The Perfect Marriage and Much More: Combining Dimension Reduction, Distance Measures and Covariance

Ravi Kashyap

SolBridge International School of Business / City University of Hong Kong

March 10, 2024

Keywords: Dimension Reduction; Johnson-Lindenstrauss; Bhattacharyya; Distance Measure; Covariance; Distribution; Uncertainty

JEL Codes: C44 Statistical Decision Theory; C43 Index Numbers and Aggregation; G12 Asset Pricing

Mathematics Subject Codes: 60E05 Distributions: general theory; 62-07 Data analysis; 62P20 Applications to economics

1 Abstract

We develop a novel methodology based on the marriage between the Bhattacharyya distance, a measure of similarity across distributions of random variables, and the Johnson-Lindenstrauss Lemma, a technique for dimension reduction. The resulting technique is a simple yet powerful tool that allows comparisons between data-sets representing any two distributions. The degree to which different entities, (markets, universities, hospitals, cities, groups of securities, etc.), have different distance measures of their corresponding distributions tells us the extent to which they are different, aiding participants looking for diversification or looking for more of the same thing. We demonstrate a relationship between covariance and distance measures based on a generic extension of Stein’s Lemma. We consider an asset pricing application and then briefly discuss how this methodology lends itself to numerous market-structure studies and even applications outside the realm of finance / social sciences by illustrating a biological application. We provide numerical illustrations using security prices, volumes and volatilities of both these variables from six different countries.

2 Introduction

The varying behavior of participants in a social system, which can also be viewed as unpredictable actions, will give rise to unintended consequences and as long as participants are free to observe the results and modify their actions, this effect will persist (Kashyap 2017; appendix 13 has a discussion of uncertainty and unintended consequences). Unintended consequences and its siamese twin, uncertainty, are fostering a trend of collecting data to improve decision making, which is perhaps leading to more analysis of the data and more actions, leading to a cycle of increasing data collection and actions, giving rise to information explosion (Dordick & Wang 1993; Korth & Silberschatz 1997; Sweeney 2001; Fuller 2010; Major & Savin-Baden 2010; Beath, Becerra-Fernandez, Ross & Short 2012). (Kashyap 2015) consider ways to reduce the complexity of social systems, which could be one way to mitigate the effect of unintended outcomes. While attempts at designing less complex systems are worthy endeavors, reduced complexity might be hard to accomplish in certain instances and despite successfully reducing complexity, alternate techniques at dealing with uncertainty are commendable complementary pursuits (Kashyap 2016).

While it might be possible to observe historical trends (or other attributes) and make comparisons across fewer number of entities; in large systems where there are numerous components or contributing elements, this can be a daunting task. In this present paper, we present quantitative measures across aggregations of smaller elements that can aid decision makers by providing simple yet powerful metrics to compare large groups of entities.

We consider a measure of similarity, the Bhattacharyya distance, across distributions of variables. We develop a novel methodology based on the marriage between the Bhattacharyya distance and the Johnson-Lindenstrauss Lemma (JL-Lemma), a technique for dimension reduction; providing us with a simple yet powerful tool that allows comparisons between data-sets representing any two distributions. The degree to which different entities, (markets, universities, hospitals, countries, cities, farms, forests, groups of securities, etc.), have different distance measures of their corresponding distributions tells us the extent to which they are different, aiding participants looking for diversification or looking for more of the same thing. To calculate the distance measure between any two random variables (both of which could be multi-variate with either different number of component random variables or observations), we utilize the JL-Lemma to reduce the dimensions of one of the random variables (either the number of component random variables or the number of observations) such that the two random variables have the same number of dimensions allowing us to apply distance measures.

We demonstrate a relationship between covariance and distance measures based on a generic extension of Stein’s Lemma. We consider an asset pricing application and also briefly discuss how this methodology lends itself to numerous market-structure and asset pricing studies and even applications outside the realm of finance / social sciences by illustrating a biological application (sections 6, 6.1, 6.2). We illustrate some ways in which our techniques can be used in practice by comparing stock prices, trading volumes, price volatilities and volume volatilities across six markets (sections 7.1; 7.2).

An unintended consequence of our efforts, has become a review of the vast literature on distance measures and related statistical techniques, which can be useful for anyone that attempts to apply the corresponding techniques to the problems mentioned here and also to the many unmentioned but possibly related ones. The results and the discussion draw upon sources from statistics, probability, economics / finance, communication systems, pattern recognition and information theory; becoming one example of how elements of different fields can be combined to provide answers to the questions raised by a particular field. All the propositions are new results and they depend on existing results which are given as lemmas without proof. Such an approach ensures that the results are instructive and immediately applicable to a wider audience.

3 Literature Review of Methodological Fundamentals

3.1 Bhattacharyya Distance

We use the Bhattacharyya distance (Bhattacharyya 1943; 1946) as a measure of similarity or dissimilarity between the probability distributions of the two entities we are looking to compare. These entities could be two securities, groups of securities, markets or any statistical populations that we are interested in studying. The Bhattacharyya distance is defined as the negative logarithm of the Bhattacharyya coefficient.

| (1) |

Here, , is the Bhattacharyya Distance between two multinomial populations each consisting of categories or classes with associated probabilities and respectively. The Bhattacharyya coefficient, , is calculated as shown below for discrete and continuous probability distributions.

| (2) |

| (3) |

Bhattacharyya’s original interpretation of the measure was geometric (Derpanis 2008). He considered two multinomial populations each consisting of categories or classes with associated probabilities and respectively. Then, as and , he noted that and could be considered as the direction cosines of two vectors in dimensional space referred to a system of orthogonal co-ordinate axes. As a measure of divergence between the two populations Bhattacharyya used the square of the angle between the two position vectors. If is the angle between the vectors then:

| (4) |

Thus if the two populations are identical: corresponding to , hence we see the intuitive motivation behind the definition as the vectors are co-linear. Bhattacharyya further showed that by passing to the limiting case a measure of divergence could be obtained between two populations defined in any way given that the two populations have the same number of variates. The value of coefficient then lies between and .

| (5) |

| (6) |

Here, the last inequality follows from Jensen’s inequality. (Comaniciu, Ramesh & Meer 2003) modify this as shown below and prove that this alternate measure, termed the modified Bhattacharyya Metric, follows all the metric axioms: positive, symmetric, is zero for the same two elements and satisfies the triangle inequality.

| (7) |

We get the following formulae (Lee and Bretschneider 2012) for the Bhattacharyya distance when applied to the case of two univariate normal distributions.

| (8) |

Here, is the Bhattacharyya distance between and normal distributions or classes. is the variance of the th distribution, is the mean of the th distribution, and are two different distributions.

The original paper on the Bhattacharyya distance (Bhattacharyya 1943) mentions a natural extension to the case of more than two populations. For an population system, each with random variates, the definition of the coefficient becomes,

| (9) |

For two multivariate normal distributions, is the Bhattacharyya distance between two multivariate normal distributions, where .

| (10) |

and are the means and covariances of the distributions, and . We need to keep in mind that a discrete sample could be stored in matrices of the form and , where, is the number of observations and denotes the number of variables captured by the two matrices.

| (11) |

| (12) |

The Bhattacharyya measure finds numerous applications in communications, pattern recognition and information theory (Mak and Barnard 1996; Guorong, Peiqi & Minhui 1996). Other measures of divergence include the Mahalanobis distance (Mahalanobis 1936) which is a measure of the distance between a point and a distribution, Kullback-Leibler (KL) divergence (Kullback & Leibler 1951) and the Hellinger or Matusita measure, , (Hellinger 1909; Matusita 1955) which is related to the Bhattacharyya distance since minimizing the Matusita distance is equivalent to maximizing the Bhattacharyya distance. The KL measure is not symmetric and is discussed in (Duchi 2007; Contreras-Reyes & Arellano-Valle 2012) when applied to normal or skew normal distributions. In (Aherne, Thacker & Rockett 1998) it is shown that the Bhattacharyya coefficient approximates the measure (Chi-Squared measure), while avoiding the singularity problem that occurs when comparing instances of the distributions that are both zero.

| (13) |

| (14) |

For discrete probability distributions and , the Kullback–Leibler divergence, , of from is defined to be,

| (15) |

For distributions and , of continuous random variables, the Kullback–Leibler divergence is defined (Bishop 2006) to be the integral below, where and denote the densities of and . (Huzurbazar 1955) proves a remarkable property that for all distributions admitting sufficient statistics the exact forms of the KL divergence come out as explicit functions of the parameters of the distribution.

| (16) |

(Schweppe 1967b) develops new expressions for the KL divergence and the Bhattacharyya distance, in terms of the effects of various conditional expectation filters (physically realizable linear systems) acting on Gaussian processes. In particular, the distances are given by time integrals of the variances and mean values of the outputs of filters designed to generate the conditional expectations of certain processes. Defining a matched filter to be one whose output is the conditional expectation of the signal contained in the input, then the performance of a matched filter is much easier to analyze than the performance of a mismatched filter. The divergence involves mismatched filters while the Bhattacharyya distance uses only matched filters. Hence the Bhattacharyya distance is easier to analyze. In (Kailath 1967) it is shown that the two measures give similar results for Gaussian processes with unequal mean value functions and that the Bhattacharyya distance yields better results when the processes have unequal covariance functions, where in fact the divergence measure fails. In (Schweppe 1967a) the Bhattacharyya distance is specialized to Markov-Gaussian processes. (Cha 2007) is a comprehensive survey on distance/similarity measures between probability density functions.

