Number of claims and ruin time for a refracted risk process

Yanhong Li

Zbigniew Palmowski

Chunming Zhao

Chunsheng Zhang

Sichuan University, Chengdu, 610065, China.

Email: yanhonglink@qq.comFaculty of Pure and Applied Mathematics,

Wrocław University of Science and Technology,

Wyb. Wyspiańskiego 27, 50-370 Wrocław, Poland, e-mail: zbigniew.palmowski@gmail.comDepartment of Statistics,

School of Mathematics, Southwest Jiaotong University, Chengdu, Sichuan, 611756, China. Email:cmzhao@swjtu.cnSchool of mathematical Sciences and LPMC Nankai University, Tianjin 300071, China.

Email: zhangcs@nankai.edu.cn

Abstract

In this paper, we consider a classical risk model refracted at given level.

We give an explicit expression for the joint density of the ruin time and the cumulative number of claims counted up to ruin time.

The proof is based on solving some integro-differential equations and employing the Lagrange’s Expansion Theorem.

Keywords: threshold dividend strategy, ruin time, number of claims, refracted risk process.

1 Introduction

The joint density of the ruin time and the numbers of claims counted until ruin time has been already studied for a classical risk process over last years.

Dickson [3] derived special expression for it using probabilistic arguments. Landriault et al. [11] analyzed this object

for the Sparre Andersen risk model with the exponential claims. Later Frostig et al. [6] generalized it to the case of a renewal risk model

with the phase-type claims and inter-arrival times. The main tool used there was the duality between the risk model and a workload of a single server queueing

model. Zhao and Zhang [20] considered a delayed renewal risk model, where the claim size is Erlang distributed and the inter-arrival time is assumed to be infinitely divisible.

Our goal is to derive expression for the joint density of the ruin time and the numbers of claims counted until ruin time for a refracted classical risk process (see

Kyrianou and Loeffen [9] for a formal definition). It is also called a compound Poisson risk model under a threshold strategy. The latter process is a classical risk process whose dynamic is changed by subtracting off a fixed linear drift

whenever the cumulative risk process is above a pre-specified level . This subtracting of the linear drift corresponds to the dividend payments

and the considered strategy is also known as a threshold strategy.

Dividend strategies for insurance risk models were first proposed by De Finetti [2] to reflect more realistically the surplus cash flows in an insurance portfolio.

More recently, many kind of risk related quantities under threshold dividend

strategies have been studied by Lin and Pavlova [17], Zhu and Yang [22],

Lu and Li [14], [15], [16],

Badescu, Drekic and Landriault [1], Gao and Yin [7] (see references therein).

The case when the drift of the refracted process is disappearing (everything above threshold is paid as dividends) is called barrier strategy, see

Lin et al. [18], Li and Garrido [12], Zhou [21] and in the references therein.

The paper is organized as follows. In Section 2 we define the model we deal with in this paper.

In Section 3 we recall properties of the translation operator and the root of the Lundberg fundamental equation. In particular, we introduce the Lagrange’s expansion theorem and some notation. In Section 4 we construct two integro-differential equations identifying the joint Laplace transform of joint density of the numbers of claims counted up to ruin time

and the ruin time.

Analytical solutions of these two integro-differential equations are given in Section 5. Applying the Lagrange’s expansion theorem in Section 6

we give the expression for above mentioned density.

2 Model

The classical risk process is given by

(1)

where denotes initial capital, is the premium rate and

represents the total amount of claims appeared up to time . That is, are non-negative i.i.d. random variables with pdf and cdf and is an independent Poisson process with a parameter .

To take into account dividend payments paid when regulated process (after deduction of dividends) is above fixed threshold level , we consider so-called refracted process given formally for by:

(2)

and .

In this case denotes intensity of dividend payments, see Figure 1.

Throughout this paper, we will assume that , which means refracted process tends to infinity almost surely.

We can then consider the ruin time:

( if ruin does not occur). Note that represents the number of claims counted until the ruin time.

The main goal of this paper is identification of the density of .

We start from analyzing its Laplace transform:

(3)

(4)

where

is the joint density of when . In above definition we have and .

Later we will use the following notation

(5)

and

(6)

3 Preliminaries

In this section we introduce few facts used further in this paper.

