Revenue Maximization in Service Systems with Heterogeneous Customers

Abstract

In this paper, we consider revenue maximization problem for a two server system in the presence of heterogeneous customers. We assume that the customers differ in their cost for unit delay and this is modeled as a continuous random variable with a distribution We also assume that each server charges an admission price to each customer that decide to join its queue. We first consider the monopoly problem where both the servers belong to a single operator. The heterogeneity of the customer makes the analysis of the problem difficult. The difficulty lies in the inability to characterize the equilibrium queue arrival rates as a function of the admission prices. We provide an equivalent formulation with the queue arrival rates as the optimization variable simplifying the analysis for revenue rate maximization for the monopoly. We then consider the duopoly problem where each server competes with the other server to maximize its revenue rate. For the duopoly problem, the interest is to obtain the set of admission prices satisfying the Nash equilibrium conditions. While the problem is in general difficult to analyze, we consider the special case when the two servers are identical. For such a duopoly system, we obtain the necessary condition for existence of symmetric Nash equilibrium of the admission prices. The knowledge of the distribution characterizing the heterogeneity of the customers is necessary to solve the monopoly and the duopoly problem. However, for most practical scenarios, the functional form of may not be known to the system operator and in such cases, the revenue maximizing prices cannot be determined. In the last part of the paper, we provide a simple method to estimate the distribution by suitably varying the admission prices. We illustrate the method with some numerical examples.

I Introduction

In many service systems, the quality of service received is characterized by the queueing delay that is experienced by the customers in the system. Examples of such service systems that can be modeled as queueing systems include road and transport systems, health-care systems, computer systems, call centers and communications systems. The customers that receive service in such systems are usually sensitive to the delay experienced in these system. Further, such customers have non-identical preferences to the delay experienced. It is often beneficial for the service system to account for these heterogeneous preferences in any optimization concerning the use of system resources. Many service systems have emerged that exploit the heterogeneous nature of customers and use it to their advantage. For example, airlines offer priority boarding queues for payment of an additional fee. In this paper, we consider the problem of exploiting the heterogeneous nature of customers for revenue maximization in parallel server systems. We model heterogeneity of customers by assuming that different customers have different cost for a unit delay.

We consider service systems that consist of two parallel, possibly heterogeneous servers where each server has an associated queue for the customers to wait. The scheduling discipline at each server is work conserving and does not discriminate between customers on the basis of their preference for delay. The servers charge an admission price to every customer joining its queue. We assume that the queues are not observable and only the expected delay as a function of the arrival rate is available. We also assume that the expected delay at any server is monotone increasing in the arrival rate of customers to that server. The customers that use the system are strategic and make an individually optimal queue-join decision. We assume that customers differ in their cost for unit delay which is characterized by a random variable with a continuous distribution denoted by For a customer, the cost at a server is the sum of the admission price and the delay cost at the server. We assume that customers cannot balk from the system without obtaining service and such traffic is commonly seen in cloud-computing, purchase of essential services etc.

In this paper, we consider the problem of revenue maximization in such a service system by suitably choosing the admission prices at two parallel servers. Depending on the objective of each of these servers, we consider two natural scenarios. In a monopoly, we assume that the two servers belong to the same operator. The objective here is to maximize the total revenue rate, i.e., the sum of the revenue rate from the two servers. In the second scenario, we assume that each server belongs to separate operators and each server has the objective of maximizing its individual revenue rate. This is an example of a duopoly where the service systems compete with one another to maximize their individual revenue rate.

Now consider the scenario of a monopoly market discussed above where the service system has two parallel servers. In the absence of balking, it is not difficult to see that a revenue maximizing strategy for the monopoly is to keep both the admission prices at infinity. This is because as customers cannot balk, they are required to choose one of the server for service. Therefore one has to consider a more meaningful model for the monopoly market. Towards this, we assume that the admission price at one of the server, say Server 2 is fixed a-priori. This dissuades the service provider from fixing the admission price at Server 1 to unreasonably high values. Our interest for this model is to characterize the revenue maximizing admission price at Server 1 for different examples of the delay functions at the queue and when customers differ in their delay cost.

Classical monopoly models have been well studied for the case of single server queues. One of the first work to analyze such a model is Naor [1]. This model considers a single server queueing system where homogeneous customers obtain a reward after service completion. The queue is observable to arriving customers who choose to either join the queue or balk. For such a system, the revenue maximizing admission price was first obtained in [1]. Subsequently, there have been several works analyzing the revenue maximization problem for various models such as a multiserver queue [2], queue [3], customers with heterogeneous service valuations [4] and queue length dependent prices [5]. While the above models assume that the queue lengths are observable, Edelson and Hilderbrand [6] were the first to consider the revenue maximization problem for the case when queues are not observable. See [7, 8, 9, 10, 11] for some other single server revenue maximization models.

The key difference of our model with that of the literature discussed above is as follows. Firstly, in our model, customers are inelastic in their demand and hence balking is not allowed. Secondly, the customers have to obtain service at either of the two servers and the admission price at one of the server is fixed. Finally, the customers have heterogeneous preference for the delay experienced in the queue. This feature makes our model meaningful but also difficult to analyze. For such parallel server models, the structural properties for the equilibrium routing have been obtained recently [12, 13]. We use the structural property of the equilibrium routing to solve the the revenue maximization problem for the monopoly.

