Weighted mining of massive collections of -values by convex optimization

Abstract

Researchers in data-rich disciplines—think of computational genomics and observational cosmology—often wish to mine large bodies of -values looking for significant effects, while controlling the false discovery rate or family-wise error rate. Increasingly, researchers also wish to prioritize certain hypotheses, for example those thought to have larger effect sizes, by upweighting, and to impose constraints on the underlying mining, such as monotonicity along a certain sequence.

We introduce Princessp, a principled method for performing weighted multiple testing by constrained convex optimization. Our method elegantly allows one to prioritize certain hypotheses through upweighting and to discount others through downweighting, while constraining the underlying weights involved in the mining process. When the -values derive from monotone likelihood ratio families like the Gaussian means model, the new method allows exact solution of an important optimal weighting problem previously thought to be nonconvex and computationally infeasible. Our method scales to massive dataset sizes.

We illustrate the applications of Princessp on a series of standard genomics datasets and offer comparisons with several previous ‘standard’ methods. Princessp offers both ease of operation and the ability to scale to extremely large problem sizes. The method is available as open-source software from github.com/dobriban/pvalue_weighting_matlab.

1 Introduction

1.1 Large-scale inference

Large-scale inference (Efron, 2012) is the new term of art for an emerging set of activities that crosscut all of scientific data analysis. Owing to new data collection and computing technology, massive inference problems are appearing that challenge traditional statistical approaches.

An emblem of the new era is the compilation of vast collections of -values to be mined and analyzed.

-

•

Workers in computational biology, working with different forms of genome-derived data—gene expression, Single Nucleotide Polymorphism (SNP), Copy Number Variation (CNV), etc.—routinely compute a -value for each relevant genomic locus, providing statistical evidence that the locus is associated with some outcome. When done for hundreds of thousands or even millions of such sites, massive collections of -values emerge (see e.g., Tusher et al., 2001; Burton et al., 2007, for representative examples).

-

•

Workers in extragalactic astronomy look for evidence of non-Gaussianity in the cosmic microwave background (CMB), by compiling -values for tests of non-Gaussianity associated with different regions, orientations and scales of the CMB data.

The emergence of large collections of -values is happening in field after field. In fact scientific publication itself can now be viewed as a collection of numerical -values:

- •

This emergence creates an urgent demand for tools that can conveniently and reliably facilitate the main tasks of large-scale inference.

1.2 Weighted testing of individual hypotheses

A primary task in large-scale inference (LSI) is simultaneous testing of individual null hypotheses—the focus of this paper. Intuitively, this task allows one to discover the ‘signals’ amid a sea of ‘noise’ -values, while providing some form of rigorous error control.

Many popular simultaneous significance tests are available, such as the Bonferoni method, Holm’s method (Holm, 1979), or the Benjamini-Hochberg method (Benjamini and Hochberg, 1995), but all suffer from a fundamental limitation: they treat the hypotheses as equal, and thus are unable to exploit important prior information about the likely significance of some hypotheses. Incorporating prior knowledge into the multiple testing problem holds the promise of achieving higher power.

Weighted Bonferroni testing of -values is an increasingly popular method to prioritize certain effects over others. We assign a weight to the -th -value, and reject the -th null hypothesis if . The larger the weight, the less stringent the rejection threshold, and the easier it is to reject a null. See the review articles of Roeder and Wasserman (2009) and Gui et al. (2012).

There is a growing trend to use weighted testing of -values, especially in the biomedical literature, where a number of successful applications to genome-wide association studies (GWAS) are listed in Table 1.

| Source | Current GWAS | Prior |

|---|---|---|

| Saccone et al. (2007) | nicotine dependence | nicotine receptor status |

| Andreassen et al. (2013) | schizophrenia | cardiovascular disease GWAS |

| Li et al. (2013) | childhood asthma | eQTL |

| Rietveld et al. (2014) | cognitive performance | educational attainment GWAS |

| Fortney et al. (2015) | extreme longevity | age-related traits |

| Sveinbjornsson et al. (2016) | aggregate over broad set | annotation in established hits |

Unfortunately, the existing -value weighting procedures have limited ability to cope with important practical requirements.

1.3 Optimal weighting and obstacles to practitioner acceptance

A motivational example arises when we can assign—say, based on earlier experimental measurements— prior effect sizes to the different hypotheses. For instance, in biomedical research we may have access to data from related studies on the same trait. Our goal is to perform weighted testing in a fashion that rigorously controls the type I error, but offers optimal detection power, under the alternative hypothesis that the specified effect sizes are true. Equivalently, we want to apply weighted multiple testing of -values with the so-called Spjøtvoll weights. See Spjøtvoll (1972), Westfall et al. (1998), Genovese et al. (2006), Rubin et al. (2006), etc.

