Entropy and credit risk in highly correlated markets

Sylvia Gottschalk111Corresponding author. Middlesex University Business School, Accounting and Finance department, The Burroughs, Hendon NW4 4BT, s.gottschalk@mdx.ac.uk. We thank Sabba Hussain for exceptional research assistance. All remaining errors are ours.

Abstract: We compare two models of corporate default by calculating the Jeffreys-Kullback-Leibler divergence between their predicted default probabilities when asset correlations are either high or low. Our main results show that the divergence between the two models increases in highly correlated, volatile, and large markets, but that it is closer to zero in small markets, when asset correlations are low and firms are highly leveraged. These findings suggest that during periods of financial instability the single-and multi-factor models of corporate default will generate increasingly inconsistent predictions.

Keywords: Structural models of default risk, single and multi-factor models, asset correlation, entropy, Kullback-Leibler divergence, random correlation matrices, financial regulation.

1 Introduction

The single-factor, single-firm structural model is the cornerstone of credit risk analysis, and has thus become the building block of international financial regulation in the Basel II and III Capital Adequacy Accords (BIS, 2006, 2011). In this model pair-wise asset correlations can be ignored provided the respective assets account for an asymptotically small share of a credit portfolio (Gordy, 2003). Although there is evidence that a multi-factor model would predict default risk more accurately because it would take into account asset correlations, the computational tractability of the single-factor model offsets its oversimplifying assumptions (Pykhtin, 2004; Emmer and Tasche, 2005; Tasche, 2006).

However, asset correlations have increased significantly in the past two decades, and even more so since the 2008 financial crisis (Aït-Sahalia and Xiu, 2015; Sandoval Jr. and De Paula Franca, 2012; Pollet and Wilson, 2010; Frank, 2009; Krishnan et al., 2009; Morana and Beltratti, 2008; Duffie et al., 2009; Das et al., 2007; Rangvid, 2001; Longin and Solnik, 1995, amongst others). Higher co-movements of asset returns have negative repercussions for portfolio diversification, in which risk reduction hinges exclusively on imperfectly correlated assets. Diversification issues also arise in the risk management of portfolios of corporate debt, and of collateralised debt obligations, in which asset correlation and default correlation have been shown to be linked (Das et al., 2006; Lopez, 2004). Credit risk analysis in industry and financial regulation relies almost exclusively on default probabilities calculated using Merton (1974)’s single factor structural model, which defines default as the event of the asset value of a corporate firm being lower than the face value if its debt. Merton (1974)’s model clearly ignores asset correlations, which are introduced in extensions developed by Vasicek (1991, 2002); Tasche (2006); Zhou (2001); Cathcart and El-Jahel (2004).

This paper builds a multi-factor model where individual corporate asset value follows a geometric Brownian motion which is correlated with that of other firms. We derive the multi-factor probability distribution of asset value and run Monte Carlo simulations assuming either high or low asset correlations111in our model correlations and volatility are either both high or both low.. We also run simulations of the single-factor probability of default, i.e., the default probability of a corporate whose asset value is not correlated with that of other firms. The correlation matrices used to simulate the multi-factor default probability are randomly generated. Under the high correlation scenario, the pair-wise correlation coefficients are in the range . In a low correlation matrix all the pair-wise correlation coefficients are in . For each pair of probabilities of default, we calculate its Jeffreys-Kullback-Leibler divergence. In the context of this paper, it quantifies the extent of the misrepresentation of the actual probability of default when the single factor rather than the multi-factor model is assumed to be the correct distribution generating asset values (or vice-versa) (Golan, 2006; Zellner, 2002; Kullback and Leibler, 1951; Burbea and Rao, 1982).

