11institutetext: Sergei Kucherenko 22institutetext: Shugfang Song

33institutetext: Imperial College London, London, SW7 2AZ, UK

33email: s.kucherenko@imperial.ac.uk,

33email: shufangsong@nwpu.edu.cn

Derivative-based Global Sensitivity Measures and Their Link with Sobol’ Sensitivity Indices

Sergei Kucherenko

Shugfang Song

Abstract

The variance-based method of Sobol’ sensitivity indices is very popular

among practitioners due to its efficiency and easiness of interpretation.

However, for high-dimensional models the direct application of this method

can be very time-consuming and prohibitively expensive to use. One of the

alternative global sensitivity analysis methods known as the method of

derivative based global sensitivity measures (DGSM) has recently become

popular among practitioners. It has a link with the Morris screening method

and Sobol’ sensitivity indices. DGSM are very easy to implement and evaluate

numerically. The computational time required for numerical evaluation of

DGSM is generally much lower than that for estimation of Sobol’ sensitivity

indices. We present a survey of recent advances in DGSM and new results

concerning new lower and upper bounds on the values of Sobol’ total

sensitivity indices . Using these bounds it is possible in most

cases to get a good practical estimation of the values of .

Several examples are used to illustrate an application of DGSM.

Keywords: Global sensitivity analysis; Monte Carlo methods; Quasi Monte Carlo methods; Derivative based global measures; Morris method; Sobol’ sensitivity indices

1 Introduction

Global sensitivity analysis (GSA) is the study of how the uncertainty in the

model output is apportioned to the uncertainty in model inputs

Salt2008 ,Sobol2005 . GSA can provide

valuable information regarding the dependence of the model output to its

input parameters. The variance-based method of global sensitivity indices

developed by Sobol’ Sobol1993 became very popular among

practitioners due to its efficiency and easiness of interpretation. There

are two types of Sobol’ sensitivity indices: the main effect indices, which

estimate the individual contribution of each input parameter to the output

variance, and the total sensitivity indices, which measure the total

contribution of a single input factor or a group of inputs Homma1996 . The total

sensitivity indices are used to identify non-important variables which can

then be fixed at their nominal values to reduce model complexity

Salt2008 . For high-dimensional models the direct

application of variance-based GSA measures can be extremely time-consuming

and impractical.

A number of alternative SA techniques have been proposed. In this paper we

present derivative based global sensitivity measures (DGSM) and their link

with Sobol’ sensitivity indices. DGSM are based on averaging local

derivatives using Monte Carlo or Quasi Monte Carlo sampling methods. These

measures were briefly introduced by Sobol’ and Gershman in

Sobol1995 . Kucherenko et al Kuch2009 introduced some other

derivative-based global sensitivity measures (DGSM) and coined the acronym

DGSM. They showed that the computational cost of numerical evaluation of

DGSM can be much lower than that for estimation of Sobol’ sensitivity

indices which later was confirmed in other works

Kiparis2009 . DGSM can be seen as a generalization and

formalization of the Morris importance measure also known as elementary

effects Morris1991 . Sobol’ and KucherenkoSobol2009 proved theoretically that there is a

link between DGSM and the Sobol’ total sensitivity index for

the same input. They showed that DGSM can be used as an upper bound on total

sensitivity index . They also introduced modified DGSM which can

be used for both a single input and groups of inputs

Sobol2010 . Such measures can be applied for problems

with a high number of input variables to reduce the computational time.

Lamboni et alLamboni2013 extended results of Sobol’ and

Kucherenko for models with input variables belonging to the class of

Boltzmann probability measures.

The numerical efficiency of the DGSM method can be improved by using the

automatic differentiation algorithm for calculation DGSM as was shown in

Kiparis2009 . However, the number of required function

evaluations still remains to be proportional to the number of inputs. This

dependence can be greatly reduced using an approach based on algorithmic

differentiation in the adjoint or reverse mode Griewank2008 .

It allows estimating all derivatives at a cost at most 4-6 times of that for

evaluating the original function Jansen2014 .

This paper is organised as follows: Section 2 presents Sobol’ global

sensitivity indices. DGSM and lower and upper bounds ontotal Sobol’ sensitivity indices for uniformly distributed variables and

random variables are presented in Sections 3 and 4, respectively. In Section

5 we consider test cases which illustrate an application of DGSM and their

links with total Sobol’ sensitivity indices. Finally, conclusions are

presented in Section 6.

