Representing sparse Gaussian DAGs as sparse R-vines allowing for non-Gaussian dependence

Abstract

Modeling dependence in high dimensional systems has become an increasingly important topic. Most approaches rely on the assumption of a multivariate Gaussian distribution such as statistical models on directed acyclic graphs (DAGs). They are based on modeling conditional independencies and are scalable to high dimensions. In contrast, vine copula models accommodate more elaborate features like tail dependence and asymmetry, as well as independent modeling of the marginals. This flexibility comes however at the cost of exponentially increasing complexity for model selection and estimation. We show a novel connection between DAGs with limited number of parents and truncated vine copulas under sufficient conditions. This motivates a more general procedure exploiting the fast model selection and estimation of sparse DAGs while allowing for non-Gaussian dependence using vine copulas. We demonstrate in a simulation study and using a high dimensional data application that our approach outperforms standard methods for vine structure estimation.

Keywords: Graphical Model, Dependence Modeling, Vine Copula, Directed Acyclic Graph

1 Introduction

In many areas of natural and social sciences, high dimensional data are collected for analysis. For all these data sets the dependence between the variables in addition to the marginal behaviour needs to be taken into account. While there exist many easily applicable univariate models, dependence models in dimensions often come with high complexity. Additionally, they put restrictions on the associated marginal distributions, such as the multivariate Student-t and Gaussian distribution. The latter is also the backbone of statistical models on directed acyclic graphs (DAGs) or Bayesian Networks (BNs), see Lauritzen (1996) and Koller and

Friedman (2009). Based on the Theorem of Sklar (1959), the pair copula construction (PCC) of Aas

et al. (2009) allows for more flexible dimensional models. More precisely, the building blocks are the marginal distributions and (conditional) bivariate copulas which can be chosen independently. The resulting models, called regular vines or R-vines (Kurowicka and

Joe, 2011) are specified by a sequence of linked trees, the R-vine structure. The edges of the trees are associated with bivariate parametric copulas. When the trees are specified by star structures we speak of C-vines, while line structures give rise to D-vines. However, parameter estimation and model selection for R-vine models can be cumbersome, see Czado (2010) and Czado

et al. (2013). In particular, the sequential approach of Dißmann et al. (2013) builds the R-vine structure from the first tree to the higher trees. Since choices in lower trees put restrictions on higher trees, the resulting model might not be overall optimal in terms of goodness-of-fit. Thus, Dißmann et al. (2013)

model the stronger (conditional) pairwise dependencies in lower trees compared to weaker ones. To reduce model complexity, pair copulas in the trees to can be set to the independence copula resulting in -truncated R-vines (Brechmann and

Czado, 2013). Another sequential model selection approach is the Bayesian approach of Gruber and

Czado (2015a), while

Gruber and

Czado (2015b) contains a full Bayesian analysis. Both methods are computationally demanding and thus not scalable to high dimensions.

Since DAGs are scalable to high dimensions, attempts were made to relate DAGs to R-vines. For example, Bauer

et al. (2012) and Bauer and

Czado (2016) provide a PCC to the density factorization of a DAG. While this approach maintains the structure of the DAG, some of the conditional distribution functions in the PCC can not be calculated recursively and thus require high dimensional integration. This limits the applicability in high dimensions dramatically. Pircalabelu et al. (2015) approximate each term in the DAG density factorization by a quotient of a C-vine and a D-vine. However, this yields in general no consistent joint distribution. Finally, Elidan (2010) uses copulas to generalize the density factorization of a DAG to non-Gaussian dependence by exchanging conditional normal densities with copula densities. Yet, the dimension of these copulas is not bounded, inheriting the drawbacks of higher dimensional copula models, i. e. lack of flexibility and high computational effort.

Our goal is to ultimately use the multitude of fast algorithms for estimating sparse Gaussian DAGs in high dimensions to efficiently calculate sparse R-vines. Thus, once a DAG has been selected, we compute an R-vine which represents a similar decomposition of the density as the DAG. This new decomposition allows us to replace Gaussian copula densities and marginals by non-Gaussian pair copula families and arbitrary marginals. We attain this without the drawback of possible higher-dimensional integration as in the approach of Bauer and

Czado (2016). However, we still exploit conditional independences described by the DAG facilitating parsimony of the R-vine. To attain this, we first build a theoretically sound bridge between DAG with at most parents, called -DAGs and -truncated R-vines. Since the class of -truncated R-vines is much smaller than the class of -DAGs, such an appealing exact representation will not exist for most DAGs. Yet, we can prove under sufficient conditions when it does and determine special classes of -DAGs which have expressions as -truncated C- and D-vines. Next, we give strong necessary conditions on arbitrary -DAGs to check whether an exact representation as -truncated R-vine exists. If not, we obtain a smallest possible truncation level . All the previous results motivate a more general procedure to find sparse R-vines based on -DAGs, attaining our final goal, to find a novel approach to estimate high dimensional sparse R-vines. The presented method is also independent of the sequential estimation of pair copula families and parameters as used by Dißmann et al. (2013). Thus, error propagation in later steps caused by misspecification in early steps is prevented. By allowing the underlying DAG model to have at most parents, we control for a specific degree of sparsity.

The paper is organized as follows: Sections 2 and 3 introduce R-vines and DAGs, respectively. Section 4 contains the main result where we first demonstrate that each (truncated) R-vine can be represented by a DAG non-uniquely. The converse also holds true for -DAGs, i. e. Markov trees. We prove a representation of DAGs as R-vines under sufficient conditions and propose necessary conditions. Afterwards, we develop a general procedure to compute sparse R-vines representing -DAGs. There, we propose a novel technique combining several DAGs. In Section 5, a high dimensional simulation study shows the efficiency of our approach. We conclude with a high dimensional data application in Section 6 and summarize our contribution. Additional results are contained in an online supplement.

2 Dependence Modeling with R-vines

Consider a random vector with joint density function and joint distribution function . The famous Theorem of Sklar (1959) allows to separate the univariate marginal distribution functions from the dependency structure such that , where is an appropriate -dimensional copula. For continuous , is unique. The corresponding joint density function is given as

| (2.1) |

where is a -dimensional copula density. This representation relies on an appropriate -dimensional copula, which might be cumbersome and analytically not tractable. As shown by Aas et al. (2009), -dimensional copula densities may be decomposed into bivariate (conditional) copula densities. Its backbone, the pair copulas can flexibly represent important features like positive or negative tail dependence or asymmetric dependence. The pair-copula-construction (PCC) in dimensions itself is not unique. However, the different possible decompositions may be organized to represent a valid joint density using regular vines (R-vines), see Bedford and Cooke (2001) and Bedford and Cooke (2002). To construct a statistical model, a vine tree sequence stores which bivariate (conditional) copula densities are present in the presentation of a -dimensional copula density. More precisely, such a sequence in dimensions is defined by such that

-

(i)

is a tree with nodes and edges ,

-

(ii)

for , is a tree with nodes and edges ,

-

(iii)

if two nodes in are joined by an edge, the corresponding edges in must share a common node (proximity condition).

Since edges in a tree become nodes in , denoting edges in higher order trees is complex. For example, edges are nodes in and an edge in between these nodes is denoted . To shorten this set formalism, we introduce the following. For a node we call a node an m-child of if is an element of . If is reachable via inclusions , we say is an m-descendant of . We define the complete union of an edge by where the conditioning set of an edge is defined as and is the conditioned set. Since and are singletons, is a doubleton for each , see Kurowicka and Cooke (2006, p. 96). For edges , we define the set of bivariate copula densities corresponding to by with the conditioned set and the conditioning set . Denote sub vectors of by . With the PCC, Equation (2.1) becomes

| (2.2) |

By referring to bivariate conditional copulas, we implicitly take into account the simplifying assumption, which states that the two-dimensional conditional copula density is independent of the conditioning value , see Stöber et al. (2013) for a detailed discussion. Henceforth, in our considerations we assume the simplifying assumption. We define the parameters of the bivariate copula densities by . This determines the R-vine copula . A convenient way to represent R-vines uses lower triangular matrices, see Dißmann et al. (2013).

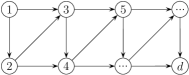

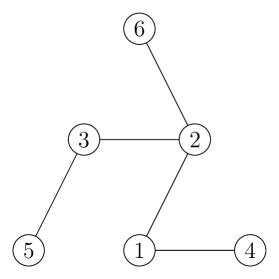

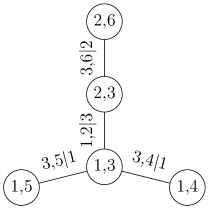

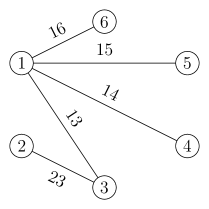

Example 2.1 (R-vine in 6 dimensions).