Entropy measures have been extensively used in finance. The maximum entropy principle (MEP) was used to estimate the probability distribution of the underlying asset of an option using the market option prices as data in Buchen and Kelly (1996); Neri and Schneider (2012), and to estimate the price of stock and bond options in Gulko (1999, 2002). Securities derivatives in incomplete markets can also be priced by minimizing cross-entropy as shown in Branger (2004). Borland (2002); Borland and Bouchaud (2004) build an option-pricing model derived from a non-Gaussian model of stock returns, which are assumed to evolve according to a

nonlinear Fokker-Planck equation which maximizes the Tsallis nonextensive entropy. Finally, Maasoumi and Racine (2002) develop an entropy metric of dependence to show -amongst other results- that stock returns are serially dependent.

Our results show that the probability of default of an uncorrelated firm diverges significantly from that of a multi-correlated firm when asset correlations are high, but that it diverges much less when asset correlations are low. In some cases, the divergence is close to zero and the two models may be considered proxies for each other, namely, when asset correlations and market size are low, and the debt-to-asset-value ratio is high (150 to 200 percent). However, when market size, debt-to-value ratios and correlations are high, the two models produce inconsistent default probabilities. Clearly, as asset correlations rise the single-factor model starts to misrepresent actual default probabilities. Further cases are analysed in Section 4.

Overall, we find that the discrepancy between the two models is exacerbated when firm’s indebtedness is between 10 to 100 percent and in highly correlated markets. Our findings have implications for financial regulation. The Basel II and III Capital Adequacy Accords stipulate that capital provisions should be calculated in accordance with a single-factor, single-firm structural model (BIS, 2006, 2011). Our paper suggests that in periods of financial instability, when asset volatility and correlations increase, one of the models may misreport default risk and thus lead to inadequate capital provisions. Our results are congruent with Aït-Sahalia and Xiu (2015); Pollet and Wilson (2010); Krishnan et al. (2009). These papers find evidence that asset correlations have more predictive power than asset volatility. Further, Das et al. (2006) found that clustering of defaults occurs during times of high volatility because both default probabilities and correlation between defaults increase.

2 Multi-factor model of corporate value

Consider dependent Brownian motions defined on a probability space , where is the filtration associated with , and a probability measure. The market has firms with correlated asset values , for . satisfies the differential equation

| (1) |

where is its drift and its volatility. The Brownian motions are correlated, in the sense that , for , with correlation coefficient , for all .

, can be rewritten as a function of independent Brownian motions . Let

| (2) |

and

| (3) |

| (4) |

We show below that the volatility of , , depends on the pair-wise covariances between the stochastic processes driving the value of the other firms in the market.

Proposition 2.1.

The solution of (4) is the set of values such that

| (5) |

where is the exponential function. Moreover, is log-Normally distributed with mean

| (6) |

and variance

| (7) |

The proof can be found in Appendix A.

Default is defined as the event of the value of the -th firm, , being lower than the face value of its debt at a given time . The probability of this event is

| (8) |

where for i=1,…,N.

| (9) |

where is the cumulative Normal distribution of when .

| (10) |

and

| (11) |

where is the cumulative Normal distribution of when .

The model presented above is closely related to the single-and multi-factor models used extensively in credit risk analysis (Tasche, 2006; Pykhtin, 2004; Vasicek, 2002). In these papers, pairwise correlations between two assets are not directly modelled. It is assumed instead that both assets are correlated to one (or more) underlying factor(s), and that the assets are independent from each other conditional on the common factor(s). Their set-up can be retrieved from our model by assuming that each Brownian motion , , where is the (single) common factor, and is a firm-specific error, rather than , for as we do above.

3 Divergence measures and simulation of correlation matrices

We examine the discrepancy between (11) and (9) by measuring the Jeffreys-Kullback-Leibler divergence between these two probabilities. Let and be two probability distribution functions over , where is the number of dependent Brownian motions in Section 2 above.

