Consistent order estimation for nonparametric Hidden Markov Models

Abstract

We consider the problem of estimating the number of hidden states (the order) of a nonparametric hidden Markov model (HMM). We propose two different methods and prove their almost sure consistency without any prior assumption, be it on the order or on the emission distributions. This is the first time a consistency result is proved in such a general setting without using restrictive assumptions such as a priori upper bounds on the order or parametric restrictions on the emission distributions. Our main method relies on the minimization of a penalized least squares criterion. In addition to the consistency of the order estimation, we also prove that this method yields rate minimax adaptive estimators of the parameters of the HMM - up to a logarithmic factor. Our second method relies on estimating the rank of a matrix obtained from the distribution of two consecutive observations. Finally, numerical experiments are used to compare both methods and study their ability to select the right order in several situations.

keywords:

[class=MSC]keywords:

journalname

1 Introduction

1.1 Context and motivation

Hidden Markov models (HMM in short) are powerful tools to study time-evolving processes on heterogeneous populations. Nonparametric HMMs–that is, hidden Markov models where the parameters are not restricted to a finite-dimensional space–have proved useful in a wide range of applications, see for instance Couvreur and Couvreur (2000) for voice activity detection, Lambert, Whiting and Metcalfe (2003) for climate state identification, Lefèvre (2003) for automatic speech recognition, Shang and Chan (2009) for facial expression recognition, Volant et al. (2014) for methylation comparison of proteins, Yau et al. (2011) for copy number variants identification in DNA analysis.

In practice, the hidden states often have an interpretation in the modelling of the phenomenon. It is thus important to be able to infer the right order in addition to the parameters when dealing with hidden Markov models. However, this task is notoriously difficult: Gassiat and Keribin (2000) show that the likelihood ratio statistic is unbounded even in the simple case where one wants to test if a HMM has 1 or 2 hidden states. As far as we know, no consistency result has been proved about order selection for nonparametric HMMs. Even for parametric HMMs, no estimator has been proved to be consistent in a general setting without assuming that an a priori upper bound on the order is known beforehand.

Not only is the order estimation useful in order to interpret the model, it is also necessary to ensure stability. This is because over estimating the order causes a loss of identifiability: there are several ways to add one state to a HMM without changing anything to its distribution. The spectral estimators (Anandkumar, Hsu and Kakade (2012); de Castro, Gassiat and Le Corff ) are especially sensitive to this problem, as shown by Lehéricy (2015) and Figure 6: as soon as the HMM becomes close to a HMM with fewer hidden states, the estimators give absurd results. Thus, estimating the right order is crucial for such methods to be effective.

Formally, a hidden Markov model is a markovian process taking value in . is a Markov chain and the observations depend only on the associated (i.e. the are independent conditionally on ). The states are assumed to be hidden, so that one has only access to the observations . When the number of hidden states (which we call the order of the HMM) is finite, the model is completely defined by its order, the initial distribution and the transition matrix of the hidden Markov chain, and the possible distributions of an observation conditionally to the values of its hidden state , which we call the emission distributions. The goal of the estimation procedures is to recover these parameters by using only the observations .

Up to now, most theoretical results on hidden Markov models dealt with the parametric frame, that is with a finite number of parameters. However, it is not always possible to restrict the model to such a convenient finite-dimensional space. Theoretical results in the nonparametric framework were only developed recently and do not address the order estimation problem. de Castro, Gassiat and Lacour (2016) propose an adaptive quasi-rate minimax least squares method. de Castro, Gassiat and Le Corff and Robin, Bonhomme and Jochmans (2014) study spectral methods. The latter is also proved to reach the minimax convergence rate but is not adaptive: it requires the regularity of the emission distributions to be known. All these methods require the order of the HMM to be known.

Our work is novel on three points. First, it deals with the nonparametric setting: we need no parametric or regularity assumption on the emission densities. Note that all our results also apply to parametric settings or even to finite observation spaces, since these are just special cases of nonparametric estimation. Secondly, we do not require any a priori upper bound on the order, an assumption that is often made in earlier works, both frequentist and bayesian. Finally, our least squares method yields estimators of all model parameters at the same time, without requiring any prior information. Oracle inequalities show that these estimators are rate minimax adaptive up to a logarithmic factor.

1.2 Related works

The first step to obtain theoretical results was to understand when hidden Markov models are identifiable. This challenging issue was only solved a few years ago, see Gassiat, Cleynen and Robin (2015) (following Allman, Matias and Rhodes (2009) and Hsu, Kakade and Zhang (2012)) and with weaker assumptions Alexandrovich and Holzmann (2014). Both proved that under generic assumptions, the parameters of the HMM can be recovered from the distribution of a finite number of consecutive observations, thus paving the way for guarantees on parameter estimation.

HMM inference is generally decomposed in two parts. The first one is the estimation of the order, and the second one is the estimation of the parameters once the order is known.

From a theoretical point of view, the order estimation problem remains widely open in the HMM framework. One can distinguish two kinds of results. The first kind does not need an a priori upper bound on the order, but is only applicable to restrictive cases. For instance, using tools from coding theory, Gassiat and Boucheron (2003) introduced a penalized maximum likelihood order estimator for which they prove strong consistency without a priori upper bound on the order of the HMM. Nevertheless, their result is restricted to a finite observation space and they have to use heavy penalties that grow as a power of the order. For the special case of Gaussian or Poisson emission distributions, Chambaz, Garivier and Gassiat (2009) showed that the penalized maximum likelihood estimator is strongly consistent without any a priori upper bound on the order. The second kind of results is more general but requires an a priori upper bound of the order just to get weak consistency of order estimators, for penalized likelihood criterion (Gassiat (2002)) as well as Bayesian approaches (Gassiat and Rousseau (2014); van Havre et al. (2016)).

On a practical side, several order estimation methods using penalized likelihood criterion have been studied numerically, see for instance Volant et al. (2014) when emission distributions are a mixture of parametric densities or Celeux and Durand (2008) for parametric HMMs. The latter also introduced cross-validation procedures that aimed for circumventing the lack of independance of the observations. In the case of nonparametric HMMs, Langrock et al. (2015) studied a method using P-splines with a custom penalization.

Then comes the question of estimating the parameters of the HMM once its order is known. In the parametric setting, the asymptotic behaviour of the maximum likelihood estimator is rather well understood (see for instance Bickel et al. (1998) or Douc et al. (2004) using techniques from Le Gland and Mevel (2000)), but so far the question of its nonasymptotic behaviour remains open. Hsu, Kakade and Zhang (2012) and Anandkumar, Hsu and Kakade (2012) proposed a spectral method for parametric HMMs based on joint diagonalization of a set of matrices and controlled its nonasymptotic error. Robin, Bonhomme and Jochmans (2014) and de Castro, Gassiat and Le Corff extended this method to the nonparametric setting, and de Castro, Gassiat and Lacour (2016) used the latter to obtain an estimator of the transition matrix of the hidden chain for a quasi-rate minimax adaptive least squares estimator of the emission densities. Our least squares estimation method is a generalization of their procedure that is able to deal with all parameters at once and does not require auxiliary estimators.

1.3 Contribution

The aim of our paper is twofold. Firstly, we introduce two estimators of the order for nonparametric HMMs and show that both converge almost surely to the right order under minimal assumptions. Secondly, we numerically assess their ability to select the right order and compare their efficiency.

Our first and main method is the penalized least squares estimator. This method is based on estimating the projection of the emission distributions onto a family of nested parametric subspaces. Our results hold for any Hilbert space, including parametric sets of emission densities and finite observation spaces. Then, for each subspace and for each possible value of the order, we look for the HMM with hidden states and with emission distributions in the chosen subspace that matches the observations “best”–where “best” means minimizing the empirical equivalent of an distance. This step provides an empirical distance between the observations and the model, which is then penalized in order to counterbalance the overfitting phenomenon that occurs when considering large models. Our first main result is that for a suitable choice of the penalty, choosing the model (i.e. the order and the subspace) which minimizes this penalized distance leads to a strongly consistent estimator of the order, see Corollary 5.

In addition, this method also provides estimators of the other parameters of the HMM for free, by taking the parameters of the HMM corresponding to the selected model. We prove an oracle inequality on the risk of these estimators, which shows that they achieve the minimax adaptive rate of convergence, up to a logarithmic term, see Theorem 10 and Corollary 11.

