochastic differential equation (SDE)

| (1.1) |

The process is a vector valued process in consisting of independent Brownian motions. Denote observation times by . Denote and assume observations

where is a -matrix. The random variable is assumed to have a continuous density , which may for example be the -density. Further, we assume is a sequence of independent random variables, independent of the diffusion process . This setup includes full observations in case (the identity matrix of dimension ). Further, if we have observations that are in a plane of dimension strictly smaller than , with error superimposed. Suppose and depend on an unknown finite dimensional parameter . Based on the information set

we wish to infer within the Bayesian paradigm.

From an applied point of view, there are many motivating examples that correspond to the outlined problem. As a first example, in chemical kinetics the evolution of concentrations of particles of different species is modeled by stochastic differential equations. In case it is only possible to measure the cumulative concentration of two species but not the single concentrations, we have incomplete observations with . A second example is given by stochastic volatility models used in finance, where the volatility process is unobserved. If the price of an asset is the first component of the model and the latent volatility the second component, then we have incomplete observations with . Note that in our setup the way in which the observations are incomplete need not be the same at all observation times (that is, may differ from for ). Hence, missing data fit naturally within our framework.

1.1 Related work

Even in case of full discrete time observations the described problem is hard as no closed form expression for the likelihood can be written down, aside from some very specific easy cases. To work around this problem, data-augmentation has been proposed where the latent data are the missing diffusion bridges that connect the discrete time observations. See for instance Roberts and Stramer (2001), Chib et al. (2004), Beskos et al. (2006), Beskos et al. (2008), Golightly and Wilkinson (2008), Golightly and Wilkinson (2010), Fuchs (2013), Papaspiliopoulos et al. (2013), and Van der Meulen and Schauer (2016). The resulting algorithm has been shown to be successful provided one is able to draw diffusion bridges between two adjacent discrete time observations efficiently. A major simplification that the fully observed case brings is that diffusion bridges can be simulated independently. The latter property is lost in case of incomplete observations: the latent process between times and depends on all observations . This dependence may seem to imply that it is infeasible to draw such diffusion bridges. Indeed this is hard, but is in fact not necessary as we can draw in blocks. This idea has appeared in several papers. Both Golightly and Wilkinson (2008) and Fuchs (2013) consider the case where with possibly several rows removed (which corresponds to not observing corresponding components of the diffusion). For set . Golightly and Wilkinson (2008) discretise the SDE and construct an algorithm according to the steps:

-

1.

Initialise and .

-

2.

For , sample filtered diffusion bridges , conditional on , , and . Sample conditional on , and . Sample conditional on , and .

-

3.

Sample conditional on .

In fact, the second step is carried out slightly differently using the “innovation scheme”, as we will discuss shortly (moreover, updating the first and last segment requires special care). Fuchs (2013) (section 7.2) proposes a similar algorithm using some variations on carrying out the second step. In both references, bridges are proposed based on the Euler discretisation of the SDE for with and accepted using the Metropolis-Hastings rule. In case of either strong nonlinearities in the drift or low sampling frequency this can lead to very low acceptance probabilities.

A diffusion bridge is an infinite-dimensional random variable. The approach taken in Golightly and Wilkinson (2008) and Fuchs (2013) is to approximate this stochastic process by a finite-dimensional vector and next carry out simulation. Papaspiliopoulos and Roberts (2012) call this the projection-simulation strategy and advocate the simulation-projection strategy where an appropriate Monte-Carlo scheme is designed that operates on the infinitely-dimensional space of diffusion bridges. For practical purposes it needs to be discretised but the discretisation error can be eliminated by letting the mesh-width tend to zero. This implies that the algorithm is valid when taking this limit. We refer to Papaspiliopoulos and Roberts (2012) to a discussion on additional advantages of the simulation-projection strategy, which we will employ in this paper.

Within the simulation-projection setup a particular version of the problem in this article has been treated in the unpublished Ph.D. thesis Jensen (2014) (chapter 6). Here, it is assumed that certain components of the diffusion are unobserved, whereas the remaining components are observed discretely without error. A major limitation of this work is that it is essential that the diffusion can be transformed to unit diffusion coefficient.

