Allocation Schemes of Resources with Downgrading

Abstract.

We consider a server with large capacity delivering video files encoded in various resolutions. We assume that the system is under saturation in the sense that the total demand exceeds the server capacity . In such case, requests may be rejected. For the policies considered in this paper, instead of rejecting a video request, it is downgraded. When the occupancy of the server is above some value , the server delivers the video at a minimal bit rate. The quantity is the bit rate adaptation threshold. For these policies, request blocking is thus replaced with bit rate adaptation. Under the assumptions of Poisson request arrivals and exponential service times, we show that, by rescaling the system, a process associated with the occupancy of the server converges to some limiting process whose invariant distribution is computed explicitly. This allows us to derive an asymptotic expression of the key performance measure of such a policy, namely the equilibrium probability that a request is transmitted at requested bitrate. Numerical applications of these results are presented.

Key words and phrases:

Resource Allocation; Scaling Methods; Loss Systems2010 Mathematics Subject Classification:

60K25; 60K30 (primary), and 90B18 (secondary)

1. Introduction

Video streaming applications have become over the past few years the dominant applications in the Internet and generate the prevalent part of traffic in today’s IP networks; see for instance Guillemin et al. [10] for an illustration of the application breakdown in a commercial IP backbone network. Video files are currently downloaded by customers from large data centers, like Google’s data centers for YouTube files. In the future, it is very likely that video files will be delivered by smaller data centers located closer to end users, for instance cache servers disseminated in a national network. It is worth noting that as shown in Guillemin et al. [11], caching is a very efficient solution for YouTube traffic. While this solution can improve performances by reducing delays, the limited capacity of those servers in terms of bandwidth and computing can cause overload.

One possibility to reduce overload is to use bit rate adaptation. Video files can indeed be encoded at various bit rates (e.g, small and high definition video). If a node cannot serve a file at a high bit rate, then the video can be transmitted at a smaller rate. It is remarkable that video bit rate adaptation has become very popular in the past few years with the specification of MPEG-DASH standard where it is possible to downgrade the quality of a given transmission, see Schwarz et al. [17], Sieber et al. [18], Añorga et al. [1], Vadlakonda et al. [21] and Fricker et al. [7]. Adaptive streaming is also frequently used in mobile networks where bandwidth is highly varying. In this paper, we investigate the effect of bit rate adaptation in a node under saturation.

Downgrading Policy

We assume that customers request video files encoded at various rates, say, for , with . Jobs of class require bit rate . The total capacity of the communication link is . If is the state of the network at some moment, with being the number of class jobs, the quantity has to be less than . The quantity is defined as the occupancy of the link. The algorithm has a parameter and works as follows: If there is an arrival of a job of class ,

-

—

if then the job is accepted;

-

—

if then the job is accepted but as a class job, i.e. it has an allocated bit rate of and service rate ;

-

—

if , the job is rejected.

For , jobs of class arrive according to a Poisson process with rate and have an exponentially distributed transmission time with rate . Additionally, it is assumed that

A Scaling Approach

To study this allocation scheme, a scaling approach is used. It is assumed that the server capacity is very large, namely scaled up by a factor . The bit rate adaptation threshold and the request arrival rates are scaled up accordingly, i.e.

| (1) |

Performances of the algorithm. Our main result shows that, for the downgrading policy and if is chosen conveniently, then

-

(1)

the equilibrium probability of rejecting a job converges to as goes to infinity;

- (2)

The above formula gives an explicit expression of the success rate of this allocation mechanism. The quantity , the probability of downgrading requests, can be seen as the “price” of the algorithm to avoid rejecting jobs.

The scaling (1) has been introduced by Kelly to study loss networks. See Kelly [14]. The transient behavior of these networks under this scaling has been analyzed by Hunt and Kurtz [12]. This last reference provides essentially a framework to establish convenient convergence theorems involving stochastic averaging principles. This line of research has been developed in the 1990’s to study uncontrolled loss networks where a request is rejected as soon as its demand cannot be accepted.

