A stochastic McKean–Vlasov equation for absorbing diffusions on the half-line

Abstract

We study a finite system of diffusions on the half-line, absorbed when they hit zero, with a correlation effect that is controlled by the proportion of the processes that have been absorbed. As the number of processes in the system becomes large, the empirical measure of the population converges to the solution of a non-linear stochastic heat equation with Dirichlet boundary condition. The diffusion coefficients are allowed to have finitely many discontinuities (piecewise Lipschitz) and we prove pathwise uniqueness of solutions to the limiting stochastic PDE. As a corollary we obtain a representation of the limit as the unique solution to a stochastic McKean–Vlasov problem. Our techniques involve energy estimation in the dual of the first Sobolev space, which connects the regularity of solutions to their boundary behaviour, and tightness calculations in the Skorokhod M1 topology defined for distribution-valued processes, which exploits the monotonicity of the loss process . The motivation for this model comes from the analysis of large portfolio credit problems in finance.

keywords:

[class=MSC]keywords:

arXiv:1605.00669 \startlocaldefs

and

t1First supporter of the project t2Supported by the Heilbronn Institute for Mathematical Research

1 Introduction

Motivation and framework

We prove the weak convergence of a system of interacting diffusions to the unique solution of a non-linear stochastic PDE on the half-line. In our model the diffusions are absorbed at the origin and the proportion of absorbed particles influences the diffusion coefficients, which leads to a description of the limiting system as the solution to a stochastic McKean–Vlasov problem. The motivation for studying the model in this paper is to extend the mathematical framework of [8] for the pricing of large portfolio credit derivatives to include processes whose dynamics are driven by statistics of the entire population. With more complicated interaction terms, the methods in [8] are no longer tractable and so we require new techniques. In particular, it is very difficult to analyse the correlation between pairs of particles in our model (an essential ingredient of [8]) and, from a practical perspective, it is desirable to allow the coefficients of the diffusions to be discontinuous, which presents a further complication.

Portfolio credit derivatives (such as the collateralised debt obligation — CDO) have a pay-off structure which depends on the total notional value of the loss due to default of entities in the portfolio across the lifetime of the product, after a process of partial asset recovery takes place. We will not explore the financial details of these contracts (see [48]), but two important effects the modeller must capture are the intensity of defaults and the tendency for defaults to occur simultaneously. Common modelling approaches include copula-based models, in which the joint probability of default over a fixed time period is modelled directly, and reduced-form models, in which the default rates are modelled as correlated stochastic processes. The model we will consider is a structural model: default times are represented as the threshold hitting times of a collection of correlated stochastic processes. These models were introduced in the context of portfolio derivatives by [31] and [55], and their origins trace back to [5] and [44] for single-name derivatives.

Our general framework is as follows. Suppose we have a collection of defaultable entities and a fixed finite time horizon . Assign the entity a risk process, , called the distance-to-default process, with chosen to be positive independent random variables supported on with common law . Default of the entity is modelled as the first hitting time of zero of the distance-to-default process:

| (1.1) |

The empirical and loss processes then track the spatial evolution of the surviving particles and the proportion of killed particles; defined respectively as

| (1.2) |

Here, denotes the Dirac delta measure of the point . The empirical process takes values in the sub-probability measures on and the loss process takes values in . For , is simply the proportion of the diffusions that take values in at time that have not yet hit the origin by time :

hence we have the relationship

In practice, once the dynamics of have been specified, the model could be used to generate realisations of from which portfolio credit derivatives (options on ) could be priced using Monte Carlo routines. Instead, we will approximate by its limit as . This is known as a large portfolio approximation, an idea first introduced in [51] and now found in several modern frameworks for copula-based models [13, 27, 43] and reduced-form models [22, 23, 45]. We will return to the question of how this approximation is generated in practice after a precise description of the limiting objects and mode of convergence.

Model specification

We will model the processes as correlated diffusions with parameters that are functions of the current proportional loss:

| (1.3) |

Here, are independent standard Brownian motions and the precise conditions on the coefficients are given in Assumption 2.1. In particular we assume is piecewise Lipschitz with finitely many discontinuities in the loss variable . (It is easy, but perhaps not immediate, to show that this collection of processes exists, see Remark 2.2.)

In [8] this model is analysed for the case when the coefficients are constants and it is shown that the sequence of empirical process, , converges to a stochastic limit which can be characterised as the unique solution to a heat equation with constant coefficients and a random transport term driven by the systemic Brownian motion [8, Thm. 1.1]. However, numerical experiments show that the constant coefficient model is too simple to adequately capture the traded prices of CDOs across all tranches simultaneously [8, Sct. 5]. This problem is common for Gaussian models — the tails of the risk processes are too light to produce large losses and so a large correlation parameter is required to generate scenarios in which many defaults occur over a given time horizon [26, 48]. Consequently, different products on the same underlying portfolio may produce different correlation parameters when calibrated to market prices. This phenomenon is known as correlation skew (see Figure 1).

There is a large literature addressing the drawbacks of Gaussian credit models. Examples include the addition of jump processes and heavy-tailed distributions [25, 41, 54], stochastic parameters and inhomogeneity [2, 7] and contagion effects [17, 28, 29]. Close relatives to our framework include [6], in which a jump process is added to the systemic factor, but in a discretised version of the system, and [32], in which the particles are taken to be general diffusions. In [1] the constant coefficient model is studied on the unit interval with absorbing boundaries at 0 and 1 and with an additional multiplicative killing rate as a model for mortgage pools.

Our present approach is inspired by Figure 1. Suppose and are fixed constants and is only a function of . If was piecewise constant across intervals corresponding to the CDO tranches in Figure 1, then an obvious strategy for calibrating to the market prices is to calibrate the first level of to the traded spread of the most junior tranche, fix this value, repeat the calibration procedure for the next most junior tranche spread and continue for all tranches. It is therefore a natural assumption to allow the diffusion coefficients in (1.3) to have finitely many discontinuities. Piecewise Lipschitz coefficients encompass this class of models whilst giving an analytically tractable system.

Main results

The dynamics of an individual distance-to-default process, , are controlled by the population behaviour, hence we have an example of a McKean–Vlasov system — see [50] for an overview. Some applications of these systems include the modelling of large collections of neurons and threshold hitting times for membrane potential levels in mathematical neuroscience [21, 42], the modelling of a large number of non-cooperative agents in mean-field games [10, 12], filtering theory [3, 16] and mathematical genetics [18]. Examples in portfolio credit modelling include [17, 49] in which systems with contagion effects are analysed under their large population limits.

As , we will find that the influence of the idiosyncratic Brownian drivers, , averages-out to a deterministic effect, but that the randomness due to the systemic Brownian motion, , remains present. Hence the system must be characterised as the pair , and we will follow an established strategy to demonstrate the convergence in law of this pair and to characterise the limiting law:

-

(i)

Prove tightness of (in a suitable topology),

-

(ii)

Characterise the limit points as weak solutions of a non-linear evolution equation,

-

(iii)

Prove uniqueness of solutions for this equation,

-

(iv)

Conclude all limiting laws agree, and hence that we have convergence in law.

The mathematical challenge comes from the interaction of the individuals through the boundary behaviour of the population and the discontinuities in the diffusion coefficients. A similar model has recently been studied where the particles interact through the quantiles of the empirical measure [15], however there is no general uniqueness theory for this problem. For a model without systemic noise there is a uniqueness theory in [35]. Discontinuous coefficients have been considered in [14], but only on the whole space and in the deterministic setting. In our model, parameter discontinuities are allowed because the limiting realisations of the loss process are strictly increasing (Proposition 4.6). This implies the infinite system spends a null set of time at points where the discontinuities in the coefficients prevent the application of the continuous mapping theorem (Corollary 5.7). Stochastic PDEs of McKean–Vlasov type are popular tools in the analysis of mean-field games with common noise [11, 36]. In [19, 20] a system of diffusions on the half-line is studied in which each particle undergoes a proportional jump towards zero whenever any of the particles hits the absorbing boundary at zero. The purpose of the model is to describe the self-excitatory behaviour of a large collection of neurons. For small values of the feedback parameter, existence and uniqueness theorems hold for the limiting system. It is shown in [9], however, that for large values of the feedback parameter the limiting system must blow-up (in the sense that no continuous solutions exist) and a complete existence and uniqueness theory in this case remains a challenge.

