Why have asset price properties changed so little in 200 years

Abstract

We first review empirical evidence that asset prices have had episodes of large fluctuations and been inefficient for at least 200 years. We briefly review recent theoretical results as well as the neurological basis of trend following and finally argue that these asset price properties can be attributed to two fundamental mechanisms that have not changed for many centuries: an innate preference for trend following and the collective tendency to exploit as much as possible detectable price arbitrage, which leads to destabilizing feedback loops.

1 Introduction

According to mainstream economics, financial markets should be both efficient and stable. Efficiency means that the current asset price is an unbiased estimator of its fundamental value (aka “right”, “fair” or “true”) price. As a consequence, no trading strategy may yield statistically abnormal profits based on public information. Stability implies that all price jumps can only be due to external news.

Real-world price returns have surprisingly regular properties, in particular fat-tailed price returns and lasting high- and low- volatility periods. The question is therefore how to conciliate these statistical properties, both non-trivial and universally observed across markets and centuries, with the efficient market hypothesis.

The alternative hypothesis is that financial markets are intrinsically and chronically unstable. Accordingly, the interactions between traders and prices inevitably lead to price biases, speculative bubbles and instabilities that originate from feed-back loops. This would go a long way in explaining market crises, both fast (liquidity crises, flash crashes) and slow (bubbles and trust crises). This would also explain why crashes did not wait for the advent of modern HFT to occur: whereas the May 6 2010 flash crash is well known, the one of May 28 1962, of comparable intensity but with only human traders, is much less known.

The debate about the real nature of financial market is of fundamental importance. As recalled above, efficient markets provide prices that are unbiased, informative estimators of the value of assets. The efficient market hypothesis is not only intellectually enticing, but also very reassuring for individual investors, who can buy stock shares without risking being outsmarted by more savvy investors.

This contribution starts by reviewing 200 years of stylized facts and price predictability. Then, gathering evidence from Experimental Psychology, Neuroscience and agent-based modelling, it outlines a coherent picture of the basic and persistent mechanisms at play in financial markets, which are at the root of destabilizing feedback loops.

2 Market anomalies

Among the many asset price anomalies documented in the economic literature since the 1980s (Schwert (2003)), two of them stand out:

-

1.

The Momentum Puzzle: price returns are persistent, i.e., past positive (negative) returns predict future positive (negative) returns.

-

2.

The Excess Volatility Puzzle: asset price volatility is much larger than that of fundamental quantities

These two effects are not compatible with the efficient market hypothesis and suggest that financial market dynamics is influenced by other factors than fundamental quantities. Other puzzles, such as the “low-volatility” and “quality” anomalies, are also very striking, but we will not discuss them here – see Ang et al. (2009); Baker et al. (2011); Ciliberti et al. (2016); Bouchaud et al. (2016) for recent reviews.

2.1 Trends and bubbles

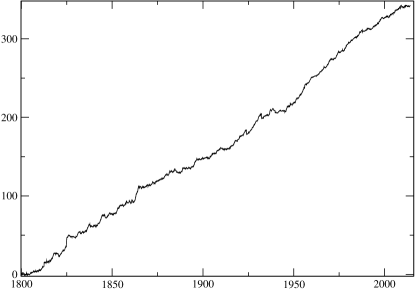

In blatant contradiction with the efficient market hypothesis, trend-following strategies have been successful on all asset classes for a very long time. Figure 1 shows for example a backtest of such strategy since 1800 (Lempérière et al. (2014)). The regularity of its returns over 200 years implies the presence of a permanent mechanism that makes price returns persistent.

Indeed, the propensity to follow past trends is a universal effect, which most likely originates from a behavioural bias: when faced with an uncertain outcome, one is tempted to reuse a simple strategy that seemed to be successful in the past (Gigerenzer and Goldstein (1996)). The relevance of behavioural biases to financial dynamics, discussed by many authors, among whom Kahneman and Shiller, has been confirmed in many experiments on artificial markets (Smith et al. (1988)), surverys (Shiller (2000); Menkhoff (2011); Greenwood and Shleifer (2013)), etc. which we summarize in Section 3.

