Optimality Conditions for Inventory Control

Abstract

This tutorial describes recently developed general optimality conditions for Markov Decision Processes that have significant applications to inventory control. In particular, these conditions imply the validity of optimality equations and inequalities. They also imply the convergence of value iteration algorithms. For total discounted-cost problems only two mild conditions on the continuity of transition probabilities and lower semi-continuity of one-step costs are needed. For average-cost problems, a single additional assumption on the finiteness of relative values is required. The general results are applied to periodic-review inventory control problems with discounted and average-cost criteria without any assumptions on demand distributions. The case of partially observable states is also discussed.

Keywords

inventory control, Markov Decision Process, policy, optimality equation, sufficient conditions

1 Introduction

This tutorial describes recent progress in the theory of Markov Decision Processes (MDPs) with infinite state and action sets that have significant applications to inventory control. Two groups of results are covered: (i) optimality conditions for MDPs with total, discounted and average-cost criteria, and (ii) optimality conditions for Partially Observable Markov Decision Processes (POMDPs) with total and discounted cost criteria.

Inventory control studies and applications are important motivating factors for studies of MDPs. The MDP studies provided important tools for the analysis of inventory control problems. The parallel development of these fields since the beginning of the second half of the 20th century is broadly recognized. For example, the abstract of the historical essay by Girlich and Chikan [37] on the history of inventory control studies states: “… we report how inventory problems have motivated the improvement of mathematical disciplines such as Markovian decision theory and optimal control of stochastic systems to provide a new basis of inventory theory in the second half of our century.” However, over a long period of time there was a gap between the modeling needs for inventory control, that require mathematical methods for the analysis of infinite-state controlled stochastic systems with unbounded action sets and weakly continuous transition probabilities, and available results for the corresponding models for MDPs. This gap was recently closed. Another topic covered in this tutorial is the recent progress in the development of optimality conditions for POMDPs. The literature on MDPs and inventory control is huge, and we do not attempt a comprehensive survey in this tutorial. For the most part only directly relevant references are provided. The reader may find coverage of these topics in the books [3, 12, 22, 24, 42, 38, 41, 40, 48, 55] on MDPs and [5, 42, 47, 60, 67] on inventory management.

Optimality results for MDPs provide sufficient conditions for the existence of stationary and Markov optimal policies satisfying optimality equations and inequalities, describe continuity properties of the value function, and guarantee the convergence of value iteration and optimal actions when the horizon length tends to infinity or the discount factor tends to 1. These results provide useful tools to analyze specific inventory control problems and to prove the optimality of particular policies. In Section 4 this is illustrated with the classic periodic-review single-product stochastic inventory problem with nonnegative arbitrarily distributed iid demand. Most of the literature on inventory control is limited to discrete or continuous demand distributions.

Consider the classic periodic-review single-product stochastic inventory problem with backorders. For a finite horizon and continuous demand, Scarf [51] established under some conditions the optimality of policies. Zabel [65] indicated some gaps in [51], corrected them, and mentioned in the last paragraph of [65] that the proofs there can be adapted to arbitrary demand distributions. Iglehart [44] and Veinott and Wagner [63] established the optimality of policies for the infinite horizon for continuous and discrete demand respectively. Zheng [66] provided an alternative proof for discrete demand. Beyer and Sethi [13] described and corrected gaps in the proofs in [44, 63]. As shown in Heyman and Sobel [Section 7.1][42], under appropriate conditions policies are optimal for a finite-horizon problem with arbitrarily distributed demand. In general, policies may not be optimal for finite horizons. For example, for a problem with convex holding costs the appropriate condition is Assumption GB in Section 4. This assumption means that, as the amount of backordered inventory increases, the backordering cost per unit time becomes larger than the value of the backordered inventory. However, as shown in Veinott [62] for discrete demand, policies are always optimal for the following three criteria: (i) infinite-horizon average costs per unit time, (ii) infinite-horizon discounted problems with a large discount factor, and (iii) finite-horizon problems with appropriately selected terminal costs. Chen and Simchi-Levi [17, 18] described optimal policies for coordinating inventory control and pricing for finite and infinite-horizon problems with general demand under a technical assumption. If the price is fixed, the problem in [17, 18] becomes the periodic-review inventory control problem, the technical assumption becomes Assumption GB, and the results in [17, 18] imply the optimality of policies. For coordinating inventory control and pricing, Huh et al. [43] provided a method for proving the optimality of stationary policies by adding specific assumptions that hold for inventory control to the MDP assumptions.

Using the results from Feinberg et al. [27] on the existence of stationary optimal policies and their properties for MDPs with general state and action sets and with possibly unbounded one-step cost functions, Feinberg and Lewis [34] proved the optimality of policies for a general demand distribution for criteria (i – iii) mentioned in the previous paragraph. Feinberg and Liang [36] provided a complete description of optimal discounted policies for arbitrary demand. These results cover the results under Assumption GB as a special case. Feinberg and Liang [35] proved the validity of the optimality equation for average costs per unit time, while the general results for MDPs [27] imply only the validity the optimality inequality. The conclusions from [34, 35, 36] are presented in Section 3.

Studies of MDPs started with investigations of models with finite state and action sets. Problems with infinite state and action sets were investigated later. The two classic objective criteria for infinite-horizon problems are: (i) minimization of expected total discounted costs, and (ii) minimization of long-run average costs per unit time. Problems with average cost criteria are usually more difficult. In particular, optimality equations can be written for expected total costs under mild conditions, and for total expected discounted costs their analyses lead to the proof of optimality of stationary policies for infinite-horizon problems. For long-run average costs, stationary policies are optimal under stronger conditions than for discounted costs, and proofs of their optimality for average-cost criteria usually use the existence of stationary optimal policies for discounted criteria, when the discount factor increases to 1. This is the so-called vanishing discount factor approach. In particular, this approach can be used to establish the validity of optimality equations (sometimes called canonical equations) and inequalities for MDPs with long-run average-costs. Average-cost optimality equations and inequalities imply the existence of optimal stationary policies for long-run average costs. In applications, average-cost optimality equations and inequalities can be written without an explicit use of the vanishing discount factor approach by using general results on the validity of average-cost optimality equations and inequalities for MDPs. However, as mentioned above, this approach is typically used in the theory of MDPs to establish the validity of such equations and inequalities.

Let us discuss optimality conditions for MDPs that are general enough to provide optimality conditions for broad classes of inventory control models. First, the state space should be an unbounded subset of a Euclidean space. This level of generality is covered by Borel state spaces (more precisely, Borel subsets of complete separable metric spaces). Euclidean spaces are examples of Borel spaces, and the general theory of MDPs with Euclidean state spaces is not simpler than for Borel spaces. Similarly to subsets of Euclidean spaces, Borel spaces are either finite, countable, or have the cardinality of the continuum. A reader, who is not familiar with the notion of Borel spaces, may view all the state and action sets in this tutorial as subsets of Euclidean spaces. Second, the cost functions may be unbounded. More precisely, the cost functions should be inf-compact as a function of two variables: a state and action. For inventory control, inf-compact cost functions can be interpreted as lower-semicontinuous functions tending to infinity if either the inventory/backorder or the order size tends to infinity. Cost functions may not be continuous. For example, they are not continuous in models with positive ordering costs. Third, transition probabilities should satisfy the property of continuity in distribution, also known under the name of weak continuity. In particular, transition probabilities are typically weakly continuous for periodic-review stochastic inventory control problems with arbitrary demand distributions; see Feinberg and Lewis [33, Section 4] for details. In particular, it is explained there, that the case of setwise continuous transition probabilities, which is often considered in the MDP literature, typically covers only discrete and continuous demand distributions. Fourth, action sets may be unbounded. This corresponds to a potentially unlimited production/supply capacity. For example, if a production/supply capacity is limited, then policies may not be optimal; see e.g., Federgruen and Zipkin [23] and Shaoxiang [57].

