Unbiased Monte Carlo Simulation of Diffusion Processes

Abstract

Monte Carlo simulations of diffusion processes often introduce bias in the final result, due to time discretization. Using an auxiliary Poisson process, it is possible to run simulations which are unbiased. In this article, we propose such a Monte Carlo scheme which converges to the exact value. We manage to keep the simulation variance finite in all cases, so that the strong law of large numbers guarantees the convergence. Moreover, the simulation noise is a decreasing function of the Poisson process intensity. Our method handles multidimensional processes with nonconstant drifts and nonconstant variance-covariance matrices. It also encompasses stochastic interest rates.

1 Introduction

We consider the parabolic PDE111We use the Einstein summation convention: there is a sum on indices appearing twice in a formula: . We also use the Kronecker delta which is 1 if and 0 if .

| (1) |

with terminal condition in a -dimensional space with time and space variables with coordinates , . All coefficients may depend on and . is a positive semi-definite symmetric matrix. It can be rewritten using Cholesky decomposition as or.

Feynman-Kac theorem states that the solution of this PDE is given by the expected value

| (2) |

under a multidimensional diffusion process

is a -dimensional vector of independent standard Brownian process. Drifts and volatilities are stochastic variables which depend on time and state variable .

The expected value (2) can be numerically estimated using Monte Carlo simulation. However common schemes exhibit some bias due to the discretization of time. This happens for instance with the simplest one, the Euler scheme. One usually controls this bias through smaller timestepping, which increases the computation time.

Bally and Kohatsu-Higa, (2015) introduce schemes without such bias (in the case where ). This is achieved using random time steps, where the time discretization is given by jump times of an independent Poisson process. In addition, one has to multiply paths contributions by some weights which are functions of the time discretization and of the path. However this can correspond to integrating random variables which are not always integrable or do not have finite variance, which leads to poor convergence.

Henry-Labordère et al., (2015) enhance this algorithm in two different ways. First, the weight functions are obtained for all diffusion processes in term of Malliavin weights. They also manage to keep the variance of the integrated variable finite in two cases: constant volatility and correlation (constant ) or one-dimensional processes without drift (). The variance is controlled by the intensity of the auxilliary Poisson process but it is not monotonous: it increases when the Poisson intensity becomes too small or too high. In particular, it is not possible to increase the average number of time steps beyond some value without increasing the variance.

Our first contribution is to introduce a different Monte Carlo scheme, with smaller variance. In particular the variance becomes asymptotically a decreasing function of the Poisson intensity.

As a second contribution, we show how to make the variance finite in the general case of a process with drift and nonconstant volatility, in any dimension.

Our third contribution is to handle the case where the discount rate is stochastic.

2 Unbiased scheme

2.1 Poisson process

Let us consider the parabolic PDE (1) with terminal condition .

We can rewrite this PDE as

where is the elliptic differential operator

The evolution operator can be expressed using a time ordered exponential

which is a notation for the infinite product

This allows to write the solution of equation (1) with terminal condition as

Expliciting variables, this means

In some cases, for instance when the stochastic process is a pure Brownian motion or a lognormal diffusion, the resulting marginal probability measure can be computed explicitely or can be simulated exactly222 On an infinitesimal time , acting on a test function can be represented by the convolution with a Gaussian kernel: Defining with , this convolution reads Integrating over infinitesimal times between and , can thus be expressed as a Feynman path integral The integral is taken over all paths starting from with a proper normalization factor . .

In other cases, we suppose that we have a different elliptic operator

with coefficients , and chosen such that the PDE can be solved exactly by Monte Carlo simulation. We denote the evolution operator by and decompose as . This means that for any function we can get the value of

under the stochastic process

With explicit coordinates this process follows the equation

| (3) |

where are independent standard Brownian motions.

We decompose the original operator as

with a corrective term

| (4) |

with

Using this split, the evolution operator becomes

On each infinitesimal time we have a term

| (5) |

The process with drift and covariance matrix is chosen so that it can be simulated without any bias. However the term given in equation (5) should be computed and taken into account at any infinitesimal time, which is numerically impossible.