Besides potentially difficult simulation of diffusion bridges, there is another well known problem related to MCMC-algorithm for the problem considered. In case there are unknown parameters in the diffusion coefficient , any MCMC-scheme that includes the latent diffusion bridges leads to a scheme that is reducible. The reason for this is that a continuous sample path fixes the diffusion coefficient by means of its quadratic variation process. This phenomenon was first discussed in Roberts and Stramer (2001) and a solution to it was proposed in both Chib et al. (2004) and Golightly and Wilkinson (2008) within the projection-simulation setup. The resulting algorithm is referred to as the innovation scheme, as the innovations of the bridges are used as auxiliary data, instead of the discretised bridges themselves. A slightly more general solution was recently put forward in Van der Meulen and Schauer (2016) using the simulation-projection setup.

1.2 Approach

Assume without loss of generality that is even. The basic idea of our algorithm consists of iterating steps of the following algorithm:

-

1.

Initialise and .

-

2.

For , sample filtered diffusion bridges , conditional on , , and .

-

3.

Sample conditional on .

-

4.

For , sample filtered diffusion bridges , conditional on , , and . Sample conditional on , and . Sample conditional on , and .

-

5.

Sample conditional on .

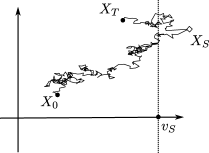

Steps (2) and (4) boil down to sampling independent bridges of the type depicted in figure 1.

Here, we have complete observations and at times and respectively, and an incomplete observation in between at time . We need to simulate a bridge connecting and , while taking care of the incomplete observation at time . For this means that we need to incorporate 2 future conditionings, an incomplete (noisy) observation at time and a complete observation at time . As is Markov and we have a full observation at time this type of conditional process is independent of all observations after time . For we need to sample a diffusion bridge connecting complete observations at times and . The latter case has been researched in many papers over the past 15 years. See for instance Eraker (2001), Elerian et al. (2001), Durham and Gallant (2002), Lin et al. (2010), Beskos et al. (2006), Delyon and Hu (2006), Schauer et al. (2016), Stuart et al. (2004), Bladt and Sørensen (2014) and references therein. However, simulation of a bridge that is conditioned on one incomplete noisy observation ahead and one more complete observation further ahead is clearly more difficult. We call such a bridge a filtered (diffusion) bridge. To the best knowledge of the authors, the problem of simulating such filtered bridges hasn’t been studied in a continuous time setup.

Using the theory of initial enlargement of filtrations, we show in section 2 that the filtered bridge process is a diffusion process itself with dynamics described by the stochastic differential equation

Here, and the function depends both on the unknown transition density and the error density . This SDE is derived by adapting results on partially observed diffusions obtained by Marchand (2012).

As is intractable, direct simulating of filtered bridges from this SDE is infeasible. However, if we replace with the transition density of an auxiliary process , then we can replace with the function , where depends on in exactly the same way as depends on . Exactly this approach was pursued in Schauer et al. (2016) in case of full observations. Naturally we choose the process to have tractable transition densities. We concentrate on linear processes, where satisfies the SDE

Next, we can simulate from the process defined by

instead of . Deviations of from can be corrected by importance sampling or an appropriate acceptance probability in a Metropolis-Hastings algorithm, provided the laws of and (considered as Borel measures on ) are absolutely continuous. Precise conditions for the required absolute continuity are derived in section 3. Comparing the forms of the SDE’s for and we see that an additional guiding term appears in the drift for . For this reason, similar as in Schauer et al. (2016), we call realisations of guided proposals.

In section 5 we show how the innovation scheme of Van der Meulen and Schauer (2016) can be adopted to the incompletely observed case considered here. Compared to Jensen (2014) this scheme removes the restrictive assumption that the diffusion can be transformed to unit diffusion coefficient. As a more subtle important additional bonus, the scheme enables adapting the innovations to the proposals used for simulating bridges (for additional discussion on this topic we refer to Van der Meulen and Schauer (2016)).

