Extended nonlinear feedback model for describing episodes of high inflation

Abstract

An extension of the nonlinear feedback (NLF) formalism to describe regimes of hyper- and high-inflation in economy is proposed in the present work. In the NLF model the consumer price index (CPI) exhibits a finite time singularity of the type , with , predicting a blow up of the economy at a critical time . However, this model fails in determining in the case of weak hyperinflation regimes like, e.g., that occurred in Israel. To overcome this trouble, the NLF model is extended by introducing a parameter , which multiplies all therms with past growth rate index (GRI). In this novel approach the solution for CPI is also analytic being proportional to the Gaussian hypergeometric function , where is a function of , , and . For this hypergeometric function diverges leading to a finite time singularity, from which a value of can be determined. This singularity is also present in GRI. It is shown that the interplay between parameters and may produce phenomena of multiple equilibria. An analysis of the severe hyperinflation occurred in Hungary proves that the novel model is robust. When this model is used for examining data of Israel a reasonable is got. High-inflation regimes in Mexico and Iceland, which exhibit weaker inflations than that of Israel, are also successfully described.

pacs:

02.30.Gp Special functions; 02.40.Xx Singularity theory; 64.60.F- Critical exponents; 89.20.-a Interdisciplinary applications of physics; 89.65.Gh Economics, econophysics; 89.65.-s Social and economic systemsI Introduction

When inflation surpasses moderate levels it damages real economic activities. For instance, it affects government’s tax revenues because they are effectively received a period later after the declaration that fix them olivera67 ; tanzi77 . The perception of relative prices changes becomes more difficult since it is not easy to distinguish whether some price grows as a consequence of a relative price change or it is part of general inflation (the Lucas problem lucas72 ). It produces inefficient changes of relative prices king12 if the adjustment process is different for different kinds of goods inducing misleading allocation of resources fisher81 . Inflation also affects currency in its property as medium of exchange, store of value, and unit of account. The degree of perturbation is greater the higher the inflation. If consumption goods become relatively more expensive than leisure due to inflation, labor market may be negatively perturbed by reduction of working hours supply cooley89 . Unanticipated increase in prices reduces real wages and expand employment taylor80 , although the positive employment effect could be lowered or reversed by the effects of falling investment. Furthermore, investment demand may be especially affected because of the shorter planning time scope and growing uncertainty. In general, when the inflation is higher then the decision horizon is shorter. Moreover, with no alternative allocation to money, savings decline and investment falls at expenses of actual consumption, lowering the capital stock growth. Therefore inflation is not a pure nominal problem,m but it is linked to real economy in many non trivial ways heymann95 . Consequently, governments try to prevent high inflation, and to lower it when reach elevated levels. Parameters can change once policy changes lucas76 . The relation between sources of inflation and the evolution of parameters is complex and not direct. These issues are also analyzed in text books on econophysics stanley99 ; stauffer99 ; sornette03b .

Models of hyperinflation are especially suitable to emphasize that inflation implies bad “states of nature” in economy. Wars, changes of social regimens, states bankruptcies are the characteristics of such regimens. These factors together with the influence of pure economical variables like expectations, money demand, velocity of circulation and quantity of money, give an increase of the consumer price index (CPI) larger than exponential as can be observed in the investigated cases cagan56 ; mizuno02 ; sornette03 ; szybisz08 ; szybisz09 ; szybisz10 ; szybisz15 ; szybisz16 . In turn, this behavior affects negatively the social network causing unpleasant situations.

The model for hyperinflation available in the literature is based on a nonlinear feedback (NLF) characterized by an exponent of a power law. In such an approach the CPI exhibits a finite time singularity of the form , allowing a determination of a critical time at which the economy would crash. This model has been successfully applied to many cases sornette03 ; szybisz08 ; szybisz09 ; szybisz10 ; szybisz15 ; szybisz16 . However, in the most recent paper szybisz16 , it is shown that for the episode of weak hyperinflation occurred in Israel it is impossible to determine a value for within the NLF model because goes to zero. In this limit one gets the linear feedback approach which does not contain information on mizuno02 . This drawback was attributed to a permanent but partially successful efforts for stopping inflation in Israel.

In order to include in the NLF formalism information on efforts for stabilization like those observed in the case of Israel, we developed an extension of this model introducing a parameter , which multiplies all the past growth rate index (GRI) contributions changing the relative weight of the therm with the power law. The interplay between and leads to multiple equilibria phenomena for episodes of high inflation. The literature on this kind of behavior in models of economics is large and diverse cooper99 , see also e.g. Refs. diamond82 ; bruno1987 ; obstfeld96 ; krugman99 ; morris00 ; nadal05 . We use the well known multiple equilibria expression to indicate the existence of multiple trajectories compatible with data which lead to very different states of nature of the economy where the final outcome is stable or not. In the extended NLF approach the solution for CPI becomes proportional to the Gaussian hypergeometric function , where is a function of , , and . Since for this hypergeometric function diverges, a finite time singularity shows up allowing a determination of . It is important to notice that the Gaussian hypergeometric appears in a variety of physical and mathematical problems. In quantum mechanics, the solution of the Schrödinger equation for some potentials is expressed in terms of flugge71 . Moreover, the eigenfunctions of the angular momentum operators are sometimes written in terms of functions abramowitz72 .

In the present work we also investigated the effects of the parameter on the non linear dynamic evolution of real inflations. Firstly, the robustness of the novel model is tested analyzing the severe hyperinflation occurred in Hungary after World War II. Next, it is successfully applied for studying the weaker hyperinflation developed in Israel and the high-inflation episodes observed in Mexico and Iceland. In order to understand better the evolution of prices in these countries, brief descriptions of historical events are provided. In these cases we found multiple equilibria.

The paper is organized in the following way. In Sec. II the NLF model is outlined with some details because it is the starting point for the extension proposed in Sec. III. The limit is discussed. Section IV is devoted to report and discuss the results obtained by applying the novel approach. Finally, the main conclusions are summarized in Sec. V.