The topology we will use for establishing tightness of the sequence of laws of is the product topology , where is the topological space of distribution-valued càdlàg processes on , introduced in [40], and is the space of real-valued continuous functions on with the topology of uniform convergence. (Throughout, denotes the space of rapidly decreasing functions and the space of tempered distributions.) It will not be necessary to explain the full details of the construction of , as the proof Theorem 1.1 uses only Theorem 3.2 and Proposition 2.7 of [40], together with facts about the classical M1 toplogy on . The topology is helpful because monotone real-valued processes are automatically tight in , a fact which has been exploited in many other applications (see [40] for references). In our infinite-dimensional setting, the decomposition trick in [40, Prop. 4.2] enables us to exploit the monotonicity of the loss process in proving tightness of the empirical process. Tightness on the product space implies the existence of subsequential limit points, whereby we recover:

Theorem 1.1 (Existence).

Let realise a limiting law of the sequence . Then is a continuous process taking values in the sub-probability measures and satisfies the regularity conditions of Assumption 2.3 and the limit SPDE:

for every and , with probability 1. Furthermore, if the limit point is attained along the subsequence , then converges in law to on the product space .

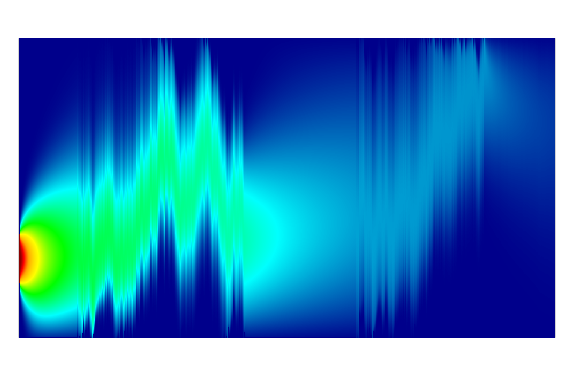

The limit SPDE is a non-linear heat equation with stochastic transport term driven by the systemic Brownian motion (see Figure 2 for an example with an exaggerated correlation change), and the space of test functions, , encodes the Dirichlet boundary conditions. In the limit, the idiosyncratic noise averages-out to produce the diffusive evolution equation. The intuition for this effect is explained easily in Section 3, however a full proof of Theorem 1.1 requires more technical details and is given in Section 5. Several estimates involving purely probabilistic arguments are presented in Section 4, where a key result is Proposition 4.6 which shows (in an asymptotic sense) that over any non-zero time interval the system must lose a non-zero proportion of mass, and hence any limiting loss process is strictly increasing.

With Theorem 1.1 established, demonstrating the full weak convergence of is a matter of proving uniqueness of solutions to the limit SPDE:

Theorem 1.2 (Uniqueness/Law of large numbers).

Let satisfy Assumption 2.1. Suppose that realises a limiting law of and that satisfies Assumption 2.3. If and solve the limit SPDE in Theorem 1.1 with respect to and , then with probability 1

Hence there exists a unique law of a solution to the limit SPDE on and converges weakly to this law. Furthermore, if realises the unique law, then converges in law to on , where .

Remark 1.3 (Strong solutions).

Remark 1.4.

(Density) In Corollary 7.4 we show that has a density process such that for all and . It is then instructive to write the limit SPDE formally as

To prove Theorem 1.2 (Section 7) we use the kernel smoothing method from [8], which is a technique for mollifying potentially exotic solutions to the limit SPDE in order to work with smooth tractable objects, at the expense of a small approximation error. The technique was used on the whole space in [37, 38]. In [8] the approximation error is controlled in the space and there the key quantity to control is the second moment of the mass near the origin: , for a candidate solution . This approach succeeds because the quantity can be written in terms of the law of a two-dimensional Brownian motion in a wedge, for which explicit formulae are available. In that case the kernel smoothing method can be used to give a precise description of the regularity of the solution [39]. As the particle interactions in our model are more complicated, however, these explicit formula are no longer available. Although we are able to show that the unique solution to the limit SPDE has a density in (Corollary 7.4), which is an auxiliary result towards Theorem 1.2, that method cannot be used to fully establish uniqueness as it relies on a crude upper bound for which neglects the effect of the absorbing boundary (Remark 7.5). Our solution to this problem is to adapt the kernel smoothing method to the dual of the first Sobolev space, which then only requires us to control the first moment (Section 6). This is an easier quantity to estimate as only individual particles need to be studied and not pairs of particles, hence we do not need to consider the complicated correlation between particles (see Propositions 4.4 and 5.6).

We must also deal with discontinuities in the coefficients of the limit SPDE and here the strict monotonicity of the limiting loss processes is again important. Our strategy is to prove uniqueness up to the first time the level of the loss reaches a discontinuity point of the coefficients, whereby continuity allows us to propagate the argument onto the next such time interval. With a strictly increasing loss process and only finitely many discontinuities, this argument terminates after finitely many iterations, whereby we have uniqueness on the whole time horizon .

Remark 1.5 (Pathological ).

We cannot choose arbitrarily and expect Theorem 1.2 to hold. As an example, let , and

For , is supported on , hence behaves as the basic constant correlation system with , which we denote . Therefore converges weakly to as , hence there is a distinct limit point for every prime, so weak convergence fails for this example.

In Section 9 we recast our results as a stochastic McKean–Vlasov problem (with randomness from ) and this shows that can be written as the conditional law of a single tagged particle:

Theorem 1.6 (Stochastic McKean–Vlasov problem).

Let be a strong solution to the limit SPDE (Remark 1.3). For any independent Brownian motion, , there exists a continuous real-valued process, , satisfying

(Here, has law and is independent of all other random variables.) Furthermore, the law of is unique.

Returning to the question of applying our model, regarding a portfolio credit derivative as an option on the loss process, , with some payoff function, , the main practical question is how to accurately estimate . This comes in two parts: we must first generate an approximation to (through ) to a given level of precision for a fixed Brownian trajectory and then we must combine such estimates into a random sample. In Section 10 we give an outline of a discrete-time algorithm for approximating the system and some potential variance reduction techniques. We leave the tasks of checking the benefits and correctness of these methods as open problems. A number of potential modifications to the model are also stated, along with their corresponding mathematical challenges.

Overview

In Section 2 we state the main technical assumptions on the model parameters and review their purpose. In Section 3 we derive the evolution equation satisfied by the empirical measure of the finite system, which gives a heuristic explanation for arriving at the limit SPDE in Theorem 1.1. In Section 4 several probabilistic estimates are derived for the finite system and these are applied in Section 5 to give a proof of Theorem 1.1. In Section 6 we describe the kernel smoothing method, which is the main tool for the proof of Theorem 1.2 in Section 7. In Section 8 several technical lemmas are presented which are used to in Section 7, but which are deferred for readability. In Section 9 we use our results to give a short proof of Theorem 1.6. In Section 10 we outline an algorithm for simulating the solution to the limit SPDE and discuss open problems relating to this and to potential model extensions.

2 Notation and assumptions

The purpose of this section is to lay out the technical definitions omitted in the introduction and to explain their purpose.

Assumption 2.1 (Coefficient assumptions).