A byproduct of our method is that we reconstruct paths from the incompletely observed diffusion process, which is often called smoothing in the literature.

1.3 Outline of this paper

In section 2 we derive the stochastic differential equation for the filtered bridge process corresponding to figure 1. Based on this expression we define guided proposals for filtered bridges. In section 2.2 we derive closed form expressions for the dynamics of the proposal process in case the measurement error is Gaussian. In section 3 we provide sufficient conditions for absolute continuity of the laws of the proposal process and true filtered bridge process. This is complemented with a closed form expression for the Radon-Nikodym derivative. The innovation scheme for estimation is presented in section 5. The proofs of a couple of results are collected in the appendix.

1.4 Notation: derivatives

For we denote by the -matrix with element given by . If , then is the column vector containing all partial derivatives of . In this setting we write the -th element of as and denote so that . Derivatives with respect to time are always written as .

2 Guided proposals for filtered bridges

Consider the filtered probability space . Assume is an -adapted Brownian motion. Let be a strong solution to the SDE given in equation (1.1) on this setup.

Throughout we assume . At times and we assume full observations and respectively. At time we assume to have the incomplete observation (with ). Assume that the -dimensional random vector has density .

We will shortly derive that the process , conditioned on is a diffusion process itself on a filtered probability space with a new filtration. To derive this result, we employ results of Jacod within the volume Jeulin and Yor (1985) on “grossissements de filtration” (see also Jeulin (1980)). Furthermore, we follow the line of reasoning outlined in Marchand (2012), where a similar type of problem is dealt with. The results we use are also nicely summarised in section 2 of Amendinger et al. (1998). Define the enlarged filtration by

The idea is to find the semi-martingale decomposition of the -Wiener process relative to .

Denote the law of the process started in at time by . We assume that admits smooth transition densities such that (with ). Suppose . For and we have

From this we find that for , has density

with respect to Lebesgue measure on . Similarly, for , has density . The function defined in the following definition plays a key role in the remainder.

Definition 2.1.

Suppose . Define

For notational convenience we write instead of , when it is clear from the context what the remaining four arguments are. To avoid abuse of notation, a transition density is always written with all its four arguments. Define

Here denotes differentiation, with precise conventions outlined in section 1.4.

Lemma 2.2.

For , the diffusion conditioned on and satisfies the SDE

| (2.1) |

where is a -Brownian motion.

Proof.

The proof is similar to the proof of Théorème 2.3.4 in Marchand (2012). The first step consists of proving that the process defined by

| (2.2) |

is a -Brownian motion, independent of . For proving this, first define

where is assumed to act on the second argument of . For notational convenience we write instead of . Then

| (2.3) |

By Itō’s lemma

Hence

| (2.4) |

Combining equation (2.3) and (2.4) gives

Théorème 2.1 of Jacod (1985) implies that

is a -martingale. By computing the quadratic variation of it is seen that is a -Wiener process on , independent of .

This results demonstrates that the filtered bridge process is a diffusion process itself with an extra term superposed on the drift of the original diffusion process. The term will be referred to as the pulling term, as it ensures a pull of the diffusion process to have the right distributions at time and . In case there is no measurement error, we have that for

As the dynamics of the bridge involve the unknown transition density of the process, it cannot be used directly for simulation purposes. For that reason, we propose to replace with the transition density of a process for which is tractable to obtain a proposal process .

Definition 2.3.

Guided proposals are defined as solutions to the SDE

| (2.5) |

Here , where

and is a probability density function on , with .

This approach was initiated in Schauer et al. (2016). We will assume throughout that is a linear process:

| (2.6) |

Define , and .

2.1 Notation: diffusions and guided processes

We denote the laws of , and viewed as measures on the space of continuous functions from to equipped with its Borel--algebra by , and respectively. For easy reference, the following table summaries the various processes and corresponding measures around.

| original, unconditioned diffusion process, defined by (1.1) | ||

| corresponding filtered bridge, conditioned on and , defined by (2.1) | ||

| proposal process defined by (2.5) | ||

| linear process defined by (2.6) whose transition densities appear | ||

| in the definition of |

The infinitesimal generator of the diffusion process is denoted by .

