Local Parametric Estimation in High Frequency Data111We are indebted to Simon Clinet, Takaki Hayashi, Dacheng Xiu, participants of the seminars in Berlin and Tokyo and conferences in Osaka, Toyama, the SoFie annual meeting in Hong Kong, the PIMS meeting in Edmonton for valuable comments, which helped in improving the quality of the paper.

Abstract

In this paper, we give a general time-varying parameter model, where the multidimensional parameter possibly includes jumps. The quantity of interest is defined as the integrated value over time of the parameter process . We provide a local parametric estimator (LPE) of and conditions under which we can show the central limit theorem. Roughly speaking those conditions correspond to some uniform limit theory in the parametric version of the problem. The framework is restricted to the specific convergence rate . Several examples of LPE are studied: estimation of volatility, powers of volatility, volatility when incorporating trading information and time-varying MA(1).

Keywords: integrated volatility; market microstructure noise; powers of volatility; quasi maximum likelihood estimator

1 Introduction

Modeling dynamics is essential in various fields, including finance, economics, physics, environmental engineering, geology and sociology. Time-varying parametric models can deal with a specific problem in dynamics, namely, the temporal evolution of systems. The extensive literature on time-varying parameter models and local parametric methods include and are not limited to Fan and Gijbels (1996), Hastie and Tibshirani (1993) or Fan and Zhang (1999) when regression and generalized regression models are involved, locally stationary processes following the work of Dahlhaus (1997, 2000), Dahlhaus and Rao (2006), or any other time-varying parameter models, e.g. Stock and Watson (1998) and Kim and Nelson (2006).

In this paper, we propose to specify local parametric methods in the particular context of high-frequency statistics for a broad class of problems. Local methods have been used extensively in the high-frequency data literature, see e.g. Mykland and Zhang (2009, 2011), Kristensen (2010), Reiß (2011) or Jacod and Rosenbaum (2013) among many others. If we define as the horizon time, the (random) target quantity in this monograph is defined as the integrated parameter

| (1) |

which can be equal to the volatility, the covariation between several assets, the variance of the microstructure noise, the friction parameter of the model with uncertainty zones (see Example 4.4 for more details), the time-varying parameters of the MA(1) model, etc. To estimate the integrated parameter, we estimate the local parameter on each block by using the parametric estimator on the observations within the block and take a weighted sum of the local parameter estimates, where each weight is equal to the corresponding block length. We call the obtained estimator the local parametric estimator (LPE).

In Section 3, we investigate conditions under which we can establish the related central limit theorem with convergence rate , where is the (possibly expected) number of observations. The framework is such that the local block length vanishes asymptotically. Basically, we aim to provide the statistician with a transparent and as simple as possible device to tackle the time-varying parameter problem based on central limit theory in the parametric version of the problem. The original key probabilistic step of the proof, which formally allows for switching from random to deterministic parameter, is the use of regular conditional distribution theory (see, e.g., Breiman (1992)). The price to pay is some kind of uniformity in the parametric limit theory results, and to show that some deviation between the parametric and the time-varying parameter model vanishes asymptotically.

In Section 4, the technology is used on five distinct examples to derive the related central limit theorems. As far as the authors know, all those results are new. Depending on the considered example, the LPE is useful for one or several of the following reasons:

-

robustness: the LPE is robust to time-varying parameters (such as the noise variance, from the model with uncertainty zones, the parameters of the MA(1) process) which are usually assumed constant. This is the case of all our examples, except for Example 4.3.

We describe the five examples in what follows. To estimate integrated volatility under noisy observations, Xiu (2010) studied the quasi-maximum likelihood-estimator (QMLE) originally examined in Aït-Sahalia et al. (2005), showed the corresponding asymptotic theory when the variance of the noise is fixed and obtained a convergence rate , which is optimal (see Gloter and Jacod (2001)). More recently, Aït-Sahalia and Xiu (2016) establish that it is robust to shrinking noise satisfying and Da and Xiu (2017) obtains central limit theorem with rate ranging from to depending on the magnitude of the noise. When assuming that it is , we show that the LPE of the QMLE is optimal (with rate ) and furthermore robust to time-varying noise variance.

Another important problem, which goes back to Barndorff-Nielsen and Shephard (2002), is the estimation of higher powers of volatility. To do that, we define a LPE where the local estimates are powers of the QMLE of volatility. Under the assumption on small noise , we show that this estimator is optimal and robust to time-varying noise variance. This is an example where the global approach does not work as the QMLE is only consistent when estimating volatility.

A more recent problem is the estimation of volatility when incorporating trading information. To do that, Li et al. (2016) assume that the noise is a parametric function of trading information with a remaining noise component of order . Their strategy consists in first estimating the parametric part of the noise, and then take the sum of square pre-estimated efficient returns. They also advocate for the use of the QMLE after price pre-estimation although they do not provide the associated limit theory. We show that the latter approach, when considering the LPE of QMLE, is optimal and provides a better asymptotic variance (AVAR) than the former technique. In addition, a modification of the local estimator as in Example 2 allows us to estimate higher powers of volatility.

A concurrent ultra high frequency approach to model the observed price was given in Robert and Rosenbaum (2011, 2012), who introduced the semiparametric model with uncertainty zones where is the 1-dimensional friction parameter, observation times are endogenous and observed prices lie on a tick grid. As most likely correlated with the volatility, it is natural to consider as a time-varying parameter. We provide a formal model extension and establish the according limit theory of the LPE of the estimator considered in their work. In addition, our empirical illustration seems to indicate that is indeed time-varying.

In the last example, we consider an application in time series and introduce a time-varying MA(1) model with null mean. The time series is observed in high frequency on and corresponds to the two-dimensional parameter of the MA(1) process. We show that the LPE of the MLE is optimal and document that it outperforms the global MLE and other concurrent approaches in finite sample.

The remaining of this paper is organized as follows. The LPM is introduced in the following section. Conditions for the central limit theory are stated in Section 3. We give the examples in Section 4. We investigate the finite sample performance of the local QMLE of volatility and compares it to the global approach in Section 5. We conclude in Section 6. Consistency in a simple model, proofs, additional numerical simulations on MA(1) model and an empirical illustration on the model with uncertainty zones are gathered in Appendix.

2 The Locally Parametric Model (LPM)

2.1 Data-generating mechanism

We assume that we observe the -dimensional vectors , where can be random, the observation times satisfy . The observations and the observation times are both related to the latent parameter .

As an example, the observations can satisfy , where stands for the efficient price, is a standard Brownian motion, corresponds to the market microstructure noise (which will be restricted to be of order due to the limitation of the technology developed in Section 3), is independent and identically distributed (IID) and independent from , and the latent parameter is equal to the volatility, i.e. .

We assume that the parameter process takes values in , a (not necessarily compact) subset of . We do not assume any independence between and the other quantities driving the observations, such as the Brownian motion of the efficient price process. In particular, there can be leverage effect (see e.g. Wang and Mykland (2014), Aït-Sahalia et al. (2017)). Also, the arrival times and the parameter can be correlated, i.e. there is (some kind of) endogeneity in sampling times.

2.2 Asymptotics

There are commonly two choices of asymptotics in the literature: the high-frequency asymptotics, which makes the number of observations explode on , and the low-frequency asymptotics, which takes to infinity. We choose the former one. Investigating the low-frequency implementation case is beyond the scope of this paper444If we set down the asymptotic theory in the same way as in p.3 of Dahlhaus (1997), we conjecture that the results of this paper would stay true..

2.3 Estimation

The approach taken here is frequent in high-frequency data. We define the block size (i.e. the number of observations in a block) as , and the number of blocks as . For we define the parameter average on the block as

| (2) |

where and its corresponding parametric estimator as . Then, we take the weighted sum of and obtain an estimator of the integrated spot process

| (3) |

where . We call (3) the local parametric estimator (LPE). We assume that

| (4) |

so that when observations are regular the block size vanishes asymptotically. In view of Condition (T) and Remark 4, we have similarly that also goes to 0 when observations are not regular.

3 The central limit theorem

We present in this section the general technology of our paper.555Note that the local approach in this paper is related to the large-T-based-approach and problem of Giraitis et al. (2014). It is mainly based on Theorem 2-2 in Jacod (1997), or similarly Theorem IX.7.3 and Theorem IX.7.28 in Jacod and Shiryaev (2003) or Theorem 2.2.15 in Jacod and Protter (2011), along with regular conditional distribution techniques (see, e.g., Section 4.3 (pp. 77-80) in Breiman (1992)). More specifically, we provide sufficient conditions to the aforementioned theorem in the particular context of this paper. Those conditions are based on the limit theory in the parametric version of the problem, which we assume pre-obtained by the statistician.