For a discrete sample in a two class scenario, (Jain 1976) shows that any estimate of the Bhattacharyya coefficient is biased and consistent using a Taylor series expansion around the neighborhood of the points. We can write the Bhattacharyya coefficient as,

| (17) |

Here, and denote the sets of parameters and respectively. The class conditional densities are given by,

| (18) |

| (19) |

| (20) |

Let and denote the maximum likelihood estimates of and , respectively, , based on samples available from each of the two classes:

| (21) |

where and are the numbers of samples for which takes the value from class and , respectively. We define a sample estimate of the Bhattacharyya coefficient as,

| (22) |

where, and respectively. (Djouadi, Snorrason & Garber 1990) derive closed-form expressions for the bias and variance of Bhattacharyya coefficient estimates based on a certain number of training samples from two classes, described by multivariate Gaussian distributions. Numerical examples are used to show the relationship between the true parameters of the densities, the number of training samples, the class variances, and the dimensionality of the observation space.

3.2 Dimension Reduction

A key requirement to apply the Bhattacharyya distance in practice is to have data-sets with the same number of dimensions. (Fodor 2002; Burges 2009; Sorzano, Vargas & Montano 2014) are comprehensive collections of methodologies aimed at reducing the dimensions of a data-set using Principal Component Analysis or Singular Value Decomposition and related techniques.

(Johnson & Lindenstrauss 1984) proved a fundamental result (JL Lemma) that says that any point subset of Euclidean space can be embedded in dimensions without distorting the distances between any pair of points by more than a factor of , for any . Whereas principal component analysis is only useful when the original data points are inherently low dimensional, the JL Lemma requires absolutely no assumption on the original data. Also, note that the final data points have no dependence on , the dimensions of the original data which could live in an arbitrarily high dimension.

Simplified versions of the original proof are in (Frankl and Maehara 1988; 1990). We use the version of the bounds for the dimensions of the transformed subspace given in (Frankl & Maehara 1990; Dasgupta & Gupta 1999). (Nelson 2010) gives a proof using the Hanson and Wright inequality (Hanson & Wright 1971). (Achlioptas 2003) gives a proof of the JL Lemma using randomized algorithms. (Venkatasubramanian & Wang 2011) present a study of the empirical behavior of algorithms for dimensionality reduction based on the JL Lemma. We point out the wonderful references for the theory of matrix algebra and numerical applications (Gentle 2007; 2012).

Lemma 1.

For any and any integer , let be a positive integer such that

Then for any set of points in , there is a map such that for all ,

Furthermore, this map can be found in randomized polynomial time and one such map is where, and is a matrix in which each entry is sampled i.i.d from a Gaussian distribution.

4 Intuition for Dimension Reduction

The above discussions of distance measures and dimension reduction are extensively used in many areas, but the combination of the two is bound to create confusions in the minds of the uninitiated. Hence, we provide examples from daily life, (both ours and from creatures in higher dimensions), to provide a convincing argument as to why the two used together can be a powerful tool for the study of complex systems governed by uncertainty.

4.1 Game of Darts

If we consider a cloud of points in multi-dimensional space. It would be reasonable to expect that the distance between the points, or how the points are distributed, gives a measure of the randomness inherent in the process generating them. When dimension reduction moves the points to lower dimensions, and the change in the distance between them stays bounded, the randomness properties of the original process are retained, to the extent as dictated, by the bounds established by the procedure performing the dimension transformation, which in our case is given by the JL Lemma.

Taking an example, from our own real lives, the marks on a dartboard in a game of darts are representative of the skills of the people throwing the darts. For simplicity, we could assume that there are three types of dart throwers: novice, intermediate and advanced. Identifying the category of the person making the marks, would be similar to identifying the type of distribution of a stochastic process. If we map the marks, on the board, to a line using a transformation, that keeps the distances between the marks bounded, a flavor of the skill level would be retained and we would be able to identify the category of the person making the marks. Dimension reduction, using a transformation that keeps the distances bounded, is in essence the same undertaking.

4.2 The Merits and Limits of Four Physical Dimensions

Another example of dimension transformation is from the physical world we live in. We are four dimensional creatures: latitude, longitude, height and time are our dimensions since we need to know these four co-ordinates to fully specify the position of any object in our universe. This is perhaps, made clear to lay audiences, (with regards to physics, such as many of us), by the movie Interstellar (Thorne 2014). Also, (Sagan 2006) has a mesmerizing account of many physical aspects including how objects, or, beings can transform from higher to lower dimensions and change shapes; but they would need to obey the laws of the lower dimension. The last dimension, time, is the one we cannot control, or, move around in. But we can change the other three co-ordinates and hence we have three degrees of freedom.

(Appendix 12) has a detailed example to build the intuition related to dimension transformation from our four dimensional physical world. This example should also make it clear to us that it is better to work with the highest dimension that we can afford to work with, since each higher dimension retains some flavors of the object we are trying to understand that might be not discernible in lower dimensions. This should also tell us that objects we observe in our universe might have many interesting properties that we are unable to observe due to the restrictions of our physical dimensions.

5 Methodological Innovations

In this section, we collect the new results developed in this paper. These can be broadly categorized into two buckets. The first is the types of distributions that we would obtain when a particular distribution type is transformed to a different dimension (different number of random variables) using the JL-Lemma (sections 5.1, 5.2, 5.3, 5.4). The second group of results considers the relationships between covariance and distance measures (section 5.5).

5.1 Normal Log-Normal Mixture

The normality or otherwise of stock price changes is discussed extensively in the literature: (Osborne 1959; 1962; Fama 1965; 1995; Mandelbrot & Taylor 1967; Kon 1984; Richardson & Smith 1993). Starting with a geometric Brownian motion for the stock price process, it can be established that stock prices are distributed log-normally, (Hull 2006). If we are looking at variables that are only positive, such as prices, quantities traded, or volatilities, then it is a reasonable initial assumption that they are distributed log normally (we relax this assumption to incorporate more generic settings in later sections).

Transforming log-normal multi-variate variables into a lower dimension by multiplication with an independent normal distribution (see: Lemma 1) results in the sum of variables with a normal log-normal mixture, (Clark 1973; Tauchen & Pitts 1983; Yang 2008), evaluation of which requires numerical techniques (Miranda & Fackler 2002). A random variable, , would be termed a normal log-normal mixture if it is of the form,

| (23) |

where, and are random variables with correlation coefficient, satisfying the below,

| (24) |

We note that for when degenerates to a constant, this is just the distribution of and is unidentified.

To transform a column vector with observations of a random variable into a lower dimension of order, , we can multiply the column vector with a matrix, of dimension .

Proposition 1.

A dimension transformation of observations of a log-normal variable into a lower dimension, , using Lemma 1, yields a probability density function which is the sum of random variables with a normal log-normal mixture, given by the convolution,

The convolution of two probability densities arises when we have the sum of two independent random variables, . The density of is given by,

When the number of independent random variables being added is more than two, or the reduced dimension after the Lemma 1 transformation is more than two, , then we can take the convolution of the density resulting after the convolution of the first two random variables, with the density of the third variable and so on in a pair wise manner, till we have the final density.

Proof.

Appendix 14.2 sketches a general proof and then tailors it to our case where the normal distribution has zero mean and the two variables are uncorrelated. ∎

Methods of estimating parameters and comparing the resulting distributions when normal (log-normal) distributions are mixed, are studied in (Fowlkes 1979; Vernic, Teodorescu & Pelican 2009). As noted earlier, the normal log-normal mixture tends to the normal distribution when the log-normal distribution has low variance and this property can be helpful for deciding when this approach is suitable.

5.2 Normal Normal Product

For completeness, we illustrate how dimension reduction would work on a data-set containing random variables that have normal distributions. This can also serve as a useful benchmark given the wide usage of the normal distribution and can be an independently useful result.

(Craig 1936) was one of the earlier attempts to investigate the probable error of the product of the two quantities, each of known probable error; becoming the first work to determine the algebraic expression for the moment-generating function of the product, but without being able to determine the distribution of the product. It was found that the distribution of is a function of the coefficient of correlation of both variables and of two parameters that are proportional to the inverse of the coefficient of variation of each variable. When the product of the means of the two random variables is nonzero, the distribution is skewed as well as having excess kurtosis, although (Aroian 1947; Aroian, Taneja & Cornwell 1978) showed that the product approaches the normal distribution as one or both of the ratios of the means to standard errors (the inverse of the coefficients of variation) of each random variable get large in absolute value.

(Aroian 1947) showed that the gamma distribution (standardized Pearson type III) can provide an approximation in some situations. Instead, the analytical solution for this product distribution is a Bessel function of the second kind with a purely imaginary argument (Aroian 1947; Craig 1936). The four moments of the product of two correlated normal variables are given in (Craig 1936; Aroian, Taneja & Cornwell 1978).

Proposition 2.

A dimension transformation of observations of a normal variable into a lower dimension, , using Lemma 1, yields a probability density function which is the sum of random variables with a normal normal product distribution, given by the convolution,

Proof.

Appendix 14.3 sketches a general proof and then tailors it to our case where the normal distribution has zero mean and the two variables are uncorrelated. ∎

Remark.

We note the following two useful results.

-

1.

By writing the product as the difference of two squared variables, it is easy to see that the product distribution is a linear combination of two Chi-Square random variables,

(25) If with a coefficient of correlation, then,

(26) Here, or central chi-squared random variables with one degree of freedom. are independent only if . Hence, in general, are dependent non central chi-squared variables.

-

2.

The result we use in (appendix 14.3) to derive the above convolution, can also be arrived at, by writing the density for using the Dirac Delta function, as,

(27) (28) (29)

(Glen, Leemis & Drew 2004) present an algorithm for computing the probability density function of the product of two independent random variables. (Springer & Thompson 1966) use the Mellin integral transform (Epstein 1948; End-note 3) to develop fundamental methods for the derivation of the probability distributions and density functions of the products of independent random variables; (Springer & Thompson 1970) use these methods to show that the products of independent beta, gamma and central Gaussian random variables are Meijer G-functions (Mathai & Saxena 1973; End-note 4).