Let , and be the coefficients in (1.3) and be the common law of the initial values of the distance-to-default processes introduced above (1.1). We assume that we have a sufficient large constant, , such that all the following hold:

-

(i)

(Initial condition) The probability measure is supported on , has a density and satisfies

for every . (Note: implies as .)

-

(ii)

(Spatial regularity) For all fixed and , with

for all , , and ,

-

(iii)

(Non-degeneracy) For all , ,

-

(iv)

(Piecewise Lipschitz in loss) There exists such that

whenever , and both for some ,

-

(v)

(Integral constraint) .

Remark 2.2 ( well defined).

To see that we can find satisfying (1.3) notice that initially , so we can find diffusions satisfying (1.3) up to the first time one of the diffusions hits the origin (i.e. with coefficients of the form ) — notice that the coefficients are globally Lipschitz by (ii) of Assumption 2.1, so standard diffusion theory applies. At this stopping time , and so the process can be restarted as a diffusion with coefficients . This gives a solution up to the first time two particles have hit the origin. Repeating this argument gives the construction of .

Condition (i) ensures that limiting realisations of the system satisfy the regularity conditions in Assumption 2.3, as required for Theorem 1.1. The tail assumption and boundary behaviour of are used in Proposition 4.4 and 4.5 to show that inherits the corresponding properties at times , and this is transferred to limit points by Proposition 5.6.

The boundedness assumption on the coefficients, given by the case in condition (ii), is used many times throughout this paper. The cases and are used in Lemma 4.1 and 4.2 to relate the law of to that of a standard Brownian motion, and in Lemma 8.1 and 8.2 to interchange coefficients and measures in the proof of Theorem 1.2.

Condition (iii) implies that there is always a diffusive effect acting on the system, and this ensures that the limiting system does not become degenerate. If or then the particles are completely dependent and move according to a drift term given by and . The assumption that is bounded away from 1 is used directly in the proof of Theorem 1.2 in (7.2) and (7.7).

Condition (v) is purely a technical assumption to ensure that the drift coefficient, , in Lemma 4.1 is uniformly bounded by a deterministic constant.

Finally, we will remark on the specific form of and . From (1.3) we can write the dynamics of a single particle as

where is a Brownian motion. Although the are coupled through , this representation allows us to relate the law of an individual particle to a standard Brownian motion as in Lemmas 4.1 and 4.2, since is bounded and is independent of . A second advantage of the taking and in this form is that the pairwise correlation between particles is purely a function of , and so is the same for all pairs. This is explicitly made use of in the construction of the time-change defined in (4.8), and there it is again important that the correlation function is bounded strictly away from 1, so that the system can be compared to a standard multi-dimensional Brownian motion.

Below are the constraints we place on solutions to the limit SPDE in Theorem 1.2 to ensure that we have uniqueness. As Theorem 1.1 indicates, these conditions are natural in the sense that all limit points of the finite system satisfy them.

Assumption 2.3 (Regularity conditions).

Let be a càdlàg process taking values in the space of sub-probability measures on . The regularity conditions on are

-

(i)

(Loss function) The process defined by is non-decreasing at all times and is strictly increasing when ,

-

(ii)

(Support) For every , is supported on ,

-

(iii)

(Exponential tails) For every

-

(iv)

(Boundary decay) There exists such that

-

(v)

(Spatial concentration) There exists and such that

It is essential that limit points satisfy condition (i) in order to apply the continuous mapping theorem to recover the limit SPDE for limit points (Corollary 5.7). There, strict monotonicity ensures that there are only finitely many such that for some , and hence that this set of times is negligible in the limit. Knowing that is monotone also allows us to split into consecutive intervals such that in the interval , and this argument is used in the uniqueness proof in Section 7 (Case 2).

Condition (ii) is natural since is supported on by construction. However, it is also convenient to take our test functions, , to be supported on , hence (ii) is needed to rule out pathological solutions that have support on the negative half-line and that would otherwise break the uniqueness claim.

3 Dynamics of the finite particle system

This section introduces the empirical process approximation to the limit SPDE from Theorem 1.1 and explains the intuition behind the convergence of . Throughout, we will drop the dependence of the coefficients on the time, space and loss variables and use the following short-hand when it is safe to do so:

Remark 3.1 (Short-hand notation).

For fixed , when there is no confusion, we may use the functional notation

Proposition 3.2 (Finite evolution equation).

For every , and

where we have the idiosyncratic driver

Proof.

Apply Itô’s formula to to obtain

If , then

| (3.1) |

Substituting this expression into the left-hand side above, summing over and multiplying by gives the result. ∎

Remark 3.3.

We need to ensure that our test functions satisfy so that equation (3.1) is valid.

Since the idiosyncratic noise, , is a sum of martingales with zero covariation, the process converges to zero in the limit as . This explains why we arrive at the limit SPDE in Theorem 1.1.

Proposition 3.4 (Vanishing idiosyncratic noise).

For every

Proof.

Since and are bounded, the result follows from Doob’s martingale inequality and the fact that

∎

The whole space process

In the proceeding sections it will be useful to work with the process defined by

| (3.2) |

which is a probability-measure valued processes on the whole of . Clearly it is the case that

| (3.3) |

Since is not affected by the absorbing boundary, from the work in Proposition 3.2 it follows that satisfies the same evolution equation as , but on the whole space. This is encoded through the test functions:

Proposition 3.5 (Evolution of ).

For every , and

where

4 Probabilistic estimates

Here we collect the main probabilistic estimates used in later proofs. The reader may wish to skip this section and use it only as a reference. We begin by noting the following simple result, which is just a consequence of the fact that are identically distributed: for any measurable , and

| (4.1) |

Under , is a diffusion and with Lemmas 4.1 and 4.2 we are able to estimate (4.1) for relevant choices of by relating the law of to that of standard Brownian motion. Specifically, in Corollary 4.3 and Propositions 4.4 and 4.5 we show that satisfies the corresponding estimates to those in Assumption 2.3 (iii), (iv) and (v), which is of direct use in Proposition 5.6 when we take a limit as . In Propositions 4.6 and 4.7 we prove two estimates for which (4.1) is not helpful. These results require us to express the quantities of interest in terms of independent particles to show that certain events concerning the increments in the loss process are asymptotically negligible.

Lemma 4.1 (Scale transformation).

Define by

and . Then and where is the Brownian motion

and the drift coefficient, , is given by

which is uniformly bounded (in and ).

Proof.

Straightforward application of Itô’s formula coupled with Assumption 2.1). ∎

Lemma 4.2 (Removing drift).

For every , there exists such that

where is the marginal law of a killed Brownian motion at time with initial distribution and is as defined in Lemma 4.1. Likewise, if is the marginal law of the Brownian motion without killing at the origin and with the same initial distribution

Proof.

Let be as in Lemma 4.1, then is also the first hitting time, , of 0 by so

| (4.2) |

Apply Girsanov’s Theorem with the change of measure

then under , is a standard Brownian motion with , and, for any and , Hölder’s inequality gives

for some constant as is uniformly bounded. Applying this bound to (4.2) gives

The result is then complete by taking . The case involving follows by dropping the dependence on . ∎

The following result is a simple consequence of Lemma 4.2 and controls the expected mass concentrated in an interval.

Corollary 4.3 (Spatial concentration).

For every there exists such that

for all and .

Proof.

Boundary estimate

A sharper application of Lemma 4.2 gives control of the concentration of mass near the origin. Notice the stronger rate of convergence due to the absorption at the boundary:

Proposition 4.4 (Boundary estimate).

There exists and such that as

where the ’s are uniform in and .

Proof.

Let be as in Lemma 4.2. The heat kernel for a Brownian motion absorbed at the origin is

| (4.3) |

for . By using the bounds and

which follows from the simple estimate , for an arbitrary function we have, writing , that

where is a numerical constant. By Assumption 2.1(i) we have a constant such that

Since the function

is maximised at , we have the bound

Taking gives

since as (recall Assumption 2.1(i)). The result is complete by applying Lemma 4.2 and noting that . ∎

Tail estimate

A similar analysis applies for the decay of the mass that escapes to infinity.