The following methods are specified666It is possible to specify the problem with a general rate of convergence, but all the considered examples from this paper are with convergence rate . to the rate of convergence . Formally, we aim to find the limit distribution of

| (5) |

Specifically, we want to show that (5) converges stably777One can look at definitions of stable convergence in Rényi (1963), Aldous and Eagleson (1978), Chapter 3 (p. 56) of Hall and Heyde (1980), Rootzén (1980), Section 2 (pp. 169-170) of Jacod and Protter (1998), Definition VIII.5.28 in Jacod and Shiryaev (2003) or Definition 1 in Podolskij and Vetter (2010). to a limit distribution. We first give the definition of stable convergence.

Definition.

(Stable convergence) A sequence of random variables is said to converge -stably to , which is defined on an extension of , if for any and for any continuous bounded function we have

3.1 Regular observation case

We consider first the simple case when observations are regular, i.e. and . We assume that is a (continuous-time) filtration on such that is adapted to it. In the following of this paper, when using the conditional expectation 888The related assumption is that is a -stopping time., we will refer to the conditional expectation of knowing . We define the discrete-time version of the filtration as . Finally, if we denote the returns of the observations as

| (6) |

we assume that the returns can be expressed as

| (7) |

where is a -dimensional non-random function999We assume that is jointly measurable, and that is taking values on a Borel space. Additionally, we assume that for any , we have , the random innovation are IID (although with distribution which can depend on ) adapted to and independent of the past information , is a (possibly multidimensional) process adapted to which stands for the past that matters in the model. We further assume that is independent from .

The key example stands as follows. We assume that the observations are following the additive model , where is the efficient price and the (shrinking) IID noise independent from , and that the parameter is . In that case , and if . The function101010The advised reader will have noticed that is not a function in the ordinary sense. We still abusively refer to it as a ”function”. takes on the form

| (8) |

Crucial to the expression (8) is that the dependence in the past is only through the past noise , i.e. we do not need to know the whole past of , but rather only the current value. This will be very useful in what follows.

We provide now the outline of the method. Our goal is to investigate the limit distribution of (5) using prior limit result on the parametric version of the problem. A common approach in high frequency statistics proofs consists in decomposing into

| (9) |

where stands for the estimator when we hold the parameter constant on each block. Then, one can usually deal with the first term and the third term (most likely using Burkholder-Davis-Gundy and Markov type of inequalities) and eventually show that they vanish asymptotically. The main work lies in establishing the central limit theory of the second term in (9). A typical proof consists in using locally parametric results along with some Riemann sum argument. But this can be cumbersome as the parameter on each block, although constant, is random. Instead, we propose to look at the further decomposition of into

| (10) | |||

| (11) |

and is a fixed non-random past. In the case of (8), we can choose . From this new decomposition, it is expected as relatively accessible to show that the first term goes to 0, so that the central limit theory will be investigated on the second term of the decomposition. By conditioning by one particular past in (11), we got rid of some randomness, although the parameter is still random. Using conditional regular distribution results in our proofs, we actually show that we can also take the parameter non-random. The price to pay for such method is to show some kind of uniformity in the parameter value when showing the limit results, and that the first term in (10) vanishes asymptotically.

We introduce some definition. For we define the returns on the th block for , and similarly , , and . We assume that

| (12) |

where is a function on . The approximated returns and the approximated estimates are defined as

| (13) | |||||

| (14) |

Basically, those two expressions can be seen as the pendant of respectively (7) and (12) when we hold the parameter constant equal to its block initial value . In the case of the key example (8), we obtain that the approximated returns are of the form

| (15) |

We also introduce the conditional parametric version as

| (16) | |||||

| (17) |

Here, we fix the past equal to in (16), which removes some randomness compared with (13). In the key example, we can (arbitrarily) choose , and this past will only "affect" the first conditional parametric version of the return on the block equal to

| (18) |

whereas for , we have . This key example is an instance where the model is 1-Markovian in the sense that the past only affects the value of the first return on the block. This is quite mild assumption, and we will see that more sophisticated models, such as the model with uncertainty zones, naturally exhibit longer past time-dependence. Moreover, we introduce a parametric version of the returns and the estimators when the parameter is equal to and the past fixed to . Accordingly, the randomness is further reduced in the following expressions. This will be useful in Condition (E).

| (19) | |||||

| (20) |

We provide now the assumptions on . The first assumption considers the continuous Itô-semimartingale case.

Condition (P1).

The parameter is of the form

| (21) |

where is adapted locally bounded (of dimension ) and is a non-negative continuous Itô-process adapted locally bounded (of dimension ), and is a standard -dimensional Brownian motion.

We introduce a norm for as . The following assumption allows for a more general process than semi-martingales. Nonetheless, this assumption is quite restrictive, in particular since does not show up on the right hand-side of (22). In practice this is useful when considering a smooth parameter which cannot be expressed as a "pure drift".

Condition (P2).

satisfies uniformly in that

| (22) |

As the uniformity of limit results on the whole space might be impossible to obtain, we allow to work on the compact subspace , which grows to as increases. Accordingly, we assume that is locally bounded on a compact set in the sense that there exists such that for any , there exists which satisfies for any .

We provide in what follows sufficient conditions to the bias condition (3.10), the increment condition (3.11) and the Lindeberg condition (3.13) in Theorem 3-2 from Jacod (1997). (Almost) equivalently, Theorem IX.7.3 and Theorem IX.7.28 in Jacod and Shiryaev (2003) or Theorem 2.2.15 in Jacod and Protter (2011) could have been used. Those conditions are based on the parametric version of the problem.

Condition (E).

For any (non random) parameter , we assume that there exists a (non random) covariance matrix positive definite such that for any , we have is bounded for any and uniformly in and in we have

| (23) | |||||

| (24) | |||||

| (25) |

We let be the number of blocks before , and the set of all bounded martingales. We now provide the central limit theorem.

Theorem 1.

(Central limit theorem with regular observation times) We assume Condition (E). Moreover, we assume Condition (P1) and that the block size is such that

| (26) |

or Condition (P2). Let be a -dimensional square-integrable continuous martingale. Furthermore, we assume that for all we have

| (27) | |||||

| (28) |

for all , where is the class of all elements of which are orthogonal to (i.e. to all components of ). Finally, we assume that

| (29) |

Then, stably in law as , we have

| (30) |

where , and . In particular, we have

| (31) |

Remark 1.

(Parametric model) Note that in the case where the time-varying parameter model is equal to the parametric model with parameter equal to , the asymptotic variance (AVAR) of is equal to the variance of the parametric model, i.e.

Remark 2.

(Estimating the asymptotic variance) If the statistician does not have a (parametric) variance estimator at hand and that her parametric estimator can be written as in Mykland and Zhang (2017), one can use the techniques of the cited paper to obtain a variance estimate. Investigating if such techniques would work in our setting is beyond the scope of this paper. If she has a variance estimator , then for any she can estimate the th block variance as , and the asymptotic variance as the weighted sum

| (32) |

This estimator will be consistent under mild uniformity assumptions.

3.2 Non regular observation case

We consider now the case when observations can be random (even endogenous). We define the increment of time as and make the first natural assumption.

Condition (T).

The observation times are such that

| (34) | |||||

| (35) |

Remark 4.

(block length) As an obvious consequence of (35), we have that the block length satisfies .

The observation times are related to , as are the returns. We assume that satisfies (7), and that all the definitions (12) - (20) follow. Finally, we define and . We adapt Condition (E) in this case.

Condition (E*).

For any (non random) parameter , we assume that there exists a (non random) covariance matrix such that for any , we have is bounded for any and uniformly in and in we have

| (36) | |||||

| (38) |

where .

We also adapt the central limit theorem.

Theorem 2.

(Central limit theorem with non regular observation times) We assume Condition (T) and Condition (E*). Moreover, we assume Condition (P1) and (26), or Condition (P2). Let be a p-dimensional square-integrable continuous martingale. Furthermore, we assume that for all we have

| (39) | |||||

| (40) |

for all . Finally, we assume that

| (41) | |||||

| (42) |

uniformly in . Then, stably in law as , we have

| (43) |

where , and . In particular, we have

| (44) |

3.3 Bias correction

As the parametric estimator must satisfy the bias condition (36), it is useful to consider in some instances a bias-corrected (BC) version of it which provides the estimate on the ith block . The BC LPE is then constructed as

4 Examples

This section provides some applications of the theory introduced in Section 3. The central limit theorems provided in this section are all new. We choose four examples with regular observations in which it is sufficient to show the conditions of Theorem 1. We further consider the model with uncertainty zones where there is endogeneity in observation times implying that we have to verify the more general conditions of Theorem 2.

4.1 Estimation of volatility with the QMLE

4.1.1 Central limit theorem

We assume that the noise has the form

where , the noise variance is time-varying, and are IID with null-mean and unity variance. In other words we have . The parameter process is defined as the two-dimensional volatility and noise variance process and thus . Correspondingly we work locally with the QMLE considered in Xiu (2010, p. 236) and we introduce the notation for the corresponding LPE .

