On Asymptotic Inference in Stochastic Differential Equations with Time-Varying Covariates

Abstract

In this article, we introduce a system of stochastic differential equations (s) consisting of time-dependent covariates and consider both fixed and random effects set-ups. We also

allow the functional part associated with the drift function to depend upon unknown parameters. In this general set-up of SDE system we establish consistency and asymptotic normality of the

M LE through verification of the regularity conditions required by existing relevant theorems. Besides, we consider the Bayesian approach to learning about the population parameters, and prove

consistency and asymptotic normality of the corresponding posterior distribution. We supplement our theoretical investigation with simulated and real data analyses, obtaining encouraging results

in each case.

Keywords:

Asymptotic normality; Functional data; Gibbs sampling; Maximum likelihood estimator; Posterior consistency; Random effects.

1 Introduction

Systems of stochastic differential equations (s) are appropriate for modeling situations where “within” subject variability is caused by some random component varying continuously in time; hence, systems are also appropriate for modeling functional data (see, for example, Zhu et al. (2011), Ramsay and Silverman (2005) for some connections between and functional data analysis). When suitable time-varying covariates are available, it is then appropriate to incorporate such information in the system. Some examples of statistical applications of -based models with time-dependent covariates are Oravecz et al. (2011), Overgaard et al. (2005), Leander et al. (2015).

However, systems of based models consisting of time-varying covariates seem to be rare in the statistical literature, in spite of their importance, and their asymptotic properties are hitherto unexplored. Indeed, although asymptotic inference in single, fixed effects models without covariates has been considered in the literature as time tends to infinity (see, for example, Bishwal (2008)), asymptotic theory in systems of models is rare, and so far only random effects systems without covariates have been considered, as , the number of subjects (equivalently, the number of s in the system), tends to infinity (Delattre et al. (2013), Maitra and Bhattacharya (2016c), Maitra and Bhattacharya (2015)). Such models are of the following form:

| (1.1) |

where, for , is the initial value of the stochastic process , which is assumed to be continuously observed on the time interval ; assumed to be known. The function , which is the drift function, is a known, real-valued function on ( is the real line and is the dimension), and the function is the known diffusion coefficient. The s given by (1.1) are driven by independent standard Wiener processes , and , which are to be interpreted as the random effect parameters associated with the individuals, which are assumed by Delattre et al. (2013) to be independent of the Brownian motions and independently and identically distributed () random variables with some common distribution.

For the sake of convenience Delattre et al. (2013) (see also Maitra and Bhattacharya (2016c) and Maitra and Bhattacharya (2015)) assume . Thus, the random effect is a multiplicative factor of the drift function; also, the function is assumed to be independent of parameters. In this article, we generalize the multiplicative factor to include time-dependent covariates; we also allow to depend upon unknown parameters.

Notably, such model extension has already been provided in Maitra and Bhattacharya (2016a) and Maitra and Bhattacharya (2016b), but their goal was to develop asymptotic theory of Bayes factors for comparing systems of s, with or without time-varying covariates, emphasizing, when time-varying covariates are present, simultaneous asymptotic selection of covariates and part of the drift function free of covariates, using Bayes factors.

In this work, we deal with parametric asymptotic inference, both frequentist and Bayesian, in the context of our extended system of s. We consider, separately, fixed effects as well as random effects. The fixed effects set-up ensues when coefficients associated with the covariates are the same for all the subjects. On the other hand, in the random effects set-up, the subject-wise coefficients are assumed to be a random sample from some distribution with unknown parameters.

It is also important to distinguish between the situation and the independent but non-identical case (we refer to the latter as non-) that we consider. The set-up is concerned with the case where the initial values and time limit are the same for all , and the coefficients associated with the covariates are zero, that is, there are no covariates suitable for the -based system. This set-up, however, does not reduce to the set-up considered in Delattre et al. (2013), Maitra and Bhattacharya (2016c) and Maitra and Bhattacharya (2015) because in the latter works was assumed to be free of parameters, while in this work we allow this function to be dependent on unknown parameters. The non- set-up assumes either or both of the following: presence of appropriate covariates and that and are not the same for all the subjects.

In the classical paradigm, we investigate consistency and asymptotic normality of the maximum likelihood estimator () of the unknown parameters which we denote by , and in the Bayesian framework we study consistency and asymptotic normality of the Bayesian posterior distribution of . In other words, we consider prior distributions of and study the properties of the corresponding posterior

| (1.2) |

as the sample size tends to infinity. Here is the density corresponding to the -th individual and is the parameter space.

In what follows, after introducing our model and the associated likelihood in Section 2, we investigate asymptotic properties of in the and non- contexts in Sections 3 and 4 respectively. Then, in Sections 5 and 6 we investigate asymptotic properties of the posterior in the and non- cases, respectively. In Section 7 we consider the random effects set-up and provide necessary discussion to point towards validity of the corresponding asymptotic results. We demonstrate the applicability of our developments to practical and finite-sample contexts using simulated and real data analyses in Sections 8 and 9, respectively. We summarize our contribution and provide further discussion in Section 10.

Notationally, “”, “” and “” denote convergence “almost surely”, “in probability” and “in distribution”, respectively.

2 The set-up

We consider the following system of models for :

| (2.1) |

where is the initial value of the stochastic process , which is assumed to be continuously observed on the time interval ; for all and assumed to be known. In the above, is the parametric function consisting of the covariates and the unknown coefficients associated with the covariates, and is a parametric function known up to the parameters .

2.1 Incorporation of time-varying covariates

We assume that has the following form:

| (2.2) |

where is a set of real constants and is the set of available covariate information corresponding to the -th individual, depending upon time . We assume that is continuous in , where is compact and is continuous, for . Let . We let

Hence, for all . The function is multiplicative part of the drift function free of the covariates. Note that consists of parameters. Assuming that , where , it follows that our parameter set belongs to the -dimensional real space . The true parameter set is denoted by .

2.2 Likelihood

We first define the following quantities:

| (2.3) |

for .