Instead, this contribution is kept only with probability over infinitesimal time , compensated by a factor of , such that its expected value is unchanged. In other words, as in Bally and Kohatsu-Higa, (2015) and Henry-Labordère et al., (2015) we consider a Poisson process with intensity . We then replace by

| (6) |

Applied to a test function , the expected value over the Poisson process gives the factor we want to take into account:

In addition, the intensity could also be a stochastic process and depend on and .

Let be the number of Poisson jumps between times and and , the jump times. Between two Poisson jumps, the evolution operator corresponds to the diffusion process (3):

The processes and can depend on the Poisson jump times and also on the value of given by the diffusion equation (3). Our explicit choice will be described in sections 3 and 5.

Integrating over all times and taking the expected value on the Poisson process, we have

Operators act on functions by integration, which can be explicited as

| (7) |

2.2 Monte Carlo simulation

In a Monte Carlo simulation, the integrals on and the evolution operators are handled by averaging over simulated paths generated according to the law given by . In order to get an unbiased Monte Carlo scheme, we generate random sampling for Poisson jump times and the values of at those times according to process (3). This process, with drift and covariance matrix is chosen so that it can be simulated exactly, i.e. such that the Monte Carlo distribution of discounted at rate , conditional to , tends to when the number of samplings goes to infinity.

Operators are differential operators acting on all the factors which follow in formula (7). The first term to depend on the differentiation variable is in fact . If we know the explicit form of this evolution kernel, we can differentiate it explicitely. This defines weights and :

These are similar to Malliavin weights, except that here the kernel includes the discount factor. With null or deterministic discount rates, and are exactly the Malliavin weights, as introduced in this context by Henry-Labordère et al., (2015). When the discount factor depends on they also incorporate the derivative of these discount factors. However multiplying by these weights at this step would result in computing the expected value of a quantity with infinite variance. We will explain this issue and how to solve it in the following sections.

The other terms which can be functions of are , , and , depending on the choice which is made for those functions. However the variations of these variables will not contribute to the final result. To make this clear, we rewrite formula (7) in a recursive way for intermediate Poisson jump times:

| (8) |

In this formula, acts by differentiation with respect to on . The formula for involves , and . However these functions and the process (3) are only intermediate objects used in the computation: the final value of does not depend on the values chosen for these functions. As a consequence, their variations do not contribute to the derivatives of . In the following, differentiations in operators are therefore computed with frozen , and . In order to make this clear, we will denote by those frozen values which should not be variated when differentiating.

2.3 Infinite variance

Let us consider the simple case of a pure Brownian process. The evolution operator is the Gaussian kernel

The corresponding Malliavin weights are therefore

with and .

The time between two jumps is given by a Poisson law with density which behaves as at small . As , Malliavin weights are of orders and . This remains true for a large class of diffusion processes. Direct multiplication by weights and in (7) would therefore give a quantity of infinite variance. This would result in poor Monte Carlo convergence. In order for the expected value over jump time to be well defined and the integrand to have finite variance, the random variable we integrate should be of order with , so that its square is of order with .

In order to have a variable which behaves as when is small, the weights should be multiplied by quantity of order . In equation (7), is multiplied by , unless is the last Poisson time ().

Let us consider first the term . According to its definition (4), it is composed of terms proportional to , and . Our strategy is therefore to make all these terms of order .

The other multiplicative term is which is not in and is multiplied by . For this term, we will exploit the specific form of to transfer the derivative on to a derivative on . This derivative is then transferred to by integration by parts.

The last piece to handle is the last Poisson time, when the weights must be multiplied by the final payoff. In this case, we use antithetic sampling as in Henry-Labordère et al., (2015) to have a final term in .

Doing so, the random variable to integrate remains of order and thus has finite variance under the Poisson law. Then the strong law of large numbers applies and the Monte Carlo convergence remains in .

3 One-dimensional Monte Carlo scheme

Let us consider first the case of a one-dimensional process

We take a deterministic discount rate and we want to price a European option of maturity with payoff . In other words, we want to solve the parabolic PDE

with terminal condition .

3.1 Monte Carlo path

We take a constant Poisson process intensity . Starting at date , we draw at random the first Poisson time . For instance, we draw a random uniform number between 0 and 1 and invert the cumulative law: . We can thus iteratively draw times until we get a date larger than . We will denote by the last Poisson time before .

