Median bias reduction of maximum likelihood estimates

Abstract

For regular parametric problems, we show how median centering of the maximum likelihood estimate can be achieved by a simple modification of the score equation. For a scalar parameter of interest, the estimator is equivariant under interest respecting parameterizations and third-order median unbiased. With a vector parameter of interest, componentwise equivariance and third-order median centering are obtained. Like Firth’s (1993, Biometrika) implicit method for bias reduction, the new method does not require finiteness of the maximum likelihood estimate and is effective in preventing infinite estimates. Simulation results for continuous and discrete models, including binary and beta regression, confirm that the method succeeds in achieving componentwise median centering and in solving the infinite estimate problem, while keeping comparable dispersion and the same approximate distribution as its main competitors.

Some key words: Binary regression; Infinite estimate; Modified score; Parameterization invariance; Separation problem; Skew normal; Tensor.

1 Introduction

In regular parametric estimation problems, both the maximum likelihood estimator and the score estimating function have an asymptotic symmetric distribution centered at the true parameter value and at zero, respectively. However, the asymptotic behaviour may poorly reflect exact sampling distributions with small or moderate sample information, sparse data or complex models. Several proposals have been developed to correct the estimate or the estimating function.

Most available methods are aimed at approximate bias adjustment, either of the maximum likelihood estimator or of the profile score function when nuisance parameters are present. We refer to Kosmidis (2014) for a review of bias reduction for the maximum likelihood estimator and to McCullagh & Tibshirani (1990), Stern (1997) and subsequent literature for bias correction of the profile score.

In the absence of nuisance parameters, the score function is exactly unbiased and therefore no correction appears to be necessary. A change of parameterization does not affect this property and the solution of the score equation, namely the maximum likelihood estimator, behaves equivariantly under reparameterizations. On the other hand, bias correction of the maximum likelihood estimator is tied to a specific parameterization.

Lack of equivariance also affects the so-called implicit bias reduction methods (Kosmidis, 2014) that achieve first-oder bias correction through a modification of the score equation, following Firth (1993). This lack of coherence is highlighted e.g. in Kosmidis (2014), but somehow overwhelmed by advantages in applications, possibly with a careful choice of the working parameterization (Kosmidis & Firth, 2010, § 4.2, Remark 3). Indeed, one major advantage of the approach in Firth (1993) and Kosmidis & Firth (2009) is that the modified estimating equation does not depend explicitly on the maximum likelihood estimate. The modified score equation has been found to overcome infinite estimate problems that may arise with positive probability mainly, but not only, in models for discrete or categorical data.

Considering first a scalar parameter of interest, we propose a new median modification of the score, or profile score, equation whose solution respects equivariance under monotone reparameterizations. Like Firth’s (1993) implicit method, this proposal does not rely on finiteness of the maximum likelihood estimate and is effective in preventing infinite estimates. The modification is obtained by considering the median, instead of the mean, as a centering index for the score and defining a new estimating function by subtracting from the score its approximate median.

Provided that the modified score equation has a unique solution, median centering of the score function implies median centering of the corresponding estimator. Therefore, the resulting estimator is approximately median unbiased (see e.g. Read, 1985), that is the true parameter value is approximately a median of the distribution of the estimator. In some instances exact median unbiased estimates can be obtained (see Hirji et al., 1989). Outside exactness cases, available approximations for median unbiased estimates are based on higher-order likelihood asymptotics. Approximations based on the modified signed likelihood ratio (Barndorff-Nielsen, 1986) have been developed in Pace & Salvan (1999), Giummole & Ventura (2002), Biehler et al. (2015). They rely, however, on finiteness of the maximum likelihood estimate. Third-order median unbiasedness of the new estimator is seen to hold in the continuous case and extensive numerical evidence indicates remarkable median centering also in the discrete case.

We show how the method can be extended to a vector parameter by simultaneously solving median bias corrected score equations for all parameter components. This leads to componentwise third-order median unbiasedness and parameterization equivariance.

Examples and simulation results in a number of models, including binary and beta regression, indicate that the new estimator provides a notable improvement over the maximum likelihood estimator and solves the infinite estimates problem, both for a scalar and for a vector parameter.

2 Median modified score for a scalar parameter of interest

2.1 No nuisance parameters

For data , consider a regular model with probability mass function , . Let be the corresponding log likelihood and , the score function. The maximum likelihood estimator is solution of . We assume that Fisher information, , and the third-order cumulant of are finite and of order , where is the sample size or, more generally, an index of information in the data.

Using Cornish-Fisher expansion (see e.g. Pace & Salvan, 1997, § 10.6), the following asymptotic expansion holds for the median under , , of the score in the continuous case

with . A modified score equation can thus be defined by equating to the leading term of its median. This suggests defining the median modified score

| (1) |

where the modification term is of order . Let be the estimator defined as solution of .

For , we have and it is shown in the Appendix that is third-order median unbiased, i.e.

| (2) |

If is the unique solution of , the events and are equivalent so that will be third-order median unbiased, i.e.

| (3) |

Like , also is asymptotically , so that Wald-type confidence intervals only differ in location. Score-type confidence intervals can also be used, based on the asymptotic distribution of .

If is a smooth reparameterization with inverse , ingredients of the modification term in (1) in the new parameterization are and , where . Hence, like , the modified score transforms as a covariant tensor of order one, namely the modified score in the parameterization is . Therefore, behaves equivariantly as does , and is also third-order median unbiased.

Firth’s (1993) method gives an estimator with bias of order in a chosen parameterization. For a scalar parameter, the corresponding modified score is

| (4) |

where , with . As shown by Kosmidis & Firth (2010, § 3.4) in the vector parameter case, does not transform as a covariant tensor of order one under reparameterizations. This is because, while behaves tensorially, the same is not true for the term . Therefore, as is natural, first-order bias correction only operates in the reference parameterization. A suggestion in Kosmidis & Firth (2010, § 4.2, Remark 3) is to obtain the correction in a parameterization where the distribution of the maximum likelihood estimator is closer to normality, such as the logit for probability parameters, and then translate the result in the parameterization of interest.

The argument leading to (2) and (3) only holds in the continuous case. Indeed, in the discrete case, the Cornish-Fisher expansion involves also oscillatory terms (see e.g. Cai & Wang, 2009, formula (A.1)). These terms will be ignored in the following and the same adjustment will be employed both in the continuous and in the discrete case. Empirical results in the paper show a gain in median unbiasedness using (1) in place of also in the discrete case. The effect of omitting the oscillatory terms in a simple logistic regression is illustrated in detail in the Supplementary Material, showing that is uniformly closer to the exact median unbiased estimator than . Moreover, as the number of points in the support of the sufficient statistic increases, gets much closer to the exact median unbiased estimator than .

For a one parameter exponential family with canonical parameter , i.e. with

| (5) |

the median modified score function has the form

where and . In this parameterization, can be seen as the score of the penalized log likelihood On the other hand, Firth’s (1993) modified score takes the form

| (6) |

The effect of the median modification is thus to penalize the likelihood by , while (6) implies a Jeffreys prior penalization.

