Relation between the rate of convergence of strong law of large numbers and the rate of concentration of Bayesian prior in game-theoretic probability

Abstract

We study the behavior of the capital process of a continuous Bayesian mixture of fixed proportion betting strategies in the one-sided unbounded forecasting game in game-theoretic probability. We establish the relation between the rate of convergence of the strong law of large numbers in the self-normalized form and the rate of divergence to infinity of the prior density around the origin. In particular we present prior densities ensuring the validity of Erdős–Feller–Kolmogorov–Petrowsky law of the iterated logarithm.

Keywords and phrases: constant-proportion betting strategy, Erdős–Feller–Kolmogorov–Petrowsky law of the iterated logarithm, one-sided unbounded game, self-normalized processes, upper class.

1 Introduction

The most basic proof of the strong law of large numbers (SLLN) in Chapter 3 of [15] uses a discrete mixture

| (1) |

of fixed proportion betting strategies. The mixture puts the weight on the points , . The sum of weights on the interval , , is expressed as

which is equal to the length of the interval . Hence this mixture can be understood as the discrete approximation to the continuous uniform distribution over the interval . In Chapter 3 of [15] this mixture is used only to prove the usual form of SLLN, and any discrete distribution having the origin as an accumulation point of mixture weights serves the same purpose. As we show in Section 4, the concentration of the mixture weights around the origin has the direct implication on the rate of convergence of SLLN forced by the mixture.

In this paper we consider a continuous mixture in the integral form. Although a proof based on a discrete mixture is conceptually simpler, the integral in a continuous mixture is more convenient for analytic treatment. In fact in this paper we give a unified treatment covering the usual SLLN, the validity (i.e., the upper bound) of the usual law of iterated logarithm (LIL), and finally the validity of Erdős–Feller–Kolmogorov–Petrowsky (EFKP) LIL [13, Chapter 5.2].

Another feature of this paper is the self-normalized form in which we consider SLLN. Let

denote the sum of random variables and and the sum of their squares, respectively. We compare to , rather than to . For example is the usual non-self-normalized SLLN, whereas is the SLLN in the self-normalized form. We often obtain cleaner statements and proofs in the self-normalized form. For instance, in measure-theoretic probability, Griffin and Kuelbs [7] showed the EFKP-LIL in the self-normalized form in i.i.d. case with some additional conditions. Later, Wang [18] and Csörgő et al. [3] eliminated some of the conditions. A similar argument in the self-normalized form can also be seen in game-theoretic probability as shown in [14]. Self-normalized processes including -statistic are known for their statistical applications. In studying self-normalized processes, self-normalized sums are regarded as important and one of the reasons is that they have close relations to -statistic; see, e.g., [5], [6]. For a survey of results concerning self-normalized processes, especially self-normalized sums, see [4], [16], and references in [14]. In the self-normalized form of SLLN we only consider paths of Reality’s moves such that . Hence the events considered in this paper are conditional events given .

Yet another feature of this paper is that we mainly consider the one-sided unbounded forecasting game. We notice that the results on the bounded forecasting game can be derived from the results on the one-sided unbounded forecasting game. Also it is an interesting fact that in the one-sided unbounded forecasting game the usual non-self-normalized SLLN does not hold. We discuss this fact in Section 6. The importance of this game will be explained in Section 2 and Section 7.

We remark on the terminology used in this paper. We use “increasing” and “decreasing” in the weak sense, i.e. we simply write “increasing” instead of more accurate “(monotone) nondecreasing”.

The organization of this paper is as follows. In Section 2 we introduce the protocol of the one-sided unbounded forecasting game and relate it to betting on positive price processes. We also define Bayesian strategies with prior densities. In Section 3 we establish some preliminary results on the capital process of a Bayesian strategy. In Section 4 we prove a general inequality for the capital process of a Bayesian strategy and apply it to prove SLLN and the validity of LIL in the self-normalized form based on Bayesian strategies. In Section 5 we define two functionals which connect prior densities and functions of the upper class for EFKP-LIL. Based on these results, we give a proof of the validity of EFKP-LIL using a corresponding Bayesian strategy. In Section 6 we prove other basic properties of the one-sided unbounded forecasting game, including the rate of SLLN in the usual non-self-normalized form and the Reality’s deterministic strategy against the usual form of SLLN. We end the paper with some discussions in Section 7.

2 The one-sided unbounded forecasting game and the Bayesian strategy

In this paper we mainly consider the one-sided unbounded forecasting game defined as follows.

The One-sided Unbounded Forecasting Game (OUFG)

Players: Skeptic, Reality

Protocol:

Skeptic starts with the initial capital .

