Optimal investment and consumption with downside risk constraint in jump-diffusion models

Abstract

This paper extends the results of the article [C. Klüppelberg and S. M. Pergamenchtchikov. Optimal consumption and investment with bounded downside risk for power utility functions. In Optimality and Risk: Modern Trends in Mathematical Finance. The Kabanov Festschrift, pages 133-169, 2009] to a jump-diffusion setting. We show that under the assumption that only positive jumps in the asset prices are allowed, the explicit optimal strategy can be found in the subset of admissible strategies satisfying the same risk constraint as in the pure diffusion setting. When negative jumps probably happen, the regulator should be more conservative. In that case, we suggest to impose on the investor’s portfolio a stricter constraint which depends on the probability of having negative jumps in the assets during the whole considered horizon.

Key words: Capital-at-risk, Value-at-Risk, expected shortfall, downside risk measure, jump-diffusion process, portfolio optimization, optimal consumption, utility maximization.

AMS classification primary: 91B70, 93E20, 49K30; secondary: 49L20, 49K45.

1 Introduction

One of the principal problems in mathematical finance is to consider a combination of optimal investment during a fixed investment interval and optimal terminal wealth at maturity. In particular, starting with an initial wealth , the investor tries to maximize the following cost function

| (1.1) |

where are two given utility functions, is the rate of consumption and is the terminal wealth depending on the control process . Such problems are of prime interest for institutional investors, selling asset funds to their customers, who are entitled to certain payment during the duration of an investment contract and expect a high return at maturity. In reality, financial activities must respect to some mandatory regulations mathematically defined by a risk measure [1]. Note that Value-at-Risk (VaR) and Expected Shortfall (ES) are such measures endorsed by the Basel Committee on Banking Supervision. However, VaR is not a convex risk measure and only the probability to exceed a VaR bound is considered, not the values of the losses. It has ben shown that ES, defined as the conditional expectation of losses above VaR, can be employed to fix this limitation. The literature for the problem of optimal portfolio under risk constraints is vast and we refer to [3, 7, 4, 27, 12] and the references therein for more detailed discussions.

Note that in order to satisfy the Basel committee requirements, investors must control the level of loss throughout the investment horizon. This problem is studied by Klüppelberg and Pergamenshchikov [20, 21] for power and logarithm utility functions in the class of the nonrandom financial strategies with continuous asset dynamics. Chouaf and Pergamenschikov [6] study the optimal investment problem with the uniformly bounded VaR for random admissible financial strategies.

Recent research in finance has paid attention to empirical evidence of jumps in stock returns [14, 13]. In fact, by incorporating jumps into the model we can allow to have sudden but infrequent market movements of large magnitude, and thus capture the skewed and fat-tailed features of stock return distributions. It has been shown by many empirical and theoretical studies that the jump risk has a substantial impact on portfolio choice, risk management and option pricing [23, 11]. In particular, optimal portfolios held by an investor facing jump risks may significantly differ from those in the absence of jumps, and ignoring jumps may lead substantial losses [10]. Unlike pure-diffusion models with portfolio constraints, the martingale duality approach [19] may not be applied directly to a jump-diffusion model since the incompleteness caused by jumps in a jump-diffusion model may not be removed through the well-known completion techniques.

Let us only mention some among a vast recent literature of the problem of optimal portfolio choice with jumps. [11] studies approximation for computing value at risk and other risk measures for portfolios that may include options and other derivatives with defaultable counterparties or borrowers. [15, 16] study the problem of optimal portfolio in a one-dimension jump-diffusion context with or without transaction costs. [22, 10, 2] solve the portfolio selection problems in jump-diffusion models with constant coefficients and no portfolio constraints where there is only one type of jumps. [17] considers the dynamic portfolio choice problem in a jump-diffusion model with constraints on portfolio weights using a particularly embedding the constrained problem in an appropriate family of unconstrained ones.

In this paper, we extend the results in [20] to a jump-diffusion setting. Let us emphasize that even in the absence of risk constraint, problem (1.1) in jump-diffusion models has not been well studied in the literature. In general, it is challenging to obtain the optimal solution in explicit form when investment and consumption are both considered. For the constrained problem, it is impossible to obtain an explicitly equivalent constraint on portfolio from the given VaR/ES constraint, which is imposed on the wealth process, due to the presence of jumps. As a result, the HJB approach may not be easily applied to solve the problem as e.g. in [27]. The finding in this present paper is two-fold. First, we show that, under suitable choices for risk preference and for two identical power utility functions , the optimal solution of the unconstrained problem is still optimal for the constrained problem when jumps in the assets are non negative. When with , the impact of constraint is dramatic and it is optimal for the investor to consume all. Second, when negative jumps are allowed in the asset prices, we propose a slightly stricter constraint that takes into account the probability of having negative jumps in the horizon. Thus, the paper may give a reasonable choice to the regulator in designing regulatory policies for models with jumps.