Proposition 4.5 (Tail estimate).

For every , as

Loss increment estimate

So far the probabilistic estimates we have seen are consequences of the behaviour of the first moment of the diffusion processes. The next two estimates require knowledge of the correlation between particles and so are harder to prove. Heuristically, the first result shows that over any non-zero time interval a non-zero proportion of particles hit the absorbing boundary. Later in Proposition 5.6 this result will directly imply that limiting loss functions are strictly increasing whenever there is a non-zero proportion of mass remaining in the system.

Proposition 4.6 (Asymptotic loss increment).

For all , (such that ) and

Proof.

Begin by noticing that, for any , if and , then . By applying Markov’s inequality and Proposition 4.5 we get the bound

Therefore fix , for , to arrive at

| (4.4) |

We now concentrate on the first term in the right-hand side above with , and fixed. Let denote the random set of indices

If , then , so by conditioning on (which is -measurable)

| (4.5) |

and

| (4.6) |

To estimate the right-hand side of (4.6) take as in Lemma 4.1 and define for . By Assumption 2.1, there exists a constant such that for all . Returning to (4.6), since if and only if , we have

From the bound , for , where

we obtain

From Assumption 2.1 , so we have such that

| (4.7) |

Our next step is to remove the dependence on the process in (4.7). To do this we split the probability on the event to get

Since is a martingale, this final probability is as , by Doob’s maximal inequality.

We have reduced the problem far enough to apply a time-change in order to extract the independence between the particles. To this end, conditioned on the event , define

| (4.8) |

then , where , is an -valued standard Brownian motion, therefore

By Assumption 2.1, , hence

where is a collection of i.i.d. standard normal random variables and are further numerical constants. By symmetry, this final probability depends only on , hence

Returning to (4.5) we now have

so the law of large numbers gives

| (4.9) |

where and where we have substituted back into (4.4). This inequality holds for all and , with the term denoting convergence as . We now choose the free parameter to be a function of , specifically

This guarantees that as , but also

as , where we have used the well-known Gaussian estimate , for and the c.d.f. and p.d.f. of the standard normal distribution. Using this choice of in (4.9) completes the result. ∎

The following is a partial converse of the previous result in that it shows that the system cannot lose a large amount of mass in a short period of time. It will be used in Proposition 5.1 to verify a sufficient condition for the tightness of .

Proposition 4.7.

For every and

Proof.

With fixed, we have

| (4.10) | ||||

where the second line uses Markov’s inequality and (4.1) and the third line uses Proposition 4.4 for and Assumption 2.1 (i) for . Define to be the random set of indices

then conditioning on gives

| (4.11) |

The conditional expectation in the summand can be bounded by

With fixed, define the process , then

for a numerical constant. As for in Lemma 4.1, we have

where is uniformly bounded by Assumption 2.1, therefore we can find such that

By applying the time-change argument from (4.8) and using Markov and Doob’s maximal inequality we have

where are independent standard Brownian motions, and is a numerical constant.

Returning to (4.11) and noticing the the right-hand side above is maximised when

The law of large numbers and the distribution of the minimum of Brownian motion gives

| (4.12) |

provided , where is the normal c.d.f. We now make the choice

which guarantees

as . Hence the result follows from (4.10), (4.11) and (4.12). ∎

5 Tightness of the system and existence of solutions; Proof of Theorem 1.1

We will now use the results from Section 4 to prove Theorem 1.1, which follows directly from the combination of Propositions 5.5, 5.6 and 5.11. We first establish tightness of the sequence of the laws of (Proposition 5.1) using the framework of [40]. The reader is referred to that article for the technical definitions of the topological spaces used in this section. Once we have tightness we can then extract limit points of the sequence , and Propositions 5.3, 5.5 and 5.6 are devoted to recovering the properties of the limiting laws from the probabilistic properties of the finite system. Finally, the limit points are shown to satisfy the evolution equation in Theorem 1.1 via a martingale argument (Proposition 5.11) and care needs to be taken over the discontinuities in the coefficients of the limit SPDE (Corollary 5.7).

Proposition 5.1 (Tightness).

The sequence is tight on the space , hence is tight on the space , where is the space of real-valued continuous paths with the topology of uniform convergence.

Remark 5.2.

We note that a version of this result is given in [40, Thm. 4.3] for the case , .

Proof.

The second statement follows from the first and the fact that joint tightness is implied by marginal tightness.

By [40, Thm. 3.2] it suffices to show that is tight on for every . To prove this we verify the conditions of [53, Thm. 12.12.2], the first of which is trivial because is a sub-probability measure so . Hence we concentrate on condition (ii), which is implied by [40, Prop. 4.1], therefore we are done if we can find such that

| (5.1) |

for all , and , where

and if

| (5.2) |

for every .

With as defined in (3.2), the decomposition in [40, Prop. 4.2] and Markov’s inequality give

For any , from Hölder’s inequality we obtain

where is the Lipschitz constant of . By Assumption 2.1 and the Burkholder–Davis–Gundy inequality [46, Thm. IV.42.1], the final expectation above is uniformly in . Therefore we have (5.1) with and .

Now consider the first supremum in (5.2). By again using the decomposition from [40, Prop. 4.2], that is , we have

The first term on the right-hand side vanishes as by the same work as for (5.1) and the second term vanishes by Proposition 4.7. Therefore

and likewise for , so we have (5.2), which completes the proof. ∎

Limit points

Tightness of ensures that the sequence is relatively compact [40, Thm. 3.2], hence every subsequence of has a further subsequence which converges in law. To avoid possible confusion about multiple distinct limit points, we will denote by any pair of processes that realises one of these limiting laws. Using to denote convergence in law, we have

as , for some subsequence . Establishing full weak convergence is equivalent to showing that there is exactly one limiting law.

So far we have that any limiting empirical process, , is an element of . The following result recovers as a probability-measure-valued process:

Proposition 5.3.

Let realise a limiting law. Then is a sub-probability measure supported on for every , with probability 1.

Remark 5.4.

Technically, what we will show is that, for every , agrees with a sub-probability measure on and from now on we associate with this measure.

Proof of Proposition 5.3.

Take . Fix , then by [40, Prop. 2.7 (i)] on . Lemma 13.4.1 of [53] gives

therefore the portmanteau theorem [4, Thm. 2.1] gives

with the final equality due to being a sub-probability measure. (The supremum over ensures that the following argument holds for all simultaneously.) By a similar analysis we have that is non-negative when is non-negative and when is supported on . Hence, is a positive linear functional on , so extends to a positive linear functional, , on the space, , of continuous and compactly support function on with the uniform topology. The Riesz representation theorem [47, Thm. 2.14] then implies that, for every , there exists a regular Borel measure, , such that

Associating and gives the result. ∎

Now that it is safe to regard a limit point, , as taking values in the sub-probability measures, it makes sense to introduce the limit loss process as . Of course we would like to know that on , however the function is not an element of , so [40, Prop. 2.7] does not allow us to deduce this fact from the continuous mapping theorem. To remedy this we must work slightly harder:

Proposition 5.5 (Convergence of the loss process).

Suppose that converges weakly to and that . Then converges weakly to on .

Proof.

For a contradiction suppose that the weak convergence does not hold. Since is increasing, and we have Proposition 4.7, the conditions of [53, Thm. 12.12.2] are satisfied and so is tight on , and because marginal tightness implies joint tightness, is also tight. By taking a further subsequence if needed, assume that for some .

