Analytic approach for reflected Brownian motion in the quadrant

Abstract

Abstract.

Random walks in the quarter plane are an important object both of combinatorics and probability theory. Of particular interest for their study, there is an analytic approach initiated by Fayolle, Iasnogorodski and Malyšev, and further developed by the last two authors of this note. The outcomes of this method are explicit expressions for the generating functions of interest, asymptotic analysis of their coefficients, etc. Although there is an important literature on reflected Brownian motion in the quarter plane (the continuous counterpart of quadrant random walks), an analogue of the analytic approach has not been fully developed to that context. The aim of this note is twofold: it is first an extended abstract of two recent articles of the authors of this paper, which propose such an approach; we further compare various aspects of the discrete and continuous analytic approaches.

keywords:

Reflected Brownian motion in the quadrant; (Random) Walks in the quarter plane; Stationary distribution; Laplace transform; Generating function; Boundary value problem; Asymptotic analysis1 Introduction

1.1 Random walks in the quarter plane

Since the seventies and the pioneered papers Malyšev, (1972); Fayolle and Iasnogorodski, (1979), random walks in the quarter plane (cf. Figure 1) are extensively studied. They are indeed an important object of probability theory and have been studied for their recurrence/transience, for their links with queueing systems (Fayolle and Iasnogorodski, (1979)), representation theory (Biane, (1992)), potential theory. Moreover, the state space offers a natural framework for studying any two-dimensional population; accordingly, quadrant walks appear as models in biology and in finance (Cont and de Larrard, (2013)). Another interest of random walks in the quarter plane is that in the large class of random processes in cones, they form a family for which remarkable exact formulas exist. Moreover, quadrant walks are popular in combinatorics, see Bousquet-Mélou and Mishna, (2010); Bostan and Kauers, (2010); Kurkova and Raschel, (2012). Indeed, many models of walks are in bijection with other combinatorial objects: maps, permutations, trees, Young tableaux, etc. In combinatorics again, famous models have emerged from quadrant walks, as Kreweras’ or Gessel’s ones, see Bousquet-Mélou and Mishna, (2010); Bostan and Kauers, (2010). Finally, walks in the quarter plane are interesting for the numerous tools used for their analysis: combinatorial (Bousquet-Mélou and Mishna, (2010)), from complex analysis (Malyšev, (1972); Fayolle and Iasnogorodski, (1979); Fayolle et al., (1999); Kurkova and Raschel, (2011, 2012); Bernardi et al., (2015)), computer algebra (Bostan and Kauers, (2010)), for instance.

1.2 Issues and technicalities of the analytic approach

In the literature (see, e.g., Malyšev, (1972); Fayolle and Iasnogorodski, (1979); Fayolle et al., (1999); Kurkova and Raschel, (2011, 2012)), the analytic approach relies on six key steps:

-

(i)

Finding a functional equation between the generating functions of interest;

-

(ii)

Reducing the functional equation to boundary value problems (BVP);

-

(iii)

Solving the BVP;

-

(iv)

Introducing the group of the walk;

-

(v)

Defining the Riemann surface naturally associated with the model, continuing meromorphically the generating functions and finding the conformal gluing function;

-

(vi)

Deriving the asymptotics of the (multivariate) coefficients.

Before commenting these different steps, let us note that altogether, they allow for studying the following three main problems:

- (P1)

- (P2)

- (P3)

The point (i) reflects the inherent properties of the model and is easily obtained. Point (ii), first shown in Fayolle and Iasnogorodski, (1979), is now standard (see Fayolle et al., (1999)) and follows from algebraic manipulations of the functional equation of (i). Item (iii) uses specific literature devoted to BVP (our main reference for BVP is the book of Litvinchuk, (2000)). The idea of introducing the group of the model (iv) was proposed in Malyšev, (1972), and brought up to light in the combinatorial context in Bousquet-Mélou and Mishna, (2010). Point (v) is the most technical a priori; it is however absolutely crucial, as it allows to access key quantities (as a certain conformal gluing function which appears in the exact formulation of (iii)). Finally, (vi) uses a double refinement of the classical saddle point method: the uniform steepest descent method.