Let us shortly explain our main idea. First, from the regulator’s point of view, jumps in the asset are not always unexpected. Roughly speaking, when jumps in asset are non negative (e.g. the markets are blooming), the risk of the investor’s portfolio is less or equal to the risk in the absence of jumps if both are constructed optimally. The assumption of non negative jumps is positively correlated to the possibility of investing more in the risky asset. It is then reasonable to look for optimal strategies among those satisfying a constraint with the same confidence level imposed on a ”modified” wealth process which is simply obtained by ignoring jumps in the initial wealth process. Because jumps are non negative, the corresponding admissible strategies form a subset of the initial admissible set. As explicitly shown in [20], this admissible subset can be deduced from an equivalent constraint which is directly imposed on the strategy. This then allows to employ the HJB approach or the direct method in [20] to get the optimal solution. In such a jump-diffusion setting but with the same modified constraint as used in the pure diffusion case, the regulator now needs to check whether the constraint is fulfilled by the optimal solution of the unconstrained problem in the jump-diffusion model. This can be confirmed under some condition on the risk preference parameter. Intuitively, the regulator should be more conservative if negative jumps probably happen. In that case, a slightly stricter constraint depending on the probability that there are negative in the risky assets during the investment horizon can be applied to ensure that the analysis for the case of non negative jump is still valid.

The remainder of the paper is organized as follows. Section 2 formulates the market model. We provide in Section 3 a complete analysis for the unconstrained problem in jump-diffusion settings. The main results of the paper are reported in Section 4. Section 5 considers the general case when the terminal utility and the consumption functions are different. Section 6 studies the case where negative jumps are allowed. Auxiliary results are reported in Appendix.

2 The market model

Consider a financial market with risky assets defined in the horizon by the system

| (2.1) |

where is a standard Brownian motion and is the compensated random Poisson measure generated by the compound Poisson process

The riskless asset is given by where is the riskless interest rate. We assume furthermore that is of independent component vector process and independent of the Brownian motion . Let

be the -dimension Lévy measure of then it is well-known that for any , , where is the common distribution function of the jump sizes and is the intensity of the Poisson process . To guarantee the positivity of the stock prices, we assume that

and for all . Denote by the vector of stock appreciation and by the matrix of the stock volatilities. We suppose throughout the paper that these processes are deterministic, continuous and is non-singular for Lebesgue almost surely .

Let be the amount of investment into bond and stocks at time . The wealth process is then given by

Assume moreover that consumption is possible and defined by the a progressively measurable non-negative process verifying . The strategy is called self-financing if the wealth process satisfies the following equation

| (2.2) |

For , denote by

| (2.3) |

the fraction of the wealth invested into -th asset. The portfolio process is assumed to be cadlag and almost surely. For convenience, define

| (2.4) |

With these notations, we rewrite (2.2) as

| (2.5) |

where . Suppose that consumption is a proportion of wealth, i.e. , where is a non-negative deterministic process holding . Define and use the notation to emphasize that the wealth process is defined with some control . Now, (2.5) can be rewritten as

| (2.6) |

Denote by

| (2.7) |

the stochastic exponential and put

| (2.8) |

Then, by Itô’s formula for jump processes, it is straightforward to see that (2.6) admits the following solution

| (2.9) |

where

| (2.10) |

and the jump part defined as

| (2.11) |

where is the sequence of jump times of , Admissible strategies are specified as follows.

Definition 2.1.

Note that the third condition, interpreted as the short selling prohibition, is necessary to make sure that is positive. We denote by the class of all admissible control processes. The effect of no short selling has been investigated for two CRRA utility functions in constant coefficient markets is studied in [18].

Remark 1.

In [18], the authors study dynamic optimal portfolio choice in a jump-diffusion with investment constraint including no-short selling and no-borrow constraints. The key idea is to construct a set of fictitious markets by adjusting the interest rate and the drift terms of stock prices. The constrained consumption-investment problem in the original market is converted into an unconstrained one in a set of fictitious markets. Then, the optimality for the original market with investment constraints can be obtained by optimally adjusting the interest rate and the stock price drift terms in the fictitious markets. For detailed discussions, see [18].

Assume now that the investor wants to optimize his expected utility of consumption over the time interval and his wealth at terminal horizon. In other words, for an initial endowment and a control process , we consider the cost function of the form

where are utility functions and is the expectation operator conditional on . For power utility functions problems, we choose for , with and the cost function is then given by

| (2.12) |

Let us now precise the risk constraints considered in this paper. The VaR defined below is also known as ”Captial at Risk”. Here we adopt the idea in [12, 20].

Definition 2.2 (Value at Risk).

For an initial endowment , a control and a real number , we define the Value at Risk (VaR) of the wealth process as

| (2.13) |

where is the lower -quantile of .