2.2 Short-term price dynamics: jumps and endogenous dynamics

Jump statistics

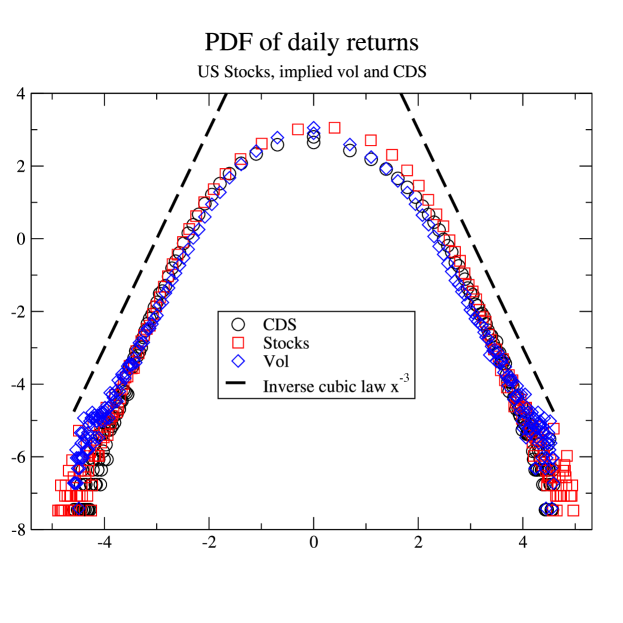

Figure 4 shows the empirical price return distributions of assets from three totally different assets classes. The distributions are remarkably similar (see also Zumbach (2015)): the probability of extreme return are all , where the exponent is close to 3 (Stanley et al. (2008)). The same law holds for other markets (raw materials, currencies, interest rates). This implies that crises of all sizes occur and result into both positive and negative jumps, from fairly small crises to centennial crises.

The endogenous nature of price jumps

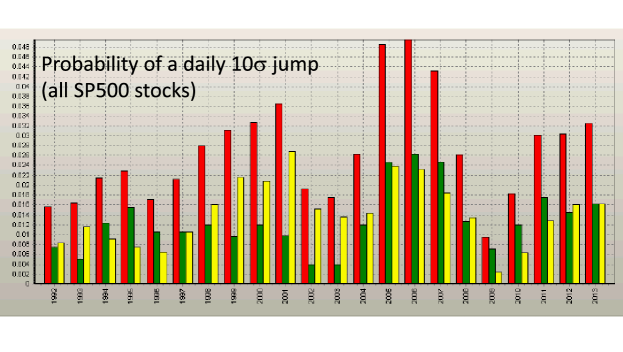

What causes these jumps? Far from being rare events, they are part of the daily routine of markets: every day, at least one 5- event occurs for one of the S&P500 components! According the Efficient Market Hypothesis, only some very significant pieces of information may cause large jumps, i.e., may substantially change the fundamental value of a given asset. This logical connection is disproved by empirical studies which match news sources with price returns: only a small fraction of jumps can be related to news and thus defined as an exogenous shock (Cutler et al. (1998); Fair (2002); Joulin et al. (2008); Cornell (2013)).

The inevitable conclusion is that most price jumps are self-inflicted, i.e., are endogenous. From a dynamical point of view, this means that feedback loops are so important that, at times, the state of market dynamics is near critical: small perturbations may cause very large price changes. Many different modelling frameworks yield essentially the same conclusion (Wyart et al. (2008); Marsili et al. (2009); Bacry et al. (2012); Hardiman et al. (2013); Chicheportiche and Bouchaud (2014)).

The relative importance of exogenous and endogenous shocks is then linked to the propensity of the financial markets to hover near critical or unstable points. The next step is therefore to find mechanisms that systematically tend to bring financial markets on the brink.

3 Fundamental market mechanisms: arbitrage, behavioural biases and feedback loops

In short, we argue below that greed and learning are two sufficient ingredients to explain the above stylized facts. There is no doubt that human traders have always tried to outsmart each other, and that the members the homo sapiens sapiens clique have some learning abilities. Computers and High Frequency Finance then merely decrease the minimum reaction speed (Hardiman et al. (2013)) without modifying much the essence of the mechanisms at play.

In order to properly understand the nature of the interaction between investors in financial markets, one needs to keep two essential ingredients

-

1.

Investor heterogeneity: the distribution of their wealth, trading frequency, computing power, etc. have heavy tails, which prevents a representative agent approach.

-

2.

Asynchronism: the number of trades per agent in a given period is heavy-tailed, which implies that they do not trade synchronously. In addition, the continuous double auction mechanism implies sequential trading: only two orders may interact at any time.

One thus cannot assume that all the investors behave in the same way, nor that they can be split into two or three categories, which is nevertheless a common assumption when modelling or analyzing market behaviour.

3.1 Speculation

Although the majority of trades are of algorithmic nature nowadays, most traders (human or artificial) use the same types of strategies. Algorithmic trading very often simply implements analysis and extrapolation rules that have been used by human traders since immemorial times, as they are deeply ingrained in human brains.

