Deterministic Income with Deterministic and Stochastic Interest Rates

Abstract

We consider an individual or household endowed with an initial capital and an income, modeled as a deterministic process with a continuous drift rate. At first, we model the discounting rate as the price of a zero-coupon bond at zero under the assumption of a short rate evolving as an Ornstein-Uhlenbeck process. Then, a geometric Brownian motion as the preference function and an Ornstein-Uhlenbeck process as the short rate are taken into consideration. It is assumed that the primal interest of the economic agent is to maximise the cumulated value of (expected) discounted consumption from a given time up to a finite deterministic time horizon or, in a stochastic setting, infinite time horizon. We find an explicit expression for the value function and for the optimal strategy in the first two cases. In the third case, we have to apply the viscosity ansatz.

Key words: optimal control, Hamilton–Jacobi–Bellman equation, Vasicek model, geometric Brownian motion, interest rate

2010 Mathematical Subject Classification: Primary

93B05

Secondary 49L20, 49L25

1 Introduction

In the recent years, there appeared a big range of papers considering dividends, consumption, capital injections, where the return functions were defined as an expected discounted value with a constant positive discounting or preference rate. Confer for instance Schmidli [10], Albrecher and Thonhauser [1], Cox and Huang [6], Eisenberg [7]. It is not our target to make a review of the existing literature. Therefore, we just refer to the references in the above publications.

In the mentioned examples, the discounting rate is a constant and does not depend on time, which makes it to a preference rate, describing investment preferences of an agent in the considered model. Indeed, it is a usual practice that economic models make an assumption of a constant and strictly positive preference rate, which implies a “sacrifice” of far future for present and/or near future. This fact leads to a distortion in representation of the economic processes, to say nothing about the unrealistic assumption of market idleness in the considered time period.

One of the possible extensions of such a model is the introduction of a stochastic interest rate. The stochastisation of the model can be interpreted in two ways. The first way is to see the stochastic rate as a possibility of a macroeconomic market changing, which would influence the consumption behaviour of a sole economic agent. A suitable example provides the recent US “Fiscal Cliff”, which is still affecting the pocket of every individual and business in the US. The second way is to interpret the stochastics in the interest rate as uncertainty about changes in individual preferences of the economic agent. For example, a cold summer can influence the earnings of a farmer family essentially. This can lead to a considerable change in the “investment behaviour”: money today can become much more preferable to money tomorrow in the years of famine compared to the years of plenty.

But what happens if we introduce a stochastic interest rate? In actuarial mathematics, the surplus of an insurance entity is usually modeled via a stochastic process due to the uncertainty about future system development: stochastic models approximate the real processes much better than deterministic ones. Adding a stochastic interest rate into a model with stochastic surplus would complicate the optimization problem a lot, even if we assume the both processes to be independent. In contrast, deterministic modeling enjoys a much greater ease of computability. Thus, to start with, in the first part of the paper we model the surplus as a deterministic process with a continuous drift function. Further, it is assumed that the discounting function is given by the price of a pure-discount bond at time zero under the spot rate evolving due to the Vasicek model. For detailed description of the bond price theory see, for instance, Brigo and Mercurio [5, p. 58].

In [8] Eisenberg, Grandits and Thonhauser considered the problem of consumption maximization for an arbitrary drift function under a constant preference rate. There, it was possible to establish an algorithm for determination of the value function. In the present problem, we use a similar principle: calculate the value function and the optimal strategy in reverse order, starting at the maturity . At first, we consider the case of restricted consumption payments and then look at the unrestricted case. Since, the case with restricted payments turned out to be more complicated, we illustrate it with an example. In a remark, we discuss the problem for an arbitrary deterministic drift function.