For discounted costs, Shapley [58] introduced a zero-sum two-person stochastic game with finite state and action sets. If one of the players has only one action at each state, this model becomes an MDP. This publication is considered as the first paper on MDPs. Blackwell [15] developed the theory for discounted costs and Borel state and action sets. In particular, Blackwell [15] studied problems with bounded costs and discovered that the objective functions may not be Borel measurable, and the dynamic programming approach to such problem should deal with more general policies than Borel measurable ones. The appropriate theory is developed in Bertsekas and Shreve [12]. Schäl [52] developed the theory for discounted costs, Borel state spaces, compact action sets, possibly unbounded above cost functions, and continuous transition probabilities. Results for two types of continuity are obtained in [52]: for setwise and weak continuity. The results on weak continuity are more important for applications and more complicated. The theory for problems with setwise continuous transition probabilities and possibly noncompact action sets is described in Hernández-Lerma and Lasserre [41]. Feinberg and Lewis [33] provided results for discounted MDPs with weakly continuous transition probabilities, possibly uncountable action sets, and inf-compact cost functions. Feinberg et al. [27] introduced the notion of -inf-compact functions and obtained more general results than in [33]; see Theorem 5.1, which is a version of [27, Theorem 2] adapted in [34] to problems with possibly nonzero terminal costs.

For average costs per unit time Blackwell [14] and Derman [19] established the existence of stationary optimal policies for the case of finite state and action sets. Derman [20] and Taylor [45] introduced optimality equations for infinite-state problems with bounded one-step costs. These equations and their version for multi-chain problems are called canonical in Dynkin and Yushkevich [22]. Sennott [54] introduced optimality conditions that lead to the validity of optimality inequalities whose solutions define stationary optimal policies; see also [55, 56] and the references therein. Cavazos-Cadena [16] provided an example when optimality inequalities do not hold in the form of equalities. Schäl [53] extends Sennott’s results to Borel state spaces, compact action spaces, and with weakly and setwise continuous transition probabilities. Hernández-Lerma [39] generalized Schäl’s [53] results for setwise continuous transition probabilities to possibly noncompact action sets. Feinberg and Lewis [33] provided sufficient optimality conditions for weakly continuous transition probabilities and possibly noncompact action sets. Feinberg et al. [27] provided results for weakly continuous transition probabilities that generalize the corresponding results in Schäl [53] and Feinberg and Lewis [33]; see Subsection 5.2 below.

The second topic covered in this tutorial is optimality conditions for POMDPs and, in particular, for inventory control problems with incomplete information on inventory levels. Research on inventory management with incomplete information was pioneered by Bensoussan et al. [6, 7, 8, 9], where particular problems are studied and the existence of optimal policies and convergence of value iterations are established. In general, for POMDPs there is a well-known reduction, introduced by Aoki [1], Åström [2], Dynkin [21], and Shiryaev [59] of a POMDP to an MDP whose states are posterior probabilities of the states of the original process. This reduction holds for problems with Borel state, action, and observation sets, and with measurable transition probabilities [12, 41, 49, 64]. However, it provides little information about the existence of optimal policies and the validity of optimality equations.

This reduction is based on Bayes’ formula, which has an explicit form only for problems with transition functions that are either discrete or have densities. As a result, except the case of finite state, action, and observation sets, very little was known on the existence of optimal policies for POMDPs. Therefore, the common approach is to study applications by problem-specific methods. The general approach, applicable to a large variety of applications, for verifying optimality conditions for POMDPs is developed in Feinberg et al. [32], and one of the applications there deals with inventory control. The general optimality results on POMDPs are presented in Section 6, and an application to inventory control is presented in Section 7.

2 Markov Decision Processes: Definitions and Optimality Conditions

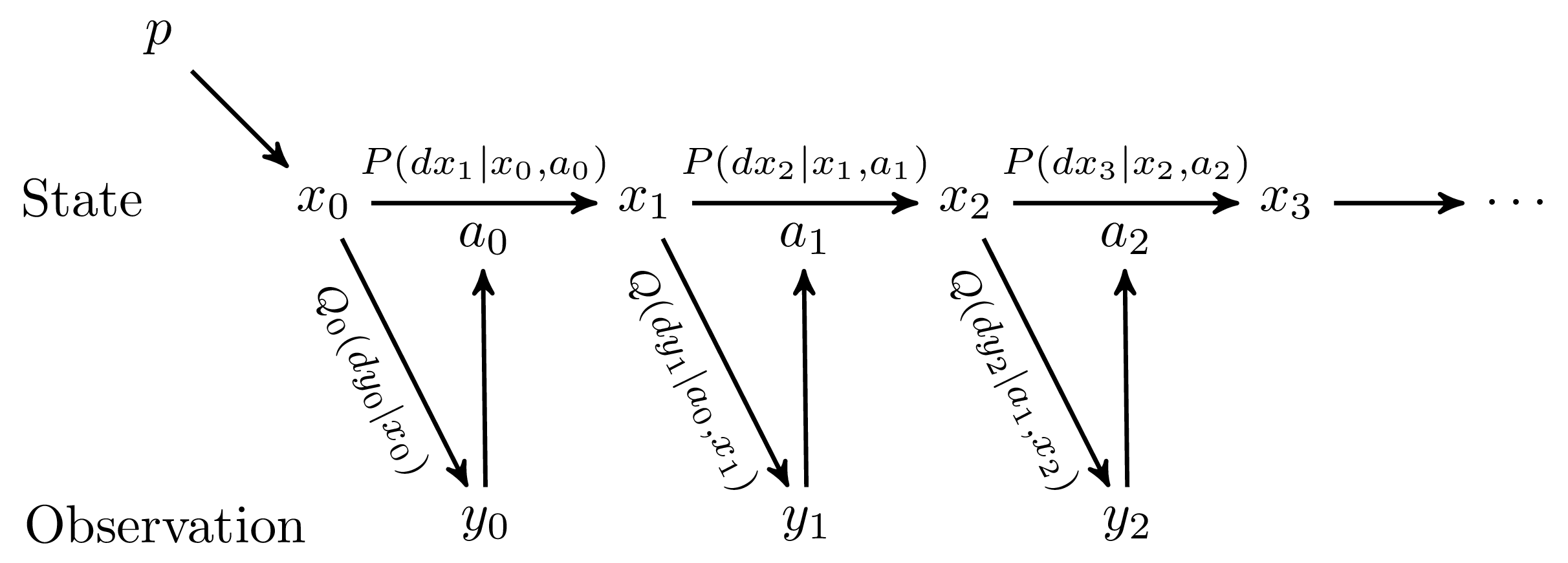

An MDP is defined by a tuple where is the state space, is the action space, is the transition probability, and is the one-step cost function. The state space and action space are both assumed to be Borel subsets of Polish (complete separable metric) spaces. If an action is selected at a state then a cost is incurred, where and the system moves to the next state according to the probability distribution on The function is assumed to be bounded below and Borel measurable, and is a transition probability, that is, is a Borel function on for each Borel subset of and is a probability measure on the Borel -field of for each

The decision process proceeds as follows: at time the current state of the system, , is observed. A decision-maker decides which action, , to choose, the cost is accrued, the system moves to the next state according to and the process continues. Let be the set of histories for A (randomized) decision rule at epoch is a regular transition probability from to In other words, (i) is a probability distribution on where and (ii) for any measurable subset , the function is measurable on A policy is a sequence of decision rules. Moreover, is called non-randomized if each probability measure is concentrated at one point. A non-randomized policy is called Markov if all decisions depend only on the current state and time. A Markov policy is called stationary if all decisions depend only on the current state. Thus, a Markov policy is defined by a sequence of measurable mappings A stationary policy is defined by a measurable mapping

The Ionescu–Tulcea theorem (see [12, p. 140-141] or [41, p. 178]) implies that an initial state and a policy define a unique probability distribution on the set of all trajectories endowed with the product -field defined by the Borel -fields of and Let be the expectation with respect to this distribution. For a finite horizon and a bounded below measurable function called the terminal value, define the expected total discounted costs

| (1) |

where and, if then When for all we shall write instead of When and for all , (1) defines the infinite horizon expected total discounted cost of denoted by instead of The average costs per unit time are defined as

| (2) |

For each function , , , or , define the optimal cost

| (3) |

where is the set of all policies. A policy is called optimal for the respective criterion if for all .

The defined model is too general for the existence of optimal policies. However, optimal policies exist under modest conditions, which typically hold for inventory control applications. The natural conditions for inventory control applications are that the transition probability is weakly continuous and the cost function is inf-compact.

The transition probability is called weakly continuous, if for every bounded continuous function the function

is a continuous function on For an -valued function , defined on a subset of a metric space consider the level sets

| (4) |

A function is called lower semi-continuous if all the level sets are closed, and a function is called inf-compact if all these sets are compact. In particular, the cost function is defined on and the level sets for are

| (5) |

As shown by Feinberg and Lewis [33], for the discounted costs weak continuity of and inf-compactness of imply the existence of optimal policies. However, the condition that the function is inf-compact can be relaxed by considering the class of -inf-compact functions.