When the demand can be adapted to the state of the network, for controlled loss networks, several (scarce) examples have been also analyzed during that period of time. One can mention Bean et al. [4, 5], Zachary and Ziedins [22] and Zachary [23] for example. Our model can be seen as a “controlled” loss networks instead of a pure loss network. Controlled loss networks may have mechanisms such as trunk reservation or may allocate requests according to some complicated schemes depending on the state of the network. In our case, the capacity requirements of requests are modified when the network is in a “congested” state.

Contrary to classical uncontrolled loss networks, as it will be seen, the Markov process associated to the evolution of the vector of the number of jobs for each class is not reversible. Additionally, the invariant distribution of this process does not seem to have a closed form expression. Kelly’s approach [13] is based on an optimization problem, it cannot be used in our case to get an asymptotic expression of some characteristics at equilibrium. For this reason, the equilibrium behavior of these policies is investigated in a two step process:

-

(1)

Transient Analysis. We investigate the asymptotic behavior of some characteristics of the process on a finite time interval when the scaling parameter goes to infinity.

-

(2)

Equilibrium. The stability properties of the limiting process are analyzed, we prove that the equilibrium of the system for a fixed converges to the equilibrium of the limiting process.

For our model, the transient analysis involves the explicit representation of the invariant distribution of a specific class of Markov processes. It is obtained with complex analysis arguments. As it will be seen, this representation plays an important role in the analysis of the asymptotic behavior at equilibrium.

It should be noted that related models have recently been introduced to investigate resource allocation in a cloud computing environment where the nodes receive requests of several types of resources. We believe that this domain will receive a renewed attention in the coming years. See Stolyar [19, 20] and Fricker et al. [8] for example. In some way one could say that the loss networks are back and this is also a motivation of this paper to shed some light on the methods that can be used to study these systems.

Outline of the paper

We consider a system in overload. Because of bit rate adaptation, requests may be downgraded but not systematically rejected as in a pure loss system. As it will be seen, the stability properties of this algorithm are linked to the behavior of a Markov process associated to the occupation of the link. Under exponential assumptions for inter-arrival and service times, this process turns out to be, after rescaling by a large parameter , a bilateral random walk instead of a reflected random walk as in the case of loss networks. Using complex analysis methods, an explicit expression of the invariant distribution of this random walk is obtained. With this result, the asymptotic expression of the probability that, at equilibrium, a job is transmitted at its requested rate (and therefore does not experience a bit rate adaptation) is derived.

This paper is organized as follows: In Section 2, we present the model used to study the network under some saturation condition. Convergence results when the scaling factor tends to infinity are proved in Section 3. The invariant distribution of a limiting process associated to the occupation of the link is computed in Section 4 by means of complex analysis techniques. Applications are discussed in Section 5.

Acknowledgments

The authors are very grateful to an anonymous referee for pointing out a gap in the proof of Theorem 2 in the first version of this work.

2. Model description

One considers a service system where classes of requests arrive at a server with bandwidth/capacity . Requests of class , , arrive according to a Poisson process with rate . A class request has a bandwidth requirement of units for a duration of time which is exponentially distributed with parameter . For the systems investigated in this paper, there is no buffering, requests have to be processed at their arrival otherwise they are rejected. Without any flexibility on the resource allocation, this is a classical loss network with one link. See Kelly [14] for example.

This paper investigates allocation schemes which consist of reducing the bandwidth allocation of arriving requests to a minimal value when the link has a high level of congestion. In other words the service is downgraded for new requests arriving during a saturation phase. If the system is correctly designed, it will reduce significantly the fraction of rejected transmissions and, hopefully, few jobs will in fact experience downgrading.

2.1. Downgrading policy

We introduce , the parameter will indicate the level of congestion of the link. It is assumed that the vector of integers is such that . The condition is used to simplify the presentation of the results and to avoid problems of irreducibility in particular but this is not essential.

If the network is in state and if the occupancy is less than , then any arriving request is accepted. If the occupancy is between and , it is accepted but with a minimal allocation, as a class job. Finally it is rejected if the link is fully occupied, i.e. . It is assumed that , for , i.e. class 1 jobs are served with the smallest service rate.