For definition of lower quantile we refer to Definition A.1. It should be stressed that the above definition is consistent with the setting in the well-known paper [4] with limit loss , which needs to be checked dynamically at any time . Note that for . The level of risk is characterized by for some coefficient , which represents a liability level for the investor’s portfolio. Now, for some , we look for a strategy for which the Value at Risk is uniformly bounded by , i.e. we are working under the following dynamical risk constraint

| (2.14) |

Also remark that the risk level and are determined by the regulator. In some cases, the investor can take in a given range. If is close to 0, risk of the portfolio risk is at low level whereas is near 1, the portfolio has a high risk of loss as in the unconstrained problem. In the latter case, the risk limit may not be active. Let us now define the second kind of constraint which, unlike the quantile, focuses on the averaged value of loss.

Definition 2.3.

For an initial endowment , a control and a real number , we define the Expected Shortfall (ES) of the wealth process as

| (2.15) |

where is the classical expected shortfall.

For the reader’s convenience, the classical definition of expected shortfall is given in Definition A.2. Note that the investor’s portfolio can be controlled by imposing continuously the following constraint: for all . Then, the same interpretation can be observed as in the case of VaR constraint. In Section 4, we study the following constrained problems:

Problem 1.

Given and , find strategy which solves

Problem 2.

Given and , find strategy which solves

Let us make here some comments on the above problems. First, the classical martingale method [19] seems to be impossible for such problems with dynamic risk constraint. Note that in pure diffusion models, it is possible to transform the VaR/ES constraint into a so-called portfolio constraint, i.e. constraint on strategies, then martingale duality might be applied by considering a new artificial market as in Cvitanic and Karatzas [8, 9]. However, this transformation seems highly challenging in the presence of jumps. Another possibility is to solve the problem approximately, i.e. we first approximate the risk constraint by a portfolio constraint then consider the corresponding approximate HJB. It is likely that such procedure need to be done in a delicate asymptotic analysis. Lastly, it might be possible to employ the so-called weak dynamic programming principle for state constraint suggested by Bouchard and Nutz [5], but then we need to look for optimal solution in the sense of viscosity solution.

Below, wishing to get a closed form of the optimal solution, we adapt the direct method used by Kluppelberg and Pergamenschikov [20].

3 Optimization problem without constraints

We provide a detailed analysis for the unconstrained problem

Problem 3.

Note that there have been very few studies in jump settings where both optimal investment and consumption are combined. Although our main aim is to deal with the constrained problem, this section may be seen as another contribution of the paper. First, the indirect value function is given by

| (3.1) |

For completeness, we begin with the simplest case thought this case has economically not much sense without a risk constraint. A detailed proof is given in Appendix D.

Theorem 3.1.

Consider Problem 3 with . Assume that for all and . Then,

-

1.

If then any control with is an optimal solution and the corresponding optimal value of is given by .

-

2.

If then the control with

(3.2) is the optimal solution and the corresponding optimal value of is given by .

3.1 The case

We now study the unconstrained problem for the case . Let us first compute the value function. By (2.9) and noting that one gets

| (3.3) |

On the other hand, by Lemma B.1

| (3.4) |

Therefore,

| (3.5) |

and

| (3.6) |

Hence, the value function is given by

| (3.7) |

From the dynamics of given in (2.6), one gets the HJB equation for the unconstrained problem

| (3.8) |

where the generator is defined by

| (3.9) |

where is the scalar product. The optimal necessary condition w.r.t is given by

We try to find a solution of the form (i.e. ), where is a -function to be determined. We have

Substituting these formulas into (3.8) we obtain

| (3.10) |

where

| (3.11) |

Let and and . Now, by the necessary optimal condition in one has

| (3.12) |

where

| (3.13) |

The next step is to solve the system (3.12). Observe first that the functions are concave on , hence supremum in (3.10) is attainable and unique. For the moment, let us assume that is a solution of system (3.12) and let be the corresponding supremum in (3.10). We then get the following Bernoulli equation

| (3.14) |

The solution of (3.14) is given by

| (3.15) |

It follows that the optimal rule is given by (which is the solution of (3.12)) and

| (3.16) |

and the optimal value of value function can be determined. Notice that when there is no jumps in the asset prices (), we obtain and the optimal value of is given by

where is defined by

| (3.17) |

which means that the result in [20] is recovered.

We summarize the above analysis in the following statement.

Theorem 3.2.

Proof. It it not difficult to check that all necessary conditions for the usual verification theorem (see e.g. [26, 24]) are satisfied. ∎

Remark 2.

It is instructive to verify the optimality by using the martingale optimality principle: the value function is a supermartingale for any admissible strategy but it becomes a martingale under the optimal strategy. This can be checked by applying Itô’s formula for the process , where is given by (3.15).

Remark 3.

The case is more challenging to show since the function in (3.15) should be chosen as an appropriate combination of two functions , . This could be done using a similar argument of Theorem 2 in [20]. However, it is also possible to see that the corresponding optimal solution does not satisfy the VaR/ES risk constraint. We will show in the next section that the presence of risk constraint has a strong impact on the investor’ portfolio so that it is optimal for him to consume all. For that reason, we do not provide a detailed result for the unconstrained in this case and refer to [20] for a detailed analysis in the pure diffusion case.