Our second estimator comes from spectral methods. Just like for our least squares procedure, we consider a nested family of parametric subspaces of a Hilbert space. Let us choose one of them, and denote by an orthonormal basis of this subspace. Then, consider the matrix defined by

This matrix contains the coordinates of the density of in the orthonormal basis . It is proved in Section 4 that the rank of is exactly equal to the order of the HMM as soon as the subspace is large enough. Therefore, finding its rank means finding the number of hidden states. However, in practice, one only has access to an empirical version of this matrix. The difficulty comes from the fact that this noisy version will almost surely have full rank. Thus, the key point is to recover the order of the true matrix given its empirical (full rank) counterpart. We achieve this by thresholding the spectrum of the empirical matrix.

Notice that other methods exist to estimate the rank of a matrix based on a noisy observation, see for instance Kleibergen and

Paap (2006) and references therein. Unfortunately, most can not be applied directly to our setting since they require an invertibility condition on the covariance matrix of the matrix entries. The CRT statistics from Robin and Smith (2000) is a notable exception, however their test of rank also requires the tuning of an unknown parameter in order to be weakly consistent.

Then, we run an implementation of these two methods and compare their efficiency on simulated data. The difficulty at this stage comes from the fact that both method involve an unknown tuning parameter. This is a common issue that appears in every model selection method in one form or another, and many heuristics have been proposed to circumvent this difficulty.

For the least squares estimator, we compare two methods which have been both proved to be theoretically valid in simple cases and empirically validated in a large variety of situations: the slope heuristics (see for instance Baudry, Maugis and Michel (2012) and references therein) and the dimension jump heuristics (introduced and proved to lead to an optimal penalization in the gaussian model selection framework by Birgé and Massart (2007)). Both behave well with our estimator and lead to a satisfying calibration of the penalty.

For the spectral estimator, we introduce a custom heuristics based on the fact that the smallest singular values of the empirical version of the matrix decrease in a simple manner. It is thus possible to calibrate an entirely data-driven threshold to distinguish “significant” singular values–that is, the ones corresponding to non-zero singular values of the real –from noise.

The numerical validation shows that our least squares method performs well in almost any situation. It is able to select the right order accurately with notably fewer observations than the spectral estimator, and is easier to calibrate. On the other hand, the spectral method is very fast, which allows to take more observations into account. This allows to obtain satisfying estimators in a short amount of time.

Regarding the inference of the other parameters, our least squares estimator offers several advantages when compared to previous methods. First, it does not need a preliminary estimation of the transition matrix or of the order, unlike de Castro, Gassiat and Lacour (2016) who used the transition matrix given by spectral estimators. Nevertheless, our method still reaches the adaptive minimax convergence rate for the estimation of the emission densities, up to a logarithmic factor. This is especially useful to avoid the cases where their auxiliary estimator fails. For instance, the spectral method that de Castro, Gassiat and Lacour (2016) used is unreliable when the order is over estimated or where the states are almost linearly dependent, see for instance Lehéricy (2015) or Figure 6. Then, our least squares method is robust to an overestimation of the order, both theoretically and numerically, thanks to the iterative initialization procedure that we introduce. This initialization method consists in using estimators from smaller models as initial point for the minimization algorithm in order to avoid getting stuck in suboptimal local extrema. We believe it can be of practical interest since it produces robust estimators and can also be used in other settings, for instance as initialization for expectation maximization algorithm for maximum likelihood estimators.

1.4 Outline of the paper

Our paper is organized as follows.

Section 2 is devoted to the notations, the model and the assumptions.

Our main procedure, the penalized least squares method, is introduced in Section 3. We first state an identifiability proposition which we use to prove strong consistency of the estimator of the order. This is done in two steps. Firstly, we control the probability to underestimate the order. This is done thanks to Proposition 1, and gives an exponential bound on the probability of error, see Theorem 3. Secondly, we control the probability to overestimate the order, see Theorem 4. For this, we introduce a general condition on the penalty, which we use to prove polynomial decrease rate, and illustrate how to easily satisfy this condition. Finally, we state oracle inequalities on the estimators of the density of consecutive observations and on the parameters of the hidden Markov model under a generic assumption, see Theorem 10 and Corollary 11, which shows that they reach the minimax convergence rate up to a logarithmic factor.

In Section 4, we introduce the spectral algorithm and propose a strongly consistent estimator of the order. This is done by thresholding the spectrum of the empirical version of the matrix , which describes the projection of the distribution of two observations on an orthonormal basis, see Theorem 13.

In Section 5, we propose practical algorithms to apply both methods and compare them. Firstly, we set the parameters on which we will test both procedures. Secondly, we compare their results and discuss their performance. Lastly, we introduce and discuss the heuristics we used to practically implement both methods.

Our main technical result, Lemma 16, can be found at the beginning of Section 6. It is used extensively for both the consistency of the estimator of the order and the oracle inequalities on the HMM parameters. The rest of this section is dedicated to the proofs of the results.

Appendix A of our supplementary material contains the spectral algorithm from de Castro, Gassiat and Le Corff and de Castro, Gassiat and Lacour (2016) that we use in our simulations. Appendix B gathers the proofs of Section 3.4, which deals with the oracle inequalities for the least squares method. Finally, Appendix C contains the proof of Lemma 16, and Appendix D contains miscellaneous lemmas and proofs.

2 Definitions and assumptions

We will use the following notations throughout the paper.

-

•

is the set of positive integers.

-

•

For , is the set .

-

•

If and are two functions, we denote by their tensor product, defined by .

-

•

is the linear space spanned by the family .

-

•

If and are two linear spaces, we denote by their tensor product, that is the linear space spanned by the tensor products of their elements: .

-

•

is the simplex in dimension . It will be seen as the set of probability measures on a finite set of size .

-

•

is the set of irreducible transition matrices of size .

-

•

is the identity matrix of size .

-

•

is the Hilbert space of square integrable functions on with respect to the measure .

-

•

The notation for a constant will mean that the value of depends on the specified parameters , , For several constants depending on the same parameters, we will write .

In the following, is a positive integer which will denote the number of consecutive observations used for the estimation procedure.

2.1 Hidden Markov models

Let be a Markov chain with finite state space of size with transition matrix and initial distribution . Without loss of generality, we can set .

Let be random variables on a measured space with -finite such that conditionally on the ’s are independent with a distribution depending only on . Let be the distribution of conditionally to . Assume that has density with respect to . We call the emission distributions and the emission densities.

Then is a hidden Markov model with parameters . The hidden chain is assumed to be unknown, so that the estimator only has access to the observations .

For , , and , let

When is a probability distribution on , a transition matrix and a -uple of probability densities, is the density of the first observations of a HMM with parameters .

For the sake of readability, we will drop the dependence in in the following and write instead of . Moreover, if is irreducible with stationary distribution , we simply write , and we write the true density .

2.2 Assumptions

Let be a subset of and be a sequence of nested subspaces of such that has dimension for all and their union is dense in . will be the subspaces on which the projections of the emission densities will be estimated.

We will need the following assumptions.

- [HX]

-

is a stationary ergodic Markov chain with parameters ;

- [HidA]

-

is invertible, and the family is linearly independent;

- [HidB]

-

is invertible, and the emission densities are all distinct;

- [HF]

-

, is closed under projection on for all and

with and larger than 1.

The ergodicity assumption in [HX] is completely standard in order to obtain convergence results. In this case, the initial distribution is forgotten exponentially fast, so that the HMM will essentially behave like a stationary process. In order to simplify the proofs, we assume the Markov chain to be stationary. One can check that our results are essentially the same when the initial distribution is not the stationary one.

[HidA] appears in spectral methods, with the hypothesis that elementwise, see for instance Hsu, Kakade and Zhang (2012). [HidA] and [HidB] also appear in identifiability issues, possibly combined with the stationarity hypothesis, see Alexandrovich and Holzmann (2014) and Gassiat, Cleynen and Robin (2015). Note that the condition on in [HidB] only involves the real order .

Even though [HidB] appears less restrictive than [HidA] about the emission densities, it is delicate to use here. The problem lies in the condition on the number of consecutive observations . For [HidB], one has to take larger than an increasing function of the order, so it requires to have an a priori upper bound on the order to choose . This is less interesting than [HidA], which can work without prior bound since it only requires for any value of the order.

3 Least squares estimation

In this section, we introduce our penalized least squares estimator and study its asymptotic properties.

3.1 Approximation spaces and estimators

We want to estimate the density of consecutive observations by minimizing the quadratic loss . We thus take the corresponding empirical loss

where for an observation sequence of length coming from a single HMM .

