Extreme value analysis for the sample autocovariance matrices of heavy-tailed multivariate time series

Abstract.

We provide some asymptotic theory for the largest eigenvalues of a sample covariance matrix of a -dimensional time series where the dimension converges to infinity when the sample size increases. We give a short overview of the literature on the topic both in the light- and heavy-tailed cases when the data have finite (infinite) fourth moment, respectively. Our main focus is on the heavy-tailed case. In this case, one has a theory for the point process of the normalized eigenvalues of the sample covariance matrix in the iid case but also when rows and columns of the data are linearly dependent. We provide limit results for the weak convergence of these point processes to Poisson or cluster Poisson processes. Based on this convergence we can also derive the limit laws of various functionals of the ordered eigenvalues such as the joint convergence of a finite number of the largest order statistics, the joint limit law of the largest eigenvalue and the trace, limit laws for successive ratios of ordered eigenvalues, etc. We also develop some limit theory for the singular values of the sample autocovariance matrices and their sums of squares. The theory is illustrated for simulated data and for the components of the S&P 500 stock index.

Key words and phrases:

Regular variation, sample covariance matrix, dependent entries, largest eigenvalues, trace, point process convergence, cluster Poisson limit, infinite variance stable limit, Fréchet distribution1991 Mathematics Subject Classification:

Primary 60B20; Secondary 60F05 60F10 60G10 60G55 60G701. Estimation of the largest eigenvalues: an overview in the iid case

1.1. The light-tailed case

One of the exciting new areas of statistics is concerned with analyses of large data sets. For such data one often studies the dependence structure via covariances and correlations. In this paper we focus on one aspect: the estimation of the eigenvalues of the covariance matrix of a multivariate time series when the dimension of the series increases with the sample size . In particular, we are interested in limit theory for the largest eigenvalues of the sample covariance matrix. This theory is closely related to topics from classical extreme value theory such as maximum domains of attraction with the corresponding normalizing and centering constants for maxima; cf. Embrechts et al. [17], Resnick [29, 30]. Moreover, point process convergence with limiting Poisson and cluster Poisson processes enters in a natural way when one describes the joint convergence of the largest eigenvalues of the sample covariance matrix. Large deviation techniques find applications, linking extreme value theory with random walk theory and point process convergence. The objective of this paper is to illustrate some of the main developments in random matrix theory for the particular case of the sample covariance matrix of multivariate time series with independent or dependent entries. We give special emphasis to the heavy-tailed case when extreme value theory enters in a rather straightforward way.

Classical multivariate time series analysis deals with observations which assume values in a -dimensional space where is “relatively small” compared to the sample size . With the availability of large data sets can be “large” relative to . One of the possible consequences is that standard asymptotics (such as the central limit theorem) break down and may even cause misleading results.

The dependence structure in multivariate data is often summarized by the covariance matrix which is typically estimated by its sample analog. For example, principal component analysis (PCA) extracts principal component vectors corresponding to the largest eigenvalues of the sample covariance matrix. The magnitudes of these eigenvalues provide an empirical measure of the importance of these components.

If are fixed, a column of the data matrix

represents an observation of a -dimensional time series model with unknown parameters. In this section we assume that the real-valued entries are iid, unless mentioned otherwise, and we write for a generic element. One challenge is to infer information about the parameters from the eigenvalues of the sample covariance matrix . In the notation we suppress the dependence of on and . If and are finite and the columns of are iid and multivariate normal, Muirhead [27] derived a (rather complicated) formula for the joint distribution of the eigenvalues .

For fixed and , assuming has centered normal entries and a diagonal covariance matrix , Anderson [1] derived the joint asymptotic density of . We quote from Johnstone [25]: “The classic paper by Anderson [1] gives the limiting joint distribution of the roots, but the marginal distribution of the largest eigenvalue is hard to extract even in the null case” (i.e., when the covariance matrix is proportional to the identity matrix).

It turns out that limit theory for the largest eigenvalues becomes “easier” when the dimension increases with . Over the last 15 years there has been increasing interest in the case when as . In most of the literature (exceptions are El Karoui [15], Davis et al. [11, 12] and Heiny and Mikosch [21]) one assumes that and grow at the same rate:

| (1.1) |

In random matrix theory, the convergence of the empirical spectral distributions of a sequence of non-negative definite matrices is the principle object of study. The empirical spectral distribution is constructed from the eigenvalues via

In the literature convergence results for the sequence of empirical spectral distributions are established under the assumption that and grow at the same rate. Suppose that the iid entries have mean and variance . If (1.1) holds, then, with probability one, converges to the celebrated Marčenko–Pastur law with absolutely continuous part given by the density,

| (1.4) |

where and . The Marčenko–Pastur law has a point mass at the origin if , cf. Bai and Silverstein [3, Chapter 3]. The point mass at zero is intuitively explained by the fact that, with probability , eigenvalues are non-zero. When and one sees that the proportion of non-zero eigenvalues of the sample covariance matrix is while the proportion of zero eigenvalues is .

While the finite second moment is the central assumption to obtain the Marčenko–Pastur law as the limiting spectral distribution, the finite fourth moment plays a crucial role when studying the largest eigenvalues

| (1.5) |

of , where we suppress the dependence on in the notation.