We start from recalling the translation operator ; see Dickson and Hipp [4].

For any integrable real-valued function it is defined as

The operator satisfies the following properties:

1.

which is the Laplcae transform of ;

2.

The operator is commutative, i.e. . Moreover, for and

(7)

More properties of the translation operator can be found in Li and Garrido [13] and Gerber and Shiu [8].

For any function we will denote by its Laplace Transform, that is .

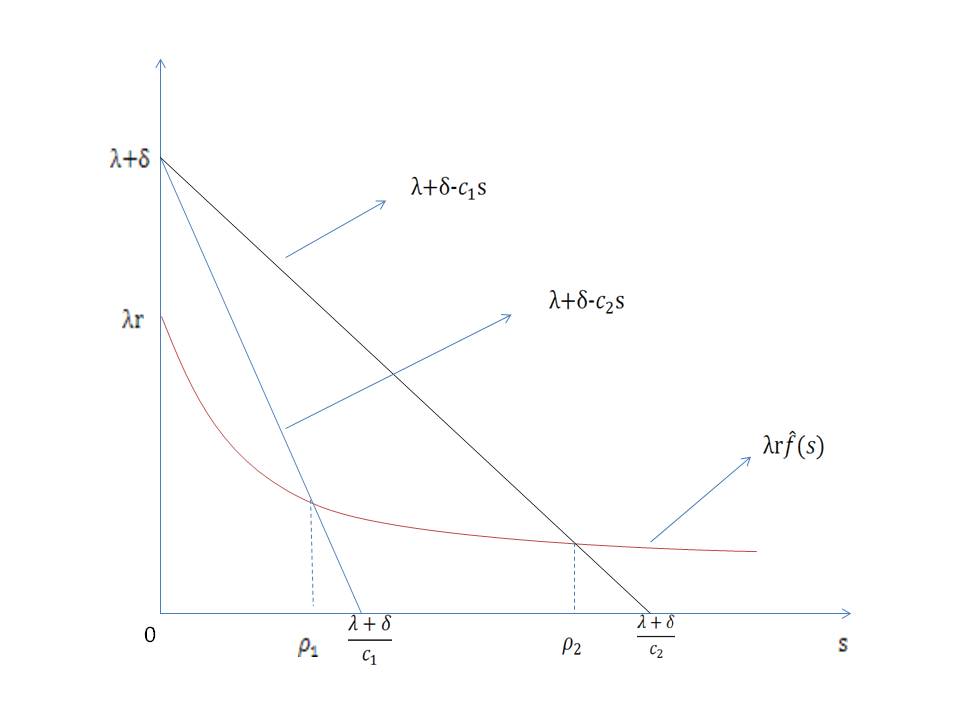

Next, for let be the positive root of the Lundberg fundamental equation

(8)

The positive roots always exists for ; see Figure 2.

Figure 2: Roots for Lundberg’s fundamental equation.

Lagrange’s Expansion Theorem.

In this paper we will also use the Lagrange’s Expansion Theorem; see pages 251-326 of Lagrange [10].

Given two functions and which are both analytic on and inside a contour surrounding a point , if satisfies the inequality

(9)

for every on the perimeter of , then , as a function of , has exactly one zero in the interior of , and we further have:

(10)

Finally, we define also the impulse function

with . We denote , with and the -fold convolution of with itself, where

for two functions and supported on .

4 Integro-differential equations for the joint Laplace transform

In this section, we derive two integro-differential equations identifying defined in

(3). We will follow the idea given in Lin and Pavlova [17].

Denote

(11)

Theorem 4.1

The joint Laplace transform satisfies the following integro-differential equations:

(12)

with the boundary condition

(13)

Remark 4.2

Note that from the integro-differential equations (12) follows that the joint Laplace transform with initial surplus above the barrier depends on the respective function with initial surplus below the barrier, but the reverse relationship does not hold true.

Proof.

Let first . Then conditioning on the occurrence of the first claim we will have two cases: the first claim occurs before the surplus has reached the barrier level

or it occurs after reaching this barrier. There are also two other cases at the moment of the arrival of the first claim:

either the risk process starts all over again with new initial surplus or the first claim leads already to ruin. Hence:

(14)

where .