Define for all , :

where and are defined in Section 2.2. In the following, we will always implicitly consider .

For all and , we define the corresponding estimators

where we dropped the dependency in for ease of notation. Then, we select the parameters using the penalized empirical loss:

which leads to the estimators

3.2 Underestimation of the order

Note that the distribution of the HMM remains unchanged under permutation of the hidden states. We will therefore use a pseudo-distance that is invariant by permutation on the set of parameters.

We define it as follows. Let , , and transition matrices of size , . Let be the set of permutations of . For all , define the swapped parameters , and by

and finally

The following properties will be of use to prove the consistency of the order estimator, but we think it can also be of independent interest to better understand the identifiability of the model. The first one is a generalization of previous identifiability results from Alexandrovich and Holzmann (2014); Gassiat, Cleynen and Robin (2015); de Castro, Gassiat and Lacour (2016).

Proposition 1.

Let , such that for all , transition matrix of size and such that [HidA] or [HidB] hold for the order . Then, for all , for all , for all transition matrix of size and all , the following holds:

Comment.

This property does not require two assumptions that appear in Alexandrovich and Holzmann (2014) and Gassiat, Cleynen and Robin (2015): that is a family of probability densities and that the Markov chain is stationary.

In particular, the fact that may not be a family of probability densities is crucial in the proof of Corollary 2, which is necessary to prove the strong consistency of the estimator of the order.

Proof.

Assume [HidA]. The spectral algorithm from de Castro, Gassiat and Le Corff applied on the linear space spanned by both sets of densities allows to retrieve the order from two consecutive observations and the parameters from three consecutive observations. Their proof works when the emission densities are not probability densities and when the chain is not stationary.

Assume [HidB]. A careful reading of the proofs of Alexandrovich and Holzmann (2014) shows that their result can be extended to general observation spaces and do not require the measures to be probabilities. ∎

The second property is the following corollary, which states that the distance between the actual model and the models where the order is underestimated is positive. It is worth noting that we do not need to be compact.

Corollary 2.

Assume [HX], ([HidA] or [HidB]) and [HF] hold. Then, for all :

Proof.

Proof in Section 6.2.1. ∎

Our first theorem shows that the probability to underestimate the order decreases exponentially with the number of observations. This comes from Corollary 2: since the empirical criterion converges to the distance (plus some constant that does not depend on the model), the penalized error will eventually become larger for orders under than for orders over , which means that we won’t underestimate the real order. The exponential decrease rate brings to mind the one studied in Gassiat and Boucheron (2003): in both cases, the exponents involve the distance between the actual model and models with underestimated orders, as can be seen in our proof.

Theorem 3.

Assume [HX], ([HidA] or [HidB]) and [HF] hold. There exists positive constants and such that the following holds.

Assume that

and

then there exists such that for all ,

Proof.

Proof in Section 6.3. ∎

3.3 Overestimation of the order and consistency

Our second theorem controls the probability to overestimate the order. It consists in overpenalizing large models so that the estimated order remains small.

We will need the following technical condition on the penalty:

Condition ([Hpen]()).

The penalty function pen satisfies

We can now state the theorem and its corollary proving the strong consistency of our estimator of the order. Note that it does not require any identifiability assumption.

Theorem 4.

Assume [HX] and [HF] hold. There exists positive constants such that the following holds.

Assume [Hpen]() holds for some , then there exists such that for all ,

Proof.

Proof in Section 6.3. ∎

Corollary 5.

Assume [HX], [HF] and ([HidA] or [HidB]) hold. There exists positive constants such that the following holds.

Assume that the penalty function satisfies

and [Hpen] holds for some , then

In particular, almost surely.

Let us comment on the condition [Hpen] when using a penalty of the form where may depend on .

-

•

If one has an a priori bound on the order, i.e. if for some known , then direct computations show that for all , , there exists depending on (for instance, works) such that [Hpen] holds for all (instead of ). This means that if one has an a priori bound on the order, then by taking a constant large enough and , the estimator is almost surely consistent.

-

•

If one does not have an a priori bound on , taking a constant does not allow to get [Hpen] for all possible , which means we can’t apply Corollary 5. However, by taking as a sequence indexed by that tends to infinity, we get that for all and , [Hpen] holds. This implies consistency with polynomial decrease of the probability of error, at the cost of overpenalizing.

Overpenalizing is actually necessary if one wants to satisfy [Hpen] for all . This is stated in the following proposition:

Proposition 6.

Let and pen be a positive penalty such that for all , [Hpen] holds, then there exists a sequence such that for all , and , .

Proof.

Proof in Appendix D.1. ∎

3.4 Oracle inequalities

Our first result for this section is an oracle inequality on the density of consecutive observations for the least squares estimator.

Theorem 7.

Assume [HX] and [HF] hold. Then there exists positive constants such that if the penalty satisfies

then for all , for all , it holds with probability larger than that

Proof.

Proof in Section B.1. ∎

Comment.

The constant before the infimum can be replaced by any constant , at the cost of changing the constants , and .

We would like to deduce an oracle inequality on the parameters of the HMM from this result. Using Cauchy-Schwarz inequality, it is easy to upper bound the error on the density by the error on the parameters: for all probability distributions and on , for all transition matrices and of size and for all ,

| (1) |

as soon as [HF] holds. The proof of this equation is detailed in Section B.2.

Thus, all we need to deduce an oracle inequality on the parameters is to lower bound the error on by the error on the parameters. Let be the set of parameters such that

| (2) |

Note that can be identified with the set

These assumptions are natural since they are necessary (but not sufficient) to ensure that if and is a probability distribution, a transition matrix and a vector of probability densities, then is also a probability distribution, a transition matrix and a vector of probability densities.

The first step in order to get a lower bound along the same lines as equation (1) is to control the behaviour of the difference near the true parameters, which comes down to proving that the quadratic form derived from the second-order expansion of

is positive definite on for . One can write the coefficients of the matrix of this quadratic form as polynomials in the coefficients of , and of the Gram matrix . However, this matrix may not be invertible: one has to consider its restriction to the space , which is equivalent to considering the quadratic form defined on by the second-order expansion of where is the natural linear injection from to (note that is bijective and bicontinous under [HF]). Since the quadratic form is always nonnegative, we only need its determinant to be non zero in order for the quadratic form to be positive definite on .

Thus, let be determinant of the matrix of this quadratic form. is also a polynomial in the coefficients of , and . The following lemma shows that there exists some parameters and satisfying the conditions for which is not zero.

Lemma 8.

There exists some parameters satisfying the conditions [HX] and [HidA] such that .

Proof.

Proof in Section B.3. ∎

What should be retained from this lemma is that is a polynomial which is not identically zero on the set of parameters satisfying the identifiability conditions. This means that one can generically assume it to be different from zero, which corresponds to the assumption

- [Hdet]

-

.

Since we assumed to be the stationary distribution of , its coefficients–and by extension –can be expressed as a rational function of the coefficients of . Taking as the numerator of the rational function deduced from , one gets another polynomial in the coefficients of and which is also non-zero. Thus, the following assumption–which we will need to lower bound the error on the density by the error on the parameters–is generically satisfied.

- [HdetStat]

-

.

Note that [Hdet] and [HdetStat] are equivalent under the assumption [HX].

Theorem 9.

Assume [HidA] and [Hdet] hold. Then there exists a positive constant such that for all , for all transition matrix of size and for all such that for all ,

Proof.

Proof in Section B.4. ∎

The following theorem is a direct consequence of the above results. It provides an oracle inequality on the parameters conditionally to the fact that the order has been correctly estimated.

Theorem 10.

Assume [HX], [HidA], [HF] and [Hdet] hold. Also assume that for all , .

Then there exists positive constants such that if the penalty satisfies

then for all , for all , conditionally to , with probability larger than :

where is the projection of on .

It is now possible to get the convergence rate of the estimators of the parameters. In order to take the event where into account, we agree that the distance between the parameters of two HMMs with different orders is bounded by some constant . Note that could even be taken as a power of without changing anything to our result.

Corollary 11.

Assume [HX], [HidA], [HF] and [Hdet] hold. Also assume that for all , , and that the penalty satisfies

Then there exists a positive constant such that for all , there exists a positive constant such that for all and for all ,

and

Let us discuss what this corollary implies. The approximation error can be bounded in a standard way by where is the regularity of the emission densities, see for instance DeVore and Lorentz (1993). One can obtain a trade-off between approximation error and penalty by choosing , which leads to the optimal rate of convergence , up to a logarithmic factor. This shows that our estimators are adaptive, quasi-rate minimax and converge almost surely to the right number of states, all at the same time.