We also consider the bias-corrected version of the QMLE , where the procedure to construct the unbiased estimator is given in Section 4.1.2. In numerical simulations under a realistic framework, this bias is not observed even with small values of (see Section 6 in Xiu (2010) and Section 5 in Clinet and Potiron (2018b)), and thus it is safe to use in practice.

The assumption of is quite restrictive in view of the related literature on the QMLE. Unfortunately in the case , the techniques of this paper do not apply. Xiu (2010) showed the CLT of the QMLE when is non time-varying and . In the same setting Clinet and Potiron (2018b) showed that the asymptotic variance can be smaller when using the LPE with fixed and documented that in finite sample the LPE was advantageous over the global QMLE. Aït-Sahalia and Xiu (2016) actually establish that the MLE is robust to noise of the form . Da and Xiu (2017) show the central limit theory with rate of convergence ranging from to depending on the magnitude of the noise.

However the techniques allow us to investigate how the LPE behaves in a different asymptotics, i.e. when the noise variance is and tends to . Moreover, we allow for heteroskedasticity in noise variance. Finally, in the case where the noise variance goes to 0 at the same speed as the variance of the returns, i.e. , we can also retrieve the integrated variance noise. In accordance with the setting of this paper, the convergence rate of both the volatility and the noise is .

To verify the conditions for the CLT, we use heavily the asymptotic results of the QMLE (see Theorem 6 in Xiu (2010)) and the MLE in the low-frequency asymptotics (see Proposition 1 on p. 369 in Aït-Sahalia et al. (2005)). The result is formally embedded in the following theorem.

Theorem 3.

(QMLE) We define the filtration generated by .

(i) We assume that . Then, -stably in law as ,

| (46) |

(ii) When , we have -stable convergence in law of to a mixed normal random variable with zero mean and asymptotic variance given by

| (47) |

where .

Remark 6.

(Estimation of high-frequency covariance with the QMLE) To estimate integrated covariance under noisy observations and asynchronous observations, Aït-Sahalia et al. (2010) introduced a QMLE based on a synchronization of observation times. It is clear that their Generalized Synchronization Method can be expressed as a LPM. In view of the close connection between their proposed estimator (2) on p. 1506 and the QMLE studied in Section 4.1, the conditions of our work can be verified and thus Theorem 2 (p. 1506) of the authors can be adapted with the LPE in a framework similar to Section 4.1, i.e. when the noise variance is and time-varying.

4.1.2 Algorithm to construct the unbiased estimator

We describe here the algorithm to obtain . Note that the bias-correction is only required when .

-

1.

We compute the local QMLEs.

-

2.

From Theorem 6 (p. 241) in Xiu (2010), we compute the corresponding and .

-

3.

We change some entries of the matrices to ensure unbiased estimates when using formula (21) and (22) in the aforementioned theorem.

-

4.

We compute the unbiased local QMLE using the formula (21) and (22) with the corrected matrices.

-

5.

The bias-corrected LPE is taken as the mean of local bias-corrected estimates.

4.2 Estimation of powers of volatility

Here the parameter is with not being the identity function. We are concerned with the estimation of powers of volatility under microstructure noise with variance in the same setting as in Section 4.1.

The problem was introduced in Barndorff-Nielsen and Shephard (2002). They showed that the case is related to the asymptotic variance of the realized volatility. One can also consult Barndorff-Nielsen et al. (2006), Mykland and Zhang (2012, Proposition 2.17, p. 138) and Renault et al. (2017) for related developments. All those studies assume no microstructure noise.

When there is microstructure noise, Jacod et al. (2010) use the pre-averaging method. In the special case of quarticity, one can also look at Mancino and Sanfelici (2012) and Andersen et al. (2014). In the case of tricicity, see Altmeyer and Bibinger (2015).

Under no microstructure noise, block estimation (Mykland and Zhang (2009, Section 4.1, p. 1421-1426)) has the ability to make the mentioned estimators approximately or fully efficient. The path followed to do that is to first estimate locally the volatility and then take a Riemann sum of . See also Jacod and Rosenbaum (2013) for an extended version of the method in some ways.

In the same spirit when allowing for microstructure noise, we propose to use locally the estimation , where is the QMLE estimate of the volatility on the th block. As pointed out in Jacod and Rosenbaum (2013), even if we use locally the bias-corrected estimator , we will pay a price for the fact that we use the function in front. In particular, an asymptotic bias quite challenging to correct for will appear in the asymptotic limit theory, as seen in Theorem 3.1 in the cited paper. To get rid of most parts of this bias, we follow the idea at the beginning of Section 3.2 of the cited work and choose such that

| (48) |

Note that this is not incompatible with the other condition (26), i.e. , that will be assumed in what follows. With (48), the part of the bias that doesn’t vanish grows to the extent that it explodes asymptotically. This leads us to consider the following two bias-corrected estimators:

| (49) | |||||

| (50) | |||||

The theorem is given in what follows. The proof uses a local delta method and then follows the proof of Theorem 3.

Theorem 4.

(powers of volatility) Let a nonnegative function such that

| (51) |

for some constants .

(i) We assume that . Then, -stably in law as ,

| (52) |

(ii) When , we have -stably in law that

To reflect on the powerfulness of the local approach, the reader can note that the global QMLE is estimating the wrong quantity when is different from the identity function, except when the volatility is constant. To see why this is the case, we consider the estimation of quarticity (i.e. with ) and we note that a global QMLE would estimate , which is except when volatility is constant different from . The extensive empirical work in Andersen et al. (2014) also indicates that the two quantities are very different in practice.

4.3 Estimation of volatility and higher powers of volatility incorporating trading information

To incorporate all the information available in high frequency data (e.g. in addition to transaction prices, we also observe the trading volume, the type of trade i.e. buyer or seller initiated, more generally bid/ask information from the limit order book), Li et al. (2016) consider the model where the noise is partially observed through a parametric function

where is the vector of information at time and is the noisy part of the original noise . See also the related papers Chaker (2017) and Clinet and Potiron (2017, 2018c, 2018d). Here again the observation times are assumed to be regular, i.e. .

The authors assume that is with mean , finite standard deviation and that , which in turn implies that . To embed this assumption in our LPM framework, there is no harm assuming that

where and are IID with null-mean and unity variance. They estimate and the underlying price as

The authors then estimate the integrated volatility with

where , and show the according central limit theory. Under suitable assumptions, they obtain the optimal convergence rate and the AVAR when :

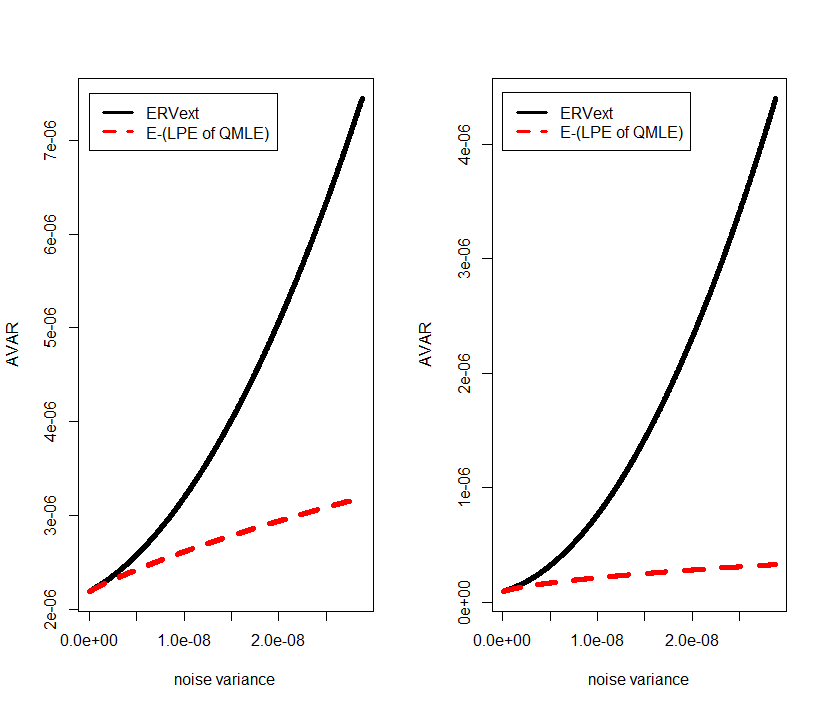

They also consider another estimator (which they call E-QMLE) which consists in using the QMLE from Xiu (2010), which we considered as a local estimator in Example 4.1, on the estimated observations . They indicate that the E-QMLE might yield a smaller AVAR (see their discussion on p. 38), and they report in their numerical study that its finite sample performance is comparable to (see Table 2 in p. 41). They do not investigate the corresponding central limit theory.

With the theory provided in our paper, we cannot investigate the E-QMLE, but rather the E-(LPE of QMLE), i.e. we apply Example 4.1 on . To keep notation of our paper, we denote the E-(LPE of QMLE) estimator of volatility and its bias-corrected version (i.e. E-(BC LPE of QMLE)). The AVARs obtained in Theorem 5 are the same as in Theorem 3. This is due to the fact that the estimation of is very accurate featuring as a rate of convergence and thus the pre-estimation does not impact the AVAR. This was already the case for the (see the proof of Theorem 3 on pp. 46-47 in Li et al. (2016)).