II Theoretical background

Let us recall that the rate of inflation is defined as

| (1) |

where is the CPI at time and is the period of the measurements. In the academic financial literature, the simplest and most robust way to account for inflation is to take logarithm. Hence, the continuous rate of change in prices is defined as

| (2) |

Usually the derivative of Eq. (2) is expressed in a discrete way as

| (3) | |||||

The GRI over one period is defined as

where a widely utilized notation

| (5) |

was introduced. It is straightforward to show that the accumulated CPI is given by

| (6) |

II.1 Adaptive inflationary expectation

In the fifties, Cagan has proposed cagan56 a model of inflation based on the mechanism of “adaptive inflationary expectation” with positive feedback between realized growth of the market price and the growth of people’s averaged expectation price . These two prices are thought to evolve due to a positive feedback mechanism: an upward change of market price in a unit time induces a rise in the people’s expectation price , and such an anticipation pushes on the market price. So, one may write

| (7) |

Actually indicates that the process induces a non exact proportional response of adaptation due to the fact that the expected inflation expands the response to the price level in order to forecast and meet the inflation of the next period. Now, one may introduce the expected GRI

| (8) |

II.2 The NLF Model

Sornette, Takayasu, and Zhou (STZ) sornette03 introduced a nonlinear feedback (NLF) process in the formalism suggesting that the people’s expectation price obeys

Here is a positive dimensionless feedback’s strength and is the exponent of the power law. This expression together with Eq. (7) leads to

| (10) |

Taking the continuous limit of this relation one obtains the following equation for the time evolution of

| (11) |

The solution for GRI follows a power law exhibiting a singularity at finite-time sornette03 ; szybisz08 ; szybisz09

| (12) |

The critical time being determined by the initial GRI , the exponent , and the strength parameter

| (13) |

The CPI is obtained by integrating according to Eq. (6). For , denoted as case (i), it becomes

(i.a) For one also gets a finite-time singularity in the -CPI according to the power law

| (15) |

This expression has been used for the analysis of hyperinflation episodes reported in previous papers sornette03 ; szybisz09 ; szybisz08 ; szybisz10 ; szybisz15 .

(i.b) For one gets a finite-time singularity for , but the log-CPI evolves as

| (16) |

converging to a finite value when time approaches the critical value

| (17) |

(ii) For the integration in Eq. (6) yields

| (18) |

Upon introducing in this expression, the time dependence of exhibits a logarithmic divergence

| (19) |

It was found that for severe episodes of hyperinflation one may get szybisz10 ; szybisz15 .

In both regimes, (i.a) and (ii), the CPI exhibits a finite-time singularity at the same critical value as GRI. Hence, these solutions correspond to a genuine divergence of .

It is important to notice that for one gets the linear feedback (LF) model suggested previously by Mizuno, Takayasu, and Takayasu (MTT) mizuno02 . In this limit one arrives at

| (20) |

Hence, the CPI grows as a function of following a double-exponential law szybisz09 ; mizuno02

| (21) |

In the LF model no can be determined. Furthermore, by setting now one gets

| (22) |

and

| (23) |

which is the Cagan’s original proposal.

III Extension of the NLF model

Let us now present a way for introducing to some extent information on saturation within the framework of the theory outlined in Sec. II.2. A simple generalization of the formalism would be to include a parameter multiplying in the feedback term

| (24) |

However, this attempt leads to a mere change of the parameter by

| (25) |

Hence, this kind of approach should be done in a more elaborated way. An adequate procedure is to multiply by all the terms corresponding to past GRI, i.e. , in Eq. (LABEL:rate00)

In this case the Eq. (10) becomes

| (27) |

The new parameter would account for the changes of actions in the private, external and/or government sector. Equation (27) may be cast into the form

| (28) | |||||

which can be rewritten as

| (29) |

Upon dividing both sides of this relation by and doing the transition from discrete to continues functions one gets a differential equation of the Bernoulli type

| (30) | |||||

where

| (31) |

are introduced to simplify the notation at this stage. Equation (30) can be cast into the form

| (32) |

Introducing the change of variables

| (33) |

one gets the linear differential equation

| (34) |

with the constrain

| (35) |

The solution is

| (36) |

which leads to

| (37) | |||||

Hence, the GRI in this extended NLF (denoted as ENLF) model becomes

| (38) | |||||

In the limit one gets

| (39) |

In turn, the CPI is given by

The general solution provided by the Wolfram’s Mathematica on line integrator reads

| (41) | |||||

where is the Gaussian hypergeometric function (see Appendix A) with

| (42) |

Furthermore, by introducing this expression for in Eq. (41), the latter equation for log-CPI can be cast into a more compact form

| (43) | |||||

with

| (44) |

and

| (45) |

Notice that for the hypergeometric function diverges. Let us emphasize that Eq. (43) embodies solutions or all sectors of . Although for a simple integration yields

The latter result can be also obtained by introducing into Eq. (43) the expression of the hypergeometric functions corresponding to

| (47) |

This procedure yields

| (48) | |||||

leading to Eq. (LABEL:lptln1).

Equations (43) and (LABEL:lptln1) have two domains of solutions, one for (implying ) and the other for (). In the Appendix B we show that in the limiting case (i.e., ) from above, the generalized expressions for GRI and CPI provided by the ENLF model reduce to the forms reported previously in Refs. szybisz09 ; sornette03 and summarized in Sec. II.

III.1 Critical time in the ENLF model

Let us now rewrite Eqs. (38), (43), and (LABEL:lptln1) in terms of and determine the critical time within this novel formalism. In so doing, after inserting the definitions of and in Eq. (38) for GRI, we obtain

| (49) |

with

| (50) |

The CPI becomes

| (51) | |||||

with

| (52) |

keeping in mind that . For , the CPI reduces to

The finite time singularity occurs at the same value of critical for GRI and for both sectors (51) [with (52)] and (LABEL:lptln2) of solutions for log-CPI, satisfying

| (54) |

In turn, the critical time can be determined by equating this relation with given by Eq. (50)

| (55) |

The result is

| (56) |

providing the new expression for .