3 Consistency and asymptotic normality of in the set-up

In the set up we have and for all . Moreover, the covariates are absent, that is, for Hence, the resulting parameter set in this case is

3.1 Strong consistency of

Consistency of the under the set-up can be verified by validating the regularity conditions of the following theorem (Theorems 7.49 and 7.54 of Schervish (1995)); for our purpose we present the version for compact parameter space.

Theorem 1 (Schervish (1995))

Let be conditionally given with density with respect to a measure on a space . Fix , and define, for each and ,

Assume that for each , there is an open set such that and that . Also assume that is continuous at for every , a.s. . Then, if is the of corresponding to observations, it holds that , a.s. .

3.1.1 Assumptions

We assume the following conditions:

-

(H1)

The parameter space such that and are compact.

-

(H2)

and are (differentiable with continuous first derivative) on and satisfy and for all , for some . Now, due to (H1) the latter boils down to assuming and for all , for some .

We further assume:

-

(H3)

For every , let be continuous in and moreover, for ,

for some and .

-

(H4)

(3.1) where is continuous in .

3.1.2 Verification of strong consistency of in our set-up

To verify the conditions of Theorem 1 in our case, note that assumptions (H1) – (H4) clearly imply continuity of the density in the same way as the proof of Proposition 2 of Delattre et al. (2013). It follows that and are continuous in , the property that we use in our proceedings below.

Now consider,

| (3.2) |

where is an appropriate open subset of the relevant compact parameter space, and is a closed subset of . The infimum of is attained at due to continuity of and in .

Let and . From Theorem 5 of Maitra and Bhattacharya (2016c) it follows that the above expectations are continuous in . Using this we obtain

| (3.3) |

where is where the supremum of is achieved. Since is independent of , the last step (3.3) follows.

Noting that and are finite due to Lemma 1 of Maitra and Bhattacharya (2016a), it follows that . Hence, , as . We summarize the result in the form of the following theorem:

Theorem 2

Assume the setup and conditions (H1) – (H4). Then the is strongly consistent in the sense that as , .

3.2 Asymptotic normality of

To verify asymptotic normality of we invoke the following theorem provided in Schervish (1995) (Theorem 7.63):

Theorem 3 (Schervish (1995))

Let be a subset of , and let be conditionally given each with density . Let be an . Assume that under for all . Assume that has continuous second partial derivatives with respect to and that differentiation can be passed under the integral sign. Assume that there exists such that, for each and each ,

| (3.4) |

with

| (3.5) |

Assume that the Fisher information matrix is finite and non-singular. Then, under ,

| (3.6) |

3.2.1 Assumptions

Along with the assumptions (H1) – (H4), we further assume the following:

-

(H5)

The true value .

-

(H6)

The Fisher’s information matrix is finite and non-singular, for all .

-

(H7)

Letting for ; for , and for , there exist constants such that for each combination of , for any , for all ,

3.2.2 Verification of the above regularity conditions for asymptotic normality in our set-up

In Section 3.1.2 almost sure consistency of the has been established. Hence, under for all . With assumptions (H1)–(H4), (H7), Theorem B.4 of Rao (2013) and the dominated convergence theorem, interchangability of differentiation and integration in case of stochastic integration and usual integration respectively can be assured, from which it can be easily deduced that differentiation can be passed under the integral sign, as required by Theorem 3. With the same arguments, it follows that in our case is differentiable in , and the derivative has finite expectation due to compactness of the parameter space and (H7). Hence, (3.4) and (3.5) clearly hold.

In other words, asymptotic normality of the , of the form (3.6), holds in our case. Formally,

Theorem 4

Assume the setup and conditions (H1) – (H7). Then, as , the is asymptotically normally distributed as (3.6).

4 Consistency and asymptotic normality of in the non- set-up

We now consider the case where the processes , are independently, but not identically distributed. In this case, where at least one of the coefficients is non-zero, guaranteeing the presence of at least one time-varying covariate. Hence, in this set-up .

Moreover, following Maitra and Bhattacharya (2016c), Maitra and Bhattacharya (2015) we allow the initial values and the time limits to be different for , but assume that the sequences and are sequences entirely contained in compact sets and , respectively. Compactness ensures that there exist convergent subsequences with limits in and ; for notational convenience, we continue to denote the convergent subsequences as and . Thus, let the limts be and .

Henceforth, we denote the process associated with the initial value and time point as and so for and , we let

| (4.1) | ||||

| (4.2) |

Clearly, and , where and are given by (2.3). In this non- set-up we assume, following Maitra and Bhattacharya (2016a), that

-

(H8)

For , and for ,

(4.3) and, for ; ,

(4.4) as , where are real constants.

For , and , we denote the Kullback-Leibler distance and the Fisher’s information as () and , respectively. Then the following results hold in the same way as Lemma 11 of Maitra and Bhattacharya (2016a).

Lemma 5

Assume the non- set-up, (H1) – (H4) and (H8). Then for any ,

| (4.5) | ||||

| (4.6) | ||||

| (4.7) |

where the limits , and are well-defined Kullback-Leibler divergences and Fisher’s information, respectively.

Lemma 5 will be useful in our asymptotic investigation in the non- set-up. In this set-up, we first investigate consistency and asymptotic normality of using the results of Hoadley (1971).

4.1 Consistency and asymptotic normality of in the non- set-up

Following Hoadley (1971) we define the following:

| (4.8) |

| (4.9) | ||||

| (4.10) |

Following Hoadley (1971) we denote by , and to be expectations of , and under ; for any sequence we denote by .

Hoadley (1971) proved that if the following regularity conditions are satisfied, then the MLE :

-

(1)

is a closed subset of .

-

(2)

is an upper semicontinuous function of , uniformly in , a.s. .

-

(3)

There exist , and for which

-

(i)

;

-

(ii)

.

-

(i)

-

(4)

-

(i)

;

-

(ii)

.

-

(i)

-

(5)

and are measurable functions of .

Actually, conditions (3) and (4) can be weakened but these are more easily applicable (see Hoadley (1971) for details).

4.1.1 Verification of the regularity conditions

Since is compact in our case, the first regularity condition clearly holds.