Recalling that the LPE of QMLE is conjectured to be more efficient than the QMLE, in particular this implies that E-(LPE of QMLE) is also conjectured to be more efficient than E-QMLE. In Figure 1, we can see that E-(LPE of QMLE) highly improves the AVAR compared to the . The improvement gets bigger as the noise of increases. When setting the volatility and the noise variance as in the setting of the numerical study in Li et al. (2016), the ratio of AVARS is equal to . When we further assume no jumps in volatility, this ratio goes to . When choosing a bigger noise variance which remains reasonable, this ratio is lower than . The overall picture is clearly in favor of the E-(LPE of QMLE). We provide the theorem of this estimator in what follows.

Theorem 5.

(E-(LPE of QMLE))

Under Assumption A in Li et al. (2016, p. 7):

(i) we assume that . Then, stably in law111111Here and in the following statements, the stable convergence in law is with respect to the filtration considered in Li et al. (2016).as ,

| (53) |

(ii) when , we have stable convergence in law of

We discuss now briefly how to estimate the higher powers of volatility, i.e. when with not being the identity function. We consider the estimators from Example 4.2. The difference with Example 4.2 is that this estimator is used on the estimated price based on the information rather than on the raw price. The related theorem is given in what follows.

Theorem 6.

(powers of volatility)

Under Assumption A in Li et al. (2016, p. 7):

(i) We assume that . Then, stably in law as ,

| (54) |

(ii) When , we have

4.4 Estimation of volatility using the model with uncertainty zones

We introduce a time-varying friction parameter extension to the model with uncertainty zones introduced in Robert and Rosenbaum (2011). To incorporate microstructure noise in the model, we define as the tick size, and the related asymptotics is such that . Correspondingly we assume that the observed price takes values on the tick grid (i.e. modulo of size ).

We discuss first a simple version of the model with uncertainty zones, which features endogeneity in arrival times. In a frictionless market, we can assume that all the returns (which we recall to be defined as ) have a magnitude of exactly one tick, and that the next transaction will occur when the latent price process crosses the mid-tick value in case of the price goes up (or when the price goes down). We extend this toy model in what follows.

The authors introduce the discrete variables that stands for the absolute size, in tick number, of the next return. In other words, the next observed price has the form . They also introduce a continuous (possibly multidimensional) time-varying parameter , and assume that conditional on the past, takes values on with

for some unknown positive differentiable with bounded derivative functions such that .

Also, the frictions induce that the transactions will not occur exactly when the efficient process crosses the mid-tick values. For this purpose, in the notation of Robert and Rosenbaum (2012), let be the parameter that quantifies the aversion to price change. The frictionless scenario corresponds to . Conversely, the agents are very averse to trade when is closer to . If we define as the value of rounded to the nearest multiple of , the sampling times are defined recursively as and for any positive integer as

| (55) | |||

Correspondingly, the observed price is assumed to be equal to the rounded efficient price .

In the extension of (55) when is time-varying, we assume that the sampling times are defined recursively as and for any positive integer as

| (56) |

The idea behind the time-varying friction model with uncertainty zones is that we hold the parameter constant between two observations.

To express the model with uncertainty zones as a LPM, we consider that . Following the definition (p. 11) in Robert and Rosenbaum (2012), we further introduce a Brownian motion independent of all the other quantities, and let denote the cumulative distribution function of a standard Gaussian random variable. We specify the definition of related to as

and . If we set the random innovation as the two-dimensional process , and the past as , we can deduce the form of in the model.121212The advised reader will have noticed that a priori, and are not independent, so that the assumptions of the LPM do not hold entirely. This problem can be circumvented as the former is actually conditionally independent from the latter.

We provide in what follows the definition of the estimators. We are not interested in estimating directly and thus we consider the subparameter to be estimated. For we define

as respectively the number of alternations and continuations of ticks. By alternation (continuation) of ticks, we mean that the return magnitude is of ticks with a direction opposite to (with the same direction as) the previous return. We define the estimator of as131313Actually, the estimator considered here slightly differs from the original definition (p. 8) in Robert and Rosenbaum (2012) as it provides smaller theoretical finite sample bias. Asymptotically, both estimators are equivalent and thus all the theory provided in Robert and Rosenbaum (2012) can be used to prove Theorem 7.

| (57) |

with

where is defined as the integer satisfying , we assume that , and in particular when . The key idea is that are consistent estimators of . Based on the friction parameter estimate, we can construct a consistent latent price estimator as

The estimator of integrated volatility is obtained using the usual realized volatility estimator on the estimated price defined as

The related local estimators are constructed from local versions of .

Theorem 7.

(Time-varying friction parameter model with uncertainty zones) Let be the filtration generated by , and . -stably in law as ,

| (58) |

where can be straightforwardly inferred from the definition of Lemma in p. 26 of Robert and Rosenbaum (2012).

Remark 7.

(convergence rate) Note that, equivalently, the convergence rate in (58) is when corresponds to the expected number of observations. One can consult Remark 4 in Potiron and Mykland (2017) for more details about this.

4.5 Application in time series: the time-varying MA(1)

We first specify the LPM for a general one-dimensional time series. In that case, we assume that the observation times are regular. We further assume that the returns stand for time series observations. Finally, we assume that the time-varying time series can be expressed as the interpolation of via

| (59) |

where is assumed to be independent of all the innovations. When is constant, numerous time series141414We can actually show that any time series in state space form can be expressed with a corresponding function. are of the form (59).

We now discuss the specific MA(1) representation. Several time-varying extensions are possible and we choose to work with the time-varying parameter model

where are standard normally-distributed white noise error terms, and is the time-varying variance. The three-dimensional parameter is defined as . We fix both the innovation and the past equal to the white noise and . We have thus expressed the MA(1) as a LPM.

We discuss how to estimate the parameters in what follows. For simplicity, we assume that . The target quantity is thus equal to . The local estimator is the MLE (see Hamilton (1994), Section 5.4). On each block (of size ), the MLE bias is of order (Tanaka (1984)) and thus the bias condition (23) is not satisfied. Nonetheless, we can correct for the bias up to the order as follows. We define the bias-corrected estimator as

where the bias function can be derived following the techniques in Tanaka (1984). In particular this implies that the bias-corrected estimator satisfies the bias condition if is chosen such that . In practice this bias can be obtained by Monte-Carlo simulations (see our simulation study).

In the parametric case and in a low frequency asymptotics where and observations times are with , known results (see, e.g., the proof of Proposition I in pp. 391-393 (Aït-Sahalia et al. (2005)) show that the asymptotic variance of the MLE is such that

The following theorem provides the time-varying version of the asymptotic theory when T is fixed.

Theorem 8.

(Time-varying MA(1)) Let the filtration generated by . We assume that and Condition (P2). Then, -stably in law as ,

4.6 Further examples

Two further examples include our own recent work. Potiron and Mykland (2017) introduced a bias-corrected Hayashi-Yoshida estimator (Hayashi and Yoshida (2005)) of the high-frequency covariance and showed the corresponding CLT under endogenous and asynchronous observations. To model duration data, Clinet and Potiron (2018a) built a time-varying Hawkes self-exciting process, derived the bias-corrected MLE and showed the CLT of the corresponding LPE.

4.7 Discussion

We provide in what follows a discussion on the efficiency and robustness of the specific examples considered in this section. The subsequent techniques may also be useful to tackle other examples from the literature.

4.7.1 Efficiency

There are many problems where is rate-optimal from Gloter and Jacod (2001), such as all the examples considered in this section. In addition, the local feature of the technology should yield efficiency in case the parametric estimator is efficient itself. This is the case of (47) in Example 4.1, Theorem 4 (ii) in Example 4.2, Theorem 5 (ii) and Theorem 6 (ii) in Example 4.3, Theorem 8 in Example 4.5, where the parametric estimator achieves the Cramér-Rao bound of efficiency locally.

In the case of (46) in Example 4.1, i.e. when estimating volatility assuming that the noise is very small , the asymptotic variance is equal to , whereas the efficient bound is attained by the RV. This increases the variance by a factor of 3, which is also observed on the MLE (when assuming the volatility is constant) when misspecified on a model which does not incorporate microstructure noise (see, e.g., Section 2.4 pp. 1486-1487 in Barndorff-Nielsen et al. (2008)).

4.7.2 Robustness to drift and jumps in the latent price process

We focus on the specific case where the observations are related to a latent continuous-Itô price model , as in Example 4.1-4.4 (Example 4.5 considers a time series without any underlying price process). We discuss how we can add a drift and jumps in in those examples.