III.2 Observables as a function of in the ENLF model

| Period | Parameters | Model | |||||

|---|---|---|---|---|---|---|---|

| 1945:04:30-1946:07:15 | 1946:09:03 | 0.150 | 0.500 | 3.82 | NLF∗ | 1.168 | |

| 1946:07:3001 | 0.1990.003 | 0.7000.004 | 4.07 | NLF | 0.759 | ||

| 1946:07:2804 | 0.2160.017 | 0.7330.044 | 3.660.17 | NLF | 0.704 | ||

| 1946:07:3001 | 0.1990.003 | 0.7000.004 | 1.00010.0058 | 4.07 | ENLF | 0.761 | |

| 1945:04:30-1946:07:31 | 1946:09:0205 | 0.1580.011 | 0.5140.026 | 4.07 | NLF | 1.123 | |

| 1946:09:0103 | 0.1600.008 | 0.5180.014 | 3.440.27 | NLF | 1.123 | ||

| 1946:09:0201 | 0.1580.001 | 0.5140.001 | 1.00030.0179 | 4.07 | ENLF | 1.123 | |

∗ The values of the parameters listed in this line were calculated using those reported by STZ sornette03 , see text.

Furthermore, the CPI can be cast into the form

| (61) | |||||

where is

| (62) |

For one gets , while at the value of becomes unity and at this point the hypergeometric function diverges. For , instead of Eq. (61) one can write

| (63) | |||||

IV Analysis of hyper- and high-inflation episodes applying the ENLF model

In a first step, we shall show that the ENLF formalism is robust for episodes of severe hyperinflation, leading to values of very close to unity. Next, cases of weaker inflations will be treated.

IV.1 Catastrophic hyperinflation in Hungary

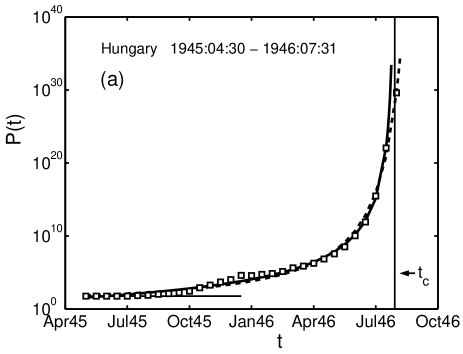

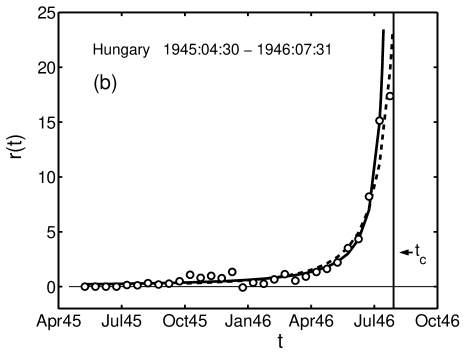

Let us begin the application of the novel approach by tackling an emblematic case. An important test for any formalism developed for describing regimes of high inflation is to verify whether it is able to account for the evolution of prices occurred in Hungary right after World War II mizuno02 ; sornette03 . For this severe hyperinflation there is available a data series collected in Table A.1 of Ref. paal00 (see also grossman00 ) constructed on a basis of a biweekly frequency. The word “biweekly” is used to designate data available on the 15th and on the last day of each month. Figure 1 shows the CPI and GRI during the period from April 30, 1945 to July 31, 1946 (i.e., from 1945:04:30 to 1946:07:31, in the case of Hungary the notation Year:Month:Day will be used). Notice that the CPI values are normalized to . Several fits of these data were performed.

An inspection to Fig. 1(b) suggests that the value at 1946:07:31 could be already affected by the stabilization policy adopted by the Hungarian government paal00 . Therefore, in a first step we performed a fit of CPI data up to 1946:07:15 with Eq. (15) setting . The numerical task was accomplished by using a routine of the book by Bevington bevington69 cited as the first reference in Chaps. 15.4 and 15.5 of the more recent Numerical Recipes press96 . In practice, the applied procedure yields the uncertainty in each parameter directly from the minimization algorithm. The parameters yielded by these fits are listed in Table 1 together with the root-mean-square (r.m.s.) residue of the fit, . A simple inspection indicates a crash at the beginning of August 1946. Values of GRI were evaluated with Eq. (12). The good quality of the fits is shown by solid curves in panels (a) and (b) of Fig. 1.

Table 1 in Ref. sornette03 indicates that STZ have also analyzed data of Hungary from 1945:04:30 to 1946:07:15. In order to facilitate a quantitative comparison with the study reported by STZ, we evaluated the parameters , , and utilized in the present work by inserting the values of , , , and listed in Table 1 of Ref. sornette03 into the following relations

| (64) | |||

| (65) | |||

| (66) |

These results are included in our Table 1. A glance at this table indicates a shift between the present results and that of STZ.

For the sake of completeness, we also analyzed CPI data including the value at 1946:07:31. This fit yielded the parameters quoted in Table 1 and the dashed curves in panels (a) and (b) of Fig. 1 show the adjustment. As expected, the new fit suggests a later date for the crash of the economy than the prediction provided by the shorter series, now the blow up would occur at the beginning of September 1946. Surprisingly, one may observe in Table 1 that the results of STZ, including the , are almost the same as that obtained in the present work with the series ending at 1946:07:31. For the sake of completeness, fits leaving free were also performed. Looking at Table 1 one may realize that no significant changes are obtained.

As planned the study of the Hungarian hyperinflation is finished by applying the ENLF formalism derived in Sec. III of the present paper. In so doing, both the shorter and larger series of CPI data were fitted to Eq. (61). The obtained parameters are also quoted in Table 1, where one can observe that all the “old” parameters remain unchanged. Predictions for GRI were computed using Eq. (LABEL:rate57). The match to Eqs. (LABEL:rate57) and (61) and those corresponding to Eqs. (12) and (15) are indistinguishable on the scales of Fig. 1. One can realize that in both cases stays equal to unity within the uncertainty. For the complete series up to 1946:07:31 the uncertainty is slightly larger, this feature could be attributed to the beginning of the stabilization process. All these results support the robustness of the extended model.