The R-vine tree sequence in Figure 1 is given by the R-vine matrix as follows. Edges in are pairs of the main diagonal and the lowest row, e. g. , , , etc. is described by the main diagonal and the second last row conditioned on the last row, e. g. ; , etc. Higher order trees are characterized similarly. For a column in , only entries of the main-diagonal right of , i. e. values in are allowed and no entry must occur more than once in a column.

R-vine matrix

![[Uncaptioned image]](/html/1604.04202/assets/x1.png)

![[Uncaptioned image]](/html/1604.04202/assets/x2.png)

![[Uncaptioned image]](/html/1604.04202/assets/x3.png)

![[Uncaptioned image]](/html/1604.04202/assets/x4.png)

![[Uncaptioned image]](/html/1604.04202/assets/x5.png) Figure 1: R-vine trees (top), (bottom), left to right.

Figure 1: R-vine trees (top), (bottom), left to right.

See Table 1 for a non exhaustive list of m-children and m-descendants of edges in the R-vine trees . For the complete list, see Appendix B, Example B.1.

With , , , the density becomes

As we model edges, the model complexity is increasing quadratically in . We can ease this by only modeling the first trees and assuming (conditional) independence for the remaining trees. Thus, the model complexity increases linearly. This truncation is discussed in detail by Brechmann and Czado (2013). Generally, for , a -truncated R-vine is an R-vine where each pair copula density assigned to an edge is represented by the independence copula density . In a -truncated R-vine, Equation (2.2) becomes

In Example 2.1, we obtain a -truncated R-vine by setting whenever . The most complex part of estimating an R-vine copula is the structure selection. To solve this, Dißmann et al. (2013) suggest to calculate a maximum spanning tree with edge weights set to absolute values of empirical Kendall’s . The intuition is to model strongest dependence in the first R-vine trees. After selecting the first tree, pair copulas and parameters are chosen by maximum likelihood estimation for each edge. Based on the estimates, pseudo-observations are derived from the selected pair-copulas. Kendall’s is estimated for these pseudo-observations to find a maximum spanning tree by taking into account the proximity condition. Thus, higher order trees are dependent on the structure, pair copulas and parameters of lower order trees. Hence, this sequential greedy approach is not guaranteed to lead to optimal results in terms of e. g. log-likelihood, AIC or BIC. Gruber and Czado (2015b) developed a Bayesian approach which allows for simultaneous selection of R-vine structure, copula family and parameters to overcome the disadvantages of sequential selection. However, this approach comes at the cost of higher computational effort and is not feasible in high dimensional set-ups, i. e. for more than ten dimensions.

3 Graphical models

3.1 Graph theory

We introduce necessary graph theory from Lauritzen (1996, pp. 4–7). A comprehensive list with examples is given in Appendix A. Let be a finite set, the node set and let be the edge set. We define a graph as a pair of node set and edge set. An edge is undirected if , and is directed if . A directed edge is called an arrow and denoted with the tail and the head. The existence of a directed edge between and without specifying the orientation is denoted by and no directed edge between and regardless of orientation is denoted by . If a graph only contains undirected edges, it is an undirected graph and if it contains only directed edges, it is a directed graph. We will not consider graphs with both directed and undirected edges. A weighted graph is a graph with weight function such that . By replacing all arrows in a directed graph by undirected edges, we obtain the skeleton of . Let be a graph and define a path of length from nodes to by a sequence of distinct nodes such that for . This applies to both undirected and directed graphs. A cycle is defined as path with . A graph without cycles is called acyclic. In a directed graph, a chain of length from to is a sequence of distinct nodes with or for . Thus, a directed graph may contain a chain from to but no path from to . A graph is a subgraph of if and . We speak of an induced subgraph if and , i. e. contains a subset of nodes of and all the edges of between these nodes. If is undirected and a path from to exists for all , we say that is connected. If is directed we say that is weakly connected if a path from to exists for all in the skeleton of . If an undirected graph is connected and acyclic, it is a tree and has edges on nodes. For undirected, , a set is said to be an separator in if all paths from to intersect . is said to separate from if it is an separator for every , .

3.2 Directed acyclic graphs (DAGs)

Let be a directed acyclic graph (DAG). If there exists a path from to , we write . Denote a disjoint union by , and define the parents , ancestors , descendants and non-descendants . We see for all . is ancestral if for all , with the smallest ancestral set containing . Let for all . A DAG with at most parents is called -DAG. For each DAG there exists a topological ordering, see Andersson and Perlman (1998). This is formalized by an ordering function . Let and such that for each pair we have , i. e. there is no path from to in . An ordering always exists, but is not necessarily unique. By , we refer to ordered increasingly according to and by we refer ordered decreasingly according to . A v-structure in is a triple of nodes where and but . The moral graph of a DAG is the skeleton of with an additional undirected edge for each v-structure . As for undirected graphs, separation can also be defined for DAGs, called d-separation. Let be an DAG. A chain from to in is blocked by a set of nodes , if it contains a node such that either

-

(i)

and arrows of do not meet head-to-head at (i. e. at there is no v-structure with nodes of ), or

-

(ii)

nor has any descendants in , and arrows of do meet head-to-head at (i. e. at there is a v-structure with nodes of ).

A chain that is not blocked by is active. Two subsets and are d-separated by if all chains from to are blocked by .

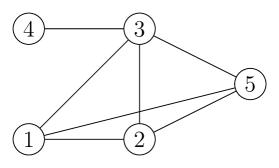

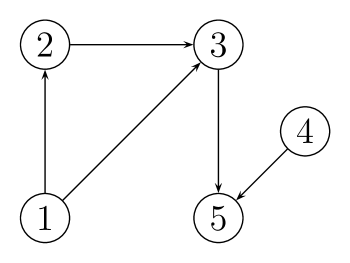

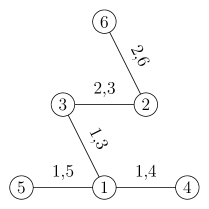

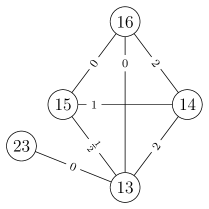

Example 3.1 (DAG in 6 dimensions).

Table 2 displays the topological ordering function, parents, descendants and non-descendants for all of the DAG in Figure 2.

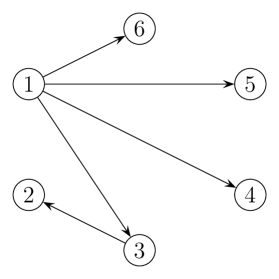

![[Uncaptioned image]](/html/1604.04202/assets/x6.png) Figure 2: DAG

1

1

-

2,3,4,5,6

-

2

2

1

3,4,5,6

-

3

4

6,2

-

1,4,5

4

6

5,2

-

1,3,6

5

5

6,2

4

1,3

6

3

2

3,4,5

1

Table 2: Properties of DAG .

Figure 2: DAG

1

1

-

2,3,4,5,6

-

2

2

1

3,4,5,6

-

3

4

6,2

-

1,4,5

4

6

5,2

-

1,3,6

5

5

6,2

4

1,3

6

3

2

3,4,5

1

Table 2: Properties of DAG .

A high value of corresponds to more non-descendants. is not unique since in . Hence, a topological ordering for is also .

3.3 Markov properties on graphs

Let and consider a random value distributed according to a probability measure . For define and denote the conditional independence of the random vectors and given by . Let be a DAG, then obeys the local directed Markov property according to if

| (3.1) |

Example 3.2 (Example 3.1 cont.).

From Lauritzen (1996, p. 51), has the local directed Markov property according to if and only if it has the global directed Markov property according to , which states that for we have that Thus, inferring conditional independences using this property requires undirected graphs. To use directed graphs, we can employ the d-separation. Lauritzen (1996, p. 48) showed that for a DAG and disjoint sets, d-separates from in if and only if separates from in . The conditional independences drawn from a DAG can be exploited using the following Proposition, see Whittaker (1990, p. 33).

Proposition 3.3 (Conditional independence).

If is a partitioned random vector with joint density , then the following expressions are equivalent:

-

(i)

,

-

(ii)

and .