The Jeffreys-Kullback-Leibler divergence measure between and is defined as

| (12) |

where

| (13) |

is the Kullback-Leibler divergence or cross-entropy222(13) reduces to the Shannon entropy when is a uniform distribution, i.e. .. (Kullback and Leibler, 1951). Although (13) does satisfy and the positivity condition whenever , it is not a true metric distance, because it is not symmetric and does not satisfy the triangle inequality (Ullah, 1996). However, it can be thought of as an “entropy distance” between and . It quantifies the loss of information occuring when considering as the correct probability distribution when the true distribution is . If we were to use the Kullback-Leibler divergence measure, we would have to arbitrarily decide whether the multi-factor or the single-factor probability of default is the true probability of default. Owing to the asymmetry of the Kullback-Leibler divergence, if the multi-factor distribution is assumed to be the true distribution, then , which differs from .

In this paper, we restrict ourselves to measuring the divergence between the probability of default resulting from two different models of corporate default without making a priori assumptions about the accuracy of any one model. Consequently, we opt for a symmetric extension of the Kullback-Leibler measure proposed in Kullback and Leibler (1951) and Burbea and Rao (1982), the Jeffreys-Kullback-Leibler divergence measure.

| (14) |

(14) remains a pseudo-metric, since it violates the triangle inequality, but it does satisfy all the other properties of a metric (Kullback and Leibler, 1951; Ullah, 1996).

3.1 Simulating correlation matrices

The most straightforward way to simulate a random correlation matrix consists of generating random data from a given distribution and then calculate their pair-wise correlations. However, the resulting matrix may not necessarily have the desired consistently high (or low) pairwise correlations. The simulated correlation structure should also be realistic. A deterministic matrix in which all off-diagonal entries are equal to 0.9 would fulfill the requirement of having a high correlation structure. It would nonetheless be a very poor proxy for the asset correlations found in most financial markets. In order to systematically generate realistic positive definite matrices with given correlations, we adapt an algorithm created by Hardin et al. (2013). In their paper, a “noise” is added to a correlation matrix in such a way that the resulting matrix will have blocks of pair-wise correlations whose values are within a predetermined range.

More precisely, let be a matrix generated by calculating the pairwise correlations of random data. From a Uniform probability distribution we draw a “noise” which is added to , , subject to the restriction that the resulting entry , , should be between . In our “high asset correlation” scenario, all the entries are within or within . In the “low asset correlation” alternative, all the entries are within or within .

Our main modification to Hardin et al. (2013)’s algorithm is that we allow , and to be negative, since financial asset correlations can be either positive or negative. In their paper correlations are always positive.

