Near-optimal Bayesian Active Learning

with Correlated and Noisy Tests

Abstract

We consider the Bayesian active learning and experimental design problem, where the goal is to learn the value of some unknown target variable through a sequence of informative, noisy tests. In contrast to prior work, we focus on the challenging, yet practically relevant setting where test outcomes can be conditionally dependent given the hidden target variable. Under such assumptions, common heuristics, such as greedily performing tests that maximize the reduction in uncertainty of the target, often perform poorly.

In this paper, we propose ECED, a novel, computationally efficient active learning algorithm, and prove strong theoretical guarantees that hold with correlated, noisy tests. Rather than directly optimizing the prediction error, at each step, ECED picks the test that maximizes the gain in a surrogate objective, which takes into account the dependencies between tests. Our analysis relies on an information-theoretic auxiliary function to track the progress of ECED, and utilizes adaptive submodularity to attain the near-optimal bound. We demonstrate strong empirical performance of ECED on two problem instances, including a Bayesian experimental design task intended to distinguish among economic theories of how people make risky decisions, and an active preference learning task via pairwise comparisons.

1 Introduction

Optimal information gathering, i.e., selectively acquiring the most useful data, is one of the central challenges in machine learning. The problem of optimal information gathering has been studied in the context of active learning (Dasgupta, 2004a; Settles, 2012), Bayesian experimental design (Chaloner & Verdinelli, 1995), policy making (Runge et al., 2011), optimal control (Smallwood & Sondik, 1973), and numerous other domains. In a typical set-up for these problems, there is some unknown target variable of interest, and a set of tests which correspond to observable variables defined through a probabilistic model. The goal is to determine the value of the target variable with a sequential policy – which adaptively selects the next test based on previous observations – such that the cost of performing these tests is minimized.

Deriving the optimal testing policy is NP-hard in general (Chakaravarthy et al., 2007); however, under certain conditions, some approximation results are known. In particular, if test outcomes are deterministic functions of the target variable (i.e., in the noise-free setting), a simple greedy algorithm, namely Generalized Binary Search (GBS), is guaranteed to provide a near-optimal approximation of the optimal policy (Kosaraju et al., 1999). On the other hand, if test outcomes are noisy, but the outcomes of different tests are conditionally independent given (i.e., under the Naïve Bayes assumption), then using the most informative selection policy, which greedily selects the test that maximizes the expected reduction in uncertainty of the target variable (quantified in terms of Shannon entropy), is guaranteed to perform near-optimally (Chen et al., 2015a).

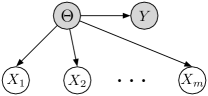

However, in many practical problems, due to the effect of noise or complex structural assumptions in the probabilistic model (beyond Naïve Bayes), we only have access to tests that are indirectly informative about the target variable (i.e., test outcomes depend on through another hidden random variable. See Fig. 1.) – as a consequence, the test outcomes become conditionally dependent given . Consider a medical diagnosis example, where a doctor wants to predict the best treatment for a patient, by carrying out a series of medical tests, each of which reveals some information about the patient’s physical condition. Here, outcomes of medical tests are conditionally independent given the patient’s condition, but are not independent given the treatment, which is made based on the patient’s condition. It is known that in such cases, both GBS and the most informative selection policy (which myopically maximizes the information gain w.r.t. the distribution over ) can perform arbitrarily poorly. Golovin et al. (2010) then formalize this problem as an equivalence class determination problem (See §2.1), and show that if the tests’ outcomes are noise-free, then one can obtain near-optimal expected cost, by running a greedy policy based on a surrogate objective function. Their results rely on the fact that the surrogate objective function exhibits adaptive submodularity (Golovin & Krause, 2011), a natural diminishing returns property that generalizes the classical notion of submodularity to adaptive policies. Unfortunately, in the more general setting where tests are noisy, no efficient policies are known to be provably competitive with the optimal policy.

Our Contribution.

In this paper, we introduce Equivalence Class Edge Discounting (ECED), a novel algorithm for practical Bayesian active learning and experimental design problems, and prove strong theoretical guarantees with correlated, noisy tests. In particular, we focus on the setting where the tests’ outcomes indirectly depend on the target variable (and hence conditionally dependent given ), and we assume that the outcome of each test can be corrupted by some random, persistent noise (§2). We prove that when the test outcomes are binary, and the noise on test outcomes are mutually independent, then ECED is guaranteed to obtain near-optimal cost, compared with an optimal policy that achieves a lower prediction error (§3). We develop a theoretical framework for analyzing such sequential policies, where we leverage an information-theoretic auxiliary function to reason about the effect of noise, and combine it with the theory of adaptive submodularity to attain the near-optimal bound (§4). The key insight is to show that ECED is effectively making progress in the long run as it picks more tests, even if the myopic choices of tests do not have immediate gain in terms of reducing the uncertainty of the target variable. We demonstrate the compelling performance of ECED on two real-world problem instances, a Bayesian experimental design task intended to distinguish among economic theories of how people make risky decisions, and an active preference learning task via pairwise comparisons (§5). To facilitate better understanding, we provide the detailed proofs, illustrative examples and a third application on pool-based active learning in the supplemental material.

2 Preliminaries and Problem Statement

The Basic Model

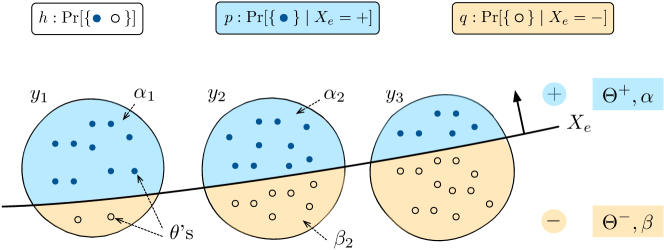

Let be the target random variable whose value we want to learn. The value of , which ranges among set , depends deterministically on another random variable with some known distribution . Concretely, there is a deterministic mapping that gives . Let be a collection of discrete observable variables that are statistically dependent on (see Fig. 1).

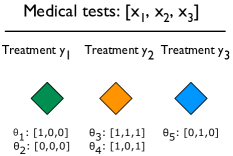

We use as the indexing variable of a test. Performing each test produces an outcome (here, encodes the set of possible outcomes of a test), and incurs a unit cost. We can think of as representing the underlying “root-cause” among a set of possible root-causes of the joint event , and as representing the optimal “target action” to be taken for root-cause . Also, each of the ’s is a “test” that we can perform, whose observation reveals some information about . In our medical diagnosis example (see Fig. 2(a)), ’s encode tests’ outcomes, encodes the treatment, and encodes the patient’s physical condition.

Crucially, we assume that ’s are conditionally independent given , i.e., with known parameters. Note that noise is implicitly encoded in our model, as we can equivalently assume that ’s are first generated from a deterministic mapping of , and then perturbed by some random noise. As an example, if test outcomes are binary, then we can think of as resulting from flipping the deterministic outcome of test given with some probability, and the flipping events of the tests are mutually independent.