To estimate DAGs, a specific distribution is assumed. For continuous data, it is most often the multivariate Gaussian. There exists a multitude of algorithms, see Scutari (2010), which are applicable also in high dimensions. While we are aware that assuming Gaussianity might be too restrictive for describing the data adequately, we consider the estimated DAG as proxy for an R-vine. An R-vine is however not restricted to Gaussian pair copulas or marginals, relaxing the severe restrictions which come along with DAG models.

4 Representing DAGs as R-vines

First, we show that each Gaussian R-vine has a representation as a Gaussian DAG. Second, we demonstrate that the converse also holds for the case of -DAGs, i. e. Markov-trees. For the case , a representation of -DAGs as -truncated R-vines is not necessarily possible. We prove under sufficient conditions when such a representation exists. Finally, we derive necessary conditions to infer if an R-vine representation of a -DAG is possible and which truncation level can be attained at best.

4.1 Representing truncated R-vines as DAGs

To establish a connection between -truncated Gaussian R-vines and DAGs, we follow Brechmann and Joe (2014) using structural equation models (SEMs). Define a SEM corresponding to a Gaussian R-vine with structure , denoted by . Let be an R-vine tree sequence and assume without loss of generality and for denote the edges in by . The higher order trees contain edges for . Based on this R-vine, define by

| (4.1) | ||||

with i.i.d. and such that for . From we obtain a graph and add a directed edge for each and . In other words, each conditioned set of the R-vine yields an arrow. By the structure of , is a DAG. By Peters and Bühlmann (2014), the joint distribution of is uniquely determined by and it is Markov with respect to . Additionally, if the R-vine is -truncated, we have at most summands on the right hand side and thus, obtain a -DAG. Furthermore, has a topological ordering . We show that it is possible for two different R-vines to have the same DAG representation.

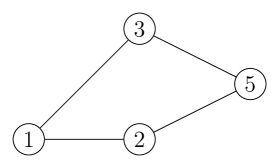

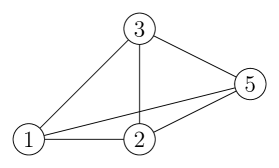

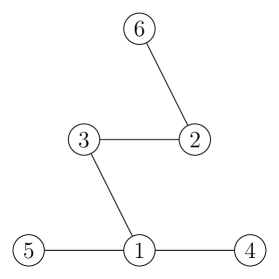

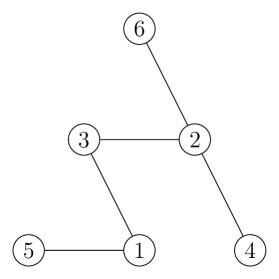

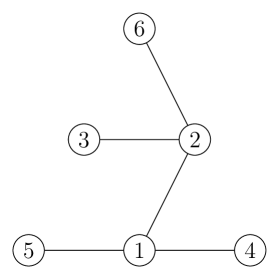

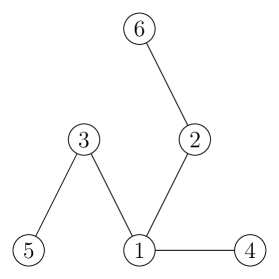

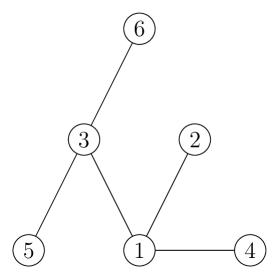

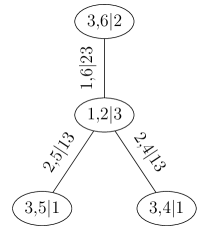

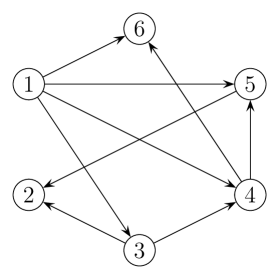

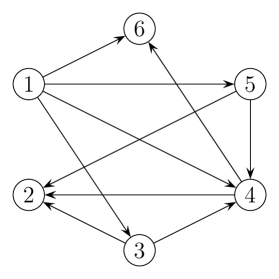

Example 4.1 (Different -truncated R-vines with same DAG representation in dimensions).

Consider the following two -truncated R-vines and their -DAG representation.

![[Uncaptioned image]](/html/1604.04202/assets/x7.png)

![[Uncaptioned image]](/html/1604.04202/assets/x8.png) Figure 3: R-vine .

Figure 3: R-vine .

![[Uncaptioned image]](/html/1604.04202/assets/x9.png)

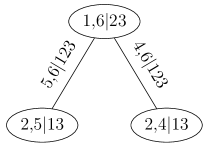

![[Uncaptioned image]](/html/1604.04202/assets/x10.png) Figure 4: R-vine .

Figure 4: R-vine .

![[Uncaptioned image]](/html/1604.04202/assets/x11.png) Figure 5: DAG of , .

Figure 5: DAG of , .

Since the conditioned sets of and in their first two trees are the same, both R-vines have the same DAG representation . Assuming fixed SEM coefficients , both R-vines also have different correlation matrices. Yet, both correlation matrices are belonging to distributions which are Markov with respect to .

Since two R-vines may have the same representing DAG, inferring an R-vine from a DAG uniquely is not necessarily possible. We formalize an R-vine representation of a DAG.

Definition 4.2 (R-vine representation of DAG).

Let be a -DAG. A -truncated R-vine representation of is an R-vine tree sequence such that contain edges where by .

We first consider the case of representing Markov-Trees, i. e. -DAGs. Afterwards, the representation of general -DAGs for is evaluated.

4.2 Representing Markov Trees as 1-truncated R-vines

Proposition 4.3 (Representing Markov Trees).

Let be a -DAG. There exists a -truncated R-vine representation of . If , .

4.3 Representing -DAGs as -truncated R-vines under sufficient conditions

First, we introduce the assumptions of our main theorem and their interpretation. Next, the proof follows with some illustrations. Let be an arbitrary -DAG. We impose under which assumptions an incomplete R-vine tree sequence is part of a -truncated R-vine representation of .

A1.

For all with , there exists an and such that . Here, is specified by the DAG .

A2.

The main diagonal of the R-vine matrix of can be written as decreasing topological ordering of the DAG , from the top left to bottom right.

Example 4.4 (Example 3.1 cont.).

A1 links each conditioned set in an edge in one of the first R-vine trees to an arrow in the DAG . We have seen this property in the representation of R-vines as DAGs in Section 4.1. Note that in a (not truncated) R-vine, each pair occurs exactly once as conditioned set, see Kurowicka and Cooke (2006, p. 96). A2 maps the topological ordering of onto the conditioned sets of the R-vine tree such that

| (4.2) |

This can be seen as for a column , the elements must occur as a diagonal element to the right of , i. e. as diagonal entries in a column . By definition of topological orderings, we obtain (4.2). To interpret A2, recall that in a DAG we have . For higher R-vine trees we want to truncate, A1 assures that all parents are in the conditioning set for these trees. A2 gives us that only pairs of for are in the conditioned sets in these trees. This holds true since the later a node occurs in the topological ordering, the more non-descendants it has. Thus, A2 maps the structure of DAG and the R-vine .

Theorem 4.5 (Representing DAGs as truncated R-vines).

Let be a -DAG. If there exists an incomplete R-vine tree sequence such that A1 and A2 hold, then can be completed with trees which only contain independence copulas. In particular, these independence pair copulas encode conditional independences derived from the -DAG by the local directed Markov property.

The main benefit now is that we can use the R-vine structure instead of the DAG structure, which is most often linked to the multivariate Gaussian distribution. For the proof, we first present two lemmas. These and the proof itself will be continuously illustrated.

Proof.

Consider an arbitrary edge We have , since conditioned sets in an R-vine tree sequence are unique and all conditioned sets of the form with occurred already in the first trees by A1. Additionally, , since otherwise would violate A2, as . Finally, , since the two elements of a conditioned set must be distinct. Thus, we have and hence . ∎

Example 4.7 (Example 4.4 cont.).

Illustrating Lemma 4.6, consider the R-vine matrix of Example 4.4 and column . To complete , we need to fill in e. g. . Valid entries can come from the main diagonal of right of , i. e. . Since and by A1, the edges in the first two R-vine trees are and , the only remaining entry is . This can only be a non-descendant of because of A2.

Proof.

Consider for . We have the following two cases.

First case: . All parents of occurred in the conditioned set of edges together with in the first R-vine trees. Hence, and .

Second case: . Similarly to the first case, we conclude . Let with . To obtain the elements of , recall A2 and consider the column of the R-vine matrix in which is in the diagonal, say column . The entries describe the elements which occurred in conditioned sets together with in the first trees. As these entries may only be taken from the right of , these must be non-descendants of .