We first show how to add a drift component. By Girsanov theorem, in conjunction with local arguments (see, e.g., pp. 158-161 in Mykland and Zhang (2012)), we can weaken the price and volatility local-martingale assumption by allowing them to follow an Itô-process (of dimension 2 in case of volatility or powers of volatility estimation), with a volatility matrix locally bounded and locally bounded away from 0, and drift which is also locally bounded.

It is also easy to see that we can allow for finite activity jumps in . To do that, we assume that is taking values on a compact set151515The MLE is always performed on a compact set, so the assumption is trivially satisfied in that case, which corresponds to Example 4.1-4.3. Moreover, the estimator of in Example 4.4 is bounded by definition, but one would need to bound the volatility estimator to apply the technique.. Consider the set of blocks where there is at least one jump in . As the number of blocks , the cardinality of is at most finite, and thus we have that

It is then immediate to adapt the proof of the CLT. On the other hand, if infinitely many jumps are possible in both the price process and the parameter, the theoretical development is beyond the scope of this paper.

4.7.3 Robustness to jumps in

By a similar reasoning as for when adding jumps in , the techniques of this paper are robust to jumps (of finite activity) in in all our examples.

4.7.4 Non regular observation times

We also assume here that there is a latent price process and reason about the type of observation times which falls into the LPM. We consider first the time deformation of Barndorff-Nielsen et al. (2008, Section 5.3, pp. 1505-1507). To express their setting as a LPM, we assume that the observation times are of the form

| (60) |

where is a stochastic process satisfying , with a strictly positive parameter of the LPM. We can then construct a (change of time) process so that for the observations are regular. In view of Dambis Dubins-Schwarz theorem (see, e.g., Theorem 1.6 on p. 181 in Revuz and Yor (1999)) we have that In addition, it is immediate to see that Condition (T) and (42) hold in that case.

Alternatively one can assume that the quadratic variation of time (see, e.g., Assumption A on p. 1939 in Mykland and Zhang (2006)) exists and that observation times are independent of the price process. Under suitable assumptions, we can also show that Condition (T) and (42) hold.

Our setting can actually allow for (some kind of) endogenous stopping times as in the case of the model with uncertainty zones detailed in Example 4.4. The type of endogeneity is such that there is no asymptotic bias in the related central limit theorem.

Finally, the model allows for endogenous observation times in the general multidimensional HBT model introduced in Potiron and Mykland (2017). In that case, the central limit theorem features an asymptotic bias.161616Details about the model can be found in a previous version of the manuscript circulated under the name ”Estimating the Integrated Parameter of the Locally Parametric Model in High-Frequency Data”.

4.7.5 Estimating time-varying functions of

Another nice corollary about the introduced theory is that we can obtain the central limit theorem of the powers of the integrated parameter for smooth enough when using the local estimates . Essentially, the proof uses on each block a Taylor expansion as in the delta method. We apply the technique on the local QMLE in Example 4.2 and on an adapted estimator from Li et al. (2016) in Example 4.3 to estimate the higher powers of volatility.

5 Numerical study: estimation of volatility with the QMLE

5.1 Goal of the study

To investigate the finite sample performance of the LPE, we consider the local QMLE introduced in Section 4.1. The goal of the study is twofold. First, we want to investigate how the LPE performs compared to the global QMLE. Second, we want to discuss about the choice of the number of blocks in practice. Complementary simulation results can be found in Clinet and Potiron (2018b).

5.2 Model design

We perform Monte-Carlo simulations of M=1,000 days of high-frequency observations where the related horizon time is set to (i.e. annualized). One working day stands for 6.5 hours of trading activity, which can also be expressed as 23,400 seconds. We consider three high-frequency sampling frequency scenarios: every second, every other second, and every three seconds.

We perform local QMLE with number of blocks ranging from (i.e. the global QMLE case) to . The corresponding number of observations per block ranges from to in the case of 1-second sampling frequency, from to if we sample ever other second, and from to when subsampling every three seconds. Note that the minimal number of observations per block remains reasonable in view of the finite sample performance of the global QMLE (see the numerical study in Xiu (2010)).

We bring forward the Heston model with U-shape intraday seasonality component and jumps in volatility as

where

where the parameters are set to , , , , , , the volatility jump size parameter , the volatility jump time follows a uniform distribution on , , , , is a standard Brownian motion such that , , is sampled from a Gamma distribution of parameters , which corresponds to the stationary distribution of the CIR process. For further reference, see Clinet and Potiron (2018b). The model is almost the same as that of Andersen et al. (2012). Finally, the noise is assumed normally distributed with zero-mean and constant variance set so that the noise to signal ratio defined as

| (61) |

is equal to .

5.3 Results

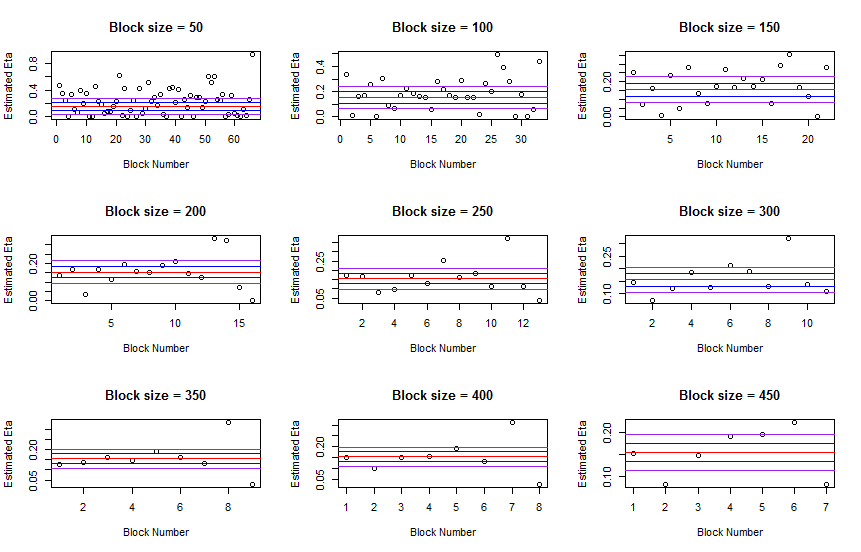

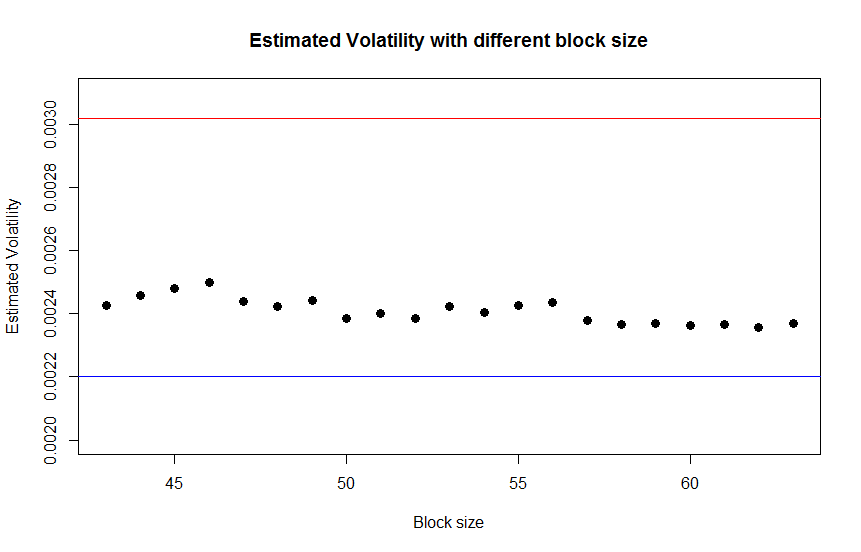

Table 1 reports the sample bias, standard deviation and the RMSE of the local quasi maximum likelihood volatility estimator. The number of blocks ranges from , which corresponds to the global QMLE, to . Regardless of the sampling frequency, the numerical experiment results are quite similar. There is a very small sample bias (the bias to standard deviation ratio magnitude is around ), which increases with the number of blocks while staying very small, all of which hinting that the it is not necessary to use a bias correction of the local QMLE in practice. The standard deviation decreases and then stays (roughly) stable. The picture for the RMSE is the same, all of this very much in line with the fact that almost all the theoretical gain is already obtained in the case of blocks (see Clinet and Potiron (2018b)). Finally, the smallest RMSE is obtained with blocks when sampling at 1-second frequency, in case of 2-second frequency and with 3-second subsampling observations indicating that the finer the sampling frequency the larger the number of blocks should be used. The gains in terms of RMSE goes almost up to when sampling at the finest frequency, whereas less than in the other scenarios.