4 Spectral estimation

In this section, we introduce our spectral order estimator. We will assume [HX] and [HidA] hold.

The idea of this method is to use the matrix containing the coordinates of the density of two consecutive observations in an orthonormal basis. Take and let be an orthonormal basis of . For ease of notation, we will drop the dependency in and write instead of . Let us introduce the matrice and its empirical estimator, defined by

contains the coordinates of the density of with respect to on the basis . It holds that

| (3) |

with the coordinates of the emission densities on the orthonormal basis:

When the emission densities are linearly independent, has full rank for large enough.

The key remark for our method is that contains explicit information about the order of the HMM, as stated in the following lemma:

Lemma 12.

There exists such that for all , has rank .

In the following, we will assume for given by this lemma.

In practice, one only has access to the matrix , which can be seen as a noisy version of . In particular, there is no reason for it to have only nonzero singular values. On the contrary, the spectrum becomes noisy, and when some singular values of are too small, they can be masked by this noise. As seen in equation (3), this can occur when or are close to not having full rank, which means for that the emission densities are almost linearly dependent.

Denote by the singular values of the matrix . We can now state the theorem proving the consistency of the spectral order estimator:

Theorem 13.

Let .

There exists and such that for all and ,

so that almost surely.

Comment.

It is possible to take , constant and depending on in an explicit way as long as grows slowly enough, that is and where is defined in Lemma 14.

Proof.

The following result from appendix E of de Castro, Gassiat and Le Corff allows to control the difference between the spectra of and .

Lemma 14.

There exists some constant depending only on such that for any positive , and ,

where

In particular, taking and assuming and , one has with probability that

for all , using that for any matrix , one has .

Let . We will need Weyl’s inequality (a proof may be found in Stewart and Sun (1990) for instance):

Lemma 15 (Weyl’s inequality).

Let be matrices with , then for all ,

Using this inequality, one gets that with probability at least , for all , and for all , .

In particular, if , then with probability at least , the order is exactly the number of singular values of which are larger than . Finally, observe that under the condition ,

since one can assume without loss of generality that . By taking , this concludes the proof. ∎

5 Numerical experiments

In this section, we show the results of our estimators on simulated data. The simulation parameters are introduced in Section 5.1. We show the numerical results and discuss their ability to select the right order in practice in Section 5.2, and we present the data-driven methods and heuristics we used for the numerical implementation in Section 5.3.

5.1 Simulation parameters

We will consider with being the Lebesgue measure. We will use a trigonometric basis on to generate the approximation spaces . More precisely, define

for all and . We take the spaces induced by the trigonometric basis.

Comment.

Taking the same vectors in all bases is not mandatory to ensure theoretical consistency, but in practice it allows us to take an additional initial point for the minimization step and improves the stability of the algorithm (see Step 1 below).

We will assume to be linearly independent, so that one only needs observations to recover the parameters of the HMM.

In order to assess the performances of the different procedures, we generate observations of a HMM of order 3 for several values of , using the following parameters:

-

•

Emission distributions: Beta distributions with two possible sets of parameters: [, and ] or [, and ];

-

•

Markov chain parameters:

Finally, we take and the maximum values of and for which we will compute the estimators.

The simulation codes are available in MATLAB at https://www.normalesup.org/~llehericy/HMM_order_simfiles/.

5.2 Numerical results

| 0.2 | 0 | |

| 1 | 0 | |

| 1 | 1 | |

| 1 | 1 |

| 0.3 | 0 | |

| 0.9 | 0 | |

| 1 | 0 | |

| 1 | 0.1 |

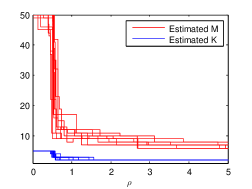

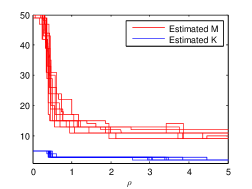

Figure 1 summarizes the results of both procedures. Both select the right order as soon as the number of observations is sufficient.

The spectral method is easily put in pratice and runs extremely fast. It doesn’t need a time-consuming contrast minimization step or an initial point. However, the thresholding of the singular values is a delicate issue, and if the order is incorrect, then the theoretical results about the spectral estimators of the parameters don’t hold and this method may behave poorly.

The performances of the least squares method are much better (see Figure 1 for comparing the order estimators and de Castro, Gassiat and Lacour (2016) for comparing the emission densities estimators). In addition, the model selection step is easy to handle and gives an estimator of the order that we proved to be consistent, estimators of the HMM parameters that we proved to be quasi-rate minimax and a way to check whether the model fits the data well (see Section 5.3.1), all at the same time. However, the minimization of the (non-convex) empirical contrast is a time-consuming step, especially for large samples and large models.

Choosing the right method is thus a question of computational power and amount of available data. For small datasets where one wants to get accurate results, the least squares method is best. Conversely, on large datasets and large models, the spectral method is a good choice in order to obtain many estimators in a reasonable amount of time.

5.3 Practical implementation

5.3.1 Least squares method

The first issue that one encounters when trying to minimize the least squares criterion is that it is not convex. Several algorithms have been proposed to overcome this difficulty. We chose to use CMA-ES (for Covariance Matrix Adaptation Estimation Strategy, see Hansen (2006)) in order to find a minimizer. This estimator is easy to use and works well in many situations, but–like all approximate minimization algorithms–it requires a good initial point since it might otherwise remain stuck in local minima.

One part of our method consists in using previous estimates as initial points for further steps to counter this phenomenon, since it is likely that this way the estimators stay near the real minimizer. Our practical algorithm is the following:

-

1.

Minimize on each model, for and . We take several initial points for model according to the following cases:

-

•

. Use a HMM with a single state and a uniform emission distribution.

-

•

. Take the estimator from model . For each hidden state of the corresponding HMM, use the model where this state is duplicated. More precisely, the Markov chain where state is duplicated is obtained by replacing the state from chain with two states and such that for each state ,

and

-

•

. Use estimator from model with the -th coordinate of each emission density set to zero. This is only interesting if all are spanned by the first vectors of a given orthonormal basis, like for trigonometric spaces.

Then, after minimization from each one of these initial points, take the estimator that minimizes .

-

•

-

2.

Tune the parameter of the penalty with the slope heuristics or the dimension jump method (see below) and select and .

-

3.

Return the estimator for and .

This iterative initialization procedure relies on the heuristics that when the order is underestimated, then several states are ”merged” together. Duplicating a merged state will allow to separate them effectively while still taking advantage of the computations done up to now. It is meant to avoid having to recalculate all states at the same time (which could get us stuck in sub-optimal local minima) when the best solution is likely to be a small modification of the previous estimator. In addition, when the order is overestimated, it allows to make sure the empirical criterion is indeed decreasing with the dimension of the model by giving an estimator that performs at least as well as those from smaller models. This makes our method robust to an overestimation of the order.

The last practical issue is a very common one in the model selection setting: the constant of the penalty is unknown and has to be estimated before one can select the right model. Several data-driven estimators have been proposed to circumvent this difficulty, for instance dimension jump heuristics, slope heuristics, bootstrap or cross validation. We focus on the first two, which have several advantages in our setting. First, they are easy to use, are proved to be theoretically valid in many settings and work well in a wide range of applications (see for instance Baudry, Maugis and Michel (2012) and references therein). Secondly, they take advantage of the structure of our problem and both give a qualitative way to check whether the choice of penalty is valid or not, and by extension whether the model is misspecified or not.

Dimension jump heuristics

In this paragraph, we study the selected parameters

and the selected complexity

with .

Assume that there exists such that is a minimal penalty, that is a penalty such that as tends to infinity, for all , the size of the model chosen for penalty remains small in some sense and for all , the size of the model becomes huge. Then, for large enough, this will appear on the graph of the selected model complexity as a “dimension jump”: around some constant , the complexity will abruptly drop from large models to small models. This is clearly the case in Figure 2. Figure 3 shows the behaviour of and with . A dimension jump also occurs with these functions. It is most visible for .

Finally, once the dimension jump location has been estimated, we take to select the final parameters.

