Prediction performance after learning

in Gaussian process regression

Abstract

This paper considers the quantification of the prediction performance in Gaussian process regression. The standard approach is to base the prediction error bars on the theoretical predictive variance, which is a lower bound on the mean square-error (MSE). This approach, however, does not take into account that the statistical model is learned from the data. We show that this omission leads to a systematic underestimation of the prediction errors. Starting from a generalization of the Cramér-Rao bound, we derive a more accurate MSE bound which provides a measure of uncertainty for prediction of Gaussian processes. The improved bound is easily computed and we illustrate it using synthetic and real data examples.

Please cite this version:

Johan Wågberg, Dave Zachariah, Thomas B. Schön and Petre Stoica. Prediction performance after learning in Gaussian process regression. In Proceedings of the 20th International Conference on Artificial Intelligence and Statistics (AISTATS), Fort Lauderdale, FL, USA, April, 2017.

1 Introduction

In this paper we consider the problem of learning a function from a dataset where

| (1) |

The aim is to predict at a test point . In machine learning, spatial statistics and statistical signal processing, it is common to model as a Gaussian process (GP) and as an uncorrelated zero-mean Gaussian noise [17, 2, 9, 10]. This probabilistic framework shares several properties with kernel and spline-based methods [14, 19, 12]. One of the strengths of the GP framework is that both a predictor and its error bars are readily obtained using the mean and variance of . This quantification of the prediction uncertainty is valuable in itself but also in applications that involve decision making, e.g. in the exploration-exploitation phase of active learning and control [8, 5, 4]. Another recent example is Bayesian optimization techniques using Gaussian processes [15].

In general, however, the model for is not fully specified but contains unknown hyperparameters, denoted , that can be learned from data. Plugging an estimate into the predictor will therefore inflate its errors due to the uncertainty of the learned model itself. In this case the standard error bounds will systematically underestimate the actual prediction errors. One possibility is to assign a prior distribution to and marginalize out the parameters from the posterior distribution of [21]. While conceptually straight-forward, this approach is challenging to implement in general as it requires the user to choose a reasonable prior distribution and computationally demanding numerical integration techniques.

Our contribution in this paper is the derivation of more accurate error bound for prediction after learning, using a generalization of the Cramér-Rao Bound (CRB) [11, 3]. The bound is computationally inexpensive to implement using standard tools in the GP framework. We illustrate the bound using both synthetic and real data.

2 Problem formulation and related work

We consider a general input space . To establish the notation ahead we write the Gaussian process and the vector of hyperparameters as

| (2) |

where denotes the variance of in (1). The vectors and parameterize the mean and covariance functions, and , respectively. For an arbitrary test point we write and consider the mean-square error

where the expectation is taken with respect to and the data . When is given, the optimal predictor is

| (3) |

where , and . In addition, and . Eq. (3) is equal to the mean of the predictive distribution and is a function of both and [12]. The minimum MSE then follows directly from the predictive variance, denoted . Here, however, we provide an alternative derivation based on a generalization of the CRB [20, 7, 22]. This tool will also enable us to tackle the general problem considered later on.

Result 1.

When is known,

| (4) |

where .

Proof.

The Bayesian Cramér-Rao Bound (BCRB) is given by

where is the Bayesian information of [20]. Using the chain rule, , we obtain

| (5) | ||||

under the assumptions made. Then the Bayesian information equals

| (6) |

∎

Remarks: The lower bound (4) on the MSE, and the corresponding minimum error bars for a predictor , reflects the uncertainty of alone. The bound is attained when coincides with (3) which depends on . In general, however, is unknown and typically learned from the data. Then the bound (4) will not reflect the additional errors of arising from the unknown model parameters . The effect is a systematic underestimation of the prediction errors. For illustrative purposes we present an example with one-dimensional inputs, see Example 1 below.

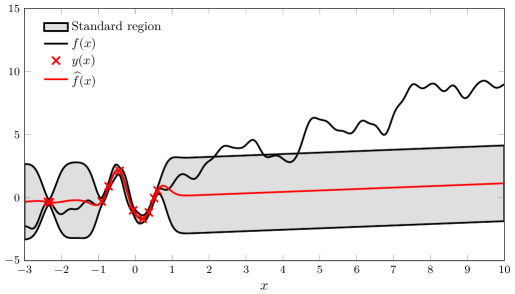

Example 1.

Consider the Gaussian process (1) for with a linear mean function and a squared-exponential covariance function. That is, and in (2). The process is sampled at different points and the unknown hyperparameters are learned from the dataset by maximizing the marginal likelihood, , where the vector contains the latent function values in the data.