Mathematically, the stochastic model is close to a loss network with the restriction that a job may change its requirements depending on the state of the network. This is a controlled loss network, see Zachary and Ziedins [23]. It does not seem that, like in uncontrolled loss networks, the associated Markov process giving the evolution of the vector has reversibility properties, or that its invariant distribution has a product form expression. Related schemes with product form are trunk reservation policies for which requests of a subset of classes are systematically rejected when the level of congestion of the link is above some threshold. See Bean et al. [4] and Zachary and Ziedins [22] for example. Concerning controlled loss networks, mathematical results are more scarce. One can mention networks where jobs requiring congested links are redirected to less loaded links. Several mathematical approximations have been proposed to study these models. See the surveys Kelly [14] and Zachary and Ziedins [23]. In our model, in the language of loss networks, the control is on the change of capacity requirements instead of a change of link.

2.2. Scaling Regime

The invariant distribution being, in general, not known, a scaling approach is used. The network is investigated under Kelly’s regime, i.e. under heavy traffic regime with a scaling factor . It has been introduced in Kelly [13] to study the equilibrium of uncontrolled networks. The arrival rates are scaled by : is replaced by as well as the capacity by and the threshold by which are such that

| (2) |

for .

Definition 1.

For and , denotes the number of class jobs at time in this system and .

It will be assumed that the system is overloaded when the jobs have their initial bandwidth requirements

| () |

with and , . The first condition gives that, without any change on the bandwidth requirement of jobs, the system will reject jobs. The second condition implies that the network could accommodate all jobs without losses (with high probability) if all of them would require the reduced bit rate and service rate .

It should be noted that, from the point of view of the design of algorithms, the constant has to be defined. If one takes then,

| () | |||

| () |

hold.

If , it is not difficult to see that the system is equivalent to a classical underloaded loss network with one link and multiple classes of jobs. There is, of course, no need to use downgrading policies since the system can accommodate incoming requests without any loss when is large. See Kelly [14] or Section 7 of Chapter 6 of Robert [15] for example.

3. Scaling Results

In this section, we prove convergence results when the scaling parameter goes to infinity. These results are obtained by studying the asymptotic behavior of the occupation of the link around ,

| (3) |

In the context of loss networks, the analogue of such quantity is the number of empty places. The following proposition shows that, for the downgrading policy, the boundary does not play a role after some time if Condition () holds.

Proposition 1.

Proof.

Define

where is the process of the number of jobs of an independent queue with , service rate and arrival rate and, for ,

where is a sequence of i.i.d. exponentially distributed random variables with rate .The quantity is the number of initial class jobs still present at time . Using Theorem 6.13 of Robert [15], one gets the convergence in distribution

and, consequently,

| (4) |

Since for ,

by Condition (). Note that the asymptotic occupancy, when is large, remains below the initial occupancy.

If and such that , let

then, on the event , the downgrading policy gives that the identity in distribution

| (5) |

holds. Condition () gives the existence of such that

Convergence (4) shows that the sequence converges in distribution to .

We are now investigating the asymptotic behavior of the process defined by Relation (3). The variable indicates if the network is operating in saturation at time , , or not, . In pure loss networks, when is large, up to a change of time scale, the analogue of this process, the process of the number of empty places converges to a reflected random walk in . In our case, as it will be seen, the corresponding process is in fact a random walk on .

Definition 2.

For , let be the Markov process on whose -matrix is defined by, for and ,

| (6) |

with .

The following proposition summarizes the stability properties of the Markov process .

Proposition 2.

If , then the Markov process is ergodic if with

| (7) |

denotes the corresponding invariant distribution.

Proof.

The Markov process on behaves like a random walk on each of the two half-lines and . Definition (7) implies that if , then the drift of the random walk is positive when in and negative when in . This property implies the ergodicity of the Markov process by using the Lyapounov function , for example. See Corollary 8.7 of Robert [15] for example. ∎

One now extends the expression for the values . This will be helpful to describe the asymptotic dynamic of the system. See Theorem 1 further.

