Distributionally Robust Stochastic Optimization with Wasserstein Distance

Rui Gao \AFFDepartment of Information, Risk and Operations Management, University of Texas at Austin, Austin, TX 78705, rui.gao@mccombs.utexas.edu \AUTHORAnton J. Kleywegt \AFFH. Milton Stewart School of Industrial and Systems Engineering, Georgia Institute of Technology, Atlanta, GA 30332, anton@isye.gatech.edu

Distributionally robust stochastic optimization (DRSO) is an approach to optimization under uncertainty in which, instead of assuming that there is a known true underlying probability distribution, one hedges against a chosen set of distributions. In this paper we first point out that the set of distributions should be chosen to be appropriate for the application at hand, and that some of the choices that have been popular until recently are, for many applications, not good choices. We next consider sets of distributions that are within a chosen Wasserstein distance from a nominal distribution. Such a choice of sets has two advantages: (1) The resulting distributions hedged against are more reasonable than those resulting from other popular choices of sets. (2) The problem of determining the worst-case expectation over the resulting set of distributions has desirable tractability properties. We derive a strong duality reformulation of the corresponding DRSO problem and construct approximate worst-case distributions (or an exact worst-case distribution if it exists) explicitly via the first-order optimality conditions of the dual problem.

Our contributions are four-fold. (i) We identify necessary and sufficient conditions for the existence of a worst-case distribution, which are naturally related to the growth rate of the objective function. (ii) We show that the worst-case distributions resulting from an appropriate Wasserstein distance have a concise structure and a clear interpretation. (iii) Using this structure, we show that data-driven DRSO problems can be approximated to any accuracy by robust optimization problems, and thereby many DRSO problems become tractable by using tools from robust optimization. (iv) Our strong duality result holds in a very general setting. As examples, we show that it can be applied to infinite dimensional process control and intensity estimation for point processes.

distributionally robust optimization; Wasserstein metric; data-driven decision-making; ambiguity set; worst-case distribution \MSCCLASSPrimary: 90C15; secondary: 90C46 \ORMSCLASSPrimary: programming: stochastic

1 Introduction

In decision making problems under uncertainty, a decision maker wants to choose a decision from a feasible region . The objective function depends on a quantity whose value is not known to the decision maker at the time that the decision has to be made. In some settings it is reasonable to assume that is a random element with distribution supported on , for example, if multiple realizations of will be encountered. In such settings, the decision making problems can be formulated as stochastic optimization problems as follows:

We refer to Shapiro et al. [47] for a thorough study of stochastic optimization. One major criticism of the formulation above for practical applications is the requirement that the underlying distribution be known to the decision maker. Even if multiple realizations of are observed, still may not be known exactly, while use of a distribution different from may sometimes result in bad decisions. Another major criticism is that in many applications there are not multiple realizations of that will be encountered, for example in problems involving events that may either happen once or not happen at all, and thus the notion of a “true” underlying distribution does not apply. These criticisms motivate the notion of distributionally robust stochastic optimization (DRSO), that does not rely on the notion of a known true underlying distribution. One chooses a set of probability distributions to hedge against, and then finds a decision that provides the best hedge against the set of distributions by solving the following minmax problem:

| (DRSO) |

Such a minmax approach has its roots in Von Neumann’s game theory and has been used in many fields such as inventory management (Scarf et al. [45], Gallego and Moon [25]), statistical decision analysis (Berger [9]), as well as stochastic optimization (Žáčková [56], Dupačová [20], Shapiro and Kleywegt [48]). Recently it regained attention in the operations research literature, and sometimes is called data-driven stochastic optimization or ambiguous stochastic optimization.

A central question is: how to choose a good set of distributions to hedge against? A good choice of should take into account the properties of the practical application as well as the tractability of problem (DRSO). Two typical ways of constructing are moment-based and distance-based. The moment-based approach considers distributions whose moments (such as mean and covariance) satisfy certain conditions (Scarf et al. [45], Delage and Ye [19], Popescu [43], Zymler et al. [58]). It has been shown that in many cases the resulting DRSO problem can be formulated as a conic quadratic or semi-definite program. However, the moment-based approach is based on the curious assumption that certain conditions on the moments are known exactly but that nothing else about the relevant distribution is known. More often in applications, either one has data from repeated observations of the quantity , or one has no data, and in both cases the moment conditions do not describe exactly what is known about . In addition, the resulting worst-case distributions sometimes yield overly conservative decisions (Wang et al. [52], Goh and Sim [29]). For example, Wang et al. [52] shows that for the newsvendor problem, by hedging against all the distributions with fixed mean and variance, Scarf’s moment approach yields a two-point worst-case distribution, and the resulting decision does not perform well under other more likely scenarios.

The distance-based approach considers distributions that are close, in the sense of a chosen statistical distance, to a nominal distribution , such as an empirical distribution or a Gaussian distribution (El Ghaoui et al. [21], Calafiore and El Ghaoui [16]). Popular choices of the statistical distance are -divergences (Bayraksan and Love [6], Ben-Tal et al. [7]), which include Kullback-Leibler divergence (Jiang and Guan [32]), Burg entropy (Wang et al. [52]), and Total Variation distance (Sun and Xu [49]) as special cases, Prokhorov metric (Erdoğan and Iyengar [22]), and Wasserstein distance (Wozabal [53, 54], Esfahani and Kuhn [23], Zhao and Guan [57]).

1.1 Motivation: Potential Issues with -divergence

Despite its widespread use, -divergence has a number of shortcomings. Here we highlight some of these shortcomings. In a typical setup using -divergence, is partitioned into bins represented by points . The nominal distribution associates observations with bin . That is, the nominal distribution is given by , where . Let denote the set of probability distributions on the same set of bins. Let be a chosen convex function such that , with the conventions that for all , and . Then the -divergence between is defined by

Let denote a chosen radius. Then denotes the set of probability distributions given by the chosen -divergence and radius . The DRSO problem corresponding to the -divergence ball is then given by

It has been shown in Ben-Tal et al. [7] that the -divergence ball can be viewed as a statistical confidence region (Pardo [40]), and for several choices of , the inner maximization of the problem above is tractable.

One well-known shortcoming of -divergence balls is that, either they are not rich enough to contain distributions that are often relevant, or they they hedge against many distributions that are too extreme. For example, for some choices of -divergence such as Kullback-Leibler divergence, if the nominal , then , that is, the -divergence ball includes only distributions that are absolutely continuous with respect to the nominal distribution , and thus does not include distributions with support on points where the nominal distribution is not supported. As a result, if and is discrete, then there are no continuous distributions in the -divergence ball . Some other choices of -divergence exhibit in some sense the opposite behavior. For example, the Burg entropy ball includes distributions with some amount of probability allowed to be shifted from to any other bin, with the amount of probability allowed to be shifted depending only on and not on how extreme the bin is. See Section 5.1 for more details regarding this potential shortcoming.

Next we illustrate another shortcoming of -divergence that will motivate the use of Wasserstein distance.

Example 1.1

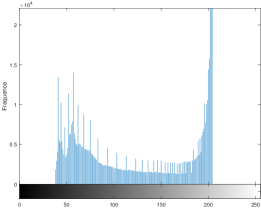

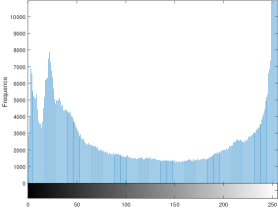

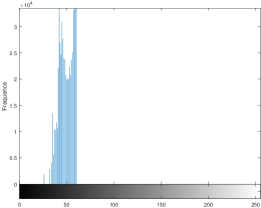

Suppose that there is an underlying true image (1b), and a decision maker possesses, instead of the true image, an approximate image (1a) obtained with a less than perfect device that loses some of the contrast. The images are summarized by their gray-scale histograms. (In fact, (1a) was obtained from (1b) by a low-contrast intensity transformation (Gonzalez and Woods [30]), by which the black pixels become somewhat whiter and the white pixels become somewhat blacker. This type of transformation changes only the gray-scale value of a pixel and not the location of a gray-scale value, and therefore it can also be regarded as a transformation from one gray-scale histogram to another gray-scale histogram.) As a result, roughly speaking, the observed histogram is obtained by shifting the true histogram inwards. Also consider the pathological image (1c) that is too dark to see many details, with histogram . Suppose that the decision maker constructs a Kullback-Leibler (KL) divergence ball . Note that . Therefore, if is chosen small enough (less than ) for to exclude the pathological image (1c), then will also exclude the true image (1b). If is chosen large enough (greater than ) for to include the true image (1b), then also has to include the pathological image (1c), and then the resulting decision may be overly conservative due to hedging against irrelevant distributions. If an intermediate value is chosen for (between and ), then includes the pathological image (1c) and excludes the true image (1b). In contrast, note that the Wasserstein distance satisfies , and thus Wasserstein distance does not exhibit the problem encountered with KL divergence (see also Example 2.4).