To conclude the statement for the R-vine trees , we use an inductive argument. Let and is in the diagonal of the R-vine matrix in column . Then, for the conditioning set of we have . For the set we have shown that it can only consist of parents and non-descendants of . As can only have a value occurring in the main diagonal of the R-vine matrix to the right of column , it must be a non-descendant of . The same argument holds inductively for the trees . Thus, we have shown that for each edge with we have .

∎

Example 4.9 (Example 4.7 cont.).

Consider the first column of with . Since , and , independently of the values in , is in the conditioning set for each of these edges. There will be more nodes in the conditioning set but in higher trees, yet, these are non-descendants of by A2.

Proof.

Abbreviate and set with arbitrary but fixed. For the node in the DAG we have by the directed local Markov property (3.1) that and thus with Lemma 4.6,

| (4.3) |

Set , plug it into (4.3) obtaining

| (4.4) |

exploiting , i. e. a node can not be part of the conditioning and the conditioned set of the same edge. Applying Proposition 3.3 on (4.4) yields by dropping in (4.4). is a disjoint union on which Proposition 3.3 can be applied to conclude . By definition of , we have and obtain the final result Since each edge is assigned a pair copula density, we can now choose the independence copula density for these edges in backed by the conditional independence properties of the DAG. The resulting R-vine is thus a -truncated R-vine. ∎

Example 4.10 (Example 4.9 cont.).

We illustrate Theorem 4.5 using the previous Examples 4.7 and 4.9. Consider column of and edge . From the conditional independence obtained from the DAG , we select the non-descendants of to neglect, i. e. , to yield by application of Proposition 3.3 and finally by second application of Proposition 3.3.

Computing an R-vine representation of an arbitrary -DAG is a complex combinatorial problem and the existence of an incomplete R-vine tree sequence satisfying A1 and A2 is not clear. We first show classes of -DAGs where we can prove the existence of their R-vine representations. Afterwards, we introduce necessary conditions for the existence of an -truncated R-vine representation.

Corollary 4.11 (-DAGs with R-vine representation).

Let be a -DAG such that is an increasing topological ordering of . If, for all , , we have or , an R-vine representation of exists.

Proof.

Let . The R-vine representation is given by being path from to according to the topological ordering of , i. e. a D-vine. Because of the proximity condition, are uniquely determined by . In tree , the edges have the form and each conditioned set in the first R-vine trees represents an arrow of , satisfying A1. A2 also holds since in a D-vine, the main diagonal of the R-vine matrix can be written as ordering of the path . If , is given a star with central node . is a star with central node and so on, giving rise to a C-vine. In tree , the edges have the form for , satisfying A1. The main diagonal of the R-vine matrix of a C-vine is ordered according to the central nodes in the C-vine, satisfying A2. To both, Theorem 4.5 applies. Examples of a -DAG with D-vine and a -DAG with C-vine representation are shown in Figure 6. ∎

We now present necessary conditions for the first tree of an R-vine representation. It is of particular importance as it influences all higher order trees by the proximity condition.

4.4 Necessary conditions for Theorem 4.5

Proposition 4.12 (Necessary conditions).

Consider a -DAG and the sets

Assume there exists an R-vine representation such that A1 and A2 hold. For , denote the induced subgraphs of on . Thus, in are all edges in between nodes of . Then, must be such that

-

(i)

for all with , contains a path involving all nodes of ,

-

(ii)

the union of the induced subgraphs is acyclic for .

Proof.

To show assume satisfies A1 and A2. Choose with arbitrary but fixed. Order the set such that is the conditioned set of an edge , ensured by A2. Then, by the proof of Theorem 4.5, each edge corresponding to must have the form . By the set formalism, see Example 2.1, and the proximity condition, see (iii) on page (iii), we have requiring and . For we can conclude in a first step and in a second step . This can be extended to and yields for . Thus, and its parents, i. e. represent a path in . Showing , for each the graph is a subgraph of by . Thus, the union of over all must be a subgraph of . Since is a tree, it is acyclic, hence, each of its subgraphs must be, and so the graph in . ∎

Whereas the proof of is a direct consequence of the proximity condition, the proof of is less intuitive. We illustrate this property.

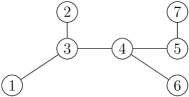

Example 4.13 (DAG in dimensions).

Consider the DAG in Figure 7. By Proposition 4.12, we need to find an R-vine tree such that the induced subgraphs contain a paths involving all nodes of for .

This is not possible. If it would be, use the path from to , from to and finally from to . However, this creates a cycle and as such can not be a tree. Yet, removing any edge which closes the cycle yields an induced subgraph which is no longer connected, i. e. a path. Thus, the DAG can not be represented by a -truncated R-vine. -truncated R-vines are possible which are shown in Appendix B, Example B.2.

Based on Proposition 4.12, we are given an intuition how to construct an admissible first R-vine tree of for a DAG . Moreover, it also yields a best possible truncation level for which a -truncated R-vine representation exists.

Corollary 4.14 (Best possible truncation level ).

Consider a -DAG . Let be a tree and for each let be the length of the unique path from to in . If is extended by successive R-vine trees , then the truncation level can be bound from below by

An example and the proof, using the proximity condition, d-separation and the graphical structure of is given in Appendix C.2. A1 and A2 are strong assumptions and hence only rarely satisfied for arbitrary DAGs. This gives rise to a heuristic approach for arbitrary -DAGs to find a sparse R-vine representation exploiting their conditional independences.

4.5 Representing -DAGs as sparse R-vines

Our goal is to find an R-vine representation of an arbitrary -DAG for . For the first R-vine tree , we have candidates. Considering all these and checking Proposition 4.12 is not feasible. Additionally, A2 is hard to check upfront since it is not fully understood how a certain R-vine matrix diagonal relates to specific R-vines. Fixing the main diagonal may thus result in suboptimal models. Hence, Theorem 4.5 can not be applied directly. Denote a -DAG. By A1, arrows in shall be modelled as conditioned sets in R-vine trees for . Yet, for , there may be up to candidate edges for which is limited to edges. Hence, it is crucial to find the most important arrows of for . An heuristic measure for the importance of an arrow in , fitted on data, is how often the arrow exists in ,…,-DAGs , also fitted on data. However, also an arrow is possible. Since R-vines are undirected graphical models, we neglect the orientation of arrows in the DAGs by considering their skeletons. Thus, for each edge in the skeleton of the DAG we estimate DAGs on the data, obtain their skeletons and count how often the edge exists in these graphs. An edge might be more important than an edge with , which we describe by a non-increasing function of the maximal number of parents . Formally, consider -DAGs for estimated on data. Denote the skeleton of for and define an undirected graph with edge weights for given by

| (4.5) |

with non-increasing for . In the remainder, . To our knowledge, this approach has not been used before. On , find a maximum spanning tree by, e. g. Prim (1957), maximizing the sum of weights . The higher order trees are built iteratively. First, define a full graph on and delete each edge in not allowed by the proximity condition. Denote the edges with conditioned and conditioning set for . Set weights for according to

| (4.6) |

Thus, has positive weight if its conditioned set is an edge in at least one of the skeletons . We can not ensure A2, and thus not use the directed local Markov property as in Theorem 4.5. We overcome this using d-separation. More precisely, for , , we check if is d-separated from given in . To facilitate conditional independence, i. e. sparsity, for assign

In the remainder, , i. e. it will not exceed the weight of an edge with in any of the DAGs as we want to model relationships in the DAGs prioritized. All other weights are zero and a maximum spanning tree algorithm is applied on . If an edge with weight is chosen, we can directly set the independence copula. We repeat this for . Since each pair of variables occurs exactly once as conditioned set in an R-vine, each weight in is used exactly once. The actual truncation level is such that the R-vine trees contain only the independence copula. The corresponding algorithm is given in Appendix G, for a toy example, see Appendix D. We test it in the following simulation study and application.

5 Simulation Study

For the next two sections, let and define

-

(i)

x-scale: the original scale of with density ,

-

(ii)

u-scale or copula-scale: , the cdf of and , ,

-

(iii)

z-scale: , the cdf of thus , .