For two sets and where and for two functions and defined on and respectively, function defined on is called the restriction of to if when

Definition 2.1

Definition 2.1 corresponds to Definition 9.1 of a -inf-compact function on in the following way. For a given function define

and for all Then the function is -inf-compact if and only if the function is -inf-compact on We mainly apply the notion of a -inf-compact function to the situation when and are Polish spaces in which the state and action sets and are defined respectively. In many inventory control applications, and So, if the state and action sets and are explicitly defined as Polish spaces, we assume that and are Polish spaces containing and that are mentioned in the definition of an MDP. The examples include and

For a function -inf-compactness is a more general and natural property than inf-compactness. For example, for the function is -inf-compact, but it is not inf-compact. As shown in Feinberg et al. [27], the following assumption is sufficient for the existence of optimal policies for discounted MDPs.

Assumption W*. The following conditions hold:

(i) the transition probability is weakly continuous;

(ii) the cost function is -inf-compact.

We list some of the properties of MDPs that take place under Assumption W* (see Theorem 5.1 for details):

-

1.

For a bounded below, lower semi-continuous terminal value function the final-horizon optimality equation holds for all

(6) where for all . In particular, this is true for and

-

2.

The function is lower semicontinuous, where . If the function is bounded below and lower semi-continuous, then the functions for and are lower semi-continuous. If in addition for all then where . In particular, this is true for that is, where .

-

3.

For the infinite-horizon value function satisfies the optimality equation

(7) a stationary optimal policy exists, and a stationary policy is optimal if and only if

(8) -

4.

If the one-step cost function is inf-compact, then the value function is inf-compact, when The same is true for the value functions when the terminal value is a bounded below, lower semi-continuous function and

In particular, the fourth property is useful for proving the existence of stationary optimal policies for inventory control problems. It is well-known that for average costs per unit time optimal policies may not exist under Assumption W*. For example, optimal policies may not exist for a countable state space and finite action sets; see e.g., Ross [50, Section 5.1] and for a finite state set, compact action sets, and continuous transition probabilities and costs; see e.g., Dynkin and Yushkevich [22, Section 7.8]. Next we formulate a general condition, that typically holds for inventory control problems, which together with Assumption W* guarantees the existence of optimal policies for average-cost MDPs. If define for :

Assumption B. The following conditions hold:

(i)

(ii) for all

We notice that the function is nonnegative and Assumption B implies that cannot take infinite values; see Schäl [53]. If Assumption B(i) does not hold then the average-cost problem is trivial: all policies lead to infinite average losses per unit time. This assumption holds in all well-defined problems and usually it is easy to verify. The validity of Assumption B(ii) probably follows from various ergodicity and communicating conditions, but this relation has not been studied in the literature. As explained in the text following Theorem 5.5 below, Assumption B(ii) holds and can be easily verified for inventory control problems. As shown in Feinberg et al. [27], Assumptions W* and B imply the existence of stationary optimal policies for average-cost MDPs, which follows from the validity of optimality inequalities.

For consider

According to Schäl [53, Lemma 1.2], Assumption B(i) implies

| (9) |

According to Schäl [53, Proposition 1.3], if there exists a measurable function and a stationary policy satisfying the Optimality Inequality

| (10) |

then is average-cost optimal and for all . Assumptions W* and B imply the existence of a stationary policy satisfying optimality inequality (10).

Another form of an optimality inequality was introduced in Feinberg et al. [27], where it was shown that, if there exists a measurable function and a stationary policy such that

| (11) |

then is average-cost optimal and

| (12) |

Observe that inequality (11) is weaker than (10) because (10) implies (11).

The existence of stationary optimal policies satisfying inequality (11) is proved in Feinberg et al. [27] under Assumptions W* and an assumption called B there, which consists of Assumption B(i) and the following assumption [27]:

| (13) |

which is weaker than Assumption B(ii). However, an example of an MDP, satisfying Assumptions W* and B , but not satisfying Assumption B(ii), is currently unknown.

Remark 2.2

The definition of an MDP usually includes the sets of available actions We do not do this explicitly because we allow to be equal to In other words, a feasible pair is modeled as a pair with finite costs. To transform this model to a one with feasible action sets, it is sufficient to consider the sets of available actions such that where In order to transform an MDP with action sets to an MDP with the action set it is sufficient to set when Early works on MDPs by Blackwell [15] and Strauch [61] considered models with for all This approach caused some problems with the generality of the results because the boundedness of the cost function was assumed and therefore for all If the cost function is allowed to take infinitely large values, models with are as general as models with

3 MDPs Defined by Stochastic Equations

Inventory control problems are often defined by equations

| (14) |

where is the amount of inventory available at the end of day is the ordered quantity at the end of day , and is the demand on day For the classic periodic-review problem with backlogs and for a problem with lost sales The system can also incur losses of inventory, there could be lead times, and so on. So, the function can have a more complicated form, and interpretations of its parameters may be different for different problems. Also, in this paper we only consider independent and identically distributed demands, that is, are independent and identically distributed.

Let be a metric space, be its Borel -field, and be a probability measure on . Consider a stochastic sequence whose dynamics are defined by equation (14), where are independent and identically distributed random variables with values in whose distributions are defined by a probability measure and is a measurable mapping.

Equation (14) defines the transition probability

| (15) |

from and is the distribution of given and where is the indicator function.

The following lemma relates Assumption W*(ii) to the problems defined by stochastic equations.

Lemma 3.1

(Hernández-Lerma [38, p. 92]). If the function is continuous then the transition probability is weakly continuous.

Consider an MDP with the transition probability defined by a continuous function If the one-step cost function is inf-compact, then, for a random variable with the same distribution as formulae (6)–(8) can be rewritten as

| (16) |

4 The Classic Periodic-Review Problem with Backorders

In this section we consider a discrete-time periodic-review inventory control problem with back orders and prove the existence of an optimal policy. For this problem the dynamics are defined by the following stochastic equation

| (20) |

where is the inventory at the end of period , is the amount ordered at the end of period and is the demand during period . The demand is assumed to be i.i.d. In other words, the dynamics of the system is defined by equation (14) with the function Of course, this function is continuous. Here we consider the case, when there is a single commodity. In this case, and are real numbers.

A decision-maker views the current inventory of a single commodity at the end of the day and makes an ordering decision. Assuming zero lead times, the products are immediately available to meet demand. Demand is then realized, the decision-maker views the remaining inventory, and the process continues. Assume the unmet demand is backlogged and the cost of inventory held or backlogged (negative inventory) is modeled as a convex function. The demand and the order quantity are assumed to be non-negative. The dynamics of the system are defined by (20). Let

-

(a)

be the discount factor,

-

(b)

be a fixed ordering cost,

-

(c)

be the per unit ordering cost,

-

(d)

be a nonnegative random variable with the same distribution as and

-

(e)

denote the holding/backordering cost per period. It is assumed that is a convex function, as and for all

Without loss of generality, assume that . The fact that avoids the trivial case. For example, if almost surely then the policy that never orders when the inventory level is non-negative and orders up to zero when the inventory level is negative, is optimal under the average cost criterion. Note that since, in view of Jensen’s inequality,

Let us define the state space the action set where the transition probability defined in (15) with and the one-step cost function

The function is inf-compact and, of course, the function is continuous. Therefore, Assumption W* holds. It is relatively easy to show that Assumption B holds. Thus, optimality equations exist for finite horizon and infinite horizon problems. In particular, they exist for problems with total discounted and average-cost criteria.

Optimality equations and inequalities can be written as

| (21) | ||||

| (22) | ||||

| (23) |

where and

| (24) | ||||

| (25) | ||||

| (26) |

We also write instead of when

Definition 4.1

Let and be real numbers such that , Suppose denotes the current inventory level at decision epoch . A policy is called an policy at step if it orders up to the level if and does not order when A Markov policy is called an policy if it is an policy at all steps A policy is called an policy if it is stationary and it is an policy at all steps

The standard methods for proving the optimality of and policies for discounted costs was introduced by Scarf [51], and is based on the notion of a -convex function.

Definition 4.2

A function is called -convex, if for each and for each ,

For an inf-compact function let

| (27) | ||||

| (28) |

These real numbers exist because the function is inf-compact. In addition, is defined uniquely and does not depend on In addition, is defined uniquely and does not depend on the choice of if there are more than one satisfying (27).