In the second part of the paper we model the surplus as a deterministic process with constant drift. But the discounting function is now a stochastic process. At first, we consider the case where the consumption of the considered economic agent is linked to a stock whose price follows a geometric Brownian motion. Then, we model the short rate as an Ornstein-Uhlenbeck process with special parameters. Just in the first case, it was possible to determine the optimal strategy and the value function. In the second case we had to apply the viscosity ansatz. Also, in the second case we consider just the case with restricted consumption rates. The case with unrestricted rates has to be considered separately and will be studied in our future research.

To the best of our knowledge, interest rate theory is an unploughed field in insurance mathematics and can open up a lot of research possibilities. Some of them are mentioned in the concluding remark.

2 Deterministic Preference Function

Consider the surplus process, where the surplus rate is given by a non-negative constant :

Assume, an individual or household consumes goods depending on the price of a zero-coupon bond at time zero. The short rate is a stochastic quantity and is given by a Vasicek model. Our target is to maximise the cumulated value of the discounted consumption from a given time up to a finite deterministic time horizon . We do not allow the consumption to cause the ruin, which means that the endpoint of our journey will be always . The surplus process under the consumption process is

We call a strategy admissible if and for all . The return function corresponding to an admissible strategy is defined as

where and is an Ornstein-Uhlenbeck process with , i.e. fulfils the following integral equation

where is the initial value of the process, , are constants and is a standard Brownian motion. Here, due to Brigo and Mercurio [5] denotes the price at zero of a zero-coupon bond (or pure-discount bond) with maturity . We target to maximize the expected value of discounted consumption.

The HJB equation corresponding to the problem is given by

In Borodin and Salminen [4, p. 525] one finds a closed expression for :

Letting and , we have

| (1) |

Let

| (2) |

Then, the HJB equation becomes

| (3) |

Depending on the parameter choice, the function will have different properties.

2.1 The Properties of

Consider at first the derivative of .

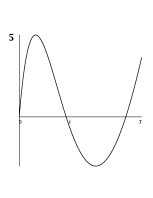

Thus, in order to determine the behaviour of , substitute by and consider the quadratic function . It is clear that is a parabola opened upwards. In particular, has at most zeros and :

| (4) | |||

-

•

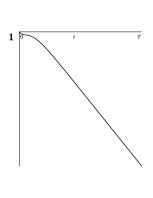

If , then is increasing on .

-

•

If , then we have to consider and with .

Assume, . The following scenarios are possible

-

1.

and . Then, is decreasing on .

-

2.

or . In this case is increasing on .

-

3.

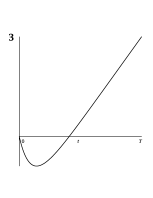

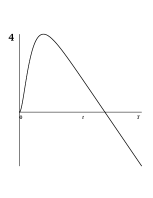

and . Then, is decreasing on and increasing on , where

(5) -

4.

and . Then, is increasing on and decreasing on , where

(6) -

5.

. Then, is increasing on and decreasing on .

The possible development scenarios of are illustrated in Figure 1.

Remark 2.1

In particular, is injective on , and on , so that we can define inverse functions of acting just on the one of the above intervals:

| , | ||

| , | ||

| . |

For the sake of simplicity, we introduce

| (7) | |||

| (8) | |||

| or correspondingly. |

At first, we will consider the case where the payouts are bounded by some positive constant , in the last part we consider the unrestricted case.

3 The Optimal Strategy and the Value Function for the Zero-Bond Discounting

We will consider just the fifth case, where has a maximum and a minimum. The other cases described above can be handled in a similar way.

3.1

Since , the process remains non-negative even if we pay out on the maximal rate up to . Thus, for a given pair we have to compare and . The optimal strategy is then given by

| (9) |

The value function is then given by

| (10) |

In particular, it holds . It is easy to check, that the value function solves the corresponding HJB equation (3), is continuously differentiable with respect to and to . Note, that in all five cases the optimal strategy does not depend on the initial capital .

3.2

Here, the maximal payout boundary exceeds the drift .

Let and be the maximum and the minimum point of correspondingly, defined in (6) and (5).

