XXX

Biswas, Gopalakrishnan, and Dutta

Managing Overstaying Electric Vehicles in Park-and-Charge Facilities

Managing Overstaying Electric Vehicles in Park-and-Charge Facilities

Arpita Biswas

\AFFXerox Research Centre India, Bangalore, Karnataka 560103,

Arpita.Biswas@xerox.com

\AUTHORRagavendran Gopalakrishnan

\AFFXerox Research Centre India, Bangalore, Karnataka 560103,

Ragavendran.Gopalakrishnan@xerox.com

\AUTHORPartha Dutta

\AFFXerox Research Centre India, Bangalore, Karnataka 560103,

Partha.Dutta@xerox.com

With the increase in adoption of Electric Vehicles (EVs), proper utilization of the charging infrastructure is an emerging challenge for service providers. Overstaying of an EV after a charging event is a key contributor to low utilization. Since overstaying is easily detectable by monitoring the power drawn from the charger, managing this problem primarily involves designing an appropriate “penalty” during the overstaying period. Higher penalties do discourage overstaying; however, due to uncertainty in parking duration, less people would find such penalties acceptable, leading to decreased utilization (and revenue). To analyze this central trade-off, we develop a novel framework that integrates models for realistic user behavior into queueing dynamics to locate the optimal penalty from the points of view of utilization and revenue, for different values of the external charging demand. Next, when the model parameters are unknown, we show how an online learning algorithm, such as UCB, can be adapted to learn the optimal penalty. Our experimental validation, based on charging data from London, shows that an appropriate penalty can increase both utilization and revenue while significantly reducing overstaying.

park-and-charge; revenue optimization; sustainable behavior; multi-armed bandits \SUBJECTCLASSPrimary: Queues: applications, optimization; secondary: Probability: stochastic model applications

1 Introduction.

As the number of on-road Electric Vehicles (EVs) increases rapidly, lack of adequate charging infrastructure is an area of growing concern. For example, a recent New York Times article reports that in California, scarcity of park-and-charge spots is a chronic problem: “Electric-vehicle owners are unplugging one another’s cars, trading insults, and creating black markets and side deals to trade spots in corporate parking lots” [NYTimesArticle]. While investing in a wide-spread deployment of charging stations by both public and private service providers is needed to address the infrastructure problem in the long-term, effective use of the existing charging infrastructure can help in significantly reducing this problem. In particular, curbing improper utilization of park-and-charge spots can improve their availability. Two prominent causes of utilization degradation are (i) the overstaying problem, where an EV continues to occupy a park-and-charge spot even after it is fully charged, and (ii) the “icing” problem, where a gas-powered car (Internal Combustion Engine or ICE vehicle) occupies a park-and-charge spot.

While icing and overstaying in park-and-charge spots are illegal in increasingly many jurisdictions, there is little or no enforcement [NoEnforcementIcing], as a result of which the frustrated users resort to ad-hoc measures ranging from mild (e.g., leaving courtesy notices) [CourtesyNotice1, CourtesyNotice2] to drastic (e.g., publicly shaming the violator by posting a picture of the violation showing the violator’s license plate on blogs and social media) [PublicShaming1, PublicShaming2]. Extension cables that can help charge a vehicle parked a few spots away from an occupied park-and-charge spot are available in the market, but are very expensive [ExtensionCable]. A longer term solution to these problems, however, will require both enforcement and an appropriate penalty for these events.

While enforcement with heavy penalty may help curb icing, a gentler approach is prudent to manage overstaying EVs. Depending on the demand for charging, overstaying EVs potentially block access to other EVs that might need charging, and so, it is important to discourage such behavior by imposing penalties. But, imposing too high a penalty might turn away EVs from using the park-and-charge facility altogether due to increased risk of a steep fine, since EV users may not exactly know their parking duration beforehand.

Our central contribution in this paper is a novel framework that combines a realistic user behavior model with traditional queueing dynamics to capture this trade-off and study the optimal penalty from the points of view of both utilization and revenue. Next, when the model parameters are unknown, we show how the well known UCB learning algorithm can be adapted to learn the optimal penalty over a period of time. Our experiments, based on charging data from London, show that an appropriate penalty results in increased utilization and significantly increased revenue. Also, perhaps surprisingly, we observe that the utilization achieved by imposing the revenue-maximizing penalty is very close to the maximum utilization.