The standard method for proving the optimality of policies is to consider and prove by induction that these functions are inf-compact and -convex, which implies from the optimality equation (21) optimality of policies with and defined by (27), (28) with . The next step would be to consider and prove the optimality of policies for infinite-horizon problems.

However, it is possible that the functions are not inf-compact, and the described approach fails. Then the natural approach is to try to do the same steps for the function for a specially selected terminal value function The natural candidate is the function where is the infinite-horizon value for the problem with the ordering cost It is possible to show that there exists such that the functions are inf-compact, and this implies the optimality of -policies for all finite-horizon problems with the terminal value for all which implies optimality of -policies for the infinite horizon discounted criterion with the discount factor In addition, it is always true that , and the following lemma holds.

The optimality of -optimal policies for large discount factors imply optimality of policies for average costs per unit time. The following theorem takes place.

Theorem 4.4

([34]). Consider whose existence is stated in Lemma 4.3. The following statements hold for the inventory control problem.

(i) For and define . Consider real numbers satisfying (27) and defined in (28). Then for each the policy, is optimal for the -horizon problem with the terminal values .

(ii) For the infinite-horizon expected total discounted cost criterion with a discount factor define . Consider real numbers satisfying (27) and defined in (28). Then the policy is optimal for the discount factor Furthermore, the sequence of pairs is bounded, where and are described in statement (i), If a limit point of this sequence, then the policy is optimal for the infinite-horizon problem with the discount factor

(iii) Consider the infinite-horizon average cost criterion. For each , consider an optimal policy for the discounted cost criterion with the discount factor whose existence follows from Statement (ii). Let with Every sequence is bounded and each limit point defines an average-cost optimal policy.

As explained above, policies may not be optimal for finite-horizon problems for all discount factors and may not be optimal for infinite-horizon discounted problems with a small discount factor. Let us consider the assumption on the growth of backordering costs, that was probably introduced by Veinott and Wagner [63] for problems with discrete demand. This assumption ensures that the functions and are inf-compact, and, as explained above, this implies the optimality of policies and policies for finite-horizon and infinite-horizon discounted problems respectively for all and for all

Assumption GB. There exist such that and

| (29) |

Lemma 4.5

The following theorem describes the optimality of policies and policies for finite-horizon and infinite-horizon discounted problems under Assumption GB.

Theorem 4.6

(i) For and consider real numbers satisfying (27) and defined in (28) with Then for every the policy, is an optimal policy for the -horizon problem with the zero terminal values.

(ii) Let Consider real numbers satisfying (27) and defined in (28) for Then the policy is optimal for the infinite-horizon problem with the discount factor Furthermore, a sequence of pairs considered in statement (i) is bounded, and, if is a limit point of this sequence, then the policy is optimal for the infinite-horizon problem with the discount factor

As stated in Theorem 4.4, -policies are optimal for average costs per unit time. However, Theorem 4.6 states the optimality of policies and policies for finite-horizon and infinite-horizon discounted problems for all discount factors only under Assumption GB. The structure of discount optimal policies for all discount factors is investigated in Feinberg and Liang [36], where the following parameters were introduced:

| (30) |

and

| (31) |

For example, for models with linear holding and bacordering costs considered in [5, 11], when

where and are positive holding and backordering cost rates, and typically

The convexity and inf-compactness of imply that . Therefore, . In addition, Assumption GB is equivalent to . In addition, is the minimal possible value of the parameter whose existence is claimed in Lemma 4.3. These facts and their corollaries are summarized in the following theorem.

Theorem 4.7

Define and

| (32) |

Then for all

Define the following function for all and

| (33) |

Observe that Since is a convex function, then the function is convex for all and

Let and

| (34) |

where the infimum of an empty set is . Since the function is non-negative, then the function is non-decreasing in for all and Therefore, (i) is non-increasing in , that is, , if and (ii) in view of the definition of , for each

| (35) |

The following theorem provides the complete description of optimal finite-horizon policies for all discount factors

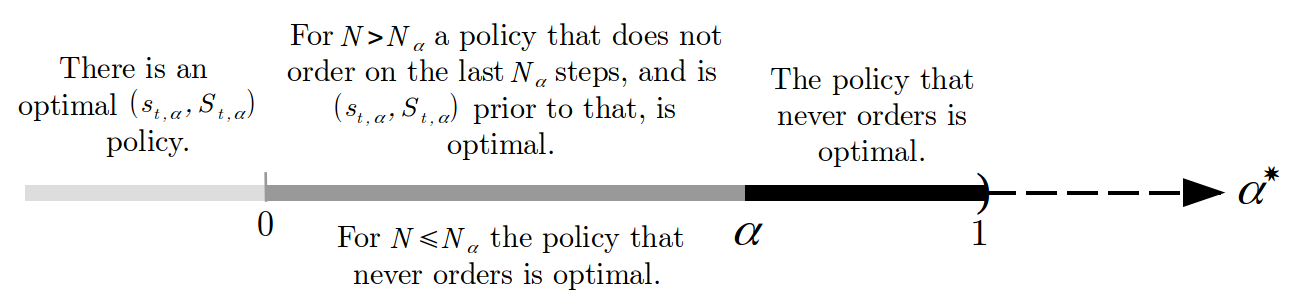

Theorem 4.8

| There is | For the natural number defined in (34), | The policy | |

| an optimal | if then a policy that never orders at | that never | |

| steps and is an | orders is | ||

| policy. | policy at steps is optimal; | optimal. | |

| if then a policy that never orders is | |||

| optimal. |

The following theorem provides the complete description of optimal infinite-horizon policies for all discount factors

Theorem 4.9

([36]). Let Consider defined in (31). The following statements hold for the infinite-horizon problem with the discount factor

(i) if then an policy is optimal, where the real numbers satisfy (27) and are defined in (28) with Furthermore, a sequence of pairs considered in Theorem 4.8 (ii,b) is bounded, and, for if is a limit point of the sequence, then the policy is optimal for the infinite-horizon problem with the discount factor

(ii) if then the policy that never orders is optimal.

| There is an optimal | The policy that never | |

| policy. | orders is optimal. |

The above theorems describe stationary optimal policies for all discount factors. However, it is possible that for a given discount factor at some states there are multiple optimal actions. Therefore, there may exist multiple stationary optimal policies. It is also possible to describe all stationary optimal policies; Feinberg and Liang [36]. The results on MDPs imply that the functions and are lower semi-continuous. However, for this problem they are continuous; Feinberg and Liang [36]. In addition, optimality inequalities (10) and (23) hold in the form of equalities; Feinberg and Liang [35].

5 MDPs with Infinite State Spaces and Weakly Continuous Transition Probabilities

This section describes the theory of dynamic programming for infinite-state problems with weakly continuous transition probabilities. The main focus is on the existence of optimal policies and the validity of optimality equations for problems with discounted costs and optimality inequalities for average-cost problems. We also discuss the convergence of optimal values and actions when the horizon length tends to infinity for finite horizon problems and when the discount factor increases to 1 for infinite horizon problems.

5.1 Total Discounted Costs

The following theorem describes the validity of optimality equalities, the lower semi-continuity of value functions and the convergence of value iterations. For zero terminal values, this theorem is presented in Feinberg et al. [27]. The case of nonzero terminal values is added in Feinberg and Lewis [34]. The case of inf-compact cost functions which leads to the inf-compactess of value functions, is studied in Feinberg and Lewis [33]. The inf-compactness of value functions is important for the analysis of average-cost problems. The proof of Theorem 5.1 uses the generalization of Berge’s theorem described in Appendix.

Theorem 5.1

([27, 34]). Let Assumption W* hold. Consider a bounded below, lower semi-continuous function and Then:

-

(i)

the functions , are lower semi-continuous;

-

(ii)

the finite-horizon optimality equalities (6) hold with for all and the nonempty sets

satisfy the following properties:

-

(a)

the graph , is a Borel subset of , and

-

(b)

if , then and, if , then is compact;

-

(a)

-

(iii)

for a problem with the terminal value function for each , there exists a Markov optimal -horizon policy and if, for an -horizon Markov policy the inclusions , hold then this policy is -horizon optimal;

-

(iv)

if the cost function is inf-compact, the functions are inf-compact.