1.3 Reflected Brownian motion in the quarter plane

There is a large literature on reflected Brownian motion in quadrants (and also in orthants, generalization to higher dimension of the quadrant), to be rigorously introduced in Section 3. First, it serves as an approximation of large queuing networks (see Foddy, (1984); Baccelli and Fayolle, (1987)); this was the initial motivation for its study. In the same vein, it is the continuous counterpart of (random) walks in the quarter plane. In other directions, it is studied for its Lyapunov functions in Dupuis and Williams, (1994), cone points of Brownian motion in Le Gall, (1987), intertwining relations and crossing probabilities in Dubédat, (2004), and of particular interest for us, for its recurrence/transience in Hobson and Rogers, (1993). The asymptotic behavior of the stationary distribution (when it exists) is now well known, see Harrison and Hasenbein, (2009); Dai and Miyazawa, (2011); Franceschi and Kurkova, (2016). There exist, however, very few results giving exact expressions for the stationary distribution. Let us mention Foddy, (1984) (dealing with the particular case of a Brownian motion with identity covariance matrix), Baccelli and Fayolle, (1987) (on a diffusion having a quite special behavior on the boundary), Harrison and Williams, 1987b ; Dieker and Moriarty, (2009) (on the special case when stationary densities are exponential) and Franceschi and Raschel, (2016) (on the particular case of an orthogonal reflection). We also refer to Burdzy et al., (2015) for the analysis of reflected Brownian motion in bounded planar domains by complex analysis techniques.

1.4 Main results and plan

This note is an extended abstract of the papers Franceschi and Kurkova, (2016); Franceschi and Raschel, (2016), whose main contributions are precisely to export the analytic method for reflected Brownian motion in the quarter plane. Our study constitutes one of the first attempts to apply these techniques to the continuous setting, after Foddy, (1984); Baccelli and Fayolle, (1987). In addition of reporting about the works Franceschi and Kurkova, (2016); Franceschi and Raschel, (2016), we also propose a comparative study of the discrete/continuous cases.

Our paper is organized as follows: Section 2 concerns random walks and Section 3 Brownian motion. For clarity of exposition we have given the same structure to Sections 2 and 3: in Section 2.1/3.1 we first state the key functional equation (a kernel equation), which is the starting point of our entire analysis. We study the kernel (a second degree polynomial in two variables). In Section 2.2/3.2 we state and solve the BVP satisfied by the generating functions. We then move to asymptotic results (Section 2.3/3.3). In Section 2.4/3.4 we introduce the Riemann surface of the model and some important related facts.

2 Random walks in the quarter plane

This section is devoted to the discrete case and is based mainly on Fayolle et al., (1999).

2.1 Functional equation

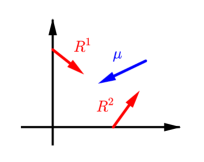

One considers a piecewise homogeneous random walk with sample paths in . There are four domains of spatial homogeneity (the interior of , the horizontal and vertical axes, the origin), inside of which the transition probabilities (of unit size) are denoted by , , and , respectively. See Figure 1. The inventory polynomial of the inner domain is called the kernel and equals

| (1) |

The inventory polynomials associated to the other homogeneity domains are

Assuming the random walk ergodic (we refer to (Fayolle et al., , 1999, Theorem 1.2.1) for necessary and sufficient conditions), we denote the invariant measure by and introduce the generating functions

Writing the balance equations at the generating function level, we have (see (Fayolle et al., , 1999, Equation (1.3.6)) for the original statement):

Lemma 1

The fundamental functional equation holds

| (2) |

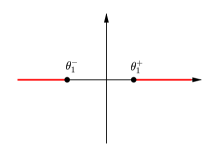

Equation (2) holds a priori in the region . Indeed, the sum up to , so that the generating functions , and are well defined on the (bi)disc. The identity (2) is a kernel equation, and a crucial role will be played by the kernel (1). This polynomial is of second order in both and ; its roots and defined by

| (3) |

are thus algebraic of degree . Writing the kernel as and defining its discriminant , one has obviously

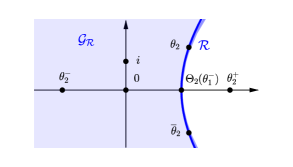

The polynomial has three or four roots, and exactly two of them are located in the unit disc, see (Fayolle et al., , 1999, Lemma 2.3.8). They are named , cf. Figure 2. On one has , so that the two values (or branches) of (that we shall call and ) are complex conjugate of one another. In particular, the set

is symmetrical w.r.t. the real axis (Figure 2). This curve will be used to set a boundary condition for the unknown function (Lemma 2).

2.2 Statement and resolution of the BVP

The analytic approach of Malyšev, (1972); Fayolle and Iasnogorodski, (1979); Fayolle et al., (1999) proposes a way for solving the functional equation (2), by reduction to a BVP. Generally speaking, a BVP consists of a regularity condition and a boundary condition.