Trend following

Trend-following in essence consists in assuming that future price changes will be of the same sign as last past price changes. It is well-known that this type of strategy may destabilize prices by increasing the amplitude and duration of price excursions. Bubbles also last longer because of heavy-tailed trader heterogeneity. Neglecting new investors for the time being, the heavy-tailed nature of trader reaction times implies that some traders are much slower than others to take part to a nascent bubble. This causes a lasting positive volume imbalance that feeds a bubble for a long time. Finally, a bubble attracts new investors that may be under the impression that this bubble grow further. The neuronal processes that contribute the emergence and duration of bubbles are discussed in section 3.4.

Contrarian behaviour

Contrarian trading consists in betting on mean-reverting behavior: price excursions are deemed to be only temporary, i.e., that the price will return to some reference (“fundamental” or other) value. Given the heterogeneity of traders, one may assume that the do not all have the same reference value in mind. The dynamical effects of this type of strategies is to stabilize price (with respect to its perceived reference value).

Mixing trend followers and contrarians

In many simplified agent-based models (De Grauwe et al. (1993); Brock and Hommes (1998); Lux and Marchesi (1999)) both types of strategies are used by some fractions of the trader populations. A given trader may either always use the same kind of strategy (Frankel et al. (1986); Frankel and Froot (1990)), may switch depending on some other process (Kirman (1991)) or on the recent trading performance of the strategies (Brock and Hommes (1998); Wyart and Bouchaud (2007); Lux and Marchesi (1999)). In a real market, the relative importance of a given type of strategy is not constant, which influences the price dynamics.

Which type of trading strategy dominates can be measured in principle. Let us denote the price volatility measured over a single time step by . If trend following dominates, the volatility of returns measured every units of time, denoted by will be larger than . Conversely, if mean-reverting dominates, . Variance-ratio tests, based on the quantity , are suitable tools to assess the state of the market (see Charles and Darné (2009) for a review); see for example the PUCK concept, proposed by Mizuno et al. (2007).

When trend following dominates, trends and bubbles may last for a long time. The bursting of a bubble may be seen as mean-reversion taking (belatedly) over. This view is too simplistic, however, as it implicitly assumes that all the traders have the same calibration length and the same strategy parameters. In reality, the periods of calibration used by traders to extrapolate price trends are very heterogeneous. Thus, strategy heterogeneity and the fact that traders have to close their positions some time imply that a more complex analysis is needed.

3.2 Empirical studies

In order to study the behaviour of individual investors, the financial literature makes use of several types of data

- 1.

-

2.

The daily investment flows in US securities of the sub-population of individual traders. The transactions of individual traders are labelled as such, without any information about the identity of the investor (Kaniel et al. (2008)).

-

3.

The daily net investment fluxes of each investor in a given market. For example, Tumminello et al. (2012) use data about Nokia in the Finish stock exchange.

- 4.

-

5.

Transactions of all individual investors of all the brokers accessing a given market. Jackson (2004) shows that the behaviour of individual investors is the same provided that they use an on-line broker.

Trend follower vs contrarian

Many surveys show that institutional and individual investors expectation about future market returns are trend-following (e.g. Greenwood and Shleifer (2013)), yet the analysis of the individual investors’ trading flow at a given frequency (i.e. daily, weekly, monthly) invariably point out that their actual trading is dominantly contrarian as it is anti-correlated with previous price returns, while institutional trade flow is mostly uncorrelated with recent price changes on average (Grinblatt and Keloharju (2000); Jackson (2004); Dorn et al. (2008); Lillo et al. (2008); Challet and de Lachapelle (2013)), . In addition, the style of trading of a given investor only rarely changes (Lillo et al. (2008)).

Both findings are not as incompatible as it seems, because the latter behaviour is consistent with price discount seeking. In this context, the contrarian nature of investment flows means that individual investors prefer to buy shares of an asset after a negative price return and to sell it after a positive price return, just to get a better price for their deal. If they neglect their own impact, i.e., if the current price is a good approximation of the realized transaction price, this makes sense. If their impact is not negligible, then the traders buy when their expected transaction price is smaller than the current price and conversely (Batista et al. (2015)).