We show that our approach of Section 4.5 calculates useful R-vine models in terms of goodness-of-fit in very short time. We collected data from January 1, 2000 to December 31, 2014 of the S&P100 constituents. At the end of the observation period, still of the original stocks were in the index. For these stocks and the index we calculated daily log-returns, obtaining data in dimensions with observations. We remove trend and seasonality off the data using ARMA-GARCH time series models with Student-t distributed residuals to obtain data on the x-scale. Afterwards, we transform the residuals to the copula-scale using their, non-parametrically estimated, empirical cumulative distribution function. For this dataset, we fitted five R-vine models using the R-package VineCopula, see Schepsmeier et al. (2016) using the algorithm of Dißmann et al. (2013), introduced on p. 2.

| Scenario | pair copula families | truncation level | level |

|---|---|---|---|

| 1 | all | - | |

| 2 | independence, t | - | |

| 3 | all | 4 | |

| 4 | all | - | |

| 5 | all | 4 |

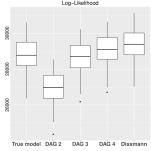

The models were fitted with settings as shown in Table 3 such that Scenarios 3, 4 and 5 exhibit more sparsity. This is done by either imposing truncation levels or performing independence tests at level while fitting the R-vines, see columns and of Table 3. leads to many more independence copulas than . From these models, replications with data points each were simulated. For each of the simulated datasets, Dissmann’s and our algorithm, see Section 4.5, were applied using -DAGs with .

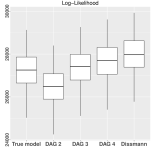

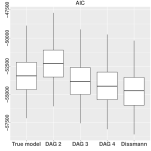

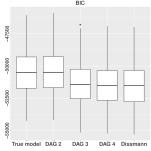

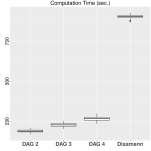

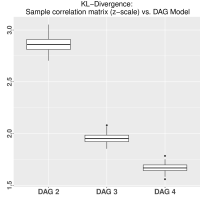

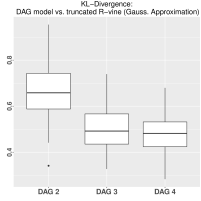

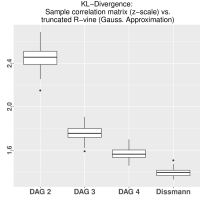

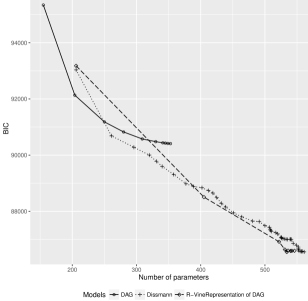

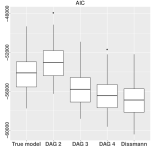

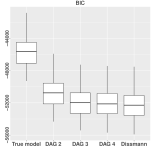

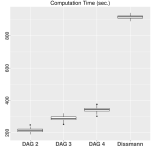

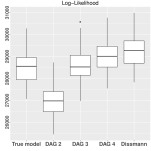

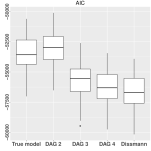

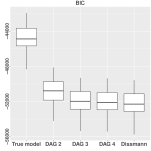

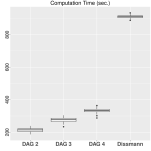

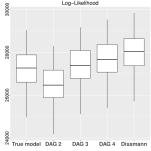

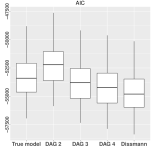

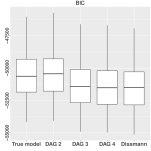

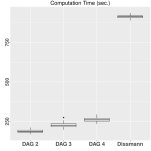

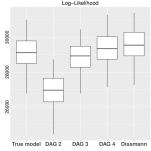

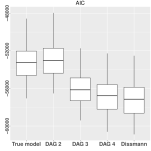

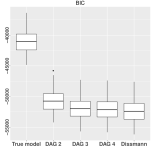

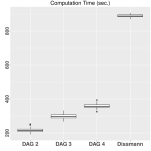

We consider the results for the sparsest Scenario 5 in Figure 8. Dissmann’s algorithm achieves better results in terms of log-Likelihood and AIC, however, tends to overfit the data. For BIC, our approach using -DAGs with achieves similar results as Dissmann. However the computation times are significantly shorter for our approach. The results are very similar for the other scenarios, henceforth we deferred their results in Appendix E. A second aspect is the distance of associated correlation matrices. We consider the data on the z-scale and calculate the Kullback-Leibler divergence, see Kullback and Leibler (1951). First, between the sample correlation matrix and the correlation matrix of , (a). Next, we compare and the correlation matrix of the representing R-vine model (b). Finally, we compare and and the correlation matrix of the Dissmann model (c).

We draw the conclusion that a -DAG is not a good approximation of the sample correlation matrix, but we obtain better fit with - and -DAG. The rather low values in the centre plot indicate that our approach maps the structure between DAG and R-vine representation quite well. In the right plot, we see that Dissmann’s algorithm obtains a smaller distance to the sample correlation matrix on the z-scale. However, the distance between -DAG and sample can still decrease for higher , whereas the Dissmann model is already fully fitted.

6 Application

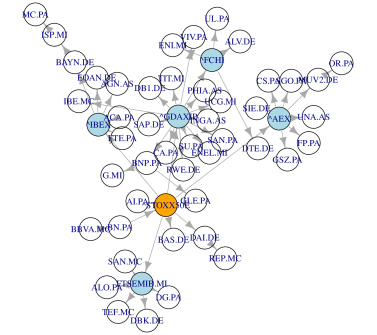

In Brechmann and

Czado (2013), the authors analyzed the Euro Stoxx 50 and collected time series of daily log returns of major stocks and indices from May 22, 2006 to April 29, 2010 with observations. For these log returns, they fitted ARMA-GARCH time series models with Student-t’s error distribution to remove trend and seasonality, obtaining standardized residuals. These are said to be on the x-scale with a marginal distribution corresponding to a suitably chosen Student-t error distribution . Using this parametric estimate for , , the copula data is calculated. Since our approach uses Gaussian DAGs, we transform the data to have standard normal marginals, i. e. to the z-scale by calculating , with the cdf of a distribution.

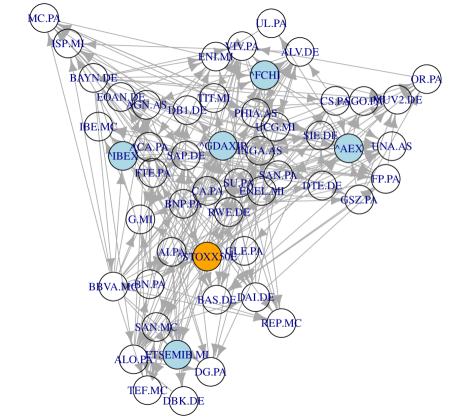

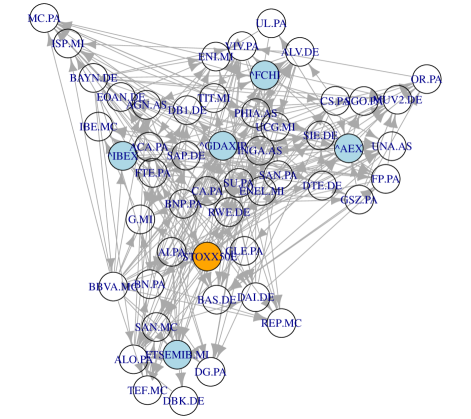

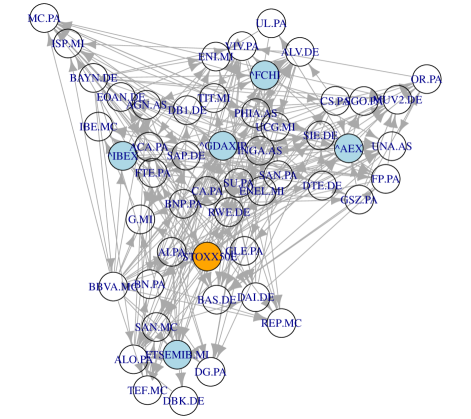

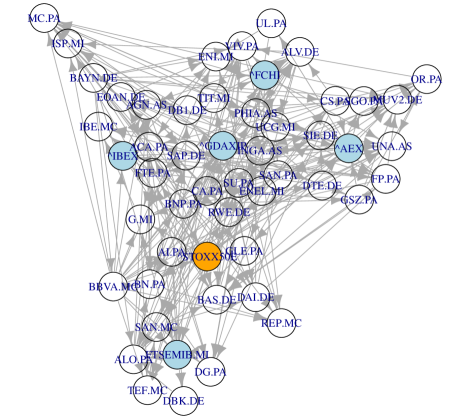

To learn -DAGs for from the z-scale data, we use the Hill-Climbing algorithm of the R-package bnlearn, see Scutari (2010) since we can limit the maximal number of parents. These -DAGs are shown in Appendix F.1. Then, we apply our algorithm RepresentDAGRVine to calculate R-vine representations of the DAGs. To find pair copulas and parameters on these R-vines with independence copulas at given edges, we adapt functions of the R-package VineCopula, see Schepsmeier et al. (2016) and is apply them onto data on the u-scale. All pair copula families of the R-package VineCopula were allowed.