For the duopoly problem with two competing and identical servers, we assume that the objective for each server is to set an admission price that maximizes its revenue rate. We are interested in studying the existence of Nash Equilibrium prices that would be set by the two servers. The earliest work analyzing the duopoly model with heterogeneous customers was by Luski [14] and Levhari and Luski [15]. Both the models assume that the customers are allowed to balk. Luski [14] is interested in knowing whether the revenue maximizing prices set by the two service systems can be equal. It is observed that when the parameters of the model are such that the customers have no incentive to balk, the revenue maximizing prices set by two identical servers is equal. This is however not the case when some of the customers prefer to balk. In this case, the equilibrium revenue maximizing prices are not equal. Levhari and Luski [15] provide a numerical analysis for the problem introduced in Luski [14]. Armony and Haviv [16] analyze this problem for the case when the customers are from a finite number of classes and each class has a distinct cost for unit delay. A numerical analysis of the Nash equilibrium admission prices between the two competing servers is provided. Chen and Wan [17] consider the revenue maximization in a duopoly with a single customer class. The service system is modeled by queues and the customers are allowed to balk from the system. These assumptions on the system model allows them to obtain the sufficient conditions for the existence of Nash equilibrium. Similar conditions were found in Dube and Jain [18] who consider an -player oligopoly with multiclass customers. The customer classes differ only in their arrival rates and have the same delay cost per unit time. A differentiated service model is considered by Dube and Jain [19] where each player now operates two types of services and each service is used by a dedicated class of customers. Again, the key result in [19] is to obtain the sufficient condition for the Nash equilibrium prices. Mandjes and Timmers [20] consider a duopoly model with two customer classes differing in their delay cost. The model assumes a finite number of customers and the utility of a queue is a decreasing function of the number of customers using this server. Given the prices at the servers, they provide an algorithm that determines the equilibrium number of customers of each class that is to be allocated to the two servers. While the existence and uniqueness of such a customer equilibrium is provided, the existence of Nash equilibrium prices is only conjectured. In [21, 22] the demand rate at different servers is modeled using specific functions (known as demand models in such literature) instead of being calculated from the (Wardrop) equilibrium conditions [23]. This assumptions make the analysis relatively simpler. Ayesta et. al. [24] consider the oligopoly pricing game for a single customer class and obtain the necessary and sufficient conditions on the Nash equilibrium prices when the queues have identical delay functions. A best-response algorithm is then provided to numerically obtain these Nash equilibrium prices.

Most of the monopoly and duopoly models described above, make simplifying assumptions on the customer classes to characterize the underlying Wardrop equilibrium [23]. Additional simplification of the analysis is obtained by considering convex and increasing delay functions at the queues. We do not make any of these assumptions in this paper. We utilize the structure of the Wardrop equilibrium that was characterized in [12, 13] to analyze the two problems. This structure on the equilibrium allows us to provide an equivalent revenue maximization formulation for both the monopoly and the duopoly that is simpler to analyze. For the duopoly problem we provide sufficient conditions on the symmetric Nash equilibrium prices when the competing servers are identical.

For most practical scenarios, the distribution function characterizing the delay cost for a customer may not be known to the service system. The revenue maximizing strategy on the other hand depend on the distribution Without any knowledge of it is not be possible to ascertain a revenue optimal admission price at the servers and in such cases, the service system is required estimate this distribution function. Towards the end of this paper, we shall provide a simple method to estimate this distribution by varying the admission prices and observing the change in the equilibrium traffic routing. The service system can then use this estimate to perform the necessary revenue maximization.

The rest of the paper is organized as follows. In the next section, we shall formalize the notations and provide some preliminaries. We then formulate the revenue maximization problems in Section III. In Section IV, we consider the monopoly problem for revenue optimization followed by the duopoly problem in Section V. Finally in Section VI, we illustrate a mechanism based on admission pricing to estimate the distribution function

II Preliminaries

We will first introduce the notations that will be used throughout this paper. In both the monopoly and the duopoly model, we assume that the system has two servers. Let denote the admission price at Server where The customers arrive according to a homogeneous Poisson process with rate and have a service requirement that is i.i.d with exponential distribution and unit mean. Let denote the delay function associated with queue when the queue arrival rate is where Note that We assume that is monotone increasing and continuously differentiable in the interior of its domain with a strictly positive derivative. Additionally we assume that the cost function at the two server satisfies the following two conditions (1) and (2)

We associate with each arriving customer a continuous random variable that quantifies a customer’s sensitivity to delay or congestion. We shall assume that the delay sensitivity for a customer is a realization of the random variable The customer arrivals constitute a marked Poisson process of intensity on Here is an absolutely continuous cumulative distribution function supported on the interval of positive reals. We additionally assume that is strictly increasing and hence for any where is the corresponding density function.

We now recall the Wardrop equilibrium conditions [23, 13] that characterize the individually optimal choice of server made by the arriving customers. A customer with delay cost entering the system must choose a queue so as to minimize Here is determined through the strategies of all customers. We assume that the quantities and for is part of common knowledge. We also assume that the customers do not have access to current or past queue occupancies, or the history of arrival times. The strategy of a customer is restricted to choosing a server according to a fixed probability distribution and such joint strategies are represented by a stochastic kernel, denoted by We interpret as the probability that a customer with delay sensitivity chooses queue at equilibrium. For the two server system, the equilibrium kernel must satisfy the following Wardrop equilibrium conditions.

| (1) |

In words, this means that if customers with delay cost choose Server at equilibrium, then the expected cost for this customer at Server must be at most the expected cost at Server for For a kernel note that the arrival rate of customers to Server is given by

We now provide the following theorem that is a restatement of Corollary 4 in [13]. This theorem characterizes the Wardrop equilibrium kernel for a system with two parallel servers.

Theorem 1

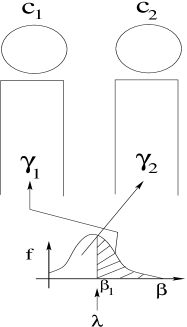

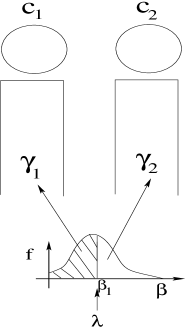

Define as the probability distribution that puts unit mass on and suppose that the kernel satisfies the Wardrop equilibrium condition. Then there exists a threshold with such that

-

•

when

(2) Further if then,

(3) -

•

When is not unique and any kernel with is a valid Wardrop equilibrium kernel where

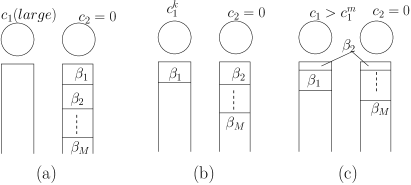

Refer Figures 2 and 2 for a representation of the Wardrop equilibrium kernel for the case when and respectively. Here denotes the underlying density function of the random variable while the shaded region identifies the delay cost parameter of those customers that choose Server 1.