(Ware & Lad 2003) has results very closely aligned to our requirements. They attempt to calculate the probability that the sum of the product of variables with a Normal distribution is negative. They first assess the distribution of the product of two independent normally distributed variables by comparing three different methods: 1) a numerical method approximation, which involves implementing a numerical integration procedure on MATLAB; 2) a Monte Carlo construction and; 3) an approximation to the analytic result using the Normal distribution under certain conditions, by calculating the first two moments of the product, and then finding a distribution whose parameters match the moments. Second, they consider the sum of the products of two Normally distributed variables by applying the Convolution Formula. Lastly, they combine the two steps to arrive at the main results while also showing that a direct Monte Carlo approximation approach could be used. (Seijas-Macías & Oliveira 2012) is a recent work that has several comparisons using Newton-Cotes numerical integration (Weisstein 2004; End-note 5).

In addition, while it useful to keep these results at the back of our mind, it is worth finding simpler distributions instead of having to numerically calculate the distance based on the normal product or the normal log-normal mixture sum. An alternate is discussed in the next section, where we set both distributions to be truncated normal.

5.3 Truncated Normal / Multivariate Normal

A truncated normal distribution is the probability distribution of a normally distributed random variable whose value is either bounded below, above or both (Horrace 2005; Burkardt 2014) and hence seems like a natural candidate to fit the distributions we are dealing with. We can estimate the parameters of the distributions (both the unchanged one and the one with the reduced dimensions) by setting them as truncated multivariate normals and calculate the distance based on these estimated distributions.

To assess the suitability of normal distributions to fit the observed sample, there are a variety of tests. The univariate sample measures of skewness and kurtosis may be used for testing univariate normality. Under normality, the theoretical values of and are and , respectively. One of the most famous tests for normality of regression residuals is the test of (Jarque & Bera 1980; 1987; End-notes 7; 8). The test statistic JB (Jarque-Bera) is a function of the measures of skewness and kurtosis computed from the sample and is based on the Lagrange multiplier test or score test.

The simplest testing problem assumes that the data are generated by a joint density function under the null hypothesis and by under the alternative, with . The Lagrange Multiplier test is derived from a constrained maximization principle (Engle 1984; End-note 6). Maximizing the log-likelihood subject to the constraint that yields a set of Lagrange Multipliers which measure the shadow price of the constraint. If the price is high, the constraint should be rejected as inconsistent with the data.

Another test frequently used is the sum of squares of the standardized sample skewness and kurtosis which is asymptotically distributed as a variate (Doornik and Hansen 2008) along with transformations of skewness and kurtosis to facilitate easier implementation and also to contend with small sample issues. (Malkovich & Afifi 1973) generalize these statistics to test a hypothesis of multivariate normality including a discussion of transformations to simplify the computational methods.

(Székely & Rizzo 2005; End-note 9) propose a new class of consistent tests for comparing multivariate distributions based on Euclidean distance between sample elements. Applications include one-sample goodness-of-fit tests for discrete or continuous multivariate distributions in arbitrary dimension . The new tests can be applied to assess distributional assumptions for many classical procedures in multivariate analysis. (Wald & Wolfowitz 1946) consider the problem of setting tolerance limits for normal distributions with unknown mean and variance. For a univariate distribution with a sample of independent observations, two functions and of the sample need to be constructed such that the probability that the limits and will include at-least a given proportion of the population is equal to a preassigned value .

Suppose has a normal distribution and lies within the interval . Then conditional on has a truncated normal distribution. Its probability density function, , for , is given by

| (30) |

Here, is the probability density function of the standard normal distribution and is its cumulative distribution function. There is an understanding that if , then , and similarly, if , then .

Proposition 3.

The Bhattacharyya distance when we have truncated normal distributions, , that do not overlap is zero and when they overlap it is given by

Here,

Proof.

Appendix 14.4. ∎

It is easily seen that

| (31) |

Looking at conditions when gives the below. This shows that the distance measure increases with greater truncation and then decreases as the extent of overlap between the distributions decreases.

| (32) |

(Kiani, Panaretos, Psarakis & Saleem 2008; Zogheib & Hlynka 2009; Soranzo & Epure 2014) list some of the numerous techniques to calculate the normal cumulative distribution. Approximations to the error function are also feasible options (Cody 1969; Chiani, Dardari & Simon 2003).

Similarly, a truncated multivariate normal distribution has the density function,

| (33) |

Here, is the mean vector and is the symmetric positive definite covariance matrix of the distribution and the integral is a dimensional integral with lower and upper bounds given by the vectors and .

Proposition 4.

The Bhattacharyya distance when we have truncated multivariate normal distributions and all the dimensions have some overlap is given by

Here,

Proof.

Appendix 14.5 ∎

Again we see that,

| (34) |

Looking at conditions when gives a similar condition as the univariate case,

| (35) | ||||

| (36) | ||||

| (37) | ||||

| (38) |

5.4 Discrete Multivariate Distribution

A practical approach would be to use discrete approximations for the probability distributions. This is typically done by matching the moments of the original and approximate distributions. Discrete approximations of probability distributions typically are determined by dividing the range of possible values or the range of cumulative probabilities into a set of collectively exhaustive and mutually exclusive intervals. Each interval is approximated by a value equal to its mean or median and a probability equal to the chance that the true value will be in the interval.

A criterion for judging the accuracy of the discrete approximation is that it preserve as many of the moments of the original distribution as possible. (Keefer & Bodily 1983; Smith 1993) provide comparisons of commonly used discretization methods. (Miller & Rice 1983) look at numerical integration using gaussian quadrature as a means of improving the approximation. This approach approximates the integral of the product of a function and a weighting function over the internal by evaluating at several values and computing a weighted sum of the results.

| (39) |

For the case of a discrete approximation of a probability distribution, the density function with support is associated with the weighting function and the probabilities with the weights . We approximate by a polynomial, and choose and (or ) to provide an adequate approximation for each term of the polynomial. This translates to finding a set of values and probabilities such that,

| (40) |

A discrete approximation with probability-value pairs can match the first moments exactly by finding and that satisfy the below equations, which are solved using well known techniques.

| (41) | ||||

| (42) | ||||

| (43) | ||||

| (44) | ||||

| (45) |

Among several alternatives to distribution approximations, (Wallace 1958), restricts attention to finding asymptotic expansions in which the errors of approximation approach zero as some parameter, typically sample size, tends to infinity. Estimating the parameters of the distributions (both the unchanged one and the one with the reduced dimensions) by setting them as discrete multivariate distributions and calculating the distance based on these estimated distributions is a practical alternative to using the truncated normal distributions.

5.5 Covariance and Distance

We compare the covariance between two random variables and the Bhattacharyya coefficient, assuming support over relevant portions of the real line and that the density function is differentiable. Consider the covariance and the distance of and . It is easily seen that the distance between the distributions is in both cases, but the covariance is when they are exactly the same and in the other case. This shows that despite knowing the distance we do not have full information about the co-movements of the two distributions. Hence distance is not a substitute for covariance but rather a very useful complement, since knowing the two will tell us the magnitudes of how one variable will change if we know the other and the likelihood of observing certain values from one distribution if have observed values from the other one.

An interesting result concerning the covariance is given by Stein’s lemma (Stein 1973; 1981; Rubinstein 1973; 1976) which connects the covariance between two random variables that are joint normally distributed and the covariance between any function of one of the random variables and the other. If and have a joint distribution that is bivariate normal and if is a continuously differentiable function of then,

| (46) |

It easily follows that, if is a normal random variable with mean and variance and if is a differentiable function with derivative such that , we then have,

| (47) |

(Losq & Chateau 1982) extend the result to the case when is a function of random variables. (Wei & Lee 1988) extend this further to the case where both variables are functions of multivariate normal random variables. (Siegel 1993) derives a remarkable formula for the covariance of with the minimum of the multivariate normal vector .

| (48) |

(Liu 1994) uses a multivariate version of Stein’s identity to devise the below more generalized formula, where is the th largest among ,

| (49) |

(Kattumannil 2009) extends the Stein lemma by relaxing the requirement of normality. If the continuous random variable has support over the interval , that is , with mean , variance , density function and cumulative distribution . Let be a real valued function such that and . Suppose is a differentiable function with derivative and there exists a non-vanishing (non-zero over the support) function such that,

| (50) |

| (51) |

| (52) |

Integrating with respect to from to and assuming shows that for a given the value of uniquely determines the distribution of .

| (53) |

| (54) |

Similarly, integrating with respect to from to and assuming ,

| (55) |

For any absolutely continuous function, , with derivative satisfying , and provided we have the following identity,

| (56) |

(Teerapabolarn 2013) is a further extension of this normality relaxation to discrete distributions. Another useful reference, (Kimeldorf & Sampson 1973), provides a class of inequalities between the covariance of two random variables and the variance of a function of the two random variables. Let be an open convex subset of the plane and be the class of all pairs of real random variables having finite variances and . Assume that is a function with continuous partial first derivatives in the domain characterized by the following functional inequality and an equivalent partial differential inequality,

| (57) |

| (58) |

If the above equivalent necessary and sufficient conditions are satisfied we have,

| (59) |

We now derive the following general extension to Stein’s lemma, that does not require normality, involving the covariance between a random variable and a function of another random variable.

Proposition 5.

If the continuous random variables and have support over the interval , that is , with means , variances , density functions , cumulative distributions and joint density function, . Let be a real valued function such that and . Suppose is a differentiable function with derivative with respect to and there exists a non-vanishing (non-zero over the support) function such that,

Assuming shows that for a given the value of uniquely determines the joint distribution of and .

Similarly, assuming gives,

For any absolutely continuous function, , with derivative satisfying , and provided , we have the following identity,

Proof.

Appendix 14.6. ∎

Corollary 1.

It is easily seen that ,

Proof.