FOR :

Skeptic announces .

Reality announces

.

Collateral Duties: Skeptic must keep nonnegative. Reality must keep from tending to infinity.

In game-theoretic probability the initial capital is usually standardized to be 1. However the value of the initial capital is not relevant in discussing whether Skeptic can force an event or not. Also notation is sometimes simpler if we allow arbitrary positive value for .

In OUFG, Reality’s move is unbounded on the positive side. On the other hand, in the bounded forecasting game (BFG) of Chapter 3 of [15], is restricted as . Since the Reality’s move space is smaller in BFG than in OUFG, Reality is weaker against Skeptic in BFG than in OUFG. This implies that if Skeptic can force an event in OUFG, then he can force in BFG. In this sense the one-sided version of SLLN (cf. (3.9) in Lemma 3.3 of [15]) in OUFG is stronger than that in BFG. This is one of the reasons why we mainly consider OUFG in this paper.

Let denote the proportion of the capital Skeptic bets on the round . The collateral duty of Skeptic is in OUFG, whereas it is in BFG. This again reflects the fact that Skeptic is stronger in BFG than in OUFG.

OUFG is a natural protocol, when we consider betting on a positive price process of some risky financial assets. Let

denote the return of the price process. Then and there is no upper bound for the return if is allowed to take an arbitrary large value. Furthermore we can write as

| (2) |

Hence is the proportion of the current capital Skeptic keeps as cash, which does not change the value from round to round, and is the proportion of the current capital Skeptic bets on the risky asset.

When is a constant, we call the strategy the constant-proportion betting strategy or the -strategy. The capital process of the -strategy is written as

We now consider continuous mixture of -strategies where the initial capital is distributed according to the (unnormalized) prior density of an absolutely continuous finite measure on the unit interval :

The betting proportion of the Bayesian strategy with the prior density is defined as

| (3) |

Then the capital process of this strategy is written as

| (4) |

with the initial capital . The equation (4) is checked by induction on , since with given in (3), we have

A similar argument is also in [14]. One should notice that the equation (1) can be seen as one discretization of (4), where is the uniform density on .

We are concerned with the rate of increase of as . Hence we require some regularity conditions on the behavior of around the origin. The following condition on is convenient in discussing EFKP-LIL in Section 5.

Assumption 2.1.

There exist and such that

-

1.

is a prior density, that is, nonnegative and integrable on ,

-

2.

on , and

-

3.

is increasing on .

For simplicity, we allow the case that the integral of on is not , which does not cause a problem when considering limit theorems. Note that we are allowing , but by the monotonicity and the integrability we are assuming . Assumption 2.1 holds for particular examples discussed in the next section. Concerning the condition on in Assumption 2.1, Skeptic can always allocate the initial capital of to the uniform prior of Section 4.2 to satisfy this condition.

3 Preliminary results

In this section we see the self-normalized form of SLLN in the one-sided unbounded forecasting game.

Proposition 3.1.

In OUFG, by any Bayesian strategy with satisfying Assumption 2.1, Skeptic weakly forces

| (5) |

We can prove this proposition by more or less the same way as in Lemma 3.3 of [15]. The difference is that the mixture we use here is not discrete but continuous. We will see later that we can show stronger forms in similar arguments.

We begin with the following simple lemma. The particular case is used in Lemma 3.3 of [15]. We prove this lemma separately in a stronger form for later use.

Lemma 3.2.

For any

| (6) |

Proof.

Let

Then and

Hence for or , and only for . This implies the lemma. ∎

Proof of Proposition 3.1.

We use Lemma 3.2 with . Suppose that Reality has chosen a path such that and . Then there exists a sufficiently small such that for infinitely many . For such an ,

Notice that the strategy and the capital process do not depend on . Because , we have . ∎

Remark 3.3.

Skeptic cannot force the event . Reality can announce for all , and and for all .

4 Rate of convergence of SLLN implied by a Bayesian strategy

In this section we present results on the rate of convergence of SLLN by a Bayesian strategy, by establishing some lower bounds for the capital process. Note that since the Bayesian strategy already weakly forces (5), we only need to consider lower bounds when is sufficiently small.

In Section 4.1 we present our first inequality, which will be used to show the rate of convergence of SLLN for the uniform prior in Section 4.2. Then we give a more refined inequality in Section 4.3, which will be used to show the rate of convergence of SLLN for the power prior (Section 4.4), for the prior ensuring the validity in the usual form of LIL (Section 4.5) and for the prior ensuring the validity of a typical form of EFKP-LIL (Section 4.6).

4.1 A lower bound for the capital process of a Bayesian strategy

Our first theorem of this paper bounds from below as follows.