| Country | Period | Parameters | Model | ||||||

|---|---|---|---|---|---|---|---|---|---|

| Iceland | 1960-1983a | 0.0970.032 | 0.0630.026 | LF | 0.0817b | ||||

| 2049122 | 0.120 | 0.0680.027 | 0.1360.225 | NLF | 0.0828b | ||||

| 2141264 | 0.107 | 0.0650.026 | 0.0610.096 | NLF | 0.0818c | ||||

| 2291 | 0.076 | 0.0640.051 | 0.0371.664 | 1.0440.073 | 0.7650.391 | ENLF(z0) | 0.0817b | ||

| 204918 | 0.092 | 0.0670.014 | 0.1510.033 | 1.0420.066 | 0.774 | ENLF(tc) | 0.0825b | ||

| 2049.75.8 | 0.091 | 0.0670.006 | 0.1510.011 | 1.0420.022 | 0.750 | ENLF(tc) | 0.0825c | ||

| Israel | 1969-1985 | 1988.06 | 0.077 | 0.149 | STZd | 0.085 | |||

| 0.1760.035 | 0.1010.035 | LF | 0.0876b | ||||||

| 206172 | 0.184 | 0.1090.035 | 0.0690.061 | NLF | 0.0947b | ||||

| 2527456 | 0.177 | 0.1020.035 | 0.0100.009 | NLF | 0.0883c | ||||

| 2170 | 0.130 | 0.1040.016 | 0.0220.117 | 1.0760.008 | 0.7780.022 | ENLF(z0) | 0.0890b | ||

| 2015.54.8 | 0.146 | 0.1160.018 | 0.1720.021 | 1.0690.068 | 0.758 | ENLF(tc) | 0.1046b | ||

| 2015.60.6 | 0.144 | 0.1160.003 | 0.1720.003 | 1.0720.008 | 0.750 | ENLF(tc) | 0.1044c | ||

| 1969-1984 | 0.1780.045 | 0.1000.040 | LF | 0.0885b | |||||

| 204879 | 0.189 | 0.1070.041 | 0.0810.093 | NLF | 0.0942b | ||||

| 2430489 | 0.179 | 0.1010.041 | 0.0120.014 | NLF | 0.0892c | ||||

| 2273 | 0.130 | 0.1020.019 | 0.0220.161 | 1.0770.011 | 0.7750.029 | ENLF(z0) | 0.0895b | ||

| 2014.86.2 | 0.149 | 0.1120.021 | 0.1700.027 | 1.0710.085 | 0.758 | ENLF(tc) | 0.0993b | ||

| 2014.90.7 | 0.147 | 0.1120.003 | 0.1700.003 | 1.0740.010 | 0.750 | ENLF(tc) | 0.0992c | ||

| Mexico | 1960-1988a | 0.1520.028 | 0.0140.008 | LF | 0.0808b | ||||

| 213299 | 0.162 | 0.0160.009 | 0.0430.028 | NLF | 0.0890b | ||||

| 3175731 | 0.153 | 0.0150.008 | 0.0060.004 | NLF | 0.0817c | ||||

| 2069 | 0.127 | 0.0180.008 | 0.0820.149 | 1.0610.014 | 0.7630.052 | ENLF(z0) | 0.0941b | ||

| 2033.61.3 | 0.139 | 0.0200.002 | 0.1340.005 | 1.0580.014 | 0.751 | ENLF(tc) | 0.1045b | ||

| 2033.60.3 | 0.139 | 0.0200.001 | 0.1330.001 | 1.0580.002 | 0.750 | ENLF(tc) | 0.1043c | ||

a Data from Ref. FRED . b . c . d The values of the parameters listed in this line were calculated using those reported by STZ sornette03 (see text), in addition, =1.04.

IV.2 Weak hyperinflation in Israel

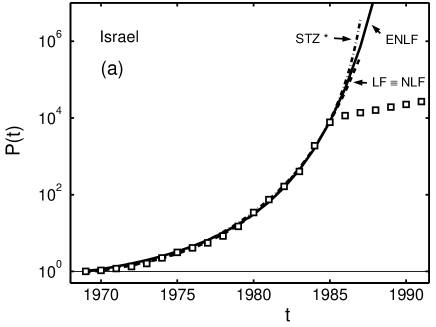

Let us now examine the case of Israel, which have been already studied in a previous work szybisz16 . Figure 2(a) shows the yearly data for the CPI in Israel computed using data taken from a Table of the International Monetary Fund (IMF) imf . The upward curvature of the logarithm of CPI as a function of time indicates that from 1969 to 1985 the hyperinflation exhibits a faster than exponential growth. The inflation got triple-digit rates of about at their peak in the mid-1980’s. Leiderman and Liviatan leiderman03 attributed this response to the implicit preference for short-term considerations of avoiding unemployment over long-term monetary stability. In 1985 a new strategy was applied to stop the hyperinflation.

The results for the parameters and the obtained in the previous work szybisz16 are reproduced in Table 2. Two time series of CPI were examined: one with data from 1969 until 1985 (this series has been studied in Refs. mizuno02 and sornette03 ) and the other excluding the value of 1985 when the final stabilization started. From that analysis it was concluded that when applying the NLF model the fits indicate a strong correlation between and . In Table 2 two sets of parameters are provided, one corresponds to stopping minimization when the change of from the “” to the “”-iteration becomes less than and the other for . Let us mention that for that study was set equal to zero. The fitting procedure showed that decreases approaching zero while increases, this occurs in such a way that the product converges to a constant yielding a well defined value of the parameter given by [see Eq. (13)]

| (67) |

which is also quoted in Table 2. Since for the NLF model converges towards the LF model of MTT

| (68) |

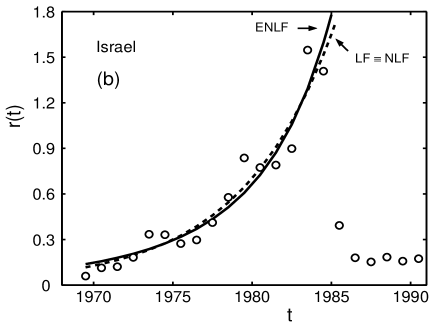

that study was completed by fitting the CPI data directly with Eq. (21). The obtained parameters are also quoted in Table 2. Figure 2(a) shows the good quality of the fit for the larger series. It is also worthwhile to mention that the present value for the parameter utilized in the original LF model, i.e. , is in good agreement with the result quoted by MTT in Table 1 of Ref. mizuno02 . For the sake of completeness, we plotted in Fig. 2(b) the measured data of GRI together with the theoretical values provided by Eqs. (12) and (20), which are indistinguishable on the scale of the drawing.