3.2 One-dimension case

We provide more analysis about the optimal rule for the case of one dimension.

Theorem 3.3.

Assume that for almost surely ,

Then there exists a solution to (3.21). Let be the optimal value of the function in the HJB equation (3.20) and consider defined by (3.16) in which we have replaced with . Then, is an optimal solution to the problem and the wealth process is given as the unique solution of

| (3.19) |

Proof. As above, we get corresponding HJB equation

| (3.20) |

where

where is defined in (3.11). The necessary condition for optimality is given by , where

| (3.21) |

where defined by (3.13). Note that is continuous on with and

Furthermore,

since and the support of is . So, by the theorem of mean values, for any , there exists such that . The conclusion then follows the usual verification step. ∎

Remark 4.

For infinite horizon cases, extra conditions need to be imposed to get the uniform integrability. For general cadlàg coefficients, we can formulate a specific verification theorem as in [20].

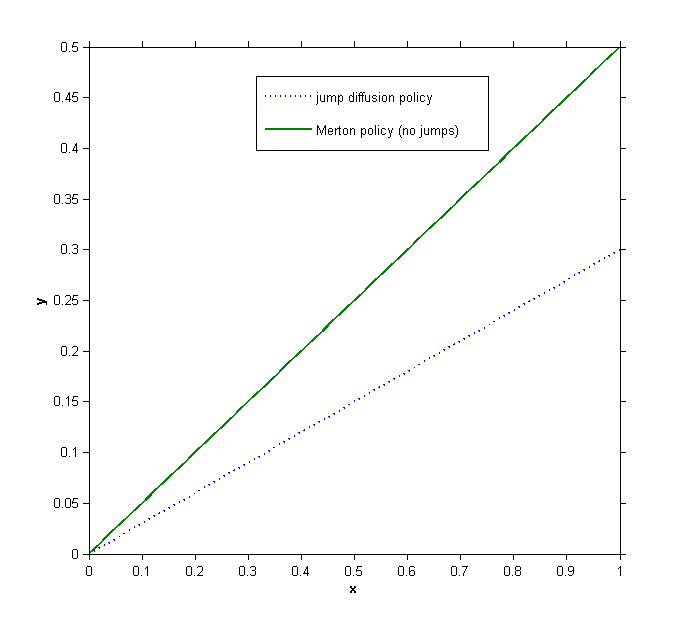

We now compare the optimal rule obtained above with the no-jump optimal strategy of the classical Merton problem.

Lemma 3.1 (comparision).

The presence of jumps reduces the quantity asset and consume more, i.e

Proof. A proof is given in Appendix E. ∎

4 The optimization problems with risk constraint

In this section, we study the Problem 1 and Problem 2. We assume in this section that the following condition holds:

Assumption :The jump sizes of stock prices are non-negative.

As discussed in Section 1, when jumps in the assets are non negative (e.g. the markets are blooming), the risk of the investor’s portfolio is smaller or at the same level than in the absence of jumps. Intuitively, positive jumps encourage the agent to invest more in the risky asset. It is then reasonable to look for the optimal strategy satisfying the constraint with the same confidence level but with ignored jumps. Because jumps are non negative, these strategies form a subset of the initial admissible set. As explicitly shown in [20], this admissible subset can be deduced from an equivalent constraint which is directly imposed on the strategy. This then allows to employ the HJB approach or the direct method in [20] to get the optimal solution.

4.1 The case

To present the results for the Problem 1 with VaR constraint, we define and

| (4.1) |

Theorem 4.1.

Consider Problem 1 with under Assumption .

-

1.

If then any control with positive component vector satisfying

with , is an optimal solution and the corresponding optimal value of is given by .

-

2.

Suppose that has non-negative components, i.e.

and defined in (2.8) is strictly positive. Then, for

(4.2) the control defined by

(4.3) is the optimal and is the corresponding optimal value.

Proof. From (D.3) one gets an upper bound for the value function

We show that this upper bound can be attained by choosing the suitable optimal strategy.

Step 1: By the linear property of lower quantile one easily observes that the constraint in Problem 1 is equivalent to

| (4.4) |

Under assumption , the process is bigger than 1 a.s. hence, by Lemma A.3 . Therefore, if is an optimal solution to Problem 1 under the weaker constraint

| (4.5) |

then it is also an optimal solution to Problem 1 with initial constraint (4.4). We now solve Problem 1 with constraint (4.5), which is now can be transformed into an more explicit form

| (4.6) |

Step 2: Suppose first that hence for all . Now, (4.6) becomes

| (4.7) |

which is satisfied if

since . The latter inequation has solution , where

| (4.8) |

Thus, for , with any non-negative component vector and satisfying , the value function attains its maximal value and the first case is proved.