Proof:

The first part is simply a restatement of Corollary 4 in [13] for the case and the proof for is along similar lines. We now prove the second part. Consider the case when and recall the assumption that and must be such that To see why this must be true, suppose that this is not true and let Customers from the queue with a higher delay cost will have an incentive to move to the queue with a lower delay cost. This implies that a with is not at equilibrium. Recall the definition Since, and we have Now for any kernel satisfying since the cost for any customer at the two servers is equal. Hence there is no incentive for any customer to deviate from its choice of the server. The Wardrop equilibrium kernel though not unique must however satisfy . ∎

III Problem Formulations

Having characterized the Wardrop equilibrium kernel for a two server system, we will now formulate the revenue maximization problems for both the monopoly and the duopoly model. Let denote the revenue rate at server when the arrival rate of customers due to the corresponding kernel is for For the monopoly model, let denote the revenue rate for the monopoly service system. Since it suffices to express the revenue rate as a function of only We have

Note from Theorem 1, that the argument is determined by the kernel which in turn depends on the admission prices and This dependence will be made explicit by writing as and the revenue optimization problem for the monopoly can now be stated as follows.

| (P1) | ||||||

| subject to |

where is an arbitrarily large value such that is a technical requirement to ensure a compact domain and one could also define in which case we have for any To be able to solve program P1 using standard optimization techniques, a closed form expression for would be convenient. When and from Theorem 1 and the definition of , it can be seen that

| (4) |

where

A similar condition follows when and it can be seen that obtaining an explicit expression for is difficult. Note that we have not assumed any functional form for and and for certain choice of these functions, a closed form expression for may not be possible. Without an analytic expression for it is difficult to solve the revenue maximization problem. Therefore we require an alternative approach to solve program One possible alternative is to let the equilibrium (the value of at equilibrium) be the optimization variable and represent other variables of the system such as as a function of With slight abuse of notation, we will use to denote the admission price at Server when the arrival rate to Server at equilibrium is where Similarly, we shall use to represent the threshold corresponding to an equilibrium arrival rate of to Server Note that is also a function of This is because the equilibrium depends on the difference and not on their individual values. This is clear from Theorem 1 (Eq. (3)). Therefore for a given and one can determine using Eq. (3). We have suppressed this dependence on to simplify notation. For the monopoly model as is assumed fixed. Thus the equivalent revenue optimization problem for the monopoly is as follows.

| (P2) | ||||||

| subject to |

where determines the domain for the feasible values of as a function of An intuitive explanation for the quantity is as follows. Consider the case From Theorem 1, we have where Using the notation we have For any since the increase in the admission price at Server 1 makes the server more costly and decreases the resulting Clearly, for any and and in program P2 cannot be defined for Therefore when the domain for the optimization variable should be restricted to In general, for an arbitrary the domain for in program P2 is defined using and this will be characterized formally in Section IV.

Now consider the duopoly market with two competing servers charging admission prices and to their arriving customers. The objective of Server is to choose an admission price that maximizes its revenue rate For this duopoly, the revenue optimization problem for Server is as follows.

| (P3) | ||||||

| subject to | ||||||

| given |

where represents the admission price at the server other than i.e., and

For the duopoly market, the aim is to obtain the Nash equilibrium set of admission prices to be charged at the two servers. We shall denote the Nash equilibrium prices by the tuple Using the notion of the best response function [25], can be characterized as follows. Let denote the admission price at Server that maximizes the server revenue for a given value of for Clearly, is the maximizer in program P3 and it is easy to see that

and

However as argued earlier, the closed form expression for is not easy to obtain. This makes it difficult to solve program P3 and obtain the best responses for As a result, obtaining is in general not easy. As in the case of the monopoly program, to obtain we need to first reformulate program P3 by letting denote the optimizing variable. The corresponding optimization problem is as follows.

| (P4) | ||||||

| subject to | ||||||

| given |

can be interpreted as the admission price at Server that leads to the equilibrium arrival rate of when the other server charges Note again that will be a function of but we do not make this explicit in the notation. To lighten notation, we will not make this dependence explicit. Now let denote the maximizer in program P4 for a given value of . Then the best response is in fact given by the function Therefore, once the function is characterized, the best response now denoted by satisfies We now have

where and as stated earlier, is the maximizer in program P4 for It is therefore clear that can be obtained once we have characterized We shall analyze the program P4 in detail in Section V and explicitly characterize the functions for to be able to obtain .

IV Monopoly Market

In this section, we will analyze the monopoly program To be able to solve program we need to characterize for a fixed value of This procedure is outlined below. From Eq. (3) of Theorem 1, we know that when (and hence ) we have

We will express the right hand side of the above equation as a function of i.e.,

| (5) |

where represents the threshold for a kernel that satisfies Theorem 1 and corresponds to an equilibrium arrival rate of Note that characterizes the difference as a function of For a fixed and for a satisfying (the domain of in program P2) we see that We characterize in the following manner. We first characterize using Lemmas 1 and 2. Then in Lemma 3, we characterize For a fixed we then obtain in Lemma 5 that determines the domain of . To prove this lemma we need to characterize the uniqueness of kernel for a fixed difference This is part of Lemma 4. Finally we characterize in Theorem 2 using and

Recall that we make minimal assumptions on the distribution and on the delay cost function For our numerical examples and also to illustrate the properties of the functions and we consider the following examples for and The distribution is from one of the following;

-

•

Uniform distribution over the range

-

•

Exponential distribution with mean

-

•

Gamma distribution with shape and scale .