Assuming (1.1) and iid entries with zero mean, unit variance and finite fourth moment, Geman [20] showed that

| (1.6) |

Johnstone [25] complemented this strong law of large numbers by the corresponding central limit theorem in the special case of iid standard normal entries:

| (1.7) |

where the limiting random variable has a Tracy–Widom distribution of order 1. Notice that the centering can in general not be replaced by . This distribution is ubiquitous in random matrix theory. Its distribution function is given by

where is the unique solution to the Painlevé II differential equation

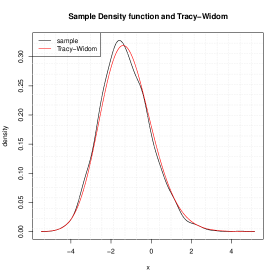

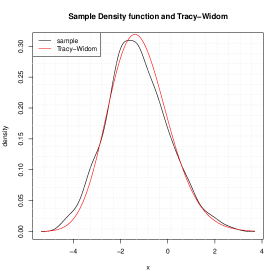

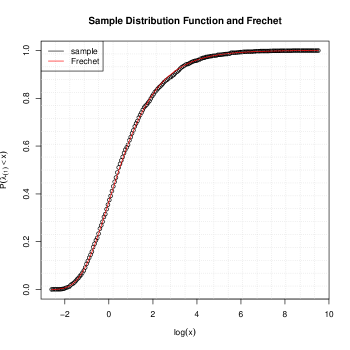

where as and Ai is the Airy kernel; see Tracy and Widom [35] for details. We notice that the rate compares favorably to the -rate in the classical central limit theorem for sums of iid finite variance random variables. The calculation of the spectrum is facilitated by the fact that the distribution of the classical Gaussian matrix ensembles is invariant under orthogonal transformations. The corresponding computation for non-invariant matrices with non-Gaussian entries is more complicated and was a major challenge for several years; a first step was made by Johansson [24]. Johnstone’s result was extended to matrices with iid non-Gaussian entries by Tao and Vu [34, Theorem 1.16]. Assuming that the first four moments of the entry distribution match those of the standard normal distribution, they showed (1.7) by employing Lindeberg’s replacement method, i.e., the iid non-Gaussian entries are replaced step-by-step by iid Gaussian ones. This approach is well-known from summation theory for sequences of iid random variables. Tao and Vu’s result is a consequence of the so-called Four Moment Theorem, which describes the insensitivity of the eigenvalues with respect to changes in the distribution of the entries. To some extent (modulo the strong moment matching conditions) it shows the universality of Johnstone’s limit result (1.7). Later we will deal with entries with infinite fourth moment. In this case, the weak limit for the normalized largest eigenvalue is distinct from the Tracy–Widom distribution: the classical Fréchet extreme value distribution appears. In Figure 1 we illustrate how the Tracy–Widom approximation works for Gaussian and non-Gaussian entries of and in Figure 2 we also illustrate that this approach fails when .

Figure 1 compares the sample density function of the properly normalized largest eigenvalue estimated from 2000 simulated sample covariance matrices () with the Tracy–Widom density. If has infinite fourth moment and further regularity conditions on the tail hold then the Tracy–Widom limiting law needs to be replaced by the Fréchet distribution; see Section 1.2 for details. Figure 2 illustrates this fact with a simulated ensemble whose entries are distributed according to the heavy-tailed distribution from (4.3) below with .

1.2. The heavy-tailed case

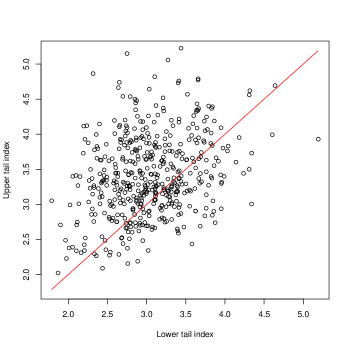

So far we focused on “light-tailed” in the sense that its entries have finite fourth moment. However, there is statistical evidence that the assumption of finite fourth moment may be violated when dealing with data from insurance, finance or telecommunications. We illustrate this fact in Figure 3 where we show the pairs of lower and upper tail indices of log-return series composing the S&P 500 index estimated from daily observations from 01/04/2010 to 02/28/2015. This means we assume for every row of that the tails behave like

for non-negative constants . We apply the Hill estimator (see Embrechts et al. [17], p. 330, de Haan and Ferreira [13], p. 69) to the time series of the gains and losses in a naive way, neglecting the dependence and non-stationarity in the data; we also omit confidence bands. From the figure it is evident that the majority of the return series have tail indices below four, corresponding to an infinite fourth moment.

The behavior of the largest eigenvalue changes dramatically when has infinite fourth moment. Bai and Silverstein [4] proved for an matrix with iid centered entries that

| (1.8) |

This is in stark contrast to Geman’s result (1.6).

In the heavy-tailed case it is common to assume a regular variation condition:

| (1.9) |

where are non-negative constants such that and is a slowly varying function. In particular, if we have . The regular variation condition on (we will also refer to as a regularly varying random variable) is needed for proving asymptotic theory for the eigenvalues of . This is similar to proving limit theory for sums of iid random variables with infinite variance stable limits; see for example Feller [19].