For the second regularity condition, note that given , is continuous by our assumptions (H1) – (H4), as already noted in Section 3.1.2; in fact, uniformly continuous in in our case, since is compact. Hence, for any given , there exists , independent of , such that implies . Now consider a strictly positive function , continuous in and , such that . Let . Since and are compact, it follows that . Now it holds that implies , for all . Hence, the second regularity condition is satisfied.

Let us now focus attention on condition (3)(i).

| (4.11) |

Let us denote by . Here , and is so small that for all . It then follows from (4.11) that

| (4.12) |

The supremums in (4.12) are finite due to compactness of . Let the supremum be attained at some where Then, the expectation of the square of the upper bound can be calculated in the same way as (3.3) noting that in this case will be . Since under , finiteness of moments of all orders of each term in the upper bound is ensured by Lemma 10 of Maitra and Bhattacharya (2016a), it follows that

| (4.13) |

where , with being a continuous function of , continuity being again a consequence of Lemma 10 of Maitra and Bhattacharya (2016a). Since because of compactness of , and ,

regularity condition (3)(i) follows.

To verify condition (3)(ii), first note that we can choose such that and . It then follows that for every . The right hand side is bounded by the same expression as the right hand side of (4.12), with only replaced with . The rest of the verification follows in the same way as verification of (3)(i).

Verification of (4)(ii) follows exactly in a similar way as verified in Maitra and Bhattacharya (2016c) except that the concerned moment existence result follows from Lemma 10 of Maitra and Bhattacharya (2016a). Regularity condition (5) is seen to hold by the same arguments as in Maitra and Bhattacharya (2016c).

In other words, in the non- framework, the following theorem holds:

Theorem 6

Assume the non- setup and conditions (H1) – (H4) and (H8). Then it holds that , as .

4.2 Asymptotic normality of in the non- set-up

Let ; also, let be the vector with -th component , and let be the matrix with -th element .

For proving asymptotic normality in the non- framework, Hoadley (1971) assumed the following regularity conditions:

-

(1)

is an open subset of .

-

(2)

.

-

(3)

and exist a.s. .

-

(4)

is a continuous function of , uniformly in , a.s. , and is a measurable function of .

-

(5)

for .

-

(6)

, where for any vector , denotes the transpose of .

-

(7)

as and is positive definite.

-

(8)

, for some .

-

(9)

There exist and random variables such that

-

(i)

.

-

(ii)

, for some .

-

(i)

Condition (8) can be weakened but is relatively easy to handle. Under the above regularity conditions, Hoadley (1971) prove that

| (4.15) |

4.2.1 Validation of asymptotic normality of in the non- set-up

Condition (1) holds also for compact ; see Maitra and Bhattacharya (2016c). Condition (2) is a simple consequence of Theorem 6.

Conditions (3), (5) and (6) are clearly valid in our case because of interchangability of differentiation and integration, which follows due to (H1) – (H4), (H7) and Theorem B.4 of Rao (2013). Condition (4) can be verified in exactly the same way as condition (2) of Section 4.1 is verified; measurability of follows due to its continuity with respect to . Condition (7) simply follows from (4.7). Compactness, continuity, and finiteness of moments guaranteed by Lemma 10 of Maitra and Bhattacharya (2016a) imply conditions (8), (9)(i) and 9(ii).

In other words, in our non- case we have the following theorem on asymptotic normality.

Theorem 7

Assume the non- setup and conditions (H1) – (H8). Then (4.15) holds, as .

5 Consistency and asymptotic normality of the Bayesian posterior in the set-up

5.1 Consistency of the Bayesian posterior distribution

As in Maitra and Bhattacharya (2015) here we exploit Theorem 7.80 presented in Schervish (1995), stated below, to show posterior consistency.

Theorem 8 (Schervish (1995))

Let be conditionally given with density with respect to a measure on a space . Fix , and define, for each and ,

Assume that for each , there is an open set such that and that . Also assume that is continuous at for every , a.s. . For , define , where

| (5.1) |

is the Kullback-Leibler divergence measure associated with observation . Let be a prior distribution such that , for every . Then, for every and open set containing , the posterior satisfies

| (5.2) |

5.1.1 Verification of posterior consistency

The condition of the above theorem is verified in the context of Theorem 1 in Section 3.1.2. Continuity of the Kullback-Liebler divergence follows easily from Lemma 10 of Maitra and Bhattacharya (2016a). The rest of the verification is the same as that of Maitra and Bhattacharya (2015).

Hence, (5.2) holds in our case with any prior with positive, continuous density with respect to the Lebesgue measure. We summarize this result in the form of a theorem, stated below.

Theorem 9

Assume the set-up and conditions (H1) – (H4). Let the prior distribution of the parameter satisfy almost everywhere on , where is any positive, continuous density on with respect to the Lebesgue measure . Then the posterior (1.2) is consistent in the sense that for every and open set containing , the posterior satisfies

| (5.3) |

5.2 Asymptotic normality of the Bayesian posterior distribution

As in Maitra and Bhattacharya (2015), we make use of Theorem 7.102 in conjunction with Theorem 7.89 provided in Schervish (1995). These theorems make use of seven regularity conditions, of which only the first four, stated below, will be required for the set-up.

5.2.1 Regularity conditions – case

-

(1)

The parameter space is .

-

(2)

is a point interior to .

-

(3)

The prior distribution of has a density with respect to Lebesgue measure that is positive and continuous at .

-

(4)

There exists a neighborhood of on which is twice continuously differentiable with respect to all co-ordinates of , .

Before proceeding to justify asymptotic normality of our posterior, we furnish the relevant theorem below (Theorem 7.102 of Schervish (1995)).

Theorem 10 (Schervish (1995))

Let be conditionally given . Assume the above four regularity conditions; also assume that there exists such that, for each and each ,

| (5.4) |

with

| (5.5) |

Further suppose that the conditions of Theorem 8 hold, and that the Fisher’s information matrix is positive definite. Now denoting by the associated with observations, let

| (5.6) |

where for any ,

| (5.7) |

and is the identity matrix of order . Thus, is the observed Fisher’s information matrix.

Letting , it follows that for each compact subset of and each , it holds that

| (5.8) |

where denotes the density of the standard normal distribution.