Lemma 2

The function satisfies the following BVP:

-

•

is meromorphic in the bounded domain delimitated by and has there identified poles;

-

•

for any ,

Proof 2.1.

The regularity condition follows from Theorem 5, which provides a (maximal) meromorphic continuation of the function . We now turn to the boundary condition. For , we evaluate the functional equation (2) at and divide by . We then make the difference of the identities corresponding to and . Finally, we substitute and , noting that when , by construction. Notice that we have chosen the segment connecting the points inside of the unit disc (Figure 2), in which we know that the generating function is well defined.

Although Lemma 2 could be written more precisely (by giving the number and the location of the poles of ), we shall prefer the above version, since we focus in this note on the main ideas of the analytic approach.

Lemma 2 happens to characterize the generating functions, as it eventually leads to an explicit expression for , see Theorem 3. Before stating this central result (borrowed from (Fayolle et al., , 1999, Theorem 5.4.3)), we need to introduce a function called a conformal gluing function. By definition it satisfies for and is one-to-one inside of . This function will be constructed in Theorem 6 of Section 2.4.

Theorem 3.

There exist two functions and , constructed from , , and , such that the following integral formulation for holds:

A similar contour integral representation exists for , and eventually the functional equation (2) provides us with an explicit expression for the bivariate function .

2.3 Asymptotics of the stationary probabilities

The asymptotics of coefficients of unknown generating functions satisfying the functional equation (2) has been obtained by Malyšev, (1973) via analytic arguments. He computed the asymptotics of the stationary probabilities as and , for any given . Let us briefly present these results. It is assumed in Malyšev, (1973) that the random walk is simple, meaning that

| (4) |

It is also assumed that both coordinates of the interior drift vector are negative (as in Figure 3). For , we define the point as follows. Introducing as in Kurkova and Raschel, (2011) the function on , the mapping

is a homeomorphism between and the unit circle. The point is the unique solution to . Finally, .

Following Malyšev, (1973), we introduce the sets of parameters

and and accordingly. The automorphisms and are defined in Section 2.4 by (8). The following theorem is proven in Malyšev, (1973).

Theorem 4.

Let with . Then as we have

| (5) |

where , and are constants that can be expressed in terms of the functions and . The point is a solution of the system and similarly, is a solution of .

Proof 2.2.

The stationary probabilities are first written as two-dimensional Cauchy integrals, then reduced via the residue theorem to one-dimensional integrals along some contours. The asymptotics of these integrals is characterized either by the saddle point in the case of the set of parameters or by a pole or that is encountered when moving the integration contour to the saddle point; this happens for the sets of parameters , and .

This approach has been applied for the analysis of the join the shortest queue problem in Kurkova and Suhov, (2003), and for computing the asymptotics of Green functions for transient random walks in the quarter plane reflected at the axes (see Kurkova and Malyshev, (1998)) or killed at the axes (cf. Kurkova and Raschel, (2011)). Moreover, as illustrated in Kurkova and Raschel, (2011); Kurkova and Suhov, (2003), the assumption (4) is not crucial for the applicability of the method. The limiting cases and can also be treated via this approach, with some additional technical details (the saddle point then coincides with a branch point of the integrand), it is done in Kurkova and Raschel, (2011).

2.4 Riemann surface and related facts

In Section 2.1 the set

has appeared very naturally, since in order to state the BVP (our Lemma 2), we introduced the functions and , which by construction cancel the kernel, see (3).

In this section the central idea is to consider the (global) complex structure of . The set turns out to be a Riemann surface of genus , i.e., a torus. This simply comes from the reformulation of the identity as

Moreover, the Riemann surface of the square root of a polynomial of degree or is classically a torus (with this terminology, the roots of the discriminant are branch points).

This new point of view on brings powerful tools. Of particular interest is a parametrization of in terms of Weierstrass elliptic functions:

| (6) |

This parametrization is totally explicit: and are rational functions in the -Weierstrass function and its derivative (see (Fayolle et al., , 1999, Lemma 3.3.1)); the periods and admit expressions as elliptic integrals in terms of (cf. (Fayolle et al., , 1999, Lemma 3.3.2)), etc. Moreover, as any functions of and/or , the functions and can be lifted on by setting

| (7) |

Group of the walk

Introduced in Malyšev, (1972) in a probabilistic context and further used in Fayolle et al., (1999); Bousquet-Mélou and Mishna, (2010), the group of the walk is a dihedral group generated by

| (8) |

(One easily verifies that these generators are idempotent: .) The group can be finite or infinite, according to the order of the element . The generator (resp. ) exchanges the roots in (resp. in ) of . Viewed as a group of birational transformations in Bousquet-Mélou and Mishna, (2010), we shall rather see it as a group of automorphisms of the Riemann surface .