In (1.4) we have seen that the sequence of empirical spectral distributions converges to the Marčenko–Pastur law if the centered iid entries possess a finite second moment. Now we will discuss the situation when the entries are still iid and centered, but have an infinite variance. Here we assume the entries to be regularly varying with index . Assuming (1.1) with in this infinite variance case, Belinschi et al. [5, Theorem 1.10] showed that the sequence converges with probability one to a non-random probability measure with density satisfying

see also Ben Arous and Guionnet [7, Theorem 1.6]. The normalization is chosen such that as . An application of the Potter bounds (see Bingham et al. [9, p. 25]) shows that .

It is interesting to note that there is a phase change in the extreme eigenvalues in going from finite to infinite fourth moment, while the phase change occurs for the empirical spectral distribution going from finite to infinite variance.

The theory for the largest eigenvalues of sample covariance matrices with heavy tails is less developed than in the light-tailed case. Pioneering work for in the case of iid regularly varying entries with index is due to Soshnikov [32, 33]. He showed the point process convergence

| (1.10) |

under the growth condition (1.1) on . Here

| (1.11) |

and is an iid standard exponential sequence. In other words, is a Poisson point process on with mean measure , . Convergence in distribution of point processes is understood in the sense of weak convergence in the space of point measures equipped with the vague topology; see Resnick [29, 30]. We can easily derive the limiting distribution of for fixed from (1.10):

In particular,

where the limit has Fréchet distribution with parameter and distribution function

We mention that the tail balance condition (1.9) may be replaced in this case by the weaker assumption for a slowly varying function . Indeed, it follows from the proof that only the squares contribute to the point process limits of the eigenvalues . A consequence of the continuous mapping theorem and (1.10) is the joint convergence of the upper order statistics: for any ,

It follows from standard theory for point processes with iid points (e.g. Resnick [29, 30]) that (1.10) remains valid if we replace by the point process . Then we also have for any ,

| (1.12) |

where

denote the order statistics of .

Auffinger et al. [2] showed that (1.10) remains valid under the regular variation condition (1.9) for , the growth condition (1.1) on and the additional assumption . Of course, (1.12) remains valid as well. Davis et al. [12] extended these results to the case when the rows of are iid linear processes with iid regularly varying noise. The Poisson point process convergence result of (1.10) remains valid in this case. Different limit processes can only be expected if there is dependence across rows and columns.

In what follows, we refer to the heavy-tailed case when we assume the regular variation condition (1.9) for some .

1.3. Overview

The primary objective of this overview is to make a connection between extreme value theory and the behavior of the largest eigenvalues of sample covariance matrices from heavy-tailed multivariate time series. For time series that are linearly dependent through time and across rows, it turns out that the extreme eigenvalues are essentially determined by the extreme order statistics from an array of iid random variables. The asymptotic behavior of the extreme eigenvalues is then derived routinely from classical extreme value theory. As such, explicit joint distributions of the extreme order statistics can be given which yield a plethora of ancillary results. Convergence of the point process of extreme eigenvalues, properly normalized, plays a central role in establishing the main results.

In Section 2 we continue the study of the case when the data matrix consists of iid heavy-tailed entries. We will consider power-law growth rates on the dimension that is more general than prescribed by (1.1). In Section 3 we introduce a model for which allows for linear dependence across the rows and through time. The point process convergence of normalized eigenvalues is presented in Section 3.4. This result lays the foundation for new insight into the spectral behavior of the sample covariance matrix, which is the content of Section 4.1.

Sections 4.1 and 4.3 are devoted to sample autocovariance matrices. Motivated by [26], we study the eigenvalues of sums of transformed matrices and illustrate the results in two examples. These results are applied to the time series of S&P 500 in Section 4.2. Appendix A contains useful facts about regular variation and point processes.

2. General growth rates for in the iid heavy-tailed case

This section is based on ideas in Heiny and Mikosch [21] where one can also find detailed proofs.

Growth conditions on

In many applications it is not realistic to assume that the dimension of the data and the sample size grow at the same rate. The aforementioned results of Soshnikov [32, 33] and Auffinger et al. [2] already indicate that the value in the growth rate (1.1) does not appear in the distributional limits. This obervation is in contrast to the light-tailed case; see (1.6) and (1.7). Davis et al. [11, 12] and Heiny and Mikosch [21] allowed for more general rates for than linear growth in . Recall that is the number of rows in the matrix . We need to specify the growth rate of to ensure a non-degenerate limit distribution of the normalized singular values of the sample autocovariance matrices. To be precise, we assume

| () |

where is a slowly varying function and . If , we also assume . Condition is more general than the growth conditions in the literature; see [2, 11, 12].

Theorem 2.1.

Assume that has iid entries satisfying the regular variation condition (1.9) for some . If we also suppose that . Let be an integer sequence satisfying with . In addition, we require

| () |

Then

| (2.1) |

where the convergence holds in the space of point measures with state space equipped with the vague toplogy; see Resnick [29].

A discussion of the case

We mentioned earlier that in the heavy-tailed case, limit theory for the largest eigenvalues of the sample covariance matrix is rather insensitive to the growth rate of and that the limits are essentially determined by the diagonal of this matrix. This is confirmed by the following result.

Proposition 2.2.

Proposition 2.2 is not unexpected for two reasons:

-

•

It is well-known from classical theory (see Embrechts and Veraverbeke [18]) that for any iid regularly varying non-negative random variables with index , is regularly varying with index while is regularly varying with index . Therefore and are regularly varying with indices and , respectively.