As laid out initially, the paper has two goals. The first was to find truncated R-vines related to Gaussian DAGs which overcome the restriction of Gaussian distributions. Thus, we compare the goodness-of-fit of the -DAGs to their R-vine representations from our algorithm. Given that our approach represents the structure of the DAGs well and there is non-Gaussian dependence, the variety of pair copula families of an R-vine should improve the fit notably. Second, we want to check whether our approach can compete with Dissmann’s algorithm. Using their algorithm, we calculate a sequence of -truncated R-vines for , using an level independence test. Overall, we consider three different models in terms of the number of parameters and the corresponding log-likelihood and BIC values. Comparing the log-likelihood of DAGs and R-vines, we have to bear in mind that the marginals in the DAG are assumed to be standard normal and we also have to assume the same marginals for the R-vines, as done in e. g. Hobæk Haff et al. (2016). Yet, an advantage of vine copulas is that we can model marginals independently of the dependency structure. Thus, there is additional upside potential for the R-vine model.

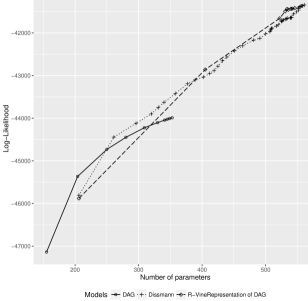

The results are given in Figure 10 and Tables A4, LABEL:table:application:dissmann in Appendix F.2. The DAG models have the least parameters but their goodness-of-fit falls behind the two competitors. The reason is the presence of non-Gaussian dependence, i. e. -copulas in the data which can not be modelled by the DAG. Comparing Dissmann’s approach to our algorithm, we see a very similar behaviour when it comes to log-likelihood and BIC. However, our approach finds more parsimonious models given fixed levels of BIC. The computation time for our algorithm ranges from 125 sec. for a -DAG to 270 sec. for a -DAG. Dissmann’s algorithm needs more than 600 sec. for a first R-vine tree and up to 760 sec. for a full estimation. Thus, our approach is about to times faster. This is also what we inferred from the simulation study. The computations were performed on a Linux Cluster with cores. Our approach is significantly faster, since given a specific edge , Dissmann’s algorithm first carries out an independence test for the pair copula. If the hypothesis is rejected, a maximum likelihood fit of the pair copula is carried out. Our approach checks based on the d-separation in and the corresponding copula is set to the independence. The actual truncation levels of the R-vine representations are given in Table A4. They are relatively high given the number of parents of these DAGs. However, this is because of very few non independence copulas in higher trees. For example, in the R-vine representation of the -DAG, contain non-independence copulas of edges, i. e. about % are non-independence, see also Figure A30 in Appendix F.3. This sparsity pattern is not negatively influencing the computation times or BIC as our examples demonstrated. It is also not intuitively apparent that a specific truncation level is more sensible to describe the data compared to a generally sparse structure.

7 Conclusion

This paper aimed to link high dimensional DAG models with R-vines. Thus, the DAGs can be represented by a flexible modeling approach, overcoming the restrictive assumption of multivariate normality. Additionally, we intended to find new ways for non-sequential estimation of R-vine structures, a computationally highly demanding task. We proved a connection under sufficient conditions mapping -DAGs to -truncated R-vines. Afterwards, we gave necessary conditions for the corresponding DAGs to infer whether such R-vine models exist. For most cases more complex than a Markov Tree or special cases, an exact representation of a -DAGs in terms of a truncated R-vine is not possible. However, it motives a general procedure to find more parsimonious R-vine models comparable to the standard algorithm, but multiple times faster. We expect this to leverage the application of R-vines in even higher dimensional settings with up to variables.

Acknowledgement

The authors gratefully acknowledge the helpful comments of the referees, which further improved the manuscript. The first author is thankful for support from Allianz Deutschland AG. The second author is supported by the German Research foundation (DFG grant GZ 86/4-1). Numerical computations were performed on a Linux cluster supported by DFG grant INST 95/919-1 FUGG.

References

- Aas et al. (2009) Aas, K., C. Czado, A. Frigessi, and H. Bakken (2009). Pair-copula constructions of multiple dependence. Insurance, Mathematics and Economics 44, 182–198.

- Andersson and Perlman (1998) Andersson, S. A. and M. D. Perlman (1998). Normal linear regression models with recursive graphical markov structure. Journal of Multivariate Analysis 66, 133–187.

- Bauer and Czado (2016) Bauer, A. and C. Czado (2016). Pair-copula bayesian networks. Journal of Computational and Graphical Statistics 25(4), 1248–1271.

- Bauer et al. (2012) Bauer, A., C. Czado, and T. Klein (2012). Pair-copula constructions for non-Gaussian DAG models. Canadian Journal of Statistics 40, 86–109.

- Bedford and Cooke (2001) Bedford, T. and R. Cooke (2001). Probability density decomposition for conditionally dependent random variables modeled by vines. Annals of Mathematics and Artificial Intelligence 32, 245–268.

- Bedford and Cooke (2002) Bedford, T. and R. Cooke (2002). Vines - a new graphical model for dependent random variables. Annals of Statistics 30(4), 1031–1068.

- Brechmann and Czado (2013) Brechmann, E. and C. Czado (2013). Risk management with high-dimensional vine copulas: An analysis of the Euro Stoxx 50. Statistics & Risk Modeling 30, 307–342.

- Brechmann and Joe (2014) Brechmann, E. C. and H. Joe (2014). Parsimonious parameterization of correlation matrices using truncated vines and factor analysis. Computational Statistics & Data Analysis 77, 233–251.

- Czado (2010) Czado, C. (2010). Pair-copula constructions of multivariate copulas. In F. Durante, W. Härdle, P. Jaworki, and T. Rychlik (Eds.), Workshop on Copula Theory and its Applications. Springer, Dortrech.

- Czado et al. (2013) Czado, C., E. Brechmann, and L. Gruber (2013). Selection of vine copulas. In P. Jaworski, F. Durante, and W. Härdle (Eds.), Copulae in Mathematical and Quantitative Finance. Springer.

- Dißmann et al. (2013) Dißmann, J., E. Brechmann, C. Czado, and D. Kurowicka (2013). Selecting and estimating regular vine copulae and application to financial returns. Computational Statistics and Data Analysis 52(1), 52–59.

- Elidan (2010) Elidan, G. (2010). Copula bayesian networks. In J. Lafferty, C. Williams, J. Shawe-Taylor, R. Zemel, and A. Culotta (Eds.), Advances in Neural Information Processing Systems 23, pp. 559–567. Curran Associates, Inc.

- Gruber and Czado (2015a) Gruber, L. and C. Czado (2015a). Bayesian model selection of regular vine copulas. Preprint. https://www.statistics.ma.tum.de/fileadmin/w00bdb/www/LG/bayes-vine.pdf.

- Gruber and Czado (2015b) Gruber, L. and C. Czado (2015b). Sequential bayesian model selection of regular vine copulas. Bayesian Analysis 10, 937–963.

- Hobæk Haff et al. (2016) Hobæk Haff, I., K. Aas, A. Frigessi, and V. L. Graziani (2016). Structure learning in bayesian networks using regular vines. Computational Statistics and Data Analysis 101, 186–208.

- Koller and Friedman (2009) Koller, D. and N. Friedman (2009). Probabilistic Graphical Models: Principles and Techniques (1st ed.). MIT Press, Cambridge, Massachusetts.

- Kullback and Leibler (1951) Kullback, S. and R. Leibler (1951). On information and sufficiency. Annals of Mathematical Statistics 22, 79–86.

- Kurowicka and Cooke (2006) Kurowicka, D. and R. Cooke (2006). Uncertainty Analysis and High Dimensional Dependence Modelling (1st ed.). John Wiley & Sons, Ltd, Chicester.

- Kurowicka and Joe (2011) Kurowicka, D. and H. Joe (2011). Dependence Modeling - Handbook on Vine Copulae. Singapore: World Scientific Publishing Co.

- Lauritzen (1996) Lauritzen, S. L. (1996). Graphical Models (1st ed.). Oxford University Press, Oxford.