The reason for such behavior is that -divergence does not incorporate a notion of how close two points are to each other, for example, how likely it is that observation is given that the true value is . In Example 1.1, represents 8-bit gray-scale values. In this case, we know that the likelihood that a pixel with gray-scale value is observed with gray-scale value is decreasing in the absolute difference between and . However, in the definition of -divergence, only the relative ratio for the same gray-scale value is taken into account, while the distances between different gray-scale values is not taken into account. This phenomenon has been observed in studies of image retrieval (Rubner et al. [44], Ling and Okada [36]).

The drawbacks of -divergence motivates us to consider sets that incorporate a notion of how close two points are to each other. One such choice of is based on Wasserstein distance. Specifically, consider any underlying metric on which measures the closeness of any two points in . Let , and let denote the set of Borel probability measures on . Then the Wasserstein distance of order between two distributions is defined as

More detailed explanation and discussion on Wasserstein distance will be presented in Section 2. Given a radius , the Wasserstein ball of probability distributions is defined by

1.2 Related Work

Wasserstein distance and the related field of optimal transport, which is a generalization of the transportation problem, have been studied in depth. In 1942, together with the linear programming problem (Kantorovich [34]), Kantorovich [33] tackled Monge’s problem originally brought up in the study of optimal transport. In the stochastic optimization literature, Wasserstein distance has been used for single stage stochastic optimization (Wozabal [53, 54]), and for multistage stochastic optimization (Pflug and Pichler [42]). The challenge for solving (DRSO) is that, the inner maximization involves a supremum over possibly an infinite dimensional space of distributions. To tackle this problem, existing works focus on the setup when is the empirical distribution on a finite-dimensional space. Wozabal [53] transformed the inner maximization problem of (DRSO) into a finite-dimensional non-convex program, by using the fact that if is supported on at most points, then there are extreme distributions of that are supported on at most points. Recently, using duality theory of conic linear programming (Shapiro [46]), Esfahani and Kuhn [23] and Zhao and Guan [57] showed that under certain conditions, the inner maximization problem of (DRSO) is actually equivalent to a finite-dimensional convex problem.

In this paper, we consider any arbitrary nominal distribution on a Polish space, and study the tractability of (DRSO) via strong duality. By the time we completed the first version of this paper, we learned that Blanchet and Murthy [11] independently considered a similar problem with more general lower semi-continuous transport cost function and study its strong duality. Our focus and our approach to this problem differ from theirs in several important ways. First, we show that the strong duality holds for any measurable function , while Blanchet and Murthy [11] proves the result only when is upper semi-continuous. The upper semi-continuity is used to ensure the existence of the worst-case distribution, but is not needed for the strong duality to hold. Second, we prove the strong duality result for the inner maximization of (DRSO) using a novel, yet simple, constructive approach, in contrast with the non-constructive approaches in their work and also in Esfahani and Kuhn [23] and Zhao and Guan [57]. This enables us to establish the structural characterization of the worst-case distributions of the data-driven DRSO (Corollary 3.19(ii)), which improves the result of Wozabal [53] and the more recent result of Owhadi and Scovel [39] on extremal distributions of Wasserstein balls (Remark 3.22). It also enables us to build a close connection between DRSO and robust optimization (Corollary 3.19(iii)). Third, we focus on Wasserstein distance of order (), while they consider more general transport cost functions in which the distance between two points is measured by a lower semi-continuous function rather than a metric as in our case. Nevertheless, our proof remains valid for such transport cost functions, and in fact, for even more general cost functions that are not necessarily lower semi-continuous (Remark 3.15). In the meantime, focusing on Wasserstein distance enables us to relate the condition for the existence of a worst-case distribution to the important notion of the “growth rate” of the objective function, and enables us to provide practical guidance for choosing the ambiguity set and controlling the degree of conservativeness based on the objective function (Remark 3.7).

1.3 Main Contributions

-

•

General Setting. We prove a strong duality result for DRSO problems with Wasserstein distance in a very general setting. We show that

holds for any Polish space and measurable function (Theorem 3.14).

-

1.

Both Esfahani and Kuhn [23] and Zhao and Guan [57] assume that is a convex subset of with some associated norm. The greater generality of our results enables one to consider interesting problems such as the process control problems in Sections 4.1 and 4.2, where is the set of finite counting measures on , which is infinite-dimensional and non-convex.

- 2.

-

3.

Both Esfahani and Kuhn [23] and Zhao and Guan [57] only consider Wasserstein distance of order . By considering a bigger family of Wasserstein distances, we establish the importance for DRSO problems of the notion of the “growth rate” of the objective function, which measures how fast the objective function grows compared to a polynomial of order . It turns out that the growth rate of the objective function determines the finiteness of the worst-case objective value (Proposition 3.6), and it plays an important role in the existence conditions for the worst-case distribution (Corollary 3.16). This is of practical importance, since it provides guidance for choosing the proper Wasserstein distance and for controlling the degree of conservativeness based on the structure of the objective function.

-

1.

-

•

Constructive Proof of Duality. We prove the strong duality result using a novel, elementary, constructive approach. The results of Esfahani and Kuhn [23] and Zhao and Guan [57] and other strong duality results in the literature are based on the established Hahn-Banach theorem for certain infinite dimensional vector spaces. In contrast, our proof idea is new and is relatively elementary and straightforward: we use the weak duality result as well as the first-order optimality condition of the dual problem to construct a sequence of primal feasible solutions whose objective values converge to the dual optimal value. Our proof uses relatively elementary tools, without resorting to other “big hammers”.

-

•

Existence Conditions and the Structure of Worst-case Distributions. As a by product of our constructive proof, we identify necessary and sufficient conditions for the existence of worst-case distributions, and a structural characterization of worst-case distributions (Corollary 3.16). Specifically, for data-driven DRSO problems where (where denotes the unit mass on ), whenever a worst-case distribution exists, there is a worst-case distribution supported on at most points with the following concise structure:

for some , and

where is the dual minimizer (Corollary 3.19). Thus can be viewed as a perturbation of , where the mass on is perturbed to for all , a fraction of the mass on is perturbed to , and the remaining fraction of the mass on is perturbed to . In particular, uncertainty quantification problems have a worst-case distribution with this simple structure, and can be solved by a greedy procedure (Example 3.29). Our result regarding the existence of a worst-case distribution with such a structure improves the result of Wozabal [53] and the more recent result of Owhadi and Scovel [39] regarding the extremal distributions of Wasserstein balls.

-

•

Connection with Robust Optimization. Using the structure of a worst-case distribution, we prove that data-driven DRSO problems can be approximated by robust optimization problems to any accuracy (Corollary 3.19(iii)). We use this result to show that two-stage linear DRSO problems with linear decision rules have a tractable semi-definite programming approximation (Section 5.2). Moreover, the robust optimization approximation becomes exact when the objective function is concave in . In addition, if is convex in , then the corresponding DRSO problem can be formulated as a convex-concave saddle point problem.

The rest of this paper is organized as follows. In Section 2, we review some results on the Wasserstein distance. Next we prove strong duality for general nominal distributions in Section 3.1, and in Section 3.2 we derive additional results for finite-supported nominal distributions. Then, in Sections 4 and 5, we apply our results on strong duality and the structural description of the worst-case distributions to a variety of DRSO problems. We conclude this paper in Section 6. Auxiliary results, as well as proofs of some Lemmas, Corollaries and Propositions, are provided in the Appendix.

2 Notation and Preliminaries

In this section, we introduce notation and briefly outline some known results regarding Wasserstein distance. For a more detailed discussion we refer to Villani [50, 51].

Let be a Polish (separable complete metric) space with metric . Let denote the Borel -algebra on , and let denote the completion of with respect to a measure on such that the measure space is complete (see, e.g., Definition 1.11 in Ambrosio et al. [3]). Let denote the set of Borel measures on , let denote the set of Borel probability measures on , and let denote the subset of with finite -th moment for :

It follows from the triangle inequality that the definition above does not depend on the choice of . A function is called -measurable if it is -measurable, and a function is called -measurable if it is -measurable. To facilitate later discussion, we introduce the push-forward operator on measures.

Definition 2.1 (Push-forward Measure)

Given measurable spaces and , a measurable function , and a measure , let denote the push-forward measure of through , defined by

That is, is obtained by transporting (“pushing forward”) from to using the function . For , let denote the canonical projections given by . Then for a measure , is the -th marginal of given by and .

Definition 2.2 (Wasserstein distance)

The Wasserstein distance between is defined by

| (1) |

That is, the Wasserstein distance between is the minimum cost (in terms of ) of redistributing mass from to , which is why it is also called the “earth mover’s distance”. Wasserstein distance is a natural way of comparing two distributions when one is obtained from the other by perturbations. The minimum on the right side of (1) is attained, because is non-negative, continuous and thus lower semi-continuous (Theorem 1.3 of [50]). The following example is a familiar special case of problem (1).

Example 2.3 (Transportation problem)

Consider and , where , , for all , and . Then problem (1) becomes the classical transportation problem in linear programming:

Example 2.4 (Revisiting Example 1.1)

Next we evaluate the Wasserstein distance between the histograms in Example 1.1. To evaluate , note that the least cost way of transporting mass from to is to move the mass outwards. In contrast, to evaluate , one has to transport mass relatively long distances from right to left (changing the gray-scale values of pixels by large amounts), resulting in a larger cost than . Therefore .