This group has many applications. First, it allows for a continuation of the functions and (Theorem 5 below). It further connects the algebraic nature of the generating functions to the (in)finiteness of the group (Theorem 7). Finally, in the finite group case, elementary algebraic manipulations of the functional equations can be performed (typically, via the computation of certain orbit-sums) so as to eventually obtain D-finite expressions for the unknowns, see (Fayolle et al., , 1999, Chapter 4) and Bousquet-Mélou and Mishna, (2010).

Using the structure of the automorphisms of a torus, the lifted versions of and admit simple expressions (Fayolle et al., , 1999, Section 3.1.2):

| (9) |

where, as the periods and , is an elliptic integral (Fayolle et al., , 1999, Lemma 3.3.3). Accordingly, the group is finite if and only if , which provides a nice criterion in terms of elliptic integrals.

Continuation

While the generating function is defined through its power series in the unit disc, it is a priori unclear how to continue it to a larger domain. This is however crucial, since the curve on which it satisfies a BVP (Lemma 2) is not included in the unit disc in general.

Theorem 5.

The function can be continued as a meromorphic function to .

We notice that does not intersect by (Fayolle et al., , 1999, Theorem 5.3.3), so that Theorem 5 indeed provides a continuation of the generating function in the domain delimitated by .

Proof 2.3.

This result, stated as Theorem 3.2.3 in Fayolle et al., (1999), is a consequence of a continuation of the lifted generating functions (7) on the Riemann surface (or, better, on its universal covering — but we shall not go into these details here). The continuation on uses the (lifted) functional equation (2) and the group of the walk .

Conformal mapping

In the integral expression of Theorem 3, the conformal gluing function is all-present, as it appears in the integrand and in and as well. The introduction of the Riemann surface allows to derive an expression for this function (this is another major interest of introducing ). Let us recall that and are the periods of the elliptic functions of the parametrization (6), while comes out in the lifted expression (9) of the automorphisms.

Theorem 6.

The conformal gluing function admits the expression:

where for , is the -Weierstrass elliptic function with periods and .

Proof 2.4.

While on the complex plane, is a quartic curve, it becomes on much simpler (typically, a segment). This remark (which again illustrates all the benefit of having introduced the Riemann surface) is used in (Fayolle et al., , 1999, Section 5.5.2) so as to obtain the above expression for .

Algebraic nature of the generating functions

Recall that a function of one variable is D-finite if it satisfies a linear differential equation with polynomial coefficients.

Theorem 7.

If the group is finite, the generating functions and are D-finite.

Proof 2.5.

3 Reflected Brownian motion in the quadrant

Defining reflected Brownian motion in the quadrant

The object of study here is the reflected Brownian motion with drift in the quarter plane

| (10) |

associated to the triplet , composed of a non-singular covariance matrix, a drift and a reflection matrix, see Figure 3:

In Equation (10), is any initial point in , the process is an unconstrained planar Brownian motion starting from the origin, and for , is a continuous non-decreasing process, that increases only at time such that , namely . The columns and represent the directions in which the Brownian motion is pushed when the axes are reached.

The reflected Brownian motion associated with is well defined, see for instance Williams, (1995). Its stationary distribution exists and is unique if and only if the following (geometric flavored) conditions are satisfied (see, e.g., Harrison and Williams, 1987a ; Hobson and Rogers, (1993))

| (11) |

More that the Brownian motion in the quadrant, all results presented below concern the Brownian motion in two-dimensional cones (by a simple linear transformation of the cones). This is a major difference and interest of the continuous case, which also illustrates that the analytic approach is very well suited to that context.

3.1 Functional equation

Laplace transform of the stationary distribution

The continuous analogues of the generating functions are the Laplace transforms. As their discrete counterparts, they characterize the stationary distribution. Under assumption (11), that we shall do throughout the manuscript, the stationary distribution is absolutely continuous w.r.t. the Lebesgue measure, see Harrison and Williams, 1987a ; Dai, (1990). We denote its density by . Let the Laplace transform of be defined by

We further define two finite boundary measures and with support on the axes, by mean of the formula

The measures are continuous w.r.t. the Lebesgue measure by Harrison and Williams, 1987a , and may be viewed as boundary invariant measures. We define their moment Laplace transform by

Functional equation

There is a functional equation between the Laplace transforms , and , see (12), which is reminiscent of the discrete functional equation (2).