| Samp.freq. | 1 sec. | 1 sec. | 1 sec. | 2 sec. | 2 sec. | 2 sec. | 3 sec. | 3 sec. | 3 sec. |

|---|---|---|---|---|---|---|---|---|---|

| Nb.blocks | bias | s.d. | RMSE | bias | s.d. | RMSE | bias | s.d. | RMSE |

| 1 | -2.398 | 8.158 | 8.162 | -2.503 | 10.813 | 10.814 | -0.492 | 11.798 | 11.798 |

| 2 | -2.614 | 7.938 | 7.943 | -3.604 | 10.634 | 10.640 | -0.700 | 11.642 | 11.642 |

| 3 | -2.882 | 7.820 | 7.825 | -4.041 | 10.537 | 10.544 | -0.600 | 11.615 | 11.615 |

| 4 | -2.864 | 7.717 | 7.722 | -4.295 | 10.500 | 10.508 | -1.210 | 11.596 | 11.597 |

| 5 | -3.181 | 7.720 | 7.727 | -4.757 | 10.528 | 10.539 | -1.882 | 11.587 | 11.589 |

| 6 | -3.396 | 7.695 | 7.702 | -4.918 | 10.502 | 10.514 | -2.213 | 11.610 | 11.612 |

| 7 | -3.662 | 7.665 | 7.674 | -5.373 | 10.523 | 10.537 | -2.919 | 11.567 | 11.571 |

| 8 | -3.561 | 7.636 | 7.645 | -5.561 | 10.474 | 10.489 | -3.388 | 11.601 | 11.606 |

| 9 | -4.225 | 7.636 | 7.648 | -6.344 | 10.557 | 10.576 | -3.372 | 11.571 | 11.576 |

| 10 | -4.029 | 7.657 | 7.668 | -6.646 | 10.536 | 10.557 | -4.400 | 11.613 | 11.621 |

| 11 | -4.503 | 7.593 | 7.607 | -6.876 | 10.526 | 10.548 | -5.072 | 11.638 | 11.649 |

| 12 | -4.558 | 7.634 | 7.648 | -7.495 | 10.522 | 10.549 | -5.580 | 11.629 | 11.642 |

| 13 | -4.769 | 7.644 | 7.659 | -8.045 | 10.548 | 10.578 | -6.485 | 11.618 | 11.636 |

| 14 | -5.058 | 7.643 | 7.660 | -8.340 | 10.495 | 10.529 | -7.282 | 11.533 | 11.555 |

| 15 | -5.416 | 7.591 | 7.610 | -8.394 | 10.498 | 10.531 | -7.589 | 11.680 | 11.704 |

| 16 | -5.288 | 7.610 | 7.629 | -8.752 | 10.491 | 10.527 | -8.452 | 11.607 | 11.638 |

| 17 | -5.638 | 7.608 | 7.629 | -8.856 | 10.457 | 10.494 | -8.963 | 11.619 | 11.653 |

| 18 | -5.843 | 7.604 | 7.626 | -10.093 | 10.517 | 10.564 | -9.239 | 11.625 | 11.661 |

| 19 | -6.283 | 7.568 | 7.594 | -10.270 | 10.499 | 10.549 | -10.611 | 11.658 | 11.706 |

| 20 | -6.109 | 7.644 | 7.668 | -10.488 | 10.568 | 10.620 | -10.644 | 11.603 | 11.652 |

6 Conclusion

In this paper, we have introduced a general framework to provide theoretical tools to build central limit theorems of convergence rate in a time-varying parameter model. We have applied successfully the method to investigate estimation of volatility (possibly under trading information), higher powers of volatility, the time-varying parameters of the model with uncertainty zones and the MA(1). This allowed us to obtain estimators robust to time-varying quantities, more efficient and/or new estimators of quantities (such as in the case of higher powers of volatility).

Subsequently, we believe that many other examples can be solved using the framework of our paper, which is simple and natural. This was successfully done in our related papers Potiron and Mykland (2017) and Clinet and Potiron (2018a). In those instances, the regular conditional distribution trick significantly simplified the work of the proofs.

References

- [1] Aït-Sahalia, Y., J. Fan, R. Laeven, C.D. Wang and X. Yang (2017). Estimation of the continuous and discontinuous leverage effects. Journal of the American Statistical Association, 1-15

- [2] Aït-Sahalia, Y., J. Fan and D. Xiu (2010). High-frequency covariance estimates with noisy and asynchronous financial data. Journal of the American Statistical Association 105(492), 1504-1517.

- [3] Aït-Sahalia, Y., P.A. Mykland and L. Zhang (2005). How often to sample a continuous-time process in the presence of market microstructure noise. Review of Financial Studies 18, 351-416.

- [4] Aït-Sahalia, Y. and D. Xiu (2016). A Hausman test for the presence of market microstructure noise in high frequency data. To appear in Journal of Econometrics.

- [5] Altmeyer, R. and M. Bibinger (2015). Functional stable limit theorems for quasi-efficient spectral covolatility estimators. Stochastic Processes and their Applications 125(12), 4556-4600.

- [6] Andersen, T. G., D. Dobrev and E. Schaumburg (2012). Jump-robust volatility estimation using nearest neighbor truncation. Journal of Econometrics, 169:75-93.

- [7] Andersen, T.G., D. Dobrislav and E. Schaumburg (2014). A robust neighborhood truncation approach to estimation of integrated quarticity, Econometric Theory 30(1), 3-59.

- [8] Barndorff-Nielsen, O.E. and N. Shephard (2002). Econometric analysis of realized volatility and its use in estimating stochastic volatility models. Journal of the Royal Statistical Society: Series B (Statistical Methodology) 64(2), 253-280.

- [9] Barndorff-Nielsen, O.E., S.E. Graversen, J. Jacod, M. Podolskij and N. Shephard (2006). A central limit theorem for realised power and bipower variations of continuous semimartingales. From stochastic calculus to mathematical finance. Springer Berlin Heidelberg, 33-68.

- [10] Barndorff-Nielsen, O.E., P.R. Hansen, A. Lunde, and N. Shephard (2008). Designing realized kernels to measure the ex post variation of equity prices in the presence of noise. Econometrica 76(6), 1481-1536.

- [11] Breiman, L. (1992) Probability. Classics in Applied Mathematics 7, Society for Industrial and Applied Mathematics (SIAM), Philadelphia, PA.

- [12] Chaker, S. (2017). On high frequency estimation of the frictionless price: The use of observed liquidity variables. Journal of Econometrics 201, 127-143.

- [13] Clinet, S. and Y. Potiron (2017). Estimation for high-frequency data under parametric market microstructure noise. Working paper available at Arxiv 1712.01479.

- [14] Clinet, S. and Y. Potiron (2018a). Statistical Inference for the Doubly Stochastic Self-exciting Process. Bernoulli 24(4B), 3469-3493.

- [15] Clinet, S. and Y. Potiron (2018b). Efficient asymptotic variance reduction when estimating volatility in high frequency data. Journal of Econometrics 206, 103-142.

- [16] Clinet, S. and Y. Potiron (2018c). Testing if the market microstructure noise is fully explained by the informational content of some variables from the limit order book. Working paper available at Arxiv 1709.02502.

- [17] Clinet, S. and Y. Potiron (2018d). A relation between the efficient, transaction and mid prices: Disentangling sources of high frequency market microstructure noise. Working paper available at SSRN 3167014.

- [18] Dahlhaus, R. (1997). Fitting time series models to nonstationary processes, Annals of Statistics 25(1), 1-37.

- [19] Dahlhaus, R. (2000). A likelihood approximation for locally stationary processes, Annals of Statistics 28(6), 1762-1794.

- [20] Dahlhaus, R. and S.S. Rao (2006). Statistical inference for time-varying ARCH processes, Annals of Statistics 34(3), 1075-1114.

- [21] Da, R. and D. Xiu (2017). When Moving-Average Models Meet High-Frequency Data: Uniform Inference on Volatility. Working paper available on Dacheng Xiu’s website.

- [22] Fan, J. and I. Gijbels (1996). Local polynomial modelling and its applications: monographs on statistics and applied probability 66. CRC Press.

- [23] Fan, J. and W. Zhang (1999). Statistical estimation in varying coefficient models. Annals of Statistics, 1491-1518.

- [24] Gloter, A. and J. Jacod (2001). Diffusions with measurement errors. I. Local asymptotic normality. ESAIM: Probability and Statistics 5, 225-242.

- [25] Giraitis, L., G.Kapetanios and T. Yates (2014). Inference on stochastic time-varying coefficient models. Journal of Econometrics 179, 46-65.

- [26] Hall, P. and C.C. Heyde (1980). Martingale Limit Theory and its Application. Academic Press, Boston.

- [27] Hamilton, J.D. (1994). Time series analysis. Vol. 2. Princeton: Princeton university press.

- [28] Hastie T. and R. Tibshirani (1993). Varying-coefficient models. Journal of the Royal Statistical Society: Series B (Statistical Methodology) 757-796.

- [29] Hayashi, T. and N. Yoshida (2005). On covariance estimation of non-synchronously observed diffusion processes. Bernoulli 11, 359-379.

- [30] Jacod, J. (1997). On continuous conditional Gaussian martingales and stable convergence in law. Séminaire de Probabilités XXXI, 232-246.