For the delay cost function, we shall assume one of the following.

-

•

This corresponds to the case of linear delay.

-

•

and This corresponds to type delay cost function.

The distribution and the delay cost functions outlined above are commonly used to model heterogeneous customers and congestion costs. (Refer [26, 12, 13, 14, 15])

We now begin with the following lemma that identifies the necessary and sufficient condition on the equilibrium when either or

Lemma 1

iff while iff

Proof:

See Appendix for proof. ∎

Next, we express the threshold of Theorem 1 as a function of . Recall from the theorem that is characterized by when We let to denote the value of the threshold (characterizing ) for a given such that We have the following lemma.

Lemma 2

| (6) |

where represents the quantile function or the inverse function of the distribution

Proof:

See Appendix for proof. ∎

Note that is not defined in Lemma 2 when This is because the Wardrop kernel with is not unique and need not be characterized by a single threshold. We shall however assume from now on that when (and hence ), the corresponding kernel is also characterized by a single threshold Hence for we have

| (7) |

As a result, we define and the modified is now as follows.

| (8) |

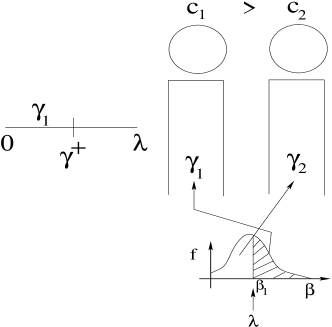

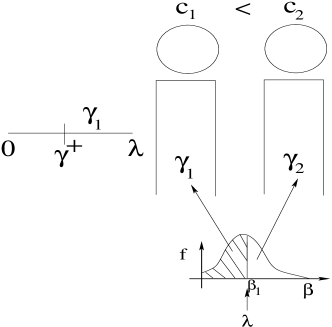

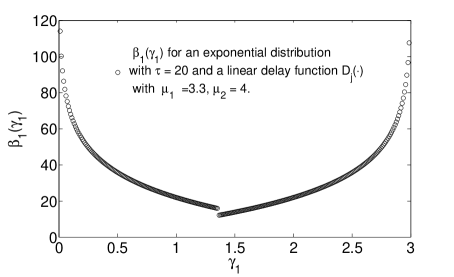

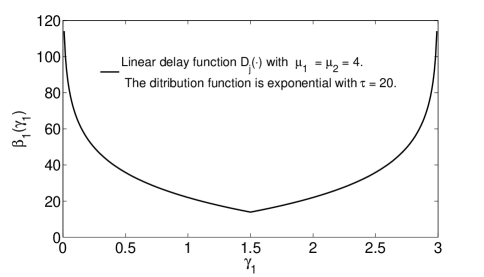

Refer Fig. 5 for a numerical evaluation of Eq. (8) for the case when is an exponential distribution with The delay functions are where and Fig. 6 corresponds to the case when the two servers are identical, i.e.,

Remark 1

Recall our assumption that is absolutely continuous and strictly increasing in its domain. Further, the support is and hence is a bijective function whose inverse exists. In fact is continuous and strictly increasing in its domain. Since is continuous in its arguments, is continuous when and However at is in general not continuous (Refer Fig. 5). For the case when the servers are identical, i.e., we see from the definition of that For this case, it is easy to see that is continuous at (but not differentiable). See Fig. 6.

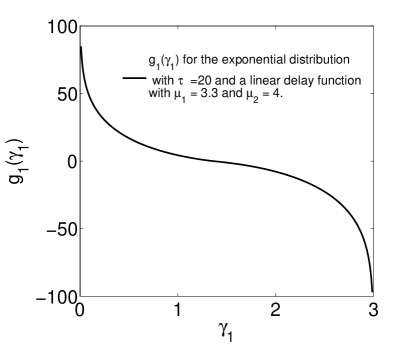

Having obtained we shall now analyze that was defined in Eq. (5). will be used later to obtain We have the following lemma.

Lemma 3

For is continuous and monotonic decreasing in Further,

Proof:

See Appendix for proof. ∎

See Fig. 7 for a numerical evaluation of when is an exponential distribution with and when the servers have a linear delay with and

To determine we also need to identify the domain over which it can be defined. As argued earlier, this domain is determined by which is characterized in Lemma 5. Before stating Lemma 5, we shall first characterize the uniqueness of and hence the kernel when While Theorem 1, guarantees existence of a characterizing kernel it does not guarantee the uniqueness of and hence the uniqueness of the kernel . This result will be used in the proof of Lemma 5.

Lemma 4

For a given the threshold characterizing the kernel in Theorem 1 is as follows.

| (9) |

where satisfies For a fixed the equilibrium and the corresponding is unique and this implies the uniqueness of

Proof:

See Appendix for proof. ∎

We now characterize in the following lemma.

Lemma 5

| (10) |

In words, when we have and for any the equilibrium However when we have in which case for suitable choices of

Proof:

See Appendix for proof. ∎

The above lemma also implies that, if then for any the equilibrium satisfies On the other hand, if the parameters of the system are such that then for any set of admission prices at Server 1, we have

Remark 2

Finally, we have the following theorem to express as a function of denoted by

Theorem 2

for For must be at least equal to i.e., Similarly when we have

Proof:

First consider a fixed satisfying for a fixed ( was characterized in Lemma 5.) The corresponding threshold is determined by Eq. (8) and hence we have for Recall that Lemma 4 relates the threshold with Since from Lemma 4, must satisfy Therefore for a fixed the admission price resulting in the arrival rate of at Server 1 is given by

In the above theorem, and are not uniquely defined and can take values that satisfy and respectively. As convention, we henceforth define and Further note that the domain for is and for is undefined. The function for can now be expressed as follows.

| (11) |

Now recall the revenue maximization problem Define as the optimizer for this program with the revenue maximizing admission price given by Since must be such that From Eq. (11), this implies that From Lemma 3 we have for and this implies that The term in is a constant and hence we have the following equivalent program for the revenue maximization problem.

| (P4) | ||||||

| subject to |

where is given by Eq. (5).