Between two succesive dates and we will simulate a process with drift and volatility . More precisely, we consider a Brownian process and we choose a function at each time , such that and which can depend on and . We then define

| (9) |

This corresponds to the Itô process

Identifying with

we define

| (10) | |||||

| (11) |

We suppose that we can write as a power series

( are coefficients which depend on but we do not make this explicit in order to simplify the notation.) Then for and we have

| (12) | |||||

| (13) |

where we use .

On the other hand, a Taylor expansion of functions and gives

| (14) | |||||

| (15) |

We have and therefore if and only if coefficients in equations (13) and (15) are equal. This means

| (16) | |||||

| (17) |

Similarly, we have if and only if

Using the expressions for and in these equations, this reads

| (18) | |||||

| (19) |

In addition, the continuity of at in (9), equivalent to , gives

| (20) |

Except expressions (16), (17), (18), (19) and (20) we have the freedom to choose all other coefficients. One simple choice is to set them to 0: for , and . Between and we thus choose the function to be

| (21) |

At time we draw a Gaussian variable with variance and then get recursively the Monte Carlo path

| (22) |

3.2 Corrective terms

Applying equations (10) and (11), our choice (2b) corresponds to a process with drift and volatility

As the discount rate is deterministic, we also take

Using these three function for with and and according to the definition of we have

with

With our explicit choice of functions , we get

3.2.1 Intermediate times

If is not the last Poisson time, i.e , acts on

| (24) |

More generally we will consider the action on this expression of a second order differential operator

In order to compute the derivatives of expression (24) with respect to we consider the change of variable from to defined as in equation (22):

with and . We introduce and notations to make clear that once the function is chosen, and are constant and should not be differentiated. This change of variable induces for the first derivative

| (25) |

Differentiating a second time with respect to we have

| (26) |

With our particular choice (2b) for the function this is

Inverting these equations we have

Thus we can write in term of variable

Using again

this becomes

| (27) |

After the change of variables from to , equation (24) becomes

| (28) |

As is a Brownian motion, in term of the new variable, the evolution operator is the product of the discount factor by a Gaussian kernel:

with

| (29) |

We have to compute the effect of the differential operator acting on given in formula (28), which we expand as

| (30) |

When acting on the second term in this formula, which contains , the derivatives on are replaced by Malliavin weights:

where the explicit form of the Gaussian kernel (29) gives

For the derivatives of the first term of expression (30) with respect to , we use the symmetry of the Gaussian kernel , therefore of , with respect to and to write

Then we integrate by part in first term of (30) to get

and similarly for the second derivative. Then we come back from to variable at time using (25) and (26) which in our case read

Combining all terms, we finally obtain

We can rewrite this as

with

| (31) | |||||

and

| (32) |

3.2.2 Payoff

On the final Poisson time , should act on

where is the payoff function.

A naive approach would be to the following. One simulates from as given in equation (22):

with and a Gaussian variable of variance . Then one computes the payoff and computes the derivatives using Malliavin weights. This means multiplying the discounted payoff by given in equation (32):

However this term behaves as at small and not as we want.

Instead, we will use antithetic sampling on this last time step, as in Henry-Labordère et al., (2015). More precisely, we compute

| (33) | |||||

and then

which simplifies to

| (34) |

The last term in has expected value and the two first terms are antithetic contributions to the option price.

If the payoff function is smooth and has a Taylor expansion, one can check that is of order . This is not true for a Call or Put option payoff in the vicinity of the strike. In this case we have . However, the probability to have the strike between and at the last time step scales as . As a consequence, the variance remains finite.

We finally discount on all time steps. As we take a deterministic discount rate in this first case, this factors out as a multiplication by

3.3 Monte Carlo scheme summary

We now sum up the whole Monte Carlo scheme in this one-dimensional case with deterministic discount factor. We consider a European option with maturity and payoff .

For each path, we do the following:

-

1.

Start from at time . Define

-

2.

On each date

-

(a)

Draw the next Poisson time with intensity . For example draw a random uniform variable between 0 and 1 and take .

If , set and go to step 3. - (b)

-

(c)

Compute and according to equation (3.2):

- (d)

-

(a)

- 3.