Notice from [53, Thm. 12.4.1] that the canonical time projection from to is only continuous at times for which its argument does not jump. That is, for every , is continuous at if and only if . To this end, define , which we know by [4, Sec. 13] is cocountable in . For define to be any function satisfying on , on and otherwise. By [40, Prop. 2.7(i)] , and define . Take

which is cocountable (since it is the countable intersection of cocountable sets) and so is dense in .

Since and is dense in , if and are not equal in law on , then it must be the case that not all of the finite-dimensional marginals of and on are equal in law. It is no loss of generality to assume that there exists , , bounded and Lipschitz and such that

By Proposition 4.5

as , therefore the Lipschitz property of gives

but , so

Since is a probability measure (recall from Proposition 5.3 that is supported on ), so taking gives the required contradiction. ∎

We are now in a position to verify the first half of Theorem 1.1, which is that any limit point must satisfy the regularity conditions from Assumption 2.3:

Proposition 5.6 (Regularity conditions).

If realises a limiting law of , then satisfies Assumption 2.3.

Proof.

Firstly, takes values in the sub-probability measures by Proposition 5.3, and that result also gives Assumption 2.3 (ii).

For conditions (iv) and (v) of Assumption 2.3, let be any finite open interval. For , take any satisfying on , on and otherwise. Taking and noting that in by [53, Thm. 11.5.1] and that these integrals are uniformly bounded (by ), we have

For both conditions (iv) and (v) we have bounds on the right-hand side which are independent of (Propositions 4.3 and 4.4), and then the conditions hold by sending . For condition (iii) we have , so . However, for with , the above work gives

so sending and (using the dominated convergence theorem) gives the result.

It remains to show (i) of Assumption 2.3. First we prove that is non-decreasing. By [4, Sec. 13] there is a (deterministic) cocountable set, , on which in . So for in [4, Thm. 2.1] implies

and hence is non-decreasing on . But is dense in and càdlàg, so we conclude is non-decreasing on . To deduce the strict monotonicity, Proposition 4.6 implies

whenever and sending gives the required result. ∎

So far we have seen no reason why it is important should be strictly increasing whenever the mass in the system is not completely depleted (). The following result is such an example and shows why this condition is needed to pass to a weak limit. The result will be applied directly in the next subsection.

Corollary 5.7 (Weak convergence of integrals).

Fix and . Let be equal to either , or . Define to be all elements in that take values in the sub-probability measures and let . Then the map

is continuous (with respect to the product topology on ) at all point which satisfy the conditions of Assumption 2.3. Consequently, if then

Proof.

For short-hand we will denote this map . Suppose that in , then

| (5.3) |

We will control and separately.

Begin by fixing and . Take sufficiently large so that for all , and , which is possible because is bounded and is rapidly decreasing. Let be a mollifier and set , then we have

Since and , so the first term vanishes as . We can then split the second term as

and here the first term vanishes as by [24, App. C, Thm. 6] since is compact and the second term can be guaranteed to be less than for sufficiently large. Taking gives .

To deal with in (5.3), first notice that since

Define , where we recall Assumption 2.1 condition v. For , let . Define to be all such that , which we know is a cocountable set [53, Cor. 12.2.1]. For , in , so if then eventually for some , whence by Assumption 2.1 condition (iv). We conclude

where is a numerical constant due to Assumption 2.1. This completes the result. ∎

Martingale approach

We complete this section and the proof of Theorem 1.1 by showing that the limit SPDE holds for a general limit point. For this we will use a martingale argument and we introduce three processes:

Definition 5.8 (Martingale components).

For a fixed test function , define the maps:

-

(i)

,

-

(ii)

,

-

(iii)

,

These processes capture the dynamics of the limit SPDE:

Lemma 5.9 (Martingale approach).

Proof.

The hypothesis gives

hence

for every , which completes the proof. ∎

Our strategy is to take a limit in Proposition 3.2 and apply weak convergence. First notice that we have:

Lemma 5.10.

For every fixed , there exists a deterministic cocountable subset of on which

Furthermore, these sequences are uniformly bounded (for fixed ).

Proof.

Note that all the above processes are uniformly bounded (for fixed ) since is a probability measure. The result then follows by Corollary 5.7. ∎

Proposition 5.11 (Evolution equation).

Proof.

Fix and let be the cocountable set of times on which we have the conclusion of Lemma 5.10. To show that is a martingale, it is enough to show that, for any arbitrary , , and continuous and bounded, that the map defined by

satisfies . By Lemma 5.10 and the boundedness and continuity of the ’s

However, from Proposition 3.2, we have that is a martingale since

| (5.4) |

therefore and so is a martingale.

For , define the map

By applying Itô’s formula to (5.4), we have

So be the boundedness of the and Proposition 3.4

so and is a martingale. The work for follows similarly, so we omit it. The result is then complete by Lemma 5.9, and the continuity of follows by the fact that the right-hand side of the evolution equation in Theorem 1.1 is continuous. ∎

6 The kernel smoothing method

The kernel smoothing method converts a measure into an approximating family of functions and, by establishing uniform results on the functions, enables us to show the existence of a density for the measure. In the next section we will use this to prove Theorem 1.2. Let be a finite signed-measure and the Gaussian heat kernel

Begin by noting the familiar fact that can be approximated by its convolution with : For every continuous and bounded

| (6.1) |

as , and

| (6.2) |

is a function. We will sometimes abuse notation and write when is a function. With denoting the usual inner product, we have

| (6.3) |

Our first observation is that is a contraction on :

Proposition 6.1 (Contraction).

Let . Then , where is the norm on .

Proof.

The Cauchy–Schwarz inequality gives

The first integral on the right-hand side integrates to one, then integrating over completes the proof. ∎

We now give a condition which shows how to recover the existence of a density via kernel smoothing.

Proposition 6.2.

Suppose that is a finite signed measure and

Then has an density, i.e. there exists such that , for every . Furthermore in .

Proof.

Smoothing in and the anti-derivative

The material above will be used to establish a preliminary regularity result (Proposition 7.1) in Section 7. However, for the main uniqueness proof we will work in a space of lower regularity and on the half-line. Recall that the first Sobolev space with Dirichlet boundary condition, , is defined to be the closure of under the norm

The dual of will be denoted by and its norm by

This is a natural space for us to work in due to the following.

Proposition 6.3.

If is a finite signed measure, then .

Proof.

First observe that , for every . Morrey’s inequality [24, Sec. 5.6, Thm. 4] gives a universal constant, , such that , and this completes the proof. ∎

To work on the half-line we will use the absorbing heat kernel defined, as in the proof of Proposition 4.4, by

| (6.4) |

and define

Notice that for every , so is an element of , and also notice that . For to approximate , we need to be supported on :

Proposition 6.4.

If is supported on , then

as , for every continuous, bounded and supported on :

Proof.

To access the norm, we will use the anti-derivative defined by

Notice that , and if is also integrable, then too. The result we will use in Section 7 is the following.

Proposition 6.5.

If , then .

Proof.

First notice that for fixed

so is integrable and hence is well-defined. Integration by parts gives

for . Therefore by Proposition 6.4 we have

which gives the result. ∎

7 Uniqueness of solutions; Proof of Theorem 1.2

In this section we will prove Theorem 1.2. Therefore take , and as in the statement with along some subsequence. Let and . The first step will be to show that has some regularity (Proposition 7.1), which is due to a comparison with from (3.2) and from the dynamics of Proposition 3.5. We then use this fact, along with energy estimates in , to complete the proof. Several technical lemmas are used throughout this section, however, to aid readability, their full statements and proofs are deferred until Section 8.

-regularity

The result we will prove in this subsection is the following:

Proposition 7.1 (-regularity).

With as introduced at the start of Section 7,

We would like to work with some process defined analogously to (3.2) that would satisfy the bound , for every and . At this stage, however, we are dealing only with weak limit points, so must recover the required process through a limiting procedure on :

Lemma 7.2 (Whole space SPDE).

Proof.