1.1 Related work.

Dynamic pricing of parking has been an area of active study in the transportation literature. In [onnokdd, rowe2011], the authors present dynamic pricing schemes for regular parking based on estimated demand to reduce both congestion and underuse. On the other hand, significant work has also been done on dynamic pricing of electric vehicle charging. In [tushar2012], the authors model the problem as a Stackelberg game between the smart grid as the leader setting the price, and the vehicle owner as the follower deciding their charging strategies. In [anglin2013, gadh2012, hafner2009], dynamic pricing of electricity for charging EVs is proposed based on the usage data in a given location and time. None of the above work, however, consider the problem of overstaying EVs. To the best of our knowledge, this is the first paper to investigate designing penalty schemes for park-and-charge facilities to combat overstaying EVs.

To address the situation where the probability distributions required for modelling user behaviour remain unavailable to the system until the users are actually observed, and the user behaviour needs to be learned over time, we model our problem as a Multi-Armed Bandit (MAB) problem, which has been well studied [bubeck2012regret, auer2002finite, cesa2006prediction, agrawal1995sample] and applied to a wide variety of domains such as crowdsourcing, online advertising, dynamic pricing, and smart grids. However, we are not aware of any application of MABs to the park-and-charge scenario.

2 Park-and-Charge system model.

We adopt a simple three-part model for a parking area:

-

(a)

Section 2.1 introduces the pricing function (during charging) and penalty function (during overstaying) for an EV.

-

(b)

Section 2.2 models how EV users respond to the posted penalty scheme, i.e., (i) whether they agree to its terms and enter the parking area, and if so, (ii) how long they stay.

-

(c)

Section 2.3 models the flow of EV users in and out of the parking area using queueing dynamics.

We end the section by defining some performance measures of interest in Section 2.4.