Figure 1 illustrates a realization of along with the predicted values . The error bars are obtained from (4) which was derived under the assumption of being known. The bars severely underestimate the uncertainty of the predictor since they remain nearly constant along the input space and do not contain the example realization of .

A tighter MSE bound than (4) has been derived for the special case in which is assumed to be known and the mean function is linear in the parameters, i.e., where is a given basis function [17]. In the statistics literature, there have been attempts to extend to the analysis to models in which the covariance parameters are unknown. The results do, however, not generalize to nonlinear and are either based on computationally demanding Taylor-series expansions or bootstrap techniques [23, 6].

The goal of this paper is to derive a computationally inexpensive lower bound on the MSE that will provide more accurate error bars on when is unknown.

3 Prediction errors after learning the hyperparameters

In the general setting when is unknown we have the following lower bound on the MSE.

Result 2.

When is learned from using an unbiased estimator, we have that:

| (7) |

where

| (8) |

Comparing with (4), the non-negative term is the additional error incurred due to the lack of information about .

First, note that will be non-zero even in the simplest models where the data has an unknown constant mean, i.e., .

Second, (7) depends on the unknown covariance parameters only via and not through any gradients as would be expected. As we show in the proofs below, this is follows from the properties of the Gaussian data distribution. In the special case of linear mean functions, , (7) coincides with MSE of the universal kriging estimator which assumes to be known [17].

Third, under standard regularity conditions, the maximum likelihood approach will yield estimates of that are asymptotically unbiased and attain their corresponding error bounds [20].

Proof.

The HCRB for is given by

| (9) |

where the matrices are given by the hybrid information matrix

| (10) |

To prepare for the subsequent steps, we introduce and let and denote the joint mean and covariance matrix respectively, i.e. . Next, we define the linear combiner

and note that

| (11) |

Similarly, .

To compute the block in (10), we first establish the following derivatives:

where the last equality follows from (5) and (11). Then we obtain

and

Similarly, . Therefore

| (12) |

Next, using the distribution of , is obtained via Slepian-Bangs formula [16, 1, 18]:

This yields a block-diagonal matrix

| (13) |

where the right-lower block does not affect (9) due to the zeros in (12). Inserting (12), (13) and (6) into (9) then yields

| (14) | ||||

where the last equality follows from the matrix inversion lemma. Using the properties of the block-inverse of , we show that the inner parenthesis equals in Appendix B. ∎

Remark: Result 2 is based on the framework in [13], se also [20]. This assumes that the bias of the learning method is zero. In Appendix A we provide an alternative proof of Result 2 that relaxes this assumption.

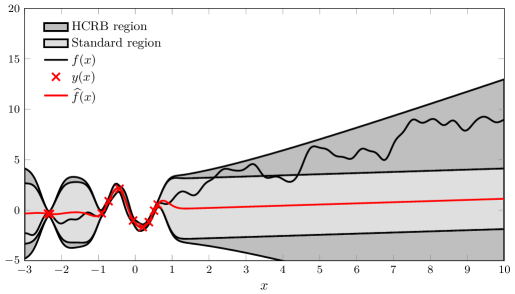

Example 1.

(cont’d) To illustrate the difference between (4) and (7), consider Figure 2. It shows the same realization of as in Figure 1, along with the predicted values . The error bars are now obtained from (7) which takes into account that has to be learned from the data. These bars clearly quantify the errors more accurately and contain the realization , in contrast to the standard approach.

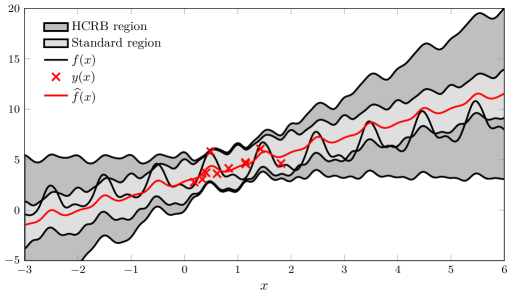

Example 2.

(Time series prediction) Here we consider a temporal process with an unknown linear trend and periodicity (per) modeled by mean function

covariance kernel

and unit noise level. In Figure 3 we show a single realization of the process together with the prediction error bars computed using both the predictive variance and the HCRB. As can be seen, falls outside of the credibility region provided by the standard method.

4 Examples

We illustrate the HCRB and its practical utility by means of several examples. For the sake of visualization, we have considered problems with one-dimensional inputs, but the HCRB is of course valid for any dimension of . The first set of examples use synthetically generated datasets in order to assess the accuracy of the error bound. The final example uses real concentration data. We used the maximum likelihood approach to learn in all examples but alternative methods, such as cross-validation, could be considered as well.