It is worth noting that this jump method also gives a qualitative way to check whether the choice of parameters is sensible: if no clear jump can be identified, then either one didn’t consider enough models to make the jump clear, or the penalty isn’t the right one, or the model cannot approximate the data distribution well.

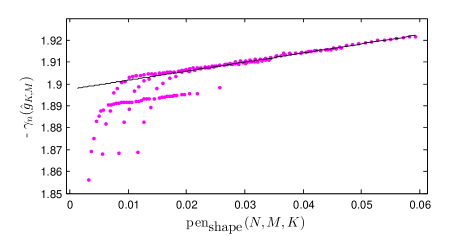

Slope heuristics

This heuristics relies on the fact that when is a minimal penalty, then the empirical contrast function is expected to behave like for large models and for some constant . This gives both a way to calibrate the constant of the penalty and to check if the chosen penalty has the right shape (see Baudry, Maugis and Michel (2012)). The final penalty is then taken as .

Figure 4 shows the graph of the empirical contrast depending on . The slope heuristics works well in this situation, suggesting that our penalty has the right shape.

5.3.2 Spectral method

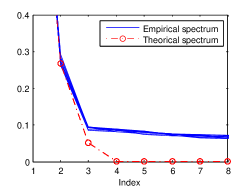

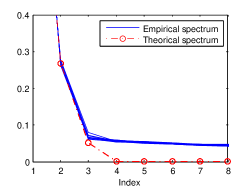

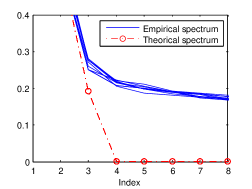

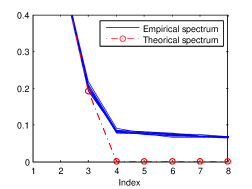

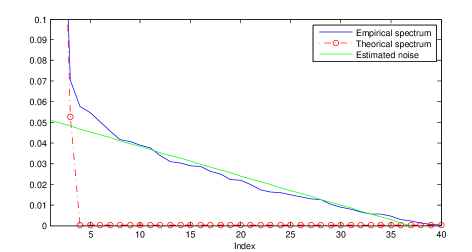

The idea of the spectral order estimation is to recover the rank of the matrix . However, this is not always possible: if one singular value of is smaller than the noise (which is the case when is close from not being invertible, i.e. when the emission densities are close from being linearly dependent, and when there are only few observations), then this method will not be able to “see” the corresponding hidden state.

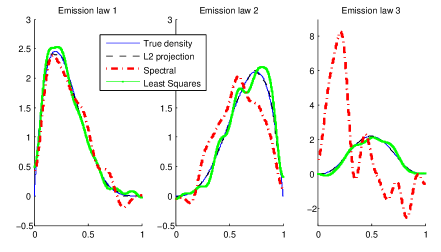

Figure 5–and in particular Figure 5(a)–illustrates this problem: the third singular value is smaller than several noisy singular values, which means it won’t be possible to recover it. Even if one knows the right order, the fact that the singular value is smaller than the noise can make it impossible for spectral methods to recover the true parameters. Figure 6 shows the result when trying to estimate the densities in the situation of Figure 5(a): when the singular value is drowned by the noise, the output of the spectral estimator is aberrant. Notice that it is not a fatality: in the same situation, the least squares method manages to give sensible estimators of the emission densities. This is an intrinsic limitation of the spectral method.

Therefore, what we need is a way to threshold the parameters in order to distinguish noise from significant singular values. The estimator is one way to achieve this, but the calibration of is a tricky problem, since the right choice of depends on the parameters of the HMM. We will use a different method, which relies on the same idea: identifying the noisy singular values which stand out from the others and saying they correspond to nonzero singular values of . Our heuristics relies on the fact that when one sorts the singular values in decreasing order, then the smallest ones approximately follow an affine relation with respect to their index. This tendency is shown in Figure 7.

We proceed as follows. Let and be two positive integers such that . We estimate the affine dependance of the singular values of with respect to their index with a linear regression using its smallest singular values. Then, we set a thresholding parameter . We say a singular value is significant if it is above times the value that the regression predicts for it. Lastly, we take as the number of consecutive significant singular values starting from the largest one. This heuristics seems to work as soon as is large enough, e.g. .

6 Proofs

6.1 Main technical result

The following lemma is the main technical result of this paper. It is the key for both the strong consistency and the oracle inequalities. It allows to control the difference between the empirical criterion and the theoretical loss for all models at the same time.

Define , so that

| (4) |

Let

| (5) |

Comment.

It is not necessary to assume that . In particular, one can take for all . In that case, we will simply write .

Lemma 16.

Assume [HX] and [HF] hold. Then there exists a sequence and positive constants such that if the penalty satisfies

then for all , and , one has with probability larger than :

Comment.

One can replace the constant in the first upper bound by any , at the cost of changing the constants , and .

The structure of the proof follows the usual method to control empirical processes, see for instance Massart (2007), Chapter 6, adapted to the HMM structure by de Castro, Gassiat and Lacour (2016). The novelty and main difficulty of the proof comes from the generalization to both nonparametric densities and an unknown number of states: we had to introduce a much finer control of the constants and of the bracketing entropy of the models in order to take the dependency in the order of the HMM into account.

The details of the proof can be found in appendix C.

6.2 Identifiability proofs

6.2.1 Proof of Corollary 2

Denote by the orthogonal projection on a linear space .

Since the union of is dense in , we can take such that [HidA] or [HidB] holds for .

We will need the following lemma.

Lemma 17.

Proof.

By linearity of the projection operator, it is enough to prove that for all ,

which is easy to check. ∎

We will make a proof by contradiction. Assume that for some . Then there exists a sequence such that in , with , a transition matrix of size and .

The orthogonal projection on is continuous, so by using Lemma 17, one gets that

Then, using the compacity of and of the set of transition matrices of size and the relative compacity of (which is a bounded subset of a finite dimension linear space), one gets (up to extraction of a subsequence) that there exists , a transition matrix of size and such that , and .

Finally, using the continuity of the function and the unicity of the limit, one gets

Then Proposition 1 contradicts the assumption , which is enough to conclude.

6.3 Consistency proofs

The definition of is equivalent to the following one:

where

Choosing rather than means that is better than , i.e.

Let

Then

We will thus control the probability of the latter event for all in the first case and in the second case.

Proof of Theorem 3

Let . We will choose a suitable value for this integer later in the proof. Assume . Then by definition of and of (equation (4)),

Using the definition of (equation (5)), one gets that

Let , and be as in Lemma 16. We can assume that so that . Let us introduce the function . Let and and assume we are in the event of probability of Lemma 16. Then, for all :

and

We assumed , so that

Corollary 2 ensures that

so that for all ,

By density of in , one gets that

so that there exists such that . If we choose this , we get that

Which implies that as soon as , i.e.

To conclude, note that there exists such that for all , . Then, letting , one has for all , with probability , for all , , which implies that .

Proof of Theorem 4

For all ,

and

Note that is the orthogonal projection of on and , so that, using the Pythagorean Theorem,

Let , and be as in Lemma 16. We can assume that so that . Let us introduce the function . Let and and assume we are in the event of probability of Lemma 16. Then, for all such that :

which implies

so that for all such that :

Now, assume that [Hpen]() holds for some and the above constant . Then there exists such that for all and for all such that ,

which is strictly positive as soon as . Thus, letting , one has for all , with probability , for all such that , , which implies that . This concludes the proof.

7 Acknowledgment

We would like to thank Elisabeth Gassiat for her precious advice and Yohann de Castro for his codes which were at the root of our numerical experiments.