- [31] Jacod, J., M. Podolskij and M. Vetter (2010). Limit theorems for moving averages of discretized processes plus noise. Annals of Statistics 38(3), 1478-1545.

- [32] Jacod, J. and P. Protter (1998). Asymptotic error distributions for the Euler method for stochastic differential equations. Annals of Probability 26, 267-307.

- [33] Jacod, J. and P. Protter (2011). Discretization of Processes. Springer.

- [34] Jacod, J. and M. Rosenbaum (2013). Quarticity and other functionals of volatility: efficient estimation. Annals of Statistics 41(3), 1462-1484.

- [35] Jacod, J. and A. Shiryaev (2003). Limit Theorems For Stochastic Processes (2nd ed.). Berlin: Springer-Verlag.

- [36] Kim, C. J. and Nelson, C. R. (2006). Estimation of a forward-looking monetary policy rule: A time-varying parameter model using ex post data. Journal of Monetary Economics 53(8), 1949-1966.

- [37] Kristensen, D. (2010). Nonparametric filtering of the realized spot volatility: A kernel-based approach. Econometric Theory 26(01), 60-93.

- [38] Li, Y., S. Xie and X. Zheng (2016). Efficient estimation of integrated volatility incorporating trading information. Journal of Econometrics 195(1), 33-50.

- [39] Mancino, M.E. and S. Sanfelici (2012). Estimation of quarticity with high-frequency data. Quantitative Finance 12(4),607-622.

- [40] Mykland, P.A., and L. Zhang (2006) ANOVA for Diffusions and Itô Processes. Annals of Statistics 34, 1931-1963.

- [41] Mykland, P.A. and L. Zhang (2009). Inference for Continuous Semimartingales Observed at High Frequency. Econometrica 77, 1403-1445.

- [42] Mykland, P.A. and L. Zhang (2011). The Double Gaussian Approximation for High Frequency Data. Scandinavian Journal Statistics 38, 215-236.

- [43] Mykland, P.A. and L. Zhang (2012). The econometrics of High Frequency Data. In M. Kessler, A. Lindner and M. Sørensen (eds.), Statistical Methods for Stochastic Differential Equations, 109-190. Chapman nad Hall/CRC Press.

- [44] Mykland, P.A. and L. Zhang (2017). Assessment of Uncertainty in High Frequency Data: The Observed Asymptotic Variance Econometrica 85(1), 197-231.

- [45] Potiron, Y. and P.A. Mykland (2017). Estimation of integrated quadratic covariation with endogenous sampling times. Journal of Econometrics 197, 20-41.

- [46] Podolskij, M. and M. Vetter (2010). Understanding limit theorems for semimartingales: a short survey. Statistica Neerlandica 64(3), 329-351.

- [47] Reiß, M. (2011). Asymptotic equivalence for inference on the volatility from noisy observations. Annals of Statistics 39(2), 772-802.

- [48] Renault, E., C. Sarisoy and B.J.M. Werker (2017). Efficient estimation of integrated volatility and related processes. Econometric Theory 33(2), 439-478.

- [49] Revuz, D. and M. Yor (1999). Continuous Martingales and Brownian motion. 3rd ed., Germany: Springer.

- [50] Robert, C.Y. and M. Rosenbaum (2011). A new approach for the dynamics of ultra-high-frequency data: the model with uncertainty zones. Journal of Financial Econometrics 9, 344-366.

- [51] Robert, C.Y. and M. Rosenbaum (2012). Volatility and covariation estimation when microstructure noise and trading times are endogenous. Mathematical Finance 22(1), 133-164.

- [52] Stock, J. H. and M. W. Watson (1998). Median unbiased estimation of coefficient variance in a time-varying parameter model. Journal of the American Statistical Association 93(441), 349-358.

- [53] Tanaka K. (1984). An asymptotic expansion associated with the maximum likelihood estimators in ARMA models. Journal of the Royal Statistical Society: Series B (Statistical Methodology) 58-67.

- [54] Wang, C.D. and P.A. Mykland (2014). The Estimation of Leverage Effect with High Frequency Data. Journal of the American Statistical Association 109, 197-215.

- [55] Xiu, D. (2010). Quasi-maximum likelihood estimation of volatility with high frequency data. Journal of Econometrics 159, 235-250.

APPENDIX

7 Consistency in a simple model

The purpose of this section is to provide an outline of the LPM and the conditions of the CLT by investigating the simpler problem of consistency in the case of a simple model. Two toy examples, the estimation of volatility with regular not noisy observations, and the estimation of the rate of a Poisson process, are discussed extensively. Morever, techniques of proofs are also mentioned throughout the section. The obtained conditions are illustrative. Proofs of the conditions along with proofs that conditions hold in the two toy examples can be found in Section 8. Finally, some detailed mathematical definitions can be found in what follows too.

The simple model

We focus on a simple setting in this section. First, we work with one dimensional returns, i.e. . Also, we assume that the observations are regular, so that . The parametric model is assumed to be very simple, in particular there is no past dependence in the returns. It assumes that there exists a parameter such that are independent and identically distributed (IID) random functions of . If we introduce an adequate IID sequence of random variables with distribution which can depend on , we can express the returns as

| (62) |

where is a non-random function. In (62), can be seen as the random innovation.

Since can in fact be time-varying, do not necessarily follow (62) in the time-varying parameter model. A formal time-varying generalization of (62) will be given in (65). In general, are neither identically distributed nor independent. are not even necessarily conditionally independent given the true parameter process , as we can see in the following two toy examples.

Example 1.

(estimating volatility) Consider when (the volatility is thus assumed to follow (21)), and , where is a standard -dimensional Brownian motion. In this case, the parameter space is . The parametric model assumes and that the distribution of the returns is , where is the increment of the Brownian motion between the th observation time and the th observation time and is the fixed volatility. Under that assumption, the returns are IID. Under the time-varying parameter model, are clearly not necessarily IID, and they are also not necessarily conditionally independent given the whole volatility process if there is a leverage effect.

Example 2.

(estimating the rate of a Poisson process) Suppose the statistician observes data on the number of events (such as trades) in an arbitrary asset, and thinks the number of events happening between and , , follows a homogeneous Poisson process with rate . The parameter rate will be assumed to follow (21), with possibly a null-volatility if the homogeneity assumption turns out to be true. Because the econometrician does not have access to the raw data, she can’t observe directly the exact time of each event. Instead, she only observes the number of events happening on a period (for instance a ten-minute block) , that is . If the statistician’s assumption of homogeneity is true, the returns are IID. In case of heterogeneity, will be a inhomogeneous Poisson process, and the returns will most likely be neither identically distributed nor independent.

We need to introduce some notation and definitions. On a given block the observed returns will be called . Formally, it means that for any . In analogy with , we introduce the approximated returns on the th block. We also introduce the corresponding observation times for . Note that . Finally, for we define the time increment between the th return and the th return of the th block as .

We provide a time-varying generalization of the parametric model (62) as well as a formal expression for the approximated returns. To deal with the former, we assume that in general

| (63) |

The time-varying parameter model in (63) is a natural extension of the parametric model (62) because the returns can depend on the parameter process path from the previous sampling time to the current sampling time . As depend on the parameter path, it seems natural to allow to be themselves process paths. For example, when the parameter is equal to the volatility process , we will assume that are equal to the underlying Brownian motion path (see Example 3 for more details). Also, as are random innovation, they should be independent of the parameter process path past, but not on the current parameter path. In the case of volatility, it means that we allow for the leverage effect. A simple particular case of (63) is given by

| (64) |

i.e. the returns depend on the parameter path only through its initial value. Finally, the approximated returns follow a mixture of the parametric model (62) with initial block parameter value. We are now providing a formal definition of our intuition. We assume that

| (65) | |||||

| (66) |

where the random innovation take values on a space that can be functional171717 is a Borel space, for example the space of -dimensional continuous paths parametrized by time . and that can depend on , are IID for a fixed but the distribution can depend on , and is a non-random function181818Let be the space of -dimensional continuous paths parametrized by time , which is a Borel space. Consequently, is also a Borel space. We assume that is a jointly measurable real-valued function on . Note that the advised reader will have seen that a priori is defined on (after translation of the domain by ) in (65) and is a vector in (66), whereas both should be defined on the space according to the definition. We match the definitions by extending them as continuous paths on . Formally, if , we extend it as for all . Similarly, if , we extend it as for all .. Note that (65) is a mere re-expression of (63) using a different notation. For any block and for any observation time of the block, we define 191919Let be a probability space. Define the sorted filtration such that for any non-negative integer that we can decompose as where and , . We assume that is a (discrete-time) filtration on . In addition, we assume that and are -measurable. the filtration up to time . The crucial assumption is that has to be independent of the past filtration202020past filtration means up to time (and in particular of ). Note that we do not assume any independence between the random innovation and the parameter process . We provide directly the definitions of and in the two toy examples.

Example 3.