4.1 Synthetic data

First, we consider a process with the popular squared-exponential covariance (SE) function

| (15) |

where we assume both the signal variance and length scale to be unknown. As mean function, we assign the most basic model, a constant mean , where is unknown. The unknown hyperparameters generating the data are denoted

| (16) |

Figure 4 shows the empirical MSE of (3) after learning the hyperparameters from observations (obtained from Monte Carlo iterations), where denotes evaluating the predictor using mean parameter , covariance parameter and noise level . We compare this error with the theoretical bounds given by (4) and (7). We see that the bound is tight as expected in this example and that systematically underestimates the errors. Similarly, when using estimated bounds by inserting the learned hyperparameters into (4) and (7) the gap between and not extreme, but still present, with the latter giving a better representation of the true error than the estimated predictive variance.

Another simple but common mean function is the linear mean . Again, using a process with the squared exponential covariance function,(15), with hyperparameters and noise level as in (16) but with a linear mean function with , we evaluate the empirical MSE (obtained by Monte Carlo samples) and the theoretical bounds in Figure 5. The hyperparameters were learned using observations. The gap between the bounds become even more pronounced in predictions outside the sampled region.

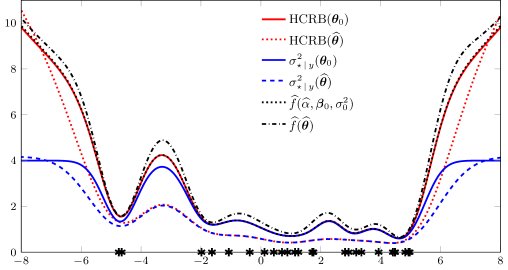

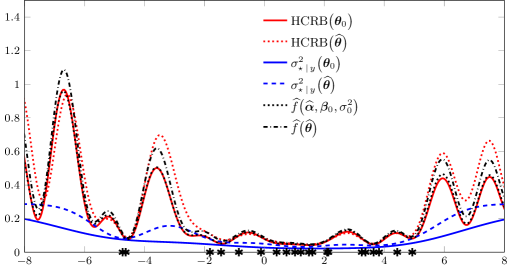

Next, we consider an example inspired by frequency estimation in colored noise, which is a challenging problem. We model a process using a sinusoid mean function

| (17) |

with unknown amplitude, frequency and phase, and a squared exponential covariance function (15). Here, we let , and . The process was sampled at non-uniformly spaced input points, cf. Figure 6. Note how the conditional variance severely underestimates the uncertainty in the predictions between and , but how the HCRB, even when estimated from data, provides a much more accurate bound.

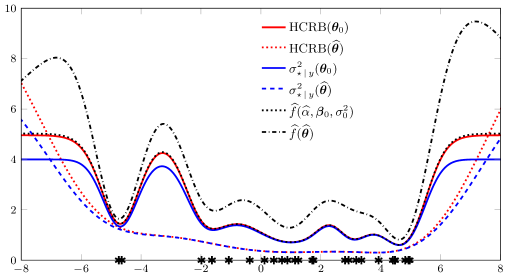

4.2 Marginalizing the mean parameters

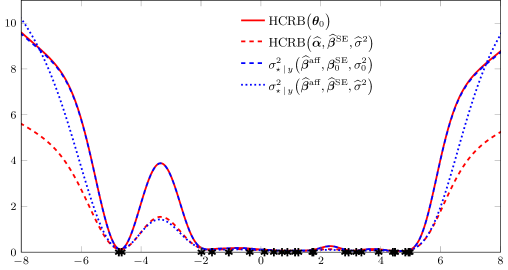

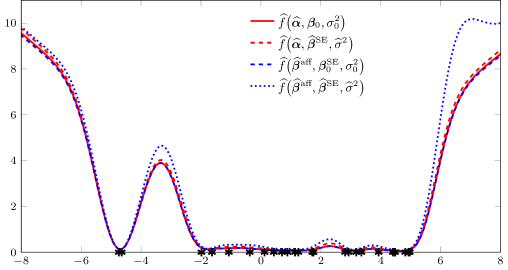

For the special case in which the mean function is linear in the parameters, that is, , it is possible to consider an alternative parameterization: A Gaussian hyperprior can be assigned with positive covariance parameters . By marginalizing out from , we then obtain an additional term to the covariance function where is augmented to the hyperparameters. Correspondly, the mean function becomes , which is a common assumption in the Gaussian process literature [12]. This model parameterization will therefore have an alternative predictive variance that captures the uncertainty of the linear mean parameters.