Although the LF model provides a good fit, it does not predict any indicative for a possible crash of the economy. Therefore, in order to estimate a , we shall apply the novel ENLF model to analyze the evolution of prices in Israel looking for multiple equilibria (or trajectories). In practice, there are two strategies for treating the parameters of the ENLF model. One is to adopt as free parameters , , , and like it was done for the analysis of data for Hungary. The other, is to consider , , , and as free parameters. It is important to notice that the whole contribution of is carried by in the form of the product , which also determines as shown above. Hence, it would be reasonable to expect a solution compatible with the LF model. Therefore, in order to check this feature, the CPI data for the period 1969-1985 were, in a first step, fitted to Eq. (61) expressed in therms of . The obtained parameters are listed in Table 2, where one can observe that the is similar to that obtained for the long NLF run. The value is consistent with zero suggesting a LF with a renormalized strength given by Eq. (30) with

| (69) |

In fact, the results for [evaluated from Eqs. (55) and (60)] and quoted in Table 2 satisfy this relation. This solution remains stable when the minimization procedure is continued. Furthermore, the use of Eq. (60) with the listed results for , , and yields , which is too large for a hyperinflation developing during the 1980’s. So, the prediction of this solution is not useful.

The fit considering , , , and as free parameters yielded the set of results reported in Table 2. The obtained values , , and are quite reasonable for a rather slow hyperinflation. If the fit is continued the parameters do not change, only the uncertainties diminish as can be seen in Table 2. Although the of this solution for is slightly larger than that determined by using , it is quite acceptable. The good quality of the present ENLF(tc) description of measured data for both CPI and GRI is shown in Fig. 2.

The value of obtained by fitting with Eq. (61) is larger than that determined by STZ* from a phenomenological fit of to Eq. (15). This feature is due to the fact that, for a regime with inflation, presents a steeper slope than

| (70) |

The steeper is the curvature the earlier becomes [see Fig. 2(a)].

Since the actions for stopping the inflation begun in 1985 leiderman03 , we also performed an analysis of the reduced period 1969-1984. The values yielded by the new sequence of fits are also included in Table 2. There one can observe small changes between the parameters corresponding to both series of data.

In summary, we can state that in the case of the hyperinflation occurred in Israel it is possible to predict a reasonable by applying the ENLF model proposed in the present paper. In fact, the interaction between and leads to multiequilibria phenomena yielding solutions with (no prediction for ) and ( is determined). As mentioned in Sec. I, the literature on multiple equilibria in economics is huge cooper99 ; diamond82 ; bruno1987 ; obstfeld96 ; krugman99 ; morris00 ; nadal05 .

IV.3 High-inflation episodes in Mexico and Iceland

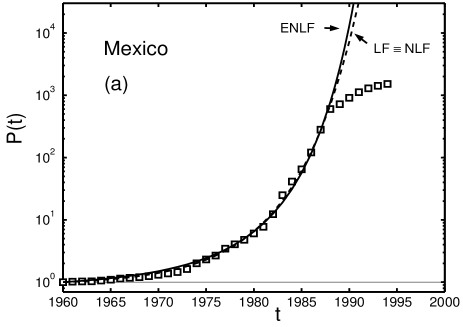

This section is devoted to study regimes of high-inflation that are not catalog as episodes of hyperinflation. Looking at tables of inflations one can find several examples of this type. If evolution of the CPI of such a sort of episodes is described by Eq. (15) one finds similar features to that encountered in the case of Israel. For illustrating this kind of behavior we selected the evolution of prices during periods of high-inflation occurred in Mexico and Iceland.

The economy of Mexico is rather large, the number of inhabitants during the period of high-inflation was close to 100 millions. The general conditions that gave rise to such an inflation have been based on domestic troubles and the management of petroleum business rojas92 ; goodman97 ; bergoeing07 . Political unrest escalated during the 1960’s. Students of the Autonomous National University of Mexico began organizing large scale demonstrations in Mexico City in 1968. These protests were followed by violent episodes including the killing of demonstrators by members of the armed forces goodman97 . At the beginning of the 70’s president Luis Echeverría Álvarez trying to avoid an ongoing insurgency distributed land to a communal farming arrangement. After this step the production decreased substantially. In addition, he promoted extensive subsidies for public and private enterprises. For instance, one of the projects was a steel complex in Michoacán. These programs could not be funded out of existing tax funds so the Central Bank printed money. One of the effects of these policies was a serious inflation accompanied by an economic crisis. At the end of the 70’s during the presidency of José López Portillo y Pacheco new oil fields were discovered in the south of Mexico. Because of the existence of these new reserves and the rising international price of petroleum, foreign bankers were willing to lend Mexico vast amount of money. By 1982 almost half of the petroleum exports earning were going to pay the interest and other scheduled payments for the foreign debt. So, these discoveries did not alleviate the problem of inflation, the annual rate of inflation hit 100% [see Fig. 3(b)]. In September 1982 the banks of Mexico were nationalized. The price of petroleum began to fall in response to the increased quantity of petroleum being supplied. When Miguel de la Madrid Hurtado came into office at the end of 1982 Mexico’s economic house was in a great state of disarray. There was a huge foreign debt requiring excessive foreign currency credit to service. He promulgated a program of economic austerity which included: increases in tax rates; reduction of the federal government budget; reduction of subsidies for some commodities; postponement of many public projects; increase of some interest rates; and relaxation of capital transfer restrictions. The moves toward privatizations started during his administration. Financial necessity forced the selling off of about 200 government enterprises. Nevertheless, the inflation continuously grew, see Fig. 3(b). In 1988, Carlos Salinas de Gotari, young technocrat with a Ph.D. in economics from Harvard University was elected president. The criterion was to find a person with expertize for dealing with Mexico’s financial and economic problems. He deepen successfully the stabilization program for stopping inflation began by de la Madrid, see Fig. 3(b).