Step 3: Now, suppose that has non-negative components and defined in (2.8) is strictly positive. Then, for all . One will try with strategy , with possible maximal values of such that (4.6) is verified. Substituting this particular candidate into this constraint, we observe that the constraint (4.6) is justified if the following holds

| (4.9) |

where and . By replacing by one gets a stronger requirement

| (4.10) |

Let

Then, and . Note that is a strictly decreasing function in in . To see this, note that

if , but this is implied by (4.2). So, if one chooses such that

| (4.11) |

then (4.10) is fulfilled. Now, equation (4.11) admits a unique positive solution given by (4.1). Finally, taking into account the condition one should choose and the proof is completed. ∎

Let us now consider Problem 2 with ES constraint. First, it is useful to rewrite the constraint in the following way

| (4.12) |

By Lemma A.3, one sees that (4.12) is deduced from Assumption and the modified constraint which is independent of jumps

| (4.13) |

By Lemma A.2 one gets

| (4.14) |

where

| (4.15) |

To formulate the optimal results, we denote by the solution of the following equation

| (4.16) |

Theorem 4.2.

Proof. Also trying with the strategy we need to choose the possible maximal value of such that the requirement (4.14) is checked. By substituting this particular candidate into one gets

where and

| (4.17) |

One will choose such that . Clearly, and , where

| (4.18) |

Our aim is to determine a sufficient condition for such that is the minimum of on and this minimum is equal to . In other words, one choose , the solution of equation (4.16). In order to guarantee that this is in fact the minimum of on one needs to check the sign of the first derivative in . One has,

Hence, is the minimum of on if for all . Using the well-known estimate for the Gaussian integral

| (4.19) |

one gets

for all if .

Let us verify that equation has a unique positive solution. To this end, remark that and is strictly decreasing if . On the other hand, (4.19) yields that

In summery one should take defined by equation (4.16). Taking into account the requirement one gets the same optimal strategy as in Theorem 4.1 where is replaced by . ∎

4.2 The case

As in [20], we show below that under some mild condition on the model parameters the unconstrained solution in Theorem 3.2 is still optimal.

Consider first the VaR constraint with non negative jumps. By (3.12) one has

where

| (4.20) |

Taking into account the above integrals are non positive (since ), one gets for all . This implies that . By Lemma C.1,

Like in the pure diffusion case, the optimal solutions of the constrained and unconstrained problems coincide.

Theorem 4.3.

Assume that jumps in assets are non negative and where

| (4.21) |

Then, under the assumption of Theorem 3.2 the optimal solution without constraint is also an optimal solution to the corresponding problem with VaR constraint.

Proof. We need to check the constraint (4.6) for the optimal solution of the problem without constraint. For this aim, it suffices to verify that

but this is an direct consequence of relation and (4.21). ∎

Let us consider the problem with ES constraint. To formulate the result, we introduce

| (4.22) |

where is defined by (4.23). Observe that .

Theorem 4.4.

Assume that jumps in assets are non negative, and the following condition holds

| (4.23) |

Then, under the assumption of Theorem 3.2 the optimal solution without constraint is also optimal for the corresponding problem with ES constraint.

Proof. We need to check the risk constraint (4.14) for strategy defined by system (3.12) and (3.16), i.e.

Taking into account that , and is decreasing, we only need to verify that

| (4.24) |

where

Using (4.19) one observes that

since by assumption. Therefore, is decreasing in and (4.24) is verified if , which can be easily deduced from (4.23). ∎

5 The case

We consider the general case where the consumption and bequest functions are different, i.e. . This case is challenging even in pure diffusion models [20] because the optimal solution without risk constraint does not satisfy the risk constraint. As a matter of fact, the constraint now has a strong impact on the optimal problem. In particular, it was shown in [20] that it is optimal to consume all (at the rate which is explicitly determined). Intuitively, the same result is expected for our present model with jumps. In this section we show that this result is still valid in the presence of jumps by adapting the method used in [20].

We first find an upper bound for the cost function and then try to point out an appropriate control at which the cost function attains that upper bound. First, recall that the cost function is given by

| (5.1) |

where

5.1 VaR constraint

One gets from the risk constraint (4.6) that

Put . The above inequality is verified if

| (5.2) |

for . Now, by Holder’s inequality and the equality , one gets

| (5.3) |

where, as in (3.17)

Let us study . Observe first that for , the function attains maximum on the whole admissible set at satisfying . By Lemma 3.1, both are concave functions and where

Therefore,

where . It follows that

where

Lemma 5.1.

Assume that and

| (5.4) |

Then, is an upper bound of the cost function.