Wasserstein distance has a dual representation due to Kantorovich’s duality (Theorem 5.10 in [51]):

| (2) |

where represents the space of -measurable functions. In addition, under the supremum above can be replaced by , where denotes the set of continuous and bounded real-valued functions on . Particularly, when , by the Kantorovich-Rubinstein theorem, (2) can be simplified to (see, e.g., Equation (5.11) in [51])

So for an -Lipschitz function , it holds that for all .

Definition 2.2 and the results above can be extended to finite Borel measures. Moreover, we have the following result.

Lemma 2.5

For any finite Borel measures with , it holds that .

Another important feature of Wasserstein distance is that metrizes weak convergence in (cf. Theorem 6.9 in Villani [51]). That is, for any sequence of measures in and , it holds that if and only if converges weakly to and as . Therefore, convergence in the Wasserstein distance of order implies convergence up to the -th moment. Villani [51, chapter 6] discusses the advantages of Wasserstein distance relative to other distances, such as the Prokhorov metric, that metrize weak convergence.

3 Tractable Reformulation via Duality

In this section we develop a tractable reformulation by deriving its strong dual. We suppress the variable of in this section, and results are interpreted pointwise for each . Given and , for any and , the inner maximization problem of (DRSO) is written as

| (Primal) |

Our main goal is to derive its strong dual

| (Dual) |

The dual problem is a one-dimensional convex minimization problem with respect to , the Lagrangian multiplier of the Wasserstein constraint in the primal problem. The term is called the Moreau-Yosida regularization of with parameter in the literature (cf. Parikh and Boyd [41]). Its measurability with respect to is established in Lemma 3.5(i) in Section 3.1.

3.1 General Nominal Distribution

In this section, we prove the strong duality result for a general nominal distribution on a Polish space . Such generality broadens the applicability of the result for (DRSO). For example, the result is useful when the nominal distribution is some distribution such as a Gaussian distribution on (Section 4.3), or even some stochastic process (Sections 4.1 and 4.2). We begin with a weak duality result, which is an application of Lagrangian weak duality.

Proposition 3.1 (Weak duality)

Consider any and . Then for any and , it holds that .

To prove the strong duality result, we consider two separate cases: and . As can be seen from (Dual), if the term is infinite for all , then . Thus, to facilitate our analysis, we introduce the following definitions.

Definition 3.2 (Regularization Operator )

Let be given by

For any and any such that , let

| (3) | |||||||

For any and any such that is nonempty, let

| (4) | |||||||

Then and represent respectively the closest and furthest distances between and any point in . Note that (resp. ) may not be equal to (resp. ).

Definition 3.3 (Growth rate)

Define the growth rate of as

Particularly, if for all , then .

If is bounded and is bounded above, then , and if is bounded and is not bounded above, then . The possibilities when is not bounded are more interesting. Next, Lemma 3.4 establishes some additional properties of , including the property that if is not bounded and , then

for any , which motivates why we call the growth rate of .

Lemma 3.4 (Properties of the growth rate )

-

(i)

Suppose that is unbounded. Then the quantity

is independent of .

-

(ii)

Suppose that . Then the growth rate is finite if and only if there exists and such that

(5) -

(iii)

Suppose that . If is unbounded and , then

for any .

Lemma 3.5 (Measurability)

For any , , and , the following hold:

-

(i)

, , , , and are -measurable.

-

(ii)

Suppose that . Then for any such that the sets

are non-empty for -almost all , there exists -measurable mappings such that and for -almost all .

-

(iii)

Suppose that . Then for any such that the sets

are non-empty for -almost all , there exists -measurable mappings such that and for -almost all .

-

(iv)

For any and such that

is non-empty for -almost all , there exists a -measurable mapping such that for -almost all .

-

(v)

Suppose that . For any , and any -measurable function such that the set

is non-empty for -almost all , there exists a -measurable mapping such that for -almost all .

Proposition 3.6 (Strong duality with infinite optimal value)

Consider any , , and . Suppose that and . Then .

Remark 3.7 (Choosing Wasserstein order )

Let

Proposition 3.6 suggests that a meaningful formulation of (DRSO) should be such that the Wasserstein order is greater than or equal to . In both Esfahani and Kuhn [23] and Zhao and Guan [57] only is considered. By considering higher orders in our analysis, we can accommodate a greater set of functions , and we also have more flexibility to choose the ambiguity set and to control the degree of conservativeness.

Lemma 3.8 (Properties of the regularization operator )

Let be a Polish space. Consider any , , and such that . Then there is a set such that , and the following holds.

-

(i)

[Monotonicity] is nondecreasing and upper-semi-continuous for all . for all and all . is concave for all . For any , any , and any such that , it holds that

For any and any such that , it holds that .

-

(ii)

[Bounds] For any such that , it holds that

-

(iii)

[Derivative] For all and all , the left partial derivative exists and satisfies

For all and such that , the right partial derivative exists and satisfies

Let denote the dual objective function given by

Lemma 3.9 (Dual objective function)

The dual objective function has the following properties:

-

(i)

for all and for all .

-

(ii)

is a convex function.

-

(iii)

is a lower semi-continuous function.

-

(iv)

as .

-

(v)

has a minimizer .

Lemma 3.10 (Structure of -optimal primal solution with )

Consider any , any , any , and any such that . Suppose that has a minimizer . Then, for any , there are a , a , a , -measurable mappings , and , such that ,

for -almost all , and

satisfies

| (6) |

and

| (7) |

Proof 3.11

Proof of Lemma 3.10. Note that for any and , the sets in Lemma 3.5(ii) are non-empty for -almost all . Hence there exists -measurable mappings such that

for -almost all .

The first-order optimality conditions and imply that

| (8) |

Next we verify that we can interchange the partial derivative and integration in (8). Recall from Lemma 3.8(i) that there is a set such that , and for all and all , and is concave for all . To show it for the right derivative in (8), consider any and any decreasing sequence . Let

Since is nondecreasing for all , for all . In addition, since is concave, for all . Note that . Thus it follows from the monotone convergence theorem that

| (9) |

To show it for the left derivative in (8), consider any and any increasing sequence with . Let be defined as before, and thus for all . In addition, since is concave, for all . That is, for all it holds that

It follows from that

Also, . Thus it follows from the dominated convergence theorem that

| (10) |

Therefore it follows from (8), (9), (10), and Lemma 3.8(iii) that

| (11) | ||||

In particular, for any with , it follows from (11) and Lemma 3.8(i) that

| (12) | ||||

Based on (12), we now construct a feasible primal solution. Note that there is a such that

| (13) |

Let . Define a distribution by

| (14) |

Then is primal feasible, because

| (15) |

Furthermore, recall that

for -almost all . This, together with (13), implies that

| (16) |

Recall that for all . Also, consider any . Recall that is non-decreasing, and thus for all and all . Also, it follows from that . Hence it follows from the dominated convergence theorem that and . Thus, given any , choose such that and , choose such that , and choose such that , , and . Set

Thus (7) follows from (15). Also, it follows from (16) that

Lemma 3.12 (Structure of -optimal primal solution with )

Consider any , any , any , and any such that . Suppose that is the unique minimizer of . If , then, for any , there are a and a -measurable mapping , such that for -almost all , and

satisfies

| (17) |

and

| (18) |

If , then for any , there is a , a , -measurable mappings , and , such that and for -almost all , , and

satisfies (17) and

| (19) |

Proof 3.13

Proof of Lemma 3.12. If is the unique minimizer of , then is increasing and convex on . For any , it follows from being increasing that

| (20) |

Consider any . It follows from Lemma 3.5 that there exists a -measurable map such that for -almost all . Also, note that . Thus,

for -almost all . This together with (20) yield that

| (21) |

Hence, the distribution is primal feasible.

Next, we separately consider the cases and . If , then for the distribution

| (22) |

it holds that

| (23) |

Thus, given any , choose such that , and choose (note that ). Set . Thus (18) follows from (21). Also, it follows from (23) that

Otherwise, if , then consider any . First, note that , and hence for all . Let

Next we show that . Note that for all . Thus

It follows from the definition of that , from that , and thus . Consider any . It follows that there exists such that and

for -almost all . Thus it follows from Lemma 3.5(v) that for any and , there exists a -measurable mapping such that

for -almost all , and

If , let . Note that , and thus there exists a such that . Then, let be given by for all , and for all . Note that is -measurable, and that . Otherwise, if , then let , and . Also in this case is -measurable, and . Let be such that

| (24) |

Define a distribution by

| (25) |

By construction, is primal feasible. Also,

| (26) |

Thus, given any , choose such that , choose such that , choose such that and (note that ), and choose . Set

Thus (19) follows from (24). It also follows from (24) that

Thus it follows from (26) that

The next theorem establishes a strong duality result when the growth rate is finite. The result follows from Lemmas 3.10 and 3.12 and by noting that

for any .

Theorem 3.14 (Strong duality with finite optimal value)

Consider any , any , any , and any such that . Then .