Note that if it is optimal to wait until and pay out everything there. Obviously, the corresponding function will solve HJB Equation (3).

Assume now , i.e. , see (8), is well-defined.

We construct a candidate strategy applying a backward algorithm on the intervals , , and , if , (7) exists; or on the intervals , , if . W.l.o.g we assume .

Let at first , then, for all . Let for , i.e. we wait until and pay out everything there. The corresponding return function obviously solves HJB Equation (3) on .

For let

yielding the return function

which shows that solves HJB Equation (3). Consider now . The strategy will depend on the value of . Define on

Note that the function is a well-defined, continuously differentiable with respect to and to function. It holds and . For let

and the corresponding return function fulfils

Hence, for the crucial condition in the HJB equation it holds due to the definition of :

showing that solves the HJB equation on .

It remains to consider . There, for every it holds . Let and the corresponding return function on :

It is easy to see that the function

| (11) |

is continuously differentiable with respect to and to .

Proposition 3.1

Proof.

Since the proof methods are well-known, we just refer to, for example, Fleming and Soner [9]. ∎

Next, we will consider the case with unrestricted payments, i.e. .

Unrestricted Payments

The case of unrestricted payments is very easy. Basically, one has to wait until a local maximum and pay out the available capital there. The corresponding HJB equation is

Considering again the fifth case ( has a maximum and a minimum), we have to distinguish between and .

If then for all it is optimal to wait until and pay out everything there, yielding as the value function .

Assume now . For , it is optimal to wait until and pay out everything there:

For , pay out the initial capital immediately, pay on the rate until , wait then until and pay out the collected drift there:

And finally, for we have to distinguish between and . W.l.o.g. we let , i.e. exists. For all , one has to wait until the maximum :

For just wait until .

Since the proof methods are well-known, we omit further explanations and just refer to, for example, Schmidli [10, p. 102].

Note that the backward algorithms for both, restricted and unrestricted payments, can be applied for an arbitrary continuously differentiable interest rate function, like for example sine or cosine.

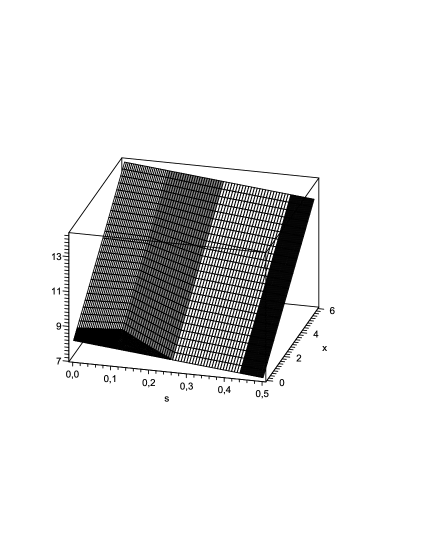

Example 3.2

Let , , , , , and .

Thus, and , and .

Note that it holds .

For , is increasing in . We wait until and pay out everything there. The value function for this area is given by the right (black) slice in Figure 2.

In we pay on the maximal possible rate up to , white slice (the second from the right) in the picture.

For , we either wait until or start immediately paying on the rate up to : second slice from the left in Figure 2. In the black area we wait, in the gray area we pay.

The value function for is given by the left slice. Like for we wait in the black area and pay in the white area.

Remark 3.3 (Arbitrary drift function)

Consider the process

where is an arbitrary continuous function with finitely many zeros in . An admissible strategy denotes now the cumulated consumption, is càdlàg, increasing and . The HJB equation in this case is

The problem of consumption maximization for unrestricted payments with deterministic constant interest rate was considered in [8]. There, it was possible to establish an algorithm for finding an explicit expression for the optimal strategy and the value function. Here, the algorithm for a constant interest rate from [8] has to be combined with the algorithm for a constant drift with pure-discount bond described earlier in this paper.

However, the finding procedure of the value function would be very time- and spaceconsuming.

An interested reader can contact the author for further information.