Substituting in the proof of the proposition 5 and simplifying gives this result. ∎

Building upon some of the above results, primarily the extension to Stein’s lemma in corollary 1, we formulate the following connection between distance (Bhattacharyya coefficient) and covariance.

Proposition 6.

The following equations govern the relationship between the Bhattacharyya coefficient, , and the covariance between any two distributions with joint density function, , means, and density functions ,

Here,

and is a non-vanishing function such that,

Proof.

Appendix 14.7. ∎

Corollary 2.

It is easily seen that ,

Proof.

Using instead of in the proof of the proposition 6 and simplifying gives this result. ∎

6 Market-structure, Microstructure and Other Applications

Our methodologies can help in the comparison of economic systems that generate prices, quantities and aid in the analysis of shopping patterns and understanding consumer behavior. The systems could be goods transacted at different shopping malls or trade flows across entire countries. Study of traffic congestion, road accidents and other fatalities across two regions could be performed to get an idea of similarities and seek common solutions where such simplifications might be applicable. The diversity of applications is limited only by our imagination since these techniques can be used in any system where data is generated and is studied to obtain a better understanding of the system.

We point below one asset pricing and one biological application to show the limitless possibilities such a comparison affords. The empirical illustration below in section 7.1 is another example of how the techniques developed here can be immediately applicable for microstructure studies. We provide a definition of microstructure that justifies why information collection and dimension reduction can be helpful procedures in this space.

Definition 1.

Market Microstructure is the investigation of the process and protocols that govern the exchange of assets with the objective of reducing frictions that can impede the transfer.

In financial markets, where there is an abundance of recorded information, this translates to the study of the dynamic relationships between observed variables, such as price, volume and spread, and hidden constituents, such as transaction costs and volatility, that hold sway over the efficient functioning of the system. The degree to which different markets or sub groups of securities have different measures of their corresponding distributions tells us the extent to which they are different. This can aid investors looking for diversification or looking for more of the same thing.

6.1 Asset Pricing Application

The price of an asset today that gives a payoff in the future (next time period) is given by the fundamental asset pricing equation that makes use of a stochastic discount factor . Multi-period versions are easily derived and hence we drop the time subscripts below. (Lucas 1978; Hansen & Richard 1987; Hansen & Jagannathan 1991; Cochrane 2009) are classic references. (Kashyap 2018) reviews the asset pricing literature with emphasis on the equity risk premium puzzle (Mehra & Prescott 1985; Mehra 1988), which is that the return on equities has far exceeded the average return on short-term risk-free debt and cannot be explained by conventional representative-agent consumption based equilibrium models. Some solution attempts and related debates are (Rietz 1988; Mehra & Prescott 1988; Weil 1989; Constantinides & Duffie 1996; Campbell & Cochrane 1999; Bansal & Yaron 2004; Barro 2006; Weitzman 2007). The puzzle is based on the assumption that consumption growth is log-normal. We can relax this assumption and derive the below relationships that can aid the many empirical attempts on asset pricing that seek to find proxies for the discount factor or to marginal utility growth, employing variables of the form, .

Proposition 7.

The asset pricing equation can be written as,

Proof.

Using proposition 5 and the definitions of and therein, gives this result. ∎

Corollary 3.

With a further restriction on , where, expected payoff is with density function and the density function of the factor is , the asset pricing equation becomes,

Proof.

Follows immediately from proposition 6. ∎

6.2 Biological Application

The field of medical sciences is not immune from the increasing collection of information (Berner & Moss 2005) and the side effects of growing research and literature (Huth 1989). The challenges of managing growing research output are significantly more complex than expanding amounts of data. This might require advances in artificial intelligence and a better understanding of the giant leap the human mind makes at times from sorting through information, summarizing it as knowledge and transcending to a state of condensed wisdom. We leave this problem aside for now; but tackle the slightly more surmountable problem of voluminous data sources.

Suppose we have a series of observations of different properties, (such as heart rate or blood sugar level and others as well), across different days from different people from different geographical regions. The goal would then be to identify people from which regions have a more similar constitution. The number of days on which the observations are made is the same for all regions; but there could be different number of participants in each region.

The data gathering could be the result of tests conducted at different testing facilities on a certain number of days and different number of people might show up at each facility on the different days the tests are done. The result of the data collection will be as follows: We have a matrix, , for each region and property , with observations across time (rows) and (columns) for number of participants from region and property . Here, we consider all properties together as representing a region. The dimension of the data matrix is given by . We could have two cases depending on the data collection results.

-

1.

That is the number of participants in a region are the same for all properties being measured. This would be the simple case.

-

2.

That is the number of participants in a region could be different for some of the properties being measured.

The simple scenario corresponding to case 1) of the data collection would be when we have a matrix, , for each region and property , with observations across time (rows) and (columns) for number of participants from that region. If we consider each property separately, we can compute the Bhattacharyya Distance across the various matrices (in pairs) separately for each property across the various regions or ’s. The multinomial approach outlined earlier can be used to calculate one coefficient for each region by combining all the properties. For the second case, we can compute the Bhattacharyya Distance across the various matrices for all the properties combined (or separately for each property) for a region using the multinomial approach after suitable dimension transformations.

To illustrate this, suppose we have two matrices, and , representing two different probability distributions, with dimensions, and , respectively. Here, and denote the number of variables captured by the two matrices and . In general, and are not equal. is the number of observations, which is the same across the two distributions. We can calculate the Bhattacharyya distance or another measure of similarity or dissimilarity between and by reducing the dimensions of the larger matrix, (say ) to the smaller one so that we have and , with the same dimension, . Here, . Each entry in is sampled i.i.d from a Gaussian distribution.

7 Empirical Illustrations

7.1 Comparison of Security Prices across Markets

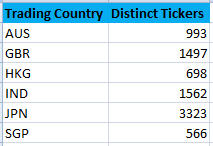

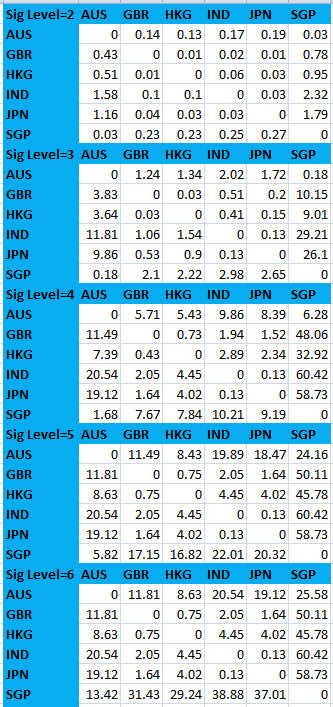

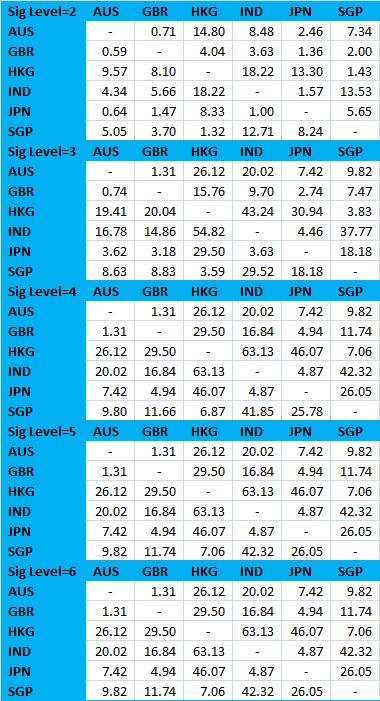

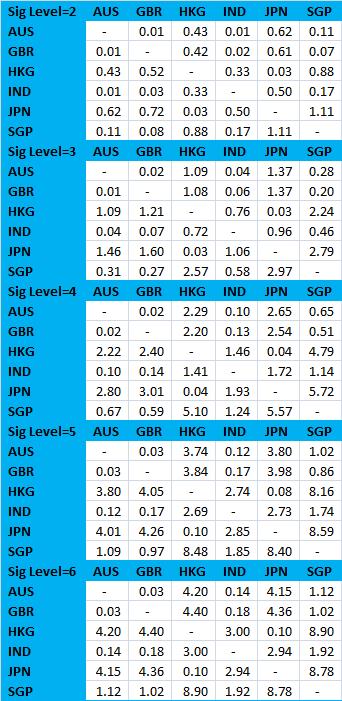

We start with a simple example illustrating how this measure could be used to compare different countries based on the prices of all equity securities traded in that market. Our data sample contains closing prices for most of the securities from six different markets from Jan 01, 2014 to May 28, 2014 (Figure 1a). Singapore with 566 securities is the market with the least number of traded securities. Even if we reduce the dimension of all the other markets with more number of securities, for a proper comparison of these markets we would need more than two years worth of data. Hence as a simplification, we first reduce the dimension of the matrix holding the close prices for each market using PCA reduction, so that the number of tickers retained would be comparable to the number of days for which we have data. The results of such a comparison are shown in Figure 1b. Some implementation pointers using statistical packages such as R are given in section 7.7.

We report the full matrix and not just the upper or lower matrix since the PCA reduction we do takes the first country reduces the dimensions up-to a certain number of significant digits and then reduces the dimension of the second country to match the number of dimensions of the first country. For example, this would mean that comparing AUS and SGP is not exactly the same as comparing SGP and AUS. As a safety step before calculating the distance, which requires the same dimensions for the structures holding data for the two entities being compared, we could perform dimension reduction using JL Lemma if the dimensions of the two countries differs after the PCA reduction.