4 Results and discussion

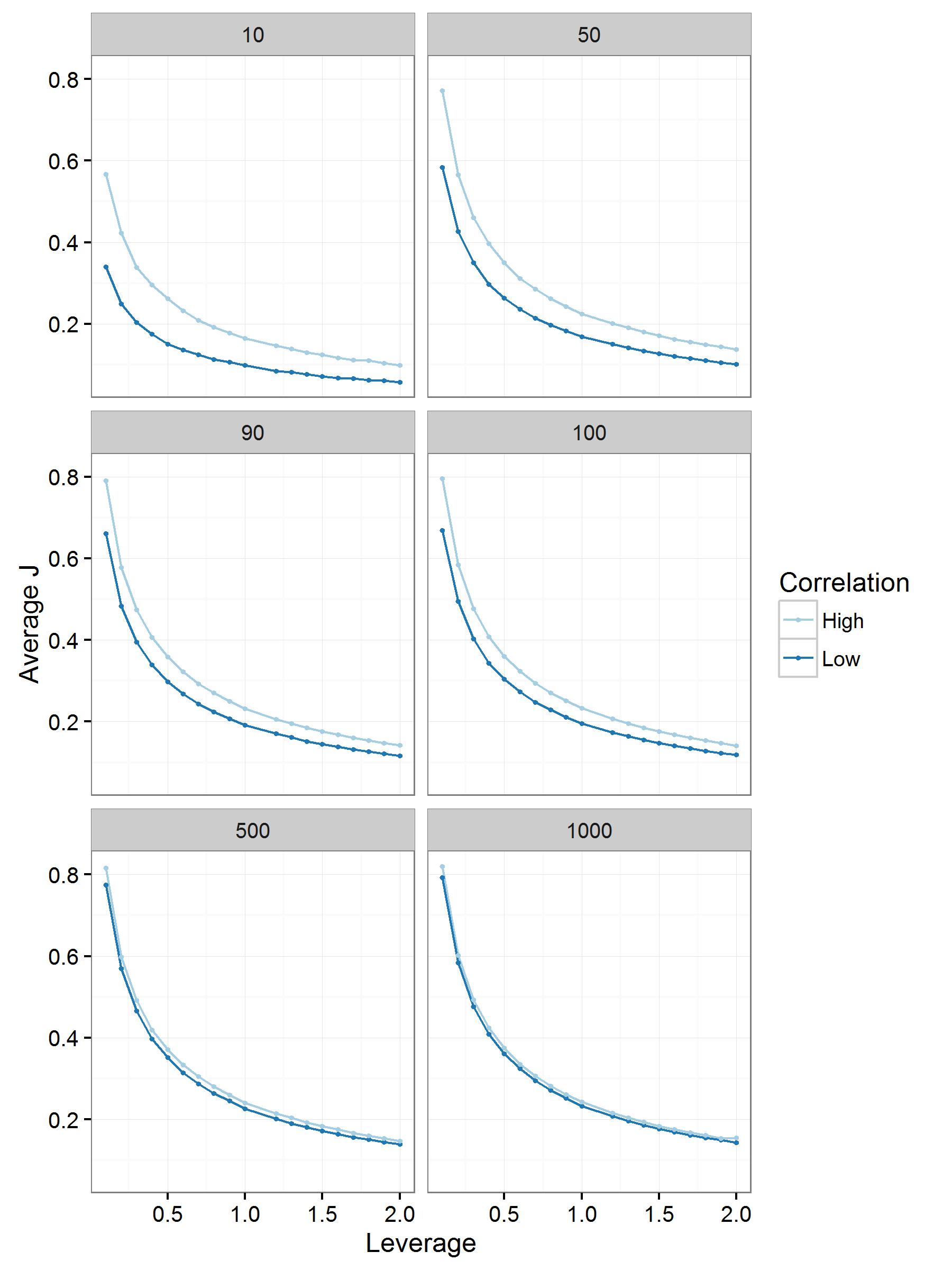

We ran 2000 Monte Carlo simulations of the multi-factor and single factor probabilities of default333All our simulations were run in R (R Core Team, 2016). The algorithm that generates random correlation matrices was adapted from Hardin et al. (2013) and Joe (2006)., for a given number of firms 10,50,90,100,500, and 1000444For the sake of simplicity, we set in the simulations., and a given level of debt leverage =0.1,.., 2, in steps of 0.1. For each simulation, we randomly estimate a high correlation matrix. This procedure is repeated for low correlation matrices. The results of each set of simulations are 2000 values for the Jeffreys-Kullback-Leibler divergence (14), from which we calculate the averages shown in Figure 1 and Table 2. Our main results are summarised as follows.

The divergence between the multi-factor and the single-factor probability of default increases with asset correlation.

For =10 to 100 firms, the graph of the low correlation divergence is significantly below that of the high correlation divergence. For firms, leverage equal to 10%, and low correlation, the average divergence is =0.3400. For the same number of firms and leverage, but high correlation, =0.5669. The divergences for a leverage of 200% -all else equal- are = 0.0575 and =0.1377. Table 1 shows analogous results for other levels of leverage and market sizes. This suggests that in periods of high correlation, e.g., financial crises, the multi-factor default probability will differ significantly from that of the single-factor model. One of the two models may underestimate the true default probability. For larger market sizes, =500 and 1000, the discrepancy between the high and low correlation divergences is reduced. This issue is addressed in detail below.