Definition 3.

One denotes , the Dirac measure at when , with

and if , with

Stochastic Evolution Equations

For , denote by a Poisson process on with rate and an i.i.d. sequence of such processes. All Poisson processes are assumed to be independent. Classically, the process can be seen as the unique solution to the following stochastic differential equations (SDE),

| (8) |

with initial condition such that .

Theorem 1 (Limiting Dynamical System).

Under Condition (), if the initial conditions are such that and

then there exists continuous process such that the convergence in distribution

| (9) |

holds for any function with finite support on . Furthermore, there exists such that satisfies the differential equations

| (10) |

where , for , is the distribution of Proposition 2 and Definition 3.

It should be noted that, since the convergence holds for the convergence in distribution of processes, the limit is a priori a random process.

Proof.

By using the same method as Hunt and Kurtz [12], one gets the analogue of Theorem 3 of this reference. Fix such that , from Proposition 1, one gets that the existence of such that

which implies that the boundary condition in the evolution equations (8) can be removed. Consequently, only the boundary condition of at plays a role which gives Relation (10) as in Hunt and Kurtz [12]. Note that, contrary to the general situation described in this reference, we have indeed a convergence in distribution because, for any , has exactly one invariant distribution (which may be a Dirac mass at infinity) by Proposition 2. See Conjecture 5 of Hunt and Kurtz [12]. ∎

The following proposition gives a characterization of the equilibrium point of the dynamical system .

Proposition 3 (Fixed Point).

Under Conditions () and (), there exists a unique equilibrium point of the process defined by Equation (9) given by

| (11) |

where

| (12) |

with . The process is ergodic in this case.

Proof.

Assume that there exists an equilibrium point of defined by Equation (9), it is also an equilibrium point of the dynamical system defined by Equation (10), then

| (13) |

with . One gets

| (14) |

We now show that the vector is on the boundary, i.e.

| (15) |

If we assume that

from Theorem 1 and the definition of , we know that, for the convergence of processes, the following relation holds

For , and ,

By using again Theorem 1 and the fact that is an equilibrium point of the dynamical system, we have, for the convergence in distribution

The left-hand side of the above expression can be arbitrarily close to when is large. By convergence of the sequence to , one gets that, for the convergence in distribution, the relation

holds for , which implies that . Thus Relation (15) holds. Finally, Relations (13) and (15) give Relation (11). One concludes therefore that , the associated process is necessarily ergodic by Proposition 2 and Relations (14).

Convergence of Invariant Distributions

In this section our main result establishes the convergence of the invariant distribution of the process as gets large. This will give in particular the convergence with respect to of the probability of not downgrading a request at equilibrium.

Lemma 1.

If the process is the process at equilibrium then, for any and ,

Proof.

Let be the process with initial state empty, then one can easily construct a coupling such that the relation

holds almost surely, where is the queue associated to class requests. One deduces that,

where is a Poisson random variable with parameter and is the stochastic ordering of random variables. One can therefore construct another coupling such that

where is a stationary version of the queue associated to class requests. The lemma is then a consequence of the following convergence in distribution of processes,

for , see Theorem 6.13 pp. 159 of Robert [15] for example. ∎

Definition 4.

Let be the dynamical system on satisfying

| (16) |

with

Lemma 2.

If and if there exists an instant such that for then and coincide on the time interval , where is the solution of Equations (10) with .

Proof.

The next proposition investigates the stability Properties of .

Proposition 4.

Let be the hyperplane

if then for all and is converging exponentially fast to defined in Proposition 3.

Proof.

It is easily checked that

so that if , then the function is constant and equal to , hence for all .

For ,

with

In matrix form, if , it can be expressed as

| (17) |

with and with

If is an eigenvector for the eigenvalue of , then

hence, is an eigenvalue if and only if it is a solution of the equation

If is the number of distinct values of , , such that , then the above equation shows that an eigenvalue is a zero of a polynomial of degree at most . Using Conditions (), it is easy to check that the relation holds. In particular is not an eigenvalue and, consequently is invertible. Due to the poles of at the , and the relations and for , one has already negative solutions of the equation . All eigenvalues of are thus negative, consequently, converges to . (See Corollary 2 of Chapter 25 of Arnol’d [2] for example.)