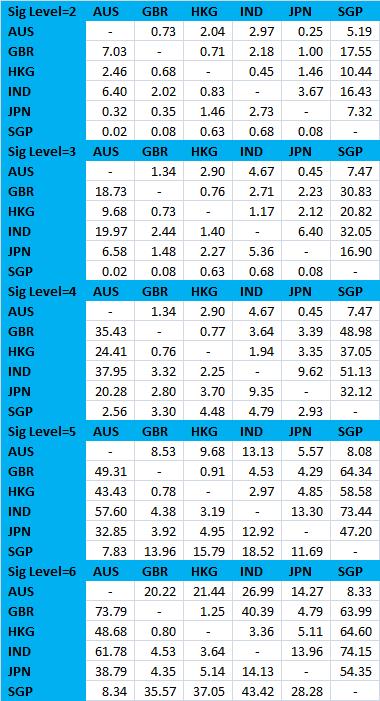

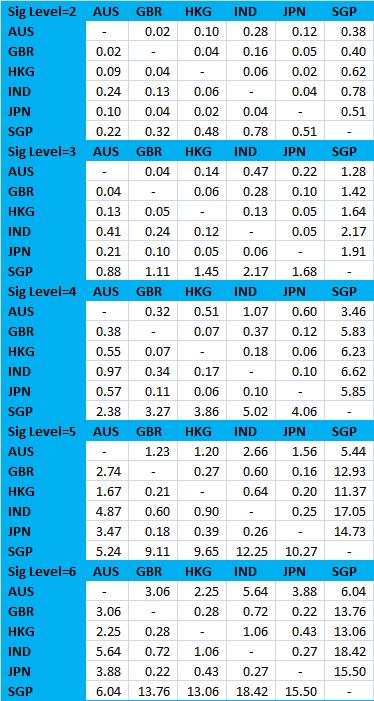

We repeat the calculations for different number of significant digits of the PCA reduction. This shows the fine granularity of the results that our distance comparison produces and highlights the issue that with PCA reduction there is loss of information, since with different number of significant digits employed in the PCA reduction, we get the result that different markets are similar. For example, in Figure 1b, AUS - SGP are the most similar markets when two significant digits are used and AUS - HKG are the most similar with six significant digits.

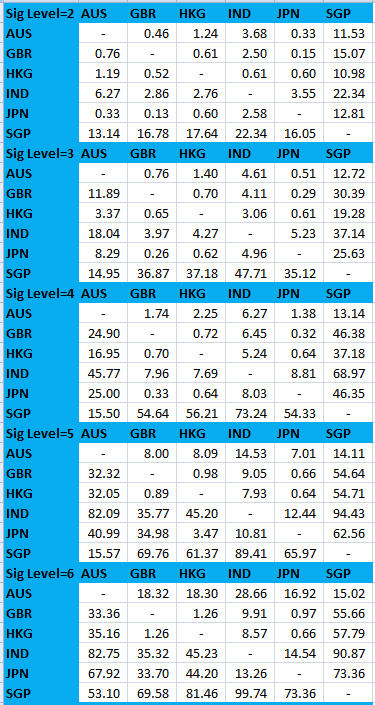

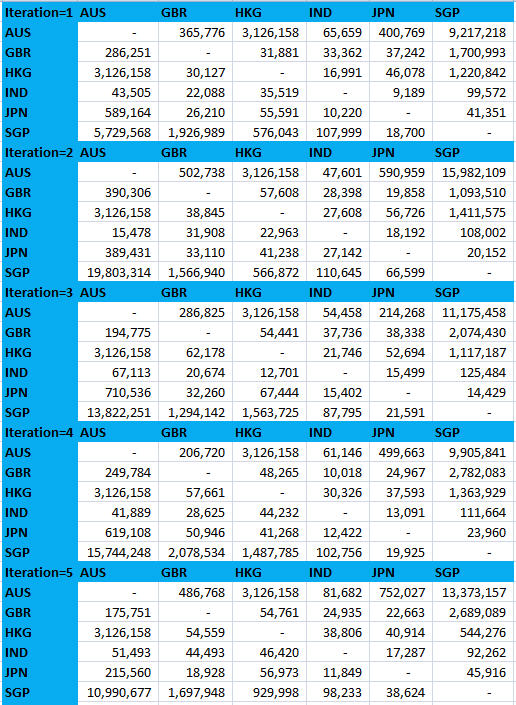

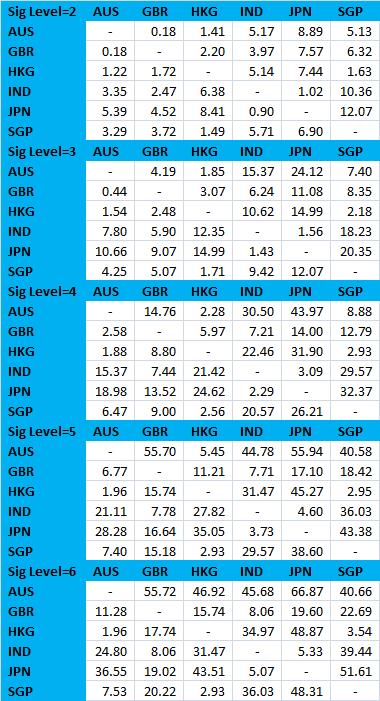

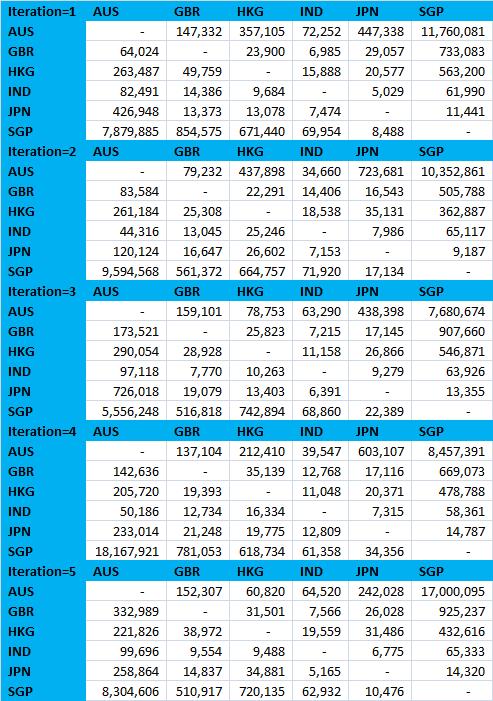

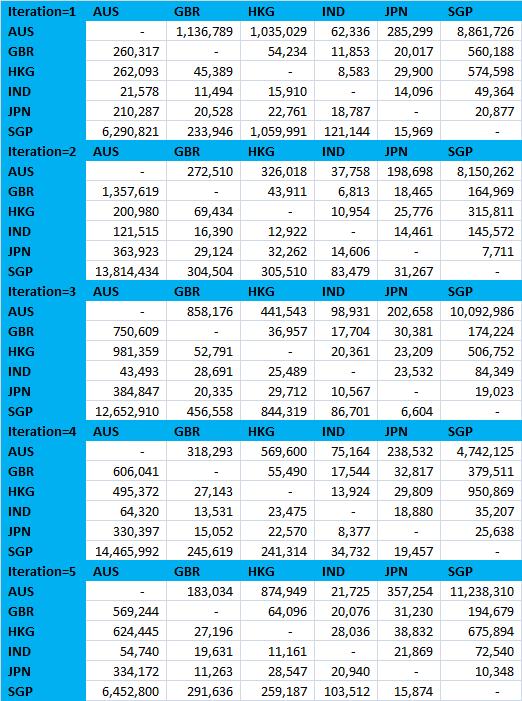

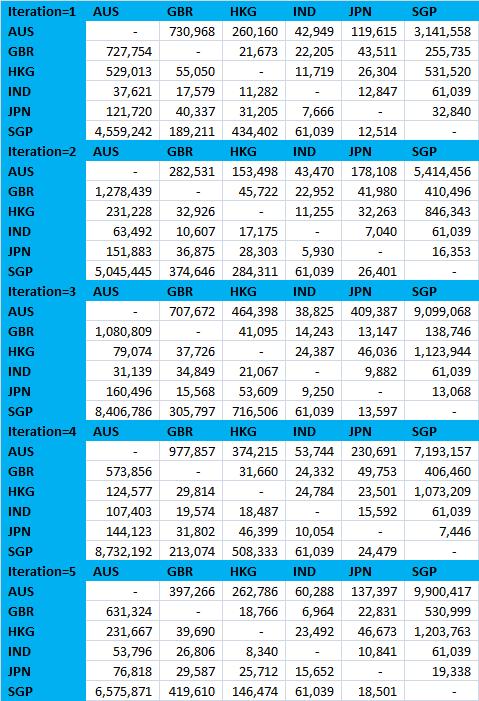

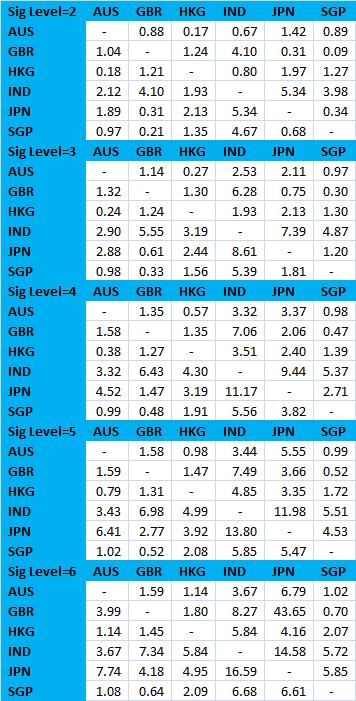

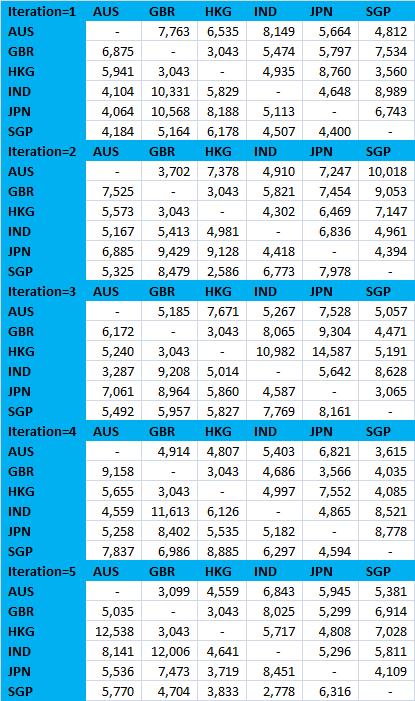

We illustrate another example, where we compare a randomly selected sub universe of securities in each market, so that the number of tickers retained would be comparable to the number of days for which we have data. The results are shown in Figure 2. The left table (Figure 2a) is for PCA reduction on a randomly chosen sub universe and the right table (Figure 2b) is for dimension reduction using JL Lemma for the same sub universe. We report the full matrix for the same reason as explained earlier and perform multiple iterations when reducing the dimension using the JL Lemma. A key observation is that the magnitude of the distances are very different when using PCA reduction and when using dimension reduction, due to the loss of information that comes with the PCA technique. It is apparent that using dimension reduction via the JL Lemma produces consistent results, since the same pairs of markets are seen to be similar in different iterations (in Figure 2b, AUS - IND are the most similar in iteration one and also in iteration five).