Proof. Consider first the case . Then since is decreasing on . Putting , one deduces that

Let us study the monotonicity of . For this aim, we compute its first derivative

| (5.5) |

Note that is a concave function, which has first positive derivative and negative second derivative on provided that . Therefore, if

| (5.6) |

On the other hand, one gets from (5.2) that

Then,

So, (5.6) holds if

| (5.7) |

Observe that (5.7) is equivalent to (5.4). Under (5.4), is increasing, which implies that since

Suppose now that . Recall that is decreasing with . There exists such that . Now,

On the other hand, observe that if . As already shown above,

As is increasing one concludes that . Hence, is always an upper bound of the cost function. ∎

Theorem 5.1.

Under the assumptions of Lemma 5.1, is the optimal solution for the problem with VaR risk constraint, where

| (5.8) |

Proof. We need to find an control at which the cost function attains the upper bound . Clearly, we should choose such that

For this aim, we solves the differential equation on

The last differential equation admits solution

which gives the optimal consumption rate defined in (5.8). ∎

5.2 ES constraint

Consider Problem 2 with ES constraint. An upper bound for the cost function is given by the following.

Lemma 5.2.

Assume that and

| (5.9) |

Then, is an upper bound of the cost function.

Proof. Recall that . First the risk constraint (4.14) implies that

| (5.10) |

It is easy to check that the function is strictly decreasing if . So, (5.10) is checked if we have

Note that . Therefore, there exists a solution for equation

| (5.11) |

and is strictly decreasing since is decreasing, which implies . Now, taking derivative of two sides (5.11) one gets

Observe that the expression in the square brackets is bounded by . It follows that

At this stage, the analysis as Lemma 5.1 can be applied to show that is an upper bound of the cost function. ∎

We have proved that under the ES constraint, it is optimal to consume all.

Theorem 5.2.

Theorems 5.1 and 5.2 show that the presence of a dynamical risk constraint has an undesired effect that the investor whose portfolio constitutes in both consumption and investment should optimally consume all. Thus, our results suggest considering the utility maximization problem (optimal investment) and the optimal consumption problem separately. Remark that [2] considers the unconstrained consumption problem in a similar jump-diffusion setting. In particular, by exploiting differences in the Brownian risk of the asset returns that lies in the orthogonal space, the authors show that optimal policy can be obtained by focusing on controlling the exposure to the jump risk.

5.3 When consumption is not possible

Let us consider the following utility maximization problem where the wealth process is given by

| (5.12) |

One then deduces the HJB equation

| (5.13) |

where the generator is defined by as in (3.9) with :

| (5.14) |

We try to find a solution of the form , and where is a -function to be determined. Substituting these formulas into (3.8) we obtain

| (5.15) |

where defined in (3.11). Thus, we get the same necessary optimal condition as in (3.12), i.e.

| (5.16) |

where defined in (3.13). Direct argument leads to the optimal solution for the unconstrained problem.

Proposition 5.1.

Proof. The conclusion follows a similar argument as in Theorem 3.2 with the remark that is the solution to the ordinary differential equation . ∎

Let us turn to the constrained problem under VaR/ES constraint. The following is just a direct consequence of Theorems 4.3 and 4.4.

Proposition 5.2.

Assume that jumps in the assets are non negative and condition (4.21) holds. Then the unconstrained solution in Proposition 5.1 is still optimal solution to the utility maximization problem with VaR constraint. The same conclusion is still true for ES constraint when (4.21) is replaced with condition (4.23).

Proposition (5.2) provides sufficient conditions so that the risk constraints VaR/ES are not active. When these conditions do not hold, it could be possible to incorporate the constraint into the HJB equation. This makes the problem more attractive but more challenging to solve, which we do not pursue it here. In fact, the challenge lies in the fact that the risk constraint is impossible to transformed into an explicit constraint on strategies as in the pure diffusion case due to the presence of jumps. Nevertheless, the HJB equation with investment constraints can be solve numerically as in [12] with an approximation on jumps sizes. In [11], the authors provide an analytical method (applying an analytical Fourier-transform) for computing value at risk, and other risk measures that allows for fat-tailed and skewed return distributions.

6 Negative jumps

We examine in this section the effect of negative jumps. In fact, the regulator should be more conservative if negative jumps probably happen. We show below that in that case, a slightly stricter constrained depending on the probability of having negative jumps in the risky assets during the investment horizon can be imposed to make the previous analysis still valid.

First, note that we still have for all even in the presence of negative jumps. Let us begin by examining the VaR constraint inequality (4.4) by introducing

| (6.1) |

We want to find a lower bound for . The latter can be written as , where and is a measurable standard normal variable independent of . Denote by , where

| (6.2) |

Now, the assumption that the jump parts of the risky assets are independent leads to the following elementary property.

Lemma 6.1.

For any , we have

Obviously, as . We try to estimate respect to . From the quantile definition, we have

| (6.3) |

On ( which is independent of ), is non negative. It follows that

or , where

| (6.4) |

Clearly, if . Thus, is decreasing down to if which implies that . We then deduce that the risk constraint (4.4) is checked if

| (6.5) |

Hence, we need to replace with in the analysis before.