Herding behaviour

Lakonishok et al. (1992) define a statistical test of global herding. US mutual funds do not herd, while individual investors significantly do (Dorn et al. (2008)). Instead of defining global herding, Tumminello et al. (2012) define sub-groups of invidivual investors defined by the synchronization of their activity and inactivity, the rationale being that people that use the same way to analyse information are likely to act in the same fashion. This in fact defines herding at a much more microscopic level. The persistent presence of many sub-groups sheds a new light on herding. Using this method, Challet et al. (2016) show that synchronous sub-groups of institutional investors also exist.

Behavioural biases

Many behavioural biases have been reported in the literature. Whereas they are only relevant to human investors, i.e. to individual investors, most institutional funds are not (yet) fully automated and resort to human decisions. We will mention two of the most relevant biases.

Human beings react different to gains and to losses (see e.g. Prospect Theory Kahneman and Tversky (1979)) and prefer positively skewed returns to negatively skewed returns (aka the “lottery ticket” effect, see Lemperiere et al. (2016)). This has been linked to the disposition bias, which causes investors to close too early winning trades and too late losing ones (Shefrin and Statman (1985); Odean (1998); Boolell-Gunesh et al. (2009)) (see however Ranguelova (2001); Barberis and Xiong (2009); Annaert et al. (2008)). An indisputable bias is overconfidence, which leads to an excess of trading activity, which diminishes the net performance Barber and Odean (2000), see also Batista et al. (2015) for a recent experiment eliciting this effect. This explains why male traders earn less than female trades Barber and Odean (2001). Excess confidence is also found in individual portfolios, which are not sufficiently diversified. For example, individual traders trust too much their asset selection abilities (Goetzmann and Kumar (2005); Calvet et al. (2007)).

3.3 Learning and market instabilities

Financial markets force investors to be adaptive, even if they are not always aware of it (Farmer (1999); Zhang (1999); Lo (2004)). Indeed, strategy selection operates in two distinct ways

-

1.

Implicit: assume that an investor always uses the same strategy and never recalibrates its parameters. The performance of this strategy modulates the wealth of the investor, hence its relative importance on markets. In the worst case, this investor and his strategy effectively disappears. This is the argument attributed to Milton Friedman according to which only rational investors are able to survive in the long run because the uninformed investors are weeded out.

-

2.

Explicit: investors possess several strategies and use them in an adaptive way, according to their recent success. In this case, strategies might die (i.e., not being used), but investors may survive.

The neo-classical theory assumes the convergence of financial asset prices towards an equilibrium in which prices are no longer predictable. The rationale is that market participants are learning optimally such that this outcome is inevitable. A major problem with this approach is that learning requires a strong enough signal-to-noise ratio (Sharpe ratio); as the signal fades away, so does the efficiency of any learning scheme. As a consequence, reaching a perfectly efficient market state is impossible in finite time.

This a major cause of market instability. Patzelt and Pawelzik (2011) showed that optimal signal removal in presence of noise tends to converge to a critical state characterized by explosive and intermittent fluctuations, which precisely correspond to the stylized facts described in the first part of this paper. This is a completely generic result and directly applies to financial markets. Signal-to-noise mediated transitions to explosive volatility is found in agent-based models in which predictability is measurable, as in the Minority Game (Challet and Marsili (2003); Challet et al. (2005)) and more sophisticated models (Giardina and Bouchaud (2003)).

3.4 Experiments

Artificial assets

In their famous work, Smith et al. (1988) found that price bubbles emerged in most experimental sessions, even if only three or four agents were involved. This means that financial bubble do not need very many investors to appear. Interestingly, the more experienced the subjects, the less likely the emergence of a bubble.

More recently, Hommes et al. (2005) observed that in such experiments, the resulting price converges towards the rational price either very rapidly or very slowly or else with large oscillations. Anufriev and Hommes (2009) assume that the subjects dynamically use very simple linear price extrapolation rules (among which trend-following and mean-reverting rules),

Neurofinance

Neurofinance aims at studying the neuronal process involved in investment decisions (see Lo (2011) for an excellent review). One of the most salient result is that, expectedly, human beings spontaneously prefer to follow perceived past trends.

Various hormones play a central role in the dynamics of risk perception and reward seeking, which are major sources of positive and negative feedback loops in Finance. Even better, hormone secretion by the body modifies the strength of feedback loops dynamically, and feedback loops interact between themselves. Some hormones have a feel-good effect, while other reinforce to risk aversion.

Coates and Herbert (2008) measured the cortisol (the “stress hormone”) concentration in saliva samples of real traders and found that it depends on the realized volatility of their portfolio. This means that a high volatility period durable increases the cortisol level of traders, which increases risk aversion and reduces activity and liquidity of markets, to the detriment of markets as a whole.