Changing variables in (14) and rearranging leads to the following equation for :

(15)

Differentiating both sides of (15) with respect to yields

first equation.

Similarly, for we have:

(16)

Differentiating both sides of (16) with respect to produces the second equation.

Note also that from equations (15) and (16) it follows that is continuous at and hence (13) holds.

This completes the proof.

5 The analytical expression for

In this section, we derive the analytical expression for () using the translation operator introduced in Section 3.

Theorem 5.1

The function can be expressed analytically as follows:

(17)

where

(18)

Proof. We adopt the approach of Willmot and Dickson [19].

Consider the second equation in (12) for .

For a fixed , we multiply both sides of this

equation by and integrate it with respect to from to :

Integrating by parts gives:

Hence

and simple rearranging leads to:

(19)

Taking for the solution of the Lundberg Fundamental Equation (8) gives

The expression for could be also derived in terms of the translation operator.

Theorem 5.2

The function can be expressed analytically in the following form:

(22)

where

(23)

and

(24)

with .

Proof. Note that the first equation in (12) does not involve the barrier level :

(25)

The information about the barrier is included in the boundary condition:

Lin et al. [17] showed that the general solution of (25) is of the form

(26)

where is the joint Laplace transform of density of the ruin time and number of claims counted up to ruin time

for the classical risk process (1) without any barrier applied.

That is,

(27)

for

(28)

In above equation (26) the quantity is a constant which we can specify by implementing (26)

and (21):

(29)

We express now the function in terms of a compound geometric distribution.

Indeed, since also satisfies equation (25), taking Laplace transforms of its both sides for sufficiently large

gives:

(30)

To determine the constant term in (30), we substitute the solution

of the Lundberg Fundamental Equation (8) for :

Dividing above equation by and simple rearranging along with implementation of the formula (7) produces:

Inverting this Laplace transforms gives classical renewal equation:

(32)

having the solution given as an Neumann infinite series (23).

To prove the last statement (24) note that the function satisfies the following integro-differential equation:

(33)

with the initial condition .

To get the analytical expression of

we take the Laplace transforms of both sides of (33) for sufficiently large (). This yields:

Since ,

(34)

Recalling that is the root of (8), we can rewrite (34) as

which, by dividing by and implementing (7), produces:

(35)

Inverting the Laplace transforms in (35) leads to the equation (24).

Including all above identities in (26) completes the proof.

6 The joint density of

In this section we

give the joint density of the number of claims counted until ruin time and the ruin time using

the Lagrange’s Expansion theorem.

We start with few facts

that will be useful in the proof of the main result.

Recall that by we denote the joint density of for the classical risk process (1)

(with infinite barrier ); see (28).

For we denote

Lemma 6.1

We have

For the following holds:

(36)

where

(37)

Proof.

Using Lagrange’s Expansion Theorem presented in Section 2 with

, , and () and

the Lundberg fundamental equation (8) we can conclude the following identity:

Substituting and rearranging leads to:

(38)

Therefore,

(39)

Since defined in (27)

is the joint Laplace transform under the classical compound Poisson risk model without a barrier we can use

Dickson [3] to complete the proof.

Using above lemmas we will prove the main result of this paper.

Theorem 6.3

For and the joint density of the number of claims until ruin and the time to ruin is given by

where for

Proof.

In order to get the joint density , we have to take inverse Laplace transform with respect to rather than and .

To do this we must find firstly the relationship between transforms with respect to , and by applying the Lagrange’s Expansion theorem.

For convenience, we will denote:

For and the joint density of the number of claims until ruin and the time to ruin is given by

(50)

where

Proof.

To obtain an expression for we first consider defined in (18).

Using (39) we can derive:

(51)

Moreover, substituting (43), (51) and (38) into (17) gives:

(52)

Comparing equations (52) and (4) completes the proof.

Acknowledgements

This research is support by the National Natural Science Foundation of China (Grant No. 11271164)

and by the FP7 Grant PIRSES-GA-2012-318984.

Zbigniew Palmowski is supported by the National Science Centre under the grant 2015/17/B/ST1/01102

(2016-2019).

References

[1]

A. Badescu, S. Drekic, and D. Landriault.

Analysis of a threshold dividend strategy for a MAP risk model.