Under model (5), , hence, if , the estimating equation provides, in the continuous case, an approximate version of the optimal median unbiased estimator for monotone likelihood ratio families, calculated as the value of such that (Lehmann & Romano, 2005, § 3.5). Use of amounts to replace the exact with its Edgeworth expansion up to terms of order . It is straightforward to see that .

In general, a regular model has locally a monotone likelihood ratio with respect to the score function (Cox & Hinkley, 1974, § 4.8.i). As a consequence, optimality of as defined e.g. in Pace & Salvan (1997, formula (3.58)) will hold locally in a neighbourhood of .

Example 1. Normal distribution with known mean. Let be a random sample from , with known . Quantities for computing (1) and (4) are given in Firth (1993, § 4.2). In particular, the adjustment in (4) is equal to zero, so that , with , is exactly unbiased. The median modified score (1) is equal to , giving , equal to the optimal median unbiased estimator plus an error of order . Consider now the parameterization with the standard deviation . By equivariance, and , while the bias reduced estimator calculated in the new parameterization is .

Example 2. Skew normal shape parameter. Let be independent realizations of a skew normal distribution with shape parameter and density , where and denote the standard normal density and distribution functions, respectively, and . The log likelihood is where . With , , the score function is Let . The expected quantities needed to compute the median modified score (1) are and , giving . The modified score (4) (see Sartori, 2006) is .

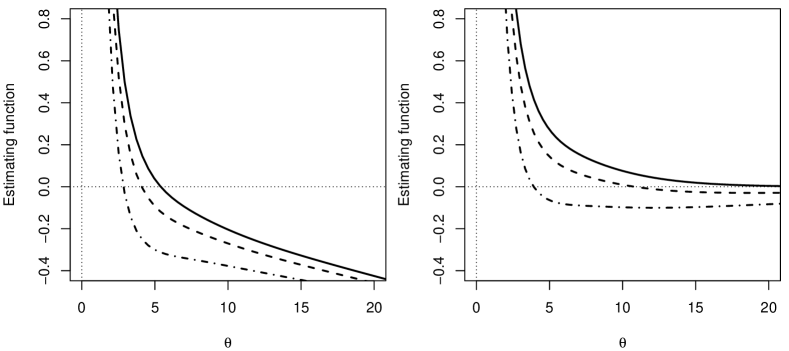

The performance of , and has been investigated by Monte Carlo simulations with 5,000 replications. Results are displayed in Table 1. Estimators are compared in terms of empirical probability of underestimation, median absolute error, bias, root mean squared error and coverage of 95% Wald-type and score-type confidence intervals. The empirical probability of underestimation is the summary of primary interest for , as the estimator is designed to satisfy (3). A natural associated measure of dispersion is the median absolute error. Estimated bias and root mean squared error are also reported to enable a fair comparison with . While and are always finite, in some samples the maximum likelihood estimate is infinite. The simulation frequency of finite maximum likelihood estimates, (), is reported in the table. As in Kosmidis & Firth (2009, § 6.2), estimated bias, root mean squared error and coverage probability of confidence intervals for are conditional upon its finiteness. Although this favours , both and are uniformly better. Median centering improvement attained by , as measured by empirical probability of underestimation, is remarkable, both for small and moderate sample sizes. On the other hand, the estimated root mean squared error is much smaller for of than for . In this case, values of are intermediate between those of and . This effect is illustrated, for the same sample as in Example 1 of Sartori (2006), in Fig. 1. Score-type confidence intervals have overall better coverage than Wald-type intervals, although this effect is substantial only for . Indeed, the penalization implied by is excessive, leading to poor coverage of Wald-type confidence intervals. Coverage probabilities for maximum likelihood should be judged with caution since samples with infinite estimates are excluded.

| PU | MAE | B | RMSE | Wald | Score | () | |||

| 5 | 20 | 36.2 | 2.31 | 1.90 | 8.44 | 94.5 | 94.7 | 72.2 | |

| 92.8 | 1.91 | -1.70 | 2.01 | 68.4 | 87.0 | ||||

| 53.8 | 1.73 | 0.94 | 4.02 | 91.1 | 92.5 | ||||

| 50 | 41.0 | 1.31 | 1.93 | 8.67 | 96.5 | 95.0 | 96.0 | ||

| 67.7 | 1.20 | -0.28 | 1.79 | 86.2 | 90.3 | ||||

| 50.3 | 1.21 | 1.25 | 4.82 | 93.9 | 93.4 | ||||

| 100 | 42.7 | 0.86 | 0.82 | 3.64 | 96.9 | 96.1 | 99.9 | ||

| 60.9 | 0.84 | 0.00 | 1.50 | 91.9 | 92.8 | ||||

| 49.8 | 0.84 | 0.49 | 2.20 | 95.5 | 95.3 | ||||

| 10 | 20 | 29.7 | 2.12 | 20.11 | 90.6 | 93.9 | 49.2 | ||

| 99.8 | 6.16 | -5.94 | 6.06 | 20.4 | 83.7 | ||||

| 73.0 | 3.57 | -1.36 | 5.35 | 83.2 | 91.7 | ||||

| 50 | 36.9 | 3.73 | 5.11 | 30.11 | 95.5 | 95.2 | 80.2 | ||

| 87.2 | 3.25 | -2.59 | 3.56 | 73.5 | 88.4 | ||||

| 52.6 | 3.10 | 2.30 | 8.67 | 92.0 | 93.4 | ||||

| 100 | 40.1 | 2.50 | 3.92 | 15.95 | 96.1 | 95.4 | 96.0 | ||

| 68.0 | 2.28 | -0.52 | 3.53 | 86.9 | 90.8 | ||||

| 49.6 | 2.32 | 2.57 | 10.01 | 93.9 | 93.9 |

-

•

PU, percentage of underestimation; MAE, median absolute error; B, bias; RMSE, root mean squared error; Wald and Score, percentage coverage of 95% Wald-type and score-type confidence intervals.

2.2 Presence of nuisance parameters

With , we denote by , , the elements of the score vector . Let be a generic entry of Fisher information, , and an entry of its inverse, . Let and be higher order partial derivatives of with respect to elements of with indices . Moreover, expected values of log likelihood derivatives are denoted as , , and .