Problem Statement

We consider sequential, adaptive policies for picking the tests. Denote a policy by . In words, a policy specifies which test to pick next, as well as when to stop picking tests, based on the tests picked so far and their corresponding outcomes. After each pick, our observations so far can be represented as a partial realization (e.g., encodes what tests have been performed and what their outcomes are). Formally, a policy is defined to be a partial mapping from partial realizations to tests. Suppose that running till termination returns a sequence of test-observation pairs of length , denoted by , i.e., . This can be interpreted as a random path111What returns in the end is random, dependent on the outcomes of selected tests. taken by policy . Once is observed, we obtain a new posterior on (and consequently on ). After observing , the MAP estimator of has error probability . The expected error probability after running policy is then defined as . In words, is the expected error probability w.r.t. the posterior, given the final outcome of . Let the (worst-case) cost of a policy be , i.e., the maximum number of tests performed by over all possible paths it takes. Given some small tolerance , we seek a policy with the minimal cost, such that upon termination, it will achieve expected error probability less than . Denote such policy by . Formally, we seek

| (2.1) |

2.1 Special Case: The Equivalence Class Determination Problem

Note that computing the optimal policy for Problem (2.1) is intractable in general. When , this problem reduces to the equivalence class determination problem (Golovin et al., 2010; Bellala et al., 2010). Here, the target variables are referred to as equivalence classes, since each corresponds to a subset of root-causes in that (equivalently) share the same “action”.

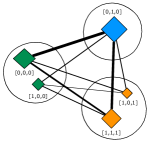

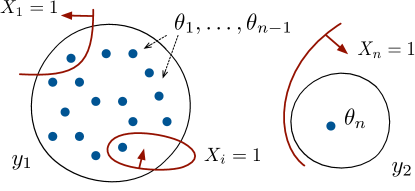

If tests are noise-free, i.e., , this problem can be solved near-optimally by the equivalence class edge cutting () algorithm (Golovin et al., 2010). As is illustrated in Fig. 2, employs an edge-cutting strategy based on a weighted graph , where vertices represent root-causes, and edges link root-causes that we want to distinguish between. Formally, consists of all (unordered) pairs of root-causes corresponding to different target values (see Fig. 2(b)). We define a weight function by , i.e., as the product of the probabilities of its incident root-causes. We extend the weight function on sets of edges , as the sum of weight of all edges , i.e., .

Performing test with outcome is said to “cut” an edge, if at least one of its incident root-causes is inconsistent with (See Fig. 2(c)). Denote as the set of edges cut by observing . The objective (which is greedily maximized per iteration of ), is then defined as the total weight of edges cut by the current partial observation :

The objective function is adaptive submodular, and strongly adaptive monotone (Golovin et al., 2010). Formally, let be two partial realizations of tests’ outcomes. We call a subrealization of , denoted as , if every test seen by is also seen by , and . A function is called adaptive submodular w.r.t. a distribution , if for any and any it holds that , where (i.e., “adding information earlier helps more”). Further, function is called strongly adaptively monotone w.r.t. , if for all , test not seen by , and , it holds that (i.e., “adding new information never hurts”). For sequential decision problems satisfying adaptive submodularity and strongly adaptive monotonicity, the policy that greedily, upon having observed , selects the test , is guaranteed to attain near-minimal cost (Golovin & Krause, 2011).

In the noisy setting, however, we can no longer attain 0 error probability (or equivalently, cut all the edges constructed for ), even if we exhaust all tests. A natural approach to solving Problem (2.1) for would be to pick tests greedily maximizing the expected reduction in the error probability . However, this objective is not adaptive submodular; in fact, as we show in the supplemental material, such policy can perform arbitrarily badly if there are complementaries among tests, i.e., the gain of a set of tests can be far better than sum of the individual gains of the tests in the set. Therefore, motivated by the objective in the noise-free setting, we would like to optimize a surrogate objective function which captures the effect of noise, while being amenable to greedy optimization.

3 The ECED Algorithm

We now introduce ECED for Bayesian active learning under correlated noisy tests, which strictly generalizes to the noisy setting, while preserving the near-optimal guarantee.

with Bayesian Updates on Edge Weights

In the noisy setting, the test outcomes are not necessarily deterministic given a root-cause, i.e., . Therefore, one can no longer “cut away” a root-cause by observing , as long as . In such cases, a natural extension of the edge-cutting strategy will be – instead of cutting off edges – to discount the edge weights through Bayesian updates: After observing , we can discount the weight of an edge , by multiplying the probabilities of its incident root-causes with the likelihoods of the observation222Here we choose not to normalize the probabilities of to their posterior probabilities. Otherwise, we can end up having 0 gain in terms of edge weight reduction, even if we perform a very informative test.: . This gives us a greedy policy that, at every iteration, picks the test that has the maximal expected reduction in total edge weight. We call such policy -Bayes. Unfortunately, as we demonstrate later in §5, this seemingly promising update scheme is not ideal for solving our problem: it tends to pick tests that are very noisy, which do not help facilitate differentiation among different target values. Consider a simple example with three root-causes distributed as , and two target values . We want to evaluate two tests: (1) a purely noisy test , i.e., , and (2) a noiseless test with and . One can easily verify that by running -Bayes, one actually prefers (with expected reduction in edge weight 0.18, as opposed to 0.112 for ).

The ECED Algorithm

The example above hints us on an important principle of designing proper objective functions for this task: as the noise rate increases, one must take reasonable precautions when evaluating the informativeness of a test, such that the undesired contribution by noise is accounted for. Suppose we have performed test and observed . We call a root-cause to be “consistent” with observation , if is the most likely outcome of given (i.e., ). Otherwise, we say is inconsistent. Now, instead of discounting the weight of all root-causes by the likelihoods (as -Bayes does), we choose to discount the root-causes by the likelihood ratio: . Intuitively, this is because we want to “penalize” a root-cause (and hence the weight of its incident edges), only if it is inconsistent with the observation (See Fig. 2(d)). When is consistent with root-cause , then and we do not discount ; otherwise, if is inconsistent with , we have . When a test is not informative for root-cause , i.e. is uniform, then , so that it neutralizes the effect of such test in terms of edge weight reduction. Formally, given observations , we define the value of observing as the total amount of edge weight discounted: .

Further, we call test to be non-informative, if its outcome does not affect the distribution of , i.e., and , . Obviously, performing a non-informative test does not reveal any useful information of (and hence ). Therefore, we should augment our basic value function , such that the value of a non-informative test is 0. Following this principle, we define , as the offset value for observing outcome . It is easy to check that if test is non-informative, then it holds that for all ; otherwise . This motivates us to use the following objective function:

| (3.1) |

as the expected amount of edge weight that is effectively reduced by performing test . We call the algorithm that greedily maximizes the Equivalence Class Edge Discounting (ECED) algorithm, and present the pseudocode in Algorithm 1.

Similar with , the efficiency (in terms of computation complexity as well as the query complexity) of ECED depends on the number of root-causes. Let be the noise rate for test . As our main theoretical result, we show that under the basic setting where test outcomes are binary, and the test noise is independent of the underlying root-causes (i.e., ), ECED is competitive with the optimal policy that achieves a lower error probability for Problem (2.1):

Theorem 1.

Fix . To achieve expected error probability less than , it suffices to run ECED for steps where denotes the number of root-causes, characterizes the severity of noise, and is the worst-case cost of the optimal policy that achieves expected error probability .