References

- Alexandrovich and Holzmann (2014) {barticle}[author] \bauthor\bsnmAlexandrovich, \bfnmGrigory\binitsG. and \bauthor\bsnmHolzmann, \bfnmHajo\binitsH. (\byear2014). \btitleNonparametric identification of hidden Markov models. \bjournalarXiv preprint arXiv:1404.4210. \endbibitem

- Allman, Matias and Rhodes (2009) {barticle}[author] \bauthor\bsnmAllman, \bfnmElizabeth S\binitsE. S., \bauthor\bsnmMatias, \bfnmCatherine\binitsC. and \bauthor\bsnmRhodes, \bfnmJohn A\binitsJ. A. (\byear2009). \btitleIdentifiability of parameters in latent structure models with many observed variables. \bjournalThe Annals of Statistics \bpages3099–3132. \endbibitem

- Anandkumar, Hsu and Kakade (2012) {binproceedings}[author] \bauthor\bsnmAnandkumar, \bfnmAnimashree\binitsA., \bauthor\bsnmHsu, \bfnmDaniel J\binitsD. J. and \bauthor\bsnmKakade, \bfnmSham M\binitsS. M. (\byear2012). \btitleA Method of Moments for Mixture Models and Hidden Markov Models. In \bbooktitleCOLT \bvolume1 \bpages4. \endbibitem

- Baudry, Maugis and Michel (2012) {barticle}[author] \bauthor\bsnmBaudry, \bfnmJean-Patrick\binitsJ.-P., \bauthor\bsnmMaugis, \bfnmCathy\binitsC. and \bauthor\bsnmMichel, \bfnmBertrand\binitsB. (\byear2012). \btitleSlope heuristics: overview and implementation. \bjournalStatistics and Computing \bvolume22 \bpages455–470. \endbibitem

- Bickel et al. (1998) {barticle}[author] \bauthor\bsnmBickel, \bfnmPeter J\binitsP. J., \bauthor\bsnmRitov, \bfnmYa’acov\binitsY., \bauthor\bsnmRyden, \bfnmTobias\binitsT. \betalet al. (\byear1998). \btitleAsymptotic normality of the maximum-likelihood estimator for general hidden Markov models. \bjournalThe Annals of Statistics \bvolume26 \bpages1614–1635. \endbibitem

- Birgé and Massart (2007) {barticle}[author] \bauthor\bsnmBirgé, \bfnmLucien\binitsL. and \bauthor\bsnmMassart, \bfnmPascal\binitsP. (\byear2007). \btitleMinimal penalties for Gaussian model selection. \bjournalProbability theory and related fields \bvolume138 \bpages33–73. \endbibitem

- Celeux and Durand (2008) {barticle}[author] \bauthor\bsnmCeleux, \bfnmGilles\binitsG. and \bauthor\bsnmDurand, \bfnmJean-Baptiste\binitsJ.-B. (\byear2008). \btitleSelecting hidden Markov model state number with cross-validated likelihood. \bjournalComputational Statistics \bvolume23 \bpages541–564. \endbibitem

- Chambaz, Garivier and Gassiat (2009) {barticle}[author] \bauthor\bsnmChambaz, \bfnmAntoine\binitsA., \bauthor\bsnmGarivier, \bfnmAurelien\binitsA. and \bauthor\bsnmGassiat, \bfnmElisabeth\binitsE. (\byear2009). \btitleA minimum description length approach to hidden Markov models with Poisson and Gaussian emissions. Application to order identification. \bjournalJournal of Statistical Planning and Inference \bvolume139 \bpages962–977. \endbibitem

- Couvreur and Couvreur (2000) {binproceedings}[author] \bauthor\bsnmCouvreur, \bfnmLaurent\binitsL. and \bauthor\bsnmCouvreur, \bfnmChristophe\binitsC. (\byear2000). \btitleWavelet-based non-parametric HMM’s: theory and applications. In \bbooktitleAcoustics, Speech, and Signal Processing, 2000. ICASSP’00. Proceedings. 2000 IEEE International Conference on \bvolume1 \bpages604–607. \bpublisherIEEE. \endbibitem

- de Castro, Gassiat and Lacour (2016) {barticle}[author] \bauthor\bparticlede \bsnmCastro, \bfnmYohann\binitsY., \bauthor\bsnmGassiat, \bfnmÉlisabeth\binitsÉ. and \bauthor\bsnmLacour, \bfnmClaire\binitsC. (\byear2016). \btitleMinimax Adaptive Estimation of Nonparametric hidden Markov models. \bjournalJournal of Machine Learning Research \bvolume17 \bpages1-43. \endbibitem

- (11) {barticle}[author] \bauthor\bparticlede \bsnmCastro, \bfnmYohann\binitsY., \bauthor\bsnmGassiat, \bfnmElisabeth\binitsE. and \bauthor\bsnmLe Corff, \bfnmSylvain\binitsS. \btitleConsistent estimation of the filtering and marginal smoothing distributions in nonparametric hidden Markov models. \bjournalIEEE Information Theory, to appear. \endbibitem

- DeVore and Lorentz (1993) {bbook}[author] \bauthor\bsnmDeVore, \bfnmRonald A\binitsR. A. and \bauthor\bsnmLorentz, \bfnmGeorge G\binitsG. G. (\byear1993). \btitleConstructive approximation \bvolume303. \bpublisherSpringer Science & Business Media. \endbibitem

- Douc et al. (2004) {barticle}[author] \bauthor\bsnmDouc, \bfnmRandal\binitsR., \bauthor\bsnmMoulines, \bfnmEric\binitsE., \bauthor\bsnmRydén, \bfnmTobias\binitsT. \betalet al. (\byear2004). \btitleAsymptotic properties of the maximum likelihood estimator in autoregressive models with Markov regime. \bjournalThe Annals of statistics \bvolume32 \bpages2254–2304. \endbibitem

- Gassiat (2002) {binproceedings}[author] \bauthor\bsnmGassiat, \bfnmElisabeth\binitsE. (\byear2002). \btitleLikelihood ratio inequalities with applications to various mixtures. In \bbooktitleAnnales de l’IHP Probabilités et statistiques \bvolume38 \bpages897–906. \endbibitem

- Gassiat and Boucheron (2003) {barticle}[author] \bauthor\bsnmGassiat, \bfnmElisabeth\binitsE. and \bauthor\bsnmBoucheron, \bfnmStéphane\binitsS. (\byear2003). \btitleOptimal error exponents in hidden Markov models order estimation. \bjournalInformation Theory, IEEE Transactions on \bvolume49 \bpages964–980. \endbibitem

- Gassiat, Cleynen and Robin (2015) {barticle}[author] \bauthor\bsnmGassiat, \bfnmElisabeth\binitsE., \bauthor\bsnmCleynen, \bfnmAlice\binitsA. and \bauthor\bsnmRobin, \bfnmStéphane\binitsS. (\byear2015). \btitleFinite state space non parametric hidden Markov models are in general identifiable. \bjournalStat. Comp. \bpages1–11. \endbibitem

- Gassiat and Keribin (2000) {barticle}[author] \bauthor\bsnmGassiat, \bfnmElisabeth\binitsE. and \bauthor\bsnmKeribin, \bfnmChristine\binitsC. (\byear2000). \btitleThe likelihood ratio test for the number of components in a mixture with Markov regime. \bjournalESAIM: Probability and Statistics \bvolume4 \bpages25–52. \endbibitem

- Gassiat and Rousseau (2014) {barticle}[author] \bauthor\bsnmGassiat, \bfnmElisabeth\binitsE. and \bauthor\bsnmRousseau, \bfnmJudith\binitsJ. (\byear2014). \btitleAbout the posterior distribution in hidden Markov models with unknown number of states. \bjournalBernoulli \bvolume20 \bpages2039–2075. \endbibitem

- Hansen (2006) {bincollection}[author] \bauthor\bsnmHansen, \bfnmNikolaus\binitsN. (\byear2006). \btitleThe CMA evolution strategy: a comparing review. In \bbooktitleTowards a new evolutionary computation \bpages75–102. \bpublisherSpringer. \endbibitem

- Hsu, Kakade and Zhang (2012) {barticle}[author] \bauthor\bsnmHsu, \bfnmDaniel\binitsD., \bauthor\bsnmKakade, \bfnmSham M\binitsS. M. and \bauthor\bsnmZhang, \bfnmTong\binitsT. (\byear2012). \btitleA spectral algorithm for learning hidden Markov models. \bjournalJournal of Computer and System Sciences \bvolume78 \bpages1460–1480. \endbibitem

- Kleibergen and Paap (2006) {barticle}[author] \bauthor\bsnmKleibergen, \bfnmFrank\binitsF. and \bauthor\bsnmPaap, \bfnmRichard\binitsR. (\byear2006). \btitleGeneralized reduced rank tests using the singular value decomposition. \bjournalJournal of econometrics \bvolume133 \bpages97–126. \endbibitem

- Lambert, Whiting and Metcalfe (2003) {barticle}[author] \bauthor\bsnmLambert, \bfnmMartin F\binitsM. F., \bauthor\bsnmWhiting, \bfnmJulian P\binitsJ. P. and \bauthor\bsnmMetcalfe, \bfnmAndrew V\binitsA. V. (\byear2003). \btitleA non-parametric hidden Markov model for climate state identification. \bjournalHydrology and Earth System Sciences Discussions \bvolume7 \bpages652–667. \endbibitem