The divergence between the multi-factor and the single-factor probability of default is inversely related to leverage.

This result indicates that the more indebted the firm, the less discrepancy between the information given by the two models. For =50 and low correlation, =0.5834 if =10%, whilst =0.1018 for =200%, all else equal. Clearly, in the case of highly indebted firms, default probability tends to be similar under either model,. Figure 1 suggests that irrespective of asset correlations, the divergence between the two probabilities tends to zero when debt leverage increases. The implication is that for lower levels of leverage, the two probabilities of default will diverge considerably, and will be influenced by asset correlations. For instance, it can be seen in Table 2 that for a leverage equal to 50%, high correlation and =50, the average divergence is =0.3498, against =0.2636. At that level of leverage, the multi-factor and single factor probabilities of default will give contradictory signals.

| Leverage | Low correlation () | High correlation () | ||||||

|---|---|---|---|---|---|---|---|---|

| N=10 | 50 | 100 | 1000 | 10 | 50 | 100 | 1000 | |

| 0.1 | 0.3400 | 0.5834 | 0.6683 | 0.7926 | 0.5669 | 0.7722 | 0.7952 | 0.8201 |

| (0.1268) | (0.0813) | (0.0658) | (0.0241) | (0.1982) | (0.1081) | (0.0763) | (0.0248) | |

| 0.5 | 0.1504 | 0.2636 | 0.3046 | 0.3610 | 0.2618 | 0.3498 | 0.3607 | 0.3751 |

| (0.0567) | (0.0382) | (0.0308) | (0.0115) | (0.0931) | (0.0488) | (0.0358) | (0.0118) | |

| 1 | 0.0980 | 0.1684 | 0.1954 | 0.2328 | 0.1651 | 0.2243 | 0.2330 | 0.2425 |

| (0.0364) | (0.0246) | (0.0201) | (0.0074) | (0.0608) | (0.0318) | (0.0229) | (0.0073) | |

| 1.5 | 0.0710 | 0.1266 | 0.1475 | 0.1772 | 0.1240 | 0.1700 | 0.1764 | 0.1833 |

| (0.0275) | (0.0186) | (0.0140) | (0.0056) | (0.0448) | (0.0239) | (0.0172) | (0.0056) | |

| 2 | 0.0575 | 0.1018 | 0.1185 | 0.1425 | 0.0992 | 0.1377 | 0.1415 | 0.1547 |

| (0.0215) | (0.0147) | (0.0119) | (0.0040) | (0.0365) | (0.0192) | (0.0134) | (0.0052) | |

2000 simulations of correlation matrices and probability of default. Standard errors in brackets.

| Leverage | N=10 | 50 | 100 | 1000 | ||||

|---|---|---|---|---|---|---|---|---|

| t | p-value | t | p-value | t | p-value | t | p-value | |

| 0.1 | -65.414 | 2.20E-16 | -62.447 | 2.20E-16 | -56.398 | 2.20E-16 | -11.241 | 2.20E-16 |

| 0.5 | -45.704 | 2.20E-16 | -62.228 | 2.20E-16 | -53.087 | 2.20E-16 | -14.13 | 0.00 |

| 1 | -42.279 | 2.20E-16 | -62.182 | 2.20E-16 | -56.788 | 1.31E-11 | -13.27 | 2.20E-16 |

| 1.5 | -45.062 | 2.20E-16 | -65.491 | 2.20E-16 | -56.619 | 2.20E-16 | -10.863 | 2.20E-16 |

| 2 | -44.008 | 2.20E-16 | -66.428 | 2.20E-16 | -56.152 | 2.20E-16 | -26.415 | 2.20E-16 |

and . Equal sample sizes.

Irrespective of asset correlations, the difference between and diminishes with the number of firms.