4 Stochastic Interest Rates

In this section, we consider a model with a stochastic discounting rate and an infinite time horizon. Like before, we assume that the surplus of the considered household is

4.1 Geometric Brownian Motion as a Discounting Process

In this subsection, we let , where is a standard Brownian motion.

Our target is to maximize the expected discounted consumption over all admissible strategies , if the discounting process is given by a geometric Brownian motion.

It means, we assume that the consumption behaviour of the considered household is linked to a stock price modelled by a geometric Brownian motion.

As an admissible strategy we denote all such that , is adapted to the filtration , generated by and for all (i.e. consumption cannot cause ruin).

The return function corresponding to a strategy and the value function are defined as

Note that . In order to guarantee the well-definiteness of the value function, we assume . Obviously,

The above integral is finite for all . The HJB equation corresponding to the problem is

| (12) |

Consider at first the case when the boundary is smaller or equal to the drift . Here, we can just pay out on the maximal rate up to without ruining. The return function corresponding to such a strategy is then given by

does not depend on and obviously solves HJB Equation (12).

Consider now . Now it is impossible to pay out on the rate till the end of the time.

Instead, we consider the strategy

| (13) |

The corresponding return function is given by

Proposition 4.1

The strategy , defined in (13), is the optimal strategy and is the value function.

Proof.

Consider the function . It holds

Thus, for all it holds

It is easy to see that the function solves HJB equation (12).

It remains to prove that . Let be an arbitrary admissible strategy, then holds

Because is bounded, the stochastic integral above is a martingale with expectation zero. Further,

Thus, applying the expectations and letting yields

. ∎

For unrestricted payments the HJB equation is

And, it is easy to see that the value function is given by

It means, we have to pay out the initial capital immediately and to pay on the rate up to the infinite time horizon. For the proof methods confer for example Schmidli [10, p. 102].

4.2 Ornstein-Uhlenbeck Process a Short Rate

Like in Section 2, we denote again by an Ornstein-Uhlenbeck process

where is a standard Brownian motion, , and let with .

Our target is to maximize the expected discounted consumption over all admissible strategies , if the interest rate is given by . A strategy is called admissible if , is adapted to the filtration , generated by and for all .

Here, we assume that the long-term mean of the process fulfils: .

The return function corresponding to a strategy and the value function are defined by

Since is now a variable and not a constant parameter like in Section 3, we manifest this fact by writing instead of for the function defined in (2). Denoting again and , we have . The HJB equation corresponding to the problem is

| (14) |

Further, the function can be estimated as follows

Using the above estimation and the fact , we find the following boundary for the value function:

| (15) |

for every choice of and all .

4.2.1 Restricted rates with .

Assume first . In this case the process will never hit zero. The return function corresponding to the constant strategy is given by:

Note that does not depend on in this case. In particular:

It is an easy exercise to prove that solves the ODE

For it is possible to interchange integration and differentiation so that

Thus,

which proves our claim. Here, the function becomes a candidate for the value function.

4.2.2 Restricted rates with .

Assume now . The return function corresponding to the strategy

| (16) |

is given by

Obviously, is continuously differentiable with respect to and twice continuously differentiable with respect to . Like in the case , we can interchange integration and derivation and obtain

The derivative of with respect to is given by

And we can conclude that solves the PDE

Note that iff .

In order to find out whether could become a good candidate for the value function, we have to investigate the properties of the function .

Due to Subsection 2.1, for a fixed and the function can have at most one zero at with

Note that . This means that for a fixed it holds either on , if , or on and on , if . Consequently, we consider just the cases 1 and 4 in Subsection 2.1, illustrated in Pictures and in Figure 1. It is easy to see that the function is increasing in and . It means that for all . Thus, for the strategy defined in (16) it holds

If and , then for every fixed the function attains its maximum at . Further, since for all and the curve

is unique with . Using the power series representation of the logarithm function, confer for example [2, p. 381], it holds for :

Thus, is negative and strictly decreasing. Let denote the inverse function of for (is well-defined because is strictly decreasing), i.e. . Then , , is positive and strictly decreasing. In particular, for and for and for . Thus, the function could not be the value function.