5.2.2 Verification of posterior normality

Observe that the four regularity conditions of Section 5.2.1 trivially hold. The remaining conditions of Theorem 10 are verified in the context of Theorem 3 in Section 3.2.2. We summarize this result in the form of the following theorem.

Theorem 11

Assume the set-up and conditions (H1) – (H7). Let the prior distribution of the parameter satisfy almost everywhere on , where is any density with respect to the Lebesgue measure which is positive and continuous at . Then, letting , it follows that for each compact subset of and each , it holds that

| (5.9) |

6 Consistency and asymptotic normality of the Bayesian posterior in the non- set-up

For consistency and asymptotic normality in the non- Bayesian framework we utilize the result presented in Choi and Schervish (2007) and Theorem 7.89 of Schervish (1995), respectively.

6.1 Posterior consistency in the non- set-up

We consider the following extra assumption for our purpose.

-

(H9)

There exist strictly positive functions and continuous in , such that for any ,

and

Now, let

| (6.1) |

| (6.2) |

and

| (6.3) |

where .

Compactness ensures that , so that . It also holds due to compactness that for ,

| (6.4) |

and

| (6.5) |

This choice of ensuring (6.4) and (6.5) will be useful in verification of the conditions of Theorem 12, which we next state.

Theorem 12 (Choi and Schervish (2007))

Let be independently distributed with densities , with respect to a common -finite measure, where , a measurable space. The densities are assumed to be jointly measurable. Let and let be the joint distribution of when is the true value of . Let be a sequence of subsets of . Let have prior on . Define the following:

Make the following assumptions:

-

(1)

Suppose that there exists a set with such that

-

(i)

,

-

(ii)

For all , .

-

(i)

-

(2)

Suppose that there exist test functions , sets and constants such that

-

(i)

,

-

(ii)

,

-

(iii)

.

-

(i)

Then,

| (6.6) |

6.1.1 Validation of posterior consistency

First note that, is given by (2.4). From the proof of Theorem 6, using finiteness of moments of all orders associated with and , it follows that has an upper bound which has finite first and second order moments under , and is uniform for all , where is any compact subset of . Hence, for each , is finite. Using compactness, Lemma 10 of Maitra and Bhattacharya (2016a) and arguments similar to that of Section 3.1.1 of Maitra and Bhattacharya (2015), it easily follows that , for some , uniformly in . Hence, choosing a prior that gives positive probability to the set , it follows that for all ,

Hence, condition (1)(i) holds. Also note that (1)(ii) can be verified similarly as the verification of Theorem 5 of Maitra and Bhattacharya (2015).

We now verify conditions (2)(i), (2)(ii) and (2)(iii). We let , where , where . Note that

| (6.7) |

so that (2)(iii) holds, assuming that the prior is such that the expectation is finite.

The verification of 2(i) can be checked in as in Maitra and Bhattacharya (2015) except the relevant changes. So, here we only mention the corresponding changes, skipping detailed verification.

Kolmogorov’s strong law of large numbers for the non- case (see, for example, Serfling (1980)), holds in our problem due to finiteness of the moments of and for every , , and belonging to the respective compact spaces. Moreover, existence and boundedness of the third order derivative of with respect to its components is ensured by assumption (H7) along with compactness assumptions. The results stated in Maitra and Bhattacharya (2016a) concerned with continuity and finiteness of the moments of and for every , , and belonging to their respective compact spaces are needed here. The lower bound of is denoted by where

The rest of the verification is same as that of Maitra and Bhattacharya (2015) along with assumption (H9).

To verify condition 2(ii) we define , where , defined as in (4.6), is the proper Kullback-Leibler divergence. This verification is again similar to that of Maitra and Bhattacharya (2015). The result can be summarized in the form of the following theorem.

Theorem 13

Assume the non- set-up. Also assume conditions (H1) – (H9). For any , let , where , defined as in (4.6), is the proper Kullback-Leibler divergence. Let the prior distribution of the parameter satisfy almost everywhere on , where is any positive, continuous density on with respect to the Lebesgue measure . Then, as ,

| (6.8) |

6.2 Asymptotic normality of the posterior distribution in the non- set-up

Below we present the three regularity conditions that are needed in the non- set-up in addition to the four conditions already stated in Section 5.2.1, for asymptotic normality given by (5.8).

6.2.1 Extra regularity conditions in the non- set-up

-

(5)

The largest eigenvalue of goes to zero in probability.

-

(6)

For , define to be the open ball of radius around . Let be the smallest eigenvalue of . If , there exists such that

(6.9) -

(7)

For each , there exists such that

(6.10)

Although intuitive explanations of all the seven conditions are provided in Schervish (1995), here we briefly touch upon condition (7), which is seemingly somewhat unwieldy. First note that condition (6) ensures consistency of the , so that , as . Thus, in (7), for sufficiently large and sufficiently small , , for all . Hence, from the definition of given by (5.6), it follows that so that, since , , for all and for large enough . Now it is easy to see that the role of condition (7) is only to formalize the heuristic arguments.

6.2.2 Verification of the regularity conditions

Assumptions (H1) – (H9), along with Kolmogorov’s strong law of large numbers, are sufficient for the regularity conditions to hold; the arguments remain similar as those in Section 3.2.2 of Maitra and Bhattacharya (2015). We provide our result in the form of the following theorem.

Theorem 14

Assume the non- set-up and conditions (H1) – (H9). Let the prior distribution of the parameter satisfy almost everywhere on , where is any density with respect to the Lebesgue measure which is positive and continuous at . Then, letting , for each compact subset of and each , the following holds:

| (6.11) |

7 Random effects model

We now consider the following system of models for :

| (7.1) |

Note that this model is the same as described in Section 2 except that the parameters now depend upon . Indeed, now is given by

| (7.2) |

where is the random effect corresponding to the -th individual for , and is the same as in Section 2.1. We let . Note that our likelihood is the product over , of the following individual densities:

where

Now, let be a function from where and ; . With this notation, the likelihood can be re-written as the product over , of the following:

| (7.3) |

where

| (7.4) |

and

| (7.5) |

are random vectors and positive definite random matrices respectively.

We assume that are Gaussian vectors, with expectation vector and covariance matrix where is the set of real positive definite symmetric matrices of order . The parameter set is denoted by .