Scandinavian Actuarial Journal, 2007(4):227–247, 2007.

[2]

B. De Finetti.

Su un’impostazione alternativa della teoria collettiva del rischio.

In Transactions of the XVth international congress of

Actuaries, pages 433–443, 1957.

[3]

D. C. M. Dickson.

The joint distribution of the time to ruin and the number of claims

until ruin in the classical risk model.

Insurance: Mathematics and Economics, 50(3):334–337, 2012.

[4]

D. C. M. Dickson and C. Hipp.

On the time to ruin for Erlang (2) risk processes.

Insurance: Mathematics and Economics, 29(3):333–344, 2001.

[5]

D. C. M. Dickson and G. E. Willmot.

The density of the time to ruin in the classical Poisson risk

model.

Astin Bulletin, 35(1):45–60, 2005.

[6]

E Frostig, S. M. Pitts, and K. Politis.

The time to ruin and the number of claims until ruin for phase-type

claims.

Insurance: Mathematics and Economics, 51(1):19–25, 2012.

[7]

H. Gao and C. Yin.

The perturbed Sparre Andersen model with a threshold dividend

strategy.

Journal of Computational and Applied Mathematics,

220(1-2):394–408, 2008.

[8]

H. U. Gerber and E. S. W. Shiu.

The time value of ruin in a Sparre Andersen model.

North American Actuarial Journal, 9(2):49–69, 2005.

[9]

A. E. Kyprianou and R. L. Loeffen.

Refracted Lévy processes.

Annales De L’ Institut Henri Poincaré Probabilités Et

Statistiques, 46(1):24–44, 2010.

[10]

J. L. Lagrange.

Nouvelle méthode pour résoudre les équations

littérales par le moyen des séries.

Chez Haude et Spener, Libraires de la Cour & de l’Acad¨¦mie royale,

1770.

[11]

D. Landriault, T. Shi, and G. E. Willmot.

Joint densities involving the time to ruin in the Sparre Andersen

risk model under exponential assumptions.

Insurance: Mathematics and Economics, 49(3):371–379, 2011.

[12]

S. Li and J. Garrido.

On a class of renewal risk models with a constant dividend barrier.

Insurance: Mathematics and Economics, 35(3):691–701, 2004.

[13]

S. Li and J. Garrido.

On ruin for the Erlang (n) risk process.

Insurance: Mathematics and Economics, 34(3):391–408, 2004.

[14]

S. Li and Y. Lu.

The distribution of total dividend payments in a Sparre Andersen

model.

Statistics and Probability Letters, 79(9):1246–1251, 2009.

[15]

S. Li and Y. Lu.

On the time and the number of claims when the surplus drops below a certain level.

Scandinavian Actuarial Journal, 5: 420–445, 2016.

[16]

Y. Lu and S. Li.

The Markovian regime-switching risk model with a threshold dividend strategy.

Insurance: Mathematics and Economics, 44(2):296–303, 2009.

[17]

X. S. Lin and K. P. Pavlova.

The compound Poisson risk model with a threshold dividend strategy.

Insurance: Mathematics and Economics, 38(1):57–80, 2006.

[18]

X. S. Lin, G. E. Willmot, and S. Drekic.

The classical risk model with a constant dividend barrier: analysis

of the Gerber-Shiu discounted penalty function.

Insurance: Mathematics and Economics, 33(3):551–566, 2003.

[19]

G. E. Willmot and D. C. M. Dickson.

The Gerber-Shiu discounted penalty function in the stationary

renewal risk model.

Insurance: Mathematics and Economics, 32(3):403–411, 2003.

[20]

C. Zhao and C. Zhang.

Joint density of the number of claims until ruin and the time to ruin

in the delayed renewal risk model with Erlang (n) claims.

Journal of Computational and Applied Mathematics, 244:102–114,

2013.

[21]

X. Zhou.

On a classical risk model with a constant dividend barrier.

North American Actuarial Journal, 9(4):95–108, 2005.

[22]

J. Zhu and H. Yang.

Ruin theory for a Markov regime-switching model under a threshold

dividend strategy.

Insurance: Mathematics and Economics, 42(1):311–318, 2008.