Lemma 8.

The following key functional equation between the Laplace transforms holds

| (12) |

where

By definition of the Laplace transforms, this equation holds at least for any with and . The polynomial in (12) is the kernel and is the continuous analogue of the kernel (1) in the discrete case. Polynomials and are the counterparts of and .

Proof 3.1.

To show (12), the main idea is to use an identity called a basic adjoint relationship (first proved in Harrison and Williams, 1987a in some particular cases, then extended in Dai and Harrison, (1992)), which characterizes the stationary distribution. (It is the continuous analogue of the well-known equation , where is the stationary distribution of a recurrent continuous-time Markov chain with infinitesimal generator .) This basic adjoint relationship connects the stationary distribution and the corresponding boundary measures and . We refer to Foddy, (1984); Dai and Miyazawa, (2011) for the details.

Elementary properties of the kernel

The kernel in (12) can be alternatively written as

| (13) |

The equation defines a two-valued algebraic function by , and similarly such that . Expressions of their branches are given by

where is the discriminant. The polynomial has two zeros, real and of opposite signs; they are denoted by and are branch points of the algebraic function . In the same way we define and its branch points .

Finally, notice that is negative on . Accordingly, the branches take complex conjugate values on this set.

3.2 Statement and resolution of the BVP

An important hyperbola

For further use, we need to introduce the curve

| (14) |

It is the analogue of the curve in Section 2.1. The curve is symmetrical w.r.t. the real axis, see Figure 4 (this is a consequence of being negative on , see above). Furthermore, it is a (branch of a) hyperbola by Baccelli and Fayolle, (1987). We shall denote by the open domain of bounded by and containing , see Figure 4. Obviously , the closure of , is equal to .

BVP for orthogonal reflections

In the case of orthogonal reflections (see Figure 3), is the identity matrix in (10), and we have and . We set

| (15) |

Lemma 9.

The function in (15) satisfies the following BVP:

-

(i)

is meromorphic on with a single pole at , of order and residue , and vanishes at infinity;

-

(ii)

is continuous on and

(16)

Proof 3.2.

The regularity condition of point (i) follows from Theorem 15, which provides a (maximal) meromorphic continuation of the function. Let us now consider (ii). Evaluating the (continued) functional equation (12) at , we obtain which immediately implies that

| (17) |

Choosing , the two quantities and are complex conjugate the one of the other, see Section 3.1. Equation (17) can then be reformulated as (16), using the definition (14) of the curve .

The BVP stated in Lemma 9 is called a homogeneous BVP with shift (the shift stands here for the complex conjugation, but the theory applies to more general shifts, see Litvinchuk, (2000)). It has a simpler form than the BVP in Lemma 2 for the discrete case, because there is no inhomogeneous term (as ) and also because in the coefficients in front of the unknowns there is no algebraic function (as ) involved. Due to its particularly simple form, we can solve it in an explicit way, using the two following steps:

-

•

Using a certain conformal mapping (to be introduced below), we can construct a particular solution to the BVP of Lemma 9.

- •

In Franceschi and Raschel, (2016) it is explained that the above method may be viewed as a variation of Tutte’s invariant approach, first introduced by Tutte for solving a functional equation arising in the enumeration of properly colored triangulations, see Tutte, (1995).

The function glues together the upper and lower parts of the hyperbola . There are at least two ways to find such a . First, it turns out that in the literature there exist expressions for conformal gluing functions for relatively simple curves as hyperbolas, see (Baccelli and Fayolle, , 1987, Equation (4.6)). Here (based on Franceschi and Raschel, (2016)), we use instead the Riemann sphere , as we will see in Section 3.4. Indeed, many technical aspects (and in particular finding the conformal mapping) happen to be quite simpler on that surface.

We will deduce from Section 3.4 that function can be expressed in terms of the generalized Chebyshev polynomial

as follows:

| (18) |

where we have noted

| (19) |

In the case of orthogonal reflection, this methods leads to the main result of Franceschi and Raschel, (2016), which is:

Theorem 10.

Let be the identity matrix in (10). The Laplace transform is equal to

Statement of the BVP in the general case

We would like to close Section 3.2 by stating the BVP in the case of arbitrary reflections (non-necessarily orthogonal). Let us define for

Similarly to Lemma 9, there is the following result:

Lemma 11.