- Peters and Bühlmann (2014) Peters, J. and P. Bühlmann (2014). Identifiability of gaussian structural equation models with equal error variances. Biometrika 101, 219–228.

- Pircalabelu et al. (2015) Pircalabelu, E., G. Claeskens, and I. Gijbels (2015). Copula directed acyclic graphs. Statistics and Computing, 1–24.

- Prim (1957) Prim, R. C. (1957). Shortest connection networks and some generalizations. Bell System Technical Journal 36, 1389–1401.

- Schepsmeier et al. (2016) Schepsmeier, U., J. Stoeber, E. C. Brechmann, B. Graeler, T. Nagler, and T. Erhardt (2016). VineCopula: Statistical Inference of Vine Copulas. R package version 2.0.6.

- Scutari (2010) Scutari, M. (2010). Learning bayesian networks with the bnlearn R package. Journal of Statistical Software 35(3), 1–22.

- Sklar (1959) Sklar, A. (1959). Fonctions dé repartition á n dimensions et leurs marges. Publ. Inst. Stat. Univ. Paris 8, 229–231.

- Stöber et al. (2013) Stöber, J., H. Joe, and C. Czado (2013). Simplified pair copula constructions-limitations and extensions. Journal of Multivariate Analysis 119(0), 101 – 118.

- Warnes et al. (2015) Warnes, G. R., B. Bolker, L. Bonebakker, R. Gentleman, W. H. A. Liaw, T. Lumley, M. Maechler, A. Magnusson, S. Moeller, M. Schwartz, and B. Venables (2015). gplots: Various R Programming Tools for Plotting Data. R package version 2.17.0.

- Whittaker (1990) Whittaker, J. (1990). Graphical Models in Applied Multivariate Statistics (1st ed.). John Wiley and Sons, Chicester.

Appendix A Definitions from Graph Theory

Definition A.1 (Graph).

Let be a finite set. Let . Then, is a graph with node set and edge set .

Definition A.2 (Edges).

Let be a graph and let be an edge. We call an edge undirected if and directed if . A directed edge is also denoted by an arrow . Hereby, is called head of the edge and is called tail of the edge. By we denote that and or and , i. e. there is either a directed edge or in . By we denote that and , i. e. there is no directed edge between and .

Definition A.3 (Directed and undirected graphs).

Let be a graph. We call directed if each edge is directed. Similarly, we call undirected if each edge is undirected.

Definition A.4 (Weighted graph).

A weighted graph is a graph with weight function such that .

Definition A.5 (Skeleton).

Let be a directed graph. If we remove the edge orientation of each directed edge , we obtain the skeleton of .

Definition A.6 (Path).

Let be a graph. A path of length from to is a sequence of distinct nodes such that for . This definition applies for both directed and undirected graphs.

Definition A.7 (Cycle).

Let be a graph and let . A cycle is defined as a path from to .

Definition A.8 (Acyclic graph).

Let be a graph. We call acyclic if there exists no cycle within .

Definition A.9 (Chain).

Let be a directed graph. A chain of length from to is a sequence of distinct nodes with or for .

Example A.10 (Paths and chains in directed graphs).

Consider the following two directed graphs .

For each of the two graphs, we consider the question whether a path or chain from to exists. In , clearly a path from to along and exists. Additionally, also a chain from to exists, as well as a chain from to since for the existence of a chain, the specific edge orientation is not relevant. With the same argument, in there exists a chain between and . However, no path between and exists as there is no edge .

Definition A.11 (Subgraph).

Let be a graph. A graph is a subgraph of if and .

Definition A.12 (Induced subgraph).

Let be a graph. A subgraph of is an induced subgraph of if .

Example A.13 (Subgraphs and induced subgraphs).

Consider the following three graphs where and are subgraphs of . is an induced subgraph of , whereas is not since the edges and are present in on the subset of nodes but are missing in .

Definition A.14 (Complete graph).

Let be a graph. is called complete if .

Definition A.15 (Connected graph).

Let be an undirected graph. If a path from to exists for all in , we say that is connected.

Definition A.16 (Weakly connected graph).

Let be a directed graph. If a path from to exists for all in the (undirected) skeleton of , we say that is weakly connected.

Definition A.17 (Tree).

Let be an undirected graph. is a tree if it is connected and acyclic.

Definition A.18 (Separator).

Let . A subset is said to be an separator in if all paths from to intersect . The subset is said to separate from if it is an separator for every , .

Definition A.19 (v-structure).

Let be a directed acyclic graph. We define a v-structure by a triple of nodes if and but .

Definition A.20 (Moral graph).

Let . The moral graph of a DAG is defined as the skeleton of where for each v-structure an undirected edge is introduced in .

Definition A.21 (d-separation).

Let be an directed acyclic graph. An chain from to in is said to be blocked by a set of nodes , if it contains a node such that either

-

(i)

and arrows of do not meet head-to-head at , or

-

(ii)

nor has any descendants in , and arrows of do meet head-to-head at .

A chain that is not blocked by is said to be active. Two subsets and are now said to be d-separated by if all chains from to are blocked by .

Example A.22 (d-separation).

We give an example of a DAG , see Figure A13.

First, we want to consider whether holds. In this case, , and . By application of the d-separation, we see that can not block a chain from to as arrows do meet head-to-head at , hence does not hold.

Second, we consider whether . Thus, , and . The chain from to via is blocked as arrows meet not head-to-head at . Second, also the chain from to via is blocked as arrows meet not head-to-head. Hence, we conclude . For another example, see (Lauritzen, 1996, p. 50).

Appendix B Examples

Example B.1 (Example 2.1 cont.).

We continue Example 2.1 showing the remaining m-children and m-descendants.

Example B.2 (Example 4.13 cont.).

We show the corresponding first and second R-vines trees as outlined which lead to -truncated R-vines.

Appendix C Proofs

C.1 Proof of Proposition 4.3

Proof.

We assume . If not, the argument can be applied to each weakly connected subgraph of . Since , there are no v-structures, hence, the moral graph is the skeleton of and is connected. Since there are arrows in , there are undirected edges in . Since each connected graph on nodes with edges is a tree, is a tree. Additionally, each edge in corresponds to an arrow in the DAG , satisfying Assumption A1. The main diagonal of the R-vine matrix can be chosen to be a decreasing topological ordering of by starting with a node which has no descendants but one parent, say and let the corresponding R-vine matrix be such that . Thus, its parent and all other nodes must occur on the diagonal to the right of it. Next, take a node which has either one descendant, i. e. or no descendant, denote and set . This can be repeated until and determines the R-vine matrix main diagonal which is a decreasing topological ordering of , satisfying Assumption A2 onto which Theorem 4.5 applies. ∎

C.2 Proof of Corollary 4.14

Proof.

Since is a tree, all paths are unique. If not, there exist two distinct paths between and and both paths together are a cycle from to . Consider an arbitrary node with parents in such that , then there exists a unique path from to , . From Theorem 4.5, our goal is to obtain edges with conditioned sets with in an R-vine tree with lowest possible order . Similar to the proof of Proposition 4.12, we try to obtain an edge

| (C.1) |

with entries in the conditioning set. The conditioned set of C.1 can not occur in a tree with because of the proximity condition and since the path between and is unique. By the d-separation, page 3.2, two nodes in a DAG connected by an arrow, i. e. and its parent , can not be d-separated by any set . Thus, the pair copula density associated to the edge (C.1) in is not the independence copula density . This tree is characterized by a path distance in and the maximum path distance over all parents of yields the highest lower bound. As it has to hold for all , we obtain a lower bound for the truncation level by the maximum over all . ∎

We present a brief example for the Corollary.

Example C.1 (Example for Corollary 4.14).

Consider the R-vine tree in Figure A16.

Assume an underlying DAG with . We have a lower bound for the truncation level since the path in from to is with a path length . Not earlier as in tree , i. e. not in the trees an edge with conditioned set can be obtained which can not be represented by the independence copula.

Appendix D Toy-example for heuristics

Example D.1 (Heuristics for transformation).

Consider the DAGs , , with at most parents, see Figure A17, from left to right.

Applying a maximum spanning tree algorithm on to find the first R-vine tree , we obtain the skeleton (see Figure A18, first figure). This is however not in general the case. We sketch the intermediate step of building , where we already removed edges not allowed by the proximity condition and assigned weights according to Equation (4.6) (see Figure A18, second to fourth figures).

We see that has the form of a so called D-vine, i. e. the R-vine tree is a path. Thus, the structure of higher order trees and is already determined, see Figure A19.