Note that a pessimistic upper bound for is the total number of tests , and hence the cost of ECED is at most times the worst-case cost of the optimal algorithm, which achieves a lower error probability . Further, as one can observe, the upper bound on the cost of ECED degrades as we increase the maximal noise rate of the tests. When , we have for all test , and ECED reduces to the algorithm. Theorem 1 implies that running for in the noise-free setting is sufficient to achieve . Finally, notice that by construction ECED never selects any non-informative test. Therefore, we can always remove purely noisy tests (i.e., ), so that , and the upper bound in Theorem 1 becomes non-trivial.

4 Theoretical Analysis

Information-theoretic Auxiliary Function

We now present the main idea behind the proof of Theorem 1. In general, an effective way to relate the performance (measured in terms of the gain in the target objective function) of the greedy policy to the optimal policy is by showing that, the one-step gain of the greedy policy always makes effective progress towards approaching the cumulative gain of OPT over steps. One powerful tool facilitating this is the adaptive submodularity theory, which imposes a lower bound on the one-step greedy gain against the optimal policy, given that the objective function in consideration exhibits a natural diminishing returns condition. Unfortunately, in our context, the target function to optimize, i.e., the expected error probability of a policy, does not satisfy adaptive submodularity. Furthermore, it is nontrivial to understand how one can directly relate the two objectives: the ECED objective of (3.1), which we utilize for selecting informative tests, and the gain in the reduction of error probability, which we use for evaluating a policy.

We circumvent such problems by introducing surrogate functions, as a proxy to connect the ECED objective with the expected reduction in error probability . Ideally, we aim to find some auxiliary objective , such that the tests with the maximal also have a high gain in ; meanwhile, should also be comparable with the error probability , such that minimizing itself is sufficient for achieving low error probability.

We consider the function , defined as

| (4.1) |

Here , and is a constant that will be made concrete shortly (in Lemma 3). Interestingly, we show that function is intrinsically linked to the error probability:

Lemma 2.

We consider the auxiliary function defined in Equation (4.1). Let be the number of root-causes, and be the error probability given partial realization . Then

Therefore, if we can show that by running ECED, we can effectively reduce , then by Lemma 2, we can conclude that ECED also makes significant progress in reducing the error probability .

Bounding the Gain w.r.t. the Auxiliary Function

It remains to understand how ECED interacts with . For any test , we define to be the expected gain of test in . Let denote the gain of test in the objective, assuming that the edge weights are configured according to the posterior distribution . Similarly, let denote the ECED gain, if the edge weights are configured according to . We prove the following result:

Lemma 3.

Let , , and be the noise rate associated with test . Fix . We consider as defined in Equation (4.1), with . It holds that

where , and .

Lemma 3 indicates that the test being selected by ECED can effectively reduce .

Lifting the Adaptive Submodularity Framework

Recall that our general strategy is to bound the one step gain in against the gain of an optimal policy. In order to do so, we need to show that our surrogate exhibits, to some extent, the diminishing returns property. By Lemma 3 we can relate , i.e., the gain in under the noisy setting, to , i.e., the expected weight of edges cut by the algorithm. Since is adaptive submodular, this allows us to lift the adaptive submodularity framework into the analysis. As a result, we can now relate the 1-step gain w.r.t. of a test selected by ECED, to the cumulative gain w.r.t. of an optimal policy in the noise-free setting. Further, observe that the objective at satisfies:

| (4.2) |

Hereby, step (a) is due to the fact that the error probability of a MAP estimator always lower bounds that of a stochastic estimator (which is drawn randomly according to the posterior distribution of ). Suppose we want to compare ECED against an optimal policy . By adaptive submodularity, we can relate the 1-step gain of ECED in to the cummulative gain of . Combining Equation (4.2) with Lemma 2 and Lemma 3, we can bound the 1-step gain in of ECED against the -step gain of , and consequently bound the cost of ECED against for Problem 2.1. We defer a more detailed proof outline and the full proof to the supplemental material.

5 Experimental Results

We now demonstrate the performance of ECED on two real-world problem instances: a Bayesian experimental design task intended to distinguish among economic theories of how people make risky decisions, and an active preference learning task via pairwise comparisons. Due to space limitations, we defer a third case study on pool-based active learning to the supplemental material.

Baselines.

The first baseline we consider is -Bayes, which uses the Bayes’ rule to update the edge weights when computing the gain of a test (as described in §3). Note that after observing the outcome of a test, both ECED and -Bayes update the posteriors on and according to the Bayes’ rule; the only difference is that they use different strategies when selecting a test. We also compare with two commonly used sequential information gathering policies: Information Gain (IG), and Uncertainty Sampling (US), which consider picking tests that greedily maximizing the reduction of entropy over the target variable , and root-causes respectively. Last, we consider myopic optimization of the decision-theoretic value of information (VoI) (Howard, 1966). In our problems, the VoI policy greedily picks the test maximizing the expected reduction in prediction error in .

5.1 Preference Elicitation in Behavioral Economics

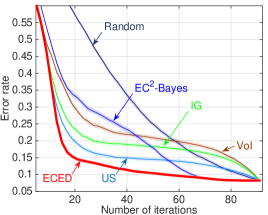

We first conduct experiments on a Bayesian experimental design task, which intends to distinguish among economic theories of how people make risky decisions. Several theories have been proposed in behavioral economics to explain how people make decisions under risk and uncertainty. We test ECED on six theories of subjective valuation of risky choices (Wakker, 2010; Tversky & Kahneman, 1992; Sharpe, 1964), namely (1) expected utility with constant relative risk aversion, (2) expected value, (3) prospect theory, (4) cumulative prospect theory, (5) weighted moments, and (6) weighted standardized moments. Choices are between risky lotteries, i.e., known distribution over payoffs (e.g., the monetary value gained or lost). A test is a pair of lotteries, and root-causes correspond to parametrized theories that predict, for a given test, which lottery is preferable. The goal, is to adaptively select a sequence of tests to present to a human subject in order to distinguish which of the six theories best explains the subject’s responses. We employ the same set of parameters used in Ray et al. (2012) to generate tests and root-causes. In particular, we have generated 16K tests. Given root-cause and test , one can compute the values of and , denoted by and . Then, the probability that root-cause favors is modeled as .

Results

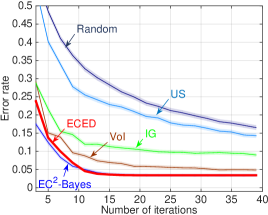

Fig. 3(a) demonstrates the performance of ECED on this data set. The average error probability has been computed across 1000 random trials for all methods. We observe that ECED and -Bayes have similar behavior on this data set; however, the performance of the US algorithm is much worse. This can be explained by the nature of the data set: it has more concentrated distribution over , but not . Therefore, since tests only provide indirect information about through , what the uncertainty sampling scheme tries to optimize is actually , hence it performs quite poorly.

5.2 Preference Learning via Pairwise Comparisons

The second application considers a comparison-based movie recommendation system, which learns a user’s movie preference (e.g., the favorable genre) by sequentially showing her pairs of candidate movies, and letting her choose which one she prefers. We use the MovieLens 100k dataset (Herlocker et al., 1999), which consists of a matrix of 1 to 5 ratings of 1682 movies from 943 users, and adopt the experimental setup proposed in Chen et al. (2015b). In particular, we extract movie features by computing a low-rank approximation of the user/rating matrix of the MovieLens 100k dataset through singular value decomposition (SVD). We then simulate the target “categories” that a user may be interested by partitioning the set of movies into (non-overlapping) clusters in the Euclidean space. A root-cause corresponds to user’s favorite movie, and tests ’s are given in the form of movie pairs, i.e., , where and are embeddings of movie and in Euclidean space. Suppose user’s movie is represented by , then test is realized as if is closer to than , and otherwise. We simulate the effect of noise by . where is the distance function, and control the level of noise in the system.