The function satisfies the following BVP:

-

(i)

is meromorphic on with at most one pole of order and is bounded at infinity;

-

(ii)

is continuous on and

(20)

Due to the presence of the function in (20), this BVP (still homogeneous with shift) is more complicated than the one encountered in Lemma 9 and cannot be solved thanks to an invariant lemma. Instead, the resolution is less combinatorial and far more technical, and the solution should be expressed in terms of both Cauchy integrals and the conformal mapping of Theorem 10. This will be achieved in a future work.

3.3 Asymptotics of the stationary probabilities

Overview

Let be a random vector that has the stationary distribution of the reflected Brownian motion. Dai and Miyazawa, (2011) obtain the following asymptotic result: for a given directional vector they find (up to a multiplicative constant) a function such that

In Franceschi and Kurkova, (2016) we solve a harder problem arisen in (Dai and Miyazawa, , 2011, §8), namely computing the asymptotics of as , where is any directional vector and any compact subset. Furthermore, we are able to find the full asymptotic expansion of the density of as and , for any given angle .

Main results

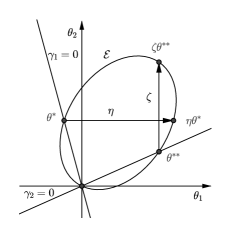

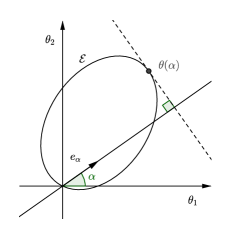

First we need to introduce some notations. The equation determines an ellipse on passing through the origin, see Figure 5. Here we restrict ourselves to the case and , although our methods can be applied without additional difficulty to other cases.

For a given angle , let us define the point on the ellipse by

| (21) |

The coordinates of can be given explicitly. One can also construct geometrically as on Figure 5.

Secondly, consider the straight lines and , depending on the reflection matrix only. They cross the ellipse at the origin. The line (resp. ) intersects the ellipse at a second point called (resp. ). To present our results, we need to define the images on of these points via the so-called Galois automorphisms and , to be introduced in Section 3.4. Namely, for the point there exists a unique point with the same second coordinate. Likewise, there exists a unique point with the same first coordinate as . Points , , and are pictured on Figure 5. Their coordinates can be made explicit.

Similarly to the discrete case, we introduce the set of parameters

and , and accordingly. The following theorem provides the main term in the asymptotic expansion of .

Theorem 12.

Let with . We assume that . Then as we have

| (22) |

where , and are constants that can be expressed in terms of functions and and the parameters.

In Franceschi and Kurkova, (2016) the constants mentioned in Theorem 12 are specified in terms of functions and . But these functions are for now unknown. As we explained in Section 3.2, in a next work we are going to obtain and as solutions of BVP, thereby determining the constants in Theorem 12.

Proof 3.3 (of the key step of Theorem 12).

Theorem 12 is proven in Franceschi and Kurkova, (2016). The first step consists in continuing meromorphically the functions and on or on the Riemann surface , see Section 3.4. Then by the functional equation (12) and the inversion formula of Laplace transform (we refer to Doetsch, (1974) and Brychkov et al., (1992)), the density can be represented as a double integral. Using standard computations from complex analysis, we are able to reduce it to a sum of single integrals. We obtain the following (with the notation (13)):

These integrals are typical to apply the saddle point method, see Fedoryuk, (1986). The coordinates of the saddle point are the critical points of the functions

It is the point . Then we have to shift the integration contour up to new contours which coincide with the steepest-descent contour near the saddle point. When we shift the contours we have to take into account the poles of the integrands and their residues. The asymptotics will be determined by the pole if we cross a pole when we shift the contour and by the saddle point otherwise.

3.4 Riemann surface and related facts

Riemann surface

The Riemann surface

may be viewed as the set of zeros of the kernel (equivalently, it is the Riemann surface of the algebraic functions and ). Due to the degree of , the surface has genus and is a Riemann sphere, i.e., homeomorphic to , see Franceschi and Kurkova, (2016). It admits a very useful rational parametrization, given by

| (23) |

with as in (19). The equation holds and .

Group of the process

We finally introduce the notion of group of the model, similar to the notion of group of the walk in the discrete setting (see Malyšev, (1972); Fayolle et al., (1999); Bousquet-Mélou and Mishna, (2010)). This group is generated by and , given by (with the notation (13))

By construction, the generators satisfy as soon as . In other words, there are (covering) automorphisms of the surface . Since , the group is a dihedral group, which is finite if and only if the element (or equivalently ) has finite order.

Algebraic nature of the Laplace transforms

With the above definition, it is not clear how to see if the group is finite, nor to see it its finiteness would have any implication on the problem. In fact, we have, with defined in (19):

Lemma 13.