Based on the first R-vine tree and Corollary 4.14 we infer the lower bound for the truncation level. We consider the sets for based on . For example, the node has the parents in . Based on the first R-vine tree we check the lengths of shortest paths between and its parents and obtain , and . By application of Corollary 4.14, this gives a lower bound for the truncation level . The lengths of the shortest paths in for all nodes can be found in Table A2.

| 1 | - | - | - |

|---|---|---|---|

| 2 | 3,4,5 | 1,3,3 | 3 |

| 3 | 1 | 1 | 1 |

| 4 | 1,3,5 | 1,2,2 | 2 |

| 5 | 1 | 1 | 1 |

| 6 | 1,4 | 1,2 | 2 |

We obtain . Note that this lower bound is not attained as we have the conditioned set in the R-vine Tree which can not be represented by the independence copula as this conditioned set is associated to an edge in the DAG . However, several edges with superscript can be associated with the independence copula by the d-separation. The trees and are only used to obtain the weights for the corresponding trees, but not with respect to check for d-separation.

Appendix E Supplementary material to simulation study

We restate the simulation setup for the remaining scenarios.

| Scenario | pair copula families | truncation level | indep. test significance level |

|---|---|---|---|

| 1 | all | - | |

| 2 | independence, t | - | |

| 3 | all | 4 | |

| 4 | all | - | |

| 5 | all | 4 |

Now, we present the results for the remaining scenarios to .

Appendix F Supplementary material to application

F.1 DAGs estimated on Euro Stoxx 50

F.2 Numerical results of fitted models

| DAG | R-vine representation of DAG | ||||||||||

| Max. parents | No. par. | log-Lik. | BIC | No. par | No. ni-pc | No. G-pc | No. non-G-pc | log-Lik. | BIC | time (sec.) | |

| 1 | 155 | -47138 | 95344 | 206 | 51 | 0 | 51 | -45880 | 93180 | 1 | 124 |

| 2 | 204 | -45365 | 92135 | 405 | 236 | 16 | 220 | -42859 | 88509 | 47 | 197 |

| 3 | 250 | -44731 | 91186 | 522 | 401 | 50 | 351 | -41661 | 86919 | 51 | 223 |

| 4 | 280 | -44448 | 90826 | 531 | 429 | 59 | 370 | -41492 | 86644 | 47 | 246 |

| 5 | 309 | -44224 | 90577 | 536 | 435 | 53 | 382 | -41455 | 86605 | 51 | 255 |

| 6 | 330 | -44104 | 90482 | 540 | 438 | 56 | 382 | -41435 | 86592 | 48 | 279 |

| 7 | 341 | -44045 | 90440 | 546 | 435 | 52 | 383 | -41418 | 86599 | 47 | 280 |

| 8 | 345 | -44026 | 90429 | 542 | 433 | 55 | 378 | -41431 | 86598 | 48 | 276 |

| 9 | 349 | -44006 | 90418 | 540 | 427 | 57 | 370 | -41436 | 86594 | 49 | 282 |

| 10 | 353 | -43990 | 90412 | 534 | 422 | 58 | 364 | -41437 | 86554 | 47 | 271 |

| trunc. level | No. par | No. ni-pc | No. G-pc | No. non-G-pc | log-Lik. | BIC | time (sec.) |

| 1 | 206 | 51 | 0 | 51 | -45808 | 93035 | 633 |

| 2 | 261 | 99 | 2 | 97 | -44445 | 90688 | 641 |

| 3 | 296 | 126 | 5 | 121 | -44120 | 90281 | 674 |

| 4 | 320 | 152 | 8 | 144 | -43899 | 90003 | 728 |

| 5 | 331 | 170 | 13 | 157 | -43750 | 89781 | 726 |

| 6 | 340 | 182 | 14 | 168 | -43628 | 89599 | 741 |

| 7 | 358 | 197 | 14 | 183 | -43422 | 89312 | 715 |

| 8 | 377 | 217 | 17 | 200 | -43194 | 88986 | 722 |

| 9 | 389 | 231 | 18 | 213 | -43101 | 88884 | 723 |

| 10 | 402 | 245 | 19 | 226 | -43037 | 88844 | 729 |

| 11 | 412 | 259 | 20 | 239 | -42950 | 88741 | 724 |

| 12 | 419 | 269 | 23 | 246 | -42882 | 88653 | 739 |

| 13 | 425 | 279 | 25 | 254 | -42781 | 88491 | 724 |

| 14 | 432 | 290 | 25 | 265 | -42654 | 88286 | 726 |

| 15 | 439 | 299 | 26 | 273 | -42566 | 88157 | 727 |

| 16 | 451 | 313 | 28 | 285 | -42420 | 87949 | 732 |

| 17 | 464 | 321 | 29 | 292 | -42303 | 87805 | 732 |

| 18 | 481 | 335 | 30 | 305 | -42170 | 87656 | 731 |

| 19 | 491 | 344 | 31 | 313 | -42126 | 87636 | 723 |

| 20 | 500 | 353 | 33 | 320 | -42023 | 87491 | 725 |

| 21 | 507 | 361 | 33 | 328 | -41969 | 87433 | 728 |

| 22 | 508 | 365 | 34 | 331 | -41933 | 87367 | 726 |

| 23 | 509 | 371 | 37 | 334 | -41907 | 87323 | 716 |

| 24 | 510 | 376 | 39 | 337 | -41886 | 87288 | 737 |

| 25 | 517 | 382 | 42 | 340 | -41839 | 87242 | 713 |

| 26 | 520 | 387 | 44 | 343 | -41808 | 87200 | 719 |

| 27 | 525 | 392 | 47 | 345 | -41730 | 87078 | 711 |

| 28 | 526 | 394 | 47 | 347 | -41723 | 87071 | 728 |

| 29 | 526 | 396 | 47 | 349 | -41710 | 87046 | 714 |

| 30 | 528 | 398 | 47 | 351 | -41695 | 87029 | 726 |

| 31 | 531 | 401 | 48 | 353 | -41678 | 87017 | 730 |

| 32 | 533 | 404 | 48 | 356 | -41668 | 87009 | 726 |

| 33 | 535 | 406 | 48 | 358 | -41657 | 87001 | 738 |

| 34 | 539 | 409 | 48 | 361 | -41647 | 87008 | 737 |

| 35 | 540 | 410 | 49 | 361 | -41643 | 87009 | 736 |

| 36 | 541 | 411 | 50 | 361 | -41638 | 87006 | 743 |

| 37 | 544 | 413 | 51 | 362 | -41556 | 86861 | 738 |

| 38 | 549 | 417 | 51 | 366 | -41506 | 86797 | 748 |

| 39 | 552 | 421 | 51 | 370 | -41464 | 86732 | 740 |

| 40 | 552 | 422 | 51 | 371 | -41432 | 86669 | 742 |

| 41 | 552 | 424 | 51 | 373 | -41414 | 86633 | 742 |

| 42 | 553 | 426 | 51 | 375 | -41390 | 86591 | 757 |

| 43 | 555 | 429 | 52 | 377 | -41378 | 86581 | 749 |

| 44 | 557 | 431 | 52 | 379 | -41368 | 86576 | 757 |

| 45 | 557 | 431 | 52 | 379 | -41368 | 86576 | 755 |

| 46 | 557 | 431 | 52 | 379 | -41368 | 86576 | 758 |

| 47 | 558 | 432 | 52 | 380 | -41366 | 86578 | 758 |

| 48 | 558 | 432 | 52 | 380 | -41366 | 86578 | 759 |

| 49 | 558 | 432 | 52 | 380 | -41366 | 86578 | 749 |

| 50 | 561 | 434 | 52 | 382 | -41346 | 86559 | 761 |

| 51 | 561 | 434 | 52 | 382 | -41346 | 86559 | 762 |

F.3 Distribution of non-independence copulas in the Euro Stoxx 50

To visualize the actual truncation levels of the R-vines based on a DAG with at most parents, we consider the distribution of independence pair copulas. Thus, we plot a matrix indicating which pair copulas are the independence copula in the R-vine representation of the DAG , see the lower triangular region of Figure A30, created with the R-package gplots, see Warnes et al. (2015). The upper triangular region encodes which pair copulas are set to the independence copula when we use an additional level independence test. We see the sparsity patterns of the corresponding R-vine models and note that each independence pair copula in the lower triangular is also in the upper triangular, where the upper triangular may also have additional independence pair copulas. It also indicates that an independence test based on the d-separation is not sufficient when dealing with non-Gaussian dependency patterns, as a huge number of pair copulas with small Kendall’s are not associated with the independence copula upfront.