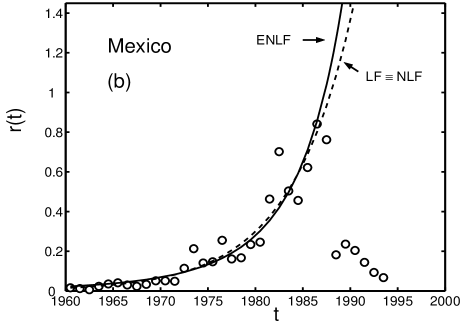

The CPI and GRI were evaluated using data of inflation taken from Ref. FRED , these observables are plotted in panels (a) and (b) of Fig. 3, respectively. The values from 1960 to 1988, previous to stabilization, have been analyzed. For the study of the Mexico’s inflation the same procedure as that applied in the case of Israel was adopted. So, in a first step, we fitted data of CPI with Eq. (15). The parameters together with the obtained by stopping the minimization procedure when the variation of between the “” and “” iterations was smaller than a standard choice are listed in Table 2. A glance at this table shows a small exponent of the power law and a large critical time . If one allows the iterations to continue, the correlation between these parameters becomes clear. For instance, in Table 2 we quoted values obtained when the change of becomes less than . As in the case of Israel, goes to and increases keeping given by Eq. (67) constant. These results indicate that the NLF model tends towards the LF one. Therefore, the analysis was completed fitting the CPI data directly with LF’s Eq. (21). The obtained parameters are included in Table 2. Notice the excellent agreement between the values of , , and yielded by the LF approach and those obtained from the “long” fit with Eq. (15) of the NLF model. The quality of the fits is depicted in Fig. 3(a). In addition, the theoretical GRI was calculated using Eqs. (12) and (20) and it is compared to data in Fig. 3(b). No difference between LF and NLF can be observed. So, no estimation for can be achieved.

Next, the CPI data for the period 1960-1988 were fitted to Eq. (61) provided by the ENLF model written in therms of , , , and . This procedure lead to the values listed in Table 2. The value , although larger than in the case of Israel, is also consistent with zero suggesting a LF. Moreover, the result for also satisfies the relation (69).

Finally, the same data of CPI were fitted with Eq. (61) of the ENLF model written in therms of , , , and . The obtained parameters are also included in Table 2 and the fit is displayed in Fig. 3(a). In this case, both parameters and are well defined and reasonable. Although the is slightly larger than that obtained with the LF model a good match of theoretical CPI with measured data is got. For completeness, the GRI was evaluated using Eq. (LABEL:rate57) and plotted in Fig. 3(b), where one may observe a good accordance with data. These results indicate that the ENLF() model provides a satisfactory description of the episode occurred in Mexico. Hence, one can state that multiple equilibria phenomena are also present in this case. The solution with shows a trajectory towards the category of hyperinflation.

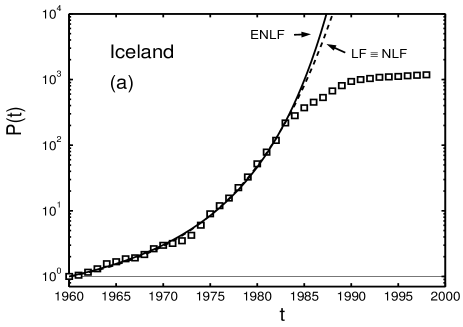

It is also interesting to study the increase of prices occurred in Iceland during the period from 1960 to 1983 andersen98 right previously to the disinflation analyzed by MTT (see Table 2 in Ref. mizuno02 ). Let us mention that Iceland is a nation with less than a half million inhabitants, so in contrast to Mexico this is a rather small economy. Iceland was under Norwegian and Danish kings along centuries. It is an independent nation since 1944. During the examined period the government’s fiscal policy was strictly Keynesian, and their aim was to create the necessary industrial infrastructure for a prosperous developed country. It was considered essential to keep unemployment down to an absolute minimum and to protect the export of fishing industry through currency manipulation and other means. Due to the country’s dependence both on unreliable fish catches and foreign demand for fish products, Iceland’s economy remained very unstable well into the 1990’s, when the country’s economy was greatly diversified. Iceland then became a member of the European Economic Area in 1994. Economic stability increased and previously chronic inflation was drastically reduced.

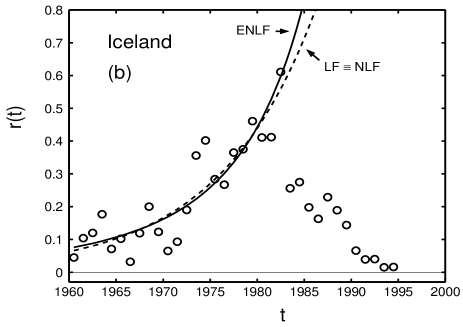

The GRI and CPI for Iceland were evaluated with data taken from FRED and are plotted in panels (a) and (b) of Fig. 4, respectively. One may observe that before stabilization the CPI reaches a value of about , being more than one order of magnitude smaller than the value corresponding to Israel and slightly smaller than that of Mexico. Moreover, a further check of this relative strength of inflations can be done comparing Fig. 4(b) with Figs. 2(b) and 3(b). Hence, the inflation of Iceland was studied in the same way as the episodes of that countries. However, in this case the analysis was begun by fitting data of CPI for the period 1960-1983 with Eq. (21) of the LF model. The obtained parameters are listed in Table 2. The quality of the adjustment is shown in Fig. 4(a). The calculated is smaller than the values quoted in Table 1 of Ref. mizuno02 , indicating that in this case the inflation was less severe than for the examples examined there. Next, a standard “short” fit of the same data for CPI with Eq. (15) of the NLF model, similar to that performed in the cases treated previously, yielded the parameters quoted in Table 2. One may realize that is consistent with zero and is rather undetermined. Furthermore, a “longer” fit indicates that goes to 0 and increases presenting an even larger uncertainty, both these features can be seen in Table 2. On the other hand, given by Eq. (67) converges to a constant value, which coincides with that yielded by the fit with the LF model. The GRI evaluated with Eqs. (12) and (20) is displayed in Fig. 4(b), no difference between the LF and NLF approaches can be observed on the scale of the drawing. So, as expected, in this case the NLF model also converges towards the LF one. Hence, no prediction for could be obtained.