Reward-seeking of male traders is regulated by testosterone. The first winning round-trip leads to an increase of the level testosterone, which triggers the production of dopamine, a hormone related to reward-seeking, i.e. of another positive round-trip in this context. This motivates the trader to repeat or increase his pleasure by taking additional risk. At relatively small doses, this exposure to reward and reward-seeking has a positive effect. However, quite clearly, it corresponds to a destabilizing feedback loop and certainly reinforces speculative bubbles. Accordingly, the trading performance of investors is linked to their dopamine level, which is partly determined by genes (Lo et al. (2005); Sapra et al. (2012)). .

Quite remarkably, the way various brain areas are activated during the successive phases of speculative bubbles has been investigated in detail. Lohrenz et al. (2007) suggest a neurological mechanism which motivates investors to try to ride a bubble: they correlate the activity of a brain area with how much gain opportunities a trader has missed since the start of a bubble. This triggers the production of dopamine, which in turn triggers risk taking, and therefore generates trades. In other words, regrets or “fear of missing out” lead to trend following.

After a while, dopamine, i.e., gut feelings, cannot sustain bubbles anymore as its effect fades. Another cerebral region takes over; quite ironically, it is one of the more rational ones: DeMartino et al. (2013) find a correlation between the activation level of an area known to compute a representation of the mental state of other people, and the propensity to invest in a pre-existing bubble. These authors conclude that investors make up a rational explanation about the existence of the bubble (“others cannot be wrong”) which justifies to further invest in the bubble. This is yet another neurological explanation of our human propensity to trend following.

3.5 Conclusion

Many theoretical arguments suggest that volatility bursts may be intimately related to the quasi-efficiency of financial markets, in the sense that predicting them is hard because the signal-to-noise ratio is very small (which does not imply that the prices are close to their “fundamental” values). Since the adaptive behaviour of investors tends to remove price predictability, which is the signal that traders try to learn, price dynamics becomes unstable as they then base their trading decision on noise only (Challet et al. (2005); Patzelt and Pawelzik (2011)). This is a purely endogenous phenomenon whose origin is the implicit or explicit learning of the value of trading strategies, i.e., of the interaction between the strategies that investors use. This explains why these stylized facts have existed for at least as long as financial historical data exists. Before computers, traders used their strategies in the best way they could. Granted, they certainly could exploit less of the signal-to-noise ratio than we can today. This however does not matter at all: efficiency is only defined with respect to the set of strategies one has in one’s bag. As time went on, the computational power increased tremendously, with the same result: unstable prices and bursts of volatility. This is why, unless exchange rules are dramatically changed, there is no reason to expect financial markets will behave any differently in the future.

Similarly, the way human beings learn also explains why speculative bubbles do not need rumour spreading on internet and social networks in order to exist. Looking at the chart of an asset price is enough for many investors to reach similar (and hasty) conclusions without the need for peer-to-peer communication devices (phones, emails, etc.). In short, the fear of missing out is a kind of indirect social contagion.

Human brains have most probably changed very little for the last two thousand years. This means that the neurological mechanisms responsible for the propensity to invest in bubbles are likely to influence the behaviour of human investors for as long as they will be allowed to trade.

From a scientific point of view, the persistence of all the above mechanisms justifies the quest for the fundamental mechanisms of market dynamics. We believe that the above summary provides a coherent picture of how financial markets have worked for at least two centuries (Reinhart and Rogoff (2009)) and why they will probably continue to stutter in the future.

References

- Ang et al. [2009] Andrew Ang, Robert J Hodrick, Yuhang Xing, and Xiaoyan Zhang. High idiosyncratic volatility and low returns: International and further us evidence. Journal of Financial Economics, 91(1):1–23, 2009.

- Annaert et al. [2008] Jan Annaert, Dries Heyman, Michele Vanmaele, and Sofieke Van Osselaer. Disposition bias and overconfidence in institutional trades. Technical report, Working Paper, 2008.

- Anufriev and Hommes [2009] M Anufriev and C Hommes. Evolutionary selection of individual expectations and aggregate outcomes. CeNDEF Working Paper University of Amsterdam, 9, 2009.

- Bacry et al. [2012] Emmanuel Bacry, Khalil Dayri, and Jean-Francois Muzy. Non-parametric kernel estimation for symmetric Hawkes processes. application to high frequency financial data. The European Physical Journal B, 85(5):1–12, 2012.

- Baker et al. [2011] Malcolm Baker, Brendan Bradley, and Jeffrey Wurgler. Benchmarks as limits to arbitrage: Understanding the low-volatility anomaly. Financial Analysts Journal, 67(1), 2011.