Let us suppose now that the parameter is partitioned as , with a scalar parameter of interest. When exact elimination of by conditioning or by marginalization is feasible, arguments in the previous subsection may be applied to the conditional or marginal score for . See e.g. Hirji et al. (1989) for exact conditional median unbiased estimators in logistic regression. In more general situations, or when an expression for the exact solution is not available, we propose a modification of the profile score. Let us denote by the profile log likelihood for , where is the maximum likelihood estimate of for a given value of . The profile score is . Let us use subscript when referring to and indices to refer to components of , so that elements of are and , . As is well known, and approximate expressions for the first three cumulants of are

| (7) |

where the error term is of order in and of order in and . In (7), Einstein summation convention is used, i.e. summation over repeated indices is understood. The quantity is an element of the inverse of the square matrix of order with entries , and is a regression coefficient of on the vector with elements , . The above expression for was obtained in McCullagh & Tibshirani (1990). Approximations and are the second and third cumulants of the efficient score for , namely , which is the leading term of the expansion of . They are obtained from formulae (7.15) and (7.16) in Barndorff-Nielsen & Cox (1989) for cumulants of residuals.

In a continuous model, using a Cornish-Fisher expansion, the median of the standardized profile score is equal to . Therefore, the median modified profile score is

| (8) |

and has median zero with error of order . The same argument as in the proof of (2) shows that . Let be the estimator defined as solution of with replaced by . If the resulting estimating equation has a unique solution, third-order median unbiasedness of follows. Although this argument only holds in the continuous case, empirical results for binary regression in Examples 4 and 7 show a gain in median unbiasedness using (8) in place of also in the discrete case. See the Supplementary Material for a numerical comparison of with the exact conditional median unbiased estimator. The asymptotic distribution of is the same as that of , that is . This can be used to construct Wald-type confidence intervals. Score-type confidence intervals can also be used, based on the asymptotic distribution of .

Substituting for has the drawback of requiring the solution of for fixed , . Although infinite values of the constrained estimate of may not be a problem in (8), joint estimation as described in § 3 is often preferable.

Parameterization equivariance of holds under interest respecting reparameterizations. In detail, let be a smooth reparameterization with and and a one-to-one function of with inverse . Then, the modified score for in the new parameterization is , so that . This tensorial behaviour of the modified profile score follows from the tensorial behaviour of the profile score and of its first-order expectation (Pace & Salvan, 1997, § 9.5.3). In addition, the efficient score also transforms tensorially and therefore so does the ratio .

If is an exponential family of order with canonical parameter , i.e.

quantities (7) are simply obtained from derivatives of . In particular, is a generic element of , , and all other quantities are the derivatives of with respect to components of appearing as subscripts. Here, is an approximation with error of order of the score for in the conditional model given (see e.g. Pace & Salvan, 1997, § 10.10.2). In the continuous case, the estimator from (8) is an approximation of the optimal conditional median unbiased estimator (Lehmann & Romano, 2005, § 5.4), solution with respect to of . The approximation is obtained by replacing with its mixed Edgeworth-saddlepoint approximation (Barndorff-Nielsen & Cox, 1989, § 7.5, Pace & Salvan, 1992) up to terms of order .

In the examples below, is compared with and with , i.e. the component of the bias reduced maximum likelihood estimator , calculated according to formula (4.1) in Firth (1993).

Example 3. Normal distribution (cont.). Consider again the setting of Example 2.1 with both and unknown and let be of interest. The maximum likelihood estimator is , with . Firth (1993, § 4.2) shows that , which coincides with the usual unbiased estimator. Formula (8) gives , so that , that is equal to the optimal median unbiased estimator plus an error of order . In the parameterization, with , the bias reduced estimator is .

Example 4. Binary regression. Let , , be independent realizations of binary random variables with probability , where , is a row vector of covariates and is a known cumulative distribution function. We assume that a generic scalar component of is of interest and treat the remaining components as nuisance parameters. Quantities needed for (8) are given in the Supplementary Material.

As an example, we consider the endometrial cancer grade dataset analyzed, among others, in Agresti (2015, § 5.7.1). The goal of the study was to evaluate the relationship between the histology of the endometrium of 79 patients and three risk factors: neovasculation, pulsatility index of arteria uterina and endometrium height. Logistic regression has been fitted with parameter , where is an intercept and the remaining parameters correspond to neovasculation, pulsatility index of arteria uterina, and endometrium height, respectively. Maximum likelihood leads to infinite maximum likelihood estimate of due to quasi-complete separation. Let us consider as the parameter of interest while the remaining regression coefficients are treated as nuisance parameters. Both and from (8) are finite with and . The corresponding standard errors are 1.551 and 2.407, respectively.

To assess the properties of estimators of , we performed a simulation study with sample size and covariates as in the endometrial dataset and with . The results are presented in Table 2. We found 684 samples out of 10,000 with data separation. Empirical probability of underestimation indicates that has a remarkable performance in terms median centering. On the other hand, as expected, has estimated bias close to zero. Coverages of Wald-type confidence intervals based on and on are comparable, while those based on are favoured by being computed only using samples with finite estimates. Score-type intervals based on perform slightly better than Wald-type ones, while score-type confidence intervals for scalar components of the parameter are not available when using bias reduction.

| PU | MAE | B | RMSE | Wald | Score | |

| 43.0 | 0.66 | 0.12 | 0.90 | 97.5 | 98.9 | |

| 53.1 | 0.56 | 0.02 | 0.90 | 97.4 | – | |

| 49.7 | 0.60 | 0.16 | 1.09 | 97.7 | 95.7 |

-

•

PU, percentage of underestimation; MAE, median absolute error; B, bias; RMSE, root mean squared error; Wald and Score, percentage coverage of 95% Wald-type and score-type confidence intervals.

The modified profile score (8) can also be seen as a median modification of a first order bias corrected profile score , with evaluated at (McCullagh & Tibshirani, 1990). This is equivalent to the score of an adjusted profile likelihood, such as the modified profile likelihood (Barndorff-Nielsen, 1983). Many available adjustments of the profile likelihood share indeed the common feature of reducing the score bias to (DiCiccio et al., 1996). In the presence of many nuisance parameters, typically the term dominates . For instance, in a stratified setting with independent , and , having marginal distribution depending on with both and diverging as in Sartori (2003), the term in (8) is of order , while is of order . Therefore, the difference between and , the maximizer of the modified profile likelihood, is of order and both estimators have the standard asymptotic behaviour provided that , as opposed to the stronger condition for the maximum likelihood estimator.

Example 5. Gamma samples with common shape parameter. Let , and , be realizations of independent gamma random variables with shape parameter and scale parameter . The needed quantities in (8) are

where and is the poly-gamma function of order Here, the conditional maximum likelihood estimator, , based on the distribution of given the stratum sums is also available and is asymptotically equivalent to both and , provided that (Sartori, 2003, Example 2).