Remark that using the modified confidence level means that the investor’ portfolio is more strictly regulatory. In general, during a normal day-life period of time even though the asset prices are allowed to go down but in a continuous way (predictable). Note that the analysis given in the previous sections can be obtained by sending to zero.

Let us now consider Problem 2 with ES constraint defined by (4.12). Along the lines in the proof of Lemma A.3 and by the positivity of one gets

As above,

where

After changing variable we obtain

In other words,

where is defined in (6.4). Now, by Lemma A.2

Thus, in the presence of negative jumps, we need to replace the function in the risk constraint (4.14) with , defined by

| (6.6) |

Then, the optimal policy can be obtained after a similar procedure.

In summary, we have proved the following main results.

Theorem 6.1.

Assume that negative jumps during the considered horizon take place with probability . Then, all results obtained in the previous sections for VaR constraint are still valid if we replace the level with defined by (6.4) in the corresponding risk constraint. For the problem with ES constraint, we have the same result by replacing with given in (6.6).

7 Concluding remark

We studied the problem of optimal investment and consumption under VaR and ES risk constraints focusing on deterministic strategies. When jumps in asset are non negative, the approach in [20] can be applied to get the optimal solution among a subset of admissible strategies obtained by ignoring jumps in the constraint but with the same confidence level. In particular, we showed that under some mild condition on the model parameters, the unconstrained solution is still optimal if two identical power utility functions are used. For different utility functions, the impact of constraint is dramatic and it is optimal for the investor to consume all. When negative jumps probably happen, the regulator should be more conservative to impose a slightly stricter constrained depending on the probability of having negative jumps in the risky assets during the investment horizon, to ensure that the analysis for the case of non negative jump is still valid.

It should be noticed that random strategies can be considered, but, to make the HJB approach still valid, it is necessary to modify the definition of quantile or use a relative VaR/ES constraint [25]. We also plan to extend the present paper to general Levy’s models. In such cases, approximating small jumps needs to be studied and the problem of stability may be interesting to investigate as in [12, 22].

Appendix: Auxiliary results

A Quantile and expected shorfall

Definition A.1 (Lower quantile).

For any random variable and , the lower -quantile of is the number defined by

| (A.1) |

The following is useful to provide an explicit form for the optimal solution.

Lemma A.1.

Let be the lower -quantile of the standard normal distribution and be the stochastic exponential defined in (2.7). Then,

| (A.2) |

Proof. It follows directly from the definition of and the linearity of lower quantile. ∎

Definition A.2 (Expected Shorfall).

For any random variable and , the expected shorfall at -quantile of is the real number defined by

| (A.3) |

for some random variable .

Again, the following simple result is useful to get the optimal solution in an explicit form.

Lemma A.2.

Let be the standard normal distribution function and be the stochastic exponential defined in (2.7). For any , we have

| (A.4) |

where is the lower -quantile of a standard normal random variable.

Proof. The definition (A.3) implies that

where . Direct calculus provides that and

and the conclusion follows. ∎

Risk of two portfolios can be compared using the following lemma.

Lemma A.3.

Let be two random variables satisfying a.s. Then, for any ,

| (A.5) |

Proof. For any , one has since almost surely. Then,

for any and hence . Let us prove the last inequality in (A.5). Clearly,

where is the distribution function of . The same representation can be also obtained for . Now, by definition,

By changing variable one obtains

and the conclusion follows by the first inequality. ∎

B Geometric Lévy martingale

Lemma B.1.

Let be a function satisfying

Then, the process defined by is a martingale and

Proof. See exercise 1.6 in [24]. ∎

C Exponential of optimal consumption rate

Lemma C.1.

For defined in (3.16) we have

| (C.1) |

Proof. It seems that a direct verification using (3.16) is technically hard. We may proceed as follows. Provided is an optimal portfolio, we need to choose such that the cost function is maximal, i.e.

where is defined by (3.15). This variation problem can be solved in two steps. First, By Holder’s inequality the above formula is bounded by

The equality happens when and are linearly independent in , i.e., a.s. on , where is a positive constant. It follows that

which implies that and the cost function is now given by

It remains to maximize by choosing an appropriate . As is concave, its maximum attains at the zero point of the first derivative , where Thus,

D Proof of Theorem 3.1

By (2.9), one has

| (D.1) |

since . Taking into account the independency of the terms in (2.11) one obtains

| (D.2) |

Therefore,

| (D.3) |

which is bounded by We then deduce that

Hence, is an upper bound of since . Now, if , the upper bound is attainable for any admissible strategy with and . In the contrary case if , then the upper bound is attained for and . ∎

E Proof of Lemma 3.1

Recall that and are respectively maximal points of

and

In other words, they are solutions to equations and , where

and

Clearly, and those two functions are decreasing. One obtains that . Moreover, as both and are concave in one has

which in turn leads to the comparison (see the defintion in (3.16)). Taking into the negative sign of one gets . ∎

References

- [1] P. Artzner, F. Delbaen, J.-C. Eber, and D. Heath. Coherent measures of risk. Mathematical Finance, 9(3):203–228, 1999.