- Langrock et al. (2015) {barticle}[author] \bauthor\bsnmLangrock, \bfnmRoland\binitsR., \bauthor\bsnmKneib, \bfnmThomas\binitsT., \bauthor\bsnmSohn, \bfnmAlexander\binitsA. and \bauthor\bsnmDeRuiter, \bfnmStacy L\binitsS. L. (\byear2015). \btitleNonparametric inference in hidden Markov models using P-splines. \bjournalBiometrics \bvolume71 \bpages520–528. \endbibitem

- Le Gland and Mevel (2000) {barticle}[author] \bauthor\bsnmLe Gland, \bfnmFrançois\binitsF. and \bauthor\bsnmMevel, \bfnmLaurent\binitsL. (\byear2000). \btitleExponential forgetting and geometric ergodicity in hidden Markov models. \bjournalMathematics of Control, Signals and Systems \bvolume13 \bpages63–93. \endbibitem

- Lefèvre (2003) {barticle}[author] \bauthor\bsnmLefèvre, \bfnmFabrice\binitsF. (\byear2003). \btitleNon-parametric probability estimation for HMM-based automatic speech recognition. \bjournalComputer Speech & Language \bvolume17 \bpages113–136. \endbibitem

- Lehéricy (2015) {bunpublished}[author] \bauthor\bsnmLehéricy, \bfnmLuc\binitsL. (\byear2015). \btitleEstimation adaptative non paramétrique pour les modèles à chaîne de Markov cachée. \bnoteMémoire de M2, Orsay. \endbibitem

- Massart (2007) {bincollection}[author] \bauthor\bsnmMassart, \bfnmPascal\binitsP. (\byear2007). \btitleConcentration inequalities and model selection. In \bbooktitleLecture Notes in Mathematics, \bvolume1896 \bpublisherSpringer, \baddressBerlin. \endbibitem

- Paulin (2013) {barticle}[author] \bauthor\bsnmPaulin, \bfnmDaniel\binitsD. (\byear2013). \btitleConcentration inequalities for Markov chains by Marton couplings. \bjournalarXiv preprint arxiv:1212.2015v2. \endbibitem

- Robin, Bonhomme and Jochmans (2014) {barticle}[author] \bauthor\bsnmRobin, \bfnmJean-Marc\binitsJ.-M., \bauthor\bsnmBonhomme, \bfnmStéphane\binitsS. and \bauthor\bsnmJochmans, \bfnmKoen\binitsK. (\byear2014). \btitleEstimating Multivariate Latent-Structure Models. \endbibitem

- Robin and Smith (2000) {barticle}[author] \bauthor\bsnmRobin, \bfnmJean-Marc\binitsJ.-M. and \bauthor\bsnmSmith, \bfnmRichard J\binitsR. J. (\byear2000). \btitleTests of rank. \bjournalEconometric Theory \bvolume16 \bpages151–175. \endbibitem

- Shang and Chan (2009) {binproceedings}[author] \bauthor\bsnmShang, \bfnmLifeng\binitsL. and \bauthor\bsnmChan, \bfnmKwok-Ping\binitsK.-P. (\byear2009). \btitleNonparametric discriminant HMM and application to facial expression recognition. In \bbooktitleComputer Vision and Pattern Recognition, 2009. CVPR 2009. IEEE Conference on \bpages2090–2096. \bpublisherIEEE. \endbibitem

- Stewart and Sun (1990) {bmisc}[author] \bauthor\bsnmStewart, \bfnmGW\binitsG. and \bauthor\bsnmSun, \bfnmJi-Guang\binitsJ.-G. (\byear1990). \btitleMatrix Perturbation Theory (Computer Science and Scientific Computing). \endbibitem

- van Havre et al. (2016) {barticle}[author] \bauthor\bparticlevan \bsnmHavre, \bfnmZoé\binitsZ., \bauthor\bsnmRousseau, \bfnmJudith\binitsJ., \bauthor\bsnmWhite, \bfnmNicole\binitsN. and \bauthor\bsnmMengersen, \bfnmKerrie\binitsK. (\byear2016). \btitleOverfitting hidden Markov models with an unknown number of states. \bjournalarXiv preprint arXiv:1602.02466. \endbibitem

- Volant et al. (2014) {barticle}[author] \bauthor\bsnmVolant, \bfnmStevenn\binitsS., \bauthor\bsnmBérard, \bfnmCaroline\binitsC., \bauthor\bsnmMartin-Magniette, \bfnmMarie-Laure\binitsM.-L. and \bauthor\bsnmRobin, \bfnmStéphane\binitsS. (\byear2014). \btitleHidden Markov models with mixtures as emission distributions. \bjournalStatistics and Computing \bvolume24 \bpages493–504. \endbibitem

- Yau et al. (2011) {barticle}[author] \bauthor\bsnmYau, \bfnmC\binitsC., \bauthor\bsnmPapaspiliopoulos, \bfnmOmiros\binitsO., \bauthor\bsnmRoberts, \bfnmGareth O\binitsG. O. and \bauthor\bsnmHolmes, \bfnmChristopher\binitsC. (\byear2011). \btitleBayesian non-parametric hidden Markov models with applications in genomics. \bjournalJournal of the Royal Statistical Society: Series B (Statistical Methodology) \bvolume73 \bpages37–57. \endbibitem

Appendix A Spectral algorithm

-

[Step 1]

Consider the following empirical estimators: for any in ,

-

•

,

-

•

,

-

•

,

-

•

.

-

•

-

[Step 2]

Let be the matrix of orthonormal right singular vectors of corresponding to its top singular values.

-

[Step 3]

Form the matrices for all .

-

[Step 4]

Set a uniformly drawn random unitary matrix and form the matrices for all .

-

[Step 5]

Compute a unit Euclidean norm columns matrix that diagonalizes the matrix : .

-

[Step 6]

Set for all and .

-

[Step 7]

Consider the emission distributions estimator defined by for all .

-

[Step 8]

Set where denotes the projection onto the simplex in dimension .

-

[Step 9]

Consider the transition matrix estimator:

where denotes the projection onto the convex set of transition matrices, and define as the stationary distribution of .

Appendix B Proofs of the oracle inequalities

B.1 Proof of Theorem 7

Let and . Then

where the first inequality comes from the definition of and the second from the definition of . Therefore,

By definition of (equation 4),

so that

Now we want to control the term. By linearity,

Using the definition of (equation 5), we get that

so that, using Lemma 16, for all and , with probability larger than , for all and ,

so that

which means that

and finally

which is the expected inequality.

B.2 Proof of equation 1

First, decompose the difference in three terms.

Then we can control each term separately. Let be an orthonormal basis of .

using Cauchy-Schwarz inequality. Then, since by [HF] and is a transition matrix, we get that

A similar decomposition leads to

and

These inequalities remain true if the states of the second set of parameters are swapped. Then, we use that by [HF] to conclude.

B.3 Proof of Lemma 8

In the following, we will identify the quadratic form derived from the second order expansion of and its matrix. Likewise, we will identify the quadratic form derived from the second order expansion of with its matrix. Without loss of generality, one can assume .

Choice of parameters and expression of .

Let be the uniform distribution on , and such that for some constant . For instance, the ’s are times the indicating functions of distinct measurable sets with same measure for . In that case, is an orthonormal basis, and the quantity can be broken down into three order one terms in , and :

-

•

the term in : ;

-

•

the term in : ;

-

•

the term in : .

Now we can make the list of all second-order terms in the expansion of the quantity :

-

•

and : ;

-

•

and : ;

-

•

and : ;

-

•

and : ;

-

•

and : ;

-

•

and : .

We can now write the matrix . In order to clarify the structure of this matrix, let us swap the components of the parameters and consider the new parameters , where (resp. ) is a vector of size containing the diagonal coefficients of (resp. ) and (resp. ) contains its other coefficients. Then the matrix is:

where .

Kernel of .

Substracting the first block of lines to the third and fourth blocks of lines and then the first block of columns to the third and fourth blocks of columns does not change the rank and leads to the matrix

Thus , where is the kernel of and denotes the dimension. If one takes away the lines and columns corresponding to and , one gets the matrix

This matrix is invertible. Therefore, . Now, for all , let and be the vectors defined as

and

One can easily check that these vectors are linearly independant and are all in . Thus, they are a basis of the kernel of : .

Nondegeneracy of restricted on .