-

•

The aforementioned tail behavior is inherited by the entries of in the following sense. By virtue of Nagaev-type large deviation results for an iid regularly varying sequence with index where we also assume that if (see Theorem A.1) we have that converges to a non-negative constant provided , where as . As a consequence of the tail behaviors of and for and Nagaev’s results we have for such that ,

where or according as or . This means that the diagonal and off-diagonal entries of inherit the tails of and , , respectively, above the high threshold .

Proposition 2.2 has some immediate consequences for the approximation of the eigenvalues of by those of . Indeed, let be a symmetric matrix with eigenvalues and ordered eigenvalues

| (2.2) |

Then for any symmetric matrices , by Weyl’s inequality (see Bhatia [8]),

If we now choose and we obtain the following result.

Corollary 2.3.

Under the conditions of Proposition 2.2,

Thus the problem of deriving limit theory for the order statistics of has been reduced to limit theory for the order statistics of the iid row-sums

which are the eigenvalues of . This theory is completely described by the point processes constructed from the points . Necessary and sufficient conditions for the weak convergence of these point processes are provided by Lemma A.2 which in combination with the Nagaev-type large deviation results of Theorem A.1 yield the following result; see also Davis et al. [11].

Lemma 2.4.

Extension to general

Next we explain that it suffices to consider only the case and how to proceed when . The main reason is that the sample covariance matrix and the matrix have the same rank and their non-zero eigenvalues coincide; see Bhatia [8, p. 64]. When proving limit theory for the eigenvalues of the sample covariance matrix one may switch to and vice versa, hereby interchanging the roles of and . By switching to , one basically replaces by . Since for any , one can assume without loss of generality that . This trick allows one to extend results for satisfying with to . We illustrate this approach by providing the direct analogs of Proposition 2.2 and Corollary 2.3.

Proposition 2.5.

Assume that has iid entries satisfying the regular variation condition (1.9) for some . If we also suppose that . Then for any sequence satisfying with we have

where denotes the spectral norm.

Note that for we have . This means that has asymptotically a much smaller dimension than and therefore it is more convenient to work with when bounding the spectral norm.

Corollary 2.6.

Under the conditions of Proposition 2.5,

3. Introducing dependence between the rows and columns

For details on the results of this section, we refer to Davis et al. [11], Heiny and Mikosch [21] and Heiny et al. [22].

3.1. The model

When dealing with covariance matrices of a multivariate time series it is rather natural to assume dependence between the entries . In this section we introduce a model which allows for linear dependence between the rows and columns of :

| (3.1) |

where is a field of iid random variables and is an array of real numbers. Of course, linear dependence is restrictive in some sense. However, the particular dependence structure allows one to determine those ingredients in the sample covariance matrix which contribute to its largest eigenvalues. If the series in (3.1) converges a.s. constitutes a strictly stationary random field. We denote generic elements of the - and -fields by and , respectively. We assume that is regularly varying in the sense that

| (3.2) |

for some tail index , constants with and a slowly varying . We will assume whenever . Moreover, we require the summability condition

| (3.3) |

for some which ensures the a.s. absolute convergence of the series in (3.1). Under the conditions (3.2) and (3.3), the marginal and finite-dimensional distributions of the field are regularly varying with index ; see Embrechts et al. [17], Appendix A3.3. Therefore we also refer to and as regularly varying fields.

3.2. Sample covariance and autocovariance matrices

From the field we construct the matrices

| (3.4) |

As before, we will write . Now we can introduce the (non-normalized) sample autocovariance matrices

| (3.5) |

We will refer to as the lag. For , we obtain the sample covariance matrix. In what follows, we will be interested in the asymptotic behavior (of functions) of the eigen- and singular values of the sample covariance and autocovariance matrices in the heavy-tailed case. Recall that the singular values of a matrix are the square roots of the eigenvalues of the non-negative definite matrix and its spectral norm is its largest singular value. We notice that is not symmetric and therefore its eigenvalues can be complex. To avoid this situation, we use the squares

| (3.6) |

whose eigenvalues are the squares of the singular values of . The idea of using the sample autocovariance matrices and functions of their squares (3.6) originates from a paper by Lam and Yao [26] who used a model different from (3.1). This idea is quite natural in the context of time series analysis.

In Theorem 3.1 below, we provide a general approximation result for the ordered singular values of the sample autocovariance matrices in the heavy-tailed case. This result is rather technical. To formulate it we introduce further notation. As before, is any integer sequence converging to infinity.

3.3. More notation

Important roles are played by the quantities and their order statistics

| (3.7) |

As important are the row-sums

| (3.8) |

with generic element and their ordered values

| (3.9) |

where we assume without loss of generality that is a permutation of for fixed .

Finally, we introduce the column-sums

with generic element and we also adapt the notation from (3.9) to these quantities.

Matrix norms

Singular values of the sample autocovariance matrices

Fix integers and . We recycle the -notation for the singular values of the sample autocovariance matrix , suppressing the dependence on . Correspondingly, the order statistics are denoted by

| (3.11) |

When we typically write instead of .