Proposition 4.2

The value function is locally Lipschitz continuous, strictly increasing and concave in ; locally Lipschitz continuous, decreasing and convex in . It holds .

Proof.

Let at first , and be an admissible -optimal strategy for . Then, is also an admissible strategy for (the argument works also the other way round) and it holds

Considering an optimal strategy for and applying the same arguments yields

Thus, is locally Lipschitz continuous and in particular continuous in .

For , let and be an -optimal strategy for . Then,

Note that is an admissible strategy for as well as for . Thus,

i.e. is convex in .

For every , it is clear that an admissible strategy for is also admissible for , which implies that is increasing in the component.

On the other hand, let be an -optimal strategy for the starting point and define to be

Obviously, is an admissible strategy for the starting point . Then, we obtain

Let , and note that depends on just via . Then noting that the random variable is normally distributed (with mean and variance ), using and the definition of in (2), we obtain the following estimation

Consider now the function . Using Borodin and Salminen, [4, p. 525], one finds

Thus, it holds

Note that since is normally distributed, the expected value above can be estimated as follows

Thus, defining

we obtain

In order to prove the convexity in the component, let , be an -optimal strategy for and be an -optimal strategy for . Then, for :

Thus, is an admissible strategy for . Since was arbitrary, we can conclude

i.e. is concave in .

Further, we know that the value function is bounded, and using the monotone convergence theorem (since is decreasing in ) we obtain

Estimation of the difference quotient of the value function with respect to .

Define now an auxiliary function and let be an admissible strategy, . Then

Let and an -optimal strategy for , then

Since, is convex in we obtain

∎

It has been shown that the value function is convex in and concave in . We conjecture that the optimal strategy is of a barrier type, i.e. we pay on the maximal rate above some barrier and do nothing below this barrier, whereas the barrier for should be equal to and the barrier for should be given by some constant . Then, we have to consider two functions, describing the value function above and below the barrier. Unfortunately, we were not able to find a closed expression for a return function corresponding to such a barrier strategy. That is why, we switch to the viscosity ansatz.

Definition 4.3

We say that a continuous function is a viscosity subsolution to (3) at if any function with such that reaches the maximum at satisfies

and we say that a continuous function is a viscosity supersolution to (14) at if any function with such that reaches the minimum at satisfies

A viscosity solution to (14) is a continuous function if it is both a viscosity subsolution and a viscosity supersolution at any .

Proposition 4.4

The value function is a viscosity solution to (14).

Proof.

Let , , and the surplus process under the constant strategy . Further, we let , and .

Since, the value function is locally Lipschitz continuous, there is an such that for , some and and for .

Let now be an -optimal strategy for the starting point . Like in Proposition (4.2), one can show that the return function , corresponding to the strategy , can be applied on the initial value .

In particular, if

Thus, for every and a given we can find a measurable strategy such that .

At first, we show that is a supersolution.

Construct now a strategy in the following way: let be defined like above, and be fixed, define for ; and if choose from on the strategy , i.e. for . Obviously, the constructed strategy is an admissible one.

Let be a twice continuously differentiable with respect to and once continuously differentiable with respect to test function, i.e. for all and .

Since is smooth enough, we obtain

| (17) |

Further, it holds for the constructed strategy :

Since, the expected value is bounded due to the definition of and was arbitrary, we have

In the next step, we rearrange the terms in the above inequality and divide it by . Letting go to in the above inequality yields

which yields the desired result.

It remains to show that is a subsolution.

Here, as usual we use the proof by contradiction. It means, we assume that is not a subsolution to (14) at some .