2 Sobol’ global sensitivity indices

The method of global sensitivity indices developed by Sobol’ is based on

ANOVA decomposition Sobol1993 . Consider the square

integrable function defined in the unit hypercube

. The decomposition of

(1)

where , is called ANOVA if conditions

(2)

are satisfied for all different groups of indices such that . These conditions guarantee that all

terms in (1) are mutually orthogonal with respect to integration.

The variances of the terms in the ANOVA decomposition add up to the total variance:

where are called

partial variances.

Total partial variances account for the total influence of the factor :

where the sum is extended over all different groups of indices satisfying condition , , where one of the indices is equal to . The corresponding total sensitivity index is defined as

Denote the sum of

all terms in ANOVA decomposition (1) that depend on :

From the definition of ANOVA decomposition it follows that

(3)

The total partial variance can be computed as

Denote the vector

of all variables but , then and

. The ANOVA

decomposition of in

(1) can be presented in the following form

where is the sum of terms independent of . Because of

(2) and (3) it is easy to show that

. Hence

(4)

Then the total sensitivity index is equal to

(5)

We note that in the case of independent random variables all definitions

of the ANOVA decomposition remain to be correct but all derivations

should be considered in probabilistic sense as shown in Sobol2005

and presented in Section 4.

3 DGSM for uniformly distributed variables

Consider continuously differentiable function defined in the unit hypercube such that .

The Morris importance measure also known as elementary

effects originally defined as finite differences averaged over

a finite set of random points Morris1991 was generalized in Kuch2009 :

(7)

Kucherenko et al Kuch2009 also introduced a new DGSM

measure:

(8)

In this paper we define two new DGSM measures:

(9)

where is a constant, ,

(10)

We note that is in

fact the mean value of . We also note that

(11)

3.1 Lower bounds on

Theorem 3.2

There exists the following lower bound between DGSM (8)

and the Sobol’ total sensitivity index

(12)

Proof

Consider an integral

(13)

Applying the Cauchy–Schwarz inequality we obtain the following result:

(14)

It is easy to prove that the left and right parts of this inequality cannot

be equal. Indeed, for them to be equal functions and

should be linearly dependent. For simplicity

consider a one-dimensional case: . Let’s assume

where is a constant. The general solution to this equation

, where is a constant. It is easy to see that this

solution is not consistent with condition (3) which should be imposed on

function .

Integral can be transformed as

(15)

All terms in the last integrand are independent of , hence we can replace integration with

respect to to integration with respect to and substitute for in

the integrand due to condition (3). Then (15) can be presented as

(16)

From (11) , hence

the right hand side of (14) can be written as .

Finally dividing (14) by and using (16), we obtain the lower bound (12).

∎

We call

the lower bound number one (LB1).

Theorem 3.3

There exists the following lower bound between DGSM (9)

and the Sobol’ total sensitivity index

(17)

Proof

Consider an integral

(18)

Applying the Cauchy–Schwarz inequality we obtain the following result:

(19)

It is easy to see that equality in (19) cannot be attained. For this to

happen functions and should be

linearly dependent. For simplicity consider a one-dimensional case:

. Let’s assume

where is a constant. This solution does not satisfy condition (3) which should be

imposed on function .

Using (20) and (21) and dividing (19) by we obtain (17).

∎

This second lower bound on we denote :

(22)

In fact, this is a set of lower bounds depending on parameter . We are

interested in the value of at which attains its maximum. Further we use star to denote

such a value : and call

(23)

the lower bound number two (LB2).

We define the maximum lower bound as

(24)

We note that both lower and upper bounds can be estimated by a set of

derivative based measures:

The inequality is reduced to an equality only if is constant. Assume that

is given by (3), then , and from (28)

we obtain (27).

∎

Further we call the

upper bound number two (UB2). We note that for

is bounded: . Therefore, .

3.3 Computational costs

All DGSM can be computed using the same set of partial derivatives

. Evaluation of

can be done

analytically for explicitly given easily-differentiable functions or

numerically.