Simulation results with 10,000 replications are shown in Table 3 for , , . We compared , , , , the bias reduced estimator in the parameterization and the estimator , where is the bias reduced estimator of in the parameterization , with , . Median centering of is considerable, even in the most extreme setting with . Median bias reduction shows coverage of Wald-type confidence intervals closer to nominal values than bias reduction. Score-type intervals based on are slightly more accurate than Wald-type ones. As expected, the parameterization is more favourable than the parameterization for bias reduction.

| PU | MAE | B | RMSE | Wald | Score | |||

| 1 | 5 | 29.9 | 1.41 | 3.48 | 8.36 | 97.5 | 97.5 | |

| 40.9 | 1.22 | 2.31 | 6.51 | 95.2 | 95.1 | |||

| 41.0 | 1.22 | 2.30 | 6.51 | 95.1 | 95.0 | |||

| 73.4 | 1.27 | -0.04 | 2.99 | 76.1 | – | |||

| 56.5 | 1.22 | 1.06 | 4.68 | 84.3 | – | |||

| 50.1 | 1.19 | 1.51 | 5.29 | 89.2 | 94.9 | |||

| 10 | 35.7 | 0.85 | 1.03 | 2.36 | 97.1 | 97.1 | ||

| 44.3 | 0.80 | 0.68 | 2.03 | 95.6 | 95.5 | |||

| 44.3 | 0.80 | 0.68 | 2.03 | 95.5 | 95.5 | |||

| 64.5 | 0.85 | -0.03 | 1.48 | 85.6 | – | |||

| 54.7 | 0.80 | 0.31 | 1.73 | 91.2 | – | |||

| 50.5 | 0.79 | 0.45 | 1.83 | 92.8 | 95.3 | |||

| 50 | 5 | 1.2 | 0.62 | 0.64 | 0.72 | 40.5 | 40.5 | |

| 47.0 | 0.17 | 0.03 | 0.26 | 95.1 | 95.1 | |||

| 48.3 | 0.17 | 0.03 | 0.26 | 95.0 | 95.0 | |||

| 58.0 | 0.18 | -0.04 | 0.26 | 90.2 | – | |||

| 51.2 | 0.06 | 0.00 | 0.09 | 92.2 | – | |||

| 48.4 | 0.17 | 0.03 | 0.26 | 92.5 | 97.1 | |||

| 10 | 6.2 | 0.27 | 0.28 | 0.34 | 67.8 | 67.8 | ||

| 48.6 | 0.11 | 0.01 | 0.17 | 95.1 | 95.1 | |||

| 49.0 | 0.11 | 0.01 | 0.17 | 95.1 | 95.1 | |||

| 53.6 | 0.12 | -0.01 | 0.17 | 93.4 | – | |||

| 50.5 | 0.04 | 0.00 | 0.06 | 93.9 | – | |||

| 49.5 | 0.12 | 0.01 | 0.17 | 94.0 | 96.0 |

-

•

PU, percentage of underestimation; MAE, median absolute error; B, bias; RMSE, root mean squared error; Wald and Score, percentage coverage of 95% Wald-type and score-type confidence intervals.

Example 6. Common odds ratio in tables. Consider independent pairs of observations , realizations of independent binomial variables and . Let and . This model may arise in case-control studies, with 1 case and controls in each table, and where interest is about , representing the influence of some risk factor. As in Breslow (1981), we consider sparse settings with large and small , where improvements over the maximum likelihood estimator are particularly needed. This is also an instance where invariance is important, since results are often reported in terms of odds ratio . The median modified profile score is a special case of that in Example 2.2. The conditional maximum likelihood estimator is available, based on the conditional distribution of given , .

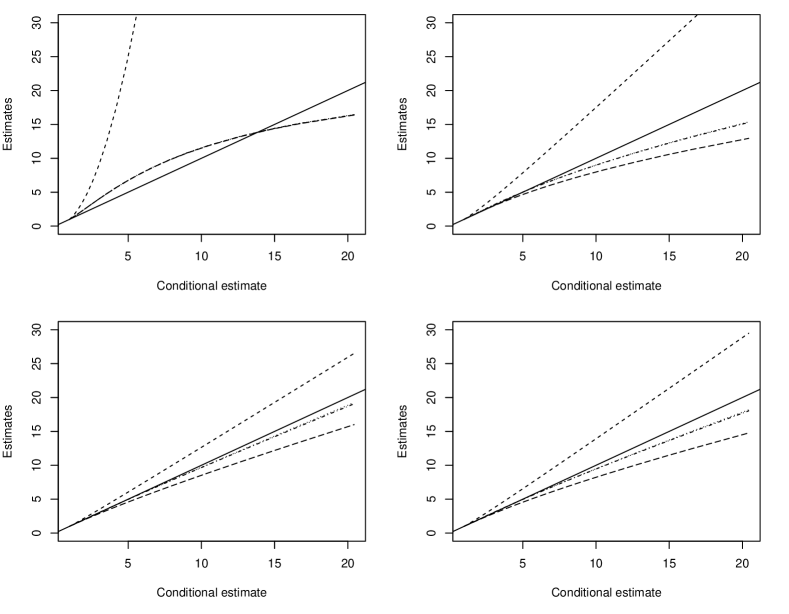

The aim is to compare the various methods with conditional maximum likelihood, which gives consistency also for fixed and can be considered as a gold standard. The comparison is made on the odds ratio scale, using for bias reduction and equivariance for the other estimators. As in Sartori (2003, Example 3), we focus on particular instances with odd values of and with , , so that all tables have the same number of successes and failures. In this case, and, for a given , both and are functions of only. Although and depend also on , numerical evidence indicates that such dependence vanishes as increases. For and various values of , estimates of the odds ratio are plotted versus in Figure 2. Median modified estimates are almost indistinguishable from those based on modified profile likelihood, as expected, and both are the closest to . On the contrary, markedly departs from , especially for small and as increases, while overcorrects, in particular for large values of . Other values of give the same results in terms of estimates, while accuracy of inference is affected since standard errors decrease as increases.

3 Median modified score for a vector parameter

For estimation of the full vector parameter , with , a direct extension of the rationale leading to (1) does not seem to be practicable due to lack of a manageable definition of multivariate median. Actually, a number of definitions have been proposed (Oja, 2013), but none seems suitable for developing a median modification of the score vector. For instance, with the simplest definition, i.e. taking the vector of approximate marginal medians as an approximate median of the score vector, dependence among score components is ignored. Other available definitions of multivariate median would involve the joint distribution of the score vector in a rather complex way and do not seem to provide feasible proposals.

Instead, the approach we follow is to set up a system of estimating equations giving, for each , , the same estimate as (8), up to terms of order included. This is obtained by defining the median modified score vector with components

| (9) |

where , and , , are as in (7) with . In (9), and in related formulae (7), indices take values in , and are summed when repeated. Moreover, all quantities involved are evaluated at , so that no constrained estimates are involved. Then, the joint estimate is defined as solution of .

For each , behaves tensorially under interest respecting reparameterizations of . As a consequence, is equivariant under joint reparameterizations that transform each component of separately.

Denoting by the vector with components given by the efficient scores , we can write , with a nonsingular and nonstochastic matrix of order . As shown in (16), . Moreover, , so that . Hence, solving is equivalent to solving

| (10) |

with having elements . There is no general guarantee that (10) has a solution. However, is of order , so that, asymptotically, existence of is guaranteed whenever exists. Moreover, and the asymptotic distribution of is the same as that of .