Results

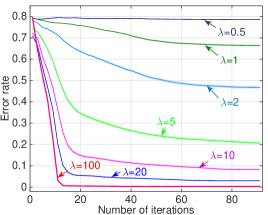

Fig. 3(b) shows the performance of ECED compared other baseline methods, when we fix the size of to be 20 and to be 10. We compute the average error probability across 1000 random trials for all methods. We can see that ECED consistently outperforms all other baselines. Interestingly, -Bayes performs poorly on this data set. This may be due to the fact that the noise level is still high, misguiding the two heuristics to select noisy, uninformative tests. Fig. 3(c) shows the performance of ECED as we vary . When , the tests become close to deterministic given a root-cause, and ECED is able to achieve error with tests. As we increase the noise rate (i.e., decrease ), it takes ECED many more queries for the prediction error to converge. This is because with high noise rate, ECED discounts the root-causes more uniformly, hence they are hardly informative in . This comes at the cost of performing more tests, and hence low convergence rate.

6 Related Work

Active learning in statistical learning theory.

In most of the theoretical active learning literature (e.g., Dasgupta (2004b); Hanneke (2007, 2014); Balcan & Urner (2015)), sample complexity bounds have been characterized in terms of the structure of the hypothesis class, as well as additional distribution-dependent complexity measures (e.g., splitting index (Dasgupta, 2004b), disagreement coefficient (Hanneke, 2007), etc); In comparison, in this paper we seek computationally-efficient approaches that are provably competitive with the optimal policy. Therefore, we do not seek to bound how the optimal policy behaves, and hence we make no assumptions on the hypothesis class.

Persistent noise vs non-persistent noise.

If tests can be repeated with i.i.d. outcomes, the noisy problem can then be effectively reduced to the noise-free setting (Kääriäinen, 2006; Karp & Kleinberg, 2007; Nowak, 2009). While the modeling of non-persistent noise may be appropriate in some settings (e.g., if the noise is due to measurement error), it is often important to consider the setting of persistent noise in many other applications. In many applications, repeating tests are impossible, or repeating a test produces identical outcomes. For example, it could be unrealistic to replicate a medical test for practical clinical treatment. Despite of some recent development in dealing with persistent noise in simple graphical models (Chen et al., 2015a) and strict noise assumptions (Golovin et al., 2010), more general settings, which we focus on in this paper, are much less understood.

7 Conclusion

We have introduced ECED, which strictly generalizes the algorithm, for solving practical Bayesian active learning and experimental design problems with correlated and noisy tests. We have proved that ECED enjoys strong theoretical guarantees, by introducing an analysis framework that draws upon adaptive submodularity and information theory. We have demonstrated the compelling performance of ECED on two (noisy) problem instances, including an active preference learning task via pairwise comparisons, and a Bayesian experimental design task for preference elicitation in behavioral economics. We believe that our work makes an important step towards understanding the theoretical aspects of complex, sequential information gathering problems, and provides useful insight on how to develop practical algorithms to address noise.

Acknowledgments

This work was supported in part by ERC StG 307036, a Microsoft Research Faculty Fellowship, and a Google European Doctoral Fellowship.

References

- Balcan & Urner (2015) Balcan, Maria-Florina and Urner, Ruth. Active learning–modern learning theory. Encyclopedia of Algorithms, 2015.

- Bellala et al. (2010) Bellala, G., Bhavnani, S., and Scott, C. Extensions of generalized binary search to group identification and exponential costs. In NIPS, 2010.

- Chakaravarthy et al. (2007) Chakaravarthy, V. T., Pandit, V., Roy, S., Awasthi, P., and Mohania, M. Decision trees for entity identification: Approximation algorithms and hardness results. In SIGMOD/PODS, 2007.

- Chaloner & Verdinelli (1995) Chaloner, K. and Verdinelli, I. Bayesian experimental design: A review. Statistical Science, 10(3):273–304, 1995.

- Chen & Krause (2013) Chen, Yuxin and Krause, Andreas. Near-optimal batch mode active learning and adaptive submodular optimization. In ICML, 2013.

- Chen et al. (2015a) Chen, Yuxin, Hassani, S. Hamed, Karbasi, Amin, and Krause, Andreas. Sequential information maximization: When is greedy near-optimal? In COLT, 2015a.

- Chen et al. (2015b) Chen, Yuxin, Javdani, Shervin, Karbasi, Amin, Bagnell, James Andrew, Srinivasa, Siddhartha, and Krause, Andreas. Submodular surrogates for value of information. In AAAI, 2015b.

- Dasgupta (2004a) Dasgupta, S. Analysis of a greedy active learning strategy. In NIPS, 2004a.

- Dasgupta (2004b) Dasgupta, Sanjoy. Analysis of a greedy active learning strategy. In NIPS, 2004b.

- Golovin & Krause (2011) Golovin, Daniel and Krause, Andreas. Adaptive submodularity: Theory and applications in active learning and stochastic optimization. JAIR, 2011.

- Golovin et al. (2010) Golovin, Daniel, Krause, Andreas, and Ray, Debajyoti. Near-optimal bayesian active learning with noisy observations. In NIPS, 2010.

- Hanneke (2007) Hanneke, Steve. A bound on the label complexity of agnostic active learning. In ICML, 2007.

- Hanneke (2014) Hanneke, Steve. Theory of disagreement-based active learning. Foundations and Trends® in Machine Learning, 7(2-3):131–309, 2014.

- Herlocker et al. (1999) Herlocker, Jonathan L., Konstan, Joseph A., Borchers, Al, and Riedl, John. An algorithmic framework for performing collaborative filtering. In SIGIR, 1999.

- Howard (1966) Howard, R.A. Information value theory. Systems Science and Cybernetics, IEEE Trans. on, 2(1):22–26, 1966.

- Kääriäinen (2006) Kääriäinen, Matti. Active learning in the non-realizable case. In Algorithmic Learning Theory, pp. 63–77, 2006.

- Karp & Kleinberg (2007) Karp, Richard M and Kleinberg, Robert. Noisy binary search and its applications. In SODA, 2007.

- Kosaraju et al. (1999) Kosaraju, S Rao, Przytycka, Teresa M, and Borgstrom, Ryan. On an optimal split tree problem. In Algorithms and Data Structures, pp. 157–168. Springer, 1999.

- Nowak (2009) Nowak, Robert. Noisy generalized binary search. In NIPS, 2009.

- Ray et al. (2012) Ray, Debajyoti, Golovin, Daniel, Krause, Andreas, and Camerer, Colin. Bayesian rapid optimal adaptive design (broad): Method and application distinguishing models of risky choice. Tech. Report, 2012.

- Runge et al. (2011) Runge, M. C., Converse, S. J., and Lyons, J. E. Which uncertainty? using expert elicitation and expected value of information to design an adaptive program. Biological Conservation, 2011.