Note from Lemma 3 that is a continuous function of its domain. Program P4 involves maximizing a continuous function over a compact set and hence a maximizer exists. The original monopoly program P1 has been significantly simplified to the equivalent program P4. Since is strictly decreasing (and hence quasi-convex), is in fact a product of two quasi-convex functions. (However product of quasi-convex functions need not be quasi-convex function). One can now use standard non-linear optimization techniques to obtain To further understand Program P4, we perform a numerical evaluation of under a combination of assumptions on the distribution functions and the delay functions that were outlined earlier.

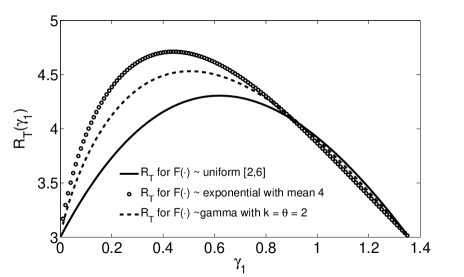

Example 1: In this example we shall assume that the for We assume that and Further, the arrival rate and we consider the following three examples for the distribution (1) has a uniform distribution with support on (2) has an exponential distribution with mean and (3) has a Gamma distribution with the scale and shape parameters and respectively. Note that with these three distributions have the same mean. We plot as a function of in Fig. 8 where we assume When has the uniform distribution, The optimal revenue rate while the admission price maximizing is 3.106. The corresponding values for the exponential distribution are and while the values for gamma distribution are and .

Example 2: In this example, we assume that where again and Note that for The choice of is as in the previous example. A plot of as a function of is provided in Fig. 9. When has the uniform distribution, The optimal revenue rate while the admission price maximizing is . The corresponding values for the exponential distribution are and while the values for gamma distribution are and .

We conclude the analysis of the revenue maximization problem with the following observations made from the two examples given above.

-

•

Firstly, we see that for the given examples of is a unimodal function in For the three distribution functions, it can be shown that is differentiable in its arguments. For such distribution functions with differentiable this implies that and hence is differentiable in when From Rolle’s Theorem (Theorem 10.2.7 [27]), this implies that there exists a such that A satisfying this equation is the revenue maximizing arrival rate to server 1. The admission price corresponding to this can now be obtained using Eq. (11).

-

•

For each of the three distributions, note that we have However, the Revenue rate as a function of is distinct in all the three cases. This implies that the revenue rate depends on the higher moments of the distribution and not just on its mean value.

-

•

Finally, note that depends on admission price through the addition factor of For different values of the corresponding does not change. However it is easy to see from Eq. (11) that increases linearly in

V Duopoly

In this section, we shall consider program P4 for revenue maximization in the duopoly system. Much of the analysis in this section follows from that of the previous section. Let denote the optimization variable and represent the admission prices at the respective servers as a function of the arrival rates. Towards this, we continue with the use of the notation for Note that while in the monopoly case, the admission price was considered fixed, in the duopoly of this section, it is the strategy for the second server and hence will not be a constant. The revenue function for Server is given by

where represents the admission price at Server resulting in an equilibrium arrival rate of As noted in the previous section, is a function of the admission price at the other server. For a fixed strategy at Server from Eq. (11) the revenue function can be redefined as

| (12) |

It can be argued as in the previous section that for a fixed

| (13) |

where

| (14) |

where from Eq. (8) is as follows

| (15) |

It is easy to see that is also continuous and strictly decreasing in Further, when The revenue maximization problem for the duopoly is re-stated as follows.

| (P7) | ||||||

| subject to | ||||||

| given |

For a given recall that denotes the maximizer of program P4 and hence of the above program. Also recall that denotes the best response admission price at Server in response to the admission price at the other facility. Then the Nash equilibrium set of admission prices, denoted by is characterized as follows.

| (16) |

where for

We begin the analysis for the duopoly problem by first identifying that lies in the interior of the domain. We have the following lemma.

Lemma 6

Proof:

See Appendix for proof. ∎

For a given since lies in the interior of the domain, satisfies and

Define . Then is obtained as a solution to the following.

| (P8) |

From the above discussion, it should be clear that obtaining the closed form expression for satisfying the simultaneous equations of (16) is, in general, not easy. Note that our analysis till now makes minimal assumptions on the distribution function or on the delay function For certain choices of these functions, it may be difficult to obtain a closed form expression for The objective function also need not be a concave function. In that case, a brute force search among all the local maxima points needs to be carried out to choose the right Instead of satisfying ourselves with some numerical examples, in the following subsection we shall analyze the Nash equilibrium under the restriction that the two servers are identical i.e., the average delay at any queue is the same for the same arrival rate. Under this setting, our interest is to characterize the symmetric Nash equilibrium such that

V-A Characterizing a symmetric Nash equilibrium

In this section we shall characterize the necessary conditions for the existence of a symmetric Nash equilibrium, i.e., where A natural scenario where such an equilibrium is possible is when the two servers have identical delay functions. In this section, we restrict to this case and assume that for As the service systems are identical in their delay characteristics, it is desirable to identify conditions for existence of a symmetric Nash equilibrium. We begin with the following definition. Define as follows.

Based on these definitions, we have the following lemma.

Lemma 7

Proof:

From the definition of in Eq. (5) we have

where the partial derivatives on the r.h.s. are w.r.t. Now from the definition of and from Eq. (8) we have

Similarly, from the definition of we have

where the partial derivatives on the r.h.s are now w.r.t Note that since we have Further note that since the servers are identical, i.e., for from the definition of we have From Eq. (15) and the fact that , we have

This proves that ∎

We now have the following theorem, that characterizes the necessary condition for a symmetric Nash equilibrium.

Theorem 3

Let be a symmetric Nash equilibrium for the duopoly price competition. Then .