To obtain the likelihood involving we refer to the multidimensional random effects set-up of Delattre et al. (2013). Following Lemma 2 of Delattre et al. (2013) it then follows in our case that, for each and for all , are invertible.

Setting we obtain

| (7.6) |

as our desired likelihood after integrating (7.3) with respect to the distrbution of .

With reference to Delattre et al. (2013) in our case

Hence, Proposition (10)(i) of Delattre et al. (2013) can be seen to be hold here in a similar way by replacing and by and respectively.

Asymptotic investigation regarding consistency and asymptotic normality of and Bayesian posterior consistency and asymptotic posterior normality in both and non- set-ups can be established as in the one dimensional cases in Maitra and Bhattacharya (2016c) and Maitra and Bhattacharya (2015) with proper multivariate modifications by replacing and with and respectively, and exploiting assumptions (H1) – (H9).

8 Simulation studies

We now supplement our asymptotic theory with simulation studies where the data is generated from a specific system of s with one covariate, with given values of the parameters. Specifically, in the classical case, we obtain the distribution of the s using parametric bootstrap, along with the 95% confidence intervals of the parameters. We demonstrate in particular that the true values of the parameters are well-captured by the respective 95% confidence intervals. In the Bayesian counterpart, we obtain the posterior distributions of the parameters along with the respective 95% credible intervals, and show that the true values fall well within the respective 95% credible intervals.

8.1 Distribution of when

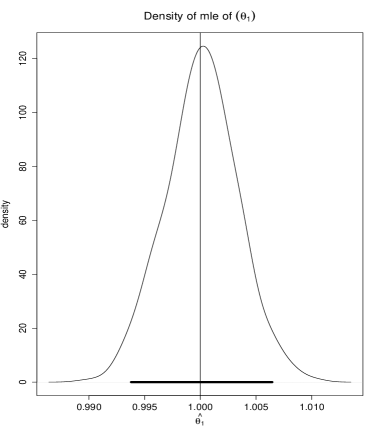

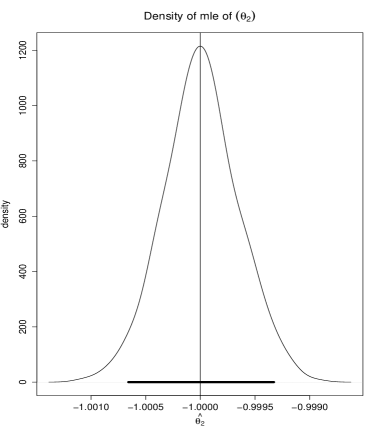

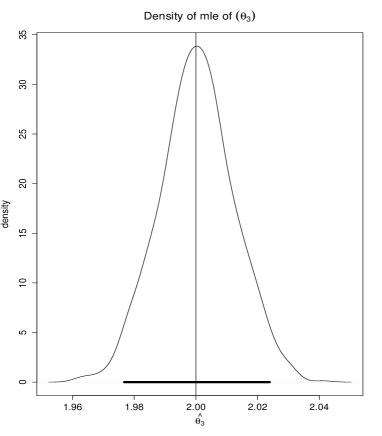

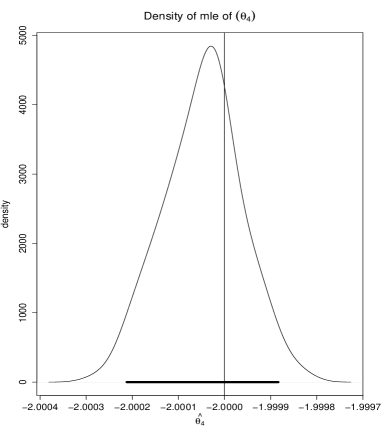

To demonstrate the finite sample analogue of asymptotic distribution of as , we consider individuals, where the -th one is modeled by

| (8.1) |

for . We fix our diffusion coefficient as . We consider the initial value and the time interval with . Further, we choose the true values as .

We assume that the time dependent covariates satisfy the following

| (8.2) |

for , where the coeffiicients for . After simulating the covariates using the system of s (8.2), we generate the data using the system of s (8.1). In both the cases we discretize the time interval into equispaced time points.

The distributions of the s of the four parameters are obtained through the parametric bootstrap method. In this method we simulated the data 1000 times by simulating as many paths of the Brownian motion, where each data set consists of 20 individuals. Under each data set we perform the “block-relaxation” method (see, for example, Lange (2010) and the references therein) to obtain the . In a nutshell, starting with some sensible initial value belonging to the parameter space, the block-relaxation method iteratively maximizes the optimizing function (here, the log-likelihood), successively, with respect to one parameter, fixing the others at their current values, until convergence is attained with respect to the iterations. Details follow.

For the initial values of the for , required to begin the block-relaxation method, we simulate four variates independently, and set them as the initial values ; . Denoting by the value of at the -th iteration, for , and letting be the likelihood, the block-relaxation method consists of the following steps:

-

(1)

At the -th iteration, for , obtain by solving the equation , conditionally on Let .

-

(2)

Letting denote the Euclidean norm, if , set , where stands for the maximum likelihood estimator of .

-

(3)

If, on the other hand, , increase to and continue steps (1) and (2).

Once we obtain the by the above block-relaxation algorithm, we then plug-in in (8.1) and generate data sets from the resulting system of s, and apply the block-relaxation algorithm to each such data set to obtain the associated with the data sets. Thus, we obtain the distribution of the using the parametric bootstrap method.

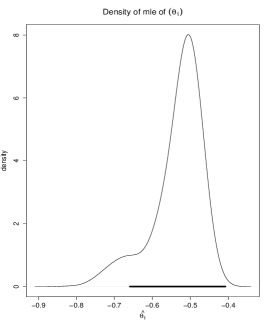

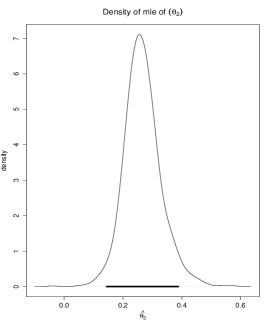

The distributions of the components of (denoted by for ) are shown in Figure 8.1, where the associated confidence intervals are shown in bold lines. As exhibited by the figures, the 95% confidence intervals clearly contain the true values of the respective components of .