2.2 Pulling term induced by a linear process

In this section we derive closed form expressions for and . For the remainder of the this paper we make the following assumption.

Assumption 2.4.

is the density of the distribution.

Note that this is an assumption on which appears in the proposal, and not on which is the density of the error at time .

We start with a recap of a few well known results on linear processes. See for instance Liptser and Shiryaev (2001). Define the fundamental matrix as the matrix satisfying

Set . For a linear process it is known that its transition density satisfies

with

| (2.7) |

and

| (2.8) |

Lemma 2.5.

For

| (2.9) |

and

Here,

| (2.10) |

Proof.

The proof is given in section 6.1. ∎

Corollary 2.6.

Assume and . Define

| (2.11) | ||||

| (2.12) |

Then

| (2.13) |

and

Here,

with any vector such that .

Moreover,

Proof.

Remark 2.7.

Suppose and which corresponds to a full observation at time without error. Then and the second term in (for ) disappears. Furthermore then, . In this way, we recover the result for the full observation case.

Example 2.8.

Suppose is a two-dimensional Brownian Motion, where we only observe the first component at time and both at time . In this case , and . It is easy to see that

By corollary 2.6, it follows that for

Denote the -th component of a vector by . The first component of equals

while the second component equals . From this, we see that the second component is the same as when there would be no conditioning at time .

3 Absolute continuity result

In this section we derive conditions for which and give a closed form expression for the Radon-Nikodym derivative. We have the following assumption on .

Assumption 3.1.

-

1.

The functions and are uniformly bounded, Lipschitz in both arguments and satisfy a linear growth condition on their second argument.

-

2.

Kolmogorov’s backward equation holds:

Here acts on .

-

3.

Uniform ellipticity: there exists an such that for all , and

We have the following assumption on .

Assumption 3.2.

and are continuously differentiable on , is Lipschitz on and there exists a such that for all and all ,

Theorem 3.3.

If , then and are equivalent on with Radon-Nikodym derivative given by

The proof is given in the next subsection.

Remark 3.4.

In case there is no measurement error, we conjecture that absolute continuity will hold provided one takes such that and . Such a choice is possible if only depends on and (and not on unobserved parts of ).

3.1 Proof of theorem 3.3

For proving theorem 3.3, we need a few intermediate results.

Lemma 3.5.

If we define the process by , then is a -martingale.

Proof.

For ,

where we applied the Markov property at the second equality, Fubini at the third equality and the Chapman-Kolmogorov equations at the fourth equality. The argument on follows along the same lines. ∎

Corollary 3.6.

The function satisfies Kolmogorov’s backward equation both for and :

Proof.

The generator of the space-time process is given by . As is a martingale, is space-time harmonic: (Cf. proposition 1.7 of chapter VII in Revuz and Yor (1991)). This is exactly Kolmogorov’s backward equation. ∎

Lemma 3.7.

and similarly for (with appearing in the limit).

Proof.

First note that under our assumptions on and , theorem 21.11 in Kallenberg (2002) implies that the process is Feller. Take . The transition operator is defined by

Hence with

As is Feller, from which the result follows easily. ∎

Lemma 3.8.

Suppose . Then is Lipschitz in its second argument and satisfies a linear growth condition on both and .

Proof.

Proof of theorem 3.3.

The proof follows the line of proof in proposition 1 of Schauer et al. (2016). Consider . By lemma 3.8, is Lipschitz in its second argument and satisfies a linear growth condition on both and . Hence, a unique strong solution of the SDE for exists on .