- [2] Y. Aït-Sahalia, J. Cacho-Diaz, and T. R. Hurd. Portfolio choice with jumps: A closed-form solution. Ann. Appl. Probab., 19(2):556–584, 04 2009.

- [3] C. Atkinson and M. Papakokinou. Theory of optimal consumption and portfolio selection under a capital-at-risk (car) and a value-at-risk (var) constraint. IMA J. Mgmt Math., (16), 2005.

- [4] S. Basak and A. Shapiro. Value-at-risk-based risk management: optimal policies and asset prices. Rev. Finan. Stud., (14):371–405, 2001.

- [5] Bruno Bouchard and Marcel Nutz. Weak dynamic programming for generalized state constraints. SIAM Journal on Control and Optimization, 50(6):3344–3373, 2012.

- [6] B. Chouaf and S. Pergamenchchikov. Optimal investment with bounded var for power utility functions. In Y. Kabanov, editor, The collection of papers dedicated to the 60th anniversary of Marek Musiela. Springer, 2012.

- [7] D. Cuoco, H. Hua, and S. Issaenko. Optimal dynamic trading strategies with risk limits. 2001. Preprint, Yale International Center for Finance.

- [8] Jakvsa Cvitanić and Ioannis Karatzas. Convex duality in constrained portfolio optimization. The Annals of Applied Probability, pages 767–818, 1992.

- [9] Jakvsa Cvitanić and Ioannis Karatzas. Hedging contingent claims with constrained portfolios. The Annals of Applied Probability, pages 652–681, 1993.

- [10] S. R. Das and R. Uppal. Systemic risk and international portfolio choice. The Journal of Finance, 59(6):2809–2834, 2004.

- [11] D. Duffie and J. Pan. Analytical value-at-risk with jumps and credit risk. Finance and Stochastics, 5(2):155–180, 2001.

- [12] S. Emmer, C Klüppelberg, and R. Korn. Optimal portfolios with bounded capital at risk. Mathematical Finance, 11:365–384, 2001.

- [13] B. Eraker. Do stock trices and volatility jump? reconciling evidence from spot and option prices. The Journal of Finance, 59(3):1367–1404, 2004.

- [14] B. Erakere, M. Johnnes, and N. Polson. The impact of jumps in volatility and returns. The Journal of Finance, 58(3):1269–1300, 2003.

- [15] N.C. Framstad, B. Øksendal, and A. Sulem. Optimal consumption and portfolio in a jump diffusion market with proportional transaction costs. 1998.

- [16] N.C. Framstad, B. Øksendal, and A. Sulem. Optimal consumption and portfolio in a jump diffusion market with proportional transaction costs. Journal of Mathematical Economics, 35(2):233 – 257, 2001.

- [17] X. Jin and K. Zhang. Dynamic optimal portfolio choice in a jump-diffusion model with investment constraints. Journal of Banking & Finance, 37(5):1733 – 1746, 2013.

- [18] X. Jin and K. Zhang. Dynamic optimal portfolio choice in a jump-diffusion model with investment constraints. Journal of Banking and Finance, 37(5):1733 – 1746, 2013.

- [19] I. Karatzas and S.E. Shreve. Methods of Mathematical finance. Springer, Berlin, 1998.

- [20] C. Klüppelberg and S. M. Pergamenchtchikov. Optimal consumption and investment with bounded downside risk for power utility functions. In F. Delbaen, M. Rásonyi, and C. Stricker, editors, Optimality and Risk: Modern Trends in Mathematical Finance. The Kabanov Festschrift, pages 133–169. Springer, Heidelberg-Dordrecht-London-New York, 2009.

- [21] Claudia Klüppelberg and SM Pergamenshchikov. Optimal consumption and investment with bounded downside risk measures for logarithmic utility functions. Advanced Financial Modelling. Radon Ser. Comput. Appl. Math., Walter de Gruyter, Berlin, 8:245–273, 2009.

- [22] Jun Liu, Francis A Longstaff, and Jun Pan. Dynamic asset allocation with event risk. The Journal of Finance, 58(1):231–259, 2003.

- [23] R.C Merton. Option pricing when underlying stock returns are discontinuous. Journal of Financial Economics, 3:125–144, 1976.

- [24] B. Øksendal and A. Sulem. Applied Stochastic Control of Jump Diffusions. Springer-Verlag Berlin Heidelberg, 2007.

- [25] Traian A. Pirvu. Portfolio optimization under the value-at-risk constraint. Quantitative Finance, 7(2):125–136, 2007.

- [26] N. Touzi. Stochastic Control Problems, Viscosity Solutions and Applications to Finance. Scuola Normale Superiore di Pisa. Quaderni, Pisa, 2004.

- [27] KFC. Yiu. Optimal portfolios under a value-at-risk constraint. J. Econ. Dynam. Contr., 28:1317–1334, 2004.