The matrix

We introduce some auxiliary matrices derived from the coefficient matrix :

Notice that

| (3.12) |

We denote the ordered singular values of by

| (3.13) |

Let be the rank of so that while if is finite, otherwise for all . We also write .

Under the summability condition (3.3) on for fixed ,

| (3.14) | |||||

Therefore all singular values are finite and the ordering (3.13) is justified.

Here and in what follows, we write for any constant whose value is not of interest.

Normalizing sequence

We define by

and choose the normalizing sequence for the singular values as for suitable sequences .

Approximations to singular values

We will give approximations to the singular values in terms of the largest ordered values for ,

from the sets

respectively.

3.4. Approximation of the singular values

In the following result we povide some useful approximations to the singular values of the sample autocovariance matrices of the linear model (3.1).

Theorem 3.1.

Remark 3.2.

3.5. Point process convergence

Theorem 3.1 and arguments similar to the proofs in Davis et al. [11] enable one to derive the weak convergence of the point processes of the normalized singular values. Recall the representation of the points of a unit rate homogeneous Poisson process on given in (1.11). For , we define the point processes of the normalized singular values:

| (3.16) |

Theorem 3.4.

Assume the conditions of Theorem 3.1. Then converge weakly in the space of point measures with state space equipped with the vague topology. If either , and , or , and hold then

| (3.17) |

Proof.

Regular variation of is equivalent to

| (3.18) |

where denotes vague convergence of Radon measures on and the measure is given by , . In view of Resnick [30], Proposition 3.21, (3.18) is equivalent to the weak convergence of the following point processes:

where the limit is a Poisson random measure (PRM) with state space and mean measure .

Since as , the point processes converge weakly to the same PRM:

| (3.19) |

A continuous mapping argument together with the fact that (see (3.14)) shows that

If the assumptions of part (1) of Theorem 3.1 are satisfied an application of (3.15) (also recalling the definition of ) shows that (3.19) remains valid with the points replaced by .

The only cases which are not covered by Theorem 3.1(1) are , and , , . In these cases we get from Theorem A.1 that

i.e., . It follows from Lemma A.2 that . As before, a continuous mapping argument in combination with the approximation obtained in Theorem 3.1(2) justifies the replacement of the points by in the case . If one has to work with the quantities instead of and one may follow the same argument as above. This finishes the proof. ∎

4. Some applications

4.1. Sample covariance matrices

The sample covariance matrix is a non-negative definite matrix. Therefore its eigenvalues and singular values coincide. Moreover, , , are the eigenvalues of .

Theorem 3.1(1) yields an approximation of the ordered eigenvalues of by the quantities which are derived from the order statistics of . Part (2) of this result provides an approximation of by the quantities which are derived from the order statistics of the partial sums .

In the following example we illustrate the quality of the two approximations.

Example 4.1.

We choose a Pareto-type distribution for with density

| (4.3) |

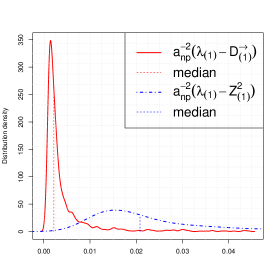

We simulated matrices for and whose iid entries have this density. We assume . Note that has rank one and . The estimated densities of the deviations and based on the simulations are shown in Figure 4. The approximation error is very small indeed.

According to the theory,

but for finite the sequence yields a better approximation to . By construction, the considered differences have a tendency to be positive but Figure 4 also shows that the median of the approximation error for is almost zero.

Theorem 3.4 and the continuous mapping theorem immediately yield results about the joint convergence of the largest eigenvalues of the matrices for and when satisfies . For fixed one gets

where are the largest ordered values of the set . The continuous mapping theorem yields for ,

| (4.4) |

An application of the continuous mapping theorem to the distributional convergence of the point processes in Theorem 3.4 in the spirit of Resnick [29], Theorem 7.1, also yields the following result; see Davis et al. [11] for a proof and a similar result in the case .

Corollary 4.2.

Assume the conditions of Theorem 3.1. If and , then

where is Fréchet -distributed. and has the distribution of a positive -stable random variable. In particular,

| (4.5) |

Remark 4.3.

The ratio

plays an important role in PCA. It reflects the proportion of the total variance in the data that we can explain by the first principal components. It follows from Corollary 4.2 that for fixed ,

Unfortunately, the limiting variable does in general not have a clean form. An exception is the case when ; see Example 4.6. Also notice that the trace of coincides with .

To illustrate the theory we consider a simple moving average example taken from Davis et al. [11].

Example 4.4.

Assume that and

| (4.6) |

In this case, the non-zero entries of are

Hence has the positive eigenvalues and . The limit point process in (3.17) is

so that

Using the fact that has a uniform distribution on we calculate

In particular, we have for the normalized spectral gap

and for the self-normalized spectral gap (see also Example 4.5 for a detailed analysis)

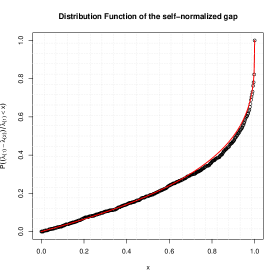

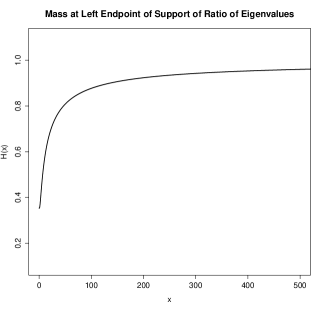

The limit distribution of the spectral gap has an atom at with probability , i.e., , and

In the iid case the limit distribution of the self-normalized spectral gap has distribution function for . This means that the atom disappears if the entries are iid. Figure 5 compares the distribution function of with for ; the atom at is clearly visible.