For larger market sizes, =500 and 1000 firms, the difference between the high/low correlation divergences diminishes, and even seems to disappear in Figure 1. Table 1 shows that for =150%, and =1000 firms, = 0.1772 whilst = 0.1833. However, this difference is statistically significant at a 1% confidence level, as evidenced by the Welch test of equality of means shown in Table 2. The Welch test is also significant at 1% confidence level for all other market sizes and leverage values. It should be emphasized that we are not suggesting that the multi-factor and single-factor default probabilities will converge or even equalize when the number of firms increases. As long as , the two probabilities of default will diverge. Tables 1 and 2 support this finding even in large markets.

The divergence between the two models increases with market size.

This can be seen in Figure 1 by comparing the value of average divergence when and . For , high correlation and leverage equal to 10%, = 0.5669, against = 0.8201 for , all else equal. When correlations are low and leverage equal to 10%, = 0.3400 for and = 0.7929 for . The level of firm indebtedness does not alter this result. For and leverage at 200%, both high and low correlation divergences become closer to zero, =0.0575 and =0.0992. For , and leverage at 200%, high and low correlation divergences become closer to each other in value, =0.1425 and =0.1547, but they are still markedly higher than the respective divergences for .

5 Conclusion

This paper builds a multi-factor model where individual corporate asset value follows a geometric Brownian motion which is correlated with that of other firms. We run simulations of the multi-factor default probability using randomly generated low and high correlation matrices. We also run simulations of the single factor default probability, i.e., the default probability of a corporate with uncorrelated asset value. For each pair of default probabilities we calculate its Jeffreys-Kullback-Leibler divergence. Overall, we find that the discrepancy between the two models is exacerbated in highly correlated markets and when firm’s indebtedness is between 10 to 100 percent. Our findings have implications for financial regulation. The Basel II and III Capital Adequacy Accords stipulate that capital provisions should be calculated in accordance with a single-factor, single-firm structural model (BIS, 2006, 2011). Our paper suggests that in periods of financial instability, when asset volatility and correlations increase, one of the models may misreport default risk and thus lead to inadequate capital provisions.

References

- Aït-Sahalia and Xiu (2015) Aït-Sahalia, Y. and Xiu, D. (2015) Increased correlation among asset classes: Are volatility or jumps to blame, or both?, Tech. Rep. 14-11, Chicago Booth School of Business.

- BIS (2006) BIS (2006) International convergence of capital measurements and capital standards: A revised framework, Tech. rep., Basel Committee on Banking Supervision.

- BIS (2011) BIS (2011) Basel III: A global regulatory framework for more resilient banks and banking systems, Tech. rep., Basel Committee on Banking Supervision.

- Borland (2002) Borland, L. (2002) A theory of non-gaussian option pricing, Quantitative Finance, 2, 415–431.

- Borland and Bouchaud (2004) Borland, L. and Bouchaud, J.-P. (2004) A non-gaussian option pricing model with skew, Quantitative Finance, 4, 499–514.

- Branger (2004) Branger, N. (2004) Pricing derivative securities using cross-entropy: An economic analysis, International Journal of Theoretical & Applied Finance, 7, 63 – 81.

- Buchen and Kelly (1996) Buchen, P. and Kelly, M. (1996) The maximum entropy distribution of an asset inferred from option prices, Journal of Financial and Quantitative Analysis, 31, 143–159.

- Burbea and Rao (1982) Burbea, J. and Rao, C. (1982) Entropy differential metric, distance and divergence measures in probability spaces: A unified approach, Journal of Multivariate Analysis, 12, 575 – 596.

- Cathcart and El-Jahel (2004) Cathcart, L. and El-Jahel, L. (2004) Multiple defaults and Merton’s model, Journal of Fixed Income, 14, 60–68.

- Das et al. (2007) Das, S., Duffie, D., Kapadia, N. and Saita, L. (2007) Common failings: How corporate defaults are correlated, Journal of Finance, LXII, 93–117.

- Das et al. (2006) Das, S., Feed, L., Geng, G. and Kapadia, N. (2006) Correlated default risk, Journal of Fixed Income, 16, 7–32.