-

4.

Multiply by the discount factor:

We finally average over all path to get the unbiased Monte Carlo estimation of the option price.

4 Numerical results

4.1 Convergence

In order to test numerically our Monte Carlo scheme, we take a model for which we can have a closed formula as a reference value. We therefore choose the Black-Scholes model

which corresponds to local drift an volatility

There already exist an unbiased Monte Carlo scheme for this model, using as a variable. For the purpose of ours tests we ignore this and we naively apply our scheme and compare it to a Euler scheme.

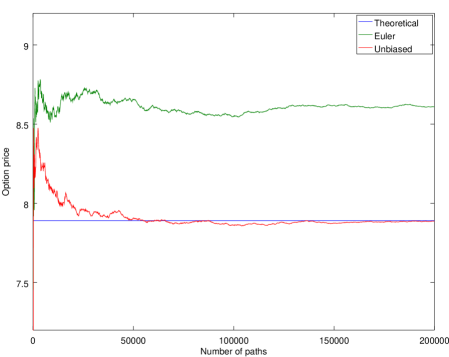

We consider an underlying with spot and volatility . We suppose the interest rate and the drift are . We price a Put option of maturity year at strike . The Black-Scholes formula gives an option price of 7.8909.

Figure 1 shows the simulated value as a function of the number of paths for the unbiased scheme with .

For comparison, it also shows the same convergence graph for a Euler scheme with the same average number of time steps . We see that this latter scheme converges to a biased value.

4.2 Comparison with Euler and Milstein scheme

When using the Euler scheme, the bias can be decreased using more time steps. This in turn increases the computation time. On the other hand, using the unbiased scheme is done at the cost of increasing the variance for small values of . Increasing the value of makes the variance smaller but also increases the computation time, as the average number of time steps is higher.

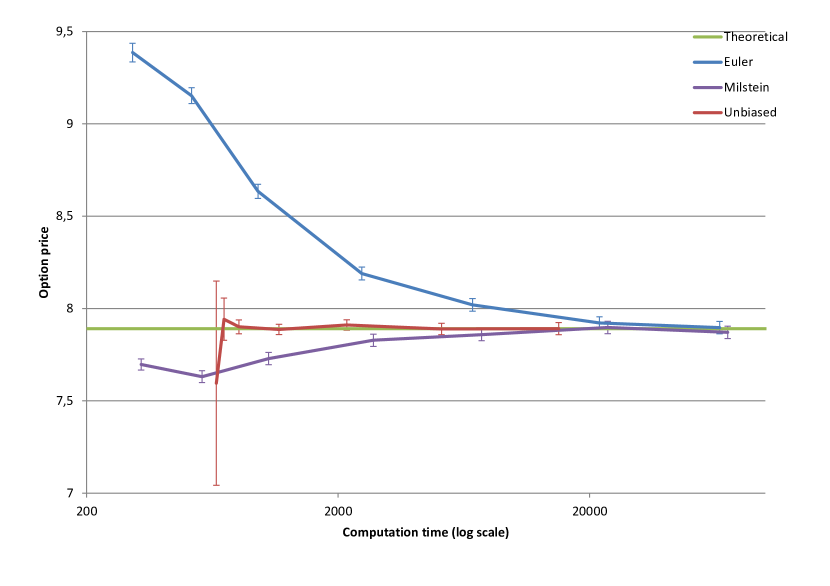

In order to assess the performance gain which can be achieved, we consider the 80% Put option described in the section 4.1 and we price it with both schemes. As the path generation has similarities with the Milstein scheme, we also compare with it. This allows to better isolate the effect of corrective terms in the unbiased scheme.

For the unbiased scheme, we use increasing values of from .01 to 29. For Euler and Milstein scheme, we take increasing numbers of time steps from 1 to 300. In all cases we draw million paths and compute numerically the estimated option price, the empirical standard deviation and the computation time. The results are shown in figure 2. The estimated prices are plotted with confidence interval against the computation time in logarithmic scale.