Equation (17) can be solved as

Therefore the function has a limit at infinity given by which is clearly . The proposition is proved. ∎

One can now prove the main result of this section.

Theorem 2.

If is the quantity defined in Proposition 3, then the equilibrium distribution of converges to when goes to infinity.

Proof.

Recall that and let be the invariant distribution of . It is assumed that the distribution of is for the rest of the proof. In particular is a stationary process.

One first proves that converges in distribution to . The boundary condition gives that the sequence of random variables is tight. If is a convergent subsequence to some random variable , by Theorem 1, one gets that, for the convergence in distribution, the relation

holds, where is a solution of Equation (10) with initial point at . Note that is a stationary process, its distribution is invariant under any time shift.

By Lemma 1 one has that the relation , for , holds almost surely on any finite time interval and, by Proposition 1, also holds almost surely on finite time intervals.

Assume that holds. The ODEs defining the limiting dynamical system are given by

as long as the condition holds, hence on the corresponding time interval, one has

so that

Since , there exists some such that .

Hence, by stationarity in distribution of , one can shift time at and assume that . On this event

| (18) |

Similarly, since for all ,

| (19) | |||

and the last quantity is independent of . Relations (18) and (19) show that and, by Equations (10) and (16), they also hold for in a small neighborhood of independent of so that for . Consequently, the dynamical system never leaves . Lemma 2 shows that the two dynamical systems and (with ) coincide. Hence, on one hand is a stationary process and, on the other hand, it is a dynamical system converging to , one deduces that it is constant and equal to . We have thus proved that the sequence converges in distribution to .

Using again Theorem 1, one gets that, for the convergence in distribution,

holds for any function with finite support on . By using the stationarity of and Lebesgue’s Theorem, one obtains

The theorem is proved. ∎

Since a job arriving at time is not downgraded if , one obtains the following corollary.

Corollary 1.

As goes to infinity, the probability that, at equilibrium, a job is not downgraded in this allocation scheme is converging to defined in Proposition 11,

4. Invariant Distribution

We assume in this section that , as defined in Proposition 2, so that is an ergodic Markov process. The goal of this section is to derive an explicit expression of the invariant distribution on of . At the same time, Proposition 5 below gives the required argument to complete the proof of Proposition 3 on the characterization of the fixed point of the dynamical system.

4.1. Functional Equation

In the following we denote by a random variable with distribution .

For , we will use the notation

For sake of simplicity, we will use and .

Lemma 3.

With the notation

the random variable is such that

| (20) |

where and are polynomials defined by

| (21) |

Proof.

Proposition 5.

Note that the right-hand side of the last relation is precisely of Relation (12) which is the result necessary to complete the proof of Proposition 3.

Proof.

With the same notations as before, from Relation (20),

holds for , with . By definition of and ,

Since is a zero of and , this gives the relation

Using the expression of , with some algebra, one gets

The proposition is proved. ∎

Relation (20) is valid on the unit circle, however the function (resp. ) is defined on (resp. ). This can then be expressed as a Wiener-Hopf factorization problem analogous to the one used in the analysis of reflected random walks on . This is used in the analysis of the queue, see Chapter VIII of Asmussen [3] or Chapter 3 of Robert [15] for example. In a functional context, this is a special case of a Riemann’s problem, see Gakhov [9]. In our case, this is a random walk in , with a drift depending on the half-space where it is located. The first (resp. second) condition in the definition of the set in Definition (7) implies that the drift of the random walk in (resp. in ) is positive (resp. negative).

The first step in the analysis of Equation (20) is to determine the locations of the zeros of and . This is the purpose of the following lemma.

Lemma 4.

(Location of the Zeros of and ) Let be in .

-

(i)

Polynomial has exactly two positive real roots and . There are roots in and roots whose modulus are strictly greater than .