(estimating volatility) In this case, is defined as the space of continuous paths parametrized by time , are the Brownian motion increment path processes between two consecutive observation times. We assume that is jointly a (possibly non-standard) -dimensional Brownian motion. Thus, the random innovation are indeed independent of the past in view of the Markov property of Brownian motions. We also define . We thus obtain that the returns are defined as and that the approximated returns are the same quantity when holding the volatility constant on the block.

Example 4.

(estimating the rate of a Poisson process) We assume that the rate of the (possibly inhomogeneous) Poisson process is , where is a non time-varying and non-random quantity such that . In this case, we assume that is the space of increasing paths on starting from which takes values in and whose jumps are equal to 1. We also assume that for any path in , the number of jumps is finite on any compact of . can be defined as standard Poisson processes , independent of each other. We also have . Thus, if we let , the returns are the time-changed Poisson processes

| (67) | |||||

| (68) |

Consistency

In the following of this section, we will make the block size go to infinity

| (69) |

Furthermore, we will make the block length vanish asymptotically. Because we assume observations are regular in this section, this can be expressed as

| (70) |

We can rewrite the consistency of as

| (71) |

where the formal definition of can be found in (75). In order to show (71), we can decompose the increments into the part related to misspecified distribution error, the part on estimation of approximated returns error and the evolution in the spot parameter error

where , which is defined formally in (76), is the parametric estimator used on the underlying non-observed approximated returns. It is not a feasible estimator and appears in (7) only to shed light on the way we can obtain the consistency of the estimator in the proofs. We first deal with the last error term in (7), which is due to the non-constancy of the spot parameter . Note that

| (73) |

and thus we deduce from Riemann-approximation212121see i.e. Proposition 4.44 in p.51 of Jacod and Shiryaev (2003) that

| (74) |

To deal with the other terms in (7), we assume that for any positive integer , the practitioner has at hand an estimator , which depends on the input of returns . On each block we estimate the local parameter as

| (75) |

The non-feasible estimator is defined as the same parametric estimator with approximated returns as input instead of observed returns

| (76) |

Note that (76) is infeasible because the approximated returns are non-observable quantities.

Example 5.

(estimating volatility) The estimator is the scaled usual RV, i.e. . Note that can also be seen as the MLE (see the discussion pp. 112-115 in Mykland and Zhang (2012)).

Example 6.

(estimating the rate of a Poisson process) The estimator to be used is the return mean .

In order to tackle the second term in (7), we make the assumption that the parametric estimator is -convergent, locally uniformly in the model parameter if we actually observe returns coming from the parametric model. This can be expressed in the following condition.

Condition (C).

Let the innovation of a block be IID with distribution . For any ,

Remark 8.

(practicability) Under Condition (C), results on regular conditional distributions222222see for instance Leo Breiman (1992), see Section 8 for more details. give us that the error made on the estimation of the underlying non-observed returns tends to 0, i.e.

| (77) |

This proof technique is the main idea of the paper. Regular conditional distributions are used to deduce results on the time-varying parameter model using uniform results in the parametric model.

Remark 9.

(consistency) Note that -convergence is slightly stronger than the simple consistency of the parametric estimator. Nonetheless, in most applications, we will have both.

We can now summarize the consistency result in this very simple case where observations occur at equidistant time intervals and returns are IID under the parametric model. Under Condition (C) and assuming that

| (78) |

we have the consistency of (3), i.e.

| (79) |

We obtain the consistency in the couple of toy examples232323see Section 8 for proofs.

Remark 10.

(LPE equal to the parametric estimator) The reader will have noticed that in the couple of examples, the LPE is equal to the parametric estimator. This is because in those very basic examples, the parametric estimator is linear, i.e. for any positive integer and

In more general examples, this equation will break, and we will obtain two distinct estimators.

8 Proofs

8.1 Preliminaries

In view of our assumptions on , we can follow standard localisation arguments (see, e.g., pp. of Mykland and Zhang (2012)) and assume without loss of generality that is a compact space. In case is an Itô semimartingale satisfying Condition (P1), we can also assume without loss of generality that there exists such that for any eigen value of , we have and that there exists such that .

Finally, we fix some notation. In the following of this paper, we will be using for any constant , where the value can change from one line to the next.

8.2 Proof of Condition (C) (77)

It is sufficient to show that Condition (C) implies that

| (80) |

By (66) and (76), we can build such that we can write

where is a jointly measurable real-valued function such that

We have that

where is a regular conditional distribution for given (see, e.g., Breiman (1992)). From Condition (C), we obtain (80).

8.3 Proof of the consistency in Example 1

Let’s show Condition (C) first. For any , the quantity

can be shown to go to 0 in probability as a straightforward consequence of Theorem of p.52 in Jacod and Shiryaev (2003).

To show the condition (78), it is sufficient to show that the following quantity

| (81) |

goes to uniformly in i. To prove this, we can use the formula , together with conditional Burkholder-Davis-Gundy inequality (BDG, see inequality (2.1.32) of p. 39 in Jacod and Protter (2011)).

8.4 Proof of Consistency in Example 2

8.5 Proof of Theorem 2 (Central limit theorem with non regular observation times)

We prove directly the central limit theorem in this general case. As a by-product, this implies the case with regular observations, i.e. Theorem 1. We can decompose as

| (82) |

with

It is clear that by (41) and by (42) along with Lemma 2.2.10 (p. 55) in Jacod and Protter (2011) and the fact that takes values in a compact set. We prove in what follows that and that , where follows the definition of Theorem 2.

We show

We consider first the case where satisfies Condition (P2). We introduce

| (83) |

It is sufficient to show that , and by virtue of Lemma 2.2.10 (p. 55) in Jacod and Protter (2011) that . We compute

where we used onditional Cauchy-Schwarz to obtain the inequality, Condition (T) along with Condition (P2) to obtain the last equality. We deduce that in this case too.

We now consider the case where satisfies Condition (P1) and (26) holds. We start by decomposing into its bias and its martingale part. We have

We will show in what follows that and . We start with the first assertion. As for the previous case, it is sufficient to show that . As is bounded, we can bound the expression via

Then, using Condition (T) along with (26), we conclude that this is .

We show now that . As it is a martingale, it is sufficient to show that . We compute

where we used conditional Hölder’s inequality with and in the first inequality, BDG with in the second inequality, Condition (T) along with (26) in the last equality.

We show

We aim to use Theorem 2-2 (p. 242) in Jacod (1997). Conditions are further specified in Theorem 3-2 (p. 244) in the case when observations are regular. Following the proof of Theorem 3-2, we can actually show that such conditions hold in the more general case when observations are not regular, choosing the filtration . It is crucial to note that we are not working with the filtration .

Consequently, our goal is to show the conditions (3.10)-(3.14) from Theorem 3-2 (p. 244) in Jacod (1997). Note that (3.12) and (3.14) are respectively implied by (39) and (40). The bias condition (3.10) is satisfied as an application of (36) along with regular conditional distribution.

In this step, we prove that (3.11) is satisfied. We introduce and

The condition (3.11) can be expressed as

| (84) |

By regular conditional distribution, (36) and (Condition (E*)), we have that

In view of (42), the conditional Cauchy-Schwarz inequality and the boundedness of , we get

Using Lemma 2.2.11 of Jacod and Protter (2011) together with conditional Cauchy-Schwarz inequality, (35) and the boundedness of , we obtain

We can apply now Proposition I.4.44 (p. 51) in Jacod and Shiryaev (2003) and we get

8.6 Proof of Theorem 3 (QMLE)

We want to show that the conditions of Theorem 1 are satisfied. We start with the case . The key result is Theorem 6 in Xiu (2010, p. 241). We choose .

We show first Condition (E). We can see easily from the key result that if we choose , then (Condition (E*)) is satisfied.

We can verify the Lindeberg condition (38) using conditional Cauchy-Schwarz inequality and the fact that the fourth moment of

is bounded.

As for the bias condition (36), we can see that as the noise shrinks faster than the order of the returns to , then the bias tends to the sum of the diagonal elements of defined in (23) in Xiu (2010, p. 241) minus unity. This equals and thus (36) is satisfied.

The condition (29) is satisfied combining the fact that the noise is independent from , the aforementioned theorem with the rationale in Section 8.3.

We now show that (27) and (28) are satisfied. Actually, we can show trivially that (27) holds for the reference continuous martingale . We recall that we are "only" showing stable convergence with respect to , and we show now the condition related to stable convergence (28). Actually, we can assume that , this will imply that the result holds for any . From Theorem 6 in Xiu (2010), we have that

We can develop , where , , and . Because the noise is independent from , it is clear that , and . As for , we can express

and from this expression straightforward computation leads to

We consider now the case , i.e. when both the noise variance and the returns are of the same rate. In that case, we need to use the bias-corrected estimator so that we can verify the conditions of Theorem 1. The key result here is Proposition 1 (p. 369) along with its proof (p. 391-393) in Aït-Sahalia et al. (2005).