8.2 Posterior distribution of the parameters when

We now consider simulation study for the Bayesian counterpart, using the same data set simulated from the system of s given by (8.1), with same covariates simulated from (8.2). We consider an empirical Bayes prior based on the such that for , independently, where is the of and is such that the length of the 95% confidence interval associated with the distribution of the , after adding one unit to both lower and upper ends of the interval, is the same as the length of the 95% prior credible interval . In other words, we select such that the length of the corresponding 95% prior credible interval is the same as that of the enlarged 95% confidence interval associated with the distribution of the corresponding .

To simulate from the posterior distribution of , we perform approximate Bayesian computation (ABC) (Tavaŕe et al. (1997), Beaumont et al. (2002), Marjoram et al. (2003)), since the standard Markov chain Monte Carlo (MCMC) based simulation techniques, such as Gibbs sampling and Metropolis-Hastings algorithms (see, for example, Robert and Casella (2004), Brooks et al. (2011)) failed to ensure good mixing behaviour of the underlying Markov chains. Denoting the true data set by , our method of ABC is described by following steps.

-

(1)

For , we simulate the parameters from their respective prior distributions.

-

(2)

With the obtained values of the parameters we simulate the new data, which we denote by , using the system of s (8.1).

-

(3)

We calculate the average Euclidean distance between and and denote it by .

-

(4)

Until , we repeat steps (1)–(3).

-

(5)

Once , we set the corresponding as a realization from the posterior of with approximation error .

-

(6)

We obtain posterior realizations of by repeating steps (1)–(5).

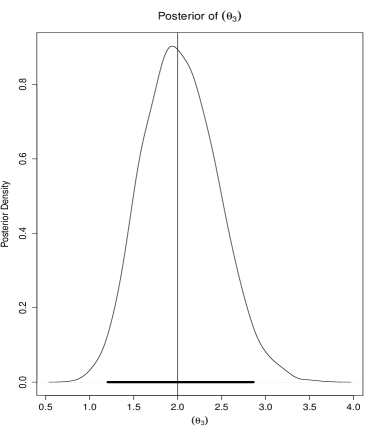

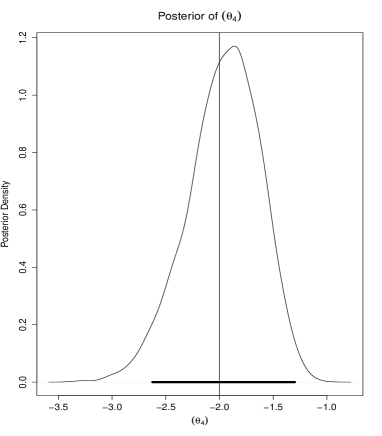

Figure 8.2 shows the posterior distribution of the parameters , for , where the posterior credible intervals are shown in bold lines. Observe that all the true values of ; , fall comfortably within the respective 95% posterior credible intervals.

9 Application to real data

We now consider application of our system consisting of covariates to a real, stock market data ( observations from August , 2013, to June , 2015) for companies. The data are available at www.nseindia.com.

Each company-wise data is modeled by the availabe standard financial models with the “fitsde” package in . The minimum value of BIC (Bayesian Information Criterion) is found corresponding to the (Chan, Karolyi, Longstaff and Sander; see Chan et al. (1992)) model. Denoting the data by , the model is described by

In our application we treat the diffusion coefficient as a fixed quantity. So, we fix the values of and as obtained by the “fitsde” function, We denote , .

We consider the “close price” of each company as our data . IIP general index, bank interest rate and US dollar exchange rate are considered as time dependent covariates which we incorporate in the model.

The three covariates are denoted by , respectively. Now, our considered system of models for national stock exchange data associated with the companies is the following:

| (9.1) |

for .