To study the effect of this alternative parameterization on the bounds and prediction, we consider a linear trend along with as given in (15). The data was generated according to this model and the HCRB is evaluated in Figure 7. The marginalized model is here and , where

corresponds to the unknown linear mean function. The predictive variance of this model was evaluated learning its hyperparameters using data from the original model and inserting them into .

For the special case in which only is learned, the correspondence between and HCRB is striking in Figure 7. In this case, also the the predictors, using the original and marginalized models, respectively, perform nearly identically. When all hyperparameters are learned in the original and marginal models, respectively, the empirical turns out to be more accurate than the empirical HCRB in the extremes. The results suggest that for linear mean functions there is a potential advantage in using the marginalized model to assess the prediction accuracy. However, in this case we also note that the performance of the predictor based on the marginalized model is degraded in comparison to that based on the original model.

4.3 CO2 concentration data

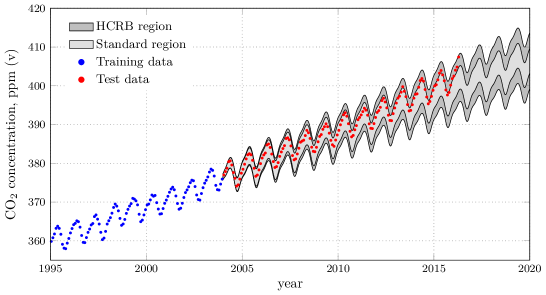

With the previous examples in mind, we now consider real concentration data111ftp://ftp.cmdl.noaa.gov/ccg/co2/trends/co2_mm_mlo.txt analyzed in [12]. The data exhibits a trend as well as periodicities. These features can be modeled using the mean and covariance functions considered in the previous example. In addition, to capture smooth variations as well as erratic patterns, we consider using a squared-exponential kernel and a rational quadratic (RQ) kernel . The final covariance function can be written as:

In this example, the hyperparameters are learned using monthly data from the years 1995 to 2003. The prediction error bars using the predictive variance and HCRB are plotted in Figure 8. Using validation data from 2004 to March 2016 we assess the error bars. As can be seen several data points fall outside of standard approach fall outside of the 99.7% credibility region but are contained in the HCRB region.

5 Discussion

We used the Hybrid Cramér-Rao Bound as a tool to analyze the prediction performance of Gaussian process regression after learning. When comparing the new bound with the commonly used predictive variance we showed that the latter will systematically underestimate the minimum MSE, even for the simplest datasets with unknown constant mean. This leads to incorrect prediction error bars. The underestimation gap arises from uncertainty of the hyperparameters and we provide an explicit and general characterization of it. The resulting HCRB is a simple closed-form expression and computationally cheap to implement.

In the examples we showed that the HCRB provides a tighter lower bound of the MSE for the standard predictor than the nominal predictive variance. The HCRB is easily computed using the quantities in the predictor itself and provides more accurate error bars, even when using estimated hyperparameters. In future work, we will investigate the accuracy of the estimated HCRB further. For the special case of linear mean functions, the results indicate a possible advantage of using an alternative marginalized model and assessing its corresponding BCRB using learned model parameters.

Acknowledgments

The authors would like to thank Dr. Marc Deisenroth and Prof. Carl E. Rasmussen for fruitful discussions.

This research is financially supported by the Swedish Foundation for Strategic Research (SSF) via the project ASSEMBLE (Contract number: RIT15-0012) . The work was also supported by the Swedish research Council (VR) via the projects Probabilistic modeling of dynamical systems (Contract number: 621-2013-5524) and (Contract number: 621-2014-5874).

Appendix A Alternative derivation of the bound

Unlike [13, 20], we will here prove Result 2 assuming only that the bias of the estimator with respect to is invariant to . That is,

where is a constant.

We begin by decomposing the MSE of an estimator :

| (18) |

where is the conditional mean (3) of . Since the first term in (18), , is independent of the estimator we will focus on finding a lower bound for the second term.

For notational simplicity, define the score function of the training data pdf as:

Then the correlation between the score function and the estimation error is

The first set of zeros follows from

The final zero follows in a similar manner.

Appendix B Proof of equality

Recall that , , , , and . Then the following holds.

Proof.

Let .