In the case of straightforward numerical estimations of all partial

derivatives and computation of integrals using MC or QMC methods, the

number of required function evaluations for a set of all input variables is

equal to , where is

a number of sampled points. Computing LB1 also requires values of

, while computing

LB2 requires only values of . In total, numerical computation of for all input variables would

require function

evaluations. Computation of all upper bounds require

function evaluations. We recall that

the number of function evaluations required for computation of

is

Salt2010 . The number of sampled points needed to

achieve numerical convergence can be different for DGSM and

. It is generally

lower for the case of DGSM. The numerical efficiency of the DGSM method can

be significantly increased by using algorithmic differentiation in the

adjoint (reverse) mode Griewank2008 . This approach allows

estimating all derivatives at a cost at most 6 times of that for

evaluating the original function Jansen2014 .

However, as mentioned above lower bounds also require computation of

so would only be reduced to

, while would be equal to .

4 DGSM for random variables

Consider a function , where are independent random variables with distribution functions

. Thus the point

is defined in the Euclidean space and

its measure is .

In this section we present the results of analytical and numerical

estimation of , , LB1, LB2 and UB1,

UB2. The analytical values for DGSM and were calculated and compared with numerical results.

For text case 2 we present convergence plots in the form of root mean square

error (RMSE) versus the number of sampled points . To reduce the scatter in

the error estimation the values of RMSE were averaged over = 25 independent

runs:

Here is numerically computed values of , LB1, LB2 or UB1, UB2, is the corresponding analytical value of

, LB1, LB2 or UB1,

UB2. The RMSE can be approximated by a trend line . Values of ( are given in brackets on the plots.

QMC integration based on Sobol’ sequences was used in all numerical tests.

Example 1. Consider a linear with respect to function:

For this function , ,

,

and .

A maximum value of is attained at =3.745, when .

The lower and upper bounds are . . . For this test function UB2 UB1.

Example 2. Consider the so-called g-function which is often used in

GSA for illustration purposes:

where ,

are constants. It

is easy to see that for this function ,

and as a result LB1=0. The total variance is . The analytical values of

, and LB2 are given in Table 1.

Table 1: The analytical expressions for , and LB2 for g-function

By solving equation

, we find that =9.64, .

It is interesting to note that does not depend on ,

and . In the extreme cases:

if

for all , , ,

while if for all , ,

. The analytical

expression for , UB1

and UB2 are given in Table 2.

Table 2: The analytical expressions for UB1 and UB2 for g-function

For this test function , , hence

. Values of , , UB and LB2 for the case of a=[0,1,4.5,9,99,99,99,99], =8 are given in Table 3

and shown in Figure 1. We can conclude that for this test function the knowledge of LB2

and UB1, UB2 allows to rank correctly all the variables in the order of

their importance.

Table 3: Values of LB*, , , UB1 and

UB1. Example 2, a=[0,1,4.5,9,99,99,99,99], =8.

Figure 1: Values of ,, LB2 and UB1 for

all input variables. Example 2,

a=[0,1,4.5,9,99,99,99,99], =8.

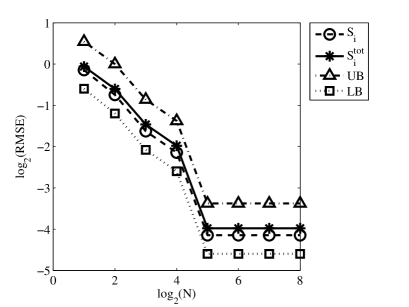

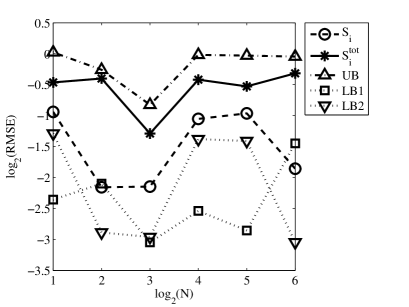

Fig. 2 presents RMSE of numerical estimations of , UB1 and LB2. For an individual input LB2 has the highest convergence rate, following by , and UB1 in terms of the number of sampled points. However, we recall that computation of all indices requires

function

evaluations for LB, while for this number is and for UB it is also .

Figure 2: RMSE of , UB

and LB2 versus the number of sampled points. Example 2,

a=[0,1,4.5,9,99,99,99,99], =8. Variable 1 (a), variable

3 (b) and variable 5 (c).

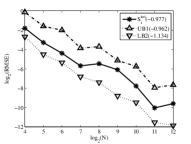

Example 3. Hartmann function , . For this test case a relationship between the values LB1, LB2 and

varies with the

change of input (Table 4, Figure 3): for variables and LB1

LB2, while for all other variables LB1

LB2 . LB* is much smaller than

for all inputs.