2.1 Pricing and penalty functions.

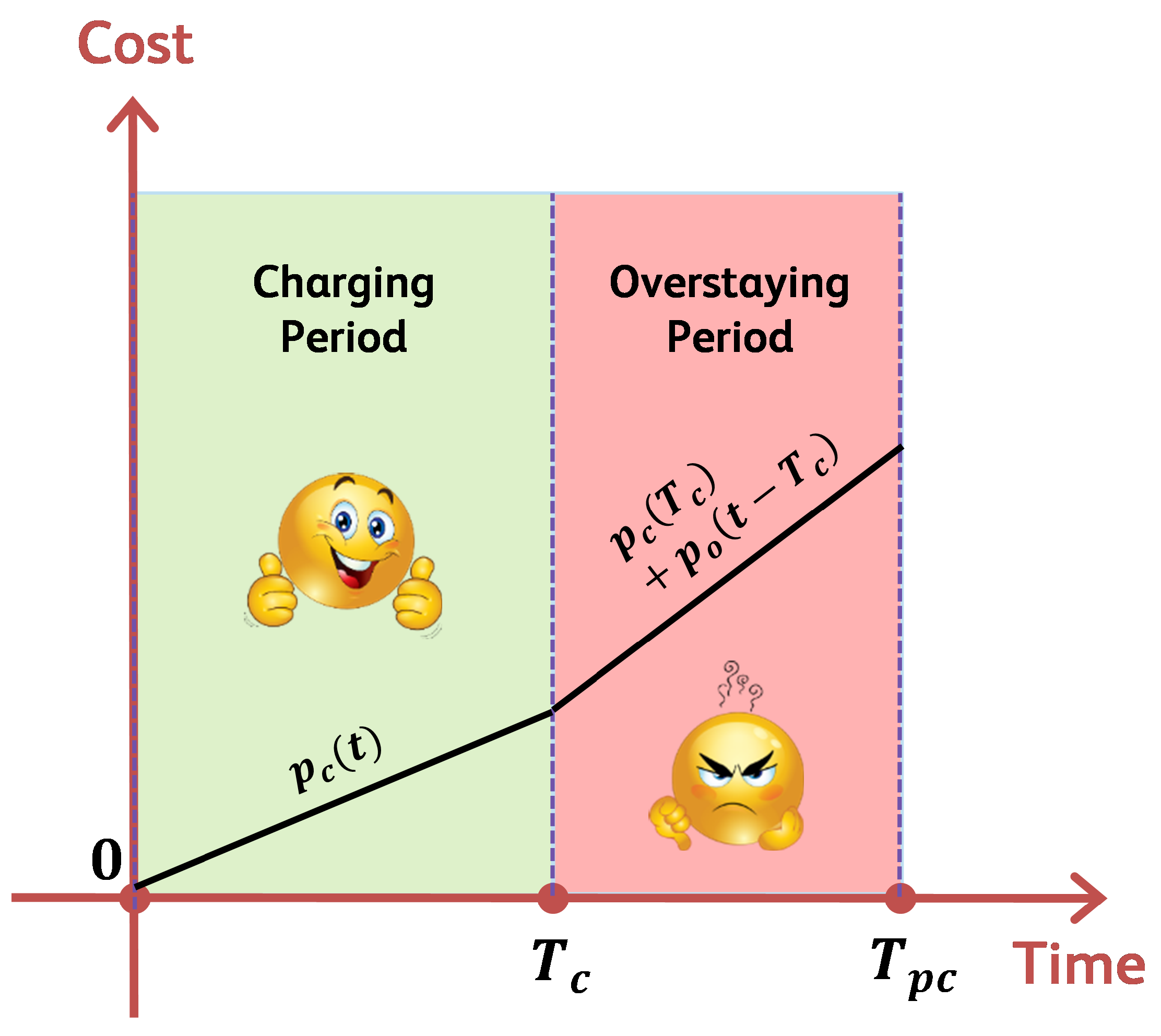

Let the price function while actively charging be and the penalty function for overstaying at a park-and-charge spot after charging is complete be , where , and and are continuous, nondecreasing functions. In addition, we assume that is a strictly increasing function, since we will need its inverse function, , to be well defined.111The framework can be extended to the case where is not strictly increasing, by defining . This could accommodate, for example, an initial “grace period” (no penalty) after charging is complete. To be realistically implementable (easily understandable by an average user), these functions should not be more complicated than simple piecewise linear functions; however, our framework is general and can accommodate arbitrary functions. These functions are illustrated in Figure 1.

2.2 EV user behavior.

We define the following parameters, for each EV user:

-

•

, the duration of time it would take to fully charge their electric vehicle,

-

•

, the length of their appointment, i.e., the EV user’s preferred parking duration, and

-

•

, the “penalty threshold”, i.e., the maximum penalty as a result of overstaying that they would bear for the convenience of an uninterrupted appointment.

Let , , be independent, nonnegative random variables with finite means and cumulative distribution functions respectively.

Penalty acceptance probability: When a user arrives at the parking area and inspects the posted penalty scheme, they know their and values, but they may not know exactly how long their appointment will last; hence is not yet realized. However, the user can still estimate the likelihood that their penalty would not exceed , as follows:

| (1) |

Thus, we assume that an arriving user will enter the parking lot with probability . Let denote its mean, given by:

| (2) |

Actual parking duration: If a user decides to enter the parking area, they park their EV at a park-and-charge spot and leave for their appointment. is then realized, and if it exceeds , we assume that the user reluctantly interrupts their appointment to avoid paying more than penalty. Thus, the actual parking duration is given by:222If the realized value of is less than , we assume that the user leaves immediately after time units, without waiting for their EV to finish charging.

| (3) |

and hence, the duration of time the EV overstays is given by:

| (4) |

Revenue collected: The revenue from an EV’s time at the park-and-charge spot (the cost to the EV user) is given by:

| (5) |

2.3 Queueing model.

Since there is a finite number of park-and-charge spots in the parking area, the impact of overstaying depends on the arrival process to the parking lot, e.g., if the inter-arrival times are uniformly distributed with a low arrival rate, a limited amount of overstaying may be harmless, as opposed to a high arrival rate during weekends at a mall. We capture such phenomena using an /// queueing model [Kleinrock75], where the EVs that accept the posted penalty scheme and enter the parking lot are the “jobs”, and the park-and-charge spots are the “servers”. The parameters and assumptions are as follows:

-

•

EVs arrive at the parking area according to a Poisson process with rate . However, only those EVs whose users accept the posted penalty scheme (with probability , given by (1)), and enter the parking area are counted for further analysis. Using the total probability theorem and the well known “Poisson splitting” property, it can be shown (see Proposition 2.1 below) that this “filtered” arrival process is still Poisson, with rate , where is given by (2).

-

•

An arriving EV that finds all park-and-charge spots occupied leaves the system (there is no waiting). Otherwise, the EV stays at a park-and-charge spot for a duration of , given by (3); thus, the service times are i.i.d. according to the cumulative distribution function of .333This could be a general distribution; however, in an /// system, the stationary distribution of its Markov chain (that tracks the number of EVs) depends on the service time distribution only through its mean.