-

(v)

for if is constant or for all then as for all

-

(vi)

for the infinite-horizon optimality equation (7) holds and the nonempty sets

satisfy the following properties:

-

(a)

the graph is a Borel subset of , and

-

(b)

if , then and, if , then is compact.

-

(a)

-

(vii)

for an infinite-horizon problem with there exists a stationary discount-optimal policy , and a stationary policy is optimal if and only if for all

-

(viii)

if the cost function is inf-compact, then the infinite-horizon value function is inf-compact,

The following theorem describes convergence properties of optimal finite-horizon actions as the time horizon increases to infinity.

Theorem 5.2

([34].) Let Assumption W* hold and Let be bounded below, lower semi-continuous, and such that for all

| (36) |

Then for such that the following two statements hold:

-

(i)

there is a compact subset of such that for all where the sets are defined in Theorem 5.1(ii);

-

(ii)

each sequence is bounded, and all its limit points belong to

Theorem 5.2 is useful for the analysis of the classic periodic-review inventory problem described in Section 4. As demonstrated in Table 1, policies may not be optimal for finite horizon problems, and the function is used to approximate optimal infinite-horizon thresholds, where is the optimal value in the same problem with zero ordering costs.

5.2 Average Costs per Unit Time

We start with the formal introduction of Assumption B.

Assumption B. The following conditions hold:

(i)

(ii) for all

Recall that the functions and are defined only for Let us set

| (37) |

In words, is the largest number such that for all sequences and

Theorem 5.3

(Feinberg et al. [27, Theorem 3]). Suppose Assumptions W* and B hold. Then there exists a stationary policy satisfying (11) with defined in (37). Thus, equalities (12) hold for this policy Furthermore, the following statements hold:

-

(i)

the function is lower semi-continuous;

-

(ii)

the nonempty sets

(38) satisfy the following properties:

-

(a)

the graph is a Borel subset of ;

-

(b)

for each the set is compact;

-

(a)

- (iii)

-

(iv)

there exists a stationary policy with for all , where

(39) -

(v)

if, in addition, the function is inf-compact, then the function is inf-compact.

Stronger results hold under Assumption B.

Theorem 5.4

(Feinberg et al. [27, Theorem 4]). Suppose Assumptions W* and B hold. Then there exists a nonnegative lower semi-continuous function and a stationary policy satisfying (10), that is, for all . Furthermore, every stationary policy , for which (10) holds, is optimal for the average costs per unit time criterion,

| (40) |

Moreover, the following statements hold:

-

(i)

the nonempty sets , satisfy the following properties:

-

(a)

the graph is a Borel subset of ;

-

(b)

for each the set is compact;

-

(a)

-

(ii)

there exists a stationary policy with for all

Alternatively to (37), as follows from Feinberg et al. [27, Theorems 3,4 and p. 603], for each sequence the function can be defined as

| (41) |

In words, is the largest number such that for all sequences It follows from these definitions that However, the questions, whether and whether the values of depend on a particular choice of the sequence has not been investigated. If the cost function is inf-compact, then the functions and are inf-compact as well; see Theorem 5.1 for the proof of this fact for and Feinberg et al. [27, Theorem 4(e) and Corollary 2] for and . We denote by the sets defined in (37), when the function is replaced with

In addition, if the one-step cost function is inf-compact, the minima of the functions possess additional properties. Set

| (42) |

In view of Theorem 5.1(viii), the function is inf-compact and Since this set is closed. The following fact is useful for verifying the validity of Assumption B(ii) in inventory control applications; see Feinberg and Lewis [33, Lemma 5.1] and the references therein.

Theorem 5.5

(Feinberg et al. [27, Theorem 6]). Let Assumptions W* and B(i) hold. If the function is inf-compact, then there exists a compact set such that for all

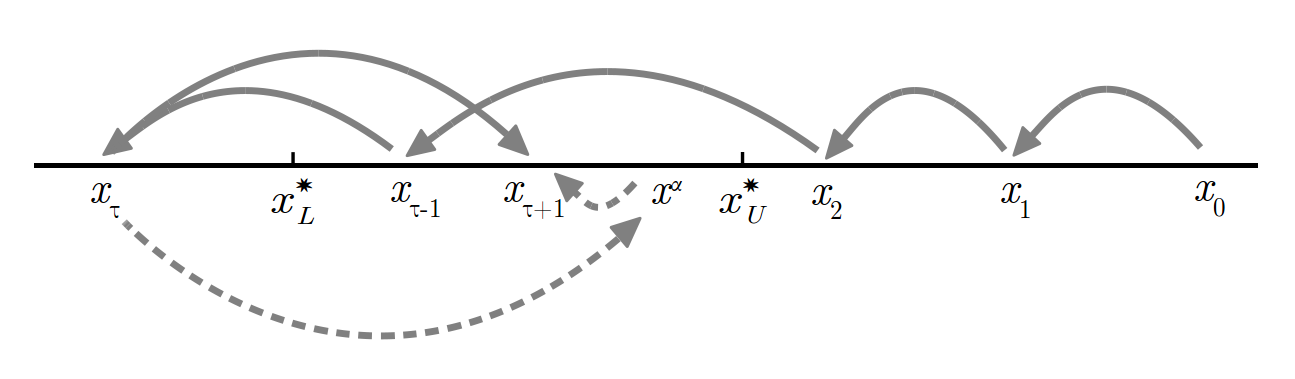

Theorem (5.5) implies that the minimum in of is achieved on a compact set which does not depend on This typically means that to prove Assumption B(ii) it is sufficient to show that for each it is possible to reach every point in in a way that the expected time and cost are finite. In inventory control applications this can be shown by lowering the inventory levels below the levels in and then by ordering up to a point in Exact mathematical justifications are usually problem-specific and use renewal theory. Here we provide a short version of the proof from Feinberg and Lewis [34]. Choose see Figure 3, where the existence of a set is stated in Theorem 5.5, and this set can be chosen to be equal to a closed interval because each compact subset of is contained in a closed finite interval. Let be a stationary optimal policy for a discount factor and be a state such that Since then Consider a policy such that, if the initial point then orders up to the level that the policy would order at state and then makes the same decisions as Since a move from state to can be presented as two instant moves: from to and from to as shown on Figure 3, then

| (43) |

For the initial inventory level the policy is defined in the following way. It does not order as long as the inventory level is greater than or equal to Then, as soon as the inventory level is less than the policy behaves in the same way as if it would behave if were the starting point, where is the first epoch when the inventory level is less than Standard arguments from renewal theory imply that and where is the expected total undiscounted holding (or backordering) cost paid until the system reaches the level Then

| (44) |

Inequalities (43) and (44) imply that Assumption B(ii) holds. Though the above proof was applied in [34] to the classic periodic review system with backorders, it is generic and applicable to other systems. For problems with lost sales the proof may be even simpler because it may be possible to define so that is the first time when there is no inventory. Then and the expected cost of a lost sale will be added to the right hand side of (43). This expected cost is typically finite.

Certain average cost optimal policies can be approximated by discount optimal policies with vanishing discount factor; see Feinberg et al. [27, Theorem 5]. The following theorem and its corollary follow from such approximations. In particular, the theorem and its corollary are useful for verifying that a limit point of optimal thresholds for vanishing discount factors is an optimal threshold for average costs per unit time.

Recall that, for the function defined in (37), for each there exist sequences and where such that Similarly, for a sequence consider the function defined in (41). Then for each there exist a sequence of points in and a subsequence of the sequence such that

Theorem 5.6

([34]). Let Assumptions W* and B hold. For and the following two statements hold:

-

(i)

for a sequence with and as if there are a sequence of natural numbers and actions such that as then where the function is defined in (37);

-

(ii)

let be a sequence of discount factors, be its subsequence, and be a sequence of states from such that as where the function is defined in (41) for the sequence If there are actions such that as then

Corollary 5.7

([34]). Let Assumptions W* and B hold. For and the following two statements hold:

-

(i)

if each sequence with and contains a subsequence such that there exist actions satisfying as then with the function defined in (37);

-

(ii)

if there is a sequence such that for every sequence of states from there are actions satisfying as then where the function is defined in (41) for the sequence

The following theorem is useful for proving asymptotic properties of optimal actions for discounted problems when the discount factor tends to 1.