Remark 3.15

Next, we investigate existence conditions for worst-case distributions and their structure. In the remainder of this section, we assume that is upper-semi-continuous, and every bounded subset in is totally bounded (see, for example, Section 45 in [37]), which is satisfied by, for example, any finite-dimensional normed space. Under this assumption, if and , then Lemma 3.8(ii) and the upper semi-continuity of imply that the set is nonempty, and that can be attained. If and , then the upper semi-continuity of imply that can be attained for -almost all , but can be infinite. Thus, if (i) , or (ii) and , then the quantities and in (4) are well-defined for -almost all (where can be infinite if ).

Corollary 3.16 (Worst-case distribution)

Consider any , , , and such that . Assume that is upper-semi-continuous, and that bounded subsets of are totally bounded. Then the following holds:

-

(i)

[Existence condition] A worst-case distribution exists if and only if any of the following conditions hold:

-

(a)

There exists a dual minimizer .

-

(b)

is the unique dual minimizer, , and

-

(c)

is the unique dual minimizer, is nonempty, and

In addition, if , then for any . Otherwise, there is such that for any .

-

(a)

-

(ii)

[Structure] Whenever a worst-case distribution exists, there exists a worst-case distribution which can be represented as a convex combination of two distributions and , each of which is a perturbation of , as follows:

where , and satisfy

(27) Let be the joint distribution given by and . For any measurable set , let

If , then is an optimal joint distribution in the definition (1) of .

-

(iii)

Suppose is convex, is a concave function, and is a convex function for -almost all , then

Moreover, whenever a worst-case distribution exists, there exists such that is primal optimal and

Remark 3.17

Compared with Corollary 4.7 in Esfahani and Kuhn [23], Corollary 3.16(i) provides a complete description of the necessary and sufficient conditions for the existence of a worst-case distribution. Note that Example 1 in Esfahani and Kuhn [23] corresponds to and . We also remark that Yue et al. [55] derives a sufficient condition on the existence of the worst-case distribution that does not require the knowledge of .

Example 3.18

We present several examples that correspond to different cases in Corollary 3.16(i). In all these examples, , for all , , , and .

- 1.

-

2.

. It follows that , and . Thus condition (i)(c) is satisfied, and the worst-case distribution is .

-

3.

. It follows that . Note that .

-

–

Note that on . Also, satisfies the condition in LABEL:itm:small, thus for all it holds that and . There is no worst-case distribution, but the objective value of converges to as .

-

–

Note that on . Also, . Thus .

-

–

3.2 Finite-Supported Nominal Distribution

In this section, we consider the setting in which the nominal distribution has finite support. Let for some , . This occurs, for example, in data-driven settings in which the nominal distribution is given by an empirical distribution constructed with observations.

Corollary 3.19 (Data-Driven DRSO)

Consider any , , and . The following hold:

-

(i)

[Strong duality] The primal problem (Primal) has a strong dual problem

(28) -

(ii)

[Structure of the worst-case distribution] Whenever a worst-case distribution exists, there exists one which is supported on at most points and has the form

(29) where , , , and for all .

-

(iii)

[Approximation by robust optimization] Suppose that there exists , such that for all . For any positive integer , consider the robust optimization problem

with uncertainty set

If , then there exists a constant independent of such that

In addition, if is convex and is concave, then .

Statement (ii) shows that the worst-case distribution is a perturbation of , where out of the points, , are perturbed with all their probability mass to an associated maximizer , while at most one point is split and perturbed to two maximizers and . If for each the set of maximizers is a singleton, then there is no need to split, and the worst-case distribution has support on points as well. Using this structure, we obtain result (iii), which states that the primal problem can be approximated by a robust optimization problem with uncertainty set , which is a subset of that contains all distributions supported on points (not necessarily distinct) with probability each. Particularly, when is concave, such approximation is exact; and when is Lipschitz and , then is an -approximation of .

Remark 3.20

As can easily be seen in the proof, the result of statement (ii) can be generalized as follows. Suppose that , then whenever a worst-case distribution exists, there exists one of the form

Remark 3.21

Remark 3.22

Under a compactness assumption on , Wozabal [53] pointed out that to solve (Primal), it suffices to consider the extreme points of the Wasserstein ball , which are distributions that are supported on at most points. Later, in Owhadi and Scovel [39], this result was improved for Polish spaces or Borel subsets of Polish spaces to distributions that are supported on at most points. Statement (ii) further strengthens these results — for arbitrary metric spaces (see Remark 3.21), it suffices to consider distributions that are supported on at most points, and this bound is tight as shown by Example 3.29 below. Moreover, out of the at most points in the support of the extreme distribution has the same probability masses as the associated points in the support of the nominal distribution. We also remark that after this work, Yue et al. [55] shows that the worst-case distribution is supported on at most points by employing the Richter-Rogosinski theorem.

Remark 3.23 (Total Variation metric)

By choosing the discrete metric on , the Wasserstein distance is equal to the Total Variation distance (Gibbs and Su [28]), which can be used for settings in which it matters whether two points are the same or different, but no other notion of difference is relevant. In this case, if is chosen such that is an integer, then there is no point indexed by in (29) such that fractions of its probability are transported to different points to obtain worst-case distribution , and the primal problem (Primal) is reduced to the robust optimization problem with uncertainty set , whether () is convex (concave) or not.

Remark 3.24 (Choosing radius )

There are multiple ways to choose the radius of the Wasserstein ball. Practically we found that the cross-validation method seems to work well for many problems. We used this method for the numerical experiments on intensity estimation in Section 4.2, and obtained good performance. It has also been used in [23] for various numerical examples including portfolio optimization and uncertainty quantification. On the other hand, one can use concentration inequalities to determine an upper bound on the radius with a statistical guarantee. For example, in the context of a model with an underlying true distribution, one can estimate a theoretical upper bound on the distance between the empirical distribution and the true distribution. The classical concentration inequalities (see, e.g., [23, 24]) provides a radius of the order , where is the dimension of the random variable. We use this technique for a one-dimensional newsvendor problem in Section 5.1. However, note that such a bound is pessimistic for problems with high-dimensional random variables, since it suggests that the number of data points needed grows exponentially (in the dimension ) to make the radius smaller while maintaining the statistical guarantee. Fortunately, for many decision problems it is unnecessary to choose a radius such that the ball contains a true distribution with guaranteed probability — our goal is not to approximate the true distribution, but only the objective value. This also means that even if we would know the exact distance between the empirical distribution and the true distribution, we should not choose the distance to be the radius. Instead, we can choose the radius such that with high probability, for every the worst-case expectation in the DRSO problem dominates the true expectation. This idea has been exploited recently in Gao [26], which shows that the radius can be in the order of in many settings, independent of the dimension of the random variable. Another principle is to choose the radius such that the uncertainty set yields a confidence region for the true minimizer, and it has been shown in Blanchet et al. [10, 12] that such choice would lead to a -bound asymptotically under proper conditions.

Remark 3.25 (Algorithmic Complexity)

According to the dual reformulation, fixing the dual variable , the dual objective function is the sum of the optimal objective values of separate maximization problems. Suppose that we have an oracle for solving the inner maximization problem for any . Thereby the number of oracle calls to evaluate the worst-case expectation scales linearly with the sample size . To optimize the finite sum problem over , there are optimal algorithms whose complexity match the theoretical lower bound (see, e.g., [1, 35]).

For an important class of problems, the inner maximization problem is easy. Examples include the following problem types:

-

1.

Problems in which the inner maximization problem has a closed-form solution, for example, when is linear in , or more generally, and (Esfahani and Kuhn [23, Remark 6.6] and Gao et al. [27]). In this case, the minimax DRSO problem is equivalent to a finite-sum optimization problem with regularization, so the complexity is linear in the sample size , and can be (nearly) independent of the dimension of under suitable conditions.

-

2.

Problems in which is (piecewise) concave in , for which the overall DRSO is equivalent to a saddle-point problem (Examples 3.27 and 3.28). In this case, the complexity is more involved since it may also depend on the size of the Wasserstein ball and the geometry of the sample space. For example, consider use of the Mirror-Prox algorithm [38] to solve the saddle-point problem in which is convex in . The complexity is proportional to the square of the radius of the Wasserstein ball, and is nearly independent of the dimension of for uncertainty sets with nice geometry. As indicated in Remark 3.24, a good way to choose is roughly , and similar to the first case above this leads to a complexity that is linear in and nearly independent of the dimension of the random variable.

Proof 3.26

Proof of Corollary 3.19.

(ii) By Corollary 3.16(ii), whenever a worst-case distribution exists, there is one supported on at most points with the form

| (30) |

where , and . Given for all , note that

The problem above is a linear program with variables, one perturbation distance constraint, and constraints , . At an extreme point optimal solution of the linear program, if the perturbation distance constraint holds as an equality, then at least of the constraints hold as equalities, or equivalently, for at most one index it holds that is fractional. Otherwise, if the perturbation distance constraint holds as a strict inequality, then exactly of the constraints hold as equalities, or equivalently, none of the is fractional. Such an extreme point optimal solution gives a worst-case distribution

where if , if , and .

(iii) Note that . If is bounded, then , and if is unbounded, then it follows from the assumption and Lemma 3.4(iii) that .