Proof:

Recall that the Nash equilibrium is characterized as

where for This implies that and since we have for Now from Lemma 3 and symmetry of the servers, this implies that and Since the servers are identical, we have and hence Since is also a solution to program P8, From the definition of this implies that Further, this implies from the definition of that

We have and hence from the definition of for we have From Lemma 7, we have and hence This completes the proof. ∎

Note that the above theorem only provides a necessary condition for the Nash equilibrium pair and we shall soon see that in fact this condition is not sufficient. We shall now provide a few examples illustrating the occurrence of symmetric Nash equilibria.

Example 3: In this example, we assume that for Let while the arrival rate is We suppose that the distribution has a uniform distribution with support of We plot and as a function of in Fig.10. The aim of this example is to check whether is a symmetric Nash equilibrium. For the set of parameters of this example we have and since

we have We now set Clearly, for a symmetric Nash equilibrium , must hold. It is easy to see from Fig. 10 that is indeed maximized when implying that Further it can be verified that Clearly, is a symmetric Nash equilibrium for this example.

Example 4: With the help of this example, we will illustrate that the necessary conditions stated in the previous theorem need not be sufficient. We shall once again assume that where As for the choice of we consider an exponential distribution with A plot of and as a function of is provided in Fig. 11. For this example we start by setting However we observe that the best response and hence Both these points and are represented in Fig. 11. Clearly, and therefore the sufficiency conditions differ from the necessary ones.

VI Estimating the distribution

Recall that denotes the distribution function for the delay sensitivity of the arriving customers. The knowledge of is necessary to determine the equilibrium kernel introduced in Theorem 1. Further, the kernel must be known for the revenue maximization problems seen in this paper. However in most practical situations, the distribution function may not be known and due to the unobservable nature of the queues it may not be possible to even elicit such information from the arriving systems. In such situations the only alternative may be to estimate this distribution function. One possible method to do so is to vary the admission prices at the servers and then measure the change in the arrival rate of customers to the different server and then use the Wardrop equilibrium conditions to estimate . In this section, we shall describe a simple procedure to estimate the underlying continuous distribution function Our proposed method is well suited for a monopoly system when the single service provider has access to both the admission prices. In this section, we also consider the case when is a discrete random variable. In this case, the customers are divided into finite number of classes differing in their values of The aim is to identify the value of for the different classes along with the Poisson arrival rates for the classes. Refer [13, 16, 20] for some examples of service systems where such discrete customer classes are considered.

Throughout this section, we shall make the following assumptions. We shall assume that the two servers are modeled as queues with service rates and and admission prices and respectively. With this assumption, we have It goes without saying that our analysis will also hold for any delay cost that is monotonic and strictly increasing in its arguments. We assume that once the admission prices and at the servers are announced and that the Wardrop equilibrium is achieved, each server will accurately determine or measure the equilibrium arrival rate and the mean delay cost for Hence the measured values and and the the corresponding quantities at the Wardrop equilibrium will be assumed to be the same. We also assume that the total arrival rate of customers to the system denoted by is known a priori and that i.e., the admission price at the first server is higher than the second. Note that since the distribution is unknown, the functions also cannot be determined and used for our procedure.

We begin by estimating the distributions that belongs to a parameterized family, say for example the exponential distribution. Let the parameter for the exponential distribution be denoted by When and at the two servers are fixed, the equilibrium and at the servers is measured immediately. We choose a such that for From this, the mean delay cost for is also calculated. Since all the quantities (except ) in Eq. (3) of Theorem (1) are known, the threshold can be determined as Now increase to where for This decreases the equilibrium to say Let denote the threshold when the arrival rate to Server 1 is Again, using the measurements of the arrival rates and the delay functions can be determined from Eq. (3). Since , from Lemma 2, we know that This implies that Clearly, the ratio is the probability of an arriving customer with and hence

| (19) |

The only unknown quantity is the exponential parameter which can now be obtained from the above equation.

Remark 3

Since the exponential distribution has a single parameter, the parameter could be obtained using only Eq. (19). For a parameterized distribution with parameters, we need simultaneous equations in terms of the underlying parameters. These can be obtained by following the procedure above for different admission price at Server 1.

We will now describe a numerical method to obtain a piecewise constant approximation for the density function that is not necessarily from a parameterized family of distribution functions. As an example, consider a random variable supported on the range Suppose the distribution function is

The corresponding density function is denoted by is for For this example assume that there are two servers with service rates and admission prices initially set to and the total arrival rate . As earlier, we assume that once the admission prices at the servers are announced, the Wardrop equilibrium is reached instantaneously and each servers can accurately determine the aggregate arrival rates and the mean delay per customer.

Increase by and for the admission price vector measure the equilibrium arrival rates and the mean delay in the queues and calculate the corresponding threshold using Eq. (3). Repeat this for a finite number of times, each time increasing from its previous value by This experiment is denoted in Table I.

| 5.0 | 5 | 1.98 | 2.84 |

|---|---|---|---|

| 5.2 | 5 | 1.69 | 3.04 |

| 5.4 | 5 | 1.44 | 3.20 |

| 5.6 | 5 | 1.23 | 3.33 |

| 5.8 | 5 | 1.05 | 3.44 |

| 6.0 | 5 | 0.89 | 3.53 |

| 6.2 | 5 | 0.75 | 3.60 |

| 6.4 | 5 | 0.63 | 3.67 |

| 6.6 | 5 | 0.52 | 3.37 |

| 6.8 | 5 | 0.43 | 3.78 |

Using the earlier notation, we observe from the table that as increases to, say , decreases to while the threshold increases (to ). As earlier, we have

where the density function is to be estimated. Assume for all that where is a constant. By assuming this, we are approximating the density function for by a horizontal line of magnitude and thus approximating by a piecewise constant function. As the approximation should converge to the true density function. We now have

| (20) |

The value of for a fixed and can be viewed as an estimate for the density function and obviously as These values of for different values of are given in Table II.

| 5 | 5.2 | 0.37 |

| 5.2 | 5.4 | 0.39 |

| 5.4 | 5.6 | 0.41 |

| 5.6 | 5.8 | 0.42 |

| 5.8 | 6.0 | 0.44 |

| 6.0 | 6.2 | 0.44 |

| 6.2 | 6.4 | 0.45 |

| 6.4 | 6.6 | 0.46 |

| 6.6 | 6.8 | 0.47 |

A plot comparing the true density function and the estimate is given in Fig. 12. The plot shows that the estimate of the density function is reasonably accurate and for better estimation, one naturally required more of such measurement points.