Theorem 5.8

([34]). Let Assumptions W* and B hold. For the following two statements hold:

-

(i)

there exists a compact set such that for all

-

(ii)

if is a sequence of discount factors then every sequence of infinite-horizon -optimal actions is bounded and therefore has a limit point

6 Partially Observable Markov Decision Processes

POMDPs model the situations, when the current state of the system may be unknown, and the decision maker uses indirect observations for decision making. A POMDP is defined by the same objects as an MDP, but in addition to the state space and action space The states and observations are linked by the transition probability from to Thus, a POMDP is defined as the tuple where the Borel state and action spaces and the transition probability and the cost function are the same objects as in an MDP. In addition, is the observation space, which is also assumed to be a Borel subset of a Polish space, and is the observation probability, which is a regular transition probability from to Sometimes we say a transition kernel or a stochastic kernel instead of transition probability. Though the initial state of the system may be unknown, the decision maker knows the probability distribution of the initial state and there is an observation probability for the first observation

In various applications it is possible that there are continuous states and discrete observations, discrete states and continuous observations, and both spaces can be discrete or continuous. So, we consider a general situation by assuming that and are Borel subsets of Polish spaces.

The following subsection describes a classic transformation of a POMDP to a Completely Observable MDP (COMDP), whose states are posterior probability distributions of states in the POMDP. This transformation was introduced by Aoki [1], Åström [2], Dynkin [21], and Shiryaev [59]. These ideas were advanced in the book by Striebel [61] and in the references provided in the following subsection. The main results of this section describe optimality conditions for POMDPs and COMDPs introduced in Feinberg et al. [32].

The POMDP evolves as follows. At time , the initial unobservable state has a given prior distribution The initial observation is generated according to the initial observation kernel At each time epoch if the state of the system is and the decision-maker chooses an action , then the cost is incurred; the system moves to state according to the transition law The observation is generated by the observation kernels , and see Figure 4. For the state space , denote by the set of probability measures on We always consider a metric on consistent with the topology of weak convergence.

Define the observable histories: and for all where and if Then a policy for the POMDP is defined as a sequence such that, for each is a transition kernel on given . Moreover, is called nonrandomized, if each probability measure is concentrated at one point. The set of all policies is denoted by . The Ionescu Tulcea theorem (Bertsekas and Shreve [12, pp. 140-141] or Hernández-Lerma and Lassere [41, p.178]) implies that, given a policy an initial distribution and a sequence of transition probabilities determine a unique probability measure on the set of all trajectories endowed with the -field, which is the product of Borel -fields on , , and respectively. The expectation with respect to this probability measure is denoted by .

Let us specify a performance criterion. For a finite horizon and for a policy , let the expected total discounted costs be

| (45) |

where is the discount factor, and When , we always assume We always assume that the function is bounded below.

For any function , including and define the optimal cost

where is the set of all policies. A policy is called optimal for the respective criterion, if for all For , the optimal policy is called -horizon discount-optimal; for , it is called discount-optimal.

6.1 Reduction of POMDPs to MDPs

In this section, we formulate the well-known reduction of a POMDP to the corresponding COMDP ([12, 22, 38, 49, 64]). This reduction constructs an MDP whose states are probability distributions on the original state space. These distributions are posteriori distributions of states after the observations become known. In addition to posterior probabilities, they are also called belief probabilities and belief states in the literature. The reduction establishes the correspondence between certain classes of policies in MDPs and POMDPs and their performances. If an optimal policy is found for the COMDP, it defines in a natural way an optimal policy for the original POMDP. The reduction holds for measurable transition probabilities, observation probabilities, and one-step costs. Except for problems with discrete transition probabilities or with transition probabilities having densities (see [3, 4]), almost nothing had been known until recently on the existence of optimal policies for POMDPs and how to find them.

To simplify notations, we sometimes drop the time parameter. Given a posterior distribution of the state at time epoch and given an action selected at epoch , denote by the joint probability that the state at time belongs to the set and the observation at time belongs to the set ,

| (46) |

where is a transition kernel on given ; see Bertsekas and Shreve [12], Dynkin and Yushkevich [22], Hernández-Lerma [38], or Yushkevich [64] for details. Therefore, the probability that the observation at time belongs to the set is

| (47) |

where is a transition kernel on given By Bertsekas and Shreve [12, Proposition 7.27], there exists a transition kernel on given such that

| (48) |

The transition kernel defines a measurable mapping , where For each pair , the mapping is defined -a.s. uniquely in ; Dynkin and Yushkevich [22, p. 309]. It is known that for a posterior distribution , action , and an observation the posterior distribution is

| (49) |

However, the observation is not available in the COMDP model, and therefore is a random variable with the distribution , and (49) is a stochastic equation that maps to The stochastic kernel that defines the distribution of on given is defined uniquely as

| (50) |

where for

Hernández-Lerma [38, p. 87]. The measurable particular choice of stochastic kernel from (48) does not affect on the definition of from (50), since for each pair , the mapping is defined -a.s. uniquely in ; Dynkin and Yushkevich [22, p. 309].

The COMDP is defined as an MDP with parameters (,,,), where

-

(i)

is the state space;

-

(ii)

is the action set available at all states ;

-

(iii)

the one-step cost function , defined as

(51) -

(iv)

the transition probabilities on given defined in (50).

If a stationary optimal policy for the COMDP exists and is found, it allows the decision maker to formulate an optimal policy for the POMDP. The details on how to do this can be found in Bertsekas and Shreve [12] or Dynkin and Yushkevich [22], or Hernández-Lerma [38]. Therefore, a POMDP can be reduced to a COMDP. This reduction holds for measurable transition kernels , , . The measurability of these kernels and the cost function lead to the measurability of transition probabilities for the corresponding COMDP.

As follows from Theorem 5.1, if the COMDP satisfies Assumption W*, then optimal policies exist, they satisfy the optimality equation, and can be found by value iterations. This is formulated in Theorem 6.2 below. The validity of Assumption W* for the COMDP is equivalent to the correctness of the following two Hypotheses:

Hypothesis (i). The transition probability from to is weakly continuous.

Hypothesis (ii). The cost function is bounded below and -inf-compact on

Following theorem states the correctness of Hypothesis (ii). The question, whether Hypothesis (i) holds, a more difficult, and the the following subsection is devoted to answering it.

Theorem 6.1

In addition to weak convergence, two types of convergence are mentioned in the next subsection: setwise convergence and convergence in total variation. Here we recall their definitions.

Let be a sequence of probability measures on a measurable space . This sequence converges setwise to a probability measure on if for each This sequence converges in total variation if where Convergence in total variation implies setwise convergence. If is a metric space and is its Borel -field, then setwise convergence implies weak convergence. Recall that is a regular transition probability from a metric space to a metric space if is a probability measure on for each and is a Borel function on for each Borel subset of A transition probability is weakly (setwise, in total variation) continuous, if, for every sequence on converging to the sequence converges weakly (setwise, in total variation) to There are two mathematical tools that are useful for the analysis of convergence of probability measures and for the analysis of MDPs and POMDPs: Fatou’s lemma for variable probabilities (see Feinberg et al. [29] and references therein) and uniform Fatou’s lemma introduced in Feinberg et al. [31].

6.2 Optimality Conditions for Discounted POMDPs

For the COMDP, Assumption W* can be rewritten in the following form:

(i) is -inf-compact on ;

(ii) the transition probability is weakly continuous in .

Theorem 5.1 has the following form for the COMDP :

Theorem 6.2

(cf. Feinberg et al. [27, Theorem 2]). Let the COMDP satisfy Assumption W*. Then:

(i) the functions , , and are lower semi-continuous on , and as for all

(ii) for any , and

| (52) | ||||

where for all , and the nonempty sets

where , satisfy the following properties: (a) the graph , is a Borel subset of , and (b) if , then and, if , then is compact;

(iii) for any , there exists a Markov optimal -horizon policy for the COMDP, and if for an -horizon Markov policy the inclusions , hold, then this policy is -horizon optimal;

(iv) for

and the nonempty sets

satisfy the following properties: (a) the graph is a Borel subset of , and (b) if , then and, if , then is compact.

(v) for an infinite horizon there exists a stationary discount-optimal policy for the COMDP, and a stationary policy is optimal if and only if for all

(vi) if the function is inf-compact, the functions , , and are inf-compact on .

Hernández-Lerma [38, Section 4.4] provided the following conditions for the existence of optimal policies for the COMDP: (a) is compact, (b) the cost function is bounded and continuous, (c) the transition probability and the observation kernel are weakly continuous transition kernels; (d) there exists a weakly continuous satisfying (48). Consider the following relaxed version of assumption (d).