If is the random variable denoting the number of EVs in the parking area, then its steady state distribution is given by:

| (6) |

where is the “offered load”. Thus, in steady state, the mean number of EVs in the parking area is:

| (7) |

Proposition 2.1

Let be a Poisson process with rate , and let each arrival counted by this process be associated with a parameter that is drawn independently for each from a common distribution . If is a filtered process that counts each -arrival with probability , then is also a Poisson process with rate , where .

Proof 2.2

Proof. The probability with which a random -arrival is counted is given by

where denotes the cumulative distribution function of . The first step follows from the total probability theorem, and the last step is the definition of expectation. It then follows from the well known Poisson splitting property that the filtered process is also Poisson with rate .

2.4 Performance measures.

We define the following performance measures of interest. Throughout, denotes an arbitrary duration of time.

-

(a)

Throughput: The throughput of the park-and-charge system, denoted by , is the average rate at which EV users leave the park-and-charge area, given by:

(8) -

(b)

Overstay: The fraction of time spent overstaying at park-and-charge spots, denoted by , is given by:

(9) -

(c)

Utilization: The utilization, denoted by , is defined as the fraction of time the park-and-charge spots were used for charging, and is given by:

(10) -

(d)

Revenue Rate: The revenue rate is defined as the average rate at which revenue is accrued from the park-and-charge spots, and is given by:

(11)

When , , are generally distributed, and the price/penalty functions , are general, the above quantities do not admit closed form expressions, and we defer their (partial) mathematical derivations to Appendix LABEL:appendix:computeExpr. However, in Section 3, we investigate a simple special case where the price/penalty functions are linear, and are Exponentially distributed, and is a constant, and derive closed form expressions for these performance measures.

Benchmarking performance: In order to measure the effectiveness of our penalty scheme, we benchmark it against a system with “ideal” human behavior, one in which the EV users, on their own, do not overstay, i.e., . Here, , and the revenue from (5) is simply .

3 Example scenario: Linear functions, Exponential distributions.

In this section, we consider a simplified scenario for which we derive closed form expressions for the performance measures, which allows better analysis of the effectiveness of imposing simple, linear penalties for overstaying. In particular, we assume:

-

•

Linearity: Let and , where and are the parameters.

-

•

and are Exponentially distributed with parameters and respectively.

-

•

is not a random variable, but a constant.

Under these assumptions, the acceptance probability from (1) and its mean from (2) can be evaluated to obtain and respectively, where

| (12) |

Conditional distribution of : While is Exponentially distributed by assumption, given that (with probability ,) an EV accepts the posted penalty and enters the parking lot (call this event ), the conditional random variable need not be Exponential. ( remains unchanged, since does not depend on it.) Thus, we first compute the conditional probability density function, , using Bayes’s rule, to obtain:

3.1 Distribution and mean of .

The complementary cumulative distribution function of , defined as , can be evaluated as:

Thus, the mean, given by , can be evaluated as:

| (13) |

where .

3.2 Distribution and mean of .

The complementary cumulative distribution function of , defined as , can be evaluated as:

Thus, the mean, given by , can be evaluated as:

| (14) |

where .