It follows from Lemma 3.8(ii) that for all and all . Let . Consider any . For each , let be such that for all . Consider any such that for all . By Lemma 3.10, there are a , a , , and for , such that ,

for all , , and

satisfies . If for any , then can be replaced with , and the statements above continue to hold. Therefore, without loss of generality, we assume that . Given , note that

The problem above is a linear program with variables and constraints in addition to the variable bounds . At an extreme point optimal solution of the linear program, at most of the variables are nonzero. In addition, for each , the constraint requires at least one of the variables to be nonzero. Thus, for at least indices , exactly one of is equal to , and for at most one index , two of are positive. Hence, an extreme point optimal solution of the linear program gives a solution of the form

where for all , , such that ,

and . Consider

Then, since , it follows that

and thus . Since , it follows that

Since , it follows that

where the second inequality follows from Lemma 3.8(i) and . Therefore

Example 3.27 (Saddle-point Problem)

Example 3.28 (Piecewise concave objective)

Esfahani and Kuhn [23] showed that if is a closed convex subset of with norm , has finite support, , and , where each is concave, then the DRSO can be formulated as a convex optimization problem. Here we show that the result can be obtained as a corollary from the structure of a worst-case distribution. If , then by Corollary 3.16(i)(i)(a), a worst-case distribution exists and, by Corollary 3.19, has the form , where for each it holds that and . Moreover, due to the concavity of , if and for some , then any convex combination satisfies , and thus . Therefore, we can assume without loss of generality that if and , then . Thus, we can consider distributions of the form

If , then by Lemma 3.12 and the concavity of , we can also consider distributions of the form above. Therefore, the original primal problem is equivalent to

Next, let . Then, by the positive homogeneity of norms and the convexity-preserving property of perspective functions (cf. Section 2.3.3 in Boyd and Vandenberghe [15]), the primal problem can be reformulated as the following convex optimization problem:

This establishes Theorem 4.4 in Esfahani and Kuhn [23], which was obtained therein by a separate procedure of dualizing twice the reformulation (28).

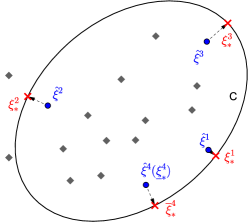

Example 3.29 (Uncertainty Quantification)

Consider a metric space such that every bounded subset in is totally bounded, and any open proper Borel subset . Let , and consider the uncertainty quantification problem

| (31) |

Next we show that it follows from Corollary 3.16(i) that problem (31) has an optimal distribution.

It follows from the definition of that .

Since is open, is upper-semi-continuous.

It follows from Lemma 3.9(v) that the dual objective function has a minimizer .

Next we consider two cases:

Case 1: There exists a dual minimizer :

Then it follows from Corollary 3.16(i)(i)(a) that a worst-case distribution exists.

Case 2: is the unique dual minimizer:

Since is a proper subset of , it follows that is nonempty, and that

Also, for any it holds that

Thus, for any it holds that

Next, let , then it follows from the monotone convergence theorem that

Therefore, it follows from Corollary 3.16(i)(i)(c) that a worst-case distribution exists.

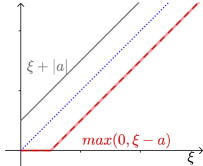

Depending on the metric , for , may or may not be on the boundary of . Next, suppose that is an intrinsic metric (so that, for , it holds that ), and that has finite support, say . Then the worst-case distribution of the problem (31) has an intuitive form. The worst-case distribution perturbs such that the set contains as little probability mass as possible, which can be achieved in a greedy fashion as follows. Suppose that are sorted such that , , and . Then to save the total budget of perturbation, stay at the same place, and the points with smaller indices have priority to be transported to their closest points in . Proceeding in this greedy way, points () are transported in full (with full mass ) to their closest points in . The next point is transported in part or in full to its closest point in — it may be the case that transporting in full to its closest point in would violate the Wasserstein distance constraint. Thus, only part , with , of its mass is transported, and the remaining mass stays at point (see Figure 3). Points stay at the same place. Therefore the worst-case distribution has the form

In fact, if , then the dual optimizer is such that

for all , and

In the discussion above we assumed that is open. The next proposition shows that for the normed space , uncertainty quantification of any Borel set can be reduced to that of an open set.

Proposition 3.30 (Continuity with respect to the boundary)

Consider a metric space such that every bounded subset in is totally bounded. Let , , and . Then for any proper Borel subset , it holds that

Example 3.31 (Finite Domain)

Next consider the special case when is finite, say for some positive integer . The nominal distribution is given by . Then the DRSO becomes

| (32) |

Corollary 3.32

Problem (32) has a strong dual

| (33) |

For any and , the worst-case distribution can be computed by solving

| (34) |

4 Applications

In this section, we apply our results to various application problems, including on/off system control and intensity estimation for point processes. In these problems, the space is a space of counting measures (sample paths of a point process), which is non-convex and infinite dimensional, and the nominal distribution is a point process. Hence, the results in Esfahani and Kuhn [23] and Zhao and Guan [57] cannot be applied to these problems.

4.1 On/Off System Control

In this problem, the decision maker faces a point process and controls a two-state (on/off) system. The point process is assumed to be exogenous, that is, the arrival times are not affected by the on/off state of the system. When the system is switched on, a cost of per unit time is incurred, and each arrival while the system is on contributes unit revenue. When the system is off, no cost is incurred and no revenue is earned. The decision maker wants to choose a control to maximize the total profit during a finite time horizon. This problem is a prototype for problems in sensor networks and revenue management.

Let the finite time horizon be denoted with , and let

be the set of sample paths of arrival times, which can also be described as the space of finite counting measures on . In many practical settings, the decision maker does not have a probability distribution for the point process. Instead, the decision maker has observations of sample paths of the point process, which constitute an empirical point process as nominal distribution. Specifically, suppose that we have data of sample paths , , where is a nonnegative integer, and for all and . Then the nominal (empirical) distribution is .

Note that if one would maximize the expected profit with respect to the nominal distribution, then it would yield a degenerate control, in which the system is switched on only momentarily at the arrival time points of the observed sample paths. Consequently, if future arrival times would differ from the historically observed arrival times by even a small amount, then the system would be switched off at future arrival times and no revenue would be earned. Due to such degeneracy and instability of optimization with respect to the nominal distribution, we resort to the distributionally robust approach.

As pointed out before, the choice of ambiguity set matters a great deal. For example, suppose that one chose to be the KL-divergence ball , that is, the set of all distributions such that for some . Then, for to hold, can put positive probability on observed sample paths only. Thus, even if one would solve a DRSO problem with KL-divergence ball , the resulting solution would be a degenerate control, in which the system is switched on only momentarily at the arrival time points of the historically observed sample paths, the same solution as when maximizing the expected profit with respect to the nominal distribution. In this section we show that solving a DRSO problem with a Wasserstein ball results in sensible solutions.

We assume that the metric on satisfies the following conditions. (Note that in this section, when we write the distance between two measures, we use the extended definition mentioned in Section 2.)

-

(i)

The metric space is a Polish space.

-

(ii)

For any nonnegative integer , and any and , where , it holds that

where and are the order statistics of and respectively.

-

(iii)

For any Borel set , , positive integer , and , where , it holds that

Note that condition (ii) is imposed only on such that , and that conditions (ii) and (iii) do not imply that . Examples of metrics that satisfy the conditions above are

and

| (35) |

These metrics are similar to the ones in Barbour and Brown [5] and Chen and Xia [17].

The set of point processes on is defined by the set of Borel probability measures on . Given the metric , we choose the distance between two point processes to be as defined in (1). Then the ambiguity set . Let denote the set of all functions such that is a Borel set. The decision maker is looking for a control that maximizes the total profit, by solving the problem

| (36) |

Next we investigate the structure of the optimal control. Let denote the interior of the set on the space with canonical topology (and thus ).

Proposition 4.1

Suppose that with . For any control , it holds that

| (37) | ||||

| (38) |

Moreover, there exists a non-negative integer such that

| (39) |

Note that

Hence, (37) shows that without changing the optimal value, we can replace by in the constraint, and (38) provides an equivalent dual reformulation that can be interpreted as the dual problem of the uncertainty quantification problem in which the nominal distribution is a Borel measure on . Then by Example 3.29, it can be solved by a greedy algorithm. Moreover, (39) shows that if is an empirical point process, then it suffices to consider the set of controls such that the system is on during a finite disjoint union of intervals with positive length.

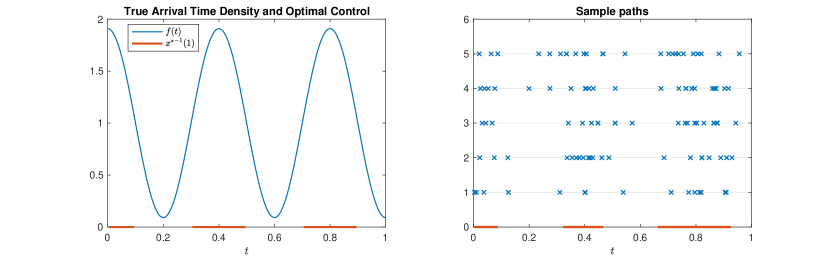

Example 4.2

Figure 4 shows results for an instance of the on/off system control problem. Suppose that the number of arrivals is Poisson distributed with mean , and given the number of arrivals, the arrival points are i.i.d. with density , . For example, corresponds to the Poisson process with rate . The optimization problem based on knowing the process is , with optimal control .