Theorem 4.1.

In OUFG, for any and ,

| (7) |

4.2 Uniform prior

Let , , be the uniform prior. By Theorem 4.1 we obtain the following result.

Proposition 4.2.

In OUFG, by the uniform prior, Skeptic weakly forces

| (9) |

Proof.

Suppose that Reality chooses a path such that , and

Then for some small positive , we have

and

for infinitely many . For such an ,

Since , we have . ∎

In Proposition 4.2, we considered continuous uniform mixture. However the same proof can be applied to discrete mixture setting. In particular the discrete mixture in the basic proof of SLLN in Chapter 3 of [15] achieves the same rate of (9). Note also that this rate is the same as the rate of SLLN of dynamic strategies studied in [9] and [8].

4.3 A refined lower bound of the capital process

By Assumption 2.1, holds around the origin. This implies that for any prior satisfying Assumption 2.1, the rate of convergence already holds. In fact, for write

Then

and the result for the uniform prior applies to the right-hand side. Hence in considering other priors satisfying Assumption 2.1, we can only consider paths such that . In particular and as . For such paths, we consider maximizing the right-hand side of (7) with respect to . For the case is large, we put and obtain the following theorem.

Theorem 4.3.

In OUFG, if , and , then

| (10) |

Proof.

Remark 4.4.

For the rest of this section we apply Theorem 4.3 to some typical nonuniform priors.

4.4 Power prior

For , let

| (12) |

For this power prior, the following result holds.

Proposition 4.5.

In OUFG, by the power prior, Skeptic weakly forces

Proof.

Consider the case for some for infinitely many . Note that the function is increasing for sufficiently large . Then for sufficiently large ,

∎

4.5 Prior for the validity of LIL

Here we present a prior for the validity of LIL. Let sufficiently small such that is positive for . Define

| (13) |

This is integrable around the origin.

Proposition 4.6.

In OUFG, by the prior (13), Skeptic weakly forces

| (14) |

Proof.

Again we use the fact that is increasing for sufficiently large . For for some and sufficiently large , we have

∎

4.6 Priors for the validity of typical EFKP-LIL

Here we generalize the prior (14) in view of EFKP-LIL. We give a more general and complete treatment of EFKP-LIL in Section 5.

Write

The following prior density

| (15) |

is integrable around the origin. We compare this with the bound , where

| (16) |

For notational simplicity we take in (15), since the coefficient of is 2 except for in (16). Note that in (15) is multiplied by 2 in (16). This is needed, because unlike the usual LIL in (14), where we considered the ratio of to , in EFKP-LIL we need to consider the difference . This difference corresponds to multiplication of by in the proof of Theorem 5.4.

Proof.

For and sufficiently large , we have

Here

Combining this with

we have

∎

5 Equivalence of prior densities and the upper class

The typical priors of the previous section suggest that higher concentration of the prior around the origin corresponds to a tighter convergence rate of SLLN. In particular, from the viewpoint of EFKP-LIL, it is of interest to establish the relation between priors and the function of the upper class.

Also it is natural to conjecture that the rate of SLLN implied by a Bayesian strategy only depends on the rate of concentration of the prior around the origin. This idea can be clarified if we classify priors with the same rate of concentration into the same class. Let denote the set of priors satisfying Assumption 2.1 by

| (17) |

5.1 The upper class

In studying the validity of EFKP-LIL, the notion of upper class of functions is essential. A positive function defined for is said to belong to the upper class in OUFG if Skeptic can force the event

For the terminology, see [13]. We characterize the upper class by an integral test:

| (18) |

A typical function in the upper class is given in (16). For convenience, we put the following regularity conditions on .

Assumption 5.1.

There exist some and , such that

-

1.

is a positive increasing function on ,

-

2.

the integral in (18) is finite, and

-

3.

for , we have

(19)

If is finite, then the integral in (18) diverges, since . Hence for satisfying Assumption 5.1. Furthermore the function is decreasing for and converges to zero as . Hence is eventually decreasing to zero. For EFKP-LIL, as the typical in (16), we are mainly concerned with functions , for which decreases to zero slower than any negative power of . Hence (19) is a mild regularity condition. We denote the set of functions satisfying Assumption 5.1 by

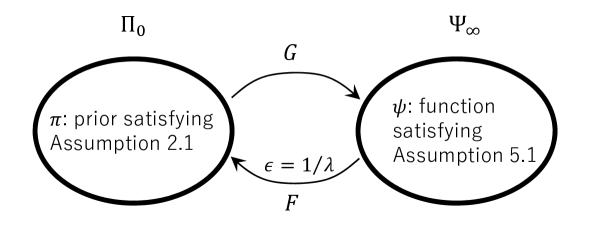

The goal is, when a is given, to find a that is a witness of the in the upper class. Now we define two functionals and as follows.