It is worth remembering that in each iteration of the JL Lemma dimension transformation we multiply by a different random matrix and hence the distance is slightly different in each iteration but within the bound established by JL Lemma. When the distance is somewhat close between two pairs of entities, we could observe an inconsistency due to the JL Lemma transformation in successive iterations. We discuss this as one area that would require further theoretical investigation in section 8.

Our approach could also be used when groups of securities are being compared within the same market, a very common scenario when deciding on the group of securities to invest in a market as opposed to deciding which markets to invest in. Such an approach would be highly useful for index construction or comparison across sectors within a market. (Kashyap 2017) summarizes the theoretical results from this paper and expands the example illustrations to open, high, low prices, volumes and price volatilities to provide a complete market microstructure study; relevant bits of this study to illustrate how our techniques can be applied to different kinds of variables are reproduced in section 7.2.

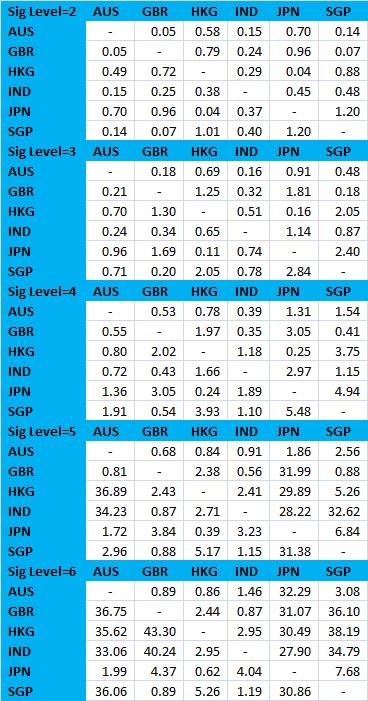

7.2 Comparison of Security Trading Volumes, High-Low-Open-Close Prices and Volume-Price Volatilities

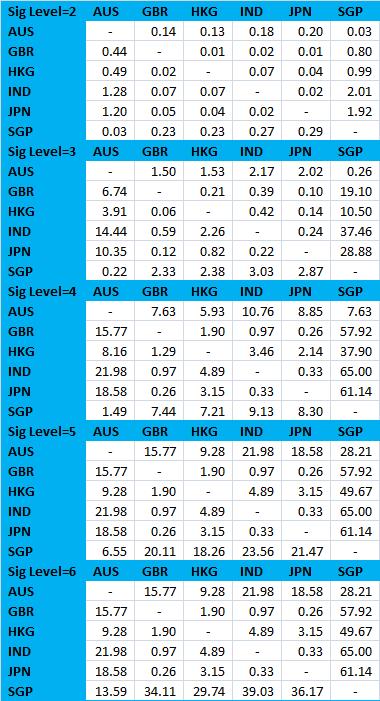

We provide several examples in (sections 7.3, 7.4, 7.5) complementary to (section 7.1) of how our techniques could be used to compare different countries based on the time series variables across all equity securities traded in that market. These illustrations are discussed in much greater detail as part of a complete study on market micro-structure in (Kashyap 2017). The data sample contains prices (open, close, high and low) and trading volumes for most of the securities from six different markets from Jan 01, 2014 to May 28, 2014 (Figure 3a). The time period under consideration, the number of securities and the bulk of the numerical analysis is similar to the comparisons done in section 7.1. To compare volatilities of prices and volumes, we calculate sixty day moving volatilities on the close price and trading volume and calculate the distance measure over the full sample and also across each of the randomly selected sub-samples.

7.3 Speaking Volumes Of: Comparison of Trading Volumes

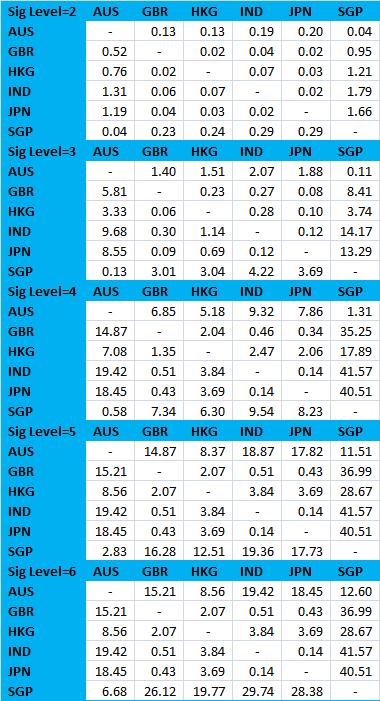

The results of the volume comparison over the full sample are shown in Figure 3b. For example, in Figure 3b, AUS - GBR are the most similar markets when two significant digits are used and AUS - GBR are the most similar with six significant digits. In this case the PCA and JL Lemma dimension reduction give similar results.

The random sample results are shown in Figure 4. The left table (Figure 4a) is for PCA reduction on a randomly chosen sub universe and the right table (Figure 4b) is for dimension reduction using JL Lemma for the same sub universe.

7.4 A Pricey Prescription: Comparison of Prices (Open, Close, High and Low)

7.4.1 Open Close

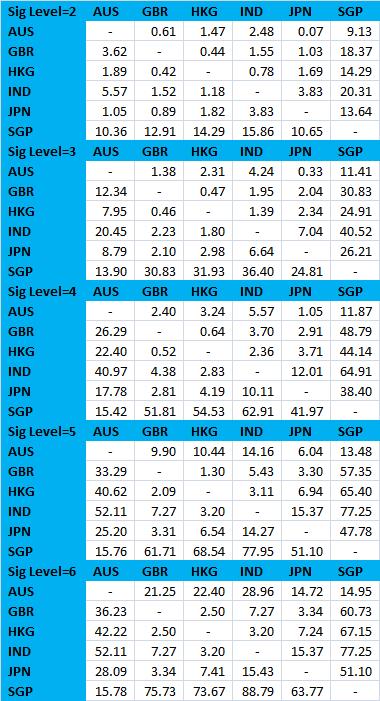

The results of a comparison between open and close prices over the full sample are shown in Figures 5, 5a, 5b. For example, in Figure 5b, AUS - SGP are the most similar markets when two significant digits are used and AUS - HKG are the most similar with six significant digits. The similarities between open and close prices, in terms of the distance measure, are also easily observed.

The random sample results are shown in Figures 6, 7. The left table (Figures 6a, 7a) is for PCA reduction on a randomly chosen sub universe and the right table (Figures 6b, 7b) is for dimension reduction using JL Lemma for the same sub universe. In Figure 7b, AUS - IND are the most similar in iteration one and also in iteration five.

7.4.2 High Low

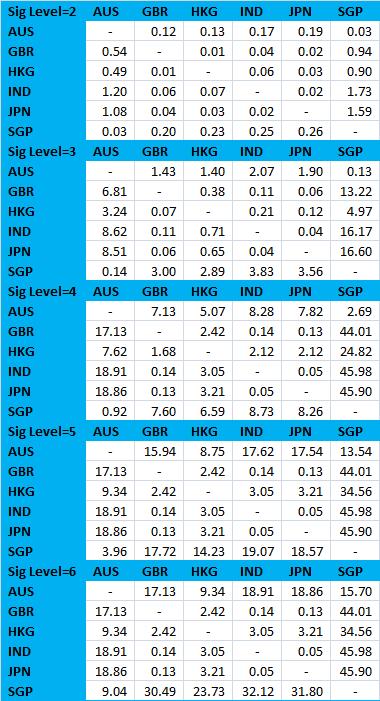

The results of a comparison between high and low prices over the full sample are shown in Figures 8, 8a, 8b. For example, in Figure 8a, AUS - SGP are the most similar markets when two significant digits are used and AUS - HKG are the most similar with six significant digits. The similarities between high and low prices are also easily observed.

The random sample results are shown in Figures 9, 10. The left table (Figures 9a, 10a) is for PCA reduction on a randomly chosen sub universe and the right table (Figures 9b, 10b) is for dimension reduction using JL Lemma for the same sub universe. In Figures 9b and 10b, AUS - IND are the most similar in iteration one and also in iteration five.