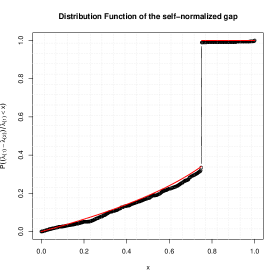

Along the same lines, we also have

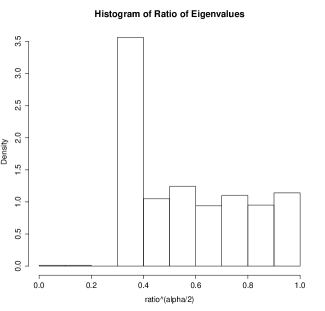

and hence the limit distribution of is supported on with mass of at . The histogram of the ratio based on 1000 replications from the model (4.6) with noise given by a -distribution with degrees of freedom, and is displayed in Figure 6.

Observing that , the histogram is remarkably close to what one would expect from a sample from the truncated uniform distribution, . The mass of the limiting discrete component of the ratio can be much larger if one conditions on being large. Specifically, for any and ,

The function approaches as indicating the speed at which the two largest eigenvalues get linearly related; see Figure 7 for a graph of in the case .

Example 4.5.

The previous example also illustrates the behavior of the two largest eigenvalues in the general case when the rank of the matrix is larger than one. We have in general

In particular, the limiting self-normalized spectral gap has representation

The limiting variable assumes values in and has an atom at the right end-point. This is in contrast to the iid case and to the case when (hence ) including the case of iid rows and the separable case; see Example 4.6.

Example 4.6.

We consider the separable case when , , where , are real sequences such that the conditions on in Theorem 3.1 hold. In this case,

Note that with the only non-negative eigenvalue

In this case, the limiting point process in Theorem 3.4 is a PRM on with mean measure of given by , . The normalized eigenvalues have similar asymptotic behavior as in the case of iid entries. For example, the log-spacings have the same limit as in the iid case for fixed ,

The same observation applies to the ratio of the largest eigenvalue and the trace in the case :

We also mentioned in Example 4.5 that the distributional limit of the self-normalized spectral gap has no atom as in the iid case.

4.2. S&P 500 data

We conduct a short analysis of the largest eigenvalues of the univariate log-return time series which compose the S&P 500 stock index; see Section 1.2 for a description of the data. Although there is strong empirical evidence that these univariate series have power-law tails (see Figure 3) we do not expect that they have the same tail index. One way to proceed would be to ignore this fact because the tail indices are in a close range and the differences are due to large sampling errors for estimating such quantities. One could also collect time series with similar tail indices in the same group. In this case, the dimension decreases. This grouping would be a rather arbitrary classification method. We have chosen a third way: to use rank transforms. This approach has its merits because it aims at standardizing the tails but it also has a major disadvantage: one destroys the covariance structure underlying the data.

Given a matrix , we construct a matrix via the rank transforms

If the rows were iid (or, more generally, stationary ergodic) with a continuous distribution then the averages under the logarithm would be asymptotically uniform on as . Hence would be asymptotically standard Fréchet -distributed. In what follows, we assume that the aforementioned univariate time series of the S&P 500 index have undergone the rank transform and that their marginal distributions are close to ; we always use the symbol for the resulting multivariate series.

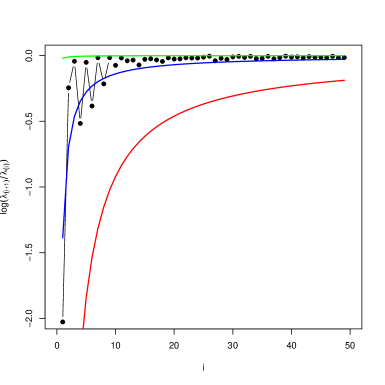

In Figure 8 we show the ratios of the consecutive ordered eigenvalues of the matrix . This graph shows the rather surprising fact that the ratios are close to one even for small values . We also show the 1, 50 and 99 % quantiles of the variables calculated from the formula

| (4.7) |

For increasing , the distribution is concentrated closely to 1, in agreement with the strong law of large numbers which yields as . The asymptotic distributions (4.7) correspond to the case when the matrix has rank . It includes the iid and separable cases; see Example 4.6. The shown asymptotic quantiles are in agreement with the rank hypothesis.

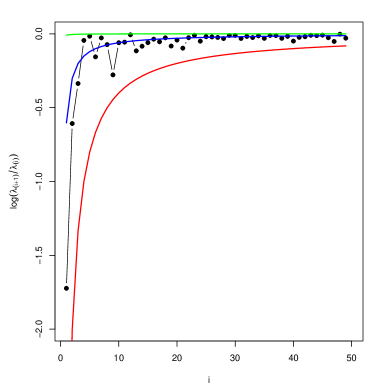

For comparison, in Figure 9 we also show the ratios for the non-rank transformed S&P 500 data and the 1, 50 and 99% quantiles of the variables , where we choose motivated by the estimated tail indices in Figure 3. The two graphs in Figure 8 and Figure 9 are quite similar but the smallest ratios for the original data are slightly larger than for the rank-transformed data.