At very low Poisson intensity (), the Monte Carlo variance of the unbiased scheme is higher than the Euler and Milstein schemes. However it quickly decreases when increases. For it becomes even lower than noise of the Euler and Milstein schemes. Beyond the Monte Carlo noise is almost stationary: the corrective terms add negligible variance compared to the basic variance of the payoff. For all values of , we check that the final estimate is consistent with the theoretical value, up to the Monte Carlo statistical error. The value which appears to be optimal with respect to computation time corresponds to an average number of time steps over the period of 1 year.

On the opposite, the Euler scheme exhibits a large bias when the number of time steps is small. This bias decreases linearly with . Performing a weighted least squares regression, we estimate the bias to behave asymptotically as . In order to have a bias equal to the Euler Monte Carlo standard deviation , we thus need time steps. This corresponds to a computation time 43 times longer than the unbiased scheme with .

The Milstein scheme has a smaller bias, asymptotically in this example. We thus need time steps to get a bias of the same magnitude as the Monte Carlo noise. This means a computation 10 times slower than the unbiased scheme.

5 Multidimensional process

We consider now the general multi-dimensional case, where all parameters can depend on and in the parabolic PDE (1):

| (35) |

According to Feynman-Kac theorem, it corresponds to the multi-dimensional process

with stochastic discount rate . is a volatility matrix such that

which can be obtained by Cholesky decomposition. are independent standard Brownian processes.

5.1 Monte Carlo path

We draw Poisson times with intensity . Between these times, we simulate a -dimensional Brownian process . This corresponds to the parabolic PDE

| (36) |

Between two Poisson times and , we will consider two change of variables333If we see the total space made of space variables and prices as a fiber bundle, this corresponds to a change of variables on the base space and the fiber.:

-

•

Space variables. We go from to , using functions :

-

•

Numéraire. We change the numéraire, using a function

The change of numéraire transfers to derivatives as444We drop indices when they are not needed in order to simplify the notation.

Using the notations

we define

and

We will also use the inverse matrix , with defining properties

The change of space variables induces the following transformations on derivatives:

We want to find functions and such that , and behaves as at small .

We suppose that we can expand and as power series in and :

In this expression, or are tensors which are symmetric in space indices .

The continuity contraint at is . It translates to

In addition, we choose numéraires such that and coincide at the beginning of the period, . Mathematically this is , which gives for all

Taking into account these constraints, equations (38) have Taylor expansions

| (39) | |||||

| (40) | |||||

| (41) |

On the other hand, a Taylor expansion of the parameters of PDE (35) gives

| (42) | |||||

| (43) | |||||

| (44) |

From its definition, is

At the beginning of the period, with and , this is

We want to make , and vanish up to terms.

Let us start with the constant term in equations (40) and (43). From a Cholesky decomposition

we get a solution

| (45) |

This also gives

Its inverse is

Equating the first order terms of equations (40) and (43), we have

where is symmetric in indices and and in indices and . We multiply this equation by and , also using :

| (46) |

where we introduced the notations

and are tensors symmetric in the two last indices. We write equation (46) for the three cyclic permutations of the indices and get

| (47) | |||||

| (48) | |||||

| (49) |

The linear combination (49) + (48) - (47) then gives

Inverting the definition of in term of we get

Equating terms in equations (39) and (42) we get

Using the property we rewrite as

and get

| (51) |

Making the additional choice for for , and , the expression for simplifies to

| (52) |

This completes the definition of as a polynomial in and

with all coefficients defined in equations (45), (51), (5.1) and (52).

Finally, equating equations (41) and (44) we get

| (53) | |||||

| (54) |

Choosing all other coefficients to be 0, we also get as a polynomial in and

Using function and we are able to solve the PDE (37) by Monte Carlo simulation. At time we draw independent Gaussian variable with variance . Then we compute the value of the system at the following date

The (stochastic) discount factor between and is

We reccursively multply it to get the discount factor up from to as

starting from .