The group is finite if and only if .

The proof of Lemma 13 is simple, once the elements and have been lifted and reformulated on the sphere :

These transformations leave invariant and , respectively, see (23). In particular, we have the following result (see Franceschi and Raschel, (2016)), which connects the nature of the solution of the BVP to the finiteness of the group. Such a result holds for discrete walks, see our Theorem 7 and Bousquet-Mélou and Mishna, (2010); Bernardi et al., (2015).

Conformal mapping

Continuation of the Laplace transforms

To establish the BVP, we have stated a boundary condition for the functions and , on curves which lie outside their natural domains of definition (the half-plane with negative real-part), see Figure 4. In the same way, in the asymptotic study we use the steepest descent method on some curves outside of the initial domain of definition. We therefore need to extend the domain of definition of the Laplace transforms.

Theorem 15.

The function can be continued meromorphically on the cut plane .

Proof 3.4.

The first step is to continue meromorphically to the open and simply connected set by setting

This is immediate (see Franceschi and Kurkova, (2016) for the details). It is then possible to pursue the extension to the whole using the invariance properties by the automorphisms and satisfied by the lifted Laplace transforms on .

Acknowledgements.

We acknowledge support from the projet MADACA of the Région Centre and from Simon Fraser University (British Columbia, Canada). We thank our three AofA referees for useful comments.References

- Baccelli and Fayolle, (1987) Baccelli, F. and Fayolle, G. (1987). Analysis of models reducible to a class of diffusion processes in the positive quarter plane. SIAM J. Appl. Math., 47(6):1367–1385.

- Bernardi et al., (2015) Bernardi, O., Bousquet-Mélou, M., and Raschel, K. (2015). Counting quadrant walks via Tutte’s invariant method. Preprint arXiv:1511.04298 (to appear in the proceedings of FPSAC 2016), pages 1–13.

- Biane, (1992) Biane, P. (1992). Minuscule weights and random walks on lattices. In Quantum probability & related topics, QP-PQ, VII, pages 51–65. World Sci. Publ., River Edge, NJ.

- Bostan and Kauers, (2010) Bostan, A. and Kauers, M. (2010). The complete generating function for Gessel walks is algebraic. Proc. Amer. Math. Soc., 138(9):3063–3078. With an appendix by Mark van Hoeij.

- Bousquet-Mélou and Mishna, (2010) Bousquet-Mélou, M. and Mishna, M. (2010). Walks with small steps in the quarter plane. In Algorithmic probability and combinatorics, volume 520 of Contemp. Math., pages 1–39. Amer. Math. Soc., Providence, RI.

- Brychkov et al., (1992) Brychkov, Y., Glaeske, H.-J., Prudnikov, A., and Tuan, V. K. (1992). Multidimensional Integral Transformations. CRC Press.

- Burdzy et al., (2015) Burdzy, K., Chen, Z.-Q., Marshall, D., and Ramanan, K. (2015). Obliquely reflected Brownian motion in non-smooth planar domains. Preprint arXiv:1512.02323, pages 1–60.

- Cont and de Larrard, (2013) Cont, R. and de Larrard, A. (2013). Price dynamics in a Markovian limit order market. SIAM J. Financial Math., 4(1):1–25.

- Dai, (1990) Dai, J. (1990). Steady-state analysis of reflected Brownian motions: Characterization, numerical methods and queueing applications. ProQuest LLC, Ann Arbor, MI. Thesis (Ph.D.)–Stanford University.

- Dai and Harrison, (1992) Dai, J. and Harrison, J. (1992). Reflected Brownian motion in an orthant: numerical methods for steady-state analysis. Ann. Appl. Probab., 2(1):65–86.

- Dai and Miyazawa, (2011) Dai, J. and Miyazawa, M. (2011). Reflecting Brownian motion in two dimensions: Exact asymptotics for the stationary distribution. Stoch. Syst., 1(1):146–208.

- Dieker and Moriarty, (2009) Dieker, A. and Moriarty, J. (2009). Reflected Brownian motion in a wedge: sum-of-exponential stationary densities. Electron. Commun. Probab., 14:1–16.

- Doetsch, (1974) Doetsch, G. (1974). Introduction to the Theory and Application of the Laplace Transformation. Springer Berlin Heidelberg, Berlin, Heidelberg.

- Dubédat, (2004) Dubédat, J. (2004). Reflected planar Brownian motions, intertwining relations and crossing probabilities. Ann. Inst. H. Poincaré Probab. Statist., 40(5):539–552.