3.3 Mean revenue.

3.4 Performance measures.

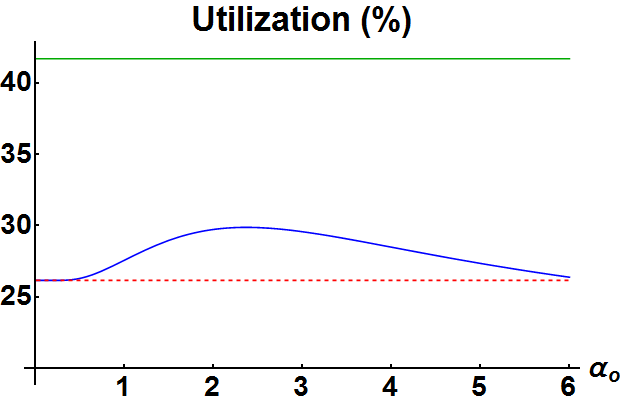

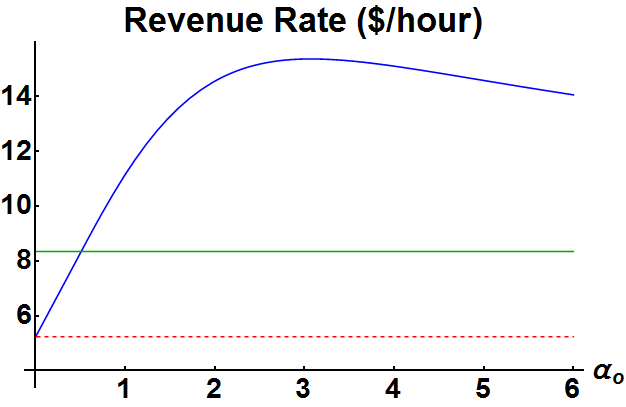

By inspecting the expressions, it can be seen that is increasing in . Hence, with increasing penalty, increases and decreases. The other quantities, including performance measures (8)-(11), are more complicated and their behavior is not obvious from inspection. As an example, when we set slots, EVs per hour, per hour, per hour, , per hour, we find that setting the penalty rate per hour provides the maximum value of utilization (), whereas the utilization with no penalty is about . (The maximum possible utilization, under the ideal setting where there is no overstaying is .) From the point of view of revenue, setting the penalty rate per hour provides the maximum revenue rate of per hour, but the decreased utilization at this penalty rate is only slightly less, at . (The ideal revenue when there is no overstaying is merely per hour.) Thus, the revenue maximizing penalty rate provides increased utilization (by ), as well as significantly increased revenue (by ). (See Figure 2.)

4 Dynamic environment.

In this section, we consider a real world setting where no prior information about the distributions , , is known, and thus, the expressions for the performance measures are also unknown to the framework. We assume that these distributions are unknown, but fixed for the day; hence, the utilization and revenue for the day depend only on .

In our model, on each day, a penalty rate is declared at the entrance to the parking area. Arriving customers behave according to their , , values (which are unknown to the system, but known to the customers), and the posted penalty rate ; their behavior is as described in Section 2.2. The system observes the customer behavior only after they enter the parking area. Thus, the performance measures (such as revenue rate, utilization, etc.) corresponding to penalty rate are only observed at the end of the day. The task is to find an optimal penalty rate for each day, such that the total revenue over all days is maximized.444Variants of the technique presented here can be used for other performance measures such as utilization.

This problem is an example of sequential decision making in an unknown and dynamic environment, where the system seeks to optimize the average revenue over all days, while continuously gathering more information about the revenue obtained by using different penalty rates . This leads to a trade-off between exploration (imposing each penalty rate sufficiently often to obtain better estimates of the corresponding revenue accumulated) and exploitation (frequently imposing the optimal penalty for which the observed revenue is maximized). Such problems naturally fall into the category of stochastic multi-armed bandit (MAB) problems [bubeck2012regret]. Each penalty rate is considered as an arm, and the daily revenue obtained by imposing that penalty rate is analogous to the reward obtained by pulling the corresponding arm. The goal in the MAB setting is to determine the arm to be pulled each time in order to maximize the total reward obtained.

4.1 Learning algorithm UCB-PC.

Let denote a finite, ordered set of penalty rates, and let denote the expected daily revenue corresponding to penalty rate , which is unknown. The (unknown) optimal penalty rate is thus given by , where . In order to estimate , on each day, we impose a penalty rate and observe the daily revenue, which is the sum of the payments made by the customers who choose to enter the parking area that day.555We observe, for each customer, whether they choose to enter the parking area or not, and if they do, their charging and overstaying times, as well as their final payment. In doing so, we keep track of the observed average daily revenues , which are then used to gradually learn the optimal penalty rate for the parking area. Algorithm 1 is based on the techniques used in the algorithm [auer2002finite], which is a well known tool for solving stochastic multi-armed bandit problems. However, assumes that the system is allowed to run only for a finite number of trials (“finite horizon multi-armed bandit”), whereas we operate under the assumption that the system runs for infinite time, and must therefore tackle the challenges involved in adapting to the infinite horizon setting.666While was our choice to illustrate the technique, we believe that our framework can also accommodate modified versions of other stochastic multi-armed bandit algorithms (such as ).

4.2 Performance analysis.

In this section, we compare the performance of our learning algorithm with an optimal algorithm that knows the expected revenues beforehand, and can therefore choose the optimal penalty every day. The loss incurred by the learning algorithm over days is termed as the regret , and can be written as

| (16) |

where denotes the expected number of days (out of ) that penalty rate is chosen by our learning algorithm. In the literature, the performance of multi-armed bandit algorithms is measured by obtaining an upper bound on this regret. In [auer2002finite], the authors show that the upper bound on the regret using is sublinear within a finite, fixed horizon ; in particular, they show that the regret is bounded above by a term that is . Next, in Theorem 4.1, we show that the regret for - is upper bounded by after the algorithm runs for days, for all .

Theorem 4.1

The expected regret of -, after the algorithm runs for days, is .