Let be the -th component of and the solution of , with given by (8). In a regular model, we show that

| (11) |

. A proof of (11) is given in the Appendix. A key property for the result is that is a diagonal matrix, so that satisfies

| (12) |

Following Jorgensen & Knudsen (2004), we call first-order insensitive to components other than , . Due to (12), terms up to order in the expansion of are not affected by terms of order in , .

Using delta method arguments as in Hall (1992, § 2.7), it follows from (11) that, in the continuous case, , so that componentwise median unbiasedness of with error of order follows from the analogous property of .

Equation (10) has the same structure as the estimating equation for bias reduction. Hence, some of the ideas in Kosmidis & Firth (2009, 2010) for the implementation of bias reduction can be adapted for median bias reduction. For instance, a modified Fisher scoring iteration can be written as

| (13) |

which differs from the analogue for only by the addition of the term . When available, is a convenient starting value. As happens for bias reduction (Kosmidis & Firth, 2010), convergence or otherwise of (13) depends on the properties of the specific assumed model. Nonetheless, assuming convergence of (13), it will be to a solution of (10).

Example 7. Binary regression (continued). Quantities needed for (9) in binary regression are the same as those in Example 2.2. Moreover, (13) simplifies to a modified iterative reweighted least squares procedure. Details are provided in the Supplementary Material and an implementation is given in the R package mbrglm (Kenne Pagui et al., 2017).

For the endometrial cancer grade dataset, estimates of the model parameters using (9) for logistic and probit regression are given in Table 4. The estimate is very close to obtained in Example 2.2 as a solution of (8).

| 4.305 (1.637) | -0.042 (0.044) | -2.903 (0.846) | ||

| 3.775 (1.489) | 2.929 (1.551) | -0.035 (0.040) | -2.604 (0.776) | |

| 3.969 (1.552) | 3.869 (2.298) | -0.039 (0.042) | -2.708 (0.803) | |

| 2.181 (0.857) | -0.019 (0.024) | -1.526 (0.433) | ||

| 1.915 (0.789) | 1.659 (0.747) | -0.015 (0.021) | -1.380 (0.403) | |

| 1.984 (0.812) | 1.971 (0.919) | -0.017 (0.022) | -1.425 (0.414) |

The same simulated samples as in Example 2.2 allow to evaluate the properties of estimators of the vector . Table 9 shows that the new method is remarkably accurate in achieving median centering for all the parameter components. It should be recalled that 684 samples out of 10,000 produced infinite maximum likelihood estimates, so that results for should be judged accordingly. The three approaches are comparable in terms of coverage of Wald-type confidence intervals, while profile score-type intervals show some improvement. Similar results have been found with a probit model and are reported in the Supplementary Material.

| PU | MAE | B | RMSE | Wald | Score | |

| 45.1 | 0.97 | 0.29 | 1.60 | 95.8 | 94.8 | |

| 43.0 | 0.66 | 0.12 | 0.90 | 97.4 | 95.2 | |

| 51.0 | 0.03 | 0.00 | 0.04 | 95.0 | 94.2 | |

| 56.0 | 0.57 | -0.26 | 1.02 | 96.0 | 94.9 | |

| 52.6 | 0.86 | 0.00 | 1.38 | 96.6 | – | |

| 53.0 | 0.56 | 0.02 | 0.90 | 97.4 | – | |

| 49.6 | 0.02 | 0.00 | 0.04 | 96.3 | – | |

| 44.4 | 0.52 | 0.01 | 0.83 | 94.8 | – | |

| 50.1 | 0.90 | 0.09 | 1.46 | 96.4 | 95.0 | |

| 49.7 | 0.59 | 0.15 | 1.07 | 97.5 | 95.3 | |

| 50.7 | 0.02 | 0.00 | 0.04 | 96.1 | 94.3 | |

| 49.6 | 0.52 | -0.10 | 0.89 | 95.8 | 94.7 |

-

•

PU, percentage of underestimation; MAE, median absolute error; B, bias; RMSE, root mean squared error; Wald and Score, percentage coverage of 95% Wald-type and score-type confidence intervals.

Example 8. Beta regression. Let , , be independent realizations of beta random variables with parameters and , i.e. with expected value and precision parameter . We assume a regression structure for the expected value , where , is a vector of covariates and is a given link function, such as the logit. The needed quantities for (9) with are the same as those required for bias reduction (Kosmidis & Firth, 2010). Details are given in the Supplementary Material. An R implementation of (13) is given in function mbrbetareg, available on GitHub.

As an application, we consider data in Griffiths et al. (1993, Table 15.4) on food expenditure for a random sample of 38 households in a large U.S. city, also available in the R package betareg. The objective is to model the proportion of income spent on food () as a function of income () and number of persons (). Estimates of , where is an intercept, and with the logit link are given in Table 6. Values for the regression coeffcients and corresponding standard errors are essentially the same for all methods, while differences are observed for the dispersion parameter.

| -0.623 (0.224) | -0.012 (0.003) | 0.118 (0.035) | 35.610 (8.080) | |

| -0.621 (0.239) | -0.012 (0.003) | 0.118 (0.038) | 30.922 (7.005) | |

| -0.621 (0.235) | -0.012 (0.003) | 0.118 (0.037) | 32.160 (7.289) |

We performed a simulation study with the same sample size and covariates as in the food expenditure data and with parameter fixed at . Results obtained from 100,000 simulated samples show identically accurate behaviour for estimators of regression parameters. Hence, only results for estimators of are displayed in Table 10, in line with those of previous examples. The complete table is reported in the Supplementary Material, together with an additional example with a smaller ratio leading to larger differences among estimators of . This also implies different confidence intervals for the regression coefficients and corresponding coverages.

| PU | MAE | B | RMSE | Wald | Score | |

| 32.7 | 6.25 | 5.46 | 11.79 | 95.1 | 95.1 | |

| 56.5 | 5.74 | 0.06 | 9.07 | 91.8 | – | |

| 49.8 | 5.69 | 1.49 | 9.56 | 93.7 | 95.8 |

-

•

PU, percentage of underestimation; MAE, median absolute error; B, bias; RMSE, root mean squared error; Wald and Score, percentage coverage of 95% Wald-type and score-type confidence intervals.

Appendix

Proof of (2). Let be the third standardized cumulant of , of order . Then, with a standard Edgeworth expansion,

where the error is of order because the term in the Edgeworth expansion is a linear combination with coefficients of order of odd Hermite polynomials evaluated at . The result in (2) follows using the expansions and .

Proof of (11). First, an expansion of is readily obtained from an expansion for (see e.g. Pace & Salvan, 1997, formula (9.61)), taking into account the effect of the modification to the profile score given in (8). In detail, being we get

| (14) |

Second, an expansion for from (9) is obtained using standard asymptotic expansions for estimating equations. Let be an estimating function with generic component . We assume that is of order with expected value . Let , and let , , , the latter two quantities being typically of order . Moreover, let , . Let be a generic entry of the inverse of the matrix with entries . An asymptotic expansion for gives

| (15) |

When , we obtain , so that expansion (15) gives the usual expansion for . The same is true if , being a linear transformation of . However, in the latter case, if , while . Indeed,

| (16) |

Since, when , we have , the indicator of , it follows that if . On the other hand, .