4.3. Sums of squares of sample autocovariance matrices

In this section we consider some additive functions of the squares of given by for . By definition of the singular values of a matrix (see (3.11)), the non-negative definite matrix has eigenvalues .

The following result is a corollary of Theorem 3.1.

Proposition 4.7.

To the best of our knowledge, sums of squares of sample autocovariance matrices were used first in the paper by Lam and Yao [26]; their time series model is quite different from ours.

Proof.

Part (1). The proof follows from Theorem 3.1 if we can show that

We have by Theorem 3.4,

| (4.8) |

where has a distribution. In view of Theorem 3.1(1) we also have

Therefore, again using Theorem 3.1(1), we have

This proves part (1).

Part (2). Now assume and , or , and . Then (4.8) is still true and we have by Theorem 3.1(2) and Theorem 3.4

We then have

The proof of the remaining part is similar and therefore omitted. ∎

Now, using Proposition 4.7 and a continuous mapping argument, we can show limit theory for the eigenvalues

of the non-negative definite random matrices

| (4.9) |

Proposition 4.8.

Assume and the conditions of Theorem 3.1 hold. If and then

where are the ordered values of the set and are the ordered eigenvalues of .

Example 4.9.

Recall the separable case from Example 4.6, i.e., , , where , are real sequences such that the conditions on in Theorem 3.1 hold. Write . It is symmetric and has rank one; the only non-zero eigenvalue is . Hence is non-negative definite. We get from (3.12) that

where

The matrix has the only non-zero eigenvalue . The factors can be positive or negative; they constitute the autocovariance function of a stationary linear process with coefficients . Accordingly, is either non-negative or non-positive definite. Now we consider the non-negative definite matrix

This matrix has rank and its largest eigenvalue is given by

An application of Proposition 4.8 yields that the ordered eigenvalues of are uniformly approximated by the quantities

| (4.10) |

Since

one gets the remarkable property that

In particular, for we get the weak convergence of the point processes towards a PRM:

Example 4.10.

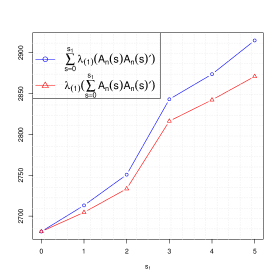

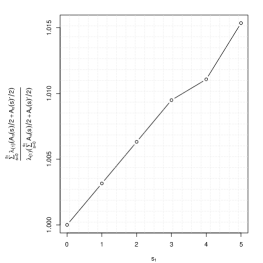

In Figure 10 we calculate the largest eigenvalues for as well as the sums of the largest eigenvalues the log-return series from the S&P 500 index described in Section 1.2. The data are not rank-transformed. We notice that the two values are surprisingly close across the values . This phenomenon could be explained by the structure of the eigenvalues in Example 4.9. Also note that the largest eigenvalue makes a major contribution to the values in Figure 10; the contribution of the squares , to the largest eigenvalue of the sum of squares is less substantial.

Appendix A Auxiliary results

Let be iid copies of whose distribution satisfies

for some tail index , where with and is a slowly varying function. If also assume . The product is regular varying with the same index and , where is slowly varying function different from ; see Embrechts and Goldie [16]. Write

and consider a sequence such that .

A.1. Large deviation results

The following theorem can be found in Nagaev [28] and Cline and Hsing [10] for and , respectively; see also Denisov et al. [14].

Theorem A.1.

Under the assumptions on the iid sequence given above the following relation holds

where is any sequence satisfying for and for .

A.2. A point process convergence result

Assume that the conditions at the beginning of Appendix A hold. Consider a sequence of iid copies of and the sequence of point processes

for an integer sequence . We assume that the state space of the point processes is .

Lemma A.2.

Acknowledgments

We thank Olivier Wintenberger for reading the manuscript and fruitful discussions.

References

- [1] Anderson, T. W. Asymptotic theory for principal component analysis. Ann. Math. Statist. 34 (1963), 122–148.

- [2] Auffinger, A., Ben Arous, G., and Péché, S. Poisson convergence for the largest eigenvalues of heavy tailed random matrices. Ann. Inst. Henri Poincaré Probab. Stat. 45, 3 (2009), 589–610.

- [3] Bai, Z., and Silverstein, J. W. Spectral Analysis of Large Dimensional Random Matrices, second ed. Springer Series in Statistics. Springer, New York, 2010.

- [4] Bai, Z. D., Silverstein, J. W., and Yin, Y. Q. A note on the largest eigenvalue of a large-dimensional sample covariance matrix. J. Multivariate Anal. 26, 2 (1988), 166–168.

- [5] Belinschi, S., Dembo, A., and Guionnet, A. Spectral measure of heavy tailed band and covariance random matrices. Comm. Math. Phys. 289, 3 (2009), 1023–1055.

- [6] Belitskiĭ, G. R., and Lyubich, Y. I. Matrix Norms and their Applications, vol. 36 of Operator Theory: Advances and Applications. Birkhäuser Verlag, Basel, 1988.