-

(ii)

Polynomial has exactly two positive real roots and . The remaining roots have a modulus strictly smaller than .

Proof.

One first notes that is a polynomial with the same form as the defined by Equation (13) in Bean et al. [4] (with , and ). The roots of are exactly the roots of . Lemma 2.2 of Bean et al. [4] gives assertion (i) of our lemma.

The proof of assertion (ii) uses an adaptation of the argument for the proof of Lemma 2.2 of Bean et al. [4]. Define the function . Recall that is a polynomial with degree . There are exactly two real positive roots for . Indeed, and it is easily checked that is strictly concave with

since , by the second condition in Definition (7). Hence has a real zero greater than .

Let be fixed, note that . Define

so that .

Fix some . By expressing these functions in terms of real and imaginary parts,

one gets

| (24) |

with

Cauchy-Schwarz’s Inequality gives the relation

since for , . Thus,

Since , can be chosen so that . From the above relation and Equation (24), one gets that for , the relation

holds. By Rouché’s theorem, one obtains that, for any , has exactly roots in . One concludes that has exactly roots in . It is easily checked that if and then the real part of is positive, hence cannot be a root of the polynomial . Consequently, has exactly roots in . The lemma is proved. ∎

Definition 5.

For , denote by the set of the zeros of different from .

Define

with and the same notations as before. By definition, function is holomorphic in and and, from Relation (20), is continuous on . The analytic continuation theorem, Theorem 16.8 of Rudin [16] for example, gives that is holomorphic on . For ,

since the cardinality of (resp. ) is (resp. ), the holomorphic function is therefore bounded on . By Liouville’s theorem, is constant, equal to . Therefore

| (25) |

Recall that is a generating function, in particular . Plugging the previous expressions for and in , one gets the relation

hence, using equation (21),

where is introduced in Definition 4. Note that is positive. We can now state the main result of this section.

Proposition 6 (Invariant Measure).

Proof.

Note that, for ,

For ,

Since by Lemma 4, has the following partial fraction decomposition

Denote

then

One concludes by using the expression of obtained before. ∎

4.2. Some Moments of

Using the probability generating function of from Equation (25), one can derive an explicit expression of the mean, the variance and the skewness of such distribution. The skewness of a random variable is a measure of the asymmetry of the distribution of ,

See Doane and Seward [6] for example.

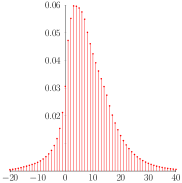

Proposition 7.

The proof is straightforward, modulo some tedious calculations of the successive derivatives of evaluated at . Figure 1 shows that the distribution of is significantly asymmetrical. For this example , and .

5. Applications

Comparison with a Pure Loss System

In this case, a request which cannot be accommodated is rejected right away. Recall that, with probability , our algorithm does not reject any request. The purpose of this section is to discuss the price of such a policy. Intuitively, at equilibrium the probability of accepting a job at requested capacity in a pure loss system is greater that the corresponding quantity for the downgrading algorithm. See Proposition 8 below. A further question is to assess the impact of such policy, i.e. the order of magnitude of the difference .

Under the same assumptions about the arrivals and under the condition

| () |

with , then, as gets large, the equilibrium probability that a request of class is accepted in the pure loss system is converging to , where is the unique solution of the equation

| (26) |

see Kelly [13]. Consequently, the asymptotic load of accepted requests is given by

Under the downgrading policy, the equilibrium probability that a job is accepted without degradation is given by , the asymptotic load of requests accepted without degradation is

for . Note that, when the service rates are constant equal to , then (resp. ) is the asymptotic throughput of accepted requests (resp. of non-degraded requests).

The following proposition establishes the intuitive property that a pure loss system has better performances in terms of acceptance.

Proposition 8.

For , the relation holds.

Proof.