- Duffie et al. (2009) Duffie, D., Eckner, A., Horel, G. and Saita, L. (2009) Frailty correlated defaults, Journal of Finance, 64, 2089–2123.

- Embrechts and Maejima (2002) Embrechts, P. and Maejima, M. (2002) Self-similar processes, Princeton University Press.

- Emmer and Tasche (2005) Emmer, S. and Tasche, D. (2005) Calculating credit risk capital charges with the one-factor model, Journal of Risk, 7, 85–101.

- Etheridge (2001) Etheridge, A. (2001) A course in financial calculus, Cambridge University Press.

- Frank (2009) Frank, N. (2009) Linkages between asset classes during the financial crisis, accounting for market microstructure noise and non-synchronous trading, Economics Series Working Papers 2009-W04, University of Oxford, Department of Economics.

- Golan (2006) Golan, A. (2006) Information and entropy econometrics: A review and synthesis, Foundations and Trends in Econometrics, 2, 1–145.

- Gordy (2003) Gordy, M. (2003) A risk-factor model foundation for ratings-based bank capital rules, Journal of Financial Intermediation, 12, 199–232.

- Gulko (1999) Gulko, L. (1999) The entropy theory of stock option pricing., International Journal of Theoretical & Applied Finance, 2, 331.

- Gulko (2002) Gulko, L. (2002) The entropy theory of bond option pricing., International Journal of Theoretical & Applied Finance, 5, 355.

- Hardin et al. (2013) Hardin, J., Garcia, S. R. and Golan, D. (2013) A method for generating realistic correlation matrices, Ann. Appl. Stat., 7, 1733–1762.

- Joe (2006) Joe, H. (2006) Generating random correlation matrices based on partial correlations, Journal of Multivariate Analysis, 97, 2177 – 2189.

- Krishnan et al. (2009) Krishnan, C., Petkova, R. and Ritchken, P. (2009) Correlation risk, Journal of Empirical Finance, 16, 353 – 367.

- Kullback and Leibler (1951) Kullback, S. and Leibler, R. A. (1951) On information and sufficiency, The Annals of Mathematical Statistics, 22, 79–86.

- Lamperti (1962) Lamperti, J. (1962) Semi-stable stochastic processes, Transactions of the American Mathematical Society, 104, 62–78.

- Longin and Solnik (1995) Longin, F. and Solnik, B. (1995) Is the correlation in international equity returns constant: 1960-1990?, Journal of International Money and Finance, 14, 3 – 26.

- Lopez (2004) Lopez, J. (2004) The empirical relationship between average asset correlation, firm probability of default, and asset size, Journal of Financial Intermediation, 13, 265–283.

- Maasoumi and Racine (2002) Maasoumi, E. and Racine, J. (2002) Entropy and predictability of stock market returns, Journal of Econometrics, 107, 291 – 312, information and Entropy Econometrics.

- Merton (1974) Merton, R. (1974) On the pricing of corporate debt: The risk structure of corporate debt, Journal of Finance, 29, 449–470.

- Morana and Beltratti (2008) Morana, C. and Beltratti, A. (2008) Comovements in international stock markets, Journal of International Financial Markets, Institutions and Money, 18, 31 – 45.

- Neri and Schneider (2012) Neri, C. and Schneider, L. (2012) Maximum entropy distribution inferred from option portfolios on an asset, Finance Stochastics, 16, 293–318.

- Pollet and Wilson (2010) Pollet, J. M. and Wilson, M. (2010) Average correlation and stock market returns, Journal of Financial Economics, 96, 364 – 380.

- Pykhtin (2004) Pykhtin, M. (2004) Multi-factor adjustment, Risk, 17, 85–90.

- R Core Team (2016) R Core Team (2016) R: A Language and Environment for Statistical Computing, R Foundation for Statistical Computing, Vienna, Austria.