- Dupuis and Williams, (1994) Dupuis, P. and Williams, R. (1994). Lyapunov functions for semimartingale reflecting Brownian motions. Ann. Probab., 22(2):680–702.

- Fayolle and Iasnogorodski, (1979) Fayolle, G. and Iasnogorodski, R. (1979). Two coupled processors: the reduction to a Riemann-Hilbert problem. Z. Wahrsch. Verw. Gebiete, 47(3):325–351.

- Fayolle et al., (1999) Fayolle, G., Iasnogorodski, R., and Malyshev, V. (1999). Random Walks in the Quarter-Plane. Springer Berlin Heidelberg, Berlin, Heidelberg.

- Fedoryuk, (1986) Fedoryuk, M. (1986). Asymptotic methods in analysis. In Current problems of mathematics. Fundamental directions, Vol. 13 (Russian), Itogi Nauki i Tekhniki, pages 93–210. Akad. Nauk SSSR, Vsesoyuz. Inst. Nauchn. i Tekhn. Inform., Moscow.

- Foddy, (1984) Foddy, M. (1984). Analysis of Brownian motion with drift, confined to a quadrant by oblique reflection (diffusions, Riemann-Hilbert problem). ProQuest LLC, Ann Arbor, MI. Thesis (Ph.D.)–Stanford University.

- Franceschi and Kurkova, (2016) Franceschi, S. and Kurkova, I. (2016). Asymptotic expansion of the stationary distribution for reflected Brownian motion in the quarter plane via analytic approach. Preprint arXiv:1604.02918, pages 1–45.

- Franceschi and Raschel, (2016) Franceschi, S. and Raschel, K. (2016). Tutte’s invariant approach for Brownian motion reflected in the quadrant. Preprint arXiv:1602.03054, pages 1–14.

- Harrison and Hasenbein, (2009) Harrison, J. and Hasenbein, J. (2009). Reflected Brownian motion in the quadrant: tail behavior of the stationary distribution. Queueing Syst., 61(2-3):113–138.

- (23) Harrison, J. M. and Williams, R. J. (1987a). Brownian models of open queueing networks with homogeneous customer populations. Stochastics, 22(2):77–115.

- (24) Harrison, J. M. and Williams, R. J. (1987b). Multidimensional reflected Brownian motions having exponential stationary distributions. The Annals of Probability, 15(1):115–137.

- Hobson and Rogers, (1993) Hobson, D. and Rogers, L. (1993). Recurrence and transience of reflecting Brownian motion in the quadrant. In Mathematical Proceedings of the Cambridge Philosophical Society, volume 113, pages 387–399. Cambridge Univ Press.

- Kurkova and Malyshev, (1998) Kurkova, I. and Malyshev, V. (1998). Martin boundary and elliptic curves. Markov Process. Related Fields, 4(2):203–272.

- Kurkova and Raschel, (2011) Kurkova, I. and Raschel, K. (2011). Random walks in with non-zero drift absorbed at the axes. Bull. Soc. Math. France, 139(3):341–387.

- Kurkova and Raschel, (2012) Kurkova, I. and Raschel, K. (2012). On the functions counting walks with small steps in the quarter plane. Publ. Math. Inst. Hautes Études Sci., 116:69–114.

- Kurkova and Suhov, (2003) Kurkova, I. and Suhov, Y. (2003). Malyshev’s theory and JS-queues. Asymptotics of stationary probabilities. Ann. Appl. Probab., 13(4):1313–1354.

- Le Gall, (1987) Le Gall, J.-F. (1987). Mouvement brownien, cônes et processus stables. Probab. Theory Related Fields, 76(4):587–627.

- Litvinchuk, (2000) Litvinchuk, G. (2000). Solvability Theory of Boundary Value Problems and Singular Integral Equations with Shift. Springer Netherlands, Dordrecht.

- Malyšev, (1972) Malyšev, V. (1972). An analytic method in the theory of two-dimensional positive random walks. Sibirsk. Mat. Ž., 13:1314–1329, 1421.

- Malyšev, (1973) Malyšev, V. (1973). Asymptotic behavior of the stationary probabilities for two-dimensional positive random walks. Sibirsk. Mat. Ž., 14:156–169, 238.

- Tutte, (1995) Tutte, W. (1995). Chromatic sums revisited. Aequationes Math., 50(1-2):95–134.

- Williams, (1995) Williams, R. (1995). Semimartingale reflecting Brownian motions in the orthant. In Stochastic networks, volume 71 of IMA Vol. Math. Appl., pages 125–137. Springer, New York.