- Settles (2012) Settles, B. Active Learning. Morgan & Claypool, 2012.

- Sharpe (1964) Sharpe, William F. Capital Asset Prices: A Theory of Market Equilibrium under Conditions of Risk. The Journal of Finance, 1964.

- Smallwood & Sondik (1973) Smallwood, Richard D and Sondik, Edward J. The optimal control of partially observable markov processes over a finite horizon. Operations Research, 21(5):1071–1088, 1973.

- Tversky & Kahneman (1992) Tversky, Amos and Kahneman, Daniel. Advances in prospect theory: Cumulative representation of uncertainty. Journal of Risk and Uncertainty, 5(4), 1992.

- Wakker (2010) Wakker, P.P. Prospect Theory: For Risk and Ambiguity. Cambridge University Press, 2010.

Appendix A Table of Notations Defined in the Main Paper

We summarize the notations used in the main paper in Table 1.

| random variable encoding the value of the target variable | |

|---|---|

| domain of the target variable | |

| value of | |

| random variable encoding the root-cause | |

| the ground set / domain of root-causes | |

| root-cause | |

| , a function that maps a root-cause to a target value | |

| the ground set of tests | |

| , number of tests | |

| test | |

| random variable encoding the test outcome | |

| observed test outcome | |

| , number of possible target values | |

| , number of root-causes | |

| policy, i.e., a (partial) mapping from observation vectors to tests | |

| random variable encoding a partial realization, i.e., set of test-observation pairs | |

| the partial realization, i.e., set of test-observation pairs observed by running policy | |

| tolerance of prediction error | |

| error probability (of a MAP decoder), having observed partial realization | |

| , expected error probability by running policy | |

| optimal policy for Problem (2.1) | |

| , the (weighted) graph constructed for the algorithm | |

| weight of edge in the graph | |

| the objective function, with . | |

| the objective function, with . | |

| discount coefficient of root-cause , used by ECED when computing . | |

| , the noise rate for a test | |

| the “basic” component in the ECED gain by observing , having observed | |

| the “offset” component in the ECED gain by observing , having observed | |

| the ECED gain which is myopically optimized at each iteration of the ECED algorithm | |

| suppose we have observed , and re-initialize the graph so that the total edge weight is . Then, is the expected reduction in edge weight, by performing test and discounting edges’ weight according to ECED. It is the re-normalized version of , i.e., . | |

| the expected gain in by performing test , and cutting edges weight according to . It can be interpreted as , as if the test’s outcome is noise-free, i.e., . | |

| the auxiliary function defined in Equation (4.1) | |

| parameter of (see Equation (4.1), Lemma 3). It is only used for analysis. | |

| , parameter of . It is only used for the analysis of ECED. | |

| the expected gain in by performing test , conditioning on partial realization | |

| constants required by Lemma 3 | |

| parameter controlling the error rate of tests (see §5) |

Appendix B The Analysis Framework

In this section, we provide the proofs of our theoretical results in full detail. Recall that for the theoretical analysis, we study the basic setting where test outcomes are binary, and the test noise is independent of the underlying root-causes (i.e., given a test , the noise rate on the outcome of test is only a function of , but not a function of ).

B.1 The Auxiliary Function and the Proof Outline

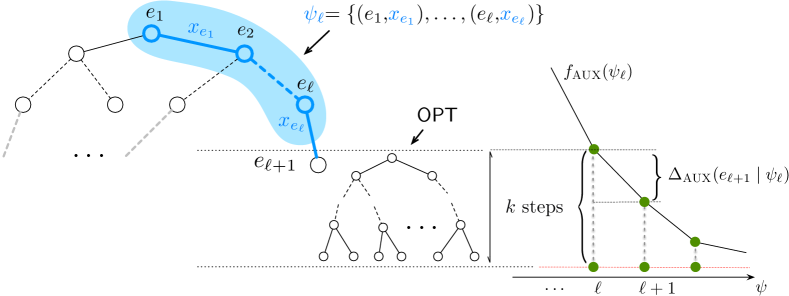

The general idea behind our analysis, is to show that by running ECED, the one-step gain in learning the value of the target variable is significant, compared with the cumulative gain of an optimal policy over steps (see Fig. 4).

In Appendix §C, we show that if tests are greedily selected to optimize the (reduction in) expected prediction error, we may end up failing to pick some tests, which have negligible immediate gain in terms of error reduction, but are very informative in the long run. ECED bypasses such an issue by selecting tests that maximally distinguish root-causes with different target values. In order to analyze ECED, we need to find an auxiliary function that properly tracks the “progress” of the ECED algorithm; meanwhile, this auxiliary function should allow us to connect the heuristic by which we select tests (i.e., ), with the target objective of interest (i.e., the expected prediction error ).

We consider the auxiliary function defined in Equation (4.1). For brevity, we suppress the dependence of where it is unambiguous. Further, we use , , and as shorthand notations for , and . Equation (4.1) can be simplified as

| (B.1) |

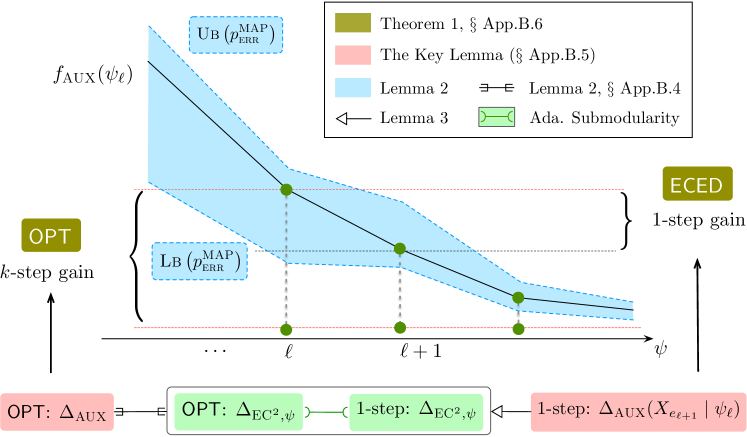

We illustrate the outline of our proofs in Fig. 5. Our goal is to bound the cost of ![]() against the cost of

against the cost of ![]() (Theorem 1; proof provided in Appendix §B.6). As we have explained earlier, our strategy is to relate the one-step gain of ECED

(Theorem 1; proof provided in Appendix §B.6). As we have explained earlier, our strategy is to relate the one-step gain of ECED ![]() with the gain of OPT in -steps

with the gain of OPT in -steps ![]() (Appendix §B.5, Lemma 8). To achieve that, we divide our proof into three parts:

(Appendix §B.5, Lemma 8). To achieve that, we divide our proof into three parts:

- 1.

-

2.

To analyze the one-step gain of ECED, we introduce another intermediate auxiliary function: For a test chosen by ECED, we relate its one-step gain in the auxiliary function

![[Uncaptioned image]](/html/1605.07334/assets/x17.png) , to its one-step gain in the objective

, to its one-step gain in the objective ![[Uncaptioned image]](/html/1605.07334/assets/x18.png) (

(![[Uncaptioned image]](/html/1605.07334/assets/x19.png) Lemma 3, detailed proof provided in Appendix §B.3). The reason why we introduce this step is that the objective is adaptive submodular

Lemma 3, detailed proof provided in Appendix §B.3). The reason why we introduce this step is that the objective is adaptive submodular ![[Uncaptioned image]](/html/1605.07334/assets/x20.png) , by which we can relate the 1-step gain of a greedy policy

, by which we can relate the 1-step gain of a greedy policy ![[Uncaptioned image]](/html/1605.07334/assets/x21.png) to an optimal policy

to an optimal policy ![[Uncaptioned image]](/html/1605.07334/assets/x22.png) .