There is however a limitation to this method. Note that when the corresponding value of Any increase or decrease in either or cannot result in a such that This is because, for the underlying distribution we have from Eq. (8) that and for any with we have As a result, the density function cannot be estimated for

VI-A Estimating Discrete Distribution

We shall now consider the case where the distribution is a discrete distribution with point masses. Thus, there are customer classes and we will assume that for each Class the associated waiting cost and the arrival rate are unknown. Further, See [13] for the analysis of Wardrop equilibrium of such a model. We continue with the assumption that there are two servers each charging an admission price and We begin by setting and to an arbitrarily large value such that while This is represented in part (a) of Fig. 13. It goes without saying that the necessary assumption is that Now start decreasing in steps of size and stop at the first instance when increases to an arbitrarily small value We use the notation and to denote the admission price and the arrival rate at Server when is decreased times by , i.e., when implies that the most sensitive delay class must now be using Server 1 along with Server 2. Since the delay function at each queue can be measured, can be easily determined from the corresponding Wardrop condition

We will now determine corresponding to this Continue decreasing The proportion of Class customers using Server keeps increasing till all Class customers use only Server When this happens, the corresponding Wardrop equilibrium condition for some satisfies

and this is represented by part (b) in Fig. 13. For a Class 2 customer to start using Server 1, the Wardrop equilibrium condition is

where Further since we have

and hence for all such that we have

This means that for any satisfying and remain unchanged. Clearly in this case Fig. 13, part (c) represents the fact that for any Class 2 customers use both the servers at Wardrop equilibrium. Continue this process till all the as well as the number of customer classes is determined. It should be noted that the accuracy of our method increases as A downside of a small is that the procedure may take a very long time to discover the system parameters.

VII Summary and Future work

In this paper, we have considered the problem of revenue maximization in parallel server systems. We specialize with the case of two servers and first assume the case when both the servers belong to the same service provider. The admission price at one of the server is required to be fixed and the service system can change the admission price at the other server to maximize its revenue. The Wardrop equilibrium when customers are heterogeneous and strategic has already been characterized in our earlier paper. We use this characterization to simplify the revenue maximization program to make it more amenable to analysis. The equivalent program is easy to interpret, analyze and provides more insight into the problem. While it is intuitive that for a fixed the revenue maximizing should always be greater than the program enables to characterize the revenue maximizing as a function of

In the second part of the paper, we consider the duopoly model where each server competes with the other one to maximize its revenue. This is a standard game-theoretic problem and the aim is to identify the Nash equilibrium set of prices. We see however that since the customers are heterogeneous, the first order necessary conditions are not easy to solve. Instead, we characterize this Nash equilibrium for a simplified case when the two servers are identical in their delay characteristics. In this case we are interested in the symmetric Nash equilibrium prices. We provide the necessary condition for this case and identify the Nash equilibrium prices for different distributions and delay cost functions

In both these problems problems and also in the social welfare maximization problem of our previous paper, an important assumption is that the distribution function is known. We relax this assumption in Section VI and provide a procedure to estimate this distribution. The proposed method is of course preliminary and assumes that one is allowed to change admission price any number of time to measure the change in the equilibrium arrival rate. Further, we have assumed that there is no cost to making such measurements. A more realistic method incorporating these practical limitations may make the problem more relevant and this is part of future work.

Appendix

Lemma 1

Proof:

We first prove that implies Recall the definition of that

Since is monotonic and increasing in for and that we have for Now let Since no customer uses Server 1 at equilibrium, this implies that for all Since (assumption) must be true.

When we will show that Suppose this is not true, i.e., while . implies As customers have an incentive to move from the server with a higher admission price to the one with a lower price. This implies that is not an equilibrium and this is a contradiction.

Now consider where From Theorem 1, implies and hence Since we have

We now prove that if then We first show that when we have Suppose that when From the definition of we have and hence customers have an incentive to move from the server with higher expected delay to the one with lower expected delay. This implies that when is not an equilibrium.

Now let From Theorem 1 we have either or or The case corresponds to the case when all customers choose Server 2 at equilibrium and this cannot happen! This is because while we have also assumed with will be possible only if

for all Now this is not possible as the left hand side is positive while the right hand side is negative. It is straightforward to see that when we have and hence When we have Again, since we have and this requires The proof for follows along similar lines and will not be provided. This completes the proof. ∎

Lemma 2

Proof:

From Lemma 1, implies that while implies Now from Theorem 1, when we have

Similarly, when we have

Now defined as the value of threshold when the equilibrium arrival rate to Server 1 is can be represented as follows.

| (21) |

Now as seen earlier, is absolutely continuous and strictly increasing in its domain. Further, the support is and hence is a bijective function whose inverse exists. In fact is continuous and strictly increasing in its domain. The statement of the lemma now follows. ∎

Lemma 3

Proof:

Recall our assumption that is continuous and monotone increasing in where Since is monotone decreasing in for Recall Eq. (8) that determines For is continuous and strictly decreasing. The continuity follows from that of Since is strictly increasing in its arguments, is decreasing in Clearly, is monotone decreasing when is such that

When is such that from the definition of we have In this range of it can be seen from Eq. (8) that is continuous and increasing in . This again implies that is continuous decreasing when satisfies

follows from the definition of where The continuity at is obvious from the fact that and ∎