- Barber and Odean [2000] Brad M Barber and Terrance Odean. Trading is hazardous to your wealth: The common stock investment performance of individual investors. The Journal of Finance, 55(2):773–806, 2000.

- Barber and Odean [2001] Brad M Barber and Terrance Odean. Boys will be boys: Gender, overconfidence, and common stock investment. The Quarterly Journal of Economics, 116(1):261–292, 2001.

- Barberis and Xiong [2009] Nicholas Barberis and Wei Xiong. What drives the disposition effect? an analysis of a long-standing preference-based explanation. the Journal of Finance, 64(2):751–784, 2009.

- Batista et al. [2015] Joao da Gama Batista, Domenico Massaro, Jean-Philippe Bouchaud, Damien Challet, and Cars Hommes. Do investors trade too much? a laboratory experiment. arXiv preprint arXiv:1512.03743, 2015.

- Boolell-Gunesh et al. [2009] S Boolell-Gunesh, Marie-Hélène Broihanne, and Maxime Merli. Disposition effect, investor sophistication and taxes: some French specificities. Finance, 30(1):51–78, 2009.

- Bouchaud et al. [2016] Jean-Philippe Bouchaud, Ciliberti Stefano, Augustin Landier, Guillaume Simon, and David Thesmar. The excess returns of ‘quality’ stocks: A behavioral anomaly. to appear in J. Invest. Strategies, 2016.

- Brock and Hommes [1998] W.A. Brock and C.H. Hommes. Heterogeneous beliefs and routes to chaos in a simple asset pricing model. Journal of Economic dynamics and Control, 22(8-9):1235–1274, 1998.

- Calvet et al. [2007] Laurent E. Calvet, John Y. Campbell, and Paolo Sodini. Down or out: Assessing the welfare costs of household investment mistakes. Journal of Political Economy, 115(5):pp. 707–747, 2007. URL http://www.jstor.org/stable/10.1086/524204.

- Challet and Marsili [2003] D. Challet and M. Marsili. Criticality and finite size effects in a realistic model of stock market. Phys. Rev. E, 68:036132, 2003.

- Challet et al. [2016] D. Challet, R. Chicheportiche, and M. Lallouache. Trader lead-lag networks and internal order crossing. 2016. in preparation.

- Challet and de Lachapelle [2013] Damien Challet and David Morton de Lachapelle. A robust measure of investor contrarian behaviour. In Econophysics of Systemic Risk and Network Dynamics, pages 105–118. Springer, 2013.

- Challet et al. [2005] Damien Challet, Matteo Marsili, and Yi-Cheng Zhang. Minority Games. Oxford University Press, Oxford, 2005.

- Charles and Darné [2009] Amélie Charles and Olivier Darné. Variance-ratio tests of random walk: an overview. Journal of Economic Surveys, 23(3):503–527, 2009.

- Chicheportiche and Bouchaud [2014] Rémy Chicheportiche and Jean-Philippe Bouchaud. The fine-structure of volatility feedback. Physica A, 410:174–195, 2014.

- Ciliberti et al. [2016] S Ciliberti, Y Lempérière, A Beveratos, G Simon, L Laloux, M Potters, and JP Bouchaud. Deconstructing the low-vol anomaly. to appear in J. Portfolio Management, 2016.

- Coates and Herbert [2008] John M Coates and Joe Herbert. Endogenous steroids and financial risk taking on a London trading floor. Proceedings of the national academy of sciences, 105(16):6167–6172, 2008.

- Cornell [2013] Bradford Cornell. What moves stock prices: Another look. The Journal of Portfolio Management, 39(3):32–38, 2013.

- Cutler et al. [1998] David M Cutler, James M Poterba, and Lawrence H Summers. What moves stock prices? Bernstein, Peter L. and Frank L. Fabozzi, pages 56–63, 1998.

- De Grauwe et al. [1993] Paul De Grauwe, Hans Dewachter, and Mark Embrechts. Exchange rate theory: chaotic models of foreign exchange markets. 1993.

- de Lachapelle and Challet [2010] David Morton de Lachapelle and Damien Challet. Turnover, account value and diversification of real traders: evidence of collective portfolio optimizing behavior. New J. Phys, 12:075039, 2010.

- DeMartino et al. [2013] Benedetto DeMartino, John P. O’Doherty, Debajyoti Ray, Peter Bossaerts, and Colin Camerer. In the Mind of the Market: Theory of Mind Biases Value Computation during Financial Bubbles. Neuron, 80:1102, 2013. doi: 10.1016/j.neuron.2013.11.002.