. -

3.

To close the loop, it remains to connect the gain of an optimal policy OPT in the objective function

![[Uncaptioned image]](/html/1605.07334/assets/x23.png) , with the gain of OPT in the auxiliary function

, with the gain of OPT in the auxiliary function ![[Uncaptioned image]](/html/1605.07334/assets/x24.png) . We show how to achieve this connection (

. We show how to achieve this connection (![[Uncaptioned image]](/html/1605.07334/assets/x25.png) ) in Appendix §B.4, by relating

) in Appendix §B.4, by relating ![[Uncaptioned image]](/html/1605.07334/assets/x26.png) to the expected reduction in prediction error, and further in §B.5, by applying the upper bound

to the expected reduction in prediction error, and further in §B.5, by applying the upper bound ![[Uncaptioned image]](/html/1605.07334/assets/x27.png) provided in §B.2.

provided in §B.2.

To make the proof more accessible, we insert the annotated color blocks from Fig. 5 (i.e., ![]() ,

, ![]() ,

, ![]() ,

, ![]() ,

, ![]() ,

, ![]() , etc), into the subsequent subsections in Appendix §B, so that readers can easily relate different parts of this section to the proof outline. Note that we only use these annotated color blocks for positioning the proofs, and hence readers can ignore the notations, as it may slightly differ from the ones used in the proof.

, etc), into the subsequent subsections in Appendix §B, so that readers can easily relate different parts of this section to the proof outline. Note that we only use these annotated color blocks for positioning the proofs, and hence readers can ignore the notations, as it may slightly differ from the ones used in the proof.

B.2 Proof of Lemma 2: Relating to

Define as the prediction error of a stochastic estimator upon observing , i.e., the probability of mispredicting if we make a random draw from . We show in Lemma 4 that is within a constant factor of :

Lemma 4.

Fix , it holds that

Proof of Lemma 4.

We can always lower bound by , since by definition, .

To prove the second part, we write for all . W.l.o.g., we assume . Then . We further have

∎

Now, we provide lower and upper bounds of the second term in the RHS of Equation (B.1):

Lemma 5.

.

Proof of Lemma 5.

We first prove the inequality on the left. Expanding the middle term involving the binary entropy of , we get

Here, step (a) is by inequality for .

To prove the second part, we first show in the following that .

W.l.o.g., we assume that the probabilities ’s are in decreasing order, i.e., . Observe that if , then . Consider the following two cases:

-

1.

. In this case, we have .

-

2.

. Since , we have

Therefore,

| (B.2) |

Furthermore, by Fano’s inequality (in the absence of conditioning), we know that . Combining with Equation (B.2) we get

where in (b) we use the fact that , since is a function of . Hence it completes the proof. ∎

Next, we bound the first term on the RHS of Equation (B.1), i.e., , against :

Lemma 6.

.

Proof of Lemma 6.

We can expand the LHS as

| LHS | ||||

| (B.3) | ||||

Since , we have

| LHS | |||

which completes the proof. ∎

Now, we are ready to state the upper bound ![]() and lower bound

and lower bound ![]() of .

of .

B.3 Proof of Lemma 3: Bounding against ,

In this section, we analyze the 1-step gain in the auxiliary function ![]() , of any test . By the end of this section, we will show that it is lowered bounded by the one-step gain in the objective

, of any test . By the end of this section, we will show that it is lowered bounded by the one-step gain in the objective ![]() .

.

Recall that we assume test outcomes are binary for our analysis, and in the following of this section, we assume the outcome of test is in instead of , for clarity purposes.

B.3.1 Notations and the Intermediate Goal

| , i.e., probability distribution on and , before performing test | |

|---|---|

| , | , |

| , | , i.e., probability distribution on and having observed |

| , | , i.e., probability distribution on and having observed |

| , | set of positive / negative root-causes |

| , | set of positive / negative root-causes associated with target |

| , | total probability mass of positive / negative root-causes |

| , | probability mass of positive / negative root-causes associated with target |

| , | , (defined in §B.3.5) |

| , i.e., root-causes and do not share the same target value |

For brevity, we first define a few short-hand notations to simplify our derivation. Let be two distributions on , and be the convex combination of the two, where and .

In fact, we are using and to refer to the posterior distribution over after we observe the (noisy) outcome of some binary test , and use to refer to the distribution over before we perform the test, i.e., , , and , where and . For , we use to denote the probability of under distribution , and use to denote the probability of under distribution .

Further, given a test , we define , to be the set of root-causes associated with target , whose favorable outcome of test is (for ) and (for ). Formally,

We then define , and , to be the set of “positive” and “negative” root-causes for test , respectively.

Let be the probability mass of the root-causes in and , i.e., , and We further define , and , then clearly we have . See Fig. 6 for illustration.

Now, we assume that test has error rate . That is, . Then, by definition of , , , , , , it is easy to verify that

| (B.4) |

For the convenience of readers, we summarize the notations provided above in Table 2.

Given root-causes and , we use to denote that the values of the target variable associated with root-causes and are different, i.e., .

We can rewrite the auxiliary function (as defined in Equation (4.1)) as follows:

If by performing test we observe , we have

otherwise, if we observe ,

Therefore, the expected gain (i.e., ![]() ) of performing test is,

) of performing test is,

| (B.5) |

In the following, we derive lower bounds for the above two terms respectively.

B.3.2 A Lower Bound on Term 1

Let . Then, we can rewrite Term as,

| Term | ||||

| (B.6) |

Part 1.

We first provide a lower bound for part 1 of Equation (B.6).

Notice that for concave function and , it holds that , then we get

Further, observe

Combining the above two equations gives us

| Part 1 |

For any root-cause pair with , and binary test , there are only 4 possible combinations in terms of the root-causes’ favorable outcomes. Namely,

-

1.

Both and maps to , i.e., .

We define such set of root-cause pairs with positive favorable outcomes as (For other cases, we define , , in a similar way).

In this case, we have

-

2.

Both and maps to . Similarly, we get

-

3.

maps to , maps to . We have

-

4.

maps to , maps to . By symmetry we have

Combining the above four equations, we obtain a lower bound on Part 1:

| Part 1 | ||||

| (B.7) |

Part 2.

Next, we will provide a lower bound on Part 2 of Equation (B.6).

By definition, we have

| Part 2 | |||

Hereby, step (a) is due to the strong concavity333If is strongly concave, then for , it holds that , where of .

Similarly with the analysis of Part 1, we consider the four sets of pairs:

-

1.

: both and maps to .

In this case, we have

-

2.

. Similarly, we get

-

3.

: maps to , maps to . We have

-

4.

: maps to , maps to . By symmetry we have

Combining the above four equations, we obtain a lower bound on Part 2:

| Part 2 | ||||

| (B.8) |

B.3.3 A Lower Bound on Term 2

B.3.4 A Combined Lower Bound for

We can rewrite Equation (B.10) as

| (B.11) |

B.3.5 Connecting with

Next, we will show that term LB1 is lower-bounded by a factor of (i.e., ![]() ), while LB2 cannot be too much less than 0. Concretely, we will show

), while LB2 cannot be too much less than 0. Concretely, we will show

-

•

, and

-

•

, for .