When (15) is applied to (9), we have and if . Therefore, terms up to order in the expansion for do not involve modification terms of order of with . The desired expansion for is thus equivalently obtained from the system

This is the same as the expansion from , plus a term given by the modification term in (9) divided by . Therefore, the resulting expansion coincides with (14).

References

- Agresti (2015) Agresti, A. (2015). Foundations of Linear and Generalized Linear Models. John Wiley & Sons.

- Barndorff-Nielsen (1983) Barndorff-Nielsen, O. E. (1983). On a formula for the distribution of the maximum likelihood estimator 70, 343–365.

- Barndorff-Nielsen (1986) Barndorff-Nielsen, O. E. (1986). Inference on full or partial parameters based on the standardized signed log likelihood ratio. Biometrika 73, 307–322.

- Barndorff-Nielsen & Cox (1989) Barndorff-Nielsen, O. E. & Cox, D. R. (1989). Asymptotic Techniques for Use in Statistics. Chapman & Hall.

- Biehler et al. (2015) Biehler, M., Holling, H. & Doebler, P. (2015). Saddlepoint approximations of the distribution of the person parameter in the two parameter logistic model. Psychometrika 80, 665–688.

- Breslow (1981) Breslow, N. (1981). Odds ratio estimators when the data are sparse. Biometrika 68, 73–84.

- Cai & Wang (2009) Cai, T. T. & Wang, H. (2009). Tolerance intervals for discrete distributions in exponential families. Statistica Sinica 19, 905–923.

- Cox & Hinkley (1974) Cox, D. R. & Hinkley, D. V. (1974). Theoretical Statistics. Chapman and Hall, London.

- DiCiccio et al. (1996) DiCiccio, T., Martin, M., Stern, S. & Young, G. (1996). Information bias and adjusted profile likelihoods. Journal of the Royal Statistical Society Series B 58, 189–203.

- Firth (1993) Firth, D. (1993). Bias reduction of maximum likelihood estimates. Biometrika 80, 27–38.

- Giummole & Ventura (2002) Giummole, F. & Ventura, L. (2002). Practical point estimation from higher-order pivots. Journal of Statistical Computation and Simulation 72, 419–430.

- Griffiths et al. (1993) Griffiths, W. E., Hill, R. C. & Judge, G. G. (1993). Learning and Practicing Econometrics. John Wiley & Sons.

- Hall (1992) Hall, P. (1992). The Bootstrap and Edgeworth Expansion. Springer, New York.

- Hirji et al. (1989) Hirji, K. F., Tsiatis, A. A. & Mehta, C. R. (1989). Median unbiased estimation for binary data. The American Statistician 43, 7–11.

- Jorgensen & Knudsen (2004) Jorgensen, B. & Knudsen, S. J. (2004). Parameter orthogonality and bias adjustment for estimating functions. Scandinavian Journal of Statistics 31, 93–114.

- Kenne Pagui et al. (2017) Kenne Pagui, E. C., Salvan, A. & Sartori, N. (2017). mbrglm: Median Bias Reduction in Binomial-Response GLMs. R package version 0.0.1.

- Kosmidis (2014) Kosmidis, I. (2014). Bias in parametric estimation: reduction and useful side-effects. Wiley Interdisciplinary Reviews: Computational Statistics 6, 185–196.

- Kosmidis & Firth (2009) Kosmidis, I. & Firth, D. (2009). Bias reduction in exponential family nonlinear models. Biometrika 96, 793–804.

- Kosmidis & Firth (2010) Kosmidis, I. & Firth, D. (2010). A generic algorithm for reducing bias in parametric estimation. Electronic Journal of Statistics 4, 1097–1112.

- Lehmann & Romano (2005) Lehmann, E. L. & Romano, J. P. (2005). Testing Statistical Hypotheses. Springer.

- McCullagh & Tibshirani (1990) McCullagh, P. & Tibshirani, R. (1990). A simple method for the adjustment of profile likelihoods. Journal of the Royal Statistical Society Series B 52, 325–344.

- Oja (2013) Oja, H. (2013). Multivariate median. In Robustness and Complex Data Structures, C. Becker, R. Fried & S. Kuhnt, eds. Springer, Berlin, pp. 3–15.

- Pace & Salvan (1992) Pace, L. & Salvan, A. (1992). A note on conditional cumulants in canonical exponential families. Scandinavian Journal of Statistics 19, 185–191.

- Pace & Salvan (1997) Pace, L. & Salvan, A. (1997). Principles of Statistical Inference from a Neo-Fisherian Perspective, vol. 4. World Scientific Pub Co Inc.

- Pace & Salvan (1999) Pace, L. & Salvan, A. (1999). Point estimation based on confidence intervals: exponential families. Journal of Statistical Computation and Simulation 64, 1–21.

- Read (1985) Read, C. B. (1985). Median unbiased estimators. In Encyclopedia of Statistical Sciences, S. Kotz, N. Johnson & C. Read, eds., vol. 5. Wiley, New York, pp. 424–426.

- Sartori (2003) Sartori, N. (2003). Modified profile likelihoods in models with stratum nuisance parameters. Biometrika 90, 533–549.

- Sartori (2006) Sartori, N. (2006). Bias prevention of maximum likelihood estimates for scalar skew normal and skew t distributions. Journal of Statistical Planning and Inference 136, 4259–4275.

- Stern (1997) Stern, S. E. (1997). A second-order adjustment to the profile likelihood in the case of a multidimensional parameter of interest. Journal of the Royal Statistical Society Series B 59, 653–665.

Supplementary material

Supplementary material includes some discussion on the discrete case and details and quantities for the implementation of the method, together with additional simulation results for Examples 4, 7 and 8.

Appendix A Comparison with exact median unbiased estimator in simple binomial regression models

Consider first a simple binomial regression model with realizations of independent random variables, with , , with covariate values , generated from a standard normal distribution. The sufficient statistic is and takes distinct values.