Definition 5.2.

| (20) | ||||

| (21) |

See Figure 1. These two functionals are “asymptotic inverse functionals” as we clarify in (27) and Theorem 5.8. Since we are interested in the case that is sufficiently small and is sufficiently large, for the rest of this paper we only consider that fulfills the condition . In fact, this condition holds true for sufficiently large because of the monotonicity of and . First we need to check that and . For checking , we use the following relation.

| (22) |

Lemma 5.3.

for . for .

Proof.

For the first part, the monotonicity of for sufficiently small holds because is eventually decreasing. The integrability of follows directly from the change of variables . Finally for by (19) and (20).

For the second part, the monotonicity of is obvious. We note the fact that , because otherwise is not integrable around the origin. Hence

| (23) |

Then as . Then as , by (22),

| (24) |

By the change of variables , the integrability of the left-hand side of (24) reduces to the integrability of around the origin. Finally

which is bounded away from zero for large . ∎

Based on this lemma, we can consider the compositions and . By direct computation we obtain

| (25) | ||||

| (26) |

5.2 Validity of EFKP-LIL via Bayesian strategy

Here we establish the validity of EFKP-LIL via a Bayesian strategy.

Theorem 5.4.

In OUFG, by a prior , Skeptic weakly forces

Proof.

As a corollary to this theorem, we state the following statement of the validity of EFKP-LIL.

Corollary 5.5.

Let be a positive increasing function defined for . Then, belongs to the upper class in OUFG if and only if

Proof.

First suppose that . Let and apply Theorem 5.4. Then Skeptic can weakly force

But in (26) we have

for all sufficiently large . Hence

Next let be a positive increasing function such that . Let . Notice that belongs to the upper class. Since is decreasing for and , we have

Then, satisfies Assumption 5.1. Hence, belongs to the upper class and so does .

Finally, suppose that is a positive increasing function, but . Then, in the fair-coin tossing game, Skeptic can force for infinitely many . This is a corollary from the classical EFKP-LIL. This fact also follows from the main theorem in [14]. Thus, Reality can comply with this event with this restriction, which means that does not belong to the upper class in OUFG. ∎

5.3 Equivalence

Consider such that the convergence rate of is very slow. Since and , the two functions and should have similar growing rates. One should also notice that, by (23),

| (27) |

In this asymptotic sense, and are inverse functionals. We clarify this point further below in Theorem 5.8.

In order to identify functions with the same rate of growth, we introduce equivalence relations in and . For two functions we write if

It is easy to check that is an equivalence relation.

For two functions we write if

Again it is easy to check that is an equivalence relation.

In the following two lemmas we prove that the functionals and preserve the equivalence relations.

Lemma 5.6.

Let . If , then .

Proof.

Since , there exist positive such that

Then

Since and diverge to as , for sufficiently small we have

Dividing this by we obtain the lemma. ∎

Lemma 5.7.

Let . If , then .

Proof.

Let denote the set of equivalence classes in with respect to and define similarly. Based on the above two lemmas and (25), (26) we have the following theorem.

Theorem 5.8.

The functionals and give bijections between and . Furthermore they are inverse functionals to each other.

Proof is obvious and omitted. The theorem says that functions in the upper class correspond to the prior densities, and the integrabilities of correspond to the integrabilities of densities.

6 Some other properties of the one-sided unbounded forecasting game

In this paper we have been considering SLLN in the self-normalized form. However SLLN for OUFG in non-self-normalized form exhibits an interesting property, which we show in the following proposition. The definition of compliance can be found in [10] and [11].

Proposition 6.1.

Let be a sequence of increasing positive reals such that . In OUFG Skeptic can weakly force if and only if .

Proof.

Suppose that . Consider Skeptic’s strategy . Then is a nonnegative martingale and by the game-theoretic martingale convergence theorem (Lemma 4.5 of [15]) Skeptic can weakly force that converges to a finite value. Then by Kronecker’s lemma Skeptic can weakly force .

The converse part can be proved by a deterministic strategy of Reality complying with . Suppose . If for infinitely many , then Reality chooses for all , which complies with the desired property.

Now, we assume that for all but finitely many . In each round Reality chooses either or . Note that , otherwise, Skeptic would be bankrupt when Reality chooses large enough. Let ,

and

We show that, for each , at least one of satisfies . Suppose otherwise. Then

Thus,

which implies

This is a contradiction.