Since is symmetric, and thus diagonalisable in an orthonormal basis,

| (6) |

where is the orthogonal projection on the space of vectors orthogonal to and is a symmetric positive definite matrix, whose smallest eigenvalue will be written in the following. The last step to conclude will require the two following lemmas:

Lemma 18.

.

Proof.

Let , then because is a basis of . Since , one gets for all because of the conditions on . Then, the conditions on imply for all , so that . ∎

Lemma 19.

There exists a constant such that for all ,

| (7) |

Proof.

is continuous. By compacity, the quantity

is reached for some . If , then , but this is impossible because of Lemma 18. Therefore . ∎

Finally, for all ,

Therefore, the quadratic form with matrix is nondegenerate on , which shows that is non-zero for these . To conclude, observe that is continuous and that our choice of parameters can be approximated by parameters satisfying [HX] and [HidA].

B.4 Proof of Theorem 9

First, assume that the quadratic form obtained from the second order expansion of

is nondegenerate. Then, a careful reading of the proof of Theorem 8 of de Castro, Gassiat and Lacour (2016) shows that their result can be adapted to our setting and leads to the desired minoration.

Thus, what we need to show is that [Hdet] (which implied the nondegeneracy of the quadratic form from ) implies the nondegeneracy of the quadratic form from (the trick being that takes as parameter while takes ). Assume [Hdet], then there exists such that

with the notation referring to the quadratic form in the second order expansion of .

Since [HidA] holds, is linearly independent, so that the application is invertible. Thus, and are two norms on the same finite-dimensional linear space , so that they are equivalent. In particular, there exists a constant such that . Therefore,

which is what we wanted to prove.

Appendix C Proof of the control of

This section contains the proof of Lemma 16.

C.1 Concentration inequality on

Define for all the sets

Let be the semi-distance defined by , and the distance induced by the norm on .

Let denote the minimal cardinality of a covering of by brackets of size for the semi-distance , that is by sets such that . is called the bracketing entropy of for the semi-distance .

The following lemma is a Bernstein-like inequality that follows from Paulin (2013), Theorem 2.4:

Lemma 20.

Let be a real valued and measurable bounded function on . Let . There exists a positive constant depending only on and such that for all and for all :

The following lemma is an extension of Theorem 6.8 from Massart (2007) and allows to obtain a concentration inequality on the supremum on all functions of a class when one can control its bracketing entropy.

Lemma 21.

Let be some measurable space, a sequence of random variables on , some countable class of real valued and measurable functions on . Assume that there exists some positive numbers and such that for all , and .

Assume also that there exists some constant such that for all and for all :

| (8) |

Assume furthermore that for any positive number , there exists some finite set of brackets covering such that for any bracket , and . Let denote the minimal cardinality of such a covering. Then, there exists a numerical constant such that for any measurable set such that ,

where

and for any measurable random variable , .

Comment.

The assumption is only used to factorise the upper bound by . Without it, the upper bound would be

In practice, this assumption doesn’t cost anything: if equation (8) holds for some constant , then it holds for any constant .

We can do without assuming to be countable. Indeed, is continuous on equipped with the infinity norm. This entails that the supremum of over is equal to the supremum of over any dense subset of (, ). Since , which is a finite dimensional metric linear space for the infinity norm, it is separable. Therefore, without loss of generality, we can get rid of the countability assumption on .

Rewriting these results, we get the following lemma:

Lemma 22.

There exists a constant depending only on and such that for all , for all measurable such that :

where

The core of the proof consists in controlling the bracketing entropy in order to find a ”good” function and constants and depending on , and such that is nonincreasing and

| (9) |

For ease of notation, we did not write the dependency of and on and .

Let us see how to conclude with such an inequality. We shall use the following result (lemma 4.23 from Massart (2007)).

Lemma 23.

Let be some countable set, and such that . Let be some process indexed by and assume that has finite expectation for any positive number , where

Then, for any function on such that is nonincreasing on and satisfies for some to

one has for any :

In our case,

With this choice of , and , this proposition holds even if is not countable for the same reason as in Lemma 22.

It follows that for all :

so that if :

and then

Note that the function is nondecreasing. On the event ,

so that and finally .

It follows that with probability :

| (10) |

and the last step of the proof will be to choose the right and (see Section C.3).

C.2 Control of the bracketing entropy

The goal of this section is to prove equation (9), that is to find , and such that

The bracketing entropy is invariant under translation and increasing with respect to the inclusion relation, so

Using Lemma 28, we get that for all , . Therefore, a bracket of size for is also a bracket of size for , which implies that

| (11) |

Let us now rewrite the definition of :

where

is equipped with the distance . A bracket for will be a set .

is equipped with the distance . A bracket will be a set .

Controlling the bracketing entropy on each of these sets will allow to control the bracketing entropy of . Let us start with them:

Lemma 24.

There exists a bracket covering of size of for the distance with cardinality

| (12) |

such that for all and , .

Lemma 25.

There exists a bracket covering of size of for the distance of cardinality

| (13) |

such that

Let us take such bracketings and consider the following set of brackets:

where

This set covers : for all , , there exists and such that and , and then by construction .

Let us now bound the size of these brackets. Let and , then if one denotes by the corresponding bracket, there exists such that:

Then, by definition of the brackets, and . In addition, we assumed and for all , so that

which implies

| (14) |

and finally by combining 11, 12, 13 and 14:

for large enough () because we assumed , , , and . Thus, Lemma 29 implies that if we write and

then for all and ,

Let us now check that this function satisfies equation (9). First, note that is nonincreasing, so that is also nonincreasing. Thus, we may define as the unique solution of the equation , and then for all :

Equation (9) follows immediately with .

Proof of Lemma 24

Let .

We start with the family with an integer between and , which gives a bracket covering of size of with cardinality smaller than . These brackets will be used to control each free component of and , that is components.

More precisely, we define the following bracket set:

This set covers and its cardinality is smaller than . To get the bracket’s size, note that

and in the end

Proof of Lemma 25

All can be written as where is an orthonormal basis of . Then, assumption [HF] implies that for all .

We will therefore start from a bracket covering of the euclidian ball of radius of , from which we will construct a covering of and of .

Lemma 26.

Let . There exists a bracket covering of size of the euclidian ball of radius of with cardinality

such that for all , , .

Proof.

We start with a bracket covering of size of the infinity ball of radius of . This can be done by a regular partition with pieces along each coordinate. One can easily check that such a covering is also a covering of size of the euclidian ball of radius of . To conclude, it is enough to notice that as soon as , and that because and . ∎

Let be such a covering. For all , and , let

and for all and ,

and finally for all and :

It is enough to show that is a bracket covering of size of that satisfies

Applying the Cauchy-Schwarz inequality, one gets that for all ,

Moreover, for all and ,

We then use that for all and ,

so that

and finally for all .

The last part of the lemma is proved by noting that for all and ,

so that

C.3 Choice of parameters

Let us come back to equation (10). Since is nonincreasing, one has as soon as , so with probability :

Let . One gets

Let with such that . Then, with probability :

Now choose , it follows that and the first point of the lemma is proved.

Moreover, one has with probability , for all :

Let . We get that with probability , for all :

Therefore the lemma holds as soon as

| (15) |

Lemma 27.

There exists constants and such that for all :

Proof.

Let .

is defined by the equation . The function is nondecreasing, so it is enough to show that for some constant that we can assume to be greater than 1.

It is easy to check that there exists a constant such that for all , , so that , which makes it possible to assume . Then

and by taking , one gets that

which means that . ∎

The condition of equation (15) becomes

which is implied by

for some constant depending only on , , and . This concludes the proof.

Appendix D

D.1 Proof of Proposition 6

Let . Note and . One can check that and for all .

Denote by the integer in the hypothesis [Hpen] corresponding to . Then for all , for all and for all ,

Taking the sum over , one gets that

since . Using that ,

Let . One gets

Therefore, there exists a non-decreasing sequence such that

and since , we get that , which concludes the proof.

We could for instance take

D.2 Auxiliary lemmas

Lemma 28.

Proof.

can be written as with a probability -uple, a transition matrix of size and for some .

The first point follows from

For the second point, we use the Cauchy-Schwarz inequality:

The last point comes from

∎

Lemma 29.

Let . Let , and . Then:

Proof.

The first point is straightforward.

For the second point, we have two cases.

-

Case 1:

. Then . Therefore, we can use that , which is enough to conclude.

-

Case 2:

. Then and . Thus,

∎