By Girsanov’s theorem (see e.g. Liptser and Shiryaev (2001)) the laws of the processes and on are equivalent and the corresponding Radon-Nikodym derivative is given by

where is a Brownian motion under and solves

(Here we lightened notation by writing instead of . In the remainder of the proof we follow the same convention and apply it to other processes as well.) Observe that by definition of and we have and , hence

| (3.3) |

Denote the infinitesimal operator of by . By definition of and we have . By Itō’s formula

Applying Itō’s formula in exactly the same manner on with and subsequently taking the limit we get

Combining the preceding two displays with (3.3) we get

| (3.4) |

where

| (3.5) |

If and satisfy Kolmogorov’s backward equation, then the first term between brackets on the right-hand-side of this display equals . This follows from lemma 1 in Schauer et al. (2016). This is naturally the case on and by corollary 3.6 on as well. Substituting this in equation 3.5 we arrive at the expression for as given in the statement of the theorem. By lemma 3.7

Combined with equation (3.4), we obtain

As entirely similar calculation reveals that

Combining the previous two displays gives

From here, the limiting argument is exactly as in Schauer et al. (2016). ∎

4 Special bridges near and

In section 5 we will need filtered processes which take the boundary conditions near and into account (besides the filtered bridge introduced above).

4.1 Near the endpoint

Near we wish to simulate a filtered bridge conditioned on and on . For this purpose, we derive the dynamics of a diffusion process starting in , conditioned . We can use exactly the same techniques as in sections 2 and 2.2 to derive the SDE for the conditioned process. In this case, should be replaced by

In lemma 2.5 we should replace and by

| (4.1) |

and

respectively. Then and are equivalent on with Radon-Nikodym derivative given by

4.2 Near the starting point

Near we wish to simulate a filtered bridge conditioned on and on . Assume has prior distribution . We simulate the filtered bridge in two steps:

-

1.

simulate , conditional on ;

-

2.

simulate a bridge connecting (the realisation of ) and .

Suppose we wish to update to (the proposal). Each proposal will be generated by first drawing conditional on using some kernel followed by sampling a bridge connecting and . Denote the conditional density of conditional on by . The “target density” is proportional to

(note that the intractable term cancels). The acceptance probability then equals , where

When (the distribution of the noise on the observations) is , a tractable expression for is obtained by taking . In that case the vector is jointly Gaussian which implies that

5 Estimation by MCMC using temporary reparametrisation

In this section we present a novel algorithm to draw from the posterior of based on incomplete observations. The basic idea for this algorithm is quite simple and outlined in section 1.2. Unfortunately, this basic scheme collapses in case there are unknown parameters in the diffusion coefficient. This is a well known phenomenon when applying data-augmentation for estimation of discretely observed diffusions. It was first noticed by Roberts and Stramer (2001) and we refer to that paper for a detailed explanation. Golightly and Wilkinson (2008) developed an MCMC algorithm that alternatively updates the parameter and the driving Brownian motion increments of the proposal process. Their derivation was developed entirely by first discretising the process. Van der Meulen and Schauer (2016) showed how this algorithm can be derived in the simulation-projection setup. Quoting from this paper: “The basic idea is that the laws of the bridge proposals can be understood as parametrised push forwards of the law of an underlying random process common to all models with different parameters . This is naturally the case for proposals defined as solutions of stochastic differential equations and the driving Brownian motion can be taken as such underlying random process.”

Here, we propose to derive such an algorithm in case of incomplete observations, which complicates the derivations considerably. We define a Metropolis-Hastings algorithm that uses temporary reparametrisations. Suppose and let be a continuous stochastic process. Let . Let . Define as the solution to the SDE

Assume is invertible. We define the mapping that maps to and define an inverse mapping that maps to . The process is referred to as the innovation process. The main idea of the algorithm below is that when we update in blocks, we temporarily reparametrise to .

In the algorithm below, we assume is even (adaptation to the case where is odd is straightforward). For denote and .

We refer to subsection 4 for simulation of and at the boundaries. We write for the corresponding map from to and similarly for the map from to . In order to conveniently handle boundary cases in the algorithm below we make the convention that the expressions and are to be understood as and respectively. We use a similar convention on the right boundary.

Define

We change the notation on defined in (3.1) slightly to accommodate dependence on :

with the modifications for the boundary cases as before.

We propose the following algorithm.

Algorithm 1.

-

1.

Initialisation. Choose a starting value for and initialise .

-

2.

Update . Independently, for do

-

(a)

Compute .

-

(b)

Sample a Wiener process .

-

(c)

Sample . Compute

Set

-

(a)

-

3.

Update .

-

(a)

Sample .