Therefore, in order to get an estimation for , we also applied the ENLF model for analyzing this episode. Firstly, the same series of CPI data was fitted to Eq. (61) written in therms of , , , and . This procedure lead to the values listed in Table 2, where one can realize that the is equal to that obtained with the LF model. The value , although presents a very large uncertainty, it is consistent with zero suggesting a LF. On the other hand, the result for also satisfies the relation (69). However, the critical time calculated with Eq. (60), , is too large making this prediction useless.

Finally, the ENLF model written in therms of , , , and was applied for describing the examined data. The fit with Eq. (61) yielded the parameters are included in Table 2. In this case both parameters, and , are reasonable. If the minimization is continued the values of the parameters remain stable, while their uncertainties diminish. In addition, the is almost equal to that provided by the fit to the LF model. As depicted in Fig. 4(a), the matching between theoretical CPI and measured data is quite good. For completeness, the GRI was evaluated using Eq. (LABEL:rate57) with the parameters of the ENLF() model. The result is plotted in Fig. 4(b), where one may observe a good accordance with data. So, the ENLF() model describes satisfactorily well the episode occurred in Iceland providing an acceptable prediction for in case that this high inflation would become a hyperinflation. This is another example of multiple equilibria.

V Summary and Conclusions

In the present work we treated regimes of hyper- and high-inflation in economy. In a previous work szybisz16 it has been found that for a weak hyperinflation, like e.g. that developed in Israel, was impossible to determine a value of within the frame of the NLF model. This model is based on a power law with an exponent , see Eq. (LABEL:rate00). The mentioned drawback has been attributed to a permanent but incomplete effort for stopping inflation. Therefore, in the present work we suggested to include in the theory information on saturation by introducing a parameter , which multiplies all the past inflation growth rates. This parameter would account for the effort done by the government for coping inflation.

In the extended approach, ENLF, reported in the present paper the solutions for GRI and CPI are also analytic as in the NLF model. In particular, the CPI is expressed in therms of the Gaussian hypergeometric function , where is a function of , , , and , see Eqs. (60)-(62). It is pertinent to notice that appears in a variety of mathematical and physical problems. For this hypergeometric function diverges leading to a finite time singularity, from which a value of can be determined. The same singularity is present in Eq. (LABEL:rate57) for GRI. So, the ENLF model proposed in the present work preserves the well-defined singularities yielded by the power law stemmed from a simple positive nonlinear feedback. This mechanism is important for understanding processes in financial crashes (see Ref. sornette03b and references therein). For completeness, in the appendix it is shown that for the limit from above, one retrieves all the expressions of the NLF model.

An analysis of the severe hyperinflation occurred in Hungary after the World War II proves that the novel ENLF approach is robust. When it is used for examining data of Israel there are two sorts of solutions. One yields consistent with zero (LF model) and the other one gives a well determined and reasonable . As a further application, high-inflation regimes exhibiting weaker inflations than that of Israel were also analyzed. The episodes occurred in Mexico and Iceland are reported in the present work. Data of both series of inflation can be described, as in the case of Israel, with the LF model. However, the ENLF() model also provides additional solutions forecasting possible blow up of the economies in case the high inflation regimes would become spirals of hyperinflation. The corresponding fits are very good and the predicted values of for crashes are acceptable.

The phenomena of multiple equilibria, a known feature in models of economics cooper99 ; diamond82 ; bruno1987 ; obstfeld96 ; krugman99 ; morris00 ; nadal05 , appears due to the fact that the introduction of enlarges the dimension of the hyper-surface, which now also presents minimums in domains where the parameters and are not strongly correlated. So, we can state that the parameter allows a more complete representation of inflationary processes. It is interesting to note that the exponent of the nonlinear feedback of inflation can be controlled by a parameter multiplying the growth rate. Different combinations of parameters may be interpreted as forces acting with its own strength, producing dynamical paths that lead to very different outcomes.

Acknowledgements.

This work was supported in part by the Ministry of Science and Technology of Argentina through Grants PIP 0546/09 from CONICET and PICT 2011/01217 from ANPCYT, and Grant UBACYT 01/K156 from University of Buenos Aires.Appendix: Limits for ()

In this appendix we show that by imposing the limit , which is equivalent to , in the generalized expressions for GRI and CPI the forms reported in Ref. szybisz09 are recovered. So, starting from Eq. (38) for GRI and keeping only linear terms of the expansion in‘powers of one gets

| (71) | |||||

which in the limit , where , yields

| (72) | |||||

recovering Eq. (12).

(i) Starting from the general solution for CPI given by Eq. (43) written as

| (73) | |||||

the limit is evaluated expanding the hypergeometric function for small values of . Using the relation

| (74) |

and the on line Mathematica one gets

| (75) |

Upon introducing this result into Eq. (73) and using the property of functions

| (76) |

the expansion of the exponential yields

| (77) |

When keeping in the CPI only the lowest order of one gets

| (78) |

Furthermore, due to the fact that

| (79) |

the remaining contributions of the Gauss’ hypergeometric function cancel out leading to

| (80) |

Now, the limit , where , leads to

in agreement with Eq. (15).

(ii) In the case of , starting from the CPI given by Eq. (LABEL:lptln1)

| (82) |

for one gets

| (83) | |||||

which coincides with Eq. (19).

References

- (1) J.H.G. Olivera, Money, Prices and Fiscal Lags: A Note on the Dynamics of Inflation, Banca Nazionale del Lavoro Quarterly Review 20 (1967) 258-267.

- (2) V. Tanzi, Inflation, Lags in Collection, and the Real Value of Tax Revenue, IMF Staff Papers, 24 (1977) 154-167; and Inflation, Real Tax Revenue, and the Case for Inflationary Finance: Theory with an Application to Argentina, IMF Staff Papers, 25 (1978) 417-451.

- (3) R.E. Lucas Jr, Expectations and the Neutrality of Money, Journal of Economic Theory 4 (2) (1972) 103-124.

- (4) M. King, Twenty years of inflation targeting (Speech), The Stamp Memorial Lecture, London School of Economics 9 October 2012.