Assumption H. ([32]). There exists a transition kernel on given satisfying (48) such that: if a sequence converges weakly to , and converges to , , then there exists a subsequence such that

and this convergence takes place almost surely in .

The following theorem provides two sufficient conditions for weak continuity of Statement (ii) can be found in Hernandez-Lerma [38, p. 90].

Theorem 6.3

([32]). If the transition probability is weakly continuous, then each of the following two conditions implies weak continuity of the transition probability from to

-

(i)

the transition probability from to is setwise continuous, and Assumption H holds,

-

(ii)

the transition probability from to is weakly continuous, and there exists a weakly continuous satisfying (48).

Weak continuity of the transition probability and continuity of the transition probability in total variation imply that Assumption H holds, and this leads to the following theorem.

Theorem 6.4

([32]). Let the transition probability from to be weakly continuous and let the transition probability from to be continuous in total variation. Then the transition probability from to is setwise continuous, Assumption H holds, and the transition probability from to is weakly continuous.

The following theorem, which follows from Theorems 6.1–6.3, relaxes assumptions (a), (b), and (d) in Hernández-Lerma [38, Section 4.4].

Theorem 6.5

([32]). Under the following conditions:

-

(a)

the cost function is -inf-compact;

-

(b)

either

-

(i)

the transition probability from to is setwise continuous and Assumption H holds,

or

-

(ii)

the transition probability from to is weakly continuous and there exists a weakly continuous satisfying (48);

-

(i)

the COMDP satisfies Assumption W* and therefore statements (i)–(vi) of Theorem 6.2 hold.

Theorem 6.6

Theorem 6.5 assumes either the weak continuity of or Assumption H together with the setwise continuity of . For some applications, including the inventory control applications described in Section 7, the filtering kernel satisfies Assumption H for some observations and it is weakly continuous for other observations. The following theorem is applicable to such situations.

Theorem 6.7

([32]). Let the observation space be partitioned into two disjoint subsets and such that is open in . Suppose the following assumptions hold:

(a) the transition probabilities to from to and from to are weakly continuous;

(b) the measure on is setwise continuous in that is, for every sequence in converging to and for every we have

(c) there exists a transition probability from to satisfying (48) such that:

-

(i)

the transition probability from to is weakly continuous;

-

(ii)

Assumption H holds on that is, if a sequence converges weakly to and a sequence converges to , then there exists a subsequence and a measurable subset of such that and converges weakly to for all ;

Then the transition probability from to is weakly continuous. If, in addition to the above conditions, the cost function is -inf-compact, then the COMDP satisfies Assumption W* and therefore statements (i)–(vi) of Theorem 6.2 hold.

The following corollary follows from Theorem 6.7.

Corollary 6.8

([32]). Let the observation space be partitioned into two disjoint subsets and such that is open in and is countable. Suppose the following assumptions hold:

(a) the transition probabilities from to and from to are weakly continuous;

(b) is a continuous function on for each

(c) there exists a stochastic kernel on given

satisfying (48) such that the

stochastic kernel on given is

weakly continuous.

Then assumption (b) and (ii) from Theorem 6.7 hold and

the transition probability from to is

weakly continuous. If, in addition to the above conditions,

the cost function is -inf-compact, then the COMDP

satisfies Assumption W*

and therefore statements (i)–(vi) of Theorem 6.2 hold.

In conclusion of this section, we would like to mention another model of a controlled Markov process with partial observations, in which the observation kernel is not defined explicitly, and a state of the system consists of two parts: one part of the state is observable and another one is not; see e.g., Rhenius [49], Yushkevich[64], Bäuerle and Rieder[3, Chapter 5]. In Feinberg et al. [30, 32] such models were called Markov Decision Models with Incomplete Information, and the most general known sufficient conditions for the existence of optimal policies for such models with the expected total costs are provided in Feinberg et al [30, Theorem 6.2].

7 Inventory Control with Incomplete Information

Bensoussan et al. [6]–[9] studied several inventory control problems for periodic review systems, when the Inventory Manager (IM) may not have complete information about inventory levels. In Bensoussan et al. [6], [9], a problem with backorders is considered. In the model considered in [6], the IM does not know the inventory level, if it is nonnegative, and the IM knows the inventory level, if it is negative. In the model considered in [9], the IM only knows whether the inventory level is negative or nonnegative. In [7] a problem with lost sales is studied where the IM only knows whether a lost sale happened or not. The underlying mathematical analysis is summarized in [8], where additional references can be found. The analysis includes transformations of density functions of demand distributions.

This section describes periodic review systems with backorders and lost sales, when some inventory levels are observable and some are not. The goal is to minimize the expected total costs. Demand distributions may not have densities. This model is introduced in Feinberg et al. [32, Section 8.2].

In the case of full observations, we model the problem as an MDP with the state space (the current inventory level), action space (the ordered amount of inventory), and action sets available at states . If in a state the amount of inventory is ordered, then the holding/backordering cost , ordering cost and lost sale cost are incurred, where it is assumed that and are nonnegative lower semi-continuous functions with values in and as Observe that the one-step cost function is -inf-compact on . For problems with back orders (no lost sales), usually for all and

Let be i.i.d. random variables with the distribution function , where is the demand at epoch The dynamics of the system are defined by where is the current inventory level and is the ordered (or scrapped) inventory at epoch For problems with backorders and for problems with lost sales . In both cases, is a continuous function defined on . To simplify and unify the presentation, we do not assume for models with lost sales. However, for problems with lost sales it is assumed that the initial state distribution is concentrated on , and this implies that states will never be visited. We assume that the distribution function is atomless (an equivalent assumption is that the function is continuous). The state transition law on given is

| (53) |

where and Since we do not assume that demands are nonnegative, this model also covers cash balancing problems and problems with returns; see Feinberg and Lewis [33] and the references therein. In a particular case, when for , orders with negative sizes are infeasible, and, if an order is placed, the ordered amount of inventory should be positive.

As mentioned above, some states (inventory levels) are observable and some are not. Let the inventory be stored in containers. From a mathematical perspective, containers are elements of a finite or countably infinite partition of into disjoint convex sets, and each of these sets is not a singleton. In other words, each container is an interval (possibly open, closed, or semi-open) with ends and such that , and the union of these disjoint intervals is In addition, we assume that for some constant for all containers, that is, the sizes of all the containers are uniformly bounded below by a positive number. We also follow the convention that the 0-inventory level belongs to a container with end points and , and a container with end points and is labeled as the -th container . Thus, container is the interval in the partition containing point 0. The containers’ labels can be nonpositive. If there is a container with the smallest (or largest) finite label then (or , respectively). If there are containers with labels and then there are containers with all the labels between and . In addition each container is either transparent or nontransparent. If the inventory level belongs to a nontransparent container, the IM only knows which container the inventory level belongs to. If an inventory level belongs to a transparent container, the IM knows that the amount of inventory is exactly see Figures 5–8.

For each nontransparent container with end points and , we fix an arbitrary point satisfying . For example, it is possible to set when If an inventory level belongs to a nontransparent container , the IM observes Let be the set of labels of the nontransparent containers. We set and define the observation set , where is the union of all transparent containers (transparent elements of the partition). If the observation belongs to a transparent container (in this case, ), then the IM knows that the inventory level . If (in this case, for some ), then the IM knows that the inventory level belongs to the container , and this container is nontransparent. Of course, the distribution of this level can be computed.

Let be the Euclidean distance on for . On the state space we consider the metric if and belong to the same container, and otherwise, where . The space is a Borel subset of a Polish space (consisting of closed containers, that is, each finite point is represented by two points: one belonging to the container and another one to the container ). We notice that as if and only if as and the sequence belongs to the same container as for a sufficiently large . Thus, convergence on in the metric implies convergence in the Euclidean metric. In addition, if for all containers , then as if and only if as Therefore, for any open set in , the set is open in We notice that each container is an open and closed set in

It is possible to show that the state transition law given by (53) is weakly continuous in . Set if the inventory level belongs to a transparent container, and if the inventory level belongs to a nontransparent container with a label . As follows from the definition of the metric , the function is continuous. Therefore, the observation transition probabilities from to and from to , , , , are weakly continuous.