Values of * also vary with the change of input. For all variables but variable 2

UB1 UB2.

Figure 3: Values of ,, UB1, LB1 and LB2

for all input variables. Example 3.

Table 4: Values of , LB1, LB2, UB1, UB2, and for all input variables.

6 Conclusions

We can conclude that using lower and upper bounds based on DGSM it is

possible in most cases to get a good practical estimation of the values of

at a fraction

of the CPU cost for estimating . Small values of upper bounds imply small values of

. DGSM can be used

for fixing unimportant variables and subsequent model reduction. For linear

function and product function, DGSM can give the same variable ranking as

. In a general case

variable ranking can be different for DGSM and variance based methods. Upper

and lower bounds can be estimated using MC/QMC integration methods using the

same set of partial derivative values. Partial derivatives can be efficiently

estimated using algorithmic differentiation in the reverse (adjoint) mode.

We note that all bounds should be computed with sufficient accuracy. Standard

techniques for monitoring convergence and accuracy of MC/QMC estimates

should be applied to avoid erroneous results.

Acknowledgements.

The authors would like to thank Prof. I. Sobol’ his invaluable contributions

to this work. Authors also gratefully acknowledge the financial support by

the EPSRC grant EP/H03126X/1.

References

(1)

A. Griewank and A. Walther.

Evaluating derivatives: Principles and techniques

of algorithmic differentiation.SIAM Philadelphia, PA, 2008.

(2)

G.H. Hardy, J.E. Littlewood and G. Polya.

Inequalities.Cambridge University Press, Second edition, 1973.

(3)

T. Homma and A. Saltelli.

Importance measures in global sensitivity analysis of

model output.

Reliability Engineering and System Safety, 52(1):1–17, 1996.

(4)

K. Jansen, H. Leovey, A. Nube, A. Griewank. and M. Mueller-Preussker.

A first look at quasi-Monte Carlo for lattice field theory problems.

Comput. Phys. Commun., 185:948–959, 2014.

(5)

A. Kiparissides, S. Kucherenko, A. Mantalaris and E.N. Pistikopoulos.

Global sensitivity analysis challenges in biological systems modeling.

J. Ind. Eng. Chem. Res., 48(15):7168–7180, 2009.

(6)

S. Kucherenko, M.Rodriguez-Fernandez, C.Pantelides and N.Shah.

Monte Carlo evaluation of derivative based global sensitivity measures

Reliability Engineering and System Safety, 94(7):1135–1148, 2009.

(7)

M. Lamboni, B. Iooss, A.L. Popelin and F. Gamboa.

Derivative based global sensitivity measures: general links with Sobol’s indices and numerical

tests.

Math. Comput. Simulat., 87:45–54, 2013.

(9)

A. Saltelli, M. Ratto, T. Andres, F. Campolongo, J. Cariboni, D. Gatelli, M.

Saisana and S. Tarantola.

Global sensitivity analysis: The Primer. Wiley, New York, 2008.

(10)

A. Saltelli, P. Annoni, I. Azzini, F. Campolongo, M. Ratto and S. Tarantola.

Variance based sensitivity analysis of model output: Design and estimator

for the total sensitivity index.

Comput. Phys. Commun., 181(2):259–270, 2010.

(11)

I.M. Sobol’

Sensitivity estimates for nonlinear mathematical models.

Matem.

Modelirovanie , 2: 112-118, 1990 (in Russian). English translation: Math.

Modelling and Comput. Experiment, 1(4):407–414, 1993.

(12)

I.M. Sobol’ and A. Gershman.

On an altenative global sensitivity estimators. In Proc SAMO, Belgirate, 1995. pages 40–42, 1995.

(13)

I.M. Sobol’.

Global sensitivity indices for nonlinear mathematical models

and their Monte Carlo estimates.

Math. Comput. Simulat. 55(1-3):271–280, 2001.

(14)

I.M. Sobol’ and S. Kucherenko.

Global sensitivity indices for nonlinear mathematical models. Review.

Wilmott Magazine, 1:56–61, 2005.

(15)

I.M. Sobol’ and S. Kucherenko.

Derivative based global sensitivity measures and their link with global sensitivity indices.

Math. Comput. Simulat., 79(10):3009–3017, 2009.

(16)

I.M. Sobol’ and S. Kucherenko.

A new derivative based importance criterion for groups of variables and its link with the global sensitivity indices.

Comput. Phys. Commun., 181(7):1212–1217, 2010.