At the end of this subsection, we will combine the above results to connect ![]() with

with ![]() (See Equation (B.18)).

(See Equation (B.18)).

LB1 VS. .

We expand the gain ![]() as

as

| (B.12) |

Define

To bound LB1 against , it suffices to show .

To prove the above inequality, we consider the following two cases:

-

1.

. In this case, we have . Then,

-

2.

. W.l.o.g., we assume . By we get .

Observe the fact that

Rearranging the terms in the above inequality, we get

(B.13) Hence,

Therefore, we get

(B.14)

A lower bound on LB2.

In the following, we will analyze LB2.

| LB2 | |||

For brevity, define , and . We can simplify the above equation as

| LB2 | ||||

| (B.15) |

Denote the summand on the RHS of the above equation as . If for any we can lower bound , we can then bound the whole sum. Fix . W.l.o.g., we assume . Then

In order to put a lower bound on the above terms, we first need to lower bound the term involving . Notice that , and . Therefore, .

We check three different cases:

-

•

, or .

In this case, . Therefore,

Here, step (a) is due to the fact that is monotone increasing for . When , we have and (otherwise, there is no uncertainty left in ) and hence the problem becomes trivial.

-

•

.

In this case, we cannot replace with or . However, notice that , we have

(B.16) To further simplify notation, we denote , and . Then the above equation can be rewritten as

If , then

Otherwise, if , we have

-

•

. In this case, we have

Step (a) is due to the fact that and therefore .

Putting the above cases together, we obtain the following equations:

Fix . Let , we have , and , so

and thus we get

That is, if , we have for all .

On the other hand, if , we get , and therefore .

B.3.6 Bounding against

To finish the proof for Lemma 3, it remains to bound against . In this subsection, we complete the proof of Lemma 3, by showing that .

Recall that is the noise rate of test . Let be the discount factor for inconsistent root-causes. By the definition of in Equation (3.1), we first expand the expected offset value of performing test :

B.4 Bounding the error probability: Noiseless vs. Noisy setting

Now that we have seen how ECED interacts with our auxiliary function in terms of the one-step gain, it remains to understand how one can relate the one-step gain to the gain of an optimal policy ![]() , over steps. In this subsection, we make an important step towards this goal.

, over steps. In this subsection, we make an important step towards this goal.

Specifically, we provide

Lemma 7.

Consider a policy of length , and assume that we are using a stochastic estimator (SE). Let be the error probability of SE before running policy , be the average error probability of SE after running in the noisy setting, and be the average error probability of SE after running in the noiseless setting. Then

Proof of Lemma 7.

Recall that a stochastic estimator predicts the value of a random variable, by randomly drawing from its distribution. Let be a policy. We denote by the expected error probability of an stochastic estimator after observing :

where denotes a set of test-outcome pairs, and denotes a path taken by , given that it observes .

Now, let us see what happens in the noiseless setting: we run exactly as it is, but in the end compute the error probability of the noiseless setting (i.e., as if we know which test outcomes are corrupted by noise). Denote the noise put on the tests by , and the realized noise by . We can imagine the noiseless setting through the following equivalent way: we ran the same policy exactly as in the noisy setting. But upon completion of we reveal what was. We thus have

The error probability upon observing and is

The expected error probability in the noiseless setting after running is

| (B.20) |

Now, we can relate to .

where (a) is by Jensen’s inequality and the fact that is concave. Combining with Equation (B.20) we complete the proof. ∎

Essentially, Lemma 7 implies that, in terms of the reduction in the expected prediction error of SE, running a policy in the noise-free setting has higher gain than running the exact same policy in the noisy setting. This result is important to us, since analyzing a policy in the noise-free setting is often easier. We are going to use Lemma 7 in the next section, to relate the gain of an optimal policy ![]() in the objective (which assumes tests to be noise-free), with the gain

in the objective (which assumes tests to be noise-free), with the gain ![]() in the auxiliary function (which considers noisy test outcomes).

in the auxiliary function (which considers noisy test outcomes).

B.5 The Key Lemma: One-step Gain of ECED VS. -step Gain of

Now we are ready to state our key lemma, which connects ![]() to

to ![]() .

.

Lemma 8 (Key Lemma).

Fix . Let be the number of root-causes, be the number of target values, be the optimal policy that achieves , and be the partial realization observed by running ECED with cost . We denote by the expected value of over all the paths at cost . Assume that . We then have

where , , , , and .

Proof of Lemma 8..

Let be a path ending up at level of the greedy algorithm. Recall that denotes the gain in if we perform test and assuming it to be noiseless (i.e., we perform edge cutting as if the outcome of test is noiseless), conditioning on partial observation . Further, recall that denotes the gain in if we perform noisy test after observing and perform Bayesian update on the root-causes.

Let be the test chosen by ECED, and be the test that maximizes , then by Lemma 3 we know

| (B.21) |

Note that is the EC2 gain of test over the normalized edge weights at step in the noiseless setting. That is, upon observing , we create a new EC2 problem instance (by considering the posterior probability over root-causes at ), and run (noiseless) greedy algorithm w.r.t. the EC2 objective on such problem instance. Recall that . By adaptive submodularity ![]() of (in the noiseless setting, see Golovin et al. (2010)), we obtain

of (in the noiseless setting, see Golovin et al. (2010)), we obtain

where by we mean the initial EC2 objective value given partial realization , and by we mean the expected gain in when we run . Note that has worst-case length .

Now, imagine that we run the policy , and upon completion of the policy we can observe the noise. We consider the gain of such policy in :

The reason for step (a) is that the error probability of the stochastic estimator upon observing , i.e., , is equivalent to the total amount of edge weight at , i.e., . The reason for step (b) is that under the noiseless setting (i.e., assuming we have access to the noise), the EC2 objective is always a lower-bound on the error probability of the stochastic estimator (due to normalization). Thus, .

Hence we get

Here denotes the error probability under , and denotes the expected error probability of running after in the noise-free setting. By Lemma 7 we get

where denotes the expected error probability of running after in the noisy setting. By (the lower bound in) Lemma 4, we know that , and hence

Taking expectation with respect to , we get

| (B.22) |

Using (the upper bound in) Lemma 2, we obtain

| (B.23) |

where (a) is by Jensen’s inequality.

B.6 Proof of Theorem 1: Near-optimality of ECED

We are going to put together the pieces from previous subsection, to give a proof of our main theoretical result (Theorem 1).

Proof of Theorem 1.

In the following, we use both and to represent the optimal policy that achieves prediction error , with worst-cast cost (i.e., length) . Define to be the (partial) realization seen by policy under realization . With slight abuse of notation, we use to denote the expected value achieved by running .

After running , we know by Lemma 2 that the expected value of is lower bounded by . That is, , where the last inequality is due to . We then have

| (B.26) |

Let , so that Inequality (B.26) implies . From here we get , and hence

where step (a) is due to the fact that for any , and step (b) is due to . It follows that

This gives us

| (B.27) |

Denote the three terms on the RHS. of Equation (B.27) as UB1, UB2 and UB3, respectively. We get

Now we set

| (B.28) |

and obtain . It is easy to verify that , and .