Let , with and . Particularly, let , , , and . Thus . The left of Figure 4 shows and . Suppose we have sample paths , each of which contains i.i.d. arrival points. The right of Figure 4 shows sample paths and the resulting DRSO solution. Even with a relatively small number of sample paths, the two controls are close to each other, and the DRSO provides not only a sensible solution (unlike the approach of optimizing the expected profit with respect to the empirical distribution), but even a good solution for the true process control problem.

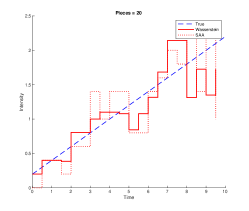

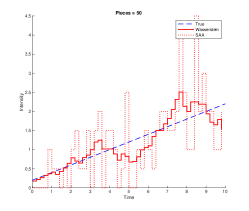

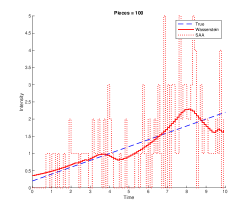

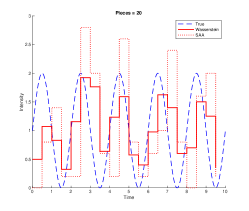

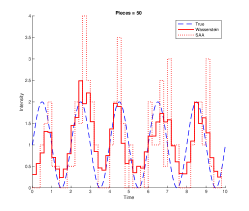

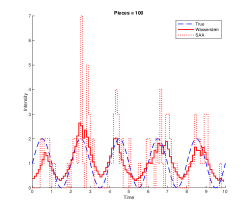

4.2 Intensity Estimation for Non-homogeneous Poisson Processes

Consider the problem of estimating the intensity function of a non-homogeneous Poisson process on using the maximum likelihood method. Given i.i.d. sample paths , , the log-likelihood function (see, e.g. Daley and Vere-Jones [18]) is written as

A common practice is to partition the time horizon into several intervals, and assume that is piecewise constant with constant value on each of the chosen intervals. Then the maximum likelihood estimator reduces to the average arrival rate on each interval. Such an approach suffers from the drawback that the estimator is sensitive to the partition of the time horizon into intervals. If the partition is very coarse, then the estimator remains constant during long intervals, and fails to capture time-varying arrival rates over shorter time periods. On the other hand, if the partition is very fine, then many intervals have zero observations, and the estimator varies too erratically over short intervals of time. A DRSO formulation with chosen to be the KL-divergence ball has a similar problem, since the resulting estimator vanishes on intervals with no observations.

Consider the DRSO formulation with Wasserstein distance

| (40) |

where is the Wasserstein ball centered at the empirical process. To facilitate further analysis, we choose defined in (35) as the distance between two counting measures. Our strong duality results imply that the dual reformulation of (40) is given by

Next we present numerical results for underlying true intensity functions given by and , . The sample size (number of sample paths) is . For both the maximum likelihood estimator and the DRSO estimator we optimized over piecewise constant with number of pieces in . The Wasserstein radius was chosen via a cross-validation method, in which half of the sample paths were used for estimating for each value of , and the other half of the sample paths were used for selecting the value of with the largest log-likelihood. The estimation results for both the maximum likelihood estimator (MLE) and the Wasserstein DRSO estimator are shown in Figure 5. Table 1 shows the distances between the estimated intensity functions and the true intensity functions. The Wasserstein DRSO estimator has superior performance in all cases. Also, the performance of the DRSO estimator is less sensitive to the fineness of the partition for the piecewise constant function than the performance of the maximum likelihood estimator — in these results the performance of the maximum likelihood estimator behaves poorly when the number of pieces is large.

| Pieces | 20 | 50 | 100 | 20 | 50 | 100 |

|---|---|---|---|---|---|---|

| Wasserstein | 0.854 | 0.893 | 0.544 | 2.008 | 2.157 | 2.087 |

| MLE | 1.510 | 6.536 | 11.906 | 6.160 | 6.591 | 11.766 |

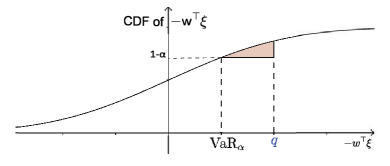

4.3 Worst-case Value-at-Risk

Value-at-risk is a popular risk measure in finance. Given a real-valued random variable that represents losses with measure that has a positive density on an interval, and , the value-at-risk of is defined by

In the spirit of El Ghaoui et al. [21], we consider the following worst-case problem. Consider a portfolio consisting of assets with allocation weights such that . Let denote the (random) return of asset , . Assume that . The worst-case with respect to the set of probability distributions is defined as

Given and , let . Then , similar to the uncertainty quantification problem (31) considered in Example 3.29. Using the rationale developed there, we obtain the following result.

Proposition 4.3

Suppose that has a positive density on , , and . Let be given, and let for all . Then, equals the unique solution of the following equation:

Example 4.4 (Worst-case with Gaussian nominal distribution)

Proposition 4.3 indicates that finding the worst-case is tractable. It should also be noted that finding the best allocation weight, i.e., optimizing over , still may be hard, since the constraint is essentially a chance constraint.

5 Discussions

In this section, we discuss some of the advantages of using the Wasserstein ambiguity set. In Section 5.1, we compare DRSO with the Wasserstein ambiguity set to DRSO with -divergence ambiguity sets for the newsvendor problem. In Section 5.2, we illustrate how the close connection between DRSO and robust optimization (Corollary 3.32(iii)) can be used to solve DRSO problems.

5.1 Newsvendor Problem: Comparison with -divergence

In this section, we consider distributionally robust newsvendor problems, and compare results obtained with the Wasserstein ambiguity set and results obtained with -divergence ambiguity sets. In the newsvendor problem, the decision maker chooses the initial inventory level before the unknown demand is observed, facing both overage and underage costs. If the demand distribution is known, the problem can be formulated as

where denotes the chosen initial inventory level, denotes the random demand, and , represent respectively the overage and underage costs per unit. Assume that , and is supported on for some positive integer . Consider the usual metric on .

Usually the demand distribution is not known. Then the decision maker may want to consider the DRSO problem

Using Corollary 3.32, we obtain a convex optimization reformulation

| Divergence | Kullback-Leibler | Burg entropy | -distance | Modified | Hellinger | Total Variation |

|---|---|---|---|---|---|---|

One may also consider -divergence ambiguity sets (Table 2 shows some common -divergences). As mentioned in Section 1, the worst-case distribution in a -divergence ambiguity set may be problematic. For example, when , such as and , the -divergence ambiguity set fails to include many relevant distributions. Specifically, since for all , the - and -divergence ambiguity sets do not include any distribution which is not absolutely continuous with respect to the nominal distribution .

When , such as , , , and , the situation is also bad. Let . Assume that are different from each other, so that is unique. Then according to Ben-Tal et al. [7] and Bayraksan and Love [6], the worst-case distribution satisfies

| (42a) | |||||

| (42b) | |||||

| (42e) | |||||

for some and , where denotes the convex conjugate function of . According to (42b), the support of the worst-case distribution and that of the nominal distribution can differ by at most one point . According to (42e), the probability mass is moved away from scenarios in to the worst scenario . Note that in many applications where the support of is unknown, the choice of the underlying space (such as ) may be somewhat arbitrary, and therefore the worst scenario (such as or ) may be arbitrary. Hence the worst-case behavior is too sensitive to arbitrary choices in the specification of .

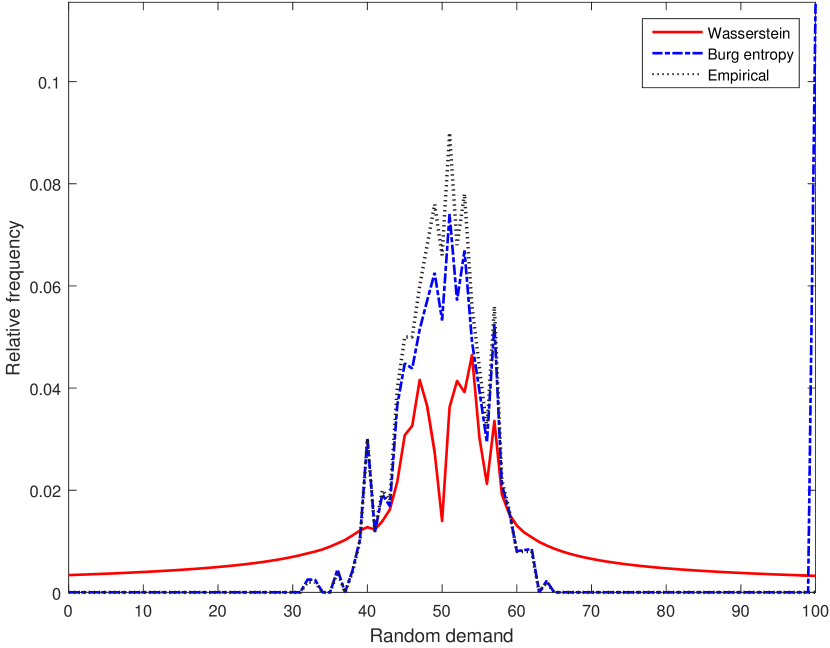

We present numerical examples of which the setup is similar to that in Wang et al. [52] and Ben-Tal et al. [7]. Let , , and representing small and large datasets. Random data are generated from Binomial and Geometric truncated on . We estimate the radius of the ambiguity set such that it covers the underlying distribution with probability greater than (see Appendix C).