- Rangvid (2001) Rangvid, J. (2001) Increasing convergence among European stock markets?: A recursive common stochastic trends analysis, Economics Letters, 71, 383 – 389.

- Sandoval Jr. and De Paula Franca (2012) Sandoval Jr., L. and De Paula Franca, I. (2012) Correlation of financial markets in times of crisis, Physica A: Statistical Mechanics and its Applications, 391, 187 – 208.

- Shreve (2004) Shreve, S. (2004) Stochastic calculus for finance II: Continuous-time models, Springer Verlag.

- Tasche (2006) Tasche, D. (2006) Measuring sectoral diversification in an asymptotic multi-factor framework, Journal of Credit Risk, 2, 33–55.

- Ullah (1996) Ullah, A. (1996) Entropy, divergence and distance measures with econometric applications, Journal of Statistical Planning and Inference, 49, 137 – 162, econometric Methodology, Part I.

- Vasicek (1991) Vasicek, O. (1991) Limiting loan loss probability distribution, KMV Corporation.

- Vasicek (2002) Vasicek, O. (2002) Probability of loss on loan portfolio, KMV Corporation.

- Zellner (2002) Zellner, A. (2002) Information processing and bayesian analysis, Journal of Econometrics, 107, 41 – 50, information and Entropy Econometrics.

- Zhou (2001) Zhou, C. (2001) An analysis of default correlations and multiple defaults, Review of Financial Studies, 14, 555–576.

Appendix A Appendix

Our proof hinges on the Brownian motion being Normally distributed with mean 0 and variance 1, and independent from . It also relies on the -self-similarity property of Brownian motions, i.e., . Before we proceed to the proof of Proposition 2.1, a couple of definitions and a theorem will be presented. A good introduction on self-similar stochastic processes is Embrechts and Maejima (2002).

A.1 Self-similarity of Brownian motions

A stochastic process is said to have independent increments, if for any and for any partition , are independent. A formal definition of a Brownian motion will be useful in the proof of Theorem A.2.

Definition A.1.

If a stochastic process satisfies

-

(i)

a.s.,

-

(ii)

it has independent and stationary increments,

-

(iii)

for each , has a Gaussian distribution with mean zero and variance , and

-

(iv)

its sample paths are continuous a.s.,

then it is called (standard) Brownian motion.

Definition A.2.

A stochastic process is said to be self-similar

if for any , there exists such that

| (15) |

where “” means equality in distribution.

The following theorem was proved by Lamperti (1962) and shows that a self-similar stochastic process is equal in distribution to the stochastic process . In many texts on the topic, a self-similar process is defined by this property.

Theorem A.1.

The following theorem will be used in our proof of Proposition 2.1.

Theorem A.2.

A Brownian motion is 1/2-self-similar.

Proof.

It is sufficient to show that for every , is also Brownian

motion as defined in A.1 above.

Conditions (i), (ii) and (iv) are trivially fulfilled. Regarding (iii), Gaussianity and mean-zero property also follow from the properties of . To obtain the variance, consider the stochastic process . Its variance is

| (16) |

Thus is a Brownian motion. ∎

A.2 Proof of Proposition 2.1

The proof that (5) is the solution of (4) can be found in Etheridge (2001) or Shreve (2004), amongst others. The distributional properties of are not proved in the literature, due to it being the building block of option-pricing models, rather than a stand-alone model as in this paper.

Proof.

Let . Then , where is a constant. The mean of is

| (17) |

since the terms in the first exponential are non-random. Given that the Brownian motions are independent, the term in the expectation function can be written as

| (18) |

From the -self-similarity property,

| (19) |

Since is N(0,1), , where is a real constant. This implies that

| (20) |

| (21) |

The variance of , , can be simplified to

| (22) |

From the 1/2-self-similarity of Brownian motion

| (23) |

Substituting in above

| (24) |

From which,

| (25) |

. Since is a constant, the mean and variance of follow trivially.

∎