Notice that in Proposition 5.1 we have carried out sufficient work to prove is tight on , hence is tight. We can therefore conclude that there is a subsequence for which converges in law. Any realisation of this limit must have a marginal law that agrees with the law of . As the work in Propositions 5.3 and 5.11 is unchanged for in place of , we conclude that is probability-measure-valued and, due to Proposition 3.5, that satisfies the limit SPDE on the whole space. Finally, we note that for every with we have , therefore

for every , by [4, Thm. 2.1]. This inequality holds for all by the continuity of and (which follows from being solutions to the limit SPDE) and suffices to give the required dominance. Condition (v) of Assumption 2.3 is satisfied by because the proof of Corollary 4.3 uses only the behaviour of . Likewise, the two-sided tail estimate is satisfied due to the same work as in Proposition 4.5. ∎

Our strategy is to use the kernel smoothing method with -energy estimates on the SPDE satisfied by . This is possible because we do not have to take boundary effects into account, which is the main difficulty in the uniqueness proof that will follow. The following lemma relates to Proposition 7.1.

Proof.

Since , . We would first like to deduce that this fact also holds for , but since the map might not be continuous on , more care must be taken.

As an immediate consequence of the final part of the previous proof and of the forthcoming proof of Proposition 7.1, we have the existence of a density process for :

Corollary 7.4 (-regularity).

With probability 1, for every there exists such that is supported on and is a density of , i.e.

Furthermore , with probability 1.

Remark 7.5.

We might hope that this argument could be used to prove uniqueness. However, notice that we have no control over , as all we have are upper bounds on solutions.

Proof of Proposition 7.1.

Fix and set the function into the SPDE from Lemma 7.2 to get

with the short-hand from Remark 3.1. We would like to move the diffusion coefficients out of the integral against , and to do so we use Lemma 8.2:

where is as defined in Lemma 8.2 and the dependence on is omitted for clarity. Applying Itô’s formula to gives

Our strategy is to integrate over , take a supremum over and then take an expectation over the previous equation. For the first task we appeal to Lemma 8.2, Lemma 8.3 and Young’s inequality with free parameter to obtain

where is a constant depending only on . Considering the third line, by Assumption 2.1 it is possible to choose small enough so that

| (7.2) |

therefore

Using Lemma 8.5 to take a supremum over and then expectation gives

where is a numerical constant.

Taking as over the previous inequality and applying Proposition 6.1 (to ) and Lemma 8.2 yields

Hence for we have . The proof is completed by propagating the argument onto by the same work as above but started from , rather than . This gives

and so in general

Since the largest such we need to take is , the simple bound

completes the proof. ∎

Resuming the uniqueness proof

Returning to proof of Theorem 1.2, notice that for a fixed , the function from (6.4) is an element of . Setting into the SPDE for gives

and by applying Lemma 8.6

To introduce the anti-derivative we integrate the above equation over and apply Lemma 8.3 to switch the time and space integrals. (Note: Lemma 8.3 is stated for , however the proof only relies on the tail bound from Assumption 2.3 condition (iii), which is satisfied by and .) We arrive at

which, after rewriting using the notation from Lemma 8.1, becomes

| (7.3) | ||||

We will now introduce the simplifying notation to denote any family of -valued processes, , satisfying

Thus a formal linear combination of terms is of order . Therefore (7.3) can be written (using Lemma 8.1) as

| (7.4) | ||||

and we claim that the integrands in the final two terms are also of order . This claim is in fact the critical boundary result from [8], but here we only need first moment estimates:

Lemma 7.6 (Boundary estimate).

We have

hence and .

Proof.

Begin by noting that

for a free parameter and a universal constant. Squaring and integrating over gives

with another numerical constant. Condition (iv) of Assumption 2.3 and the fact that , since is a sub-probability measure, allows us to write

which vanishes if we choose to satisfy

and this completes the proof. ∎

With Lemma 7.6, we can now reduce (7.4) to

| (7.5) | ||||

and this equation is also satisfied by , as so far all we have used is Assumption 2.3. Writing and , taking the difference of (7.5) for and yields

where is as in Lemma 8.1, but with replaced by . Applying Itô’s formula to the square gives

| (7.6) | ||||

Note that the initial condition for this equation is zero because and have the same initial condition.

Since the work in establishing the bounds in Lemma 8.3 only uses the tail estimate (iii) of Assumption 2.3, they remain valid and so, together with Lemma 8.7, the stochastic integrals in (7.6) are martingales for fixed and . Therefore first taking an expectation and then integrating over and using Young’s inequality with free parameter produces a constant such that

| (7.7) | ||||

where the terms involving have collapsed to order . Also notice that (7.7) remains valid if is a stopping time.

If it was the case that , then by Proposition 6.2 we would have on , and so would have completed the proof for this value of . It is therefore no loss of generality to assume that this value is bounded away from zero for all sufficiently small. Then by taking we can find a positive value such that

| (7.8) | ||||

for constant. We now want to introduce a comparison between solutions in the terms, and to do so we consider two cases.

Case 1: Globally Lipschitz coefficients

First consider the simpler case where and are Lipschitz in the loss variable, rather than piecewise Lipschitz. Therefore we have , so the inequality in (7.8) becomes

with constant.

To bound the second term above, we introduce the stopping times

From Proposition 7.1 we know that as , with probability 1. Since (7.7) is valid for stopping times we have

By using the integrating factor we obtain

and applying Fatou’s lemma and Propositions 6.3 and 6.5 gives

where .

Finally we apply Lemma 8.8 to the above inequality to reintroduce to the right-hand side. With fixed we have

where does not depend on (but does depend on ). Now fix so that we have

with independent of . By using the integrating factor we deduce

so setting and sending gives . Therefore on , and since we have Theorem 1.2 in Case 1.

Case 2: Piecewise Lipschitz coefficients

To extend the argument to the general case, we use a stopping argument and consider the system only on time intervals where the loss processes are in the same interval — recall Assumption 2.1.

Define the stopping times

and . For the reason immediately proceeding (7.6), the argument in Case 1 can be replicated on by replacing by , since before , the coefficients can be compared using the Lipschitz property on . Therefore we conclude for , which forces for and thus .

8 Technical lemmas

This section collects all the technical lemmas that were used in Section 7, and should be read only as a reference.

Lemma 8.1.

Let where is one of , or and . Define the error term

Then

Proof.

Lemma 8.2.

Let where is one of , or and . Define the error term

Then

and there exists a numerical constant such that

Proof.

Interchanging differentiation and integration with respect to gives

By bounding with the second-order derivative and using gives

We therefore have the same order of as in Lemma 8.1, so the first result follows by the same work. For the second result, notice that

and . ∎

Lemma 8.3 (Stochastic Fubini).

Proof.

By applying Young’s inequality and concavity of , it suffices to show that

First notice that

where is a polynomial of degree . Since is a probability measure, Hölder’s inequality gives

| (8.3) |

For any value of , the integrand above is bounded (recall that is fixed). Hence it suffices to bound the right-hand side of (8.3) in terms of only for large values of . Splitting the -integral on the region and its complement gives the bound

where and the depend only on and where we have used the tail estimate from Lemma 7.2. This suffices to complete the proof. ∎

Lemma 8.4 (An integration-by-parts calculation).

Let be bounded with bounded first derivatives. Assume also that these functions and their first derivatives vanish at . Then

Proof.

Integration by parts. ∎

Lemma 8.5.

There exists a constant such that

for all .

Proof.

By a similar analysis to (8.3) we know that, for every fixed , the integrand above is a rapidly decaying function of , hence the stochastic integral is a martingale, so the Burkholder–Davis–Gundy inequality [46, Thm. IV.42.1] gives a universal constant, , for which the left-hand side above is bounded by

By Lemma 8.4, this is equal to a constant multiple of

which, by Hölder’s inequality, is bounded by a constant multiple of

The result then follows by applying Young’s inequality with parameter and using the boundedness of the coefficients. ∎

Lemma 8.6 (Switching derivatives).