-

(b)

Sample . Compute

Set

-

(a)

-

4.

Adjust . For compute

-

5.

Update . Independently, for do

-

(a)

Compute .

-

(b)

Sample a Wiener process .

-

(c)

Sample . Compute

Set

-

(a)

-

6.

Update .

-

(a)

Sample .

-

(b)

Sample . Compute

Set

-

(a)

-

7.

Adjust . For compute

-

8.

Repeat steps (2)–(7).

The parameter gets updated twice during a full cycle of the algorithm, but one can choose to either omit step (3) or (6). The proof that and are the correct acceptance probabilities goes along the same lines as in the completely observed case discussed in Van der Meulen and Schauer (2016). As demonstrated in there, in steps 2(a) and 5(a) , one can also propose based on the current value of in the following way

where and is a Wiener process that is independent of . The acceptance probability remains the same under this proposal.

Remark 5.1.

If (the density of the noise at time ) depends on an unknown parameter , then we equip this parameter with a prior density . The parameter can then be updated in a straightforward manner in a separate Metropolis-Hastings step given the full path and the observations.

6 Proofs and Lemmas

6.1 Proof of lemma 2.5

For notational convenience we sometimes drop dependence on . For instance, we may write instead of .

To compute the pulling term at time we need to obtain to density of conditional on . First, we obtain the density of . For this, note that their joint density is given by . Hence,

The exponent equals

with

This implies that the joint distribution of conditional on is normal with covariance matrix and mean vector . Here, (using expressions for the inverse of a partitioned matrix and Woodbury’s formula)

and

Therefore, conditional on ,

| (6.1) |

where denotes the precision matrix, defined in equation (2.10). This implies that

It may appear that does not show up in the formula, but is appears in both and . Next, we need to take the gradient with respect to . This gives

Negating and differentiating once more yields the expression for .

6.2 Proof of corollary 2.6

We have for all and . This implies

The Schur complement of this matrix is

Applying the formula for the inverse of a partitioned matrix gives

Next, we compute

We have

and

The result for now follows upon computing

The expression for follows from

To assess the behaviour of the pulling term in equation (2.13) as , we write

Hence it follows that

and

with denoting a matrix with zeroes.

Acknowledgement. M. S. is supported by the European Research Council under ERC Grant Agreement 320637.

References

- Amendinger et al. (1998) Amendinger, J., Imkeller, P. and Schweizer, M. (1998). Additional logarithmic utility of an insider. Stochastic Process. Appl. 75(2), 263–286.

- Beskos et al. (2006) Beskos, A., Papaspiliopoulos, O., Roberts, G. O. and Fearnhead, P. (2006). Exact and computationally efficient likelihood-based estimation for discretely observed diffusion processes. J. R. Stat. Soc. Ser. B Stat. Methodol. 68(3), 333–382. With discussions and a reply by the authors.

- Beskos et al. (2008) Beskos, A., Roberts, G., Stuart, A. and Voss, J. (2008). MCMC methods for diffusion bridges. Stoch. Dyn. 8(3), 319–350.

- Bladt and Sørensen (2014) Bladt, M. and Sørensen, M. (2014). Simple simulation of diffusion bridges with application to likelihood inference for diffusions. Bernoulli 20(2), 645–675.

- Chib et al. (2004) Chib, S., Pitt, M. K. and Shephard, N. (2004). Likelihood based inference for diffusion driven models. Economics Papers 2004-W20, Economics Group, Nuffield College, University of Oxford.

- Delyon and Hu (2006) Delyon, B. and Hu, Y. (2006). Simulation of conditioned diffusion and application to parameter estimation. Stochastic Processes and their Applications 116(11), 1660 – 1675.

- Durham and Gallant (2002) Durham, G. B. and Gallant, A. R. (2002). Numerical techniques for maximum likelihood estimation of continuous-time diffusion processes. J. Bus. Econom. Statist. 20(3), 297–338. With comments and a reply by the authors.

- Elerian et al. (2001) Elerian, O., Chib, S. and Shephard, N. (2001). Likelihood inference for discretely observed nonlinear diffusions. Econometrica 69(4), 959–993.