Reality chooses her move so that for all . Then . Furthermore, . If for at most finitely many , then there exists such that for all , whence because . Hence, for infinitely many . For such an that is large enough, we have

which implies . ∎

The intuition of is the probability of so that the expectation is . Then, can be seen as a capital process in a game, and so is .

7 Discussions

In this paper we gave a unified treatment of the rate of convergence of SLLN in terms of Bayesian strategies, including the validity of LIL. Concerning LIL we did not discuss the sharpness of the bound. In OUFG the sharpness does not hold, because Reality can simply take . For the sharpness we need some boundedness condition, such as the simplified predictably unbounded forecasting game (Section 5.1 of [15], [14]). Even with some boundedness conditions, current game-theoretic proofs of the sharpness are still complicated and the nature of the weights, involving also negative ones due to short selling of a strategy, does not seem to be clear. We hope that the unified treatment of this paper also helps to streamline proofs of the sharpness.

As we discussed in (2), a Bayesian strategy for OUFG can be understood as the portfolio of cash and one risky asset. In the literature on universal portfolio by Thomas Cover and other researchers (Chapter 16 of [2], [1], [12], [17]), Bayesian strategies for many risky assets are considered. They recommend power priors such as the Dirichlet prior, which corresponds to priors in Section 4.4. From the viewpoint of the rate of convergence of SLLN, we have shown that we should take in (12) with additional multiplicative logarithmic terms. Hence our recommendations and those in universal portfolio literature seem to be different. This may be due to the difference of criteria for evaluating strategies. It is interesting to clarify these differences.

Acknowledgement

This research is supported by JSPS Grant-in-Aid for Scientific Research No. 16K12399.

References

- [1] T. M. Cover. Universal portfolios. Math. Finance, 1(1):1–29, 1991.

- [2] T. M. Cover and J. A. Thomas. Elements of Information Theory. Wiley-Interscience, Hoboken, NJ, second edition, 2006.

- [3] M. Csörgő, B. Szyszkowicz, and Q. Wang. Darling-Erdős theorem for self-normalized sums. Ann. Probab., 31(2):676–692, 2003.

- [4] V. H. de la Peña, T. L. Lai, and Q.-M. Shao. Self-normalized Processes. Springer-Verlag, Berlin, 2009.

- [5] B. Efron. Student’s -test under symmetry conditions. J. Amer. Statist. Assoc., 64:1278–1302, 1969.

- [6] P. S. Griffin. Tightness of the Student -statistic. Electron. Comm. Probab., 7:181–190 (electronic), 2002.

- [7] P. S. Griffin and J. D. Kuelbs. Some extensions of the LIL via self-normalizations. Ann. Probab., 19(1):380–395, 1991.

- [8] M. Kumon and A. Takemura. On a simple strategy weakly forcing the strong law of large numbers in the bounded forecasting game. Ann. Inst. Statist. Math., 60(4):801–812, 2008.

- [9] M. Kumon, A. Takemura, and K. Takeuchi. Sequential optimizing strategy in multi-dimensional bounded forecasting games. Stochastic Process. Appl., 121(1):155–183, 2011.

- [10] K. Miyabe and A. Takemura. The law of the iterated logarithm in game-theoretic probability with quadratic and stronger hedges. Stochastic Process. Appl., 123(8):3132–3152, 2013.

- [11] K. Miyabe and A. Takemura. Derandomization in game-theoretic probability. Stochastic Process. Appl., 125(1):39–59, 2015.

- [12] E. Ordentlich and T. M. Cover. The cost of achieving the best portfolio in hindsight. Math. Oper. Res., 23(4):960–982, 1998.

- [13] P. Révész. Random Walk in Random and Non-Random Environments. World Scientific Publishing Co. Pte. Ltd., Hackensack, NJ, third edition, 2013.

- [14] T. Sasai, K. Miyabe, and A. Takemura. Erdős-Feller-Kolmogorov-Petrowsky law of the iterated logarithm for self-normalized martingales: a game-theoretic approach, 2015. arXiv:1504.06398 [math.PR].

- [15] G. Shafer and V. Vovk. Probability and Finance: It’s only a game! Wiley-Interscience, New York, 2001.

- [16] Q.-M. Shao and Q. Wang. Self-normalized limit theorems: a survey. Probab. Surv., 10:69–93, 2013.

- [17] V. Vovk and C. Watkins. Universal portfolio selection. In Proceedings of the Eleventh Annual Conference on Computational Learning Theory (Madison, WI, 1998), pages 12–23 (electronic). ACM, New York, 1998.

- [18] Q. Wang. Kolmogrov and Erdős test for self-normalized sums. Statist. Probab. Lett., 42(3):323–326, 1999.