For all and we have

-

(i)

,

-

(ii)

.

Proof.

An easy calculation. ∎

Lemma 8.7.

For all , and

Proof.

Split the integral

at and its complement to obtain

The triangle inequality completes the result. ∎

Lemma 8.8.

Let , , , and be as in Section 7. For every there exists a constant such that

for all , and , where is a constant that does not depend on .

Proof.

The following result will be used in Section 9.

Lemma 8.9 (Interchanging stochastic integration and conditional expectation).

Suppose we are working on a probability space with filtration and is a standard Brownian motion with natural filtration . Let be a real-valued -adapted process with

Then, with probability 1,

and

for every

Proof.

As we can multiply by , it suffices to take . First, suppose that is a basic process, that is

where are real numbers and is -measurable. Then

and

where we have used the fact that is independent of since and are independent and has independent increments. So the result holds in this case and immediately extends to linear combinations of basic processes. The usual density argument then allows us to extend the result to all required . ∎

9 Stochastic McKean–Vlasov problem; Proof of Theorem 1.6

This section presents a short proof of Theorem 1.6. Take a strong solution to the limit SPDE (Remark 1.3), an independent Brownian motion and define by

(It is possible to find such an by standard diffusion theory, since is given and fixed.) Let be the conditional law of given killed at zero, that is

We will have the existence statement of Theorem 1.6 if we can prove .

Applying Itô’s formula to as in the proof of Proposition 3.2 gives

Take a conditional expectation with respect to by applying Lemma 8.9 (and using that is -measurable) to get

Now, also satisfies this equation, however in both cases the coefficients depend only on . Therefore we can regard as fixed and and as solving the limit SPDE in the special case when coefficients do not depend on the loss-variable. This is a much easier linear problem and Theorem 1.2 is certainly sufficient to conclude , as required.

10 Open problems

We end by giving some open problems arising from our model and its related extensions:

-

(i)

As indicated at the end of Section 1, the most important practical question is how do we numerically approximate from a given realisation of ? This leads to the further questions of how do we combine these approximations to get an estimator for , where is some pay-off function, and how do we calibrate the model to any data on traded prices for options with payoff ?

Our proposed algorithm for the first problem is as follows. Here, we discretise the time variable and treat the outputs of the following subroutines as functions on — in practise we would also need a discretisation scheme for the spatial variable too, but we will not consider that problem here. Fix a precision level and assume we are given a piecewise constant or piecewise linear approximation to a Brownian trajectory to precision at least (generating such a path contributes negligible computational cost in this algorithm) and an initial density . Set . For , form recursively by setting where solves the deterministic linear PDE

(10.1) for and . Set (calculated using some quadrature routine). Our approximation to the density process, , of and the loss process, , are given by piecewise interpolation of and :

where , is the floor of and .

In the case when and are constant and depends only on the loss variable and is given as a piecewise constant interpolation of with precision , the solution to (10.1) can be written explicitly in terms of the Brownian transition kernel. A numerical solution can then be found by quadrature. (This instance of the algorithm was used to produce Figure 2.) If these assumption do not hold, then further approximations may be necessary. In [30] (10.1) is solved (for the constant coefficient case) by finite element methods and the scheme is proven to converge when the system is considered on the whole space. The authors conjecture and provide numerical evidence for a convergence rate for the scheme on the half-line with space-time discretisation. A first open problem is to verify that the piecewise-constant time-discretisation, , above converges in law to the solution of limit SPDE as . A harder problem is to establish the rate of convergence, in some appropriate norm, averaged over realisations of .

Returning to the task of calculating the pay-off , we have the estimator

where are independent standard Brownian motions and denotes the approximation to the loss function using the algorithm above with precision and Brownian trajectory . As the Monte Carlo routine depends on , a natural variance reduction technique is to use multi-level Monte Carlo as in [30]. Another potentially useful technique is to alter the drift coefficient in (1.3) using Girsanov’s theorem to produce a reweighted estimator. In the case when the pay-off function, , is supported on large losses, and hence is sensitive only to rare events, changing the measure to one under which the particles have a large negative drift and multiplying by the appropriate Radon–Nikodym derivative is a form of importance sampling. A simpler observation in this scenario is that if the systemic Brownian motion has a realisation that has followed a largely increasing path on , then although that realisation is likely to contribute little to , the negative of this realisation is likely to give a heavy contribution. Hence the simple antithetic sampling routine in which we draw samples of the common Brownian motion in pairs is a candidate for variance reduction. An open problem is to verify the usefulness of these techniques either numerically or analytically.

-

(ii)

Following on from the previous point, a natural extension to the model is to replace the systemic Brownian motion term in (1.3) with a Lévy process. This would allow the possibility of generating extreme losses. Mathematically we expect to arrive at a non-linear SPDE driven by a Lévy process on the half-line — see, for example, [34].

-

(iii)

Another possibility for generating large systemic losses is to incorporate a contagion term in the particle dynamics along the lines of [19, 20]. For simplicity, consider the model where particles move according to the dynamics

(10.2) with . Whenever a particle hits the origin, every other particle jumps by size towards the boundary. This can begin an avalanche effect where a default causes many other entities to default. Convergence of a finite particle system to a limiting McKean–Vlasov equation is shown in [20], and it is known that for small values of the solution is unique. For large values of the limiting system undergoes a jump, whereby a macroscopic proportion of mass is lost in an infinitesimal period of time. It remains a challenge to prove uniqueness of solutions in this regime and to characterise a critical value of . From our perspective, a natural extension is to consider the system with a common Brownian noise term between particles.

Acknowledgement

The authors thank the anonymous referees for their helpful corrections. We are grateful to Andreas Sojmark for his very thorough reading and suggestions for improvements. SL thanks Christoph Reisinger and Francois Delarue for discussions on this material.

References

- [1] F. Ahmad, B.M. Hambly and S. Ledger. A stochastic partial differential equation model for mortgage backed securities. Preprint 2016.

- [2] L. Andersen and J. Sidenius. Extensions to the Gaussian Copula: Random Recovery and Random Factor Loadings. J. Credit Risk, 1(1):29–70, 2005.

- [3] A. Bain and D. Crisan. Fundamentals of Stochastic Filtering. Springer, New York, 2009.

- [4] P. Billingsley. Convergence of probability measures. Wiley Series in Probability and Statistics: Probability and Statistics. John Wiley & Sons Inc., New York, second edition, 1999. A Wiley-Interscience Publication.

- [5] F. Black and J. Cox. Valuing corporate securities: some effects of bond indenture provisions. J. Finance, 31(2):351–367, 1976.

- [6] K. Bujok and C. Reisinger. Numerical valuation of basket credit derivatives in structural jump-diffusion models. J. Comp. Finance, 15(4):115–158, 2012.

- [7] X. Burtschell, J. Gregory, and J.-P. Laurent. Beyond the Gaussian copula: Stochastic and Local Correlation. J. Credit Risk, 3(1):31–62, 2007.

- [8] N. Bush, B.M. Hambly, H. Haworth, L. Jin, and C. Reisinger. Stochastic Evolution Equations in Portfolio Credit Modelling. SIAM J. Financial Math., 2(1):627–664, 2011.

- [9] M.J. Cáceres, J.A. Carrillo, and B. Perthame. Analysis of non-linear noisy integrate & fire neuron models: blow-up and steady states. The Journal of Mathematical Neuroscience, 1(7), 2011.

- [10] R. Carmona and F. Delarue. Probabilistic Analysis of Mean-Field Games. SIAM J. Control Optim., 51(4):2705–2734, 2013.

- [11] R. Carmona, F. Delarue, and D. Lacker. Mean field games with common noise. http://arxiv.org/abs/1407.6181, 2015.