5.2 Corrective terms

From the definition of and , between ad , we have

Using the definitions of coefficients, this is

| (55) |

with

Equations (38) read

Using the definitions of coefficients or the fact these quantities should coincide with , and up to terms we can rewrite this as

Using these expressions for we compute

and we get

Except on the last time , acts on

| (56) |

More generally we will consider the action on this expression of a second order differential operator

As in section 3.2.1,e consider the change of variable between and defined by

On derivatives it induces

| (57) | |||||

and their inverse relations

In the new variables, the differential operator is

This operator acts on expression (56). In the new variables, the evolution operator becomes

| (58) |

where is the -dimensional Gaussian kernel

When acting on the term in , we differentiate with respect to , which means multiplying by the weights and , according to their definition

From expression (58) we have

and

For the term where directly acts on , we use the fact that given in equation (58) depends only on to transfer the derivatives from the first variable to the second one:

Then we integrate by part on to transfer the derivative on so that

and similarly for the second derivative. We then go back to the original variable at date using equations (57).

Assembling all terms, we finally get

where we define

with

We define by

which in our case, using (55) and

gives

We also define the effect of operator acting by weights multiplication as

Finally, on the last date, we keep the variance finite by antithetic sampling as in section 3.2.2. We compute

and the corresponding discount factors on the last time step

Then we can get the contribution from the path to the Monte Carlo estimate as

with

By construction has a null expected value. Thus is the average of two antithetic contributions to the option price, minus a term of null expected value.

Finally, the average of over all paths gives the Monte Carlo estimate of . It converges to it when the number of paths goes to infinity without any bias, as explained in section 2.

5.3 Monte Carlo scheme summary

In a Monte Carlo simulation, on each path we start by initializing operator by the identity and the disccount factor by 1 . We start from . We draw Poisson times . When going from date to date on a Monte Carlo path, we do the following:

-

1.

Compute all coefficients and in order to get functions and .

-

2.

Draw independent Gaussian variables with variance and get the next state as .

-

3.

Accumulate the discount factor as .

-

4.

Compute from as explained above.

When we reach the last time before maturity , we perform steps 1 and 2 with , then we compute the corrected, discounted payoff as explained above. The final value is obtained by averaging over all Monte Carlo paths.

6 Final comments

In this article, we introduce a Monte Carlo scheme which converges to the theoretical value without any bias, while keeping a finite variance. It applies to multidimensional diffusion processes and it can also handle stochastic interest rates. It allows to decrease the average number of time steps needed to reach a given precision, which can save a lot of computation time.

6.1 Related work

We leverage some interesting work presented in Henry-Labordère et al., (2015). However our Monte Carlo scheme differs in several ways.

One of the main differences is that in their scheme, paths which take into account corrective terms do not take into account the basic payoff contribution . In other words, their choice is equivalent to keeping the constant unit term in equation (6) only when there is no jump at time . This occurs with probability and this is compensated by a factor . Equation (6) is thus replaced by

The probability of not having any Poisson jump over a maturity is . Thus only this proportion of the Monte Carlo paths contains the basic payoff contribution. This is compensated by a weight coming from the product of on all infinitesimal times.

However this increases the total Monte Carlo noise, especially for large values of the Poisson intensity . In this case is close to zero and very few paths, if any, include the payoff contribution . In addition all paths contributions include a factor which can become very large.

In our scheme, the payoff contribution is kept for all paths, whether they include corrective terms or not. In addition, there is no such factor . This makes the scheme usable for any value of , even when it becomes large.

A second difference is that our simulation scheme can handle simultaneously non-zero drift and nonconstant volatilities, in any dimension.

We also show how to take into account stochastic interest rates.

6.2 Possible improvements

The Monte Carlo scheme presented here can be enhanced in several ways. In particular, one can make different choices for the precise form of functions and . Depending on the specific choice, this can allow to have a simulated path closer to the original process and thus the corrective terms would be smaller. A a simple case, one can factor in some time dependence in parameters.

In addition, the Poisson intensity can depend on time and on the stochastic variables . One could increase it in the regions where the corrective terms are higher and decrease it when they are smaller.

Acknowledgment

We thank Calypso Herrera, Martial Millet and Arnaud Rivoira for useful comments.

References

- Bally and Kohatsu-Higa, (2015) Bally, V. and Kohatsu-Higa, A. (2015). A probabilistic interpretation of the parametrix method. The Annals of Applied Probability, 25(6):3095–3138. arXiv:1510.06909.

- Henry-Labordère et al., (2015) Henry-Labordère, P., Tan, X., and Touzi, N. (2015). Exact simulation of multi-dimensional stochastic differential equations. preprint. arXiv:1504.06107.