9.1 Distribution of

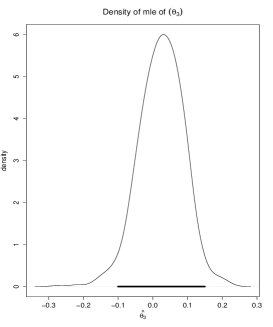

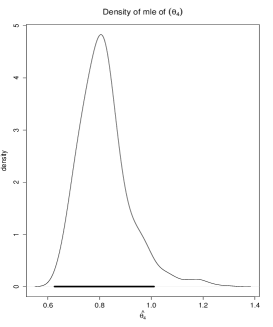

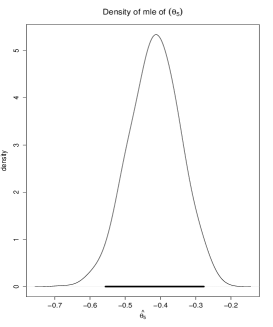

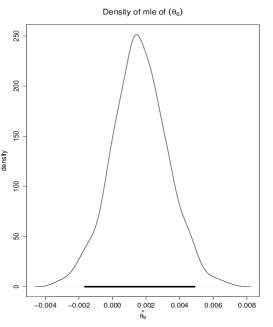

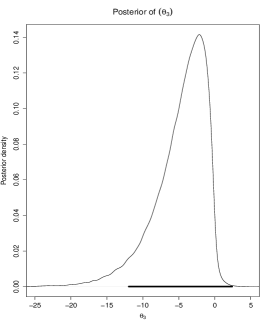

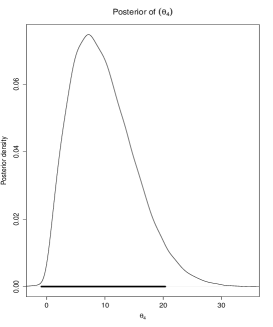

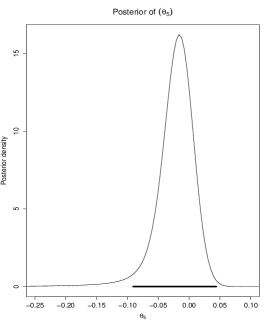

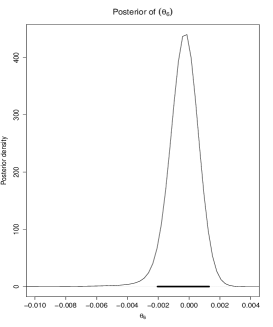

We first obtain the s of the parameters for by the block-relaxation algorithm described by Algorithm 1, in Section 8.1. In this real data set up, the process starts with the initial value for (our experiments with several other choices demonstrated practicability of those choices as well) and in step (3) of Algorithm 1, the distance is taken as instead of . Then taking the s as the value of the parameters for we perform the parametric bootstrap method where we generate the data 1000 times and with respect to each data set, obtain the s of the six parameters by the block-relaxation method as already mentioned. Figure 9.1 shows the distribution of s (denoted by for ) where the respective confidence intervals are shown in bold lines. Among the covariates, , that is, the US dollar exchange rate, seems to be less significant compared to the others, since the distribution of the of the associated coefficient, , has highest density around zero, with small variability, compared to the other coefficients. Also note that the distribution of is highly concentrated around zero, signifying that the term in the drift function of (9.1) is probably redundant.

9.2 Posterior Distribution of the parameters

In the Bayesian approach all the set up regarding the real data is exactly the same as in Section 9, that is, each data is driven by the s (9.1) where the covariates for are already mentioned in that section. In this case, we consider the priors for the parameters to be independent normal with mean zero and variance . Since in real data situations the parameters are associated with greater uncertainties compared to simulation studies, somewhat vague prior as we have chosen here, as opposed to that in the simulation study case, makes sense.

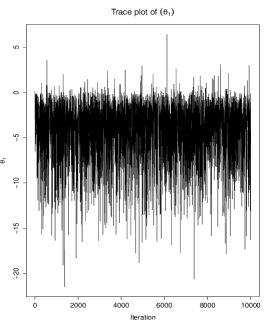

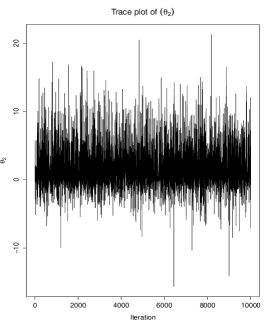

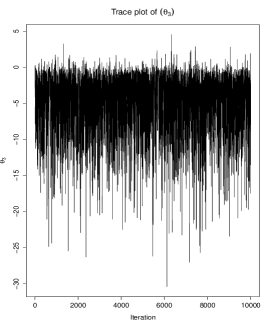

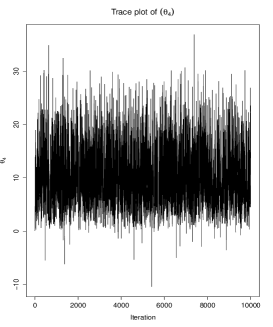

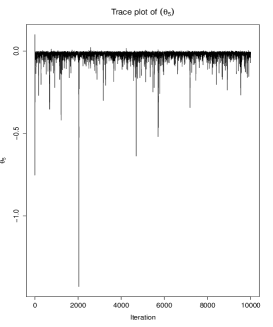

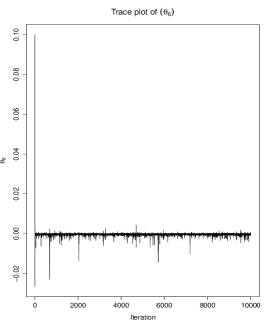

The greater uncertainty in the parameters in this real data scenario makes room for more movement, and hence, better mixing of MCMC samplers such as Gibbs sampling, in contrast with that in simulation studies. As such, our application of Gibbs sampling, were the full conditionals are normal distributions with appropriate means and variances, yielded excellent mixing. Although we chose the initial values as ; , other choices also turned out to be very much viable. We perform Gibbs sampling iterations to obtain our required posterior distributions of the parameters. Figure 9.2 shows the trace plots of the parameters associated with thinned samples obtained by plotting the output of every -th iteration. We emphasize that although we show the trace plots of only Gibbs sampling realizations to reduce the file size, our inference is based on all the realizations. From the trace plots, convergence of the posterior distributions of the parameters is clearly observed.

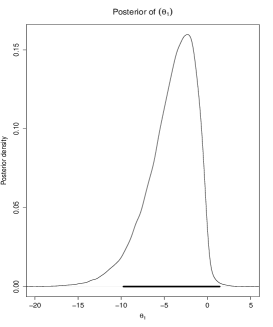

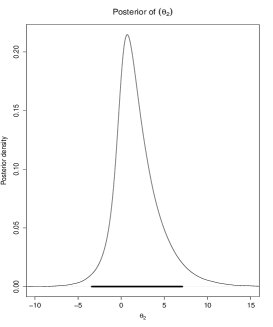

Figure 9.3 displays the posterior densities of the 6 parameters, where the credible intervals are indicated by bold lines. The posterior distribution of is seen to include zero in the highest density region; however, unlike the distribution of the , the posterior of has a long left tail, so that insignificance of is not very evident. The posterior of is highly concentrated around zero, agreeing with the of that the term in the drift function is perhaps redundant. Note that the posterior of also inclues zero in its high-density region, however, it has a long left tail, so that the significance of , and hence, of the overall drift function, is not ruled out.

10 Summary and conclusion

In based random effects model framework, Delattre et al. (2013) considered the linearity assumption in the drift function given by , assuming to be Gaussian random variables with mean and variance , and obtained a closed form expression of the likelihood of the above parameters. Assuming the set-up, they proved convergence in probability and asymptotic normality of the maximum likelihood estimator of the parameters.

Maitra and Bhattacharya (2016a) and Maitra and Bhattacharya (2016b) extended their model by incorporating time-varying covariates in and allowing to depend upon unknown parameters, but rather than inference regarding the parameters, they developed asymptotic model selection theory based on Bayes factors for their purposes. In this paper, we developed asymptotic theories for parametric inference for both classical and Bayesian paradigms under the fixed effects set-up, and provided relevant discussion of asymptotic inference on the parameters in the random effects set-up.