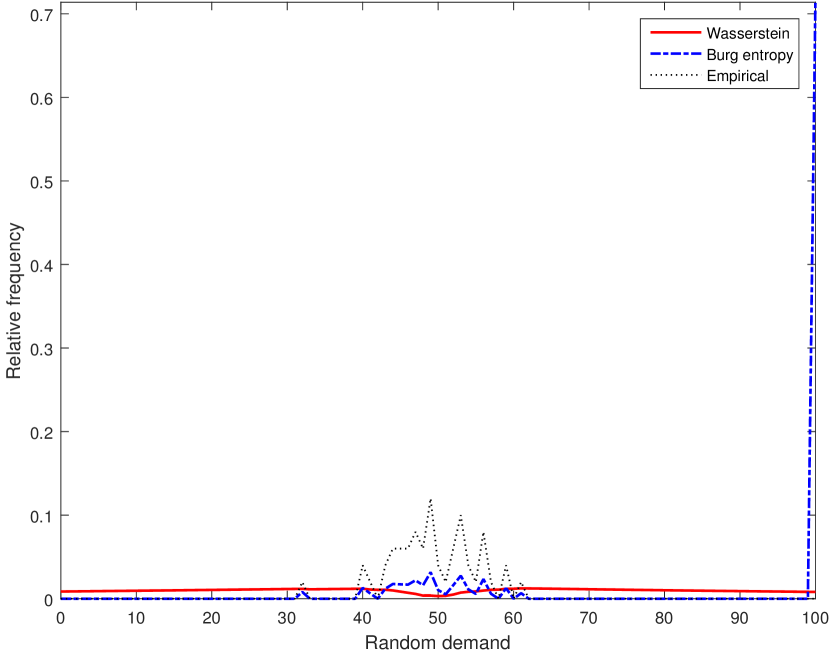

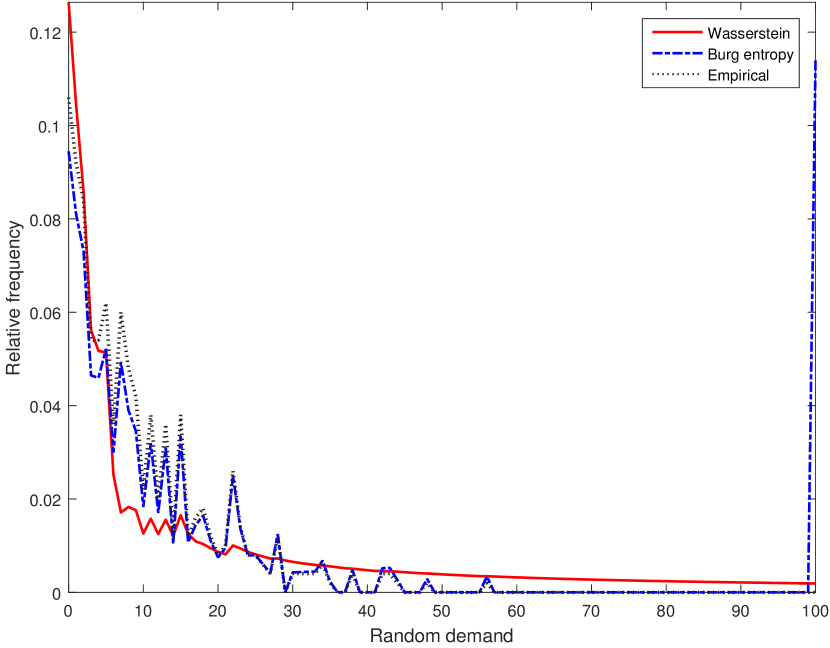

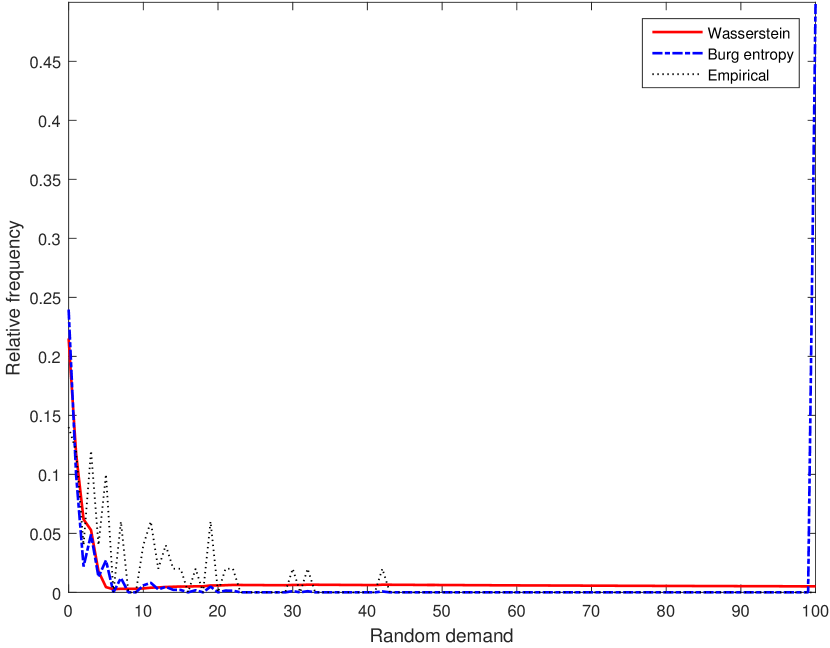

When the underlying distribution is Binomial, the symmetry of the Binomial distribution and implies that the optimal initial inventory level is close to . Intuitively, the corresponding worst-case distribution should make provision for both the possibility of high demand and the possibility of low demand. This intuition is consistent with the worst-case distributions in the Wasserstein ambiguity set, shown by the solid curves in Figures (7a)–(7b). The tails of these worst-case distributions are heavy on both the high side and the low side, and are quite smooth and reasonable for both small and large datasets. In contrast, if Burg entropy is used to define the ambiguity set, then the worst-case distributions have disconnected support, as shown by the dashed curves in Figures (7a)–(7b). There is a large spike on the boundary , displaying the “popping” behavior mentioned in Bayraksan and Love [6]. Especially when the dataset is small, the worst-case spike is huge, which makes the solution too conservative.

When the underlying distribution is Geometric, the worst-case distributions in the Wasserstein ambiguity set make provision for both the possibility of high demand and the possibility of low demand with fairly smooth variation of probability in between, as shown by solid curves in Figures (7c)–(7d). As before, if Burg entropy is used, then the tail has unrealistic spikes on the boundary, and thus the worst-case distribution is very sensitive to the somewhat arbitrary choice of truncation value . In these examples the Wasserstein ambiguity set seems to yield a more reasonable worst-case distribution.

5.2 Two-stage DRSO: Connection with Robust Optimization

In Corollary 3.19(iii) we established the close connection between the DRSO problem and robust optimization. More specifically, we showed that every DRSO problem can be approximated with high accuracy by robust optimization problems, which facilitates practical application of DRSO problems. To illustrate this point, in this section we show the tractability of two-stage linear DRSO problems.

Consider the two-stage distributionally robust stochastic optimization problem

| (43) |

where is the optimal objective value of the second-stage problem

and

Assume that and with Euclidean distance . In general, the two-stage problem (43) is NP-hard (see Section 3.3.2 in [31]). However, with tools from robust optimization, we are able to obtain a tractable approximation of (43). Let . Using Corollary 3.19(iii) with , we obtain an adjustable robust optimization approximation

| (44) | ||||

where the second set of inequalities follows from the fact that should hold for any realization with positive probability for some distribution in . Although problem (44) in general is still intractable, there has been a substantial literature on different approximations for problem (44). One approach is to consider the affinely adjustable robust counterpart (AARC), as follows. Consider that is an affine function of :

for some chosen , where . Then the AARC of (44) is

| (45) | ||||

Set for and . Note that if and only if

Set , and let

Then the first set of constraints in (45) is equivalent to

| (46) |

It follows from Theorem 4.2 in Ben-Tal et al. [8] that (46) holds if and only if there exists such that

In matrix form,

| (47) |

where (resp. ) is the (resp. ) identity matrix, is the Kronecker product of matrices, is the vectorization of matrix , and is a matrix whose -element equal to .