If all the containers are nontransparent, the observation set is countable, and conditions of Corollary 6.8 hold. In particular, the function is continuous, if the metric is considered on If some containers are transparent and some are not, the conditions of Corollary 6.8 hold. To verify this, we set and and note that is countable and the function is continuous for each because is open and closed in Note that for any , , , , and . The kernel is weakly continuous on . In addition, , where are transparent containers, is an open set in Thus the POMDP (, , , , , ) satisfies the assumptions of Corollary 6.8. Thus, for the corresponding COMDP, there are stationary optimal policies, optimal policies satisfy the optimality equations, and value iterations converge to the optimal value.

The models studied in Bensoussan et al. [6, 7, 9] correspond to the partition and with the container being nontransparent and with the container being either nontransparent (backordered amounts are not known [9]) or transparent (models with lost sales [7], backorders are observable [6]). Note that, since is atomless, the probability that is ,

The model provided in this subsection is applicable to other inventory control problems, and the conclusions of Corollary 6.8 hold for them too. For example, consider a periodic review inventory system with backorders, for which nonnegative inventory levels are known, and, when the inventory level is negative, it is known that there is a backorder, but its quantity is unknown. The partition consists of two containers: a nontransparent container and a transparent container

8 Conclusions

The tutorial describes general sufficient conditions for the existence and characterization of optimal policies for Markov Decision Processes with possibly infinite state spaces and unbounded action sets and costs. Expected total discounted cost and average cost criteria are considered. The described conditions imply the existence of optimal Markov policies in finite-horizon problems and the existence of optimal stationary policies for infinite-horizon problems. They imply the validity of optimality equations, convergence of value iterations, and continuity properties of value functions for discounted costs. They also imply the validity of optimality inequalities for average costs per unit time.

For discounted costs, these conditions consist of two assumptions: the transition probabilities are weakly continuous, and the one-step cost function is -inf-compact. These two assumptions practically always hold for periodic-review stochastic inventory control problems. The -inf-compactness property of one-step costs is weaker than inf-compactness, which typically holds for cost functions for inventory control problems. One of the reasons for the generality of the results is that their derivation is linked to a new maximum theorem, which extends Berge’s maximum theorem to possibly noncompact action sets.

For average cost MDPs, the single additional assumption is that the relative value function is well-defined. This assumption also holds for inventory control applications and can be verified easily.

The tutorial also describes optimality conditions for Partially Observable Markov Decision Processes with total discounted costs. These conditions imply the existence of optimal policies, validity of optimality equations, and convergence of value iterations. The results are illustrated with inventory control models for which some of the inventory levels are not observable.

The described results and methods are useful and insightful for investigating new and existing inventory control problems. As an illustration, a complete classification of possible solutions for the classic periodic-review stochastic single-product problem is described.

Appendix

9 Berge’s Maximum Theorem for Noncompact Action Sets and Some Properties of -Inf-Compact Functions

This appendix describes generalizations of Berge’s maximum theorem and the relevant Berge theorem on semi-continuity of the value function to possibly noncompact action sets. These theorems are important for control theory, games, and mathematical economics. The major limitation of these theorems is that they require compact action sets. The generalizations provided in Feinberg et al., [26, 28] remove this limitation. Here we present these results for metric spaces. With slight modifications they hold for Hausdorff topological spaces (see [26]), but this level of generality is not needed for the results of this tutorial. Local versions of the results presented in this appendix can be found in Feinberg and Kasyanov [25].

Let and be metric spaces, and . Consider an optimization problem of the form

| (54) |

which appears, for instance, in optimal control and game theory.

Let be the set of nonempty compact subsets of Berge’s theorem has the following formulation.

Berge’s Theorem. ([10, p. 116]). If is a lower semi-continuous function and is an upper semi-continuous set-valued mapping, then the function is lower semi-continuous.

The well-known Berge’s maximum

theorem

has the following formulation.

Berge’s Maximum Theorem. ([10, p. 116]). If

is a continuous function and

is a continuous set-valued

mapping, then the value function is continuous and

the solution multifunction , defined as

| (55) |

is upper semi-continuous and compact-valued.

For an -valued function , defined on a nonempty subset of a topological space consider the level sets

We recall that a function is lower semi-continuous on if all the level sets are closed, and a function is inf-compact (also sometimes called lower semi-compact) on if all these sets are compact. The following definition deals with the space and its subsets and

Definition 9.1

([28, Definition 1.1]). A function is called -inf-compact on , if for every compact subset of this function is inf-compact on .

The following two theorems generalize Berge’s theorem and Berge’s maximum theorem respectively to possibly noncompact action sets.

Theorem 9.2

([28, Theorem 1.2]). If the function is -inf-compact on , then the function is lower semi-continuous.

Theorem 9.3

([26, Theorem 1.2]). Assume that:

-

(a)

is lower semi-continuous;

-

(b)

is -inf-compact and upper semi-continuous on .

Then the value function is continuous and the solution multifunction is upper semi-continuous and compact-valued.

The first statement of the following lemma implies that Theorems 9.2 and 9.3 are indeed generalizations of Berge’s theorem and Berge’s maximum theorem respectively. The second statement indicates that the class of -inf-compact functions is broader than the class of inf-compact functions.

Lemma 9.4

([28, Lemma 2.1]). The following statements hold:

(i) if is lower semi-continuous on and is upper semi-continuous, then the function is -inf-compact on ;

(ii) if is inf-compact on , then the function is -inf-compact on .

Luque-Vásquez and Hernández-Lerma [46] provided an example with continuous and continuous which is inf-compact in where is not lower semi-continuous. The following two lemmas indicate that -inf-compactness of is stronger than its lower-semicontinuity and inf-compactness in

Lemma 9.5

([28, Lemma 2.2]). If is -inf-compact function on , then for every the function is inf-compact on .

Lemma 9.6

([28, Lemma 2.3]). A -inf-compact function on is lower semi-continuous on .

The following lemma provides the necessary and sufficient condition for -inf-compactness. This condition is used in Assumption W* in Feinberg et al, [27] instead of equivalent Definition A.1.

Lemma 9.7

([28, Lemma 2.5]). The function is -inf-compact on if and only if the following two conditions hold:

(i) is lower semi-continuous on ;

(ii) if a sequence with values in converges and its limit belongs to then any sequence with , satisfying the condition that the sequence is bounded above, has a limit point

Acknowledgement Some of the materials presented in this tutorial are based on results of work partially supported by NSF grant CMMI-1335296. The author thanks Jefferson Huang, Pavlo O. Kasianov, Mark E. Lewis, Yan Liang, and Matthew J. Sobel for valuable comments.

References

- [1] M. Aoki. Optimal control of partially observable Markovian systems. J. Franklin Inst., 280:367–386, 1965.

- [2] K. J. Astrom. Optimal control of Markov decision processes with incomplete state estimation. J. Math. Anal. Appl., 10(1):174–205, 1965.

- [3] N. Bäuerle and U. Rieder. Markov Decision Processes with Applications to Finance. Springer, New York, 2011.

- [4] A. Bensoussan. Stochastic Control of Partially Observable Systems. Cambridge University Press, Cambridge, 1992.

- [5] A. Bensoussan. Dynamic Programming and Inventory Control. IOS Press, Amsterdam, 2011.

- [6] A. Bensoussan, M. Cakanyildirim, J. A. Minjárez-Sosa, and S. P. Sethi. Partially observed inventory systems: the case of rain checks. SIAM J. Control Optim., 47(5):2490–2519, 2008.

- [7] A. Bensoussan, M. Cakanyildirim, and S. P. Sethi. Partially observed inventory systems: the case of zero balance walk. SIAM J. Control Optim., 46(1):176–209, 2007.

- [8] A. Bensoussan, M. Cakanyildirim, and S. P. Sethi. Filtering for discrete-time Markov processes and applications to inventory control with incomplete information. In D. Crisan and B. Rozovskii, editors, The Oxford Handbook of Nonlinear Filtering, pages 500–525. Oxford University Press, New York, 2011.

- [9] A. Bensoussan, M. Cakanyildirim, S. P. Sethi, and R. Shi. An incomplete information inventory model with presence of inventories or backorders as only observations. Journal of Optimiz. Theory Appl., 146(3):544–580, 2010.

- [10] C. Berge. Topological Spaces. Macmillan, New York, 1963.

- [11] D. P. Bertsekas. Dynamic Programming and Optimal Control. Second Edition, Vol. 1, Athena Scientific, Belmont, MA, 2000.

- [12] D. P. Bertsekas and S. E. Shreve. Stochastic Optimal Control: the Discrete-Time Case. Athena Scientific, Belmont, MA, 1996.