We further set

| (B.29) |

and obtain .

Combining the upper bound derived above for UB1, UB2, UB3, and by Equation (B.27), we get . By Lemma 2 we know that the error probability is upper bounded by . That is, with the cost specified in Equation (B.28), ECED is guaranteed to achieve .

It remains to compute the (exact) value of . Combining the definition of and with Equation (B.29) it is easy to verify that

holds for some constant . Therefore by Equation (B.28),

To put it in words, it suffices to run ECED for steps to have expected error below , where denotes the worst-case cost the optimal policy that achieves expected error probability ; hence the completion of the proof. ∎

Appendix C Examples When GBS and the Most Informative Policy Fail

In this section, we provide problem instances where GBS and/or the Most Informative Policy may fail, while ECED performs well. Since in the noise-free setting ECED is equivalent to , it suffices to demonstrate the limitations of GBS and the most informative policy, even if we provide just examples that apply to the noise-free setting.

C.1 A Bad Example for GBS: Imbalanced Equivalence Classes

We use the same example as provided in Golovin et al. (2010). Consider an instance with a uniform prior over root-causes, , and two target values , and . There are tests such that (all of unit cost). Here, is the indicator function. See Fig. 7 for illustration.

Now, suppose we want to solve Problem (2.1) for . Note that in the noise-free setting, the problem is equivalent to find a minimal cost policy that achieves 0 prediction error, because once the error probability drops below we will know precisely which target value is realized.

In this case, the optimal policy only needs to select test , however GBS may select tests in order until running test , where is the true root-cause. Given our uniform prior, it takes tests in expectation until this happens, so that GBS pays, in expectation, times the optimal expected cost in this instance. Note that in this example, ECED (equivalently, ) also selects test , which is optimal.

C.2 A Bad Example for the Most Informative Policy: Treasure Hunt

In this section, we provide a treasure-hunt example, in which the most informative policy pays times the optimal cost. This example is adapted from Golovin et al. (2010), where they show that the most informative policy (referred to as the Informative Gain policy), as well as the myopic policy that greedily maximizes the reduction in the expected prediction error (referred as the Value of Information policy), both perform badly, compared with .

Consider the problem instance in Fig. 8(a). Fix to be some integer, and let . For each target value , there exists two root-causes, i.e., , , such that . Denote a root-causes as , if it belongs to target and is indexed by . We assume a uniform prior over the root-causes: .

Suppose we want to solve Problem (2.1) for . Similarly with §C.1, the problem is equivalent to find a minimal cost policy that achieves 0 prediction error, because once the error probability drops below , we will know precisely which target value is realized.

There are three set of tests, and all of them have binary outcomes and unit cost. The first set contains one test , which tells us the value of of the underlying root-cause . Hence for all , (see Fig. 8(b)). The second set of tests are designed to help us quickly discover the index of the target value via binary search if we have already run , but to offer no information whatsoever (in terms of expected reduction in the prediction error, or expected reduction in entropy of ) if has not yet been run. There are a total number of tests in the second set . For , let be the least-significant bit of the binary encoding of , so that . Then, if , then the outcome of test is (see Fig. 8(c)). The third set of tests are designed to allow us to do a (comparatively slow) sequential search on the index of the the target values. Specifically, we have , such that (Fig. 8(d)).

Now consider running the maximal informative policy (the same analysis also applies to the value of information policy, which we omits from the paper). Note that in the beginning, no single test from results in any change in the distribution over , as it remains uniform no matter with test is performed. Hence, the maximal informative policy only picks tests from , which have non-zero (positive) expected reduction in the posterior entropy of . In the likely event that the test chosen is not the index of , we are left with a residual problem in which tests in still have no effect on the posterior. The only difference is that there is one less class, but the prior remains uniform. Hence our previous argument still applies, and will repeatedly select tests in , until a test has an outcome of 1. In expectation, the cost of is least .

On the other hand, a smarter policy will select test first, and then performs a binary search by running test to determine for all (and hence to determine the index of ). Since the tests have unit cost, the cost of is .

Since , and , we conclude that

Appendix D Case Study: Pool-based Active Learning for Classification

Experimental setup.

To demonstrate the empirical performance of ECED, we further conduct experiments on two pool-based binary active classification tasks. In the active learning application, we can sequentially query from a pool of data points, and the goal is to learn a binary classifier, which achieves some small prediction error on the unseen data points from the pool, with the smallest number of queries as possible.

Active Learning: Targets and Root-causes

To discretize the hypotheses space, we use a noisy version of hit-and-run sampler as suggested in Chen & Krause (2013). Each hypothesis can be represented by a binary vector indicating the outcomes of all data points in the training set. Then, we construct an epsilon-net on the set of hypotheses (based on the Hamming distance between hypotheses). We obtain the equivalence classes for ECED, by assigning each hypothesis to its closest center of epsilon-ball, measured by their Hamming distances. Note that the Hamming distance between two hypotheses reflects the difference of prediction error. Consider epsilon-net of fixed radius . By construction, hypotheses that lie in the some equivalence classes are at most away from each other; therefore the hypotheses which are within the epsilon-ball of the optimal hypotheses are considered to be near-optimal. Using the terminology in this paper, hypotheses correspond to root-causes, and the groups of hypothesis correspond to the target variable of interest. Running ECED, ideally, will help us locate a near-optimal epsilon-ball as quickly as possible.

Baselines.

We compare ECED with the popular uncertainty sampling heuristic (UNC-SVM), which sequentially queries the data points which are the closest to the decision boundary of a SVM classifier. We also compare with the GBS algorithm, which sequentially queries the data points that maximally reduces the volume of the version space.

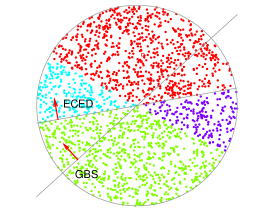

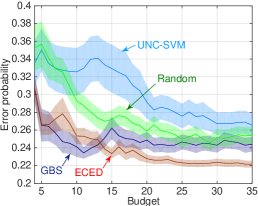

In Fig. 9(a), we demonstrate the different behaviors between GBS and on a 2-d plane. In this simple example, there are 4 color-coded equivalence classes: we first sample hypotheses uniformly within the unit circle, and then generate equivalence classes, by constructing an epsilon-net over the sampled hypotheses as previously described. Fig. 9(a) illustrates two tests (i.e., the gray lines intersecting the circles) selected by ECED and GBS, respectively. ECED primarily selects tests that best disambiguate the clusters, while GBS focuses on disambiguate individual hypotheses.

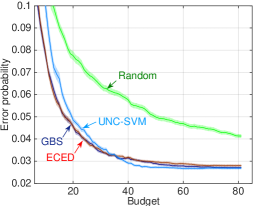

Results.

We evaluate ECED and the baseline algorithms on the UCI WDBC dataset (569 instances, 32-d) and Fourclass dataset (862 instances, 2-d). For ECED and GBS, we sample a fixed number of 1000 hypotheses in each random trial. For both instances we assume a constant error rate for all tests. Fig. 9(b) and Fig. 9(c) demonstrate that ECED is competitive with the baselines. Such results suggests that grouping of hypotheses could be beneficial when learning under noisy data.