- [7] Ben Arous, G., and Guionnet, A. The spectrum of heavy tailed random matrices. Comm. Math. Phys. 278, 3 (2008), 715–751.

- [8] Bhatia, R. Matrix Analysis, vol. 169 of Graduate Texts in Mathematics. Springer-Verlag, New York, 1997.

- [9] Bingham, N. H., Goldie, C. M., and Teugels, J. L. Regular Variation, vol. 27 of Encyclopedia of Mathematics and its Applications. Cambridge University Press, Cambridge, 1987.

- [10] Cline, D. B. H., and Hsing, T. Large deviation probabilities for sums of random variables with heavy or subexponential tails. Technical report. Statistics Dept., Texas A&M University. (1998).

- [11] Davis, R. A., Mikosch, T., and Pfaffel, O. Asymptotic theory for the sample covariance matrix of a heavy-tailed multivariate time series. Stochastic Process. Appl. (2015).

- [12] Davis, R. A., Pfaffel, O., and Stelzer, R. Limit theory for the largest eigenvalues of sample covariance matrices with heavy-tails. Stochastic Process. Appl. 124, 1 (2014), 18–50.

- [13] de Haan, L., and Ferreira, A. Extreme Value Theory: An Introduction. Springer Series in Operations Research and Financial Engineering. Springer, New York, 2006.

- [14] Denisov, D., Dieker, A. B., and Shneer, V. Large deviations for random walks under subexponentiality: the big-jump domain. Ann. Probab. 36, 5 (2008), 1946–1991.

- [15] El Karoui, N. On the largest eigenvalue of wishart matrices with identity covariance when n,p and p/n tend to infinity. Available at http://arxiv.org/abs/math/0309355 (2003).

- [16] Embrechts, P., and Goldie, C. M. On closure and factorization properties of subexponential and related distributions. J. Austral. Math. Soc. Ser. A 29, 2 (1980), 243–256.

- [17] Embrechts, P., Klüppelberg, C., and Mikosch, T. Modelling Extremal Events for Insurance and Finance, vol. 33 of Applications of Mathematics (New York). Springer, Berlin, 1997.

- [18] Embrechts, P., and Veraverbeke, N. Estimates for the probability of ruin with special emphasis on the possibility of large claims. Insurance Math. Econom. 1, 1 (1982), 55–72.

- [19] Feller, W. An Introduction to Probability Theory and its Applications. Vol. II. John Wiley & Sons, Inc., New York-London-Sydney, 1966.

- [20] Geman, S. A limit theorem for the norm of random matrices. Ann. Probab. 8, 2 (1980), 252–261.

- [21] Heiny, J., and Mikosch, T. Eigenvalues and eigenvectors of heavy-tailed sample covariance matrices with general growth rates: the iid case. Submitted (2015).

- [22] Heiny, J., Mikosch, T., and Davis, R. A. Limit theory for the singular values of the sample autocovariance matrix function of multivariate time series. Work in progress (2015).

- [23] Horn, R. A., and Johnson, C. R. Matrix Analysis, second ed. Cambridge University Press, Cambridge, 2013.

- [24] Johansson, K. Universality of the local spacing distribution in certain ensembles of Hermitian Wigner matrices. Comm. Math. Phys. 215, 3 (2001), 683–705.

- [25] Johnstone, I. M. On the distribution of the largest eigenvalue in principal components analysis. Ann. Statist. 29, 2 (2001), 295–327.

- [26] Lam, C., and Yao, Q. Factor modeling for high-dimensional time series: inference for the number of factors. Ann. Statist. 40, 2 (2012), 694–726.

- [27] Muirhead, R. J. Aspects of Multivariate Statistical Theory. John Wiley & Sons, Inc., New York, 1982. Wiley Series in Probability and Mathematical Statistics.

- [28] Nagaev, S. V. Large deviations of sums of independent random variables. Ann. Probab. 7, 5 (1979), 745–789.

- [29] Resnick, S. I. Heavy-Tail Phenomena: Probabilistic and Statistical Modeling. Springer Series in Operations Research and Financial Engineering. Springer, New York, 2007.

- [30] Resnick, S. I. Extreme Values, Regular Variation and Point Processes. Springer Series in Operations Research and Financial Engineering. Springer, New York, 2008. Reprint of the 1987 original.

- [31] Shores, T. S. Applied Linear Algebra and Matrix Analysis. Undergraduate Texts in Mathematics. Springer, New York, 2007.

- [32] Soshnikov, A. Poisson statistics for the largest eigenvalues of Wigner random matrices with heavy tails. Electron. Comm. Probab. 9 (2004), 82–91 (electronic).

- [33] Soshnikov, A. Poisson statistics for the largest eigenvalues in random matrix ensembles. In Mathematical physics of quantum mechanics, vol. 690 of Lecture Notes in Phys. Springer, Berlin, 2006, pp. 351–364.

- [34] Tao, T., and Vu, V. Random matrices: universality of local eigenvalue statistics up to the edge. Comm. Math. Phys. 298, 2 (2010), 549–572.

- [35] Tracy, C. A., and Widom, H. Distribution functions for largest eigenvalues and their applications. In Proceedings of the International Congress of Mathematicians, Vol. I (Beijing, 2002) (2002), Higher Ed. Press, Beijing, pp. 587–596.