∎

References

- [1] W.. Bangs “Array Processing with Generalized Beamformers”, Ph.D. Thesis Yale University, 1971

- [2] C.M. Bishop “Pattern Recognition and Machine Learning”, Information Science and Statistics Springer, 2006 URL: https://books.google.se/books?id=qWPwnQEACAAJ

- [3] H. Cramér “A contribution to the theory of statistical estimation” In Scandinavian Actuarial Journal 1946.1 Taylor & Francis, 1946, pp. 85–94

- [4] M. Deisenroth, D. Fox and C.. Rasmussen “Gaussian Processes for Data-Efficient Learning in Robotics and Control” In Transactions on Pattern Analysis and Machine Intelligence 37.2 IEEE, 2015, pp. 408–423

- [5] M. Deisenroth and C.E. Rasmussen “PILCO: A model-based and data-efficient approach to policy search” In Proceedings of the 28th International Conference on machine learning (ICML-11), 2011, pp. 465–472

- [6] Dick Den Hertog, Jack PC Kleijnen and AYD Siem “The correct Kriging variance estimated by bootstrapping” In Journal of the Operational Research Society 57.4 Nature Publishing Group, 2006, pp. 400–409

- [7] R.D. Gill and B.Y. Levit “Applications of the van Trees inequality: a Bayesian Cramér-Rao bound” In Bernoulli JSTOR, 1995, pp. 59–79

- [8] B. Likar and J. Kocijan “Predictive control of a gas–liquid separation plant based on a Gaussian process model” In Computers & chemical engineering 31.3 Elsevier, 2007, pp. 142–152

- [9] K.P. Murphy “Machine Learning: A Probabilistic Perspective”, Adaptive computation and machine learning series MIT Press, 2012 URL: https://books.google.se/books?id=NZP6AQAAQBAJ

- [10] F. Pérez-Cruz, S. Van Vaerenbergh, JJ.J. Murillo-Fuentes, M. Lázaro-Gredilla and I. Santamaria “Gaussian processes for nonlinear signal processing: An overview of recent advances” In IEEE Signal Processing Magazine 30.4 IEEE, 2013, pp. 40–50

- [11] C.R. Rao “Information and the accuracy attainable in the estimation of statistical parameters” In Bulletin of Calcutta Mathematical Society 37.1, 1945, pp. 81–89

- [12] C.E. Rasmussen and C.K.I. Williams “Gaussian Processes for Machine Learning”, Adaptative computation and machine learning series MIT Press, 2006 URL: https://books.google.se/books?id=vWtwQgAACAAJ

- [13] Y. Rockah and P.M. Schultheiss “Array shape calibration using sources in unknown locations–Part I: Far-field sources” In IEEE Transactions on Acoustics, Speech and Signal Processing 35.3 IEEE, 1987, pp. 286–299

- [14] B. Schölkopf and A.J. Smola “Learning with Kernels: Support Vector Machines, Regularization, Optimization, and Beyond”, Adaptive computation and machine learning MIT Press, 2002 URL: https://books.google.se/books?id=y8ORL3DWt4sC

- [15] Bobak Shahriari, Kevin Swersky, Ziyu Wang, Ryan P Adams and Nando Freitas “Taking the human out of the loop: A review of bayesian optimization” In Proceedings of the IEEE 104.1 IEEE, 2016, pp. 148–175

- [16] D. Slepian “Estimation of signal parameters in the presence of noise” In Information Theory, Transactions of the IRE Professional Group on 3.3 IEEE, 1954, pp. 68–89

- [17] M.L. Stein “Interpolation of Spatial Data: Some Theory for Kriging”, Springer Series in Statistics Springer New York, 1999 URL: https://books.google.se/books?id=5n%5C_XuL2Wx1EC

- [18] P. Stoica and R.L. Moses “Spectral analysis of signals” Pearson/Prentice Hall, 2005

- [19] J.A.K. Suykens, T. Van Gestel and J. De Brabanter “Least Squares Support Vector Machines” World Scientific, 2002 URL: https://books.google.se/books?id=g8wEimyEmrUC

- [20] H.L. Van Trees and K.L. Bell “Detection Estimation and Modulation Theory, Pt.I”, Detection Estimation and Modulation Theory Wiley, 2013 [1968] URL: http://books.google.se/books?id=dnvaxqHDkbQC

- [21] Christopher K.. Williams and Carl Edward Rasmussen “Gaussian Processes for Regression” In Advances in Neural Information Processing Systems 8 MIT Press, 1996, pp. 514–520 URL: http://papers.nips.cc/paper/1048-gaussian-processes-for-regression.pdf

- [22] D. Zachariah and P. Stoica “Cramer-Rao Bound Analog of Bayes’ Rule [Lecture Notes]” In Signal Processing Magazine, IEEE 32.2 IEEE, 2015, pp. 164–168

- [23] Dale L Zimmerman and Noel Cressie “Mean squared prediction error in the spatial linear model with estimated covariance parameters” In Annals of the institute of statistical mathematics 44.1 Springer, 1992, pp. 27–43