- [12] J.-F. Chassagneux, D. Crisan, and F. Delarue. A probabilistic approach to classical solutions of the master equation for large population equilibria. http://arxiv.org/abs/1411.3009, 2015.

- [13] U. Cherubini, E. Luciano, and W. Vecchiato. Copula Methods in Finance. The Wiley Finance Series. Wiley, 2004.

- [14] T.-S. Chiang. McKean–Vlasov equations with discontinuous coefficients. Soochow J. Math., 20(4):507–526, 1994.

- [15] D. Crisan, T.G. Kurtz, and Y. Lee. Conditional distributions, exchangeable particle systems, and stochastic partial differential equations. Ann. Inst. H. Poincaré Probab. Statist., 50(3):946–974, 2014.

- [16] D. Crisan and J. Xiong. Approximate McKean–Vlasov representations for a class of SPDEs. Stochastics, 82(1):1–16, 2010.

- [17] P. Dai Pra, W. Runggaldier, E. Sartori, and M. Tolotti. Large porfolio losses: a dynamic contagion model. Ann. Appl. Probab., 19(1):347–394, 2009.

- [18] D. Dawson and A. Greven. Spatial Fleming–Viot models with selection and mutation. Lecture Notes in Mathematics. Springer, 2014.

- [19] F. Delarue, J. Inglis, S. Rubenthaler, and E. Tanré. Global solvability of a networked integrate-and-fire model of McKean–Vlasov type, Ann. Appl. Probab. 25(4):2096–2133, 2015.

- [20] F. Delarue, J. Inglis, S. Rubenthaler, and E. Tanré. Particle systems with singular mean-field self-excitation. Application to neuronal networks, Stochastic Process. Appl. 125(6): 2451–2492, 2015.

- [21] A. De Masi, A. Galves, E. Löcherbach, and E. Presutti. Hydrodynamic limit for interacting neurons. J. Stat. Phys., 158(4):866–902, 2015.

- [22] X. Ding, K. Giesecke, and P. Tomecek. Time-Changed Birth Processes and Multiname Credit Derivatives. Oper. Res., 57(4):990–1005, 2009.

- [23] E. Errais, K. Giesecke, and L.R. Goldberg. Affine Point Processes and Portfolio Credit Risk. SIAM J. Financial Math., 1:642–665, 2010.

- [24] L.C. Evans. Partial Differential Equations. Graduate studies in mathematics. American Mathematical Society, 2010.

- [25] F. Fang, H. Jönsson, C. Oosterlee, and W. Schoutens. Fast valuation and calibration of credit default swaps under Lévy processes. J. Comp. Finance, 14(2):1–30, 2010.

- [26] C.C. Finger. Issues in the Pricing of Synthetic CDOs. J. Credit Risk, 1(1):113–124, 2005.

- [27] R. Frey and A. McNeil. Dependent Defaults in Modes of Portfolio Credit Risk. J. Risk, 6(1):59–92, 2003.

- [28] K. Giesecke, K. Spiliopoulos, R.B. Sowers, and J.A. Sirignano. Large portfolio asymptotics for loss from default. Math. Finance, 25(1):77–114, 2015.

- [29] K. Giesecke and S. Weber. Credit contagion and aggregate losses. J. Econom. Dynam. Control, 30:741–767, 2006.

- [30] M. Giles, C. Reisinger. Stochastic Finite Differences and Multilevel Monte Carlo for a Class of SPDEs in Finance. SIAM J. Financial Math., 3(1):572–592, 2012.

- [31] J. Hull and A. White. Valuing credit default swaps II: modeling default correlations. J. Derivatives, 8(3):12–21, 2001.

- [32] L. Jin. Particle systems and SPDEs with applications to credit modelling. D.Phil Thesis, University of Oxford, 2010.

- [33] I. Karatzas and S.E. Shreve. Brownian Motion and Stochastic Calculus. Graduate Texts in Mathematics. Springer New York, 1991.

- [34] K.-H. Kim. A Sobolev space theory for parabolic stochastic PDEs driven by Lévy processes on -domains. Stochastic Process. Appl., 124(1):440–474, 2014.

- [35] V.N. Kolokoltsov. Nonlinear Diffusions and Stable-Like Processes with Coefficients Depending on the Median and VaR. Appl. Math. Optim., 68:85–98, 2013.

- [36] V.N. Kolokoltsov and M. Troeva. On the mean field games with common noise and the McKean–Vlasov SPDEs. http://arxiv.org/abs/1506.04594, 2015.

- [37] P. Kotelenez. A class of quasilinear stochastic partial differential equations of McKean–Vlasov type with mass conservation. Probab. Theory Related Fields, 102(2):159–188, 1995.

- [38] T.G. Kurtz and J. Xiong. Particle representations for a class of nonlinear SPDEs. Stochastic Process. Appl., 83(1):103–126, 1999.

- [39] S. Ledger. Sharp regularity near an absorbing boundary for solutions to second order SPDEs in a half-line with constant coefficients. Stoch. Partial Differ. Equ. Anal. Comput., 2(1):1–26, 2014.

- [40] S. Ledger. Skorokhod’s M1 topology for distribution-valued processes. Electron. Commun. Probab., 21(1):1–11, 2016.

- [41] F. Lindskog and A. McNiel. Common Poisson Shock Models: Applications to Insurance and Credit Risk Modelling. ASTIN Bulletin, 33(2):209–238, 2003.

- [42] E. Luçon and W. Stannat. Mean field limit for disordered diffusions with singular interaction. Ann. Appl. Probab., 24(5):1946–1993, 2014.

- [43] S. Merino and M.A. Nyfeler. Calculating Portfolio Loss. RISK, pages 82–86, 2002.

- [44] R. Merton. On the pricing of corporate debt: the risk structure of interest rates. J. Finance, 29(2):449–470, 1974.

- [45] A. Mortensen. Semi-Analytical Valuation of Basket Credit Derivatives in Intensity-Based Models. J. Derivatives, 13(4):8–26, 2006.

- [46] L.C.G. Rogers and D. Williams. Diffusions, Markov processes, and martingales. Vol. 2. Cambridge Mathematical Library. Cambridge University Press, Cambridge, 2000. Itô calculus, Reprint of the second (1994) edition.

- [47] W. Rudin. Real and complex analysis. McGraw-Hill Book Co., New York, third edition, 1987.

- [48] P.J. Schönbucher. Credit Derivatives Pricing Models: Models, Pricing and Implementation. The Wiley Finance Series. Wiley, 2003.

- [49] K. Spiliopoulos, J.A. Sirignano, and K. Giesecke. Fluctuation analysis for the loss from default. Stochastic Process. Appl., 124(7):2322 – 2362, 2014.

- [50] A.-S. Sznitman. Topics in propagation of chaos. In Paul-Louis Hennequin, editor, Ecole d’Eté de Probabilités de Saint-Flour XIX – 1989, volume 1464 of Lecture Notes in Mathematics, chapter 3, pages 165–251. Springer Berlin Heidelberg, 1991.

- [51] O. Vasicek. Limiting loan loss probability distribution. Technical Report, KMV Corporation, 1991.

- [52] M. Veraar. The stochastic Fubini theorem revisited. Stochastics, 84(4):543–551, 2012.

- [53] W. Whitt. Stochastic-Process Limits: An Introduction to Stochastic-Process Limits and Their Application to Queues. Springer Series in Operations Research and Financial Engineering. Springer, 2002.

- [54] J.-L. Wu and W. Yang. Valuation of synthetic CDOs with affine jump-diffusion processes involving Lévy stable distributions. Math. Comput. Modelling, 57(3-4):570–583, 2013.

- [55] C. Zhou. An Analysis of Default Correlations and Multiple Defaults. Review Fin. Studies, 14(2):555–576, 2001.