In particular, there is an and an function such that , for and , where for some

Define further . Then, and ,

for all . Furthermore,

Since , the function is continuous, such that one can find an with for . W.l.o.g. assume and and define and

Let further be an arbitrary admissible strategy with , be defined like above. Note, that , because the paths are continuous. Thus, we obtain

Obviously,

Consider now the function . It holds via Ito’s formula

Using and , we obtain

This means in particular

Since is bounded for and is a.s. finite, the stochastic integral above has expectation . We can estimate the terms on the right hand side of the above inequality as follows

| (18) |

Thus, we already have shown

The same method can be applied also for by just changing the estimations in (18).

Let be now an arbitrary admissible strategy for the starting point , then the following estimation holds true:

Now, we can build the supremum over all admissible strategies on the both sides of the above inequality. In particular, for every there is an admissible strategy such that

Letting , we obtain then

which contradicts the assumption . ∎

The next result yields the uniqueness of the viscosity solution.

Proposition 4.5

Proof.

Assume, there is a pair such that . Then, there is an such that for it still holds . The following estimation is straight forward:

which means that for all there is an such that for it holds . And on the other hand due to the properties of function , for all one has .

Obviously, the function is a supersolution and using the notation from Proposition 4.2 we also obtain

Assume first and let for

Note that the function is positive and increasing for . As usual, we let

In particular, we know . Let be such that (due to the arguments above it holds and ) and define for and

Note that is continuous, which guarantees the existence of , where denotes the closure of , such that . By definition of it holds . Thus,

We can therefore conclude that there is an such that for all and .

Further, it is clear that because is bounded in it holds

.

Obviously, is decreasing in , which means that we can assume , i.e. we consider .

For and we have

Thus, there is an such that for and . For one has, independent of the values of and :

for .

Thus, .

Letting

one can show the uniqueness also for . ∎

Remark 4.6

The problem with a deterministic linear surplus and an Ornstein-Uhlenbeck process as a short rate seemed to be very simple. Nevertheless, we could not find an explicit solution to this optimization problem. The value function has been proved to be concave in and convex in , which suggests that the optimal consumption strategy should be of a barrier type. But in contrast to the case with a geometric Brownian motion as a discounting factor, it is not that easy to calculate the return functions corresponding to some barrier strategy.

References

- [1] Albrecher, H. and Thonhauser, S.: Optimality results for dividend problems in insurance. RACSAM Rev. R. Acad. Cien. Serie A. Mat. 103(2), 295–320 (2009)

- [2] Amann, H. and Escher, J.: Analysis I, Birkhäuser Verlag, Basel. (2002)

- [3] Azcue, P. and Muler, N.: Optimal reinsurance and dividend distribution policies in the Cramér–Lundberg model. Math. Finance 15, 261–308 (2005)

- [4] Borodin, A.N. and Salminen, P.: Handbook of Brownian Motion – Facts and Formulae. Birkhäuser Verlag, Basel. (1998)

- [5] Brigo, D. and Mercurio, F. : Interest Rate Models - Theory and Practice. Springer, Heidelberg. 2 Edition. (2006)

- [6] Cox J.C. and Huang C.F.: Optimal consumption and portfolio policies when asset prices follow a diffusion process. Journal of Economic Theory 49, 33 – 83 (1989)

- [7] Eisenberg J.: On optimal control of capital injections by reinsurance and investments. Bl. DGVFM 31 (2), 329–345, (2010)

- [8] Eisenberg, J., Grandits, P. and Thonhauser, S.: Optimal consumption under deterministic income. Journal of Optimization Theory and Applications, 160(1), 255–279, (2014)

- [9] Fleming, W.H. and Rishel, R.W.: Deterministic and Stochastic Optimal Control. Springer-Verlag, Berlin-New York. (1975)

- [10] Schmidli, H.: Stochastic Control in Insurance. Springer-Verlag, London. (2008)

- [11] Shreve, S.E., Lehotzky, J.P. and Gaver D.P.: Optimal consumption for general diffusions with absorbing and reflecting barriers. SIAM J. Control Optim., 22(1), 55–75, (1984)