- Eraker (2001) Eraker, B. (2001). MCMC analysis of diffusion models with application to finance. J. Bus. Econom. Statist. 19(2), 177–191.

- Fuchs (2013) Fuchs, C. (2013). Inference for diffusion processes. Springer, Heidelberg. With applications in life sciences, With a foreword by Ludwig Fahrmeir.

- Golightly and Wilkinson (2008) Golightly, A. and Wilkinson, D. J. (2008). Bayesian inference for nonlinear multivariate diffusion models observed with error. Comput. Statist. Data Anal. 52(3), 1674–1693.

- Golightly and Wilkinson (2010) Golightly, A. and Wilkinson, D. J. (2010). Learning and Inference in Computational Systems Biology, chapter Markov chain Monte Carlo algorithms for SDE parameter estimation, pp. 253–276. MIT Press.

- Jensen (2014) Jensen, A. C. (2014). Statistical Inference for Partially Observed Diffusion Processes. Ph.d. Thesis University of Copenhagen.

- Jeulin (1980) Jeulin, T. (1980). Semi-martingales et grossissement d’une filtration, volume 833 of Lecture Notes in Mathematics. Springer, Berlin.

- Jeulin and Yor (1985) Jeulin, T. and Yor, M., eds. (1985). Grossissements de filtrations: exemples et applications, volume 1118 of Lecture Notes in Mathematics. Springer-Verlag, Berlin. Papers from the seminar on stochastic calculus held at the Université de Paris VI, Paris, 1982/1983.

- Kallenberg (2002) Kallenberg, O. (2002). Foundations of modern probability. Probability and its Applications (New York). Springer-Verlag, New York, second edition.

- Lin et al. (2010) Lin, M., Chen, R. and Mykland, P. (2010). On generating Monte Carlo samples of continuous diffusion bridges. J. Amer. Statist. Assoc. 105(490), 820–838.

- Liptser and Shiryaev (2001) Liptser, R. S. and Shiryaev, A. N. (2001). Statistics of random processes. I, volume 5 of Applications of Mathematics (New York). Springer-Verlag, Berlin, expanded edition. General theory, Translated from the 1974 Russian original by A. B. Aries, Stochastic Modelling and Applied Probability.

- Marchand (2012) Marchand, J.-L. (2012). Conditionnement de processes markoviens. IRMAR, Ph.d. Thesis Université de Rennes 1.

- Papaspiliopoulos and Roberts (2012) Papaspiliopoulos, O. and Roberts, G. (2012). Importance sampling techniques for estimation of diffusion models. In Statistical Methods for Stochastic Differential Equations, Monographs on Statistics and Applied Probability, p. 311–337. Chapman and Hall.

- Papaspiliopoulos et al. (2013) Papaspiliopoulos, O., Roberts, G. O. and Stramer, O. (2013). Data Augmentation for Diffusions. J. Comput. Graph. Statist. 22(3), 665–688.

- Revuz and Yor (1991) Revuz, D. and Yor, M. (1991). Continuous martingales and Brownian motion, volume 293 of Grundlehren der Mathematischen Wissenschaften [Fundamental Principles of Mathematical Sciences]. Springer-Verlag, Berlin.

- Roberts and Stramer (2001) Roberts, G. O. and Stramer, O. (2001). On inference for partially observed nonlinear diffusion models using the Metropolis-Hastings algorithm. Biometrika 88(3), 603–621.

- Schauer et al. (2016) Schauer, M., Van der Meulen, F. H. and Van Zanten, J. H. (2016). Guided proposals for simulating multi-dimensional diffusion bridges. To appear in Bernoulli .

- Stuart et al. (2004) Stuart, A. M., Voss, J. and Wiberg, P. (2004). Fast communication conditional path sampling of SDEs and the Langevin MCMC method. Commun. Math. Sci. 2(4), 685–697.

- Van der Meulen and Schauer (2016) Van der Meulen, F. H. and Schauer, M. (2016). Bayesian estimation for diffusions using guided proposals. ArXiv e-prints arXiv:1406.4704 .