- (5) S. Fischer, R.E. Hall, and J.B. Taylor, Relative shocks, relative price variability, and inflation, Brookings Papers on Economic Activity 1981.2 (1981) 381-441.

- (6) T.F. Cooley and G.D. Hansen, The inflation tax in a real business cycle model, American Economic Review 79 (4) (1989) 733-748.

- (7) J.B. Taylor, Aggregate dynamics and staggered contracts, Journal of Political Economy 88 (1) (1980) 1-23.

- (8) D. Heymann and A. Leijonhufvud, High Inflation: The Arne Ryde Memorial Lectures, Clarendon Press, Oxford (England), 1995.

- (9) R.E. Lucas Jr, Econometric policy evaluation: A critique, in: Karl Brunner and Allan H. Meltzer (Eds), The Phillips Curve and Labor Market vol 1 of Carnegie-Rochester Conference Series on Public Policy, North-Holland, Amsterdam, 1976.

- (10) R.N. Mantegna and E. Stanley, An Introduction to Econophysics: Correlations and Complexity in Finance, Cambridge University Press, Cambridge, England, 1999.

- (11) S. Moss de Oliveira, P.M.C. de Oliveira, and D. Stauffer, Evolution, Money, War and Computers, Teubner, Stuttgart-Leipzig, 1999.

- (12) D. Sornette, Why Stock Markets Crash (Critical Events in Complex Financial Systems), Princeton University Press, Princeton, 2003.

- (13) P. Cagan, The monetary dynamics of hyperinflation, in: M. Friedman(Ed.), Studies in the Quantity Theory of Money, University of Chicago Press, Chicago, 1956.

- (14) T. Mizuno, M. Takayasu, and H. Takayasu, The mechanism of double-exponential growth in hyperinflation, Physica A 308 (2002) 411-419.

- (15) D. Sornette, H. Takayasu, and W.-X. Zhou, Finite-time singularity signature of hyperinflation, Physica A 325 (2003) 492-506.

- (16) M.A. Szybisz and L. Szybisz, Finite-time singularity in the evolution of hyperinflation episodes, http://arxiv.org/abs/0802.3553.

- (17) M.A. Szybisz and L. Szybisz, Finite-time singularities in the dynamics of hyperinflation in an economy, Phys. Rev. B 80 (2009) 026116/1-11.

- (18) L. Szybisz and M.A. Szybisz, People’s collective behavior in a hyperinflation, Advances Applic. Stat. Sciences 2 (2010) 315-331.

- (19) L. Szybisz and M.A. Szybisz, Universality of the behavior at the final stage of hyperinflation episodes in economy, Anales AFA 26 (2015) 142-147.

- (20) M.A. Szybisz and L. Szybisz, Hyperinflation in Brazil, Israel, and Nicaragua revisited, http://arxiv.org/abs/1601.00092.

- (21) R. Cooper, Coordination games: Complementarities and Macroeconomics, Cambridge University Press, Cambridge, 1999.

- (22) P.A. Diamond, Aggregate demand management in search equilibrium, Journal of Political Economy 90 (1982) 881-894.

- (23) M. Bruno and S. Fisher, Seigniorage, operating rules and the high inflation trap, National Bureau of Economic Research Cambridge, Mass., USA, 1987.

- (24) M. Obstfeld, Models of currency crises with self-fulfilling features, European Economic Review 40 (3) (1996) 1037-1047.

- (25) P. Krugman, Balance sheets, the transfer problem, and financial crises, in: International finance and financial crises, Springer Netherlands, 1999. (pp. 31-55)

- (26) S. Morris and H.S. Shin, Rethinking multiple equilibria in macroeconomic modeling, in: NBER Macroeconomics Annual, B.S. Bernanke and K. Rogoff (Eds.), MIT Press, Massachusetts, 2000. Vol 15 pp. 139-181.

- (27) J-P. Nadal, D. Phan, M.B. Gordon, and J. Vannimenus, Multiple equilibria in monopoly market with heterogeneous agents and externalities, Quantitative Finance 5 (2005) 557-568.

- (28) S. Flügge, Practical quantum mechanics, Springer, Berlin, 1971.

- (29) M. Abramowitz and I.A. Stegun, Handbook of mathematical functions, Dover, New York, 1972.

- (30) B. Paal, Measuring the Inflation of Parallel Currencies: An Empirical Reevaluation of the Second Hungarian Hyperinflation, Stanford Institute for Economic Policy Research, Discussion Paper No. 00-01, June 2000.

- (31) P.Z. Grossman and J. Horváth, The Dynamics of the Hungarian Hyperinflation, 1945-6: A New Perspective, Scholarship and Professional Work - Business, Paper 29, 2000.

- (32) P.R. Bevington, Data Reduction and Error Analysis for the Physical Sciences, McGraw Hill, New York, 1969.

- (33) W.H. Press, S.A. Teukolsky, W.T. Vetterling, and B.P. Flannery, Numerical Recipes in Fortran 77, Cambridge University Press, Cambridge, 1996.

- (34) Table of the International Monetary Fund, http://www.imf.org/external/pubs/ft/weo/2002/01/data/index.htm.

- (35) L. Leiderman and N. Liviatan, The 1985 stabilization from the perspective of the 1990’s, Israel Economic Review 1 (1) (2003) 103-131.

- (36) L. Rojas-Suárez, From the Debt Crisis Toward Economic Stability: An Analysis of the Consistency of Macroeconomic Policies in Mexico, International Monetary Fund, Working Paper No. 17, 1992.

- (37) T. Goodman, The Economy, in: Mexico a country study, T.L. Merrill and R. Miro (Eds.), Federal Research Division, Library of Congress, 1997. Chapter 3, pp. 141-228.

- (38) R. Bergoeing, P.J. Kehoe, T.J. Kehoe, and R. Soto, A decade Lost and Found: Mexico and Chile in the 1980’s, Federal Reserve Bank of Minneapolis, 2007.

- (39) Federal Reserve Bank of St. Louis, https://research.stlouisfed.org/fred2/series/

- (40) P.S. Andersen and M. Guðmundsson, Inflation and disinflation in Iceland, Bank for International Settlements, Working Papers No. 52, Basel, Switzerland, 1998.