The representation of these quantities gives that the relation to prove is equivalent to the inequality

By using the fact that and Equation (26), it is enough to show that the quantity

is positive. But this is clear since

and the terms of both series of the right hand side of this relation are non-negative due to the fact that . ∎

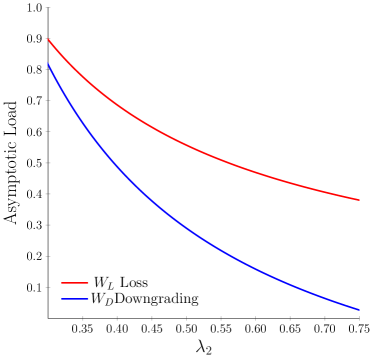

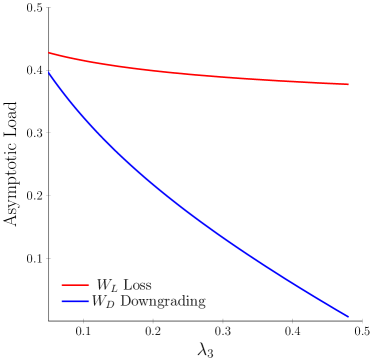

Numerical experiments have been done to estimate the difference , see Figure 2. The general conclusion is that, at moderate load under Condition (), the downgrading algorithm performs quite well with only a small fraction of downgraded jobs. As it can be seen this is not anymore true for high load where, as expected, most of requests are downgraded but nobody is lost.

conditions:

conditions:

Application to Video Transmission

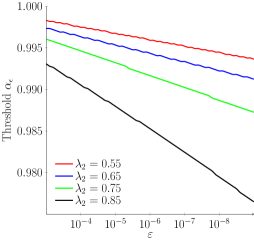

We consider now a link with large bandwidth, Gbps, in charge of video streaming. Requests that cannot be immediately served are lost. Video transmission is offered in two standard qualities, namely, Low Quality (LQ) and High Quality (HQ). From Añorga et al. [1], the bandwidth requirement for YouTube’s videos at 240p is 1485 Kbps, and for 720p it is 2737.27 Kbps.

Using the values above, after renormalization, one takes , and , . Jobs arrive at rate in this system asking for HQ transmission, but clients accept to watch the video in LQ. In particular . Service times are assumed to be the same for both qualities and taken as the unity, . Condition () is satisfied when

We define , with . The quantity is defined as the largest value of such that the loss probability of a job is less than . With the notations of Section 4, we write

Note that this is an approximation, since the variable corresponds to the case when the scaling parameter goes to infinity.

By using the explicit expression of the distribution of of Proposition 6, Figure 3 plots the threshold that ensures a loss rate less than as a function of , for several values of . In the numerical example, taking is sufficient to get a loss probability less than .

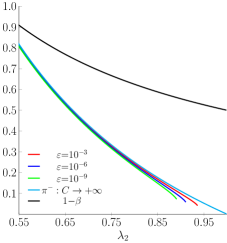

Now let be the value of defined by Corollary 1 for . Recall that is the asymptotic equilibrium probability that a job is not downgraded is given by Relation (12),

For comparison, is defined as the corresponding acceptance probability when no control is used in the system. We show in Figure 4 the relation between these quantities and the workload , for fixed loss rates of , and . We have , see Robert [15, Proposition 6.19]. The difference can be seen as the fraction of jobs which are downgraded for our policy but lost in the uncontrolled policy. Intuitively it can be seen as the price of not rejecting any job. Notice also that the curves plotting for , , are close and that is larger than . One remarks nevertheless that, for high loads, the system cannot hold these demands, because our policy is no longer effective.

References

- [1] Javier Añorga, Saioa Arrizabalaga, Beatriz Sedano, Maykel Alonso-Arce, and Jaizki Mendizabal. YouTube’s DASH implementation analysis. In Proceedings of the 19th International Conference on Communications, volume 50 of Recent Advances in Electrical Engineering Series, pages 61–66, Zakynthos, Ionion, Greece, 06 2015.

- [2] Vladimir I. Arnol’d. Ordinary differential equations. Springer-Verlag, Berlin, 1992. Translated from the third Russian edition by Roger Cooke.

- [3] Søren Asmussen. Applied probability and queues, volume 51 of Applications of Mathematics. Springer-Verlag, New York, second edition, 2003.