7.5 Taming the (Volatility) Skew: Comparison of Close Price / Volume Volatilities

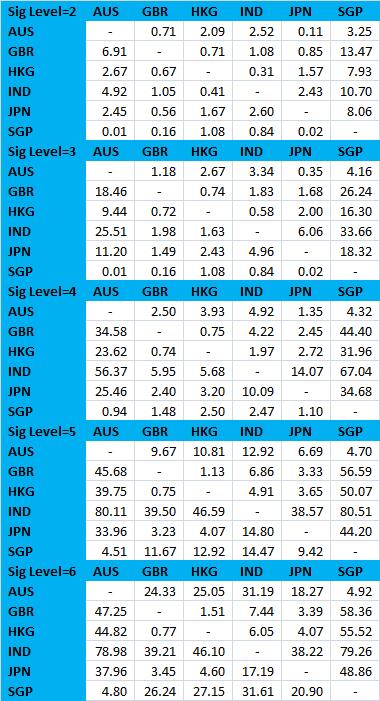

The results of a comparison between close price volatilities and volume volatilities over the full sample are shown in Figures 11, 11a, 11b. For example, in Figure 11a, AUS - GBR are the most similar markets when two significant digits are used and AUS - HKG are the most similar with six significant digits. In Figure 11b, AUS - GBR - IND are equally similar markets when two significant digits are used and AUS - GBR are the most similar with six significant digits. The difference in magnitudes of the distance measures for prices, volumes and volatilities is also easily observed. What this indicates is that, prices are from the most dissimilar or distant distributions, volatilities are less similar and volumes are from the most similar or overlapping distributions. As also observed in the volume comparisons, volume volatility comparisons give seemingly similar results when PCA or JL Lemma dimension reductions are used. By considering the price volatilities and creating portfolios of instruments that have dissimilar volatility distributions, we could reduce the overall risk or variance of the portfolio returns, becoming one potential way of mitigating the effects of wild volatility swings.

The random sample results are shown in Figures 12, 13. The left table (Figures 12a, 13a) is for PCA reduction on a randomly chosen sub universe and the right table (Figures 12b, 13b) is for dimension reduction using JL Lemma for the same sub universe. In Figure 12b AUS - SGP are the most similar in iteration one and also in iteration five. In Figure 13b, AUS - SGP are the most similar in iteration one and AUS- GBR in iteration five.

7.6 Other Complementary Case Studies

Below we mention examples of studies we are planning to undertake that can act as applications of the methodologies discussed here.

7.6.1 United Kingdom Crime Analysis

We are developing a separate application which applies the techniques in this article and also from network theory (Euler 1953; Wasserman & Faust 1994; Watts 1999; Aldous & Wilson 2003; Gribkovskaia, Halskau Sr. & Laporte 2007) to a crime data-set from the United Kingdom. The goal of this project is to identify regions with similar levels and types of crimes so that policy and enforcement decisions can be made based on lessons learnt from earlier episodes or from regions where certain legal measures have had a decent level of success. In addition, network interactions can help us to understand how crime waves might be spreading from one region to another and help with crime prevention. The crime data-set is publicly available at: UK Police Data.

7.6.2 Hong Kong and Shanghai Securities Comparison across Industrial Sectors

We are creating another numerical example on financial market data to find out which sectors in China and Hong Kong are more similar based on the stock prices and trading volumes of all securities listed on the Shanghai and Hong Kong stock exchange (Kashyap 2017 considers this question around the time when the Hong Kong and Shanghai stock exchanges were first electronically connected; though the main focus of this study is on how trading costs have changed due to this linking of the two financial markets). To perform this study, we could use any publicly available data-set downloadable from various market data providers.

7.7 Implementation Pointers

(Chaussé 2010) is a good reference for estimating the parameters of a normal distribution through the Generalized Method of Moments, GMM, (Cochrane 2009) using R package gmm. The numerical computation of a multivariate normal is often a difficult problem. (Genz 1992; Genz & Bretz 2009) describe a transformation that simplifies the problem and places it into a form that allows efficient calculation using standard numerical multiple integration algorithms. (Hothorn, Bretz & Genz 2001) give pointers for the numerical computation of multivariate normal probabilities based on the R package mvtnorm. (Manjunath & Wilhelm 2012) derive an explicit expression for the truncated mean and variance for the multivariate normal distribution with arbitrary rectangular double truncation. (Wilhelm & Manjunath 2010; Wilhelm 2015) have details on the R package tmvtnorm, for the truncated multivariate normal distribution including routines for the GMM Estimation for the Truncated Multivariate Normal Distribution. In (appendix 15), we list some R code snippets, that includes the Johnson-Lindenstrauss matrix transformation and a modification to the routine to calculate the Bhattacharyya distance, available currently in the R package fps. This modification allows much larger numbers and dimensions to be handled, by utilizing the properties of logarithms and the Eigen values of a matrix.

8 Possibilities for Future Research

There is a lot of research being done in developing distance measures, dimension reduction techniques and understanding the properties of distributions whose dimensions have been transformed. Such studies are aimed at developed better theoretical foundations as well faster algorithms for implementing newer techniques. We point out alternative approaches that might hold potential starting with some not so recent methods and then some newer techniques. (Chow & Liu 1968) present a method to approximate an dimensional discrete distribution by a product of several of its component distributions of lower order in such a way that the product is a probability extension of these distributions of lower order. A product approximation is a valid probability distribution. Only the class of second order distributions are used. There are second order approximations of which at most can be used in the approximation.

The uncertainty associated with a state estimate can be represented most generally by a probability distribution incorporating all knowledge about the state. The Kalman filter (Kalman 1960; End-note 10) exploits the fact that 1) given only the mean and variance (or covariance in multiple dimensions) of a distribution, the most conservative assumption that can be made about the distribution is that it is a Gaussian having the given mean and variance and 2) the fact that the application of a linear operator to a Gaussian distribution always yields another Gaussian distribution. Given the assumptions of 1) and 2) it is straightforward to show that the Kalman filter will yield the best possible estimate of the mean and variance of the state. The requirement that the mean and variance of the state is measurable represents little practical difficulty but the requirement that all observation and process models be linear is rarely satisfied in nontrivial applications. (Julier & Uhlmann 1996) examine an alternative generalization of the Kalman filter that accommodates nonlinear transformations of probability distributions through the use of a new representation of the mean and variance information about the current state.

(Székely, Rizzo & Bakirov 2007; Székely & Rizzo 2009; Lyons 2013) develop a new measure of dependence between random vectors called the Distance correlation. Distance covariance and distance correlation are analogous to product-moment covariance and correlation, but unlike the classical definition of correlation, distance correlation is zero only if the random vectors are independent. This is applicable to random vectors of arbitrary and not necessarily equal dimension and to any distributions with finite first moments. (Székely & Rizzo 2013) come up with the Energy distance, which is a statistical distance between the distributions of random vectors characterizing equality of distributions. The name energy derives from Newton’s gravitational potential energy (which is a function of the distance between two bodies), and there is an elegant relation to the notion of potential energy between statistical observations. Energy statistics (E-statistics) are functions of distances between statistical observations. The idea of energy statistics is to consider statistical observations as heavenly bodies governed by a statistical potential energy, which is zero if and only if an underlying statistical null hypothesis is true.

We chronicle some key simplifications we have used in our illustrative examples:

-

1.

A key limitation of our study is that we have reduced dimensions using PCA or randomly sampled a sub matrix from the overall data-set so that the length of time series available is in the range of the number of securities that could be compared. Using a longer time series for the variables would be a useful extension and a real application would benefit immensely from more history.

-

2.

We have used the simple formula for the Bhattacharyya distance applicable to multivariate normal distributions. The formulae we have developed over a truncated multivariate normal distribution or using a Normal Log-Normal Mixture could give more accurate results. Again, later works should look into tests that can establish which of the distributions would apply depending on the data-set under consideration.

-

3.

For the examples in section 7.2, for each market we have looked at seven variables, open, close, low, high, trading volume, close volatility and volume volatility. These variables can be combined using the expression for the multinomial distance to get a complete representation of which markets are more similar than others. We aim to develop this methodology and illustrate these techniques further in later works.

Once we have the similarity measures across groups of entities, a separate set of analysis can be performed to prudently select which policies or procedures can be transferred across similar entities. For example, across groups of securities, portfolios could be constructed to see how sensitive they are to different explanatory factors and then performance benchmarks could be used to gauge the risk return relationship.

When the distance is somewhat close between two pairs of entities, we could observe an inconsistency due to the JL Lemma transformation in successive iterations. It is worth remembering that if we perform multiple iterations of the JL Lemma dimension transformation (multiplying by a different random matrix); the distance could be slightly different in each iteration but within the bound established by JL Lemma. Though, in one iteration one pair could seem to be more similar than the other and the result could be reversed in the other iteration. When compared to other dimension reduction techniques such as PCA, due to loss of data, it is hard to know if the results are accurate at all when the distance between entities is too small. Theoretical bounds could be established with regards to what are the limits on the distance measure where such an inconsistency could result. Further to this, a huge branch of theoretical investigations can be undertaken regarding the interval over which the distance measure will fall when one of the random variables is multiplied by different random matrices governed by the JL-Lemma to effect the same dimension transformation.

A key point to remember is that the findings with respect to the similarity of different entities are based on the data available for the particular time period under consideration. There could be fundamental changes in the true data generating processes, which are generally unknown and the same entities for a different time period could give entirely different results. Hence, any real application that continues to collect the relevant data that is generated, should calculate the metrics on a moving time period basis (rolling) and use the latest results that are computed. Needless to say, this brings up the question of how much of the recent history we should use as we make our decisions. While our present econometric tools fall short of providing concrete answers, many practical aids and suggestions are available in any econometric guide (Hamilton 1994). This is of course true for most (all?) empirical data investigations.

Another improvement could be to normalize, or, standardize distance measures. This is perhaps applicable not just to the Bhattacharyya distance, but to other types of distance metrics as well. For example, the covariance is a useful number, but its use is magnified and the intuitive lessons compounded by the use of correlations derived from covariance measures. Again, we need to be wary of this path since anything that can be measured is magical; that is, there is always something bigger or something smaller, which can be expressed as a need to contend with the concepts of the infinite, or, the infinitesimal. So, by standardizing something we might reduce the range of the values, but it might be necessary to retain the number of significant digits that give us meaningful comparisons. Also, since we wish to compare more than two entities, it might be helpful to come up with metrics that can combine multiple distance measures at the same time. Though, it would suffice to be able to combine two of the distance measures at a time, since that is how we would compare any two probabilistic entities; just as in the covariance case other possibilities such as combining more than two at a time need not be ruled out.