- Dorn et al. [2008] Daniel Dorn, Gur Huberman, and Paul Sengmueller. Correlated trading and returns. The Journal of Finance, 63(2):885–920, 2008.

- Fair [2002] Ray C Fair. Events that shook the market. Journal of Business, 75:713–732, 2002.

- Farmer [1999] J. D. Farmer. Market force, ecology and evolution. Technical Report 98-12-117, Santa Fe Institute, 1999.

- Frankel and Froot [1990] Jeffrey A Frankel and Kenneth A Froot. Chartists, fundamentalists, and trading in the foreign exchange market. The American Economic Review, 80(2):181–185, 1990.

- Frankel et al. [1986] Jeffrey A Frankel, Kenneth A Froot, et al. Understanding the us dollar in the eighties: the expectations of chartists and fundamentalists. Economic record, 62(1):24–38, 1986.

- Giardina and Bouchaud [2003] I. Giardina and J.-Ph. Bouchaud. Crashes and intermittency in agent based market models. Eur. Phys. J. B, 31:421–437, 2003.

- Gigerenzer and Goldstein [1996] Gerd Gigerenzer and Daniel G Goldstein. Reasoning the fast and frugal way: models of bounded rationality. Psychological review, 103(4):650, 1996.

- Goetzmann and Kumar [2005] William N Goetzmann and Alok Kumar. Why do individual investors hold under-diversified portfolios? Technical report, Yale School of Management, 2005.

- Greenwood and Shleifer [2013] Robin Greenwood and Andrei Shleifer. Expectations of returns and expected returns. Rev. Fin. Studies, 2013. to appear.

- Grinblatt and Keloharju [2000] Mark Grinblatt and Matti Keloharju. The investment behavior and performance of various investor types: a study of Finland’s unique data set. Journal of Financial Economics, 55(1):43–67, 2000.

- Hardiman et al. [2013] Stephen J. Hardiman, Nicolas Bercot, and Jean-Philippe Bouchaud. Critical reflexivity in financial markets: a hawkes process analysis. The European Physical Journal B, 86(10):1–9, 2013. doi: 10.1140/epjb/e2013-40107-3. URL http://dx.doi.org/10.1140/epjb/e2013-40107-3.

- Hommes et al. [2005] Cars Hommes, Joep Sonnemans, Jan Tuinstra, and Henk Van de Velden. Coordination of expectations in asset pricing experiments. Review of Financial Studies, 18(3):955–980, 2005.

- Jackson [2004] A. Jackson. The aggregate behaviour of individual investors. 2004.

- Joulin et al. [2008] Armand Joulin, Augustin Lefevre, Daniel Grunberg, and Jean-Philippe Bouchaud. Stock price jumps: news and volume play a minor role. Wilmott Mag. Sept/Oct, 2008.

- Kahneman and Tversky [1979] Daniel Kahneman and Amos Tversky. Prospect theory: an analysis of decision under risk. Econometrica, 47:263, 1979.

- Kaniel et al. [2008] R. Kaniel, G. Saar, and S. Titman. Individual investor trading and stock returns. The Journal of Finance, 63(1):273–310, 2008.

- Kirman [1991] Alan Kirman. Epidemics of opinion and speculative bubbles in financial markets. Money and financial markets, pages 354–368, 1991.

- Lakonishok et al. [1992] Josef Lakonishok, Andrei Shleifer, and Robert W Vishny. The impact of institutional trading on stock prices. Journal of financial economics, 32(1):23–43, 1992.

- Lemperiere et al. [2016] Yves Lemperiere, Cyril Deremble, Trung-Tu Nguyen, Philip Andrew Seager, Marc Potters, and Jean-Philippe Bouchaud. Risk premia: Asymmetric tail risks and excess returns. to appear in Quantitative Finance, 2016.

- Lempérière et al. [2014] Y. Lempérière, P. Seager, M. Potters, and J.P. Bouchaud. Two centuries of trend following. Technical report, 2014.

- Lillo et al. [2008] F. Lillo, E. Moro, G. Vaglica, and R.N. Mantegna. Specialization and herding behavior of trading firms in a financial market. New Journal of Physics, 10:043019, 2008.

- Lo [2004] Andrew W Lo. The adaptive markets hypothesis. The Journal of Portfolio Management, 30(5):15–29, 2004.

- Lo [2011] Andrew W Lo. Fear, greed, and financial crises: a cognitive neurosciences perspective. by J. Fouque, and J. Langsam. Cambridge University Press, Cambridge, UK, 2011.