As our previous investigations (Maitra and Bhattacharya (2016c), Maitra and Bhattacharya (2015), for instance), in this work as well we distinguished the non- set-up from the case, the latter corresponding to the system of s with same initial values, time domain, but with no covariates. However, as already noted, this still provides a generalization to the set-up of Delattre et al. (2013) through generalization of to ; being a set of unknown parameters. Under suitable assumptions we obtained strong consistency and asymptotic normality of the under the set-up and weak consistency and asymptotic normality under the non- situation. Besides, we extended our classical asymptotic theory to the Bayesian framework, for both and non- situations. Specifically, we proved posterior consistency and asymptotic posterior normality, for both and non- set-ups.

In our knowledge, ours is the first-time effort regarding asymptotic inference, either classical or Bayesian, in systems of s under the presence of time-varying covariates. Our simulation studies and real data applications, with respect to both classical and Bayesian paradigms, have revealed very encouraging results, demonstrating the importance of our developments even in practical, finite-sample situations.

Acknowledgment

We are sincerely grateful to the EIC, the AE and the referee whose constructive comments have led to significant improvement of the quality and presentation of our manuscript. The first author also gratefully acknowledges her CSIR Fellowship, Govt. of India.

References

- Beaumont et al. (2002) Beaumont, M. A., Zhang, W., and Balding, D. J. (2002). Approximate Bayesian Computation in Population Genetics. Genetics, 162, 2025–2035.

- Bishwal (2008) Bishwal, J. P. N. (2008). Parameter Estimation in Stochastic Differential Equations. Lecture Notes in Mathematics, 1923, Springer-Verlag.

- Brooks et al. (2011) Brooks, S., Gelman, A., Jones, G. L., and Meng, X.-L. (2011). Handbook of Markov Chain Monte Carlo. Chapman and Hall, London.

- Chan et al. (1992) Chan, K. C., Karolyi, G. A., Longstaff, F. A., and Sanders, A. B. (1992). An Empirical Comparison of Alternative Models of the Short-Term Interest Rate. The Journal of Finance, 47, 1209–1227.

- Choi and Schervish (2007) Choi, T. and Schervish, M. J. (2007). On Posterior Consistency in Nonparametric Regression Problems. Journal of Multivariate Analysis, 98, 1969–1987.

- Delattre et al. (2013) Delattre, M., Genon-Catalot, V., and Samson, A. (2013). Maximum Likelihood Estimation for Stochastic Differential Equations with Random Effects. Scandinavian Journal of Statistics, 40, 322–343.

- Hoadley (1971) Hoadley, B. (1971). Asymptotic Properties of Maximum Likelihood Estimators for the Independent not Identically Distributed Case. The Annals of Mathematical Statistics, 42, 1977–1991.

- Lange (2010) Lange, K. (2010). Numerical Analysis for Statisticians. Springer, New York.

- Leander et al. (2015) Leander, J., Almquist, J., Ahlström, C., Gabrielsson, J., and Jirstrand, M. (2015). Mixed Effects Modeling Using Stochastic Differential Equations: Illustrated by Pharmacokinetic Data of Nicotinic Acid in Obese Zucker Rats. The AAPS Journal, 17, 586–596.

- Maitra and Bhattacharya (2015) Maitra, T. and Bhattacharya, S. (2015). On Bayesian Asymptotics in Stochastic Differential Equations with Random Effects. Statistics and Probability Letters, 103, 148–159. Also available at “http://arxiv.org/abs/1407.3971”.

- Maitra and Bhattacharya (2016a) Maitra, T. and Bhattacharya, S. (2016a). Asymptotic Theory of Bayes Factor in Stochastic Differential Equations: Part I. Available at “https://arxiv.org/abs/1503.09011”.

- Maitra and Bhattacharya (2016b) Maitra, T. and Bhattacharya, S. (2016b). Asymptotic Theory of Bayes Factor in Stochastic Differential Equations: Part II. Available at “https://arxiv.org/abs/1504.00002”.

- Maitra and Bhattacharya (2016c) Maitra, T. and Bhattacharya, S. (2016c). On Asymptotics Related to Classical Inference in Stochastic Differential Equations with Random Effects. Statistics and Probability Letters, 110, 278–288. Also available at “http://arxiv.org/abs/1407.3968”.

- Marjoram et al. (2003) Marjoram, P., Molitor, J., Plagnol, V., and Tavaŕe, S. (2003). Markov Chain Monte Carlo Without Likelihoods. Proceedings of the National Academy of Sciences, 100, 15324–15328.

- Oravecz et al. (2011) Oravecz, Z., Tuerlinckx, F., and Vandekerckhove, J. (2011). A hierarchical latent stochastic differential equation model for affective dynamics. Psychological Methods, 16, 468–490.

- Overgaard et al. (2005) Overgaard, R. V., Jonsson, N., Tornœ, C. W., and Madsen, H. (2005). Non-Linear Mixed-Effects Models with Stochastic Differential Equations: Implementation of an Estimation Algorithm. Journal of Pharmacokinetics and Pharmacodynamics, 32, 85–107.

- Ramsay and Silverman (2005) Ramsay, J. O. and Silverman, B. W. (2005). Functional Data Analysis. Springer, New York.

- Rao (2013) Rao, B. (2013). Semimartingales and their Statistical Inference. Chapman and Hall/CRC, Boca Ratan.

- Robert and Casella (2004) Robert, C. P. and Casella, G. (2004). Monte Carlo Statistical Methods. Springer-Verlag, New York.

- Schervish (1995) Schervish, M. J. (1995). Theory of Statistics. Springer-Verlag, New York.

- Serfling (1980) Serfling, R. J. (1980). Approximation Theorems of Mathematical Statistics. John Wiley & Sons, Inc., New York.

- Tavaŕe et al. (1997) Tavaŕe, S., Balding, D. J., Griffiths, R. C., and Donelly, P. (1997). Inferring Coalescence Times from DNA Sequence Data. Genetics, 145, 505–518.

- Zhu et al. (2011) Zhu, B., Song, P. X.-K., and Taylor, J. M. G. (2011). Stochastic Functional Data Analysis: A Diffusion Model-Based Approach. Biometrics, 67, 1295–1304.