We compare the maximum likelihood estimator, , which amounts to considering only the leading term of the Cornish-Fisher expansion for the median of , and the median bias reduced estimator, , with the exact median unbiased estimator, , for increasing values of . All three estimators vary monotonically with and the latter estimator (see, for instance, Hirji et al., 1989) is defined as , where and are such that

When is equal to either the maximum or the minimum of its possibile values, then only one of or is defined. In such case, is taken to be or , whichever exists. This estimator satisfies

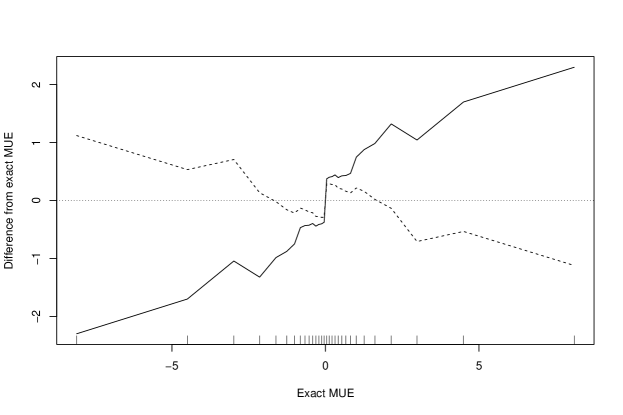

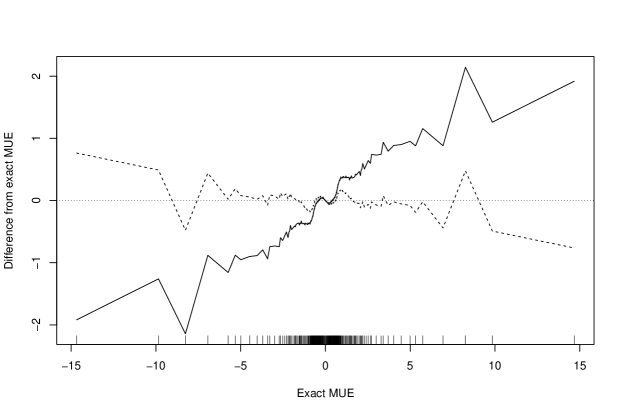

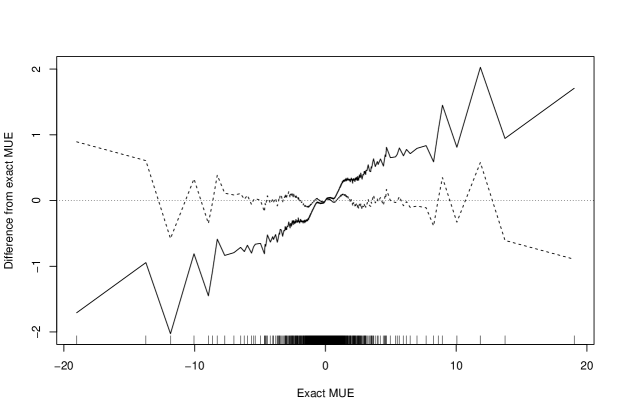

For , takes respectively , and distinct values. Figure 3 shows the differences and as functions of in the three situations. We note that the two points corresponding to the minimum and maximum values of are not reported since is respectively or . The proposed estimator is closer to than in all three situations, with relative differences getting smaller as the number of points in the sample space increases.

As an example with , consider the hypothetical clinical trial data in Hirji et al. (1989, Table 2) with patients belonging to two age groups (age less or equal than 30 years, and age greater than 30 years) of size 20 and 10, respectively. Each group is randomized to receive one of two treatments, with 9 and 6 patients receiving the first treatment in the first and second age group, respectively. Let be the binary disease outcome ( for a positive outcome, otherwise). Moreover, let be a binary age indicator ( if age is less or equal to 30 years, if age is greater than 30 years) and be a binary treatment indicator ( for the first treatment, for the second treatment), . Then, with the probability of a positive outcome, a logistic model relating the response of the -th patient to treatment and age can be written as

Here is the relative log odds of response for treatment 1 versus treatment 2, and can be considered as the parameter of interest. The exact conditional median unbiased estimator (Hirji et al., 1989) can be obtained using the definition above, applied to the conditional distribution of given . As in Hirji et al. (1989, Table 2), we compare in Table 8 , and , for all possible values of in the conditional distribution of given . Estimate is the third component of the joint bias reduced estimate , as in Example 7, and it is third order equivalent to , from (8). The bias reduced estimator is uniformly closer to the exact conditional median unbiased estimator than the maximum likelihood estimate.

| 1 | -4.489 | -6.077 | |

|---|---|---|---|

| 2 | -3.885 | -3.909 | -4.537 |

| 3 | -2.876 | -2.900 | -3.239 |

| 4 | -2.141 | -2.150 | -2.361 |

| 5 | -1.517 | -1.520 | -1.654 |

| 6 | -0.953 | -0.955 | -1.032 |

| 7 | -0.421 | -0.421 | -0.453 |

| 8 | 0.104 | 0.103 | 0.114 |

| 9 | 0.641 | 0.640 | 0.695 |

| 10 | 1.220 | 1.217 | 1.325 |

| 11 | 1.899 | 1.885 | 2.068 |

| 12 | 2.851 | 2.778 | 3.103 |

| 13 | 3.430 | 4.966 |

Appendix B Binary regression

We give details on the computation of the needed quantities for (8) and (9), used in Examples 4 and 7 of the paper, respectively. We assume , , as independent realizations of binary random variables with probability , where , is a row vector of covariates, and is a known cumulative distribution function. Below, indices , , and refer to the components of . We have

with

where and are first and second derivatives of . If is the logistic cumulative distribution function, and .

Ingredients of Fisher scoring equation (13) may be written in matrix form as and , where is the design matrix with entries , is a diagonal matrix with diagonal elements , and is a vector with elements , . Hence, (13) becomes

where the adjusted response variable includes the modification term .

Simulation results for Example 7 with probit link are in Table 9.

| PU | MAE | B | RMSE | Wald | Score | |

| 43.1 | 0.57 | 0.21 | 0.96 | 95.3 | 95.3 | |

| 43.4 | 0.38 | 0.44 | 1.55 | 97.1 | 95.0 | |

| 50.5 | 0.01 | -0.00 | 0.02 | 94.1 | 94.2 | |

| 58.1 | 0.33 | -0.18 | 0.61 | 95.5 | 95.4 | |

| 52.8 | 0.51 | -0.01 | 0.80 | 95.90 | – | |

| 51.7 | 0.33 | 0.01 | 0.52 | 97.10 | – | |

| 49.2 | 0.01 | -0.00 | 0.02 | 96.40 | – | |

| 45.0 | 0.30 | 0.01 | 0.48 | 94.50 | – | |

| 50.5 | 0.53 | 0.05 | 0.85 | 96.1 | 95.2 | |

| 49.3 | 0.34 | 0.06 | 0.58 | 97.0 | 94.9 | |

| 50.1 | 0.01 | -0.00 | 0.02 | 96.0 | 94.2 | |

| 49.8 | 0.31 | -0.06 | 0.51 | 95.6 | 95.0 |

-

•

PU, percentage of underestimation; MAE, median absolute error; B, bias; RMSE, root mean squared error; Wald and Score, percentage coverage of 95% Wald-type and Score-type confidence intervals.

Appendix C Beta regression

We give quantities for computing (9) in Example 8 of the paper. Let , , be independent realizations of beta random variables with parameters and , i.e. with expected value and precision parameter . We assume a regression structure for the expected value , where , is a row vector of covariates and is a given link function, such as the logit. We denote by the full vector of parameters. The log-likelihood has the form

where and .