Next we reformulate the second set of constraints in (45). Let and denote row of and , respectively, . For all , , and , set

Let , , and . Then the second set of constraints in (45) is equivalent to

Again by Theorem 4.2 in Ben-Tal et al. [8] the second set of constraints in (45) is equivalent to

| (48) |

Proposition 5.1

An exact semidefinite program reformulation of the AARC of (44) is given by

| (49) |

6 Conclusions

In this paper, we developed a constructive proof method to derive the dual reformulation of distributionally robust stochastic optimization with Wasserstein distance for a general setting. This approach allows us to obtain a precise structural description of the worst-case distribution. It also facilitates a connection between distributionally robust stochastic optimization and robust optimization. We showed how the results can be used to obtain theoretical and computational conclusions for a variety of problems.

7 Proofs for Section 2

8 Proofs for Section 3

8.1 Proofs for Section 3.1

8.1.1 Auxiliary results

Lemma 8.1

Consider any and any . Then there exists such that

for all .

Proof 8.2

Proof of Lemma 8.1. Note that if , then the inequality holds for any . Next we consider the case with , and we let . Let

Note that . Next let

Note that because . Next, consider

Note that for all . Also, for all . Therefore for all , which establishes the inequality for . \Halmos

Lemma 8.3

Consider any . Then for any , there exists a constant such that

for all .

8.1.2 Proof of Proposition 3.1.

Note that

Thus, for any it holds that

Hence,

8.1.3 Proof of Lemma 3.4

(i) We prove the result by contradiction. Suppose that for some , it holds that

( is allowed). Choose any . Then there exists an such that for all with it holds that

Since , it follows that

which is a contradiction.

(ii) First we show that if there exists and such that for all , then . Let if is bounded, and let

if is unbounded. If is unbounded, then it follows from (i) that

| (50) |

We are going to show that for all , and therefore .

First we show that for any and . If is bounded, then choose any such that for all . If is unbounded, then it follows from (50) that for any , there is a such that for all with , it holds that

that is, . Thus, for all with , it holds that

and hence

Also, by assumption, for any it holds that

where the second inequality follows from the elementary inequality for any and . Thus

Therefore, for all and .

Next we show that for any . Consider any and any . It follows from Lemma 8.3 that there is a constant such that

Thus

Therefore .

Next we show that if there does not exist and such that for all , then . First, observe that if there exists and such that for all , then for any it holds that

It follows that there exists and such that for all if and only if there exists and such that for all , that is, there exists and such that for all . Therefore, if there does not exist and such that for all , then for any it holds that

which implies that .

(iii) It was established in the proof of (ii) that if then there exists and such that for all , and then

Next we show that . If , then it follows from the definition of that . Next, suppose that , and consider any . We will show that for all . If , then it follows from that for all . Next, consider any , any , any , any , and any . Since as , it follows that there exists such that for all such that . Choose any . It follows from the definition of that there exists such that and

Thus, for all , and hence for all . Therefore, . Next, recall that (i) established that does not depend on the choice of , and therefore the result follows. \Halmos

8.1.4 Proof of Lemma 3.5.

(i) By Definition 1.11 in Ambrosio et al. [3], has an extension, still denoted by , such that the measure space is complete. Note that for any , it holds that

Note that the set on the right side is measurable. Since is Polish, it follows from the measurable projection theorem (cf. Theorem 8.3.2 in Aubin and Frankowska [4]), that is -measurable.

Define functions by

For any it holds that

and thus it follows from the measurable projection theorem that is -measurable. Similarly,

and thus is -measurable.

Next, note that and are also -measurable, because measurability is preserved under and .

For any it holds that

and thus it follows from the measurable projection theorem that is -measurable. Similarly,

and thus is -measurable.

(ii) For each , it follows from the measurability of and that and are in . Since is Polish and is a complete finite measure, it follows from Aumann’s measurable selection theorem (see, e.g. Theorem 18.26 in Aliprantis and Border [2]) that -measurable selections exist such that and for -almost all .

8.1.5 Proof of Proposition 3.6.

If , then for any it holds that

Observe that . Hence, for any , there exists with , such that for -almost all . By Lemma 3.5(iv), there exists a -measurable mapping such that

for -almost all . For , consider the set

Note that for all . Then and thus . Hence, for each , there exists a such that , and . Let be the restriction of on . Note that is also -measurable.

For each , let

and define the distribution

Then is a primal feasible solution, and

Since can be chosen arbitrarily large, it follows that . \Halmos

8.1.6 Proof of Lemma 3.8

(i) For any , is the infimum of nondecreasing functions. Thus is nondecreasing for all . Also, for any , is the infimum of continuous functions. Thus is upper-semi-continuous for all . Consider any sequence such that as . Since , it holds that there is a set such that and for all . Then it follows from being nondecreasing that for all and all . Let . Then , and , and for all and all . Since is the infimum of affine functions of , and for all and all , and for all and all , it follows that is concave on for all .

For the second part, consider any , any , and any , such that .

Consider any such that .

If no such exists, then it follows immediately that .

Otherwise, consider any such that .

Since it follows that .

Thus, and

That is, every such that satisfies , and thus .

For the third part, consider any and any such that . For any , consider any such that for . It follows that

Also, it follows from the definition of and that .

(ii) It follows from the definition of that for all it holds that

Also, for every that satisfies for some , it holds that

Combining the two inequalities above yields that

(iii) Consider any and any . For any , choose any such that for . Then

Similarly, . It follows that

Then it follows from the definitions of and that

Since , there is a such that is finite-valued and concave on , and the left and right derivatives exist for all . Setting and letting , it follows that

Similarly, setting and letting in the inequality above, it follows that

8.1.7 Proof of Lemma 3.9.

(i) It follows from Definition 3.3 of that for all and is finite for all , and thus for all and is finite for all .

(ii) It follows from Lemma 3.8(i) that is the sum of a linear function and an (extended real-valued) convex function on . Thus is convex.

(iii) Note that (i) and (ii) imply that is continuous everywhere except possibly at . We show that is lower semi-continuous at . Consider any sequence such that . Since is upper-semi-continuous for all , it follows that . Also, for all and . Thus for all . Hence it follows from Fatou’s lemma that

Since , it follows that , and thus is lower semi-continuous.

(iv) Since , it follows that as .

8.1.8 Proof of Corollary 3.16.

(i) Recall from Lemma 3.8(i) that there is a set such that , and for all and all . Note that if is upper-semi-continuous, and bounded subsets of are totally bounded, then for , it holds that and in Lemma 3.5(iii) are nonempty for all and all . Next we show that and are nonincreasing. Consider any and any such that . Consider any such that for . Then it follows as in the proof of Lemma 3.8(i) that . Therefore .

Next we show that, for all , it holds that is upper-semi-continuous and is lower semi-continuous at all . Consider any and any sequence such that as and for all , for some . For each and each , consider any . Note that for all . Since bounded subsets of are totally bounded, it is sufficient to consider subsequences of that converge to some . It follows from the upper-semicontinuity of and the continuity of at all that

and thus . Since , it follows that is upper-semi-continuous and is lower semi-continuous at all for all .

Next we show that for all and all , it holds that and . Consider any and any . Consider any for . Then it follows as in the proof of Lemma 3.8(iii) that

Then it follows from the definitions of and that

Setting and letting , it follows from the upper-semicontinuity of that

and hence

Similarly, setting and letting , it follows from the lower-semicontinuity of that

and hence

Next we show that if condition (i)(a) or (i)(b) or (i)(c) holds, then there exists a primal optimal distribution. First suppose that condition (i)(a) holds: there exists a dual minimizer . Since for , it holds that and in Lemma 3.5(iii) are nonempty for all , it follows that there exists -measurable mappings such that

for -almost all . As in the proof of Lemma 3.10, it follows from the first-order optimality conditions and that

| (51) | ||||

Let be such that

Let

| (52) |

Then

and thus is primal feasible. Also,

Therefore is primal optimal.

Suppose that condition (i)(b) holds: is the unique dual minimizer, , and

Then it follows in the same way as in the proof for condition (i)(a) that there exists a primal optimal distribution.

Suppose that condition (i)(c) holds: is the unique dual minimizer, is nonempty, and

Then, for , the sets in Lemma 3.5(iii) are given by

and are non-empty for -almost all . Thus there exists a -measurable mapping such that for -almost all . Let . Then

and thus is primal feasible. Furthermore,

and thus is primal optimal. Therefore we have shown that if condition (i)(a) or (i)(b) or (i)(c) holds, then there exists a primal optimal distribution.

Next we show that if there exists a primal optimal distribution, then condition (i)(a) or (i)(b) or (i)(c) holds. Consider any primal feasible distribution . Let denote the corresponding optimal solution in definition (1) of Wasserstein distance , and let denote the corresponding conditional distribution of given . Since is feasible, it holds that . Lemma 3.9(v) established existence of a dual minimizer . Note that

For to be primal optimal, it must hold that . Since , , and for all , it follows that all of the following must hold for to be primal optimal:

-

(A)

.

-

(B)

for -almost all , which in turn implies that for -almost all , and the conditional distribution should be supported on for -almost all .

Next we show that these conditions imply that condition (i)(a) or (i)(b) or (i)(c) holds. Since there is a dual minimizer , one of the following conditions must hold:

-

1∘