9 Conclusions

We have discussed various measures of similarity between probability distributions. We have shown how the marriage between the Bhattacharyya distance and the Johnson-Lindenstrauss Lemma provides us with a novel and practical methodology that allows comparisons between any two probability distributions. This combination becomes, to our limited knowledge, an example (the example?) of perfectly harmonious matrimony. We demonstrated a relationship between covariance and distance measures based on a generic extension of Stein’s Lemma. We have provided numerical examples based on security prices across six countries where we have compared trading volumes, open-close-high-low prices, price and volume volatilities; all of which act as how to guides of the techniques developed here for real life applications. We have also discussed how this methodology lends itself to numerous applications outside the realm of finance and economics.

10 Acknowledgements and End-notes

-

1.

My colleagues at SolBridge International School of Business are always full of great suggestions to improve all my papers; in particular: Dr. Chia Hsing Huang, Dr. Sangoo Shin, Dr. Xingcai Meng, Dr. Yun Jie Joseph, Dr. Narasimha Rao Kowtha, Dr. Aye Mengistu Alemu, Dr. Ben Agyei-Mensah, Dr. Taylan Urkmez, Dr. Alejandra Marin, Dr. Jerman Rose, Dr. Awan Mahmood, Dr. Jay Won Lee and Dr. KyunHwa Kim raised some interestingly tough questions at our monthly Brown Bag seminars that resulted in significant improvements in section 4 and section 8. The students of SolBridge International School of Business continue to be the inspiration for many of our papers by bringing us their concerns. In this case their worries about how their daily life is being bombarded by numerous sources of information showed us that information reduction would have many potential benefits.

-

2.

Numerous seminar participants, particularly at a few meetings of the econometric society and various finance organizations, and the faculty members of City University of Hong Kong suggested ways to improve the core results in the manuscript and prompted us to find ways to express the intuition for why we need the main results. The views and opinions expressed in this article, along with any mistakes, are mine alone and do not necessarily reflect the official policy or position of either of my affiliations or any other agency.

-

3.

In mathematics, the Mellin transform is an integral transform that may be regarded as the multiplicative version of the two-sided Laplace transform (End-note 12). The Mellin transform of a function is

The inverse transform is

This integral transform is closely connected to the theory of Dirichlet series (End-note 11), and is often used in number theory, mathematical statistics, and the theory of asymptotic expansions; it is closely related to the Laplace transform (End-note 13) and the Fourier transform (End-note 14), and the theory of the gamma function and allied special functions. To avoid extended discussions, we only provide some details here. The following link has more details: Mellin Transform, Wikipedia Link

-

4.

In mathematics, the G-function was introduced by Cornelis Simon Meijer (Meijer 1936) as a very general function intended to include most of the known special functions as particular cases. This was not the only attempt of its kind: the generalized hypergeometric function and the MacRobert E-function had the same aim, but Meijer’s G-function was able to include those as particular cases as well. The first definition was made by Meijer using a series; nowadays the accepted and more general definition is via a line integral in the complex plane, introduced in its full generality by Arthur Erdelyi in 1953. Meijer G-Function, Wikipedia Link

-

5.

In numerical analysis, the Newton-Cotes formulas, also called the Newton-Cotes quadrature rules or simply Newton-Cotes rules, are a group of formulas for numerical integration (also called quadrature) based on evaluating the integrand at equally spaced points. Newton-Cotes formulas, Wikipedia Link

-

6.

In statistics, Rao’s score test, also known as the score test or the Lagrange multiplier test (LM test) in econometrics, is a statistical test of a simple null hypothesis that a parameter of interest is equal to some particular value . It is the most powerful test when the true value of is close to . The main advantage of the score test is that it does not require an estimate of the information under the alternative hypothesis or unconstrained maximum likelihood. Score or Lagrange Multiplier Test, Wikipedia Link

-

7.

In probability theory and statistics, skewness is a measure of the asymmetry of the probability distribution of a real-valued random variable about its mean. The skewness value can be positive or negative, or undefined. Skewness, Wikipedia Link

-

8.

In probability theory and statistics, kurtosis (from Greek: kyrtos or kurtos, meaning “curved, arching”) is a measure of the “tailedness” of the probability distribution of a real-valued random variable. In a similar way to the concept of skewness, kurtosis is a descriptor of the shape of a probability distribution and, just as for skewness, there are different ways of quantifying it for a theoretical distribution and corresponding ways of estimating it from a sample from a population. Depending on the particular measure of kurtosis that is used, there are various interpretations of kurtosis, and of how particular measures should be interpreted. Kurtosis, Wikipedia Link

-

9.

In mathematics, the Euclidean distance or Euclidean metric is the “ordinary” straight-line distance between two points in Euclidean space. With this distance, Euclidean space becomes a metric space. The associated norm is called the Euclidean norm. Older literature refers to the metric as the Pythagorean metric. A generalized term for the Euclidean norm is the norm or distance. Euclidean Distance, Wikipedia Link

-

10.

In statistics and control theory, Kalman filtering, also known as linear quadratic estimation (LQE), is an algorithm that uses a series of measurements observed over time, containing statistical noise and other inaccuracies, and produces estimates of unknown variables that tend to be more accurate than those based on a single measurement alone, by estimating a joint probability distribution over the variables for each timeframe. The Kalman filter has numerous applications for guidance, navigation, and control of vehicles, particularly aircraft and spacecraft. Furthermore, the Kalman filter is a widely applied concept in time series analysis used in fields such as signal processing and econometrics. Kalman filters also are one of the main topics in the field of robotic motion planning and control, and they are sometimes included in trajectory optimization. Kalman Filter, Wikipedia Link

-

11.

In mathematics, a Dirichlet series is any series of the form

where is complex, and is a complex sequence. Dirichlet Series, Wikipedia Link

-

12.

In mathematics, the two-sided Laplace transform or bilateral Laplace transform is an integral transform equivalent to probability’s moment generating function. Two-sided Laplace transforms are closely related to the Fourier transform, the Mellin transform, and the ordinary or one-sided Laplace transform. If is a real or complex valued function of the real variable defined for all real numbers, then the two-sided Laplace transform is defined by the integral,

-

13.

In mathematics, the Laplace transform of a function , defined for all real numbers , is the function , which is a unilateral transform defined by

where is a complex number frequency parameter. , with real numbers and . An alternate notation for the Laplace transform is instead of . Laplace Transform, Wikipedia Link

-

14.

The Fourier transform (FT) decomposes a function of time (a signal) into the frequencies that make it up, in a way similar to how a musical chord can be expressed as the frequencies (or pitches) of its constituent notes. The Fourier transform of a function of time is itself a complex-valued function of frequency, whose absolute value represents the amount of that frequency present in the original function, and whose complex argument is the phase offset of the basic sinusoid in that frequency. The Fourier transform is called the frequency domain representation of the original signal. The term Fourier transform refers to both the frequency domain representation and the mathematical operation that associates the frequency domain representation to a function of time. The Fourier transform is not limited to functions of time, but in order to have a unified language, the domain of the original function is commonly referred to as the time domain. The Fourier transform of the function is traditionally denoted by adding a circumflex: . There are several common conventions for defining the Fourier transform of an integrable function . One definition that is commonly used for any real number is,

When the independent variable represents time, the transform variable represents frequency (e.g. if time is measured in seconds, then the frequency is in hertz). Under suitable conditions, is determined by for any real number , via the inverse transform:

-

15.

(Lawson 1985; Keynes 1937; 1971; 1973; McManus & Hastings 2005; Simon 1962; Kashyap 2017; Bertsekas 2002; Henderson & Searle 1981) are cited in the appendix of supplementary material. They discuss additional concepts related to uncertainty, unintended consequences, probability distributions and linear algebra. Some of these references are also used in the proofs of the mathematical results.

11 References

-

1.

Achlioptas, D. (2003). Database-friendly random projections: Johnson-Lindenstrauss with binary coins. Journal of computer and System Sciences, 66(4), 671-687.

-

2.

Aherne, F. J., Thacker, N. A., & Rockett, P. I. (1998). The Bhattacharyya metric as an absolute similarity measure for frequency coded data. Kybernetika, 34(4), 363-368.

-

3.

Aldous, J. M., & Wilson, R. J. (2003). Graphs and applications: an introductory approach (Vol. 1). Springer Science & Business Media.

-

4.

Aroian, L. A. (1947). The probability function of the product of two normally distributed variables. The Annals of Mathematical Statistics, 265-271.

-

5.

Aroian, L. A., Taneja, V. S., & Cornwell, L. W. (1978). Mathematical forms of the distribution of the product of two normal variables. Communications in Statistics-Theory and Methods, 7(2), 165-172.

-

6.

Bansal, R., & Yaron, A. (2004). Risks for the long run: A potential resolution of asset pricing puzzles. The Journal of Finance, 59(4), 1481-1509.

-

7.

Barro, R. J. (2006). Rare disasters and asset markets in the twentieth century. The Quarterly Journal of Economics, 823-866.

-

8.

Beath, C., Becerra-Fernandez, I., Ross, J., & Short, J. (2012). Finding value in the information explosion. MIT Sloan Management Review, 53(4), 18.

-

9.

Berner, E. S., & Moss, J. (2005). Informatics challenges for the impending patient information explosion. Journal of the American Medical Informatics Association, 12(6), 614-617.

-

10.

Bertsekas, D. P. (2002). Introduction to Probability: Dimitri P. Bertsekas and John N. Tsitsiklis. Athena Scientific.

-

11.