- [4] N. G. Bean, R. J. Gibbens, and S. Zachary. Asymptotic analysis of single resource loss systems in heavy traffic, with applications to integrated networks. Advances in Applied Probability, 27(1):273–292, 1995.

- [5] N. G. Bean, R. J. Gibbens, and S. Zachary. Dynamic and equilibrium behavior of controlled loss networks. Annals of Applied Probability, 7(4):873–885, 1997.

- [6] David P. Doane and Lori E. Seward. Measuring skewness: A forgotten statistic? Journal of Statistics Education, 19(2):1–18, 2011.

- [7] Christine Fricker, Fabrice Guillemin, Philippe Robert, and Guiherme Thompson. Analysis of downgrading for resource allocation. SIGMETRICS Performance Evaluation Review, 44(2):24–26, September 2016.

- [8] Christine Fricker, Fabrice Guillemin, Philippe Robert, and Guilherme Thompson. Analysis of an offloading scheme for data centers in the framework of Fog computing. ACM Transactions on Modeling and Performance Evaluation of Computing System, 1(4):16:1–12:18, 2016.

- [9] F. D. Gakhov. Boundary value problems. Dover Publications Inc., New York, 1990. Translated from the Russian, Reprint of the 1966 translation.

- [10] Fabrice Guillemin, Thierry Houdoin, and Stéphanie Moteau. Volatility of YouTube content in Orange networks and consequences. In Proceedings of IEEE International Conference on Communications, ICC 2013, Budapest, Hungary, June 9-13, 2013, pages 2381–2385, 2013.

- [11] Fabrice Guillemin, Bruno Kauffmann, Stéphanie Moteau, and Alain Simonian. Experimental analysis of caching efficiency for YouTube traffic in an ISP network. In 25th International Teletraffic Congress, ITC 2013, Shanghai, China, September 10-12, 2013, pages 1–9, 2013.

- [12] P.J. Hunt and T.G Kurtz. Large loss networks. Stochastic Processes and their Applications, 53:363–378, 1994.

- [13] F.P. Kelly. Blocking probabilities in large circuit-switched networks. Advances in Applied Probability, 18:473–505, 1986.

- [14] F.P. Kelly. Loss networks. Annals of Applied Probability, 1(3):319–378, 1991.

- [15] Philippe Robert. Stochastic Networks and Queues, volume 52 of Stochastic Modelling and Applied Probability Series. Springer, New-York, June 2003.

- [16] Walter Rudin. Real and complex analysis. McGraw-Hill Book Co., New York, third edition, 1987.

- [17] H. Schwarz, D. Marpe, and T. Wiegand. Overview of the scalable video coding extension of the H.264/AVC standard. IEEE Transactions on Circuits and Systems for Video Technology, 17(9):1103–1120, September 2007.

- [18] Christian Sieber, Tobias Hoßfeld, Thomas Zinner, Phuoc Tran-Gia, and Christian Timmerer. Implementation and user-centric comparison of a novel adaptation logic for DASH with SVC. In IM’13, pages 1318–1323, 2013.

- [19] Alexander L. Stolyar. An infinite server system with general packing constraints. Operations Research, 61(5):1200–1217, 2013.

- [20] Alexander L. Stolyar. Pull-based load distribution in large-scale heterogeneous service systems. Queueing Systems. Theory and Applications, 80(4):341–361, 2015.

- [21] S. Vadlakonda, A. Chotai, B.D. Ha, A. Asthana, and S. Shaffer. System and method for dynamically upgrading / downgrading a conference session, April 6 2010. US Patent 7,694,002.

- [22] Stan Zachary and Ilze Ziedins. A refinement of the Hunt-Kurtz theory of large loss networks, with an application to virtual partitioning. The Annals of Applied Probability, 12(1):1–22, 02 2002.

- [23] Stan Zachary and Ilze Ziedins. Loss networks. In Richard J. Boucherie and Nico M. van Dijk, editors, Queueing Networks, volume 154 of International Series in Operations Research & Management Science, pages 701–728. Springer US, 2011.