- Lo et al. [2005] Andrew W Lo, Dmitry V Repin, and Brett N Steenbarger. Fear and greed in financial markets: A clinical study of day-traders. American Economic Review, 95(2):352–359, 2005.

- Lohrenz et al. [2007] Terry Lohrenz, Kevin McCabe, Colin F Camerer, and P Read Montague. Neural signature of fictive learning signals in a sequential investment task. Proceedings of the National Academy of Sciences of the United States of America, 104(22):9493–9498, 2007.

- Lux and Marchesi [1999] T. Lux and M. Marchesi. Scaling and criticality in a stochastic multi-agent model of a financial market. Nature, 397:498–500, 1999.

- Marsili et al. [2009] M. Marsili, G. Raffaelli, and B. Ponsot. Dynamic instability in generic model of multi-assets markets. Journal of Economic Dynamics and Control, 33(5):1170–1181, 2009.

- Menkhoff [2011] Lukas Menkhoff. Are momentum traders different? implications for the momentum puzzle. Applied Economics, 43(29):4415–4430, 2011.

- Mizuno et al. [2007] Takayuki Mizuno, Hideki Takayasu, and Misako Takayasu. Analysis of price diffusion in financial markets using puck model. Physica A: Statistical Mechanics and its Applications, 382(1):187–192, 2007.

- Odean [1998] Terrance Odean. Are investors reluctant to realize their losses? The Journal of finance, 53(5):1775–1798, 1998.

- Patzelt and Pawelzik [2011] Felix Patzelt and Klaus Pawelzik. Criticality of adaptive control dynamics. Phys. Rev. Lett., 107(23):238103, 2011.

- Ranguelova [2001] Elena Ranguelova. Disposition effect and firm size: New evidence on individual investor trading activity. Available at SSRN 293618, 2001.

- Reinhart and Rogoff [2009] Carmen M Reinhart and Kenneth Rogoff. This time is different: Eight centuries of financial folly. Princeton University Press, 2009.

- Sapra et al. [2012] Steve Sapra, Laura E Beavin, and Paul J Zak. A combination of dopamine genes predicts success by professional wall street traders. PloS one, 7(1):e30844, 2012.

- Schwert [2003] G William Schwert. Anomalies and market efficiency. Handbook of the Economics of Finance, 1:939–974, 2003.

- Shefrin and Statman [1985] Hersh Shefrin and Meir Statman. The disposition to sell winners too early and ride losers too long: Theory and evidence. The Journal of finance, 40(3):777–790, 1985.

- Shiller [2000] Robert J Shiller. Measuring bubble expectations and investor confidence. The Journal of Psychology and Financial Markets, 1(1):49–60, 2000.

- Smith et al. [1988] Vernon L Smith, Gerry L Suchanek, and Arlington W Williams. Bubbles, crashes, and endogenous expectations in experimental spot asset markets. Econometrica: Journal of the Econometric Society, pages 1119–1151, 1988.

- Stanley et al. [2008] H Eugene Stanley, Vasiliki Plerou, and Xavier Gabaix. A statistical physics view of financial fluctuations: Evidence for scaling and universality. Physica A: Statistical Mechanics and its Applications, 387(15):3967–3981, 2008.

- Tumminello et al. [2012] M. Tumminello, F. Lillo, J. Piilo, and R.N. Mantegna. Identification of clusters of investors from their real trading activity in a financial market. New Journal of Physics, 14:013041, 2012.

- Wyart and Bouchaud [2007] Matthieu Wyart and Jean-Philippe Bouchaud. Self-referential behaviour, overreaction and conventions in financial markets. Journal of Economic Behavior & Organization, 63(1):1–24, 2007.

- Wyart et al. [2008] Matthieu Wyart, Jean-Philippe Bouchaud, Julien Kockelkoren, Marc Potters, and Michele Vettorazzo. Relation between bid–ask spread, impact and volatility in order-driven markets. Quantitative Finance, 8(1):41–57, 2008.

- Zhang [1999] Y.-C. Zhang. Towards a theory of marginally efficient markets. Physica A, 269:30, 1999.

- Zumbach [2015] Gilles Zumbach. Cross-sectional universalities in financial time series. Quantitative Finance, 15(12):1901–1912, 2015.

- Zumbach and Finger [2010] Gilles Zumbach and Christopher Finger. A historical perspective on market risks using the DJIA index over one century. Wilmott Journal, 2(4):193–206, 2010.