Let and , with the polygamma function of order , . The needed quantities for (9) are

An R implementation of the method, using formula (13) of the paper, is given in function mbrbetareg available

at https://github.com/eulogepagui/mbrbetareg.

Complete simulation results for Example 8 are in Table 10.

| PU | MAE | B | RMSE | Wald | Score | |

| 50.0 | 0.15 | 0.00 | 0.22 | 93.1 | 94.3 | |

| 50.6 | 0.00 | 0.00 | 0.00 | 93.5 | 94.8 | |

| 50.5 | 0.02 | 0.00 | 0.04 | 93.2 | 94.5 | |

| 32.7 | 6.25 | 5.46 | 11.79 | 95.1 | 95.1 | |

| 49.8 | 0.15 | 0.00 | 0.22 | 94.7 | – | |

| 50.2 | 0.00 | 0.00 | 0.00 | 95.2 | – | |

| 50.9 | 0.02 | 0.00 | 0.04 | 94.9 | – | |

| 56.5 | 5.74 | 0.06 | 9.07 | 91.8 | – | |

| 49.9 | 0.15 | 0.00 | 0.22 | 94.3 | 94.4 | |

| 50.3 | 0.00 | 0.00 | 0.00 | 94.8 | 94.8 | |

| 50.8 | 0.02 | 0.00 | 0.04 | 94.5 | 94.5 | |

| 49.8 | 5.69 | 1.49 | 9.56 | 93.7 | 95.8 |

-

•

PU, percentage of underestimation; MAE, median absolute error; B, bias; RMSE, root mean squared error; Wald and Score, percentage coverage of 95% Wald-type and score-type confidence intervals.

As a further example, we consider the gasoline yield data as in Kosmidis & Firth (2010, Section 4.3). Here and the response variable is the proportion of crude oil converted to gasoline after distillation and fractionation. Covariates are 9 indicators representing the 10 distinct experimental settings in the data and the temperature in degrees Fahrenheit at which all gasoline has vaporized. Estimates of , where is an intercept, are the coefficients of the 9 indicators, is the coefficient of the temperature, and with the logit link are given in Table 11. Values for the regression coefficients are essentially the same for all methods, while notable differences are observed for the dispersion parameter. These in turn influence estimates of standard errors for the regression coefficients.

We performed a simulation study with the same sample size and covariates as in the gasoline yield data and with parameter fixed at . Results obtained from 100,000 simulated samples in Table 12 show marked differences among estimators of , with achieving median centering. These differences also imply different coverages of confidence intervals for the regression coefficients. In this rather extreme case score-type confidence intervals are numerically very unstable and only results for Wald-type intervals are reported.

| -6.160 (0.182) | -6.142 (0.236) | -6.144 (0.228) | |

| 1.728 (0.101) | 1.723 (0.131) | 1.724 (0.127) | |

| 1.323 (0.118) | 1.319 (0.153) | 1.319 (0.148) | |

| 1.572 (0.116) | 1.567 (0.150) | 1.568 (0.145) | |

| 1.060 (0.102) | 1.057 (0.132) | 1.058 (0.128) | |

| 1.134 (0.104) | 1.130 (0.134) | 1.131 (0.130) | |

| 1.040 (0.106) | 1.037 (0.137) | 1.038 (0.133) | |

| 0.544 (0.109) | 0.542 (0.141) | 0.543 (0.137) | |

| 0.496 (0.109) | 0.494 (0.141) | 0.495 (0.136) | |

| 0.386 (0.119) | 0.385 (0.154) | 0.385 (0.148) | |

| 0.011 (0.000) | 0.011 (0.001) | 0.011 (0.001) | |

| 440.278 (110.026) | 261.038 (65.216) | 279.409 (69.809) |

| PU | MAE | B | RMSE | Wald | |

| 52.63 | 0.124 | -0.015 | 0.183 | 86.82 | |

| 48.67 | 0.068 | 0.004 | 0.102 | 86.86 | |

| 48.14 | 0.081 | 0.005 | 0.119 | 86.95 | |

| 48.75 | 0.078 | 0.004 | 0.116 | 87.19 | |

| 49.18 | 0.070 | 0.002 | 0.103 | 87.12 | |

| 49.55 | 0.070 | 0.002 | 0.103 | 87.70 | |

| 49.10 | 0.071 | 0.003 | 0.107 | 87.20 | |

| 49.84 | 0.073 | 0.001 | 0.109 | 87.29 | |

| 49.69 | 0.074 | 0.002 | 0.110 | 86.57 | |

| 49.60 | 0.081 | 0.002 | 0.118 | 87.23 | |

| 47.51 | 0.000 | 0.000 | 0.000 | 87.14 | |

| 5.65 | 254.489 | 302.277 | 395.193 | 74.92 | |

| 50.00 | 0.125 | -0.002 | 0.182 | 94.76 | |

| 49.95 | 0.069 | 0.001 | 0.102 | 94.69 | |

| 49.16 | 0.081 | 0.002 | 0.119 | 94.32 | |

| 49.81 | 0.078 | 0.000 | 0.116 | 94.86 | |

| 50.06 | 0.069 | 0.000 | 0.102 | 94.73 | |

| 50.44 | 0.070 | 0.000 | 0.103 | 94.95 | |

| 49.82 | 0.071 | 0.001 | 0.106 | 94.42 | |

| 50.02 | 0.073 | 0.000 | 0.109 | 94.45 | |

| 49.96 | 0.074 | 0.001 | 0.110 | 94.57 | |

| 49.81 | 0.081 | 0.001 | 0.118 | 94.97 | |

| 49.82 | 0.000 | 0.000 | 0.000 | 94.67 | |

| 58.12 | 93.669 | 0.209 | 151.152 | 84.83 | |

| 50.30 | 0.125 | -0.004 | 0.182 | 93.83 | |

| 49.67 | 0.069 | 0.002 | 0.102 | 93.97 | |

| 49.08 | 0.081 | 0.002 | 0.119 | 93.60 | |

| 49.67 | 0.078 | 0.001 | 0.116 | 94.04 | |

| 49.83 | 0.069 | 0.001 | 0.102 | 93.98 | |

| 50.25 | 0.070 | 0.000 | 0.103 | 94.24 | |

| 49.64 | 0.071 | 0.001 | 0.106 | 93.67 | |

| 49.95 | 0.073 | 0.001 | 0.109 | 93.68 | |

| 49.88 | 0.074 | 0.001 | 0.110 | 93.90 | |

| 49.81 | 0.081 | 0.001 | 0.118 | 94.29 | |

| 49.51 | 0.000 | 0.000 | 0.000 | 94.02 | |

| 49.76 | 92.138 | 31.176 | 164.736 | 88.72 |

-

•

PU, percentage of underestimation; MAE, median absolute error; B, bias; RMSE, root mean squared error; Wald, percentage coverage of 95% Wald-type confidence intervals.