Lemma 4

Proof:

Suppose From the definition of and from Eq. (5), this implies that

for all From the Wardrop equilibrium condition, this implies that for This implies that and from Eq. (2) we have Similarly when, we have

where Again, from the Wardrop equilibrium condition, this implies that for Hence and from Eq. (2), we have

Now suppose where we know that and From Lemma 3, we know that is monotonically decreasing in Therefore there exists a unique with such that This proves the uniqueness of To see how note that implies that

Now if we have In this case,

for This means that for all Similarly, we have

| (22) |

and when Similar arguments hold when and hence when

From Theorem 1, is characterized by and for a fixed is unique. This implies uniqueness of It is important to mention that is unique when because of the assumptions made to ensure well defined at . ∎

Lemma 5

Proof:

Suppose satisfies Assume that so that we have From Lemma 4 this implies that the equilibrium satisfies . Let us label this as Now increase from by a small such that there exists that satisfies Now from the monotonicity of it is clear that the equilibrium is decreasing as increases. This implies that a higher caused by increasing will only lead to a satisfying Clearly, for any choice of we have and hence for this case

Now suppose that When this implies and from Lemma 4 this implies with the corresponding satisfying As we increase the equilibrium decreases and hence satisfies The compact representation now follows. ∎

Lemma 6

Proof:

To reduce the notations, we represent by in the proof of the lemma. We shall prove that and the proof for is along similar lines. Suppose Then from the requirement that we have either (1) and or (2) and First consider the case when and This implies that and hence the revenue made by Server 1 at equilibrium is zero. Further since this is an equilibrium, there is no incentive for the server to change the admission price and increase its revenue. We shall now show that this is not true. From Theorem 2, we know that for a given the admission price at Server must be at least Now we know that setting will result in Now due to the assumption that (1) and (2) there exists an such that setting will result in The revenue earned is non-zero and there is clearly an incentive to deviate from any value greater than This implies that and is not possible. The proof for and is along the same lines. ∎

References

- [1] P. Naor, The regulation of queue size by levying tolls, Econometrica 37 (1969) 15–24.

- [2] N. Edelson, D. Hilderbrand, Individual and social optimization in a multiserver queue with a general cost benefit structure, Econometrica 40 (1972) 515–528.

- [3] U. Yechiali, On optimal balking rules and toll charges in the GI/M/1 queue, Operations Research 19 (1971) 349–370.

- [4] C. Larsen, Investigating sensitivity and the impact of information on pricing decisions in an M/M/1/ models, International Journal of Production Economics (1998) 365–377.

- [5] H. Chen, M. Frank, State dependent pricing with a queue, IIE Transactions 33 (10) (2001) 847–860.

- [6] N. Edelson, D. Hilderbrand, Congestion toll for Poisson queuing processes, Econometrica 43 (1975) 81–92.

- [7] H. Mendelson, Pricing services: queueing effects, Communications of the ACM 28 (5) (1985) 312–321.

- [8] H. Mendelson, S. Whang, Optimal incentive-compatible priority pricing for the M/M/1 queue, Operations Research 38 (5) (1990) 870–883.

- [9] R. M. Bradford, Incentive compatible pricing and routing policies for multi-server queues, European Journal of Operational Research 89 (1996) 226–236.

- [10] Y. Masuda, S. Whang, Dynamic pricing for network service: equilibrium and stability, Management Science 45 (1999) 857–869.

- [11] H. Chen, M. Frank, Monopoly pricing when customers queue, IIE Transactions 36 (6) (2004) 569–581.

- [12] T. Bodas, A. Ganesh, D. Manjunath, Load balancing and routing games with admission price, in: Proceedings of the IEEE Conference on Decision and Control, 2011.

- [13] T. Bodas, A. Ganesh, D. Manjunath, Tolls and welfare optimization for multiclass traffic in multiqueue systems, arXiv preprint arXiv:1409.7195.

- [14] I. Luski, On partial equilibrium in a queuing system with two servers, The Review of Economic Studies 43 (1976) 519–525.

- [15] D. Levhari, I. Luski, Duopoly pricing and waiting lines, European Economic Review 11 (1978) 17–35.

- [16] M. Armony, M. Haviv, Price and delay competition between two service providers, European Journal of Operation Research 147 (2003) 32–50.

- [17] H. Chen, Y. Wan, Price competition of make-to-order firms, IIE Transactions 35 (9) (2003) 817–832.

- [18] P. Dube, R. Jain, N-player Bertrand-Cournot games in queues: Existence of equilibrium, in: Proceedings of the 46th Annual Allerton Conference on Communication, Control, and Computing, 2008, 2008, pp. 491–498.

- [19] P. Dube, R. Jain, Diffserv pricing games in multi-class queueing network models, in: Proceedings of International Teletraffic Congress (ITC-22), 2010.

- [20] M. Mandjes, J. Timmer, A duopoly model with heterogeneous congestion-sensitive customers, European Journal of Operational Research 3 (2007) 445–467.

- [21] G. Allon, A. Federgruen, Service competition with general queueing facilities, Operations Research 56 (2008) 827–849.

- [22] G. Allon, A. Federgruen, Competition in service industries, Operations Research 55 (2007) 37–55.

- [23] J. G. Wardrop, Some theoretical aspects of road traffic research communication networks, Proceedings of Industrial and Civil Engineering 1 (1952) 325–378.

- [24] U. Ayesta, J. Anselmi, A. Wierman, Competition yields efficiency in load balancing games, in: Proceedings of the IFIP Performance, 2011, pp. 968–1001.

- [25] M. J. Osborne, An Introduction To Game Theory, Oxford University Press, USA, 2003.

- [26] T. Bodas, D. Manjunath, On load balancing equilibria in multiqueue systems with multiclass traffic, in: Proceedings of NETGCOOP, 2011.

- [27] T. Tao, Analysis (Volume 1), Hindustan Book Agency, 2006.