The Spjøtvoll weights can have certain unusual properties which render them unacceptable to practitioners. Among these are the fact that the weights themselves need not be monotone in the effect sizes ; and the fact that some of the formally optimal weights can be very close to zero, causing the weighted -value statistic to behave in an unstable fashion. Practitioners simply don’t consider it safe and effective to rely on weights with such properties. Existing approaches developed to cope with these unfortunate aspects of the optimal weights involve nonconvex optimization (Westfall et al., 1998; Westfall and Krishen, 2001), and so don’t scale well to large problem sizes. So at the moment, there is no computationally effective way to impose ‘practitioner’ constraints such as monotonicity and strict positivity; in the era of practical large scale of inference we cannot yet apply optimal weighting to massive collections of -values.

1.4 Princessp: New approach based on convex optimization

This paper develops Princessp, a new approach to weighted Bonferroni multiple testing of -values which resolves the practitioner obstacles just mentioned. Princessp employs convex optimization and so can scale to very large problem sizes. It allows linear inequality constraints to be imposed, constraints which can include monotonicity of weights in the effect size and also lower bounds keeping all weights at a definite distance from zero. Hence the key priorities of practitioners—scale, monotonicity and definite positiveness of the weights—are all handled by our new Princessp method.

In more detail, we now enumerate our main contributions:

-

1.

We formulate Princessp as the constrained convex optimization problem of computing -value weights maximizing average power of the weighted Bonferroni method (Sec. 2). The concavity of the receiver-operating characteristic (ROC) is the key property enabling this approach. We establish concavity in the important setting of of two-sided tests in exponential families.

-

2.

We give several examples of practical convex constraints to be used with Princessp (Sec. 2.3). Our framework allows us to consider in a unified way several types of weights (such as stratified or smooth weights) that have been considered in previous work, and also leads to new methods (such as bounded and monotone weights, Sec. 3).

-

3.

We develop an efficient interior-point method for monotone bounded weights under normal observations (Sec. 4). The direct use of interior-point methods leads to a severely ill-conditioned KKT system, and is inapplicable to large-scale problems. Therefore, we develop a new subsampling algorithm to avoid the ill-conditioning (Sec. 4.2.2). We establish that subsampling is fast and accurate.

This allows us to efficiently solve large-scale problems with potentially tens of millions of hypotheses, such as those common in genomics. A MATLAB implementation of this method, as well as the code to reproduce our computational results is available at github.com/dobriban/pvalue_weighting_matlab, and will be provided in the software supplement.

-

4.

We illustrate Princessp on a series of standard genome-wide association study (GWAS) datasets (Sec. 3.2). The boundedness of the weights seems to be important here, and leads to a good empirical performance compared to the state of the art weighted Bonferroni methods.

We start in Sec. 2 by explaining Princessp first in the Gaussian case, then more generally for monotone likelihood ratio families and two-sided tests. We give several concrete examples of convex constraints (Sec. 2.3). We study the important special case of monotone -value weights (Sec. 3), illustrating their empirical performance on standard GWAS datasets and simulated data (Sec. 3.2). Finally, we develop numerical methods to compute them (Sec. 4.2).

2 Princessp: Convex -value weights

To explain our framework, we start with the normal means model. Suppose we observe test statistics , and want to test the individual hypotheses against simultaneously. Here are the standardized effect sizes, which are arbitrary fixed parameters.

We construct -values , and reject the -th null if , with and . This is the weighted Bonferroni procedure, which controls the family-wise error rate—the probability of making any false rejections—at level . The weights are based on independent prior data. Without loss of generality we assume .

To optimize the choice of weights, it is customary to proceed in two stages. First we assume that we know , and derive formally optimal “oracle” weights depending on the unknown parameters. Second, when are unknown but we can construct estimators based on some empirical data, we use the weights . In this paper, we will focus on the first stage. In practice this corresponds to oracle weighting conditioning on . Thus we do weighting as if the true parameters were , but we do not use those estimates for other statistical inference tasks. We return to this issue at the end of the section.

If are known, we can assign zero weight to any non-negative ; so in the remainder we will assume that all . We can choose the remaining weights to maximize the expected number of discoveries. The statistical power to reject when the true parameter is equals , leading to the optimization problem

| (1) |

This class of weighted multiple testing problems was studied first by Spjøtvoll (1972), thus we call this the Gaussian Spøtvoll weights problem. Rubin et al. (2006) and Roeder and Wasserman (2009) showed that the weights are , for the unique such that the weights sum to . They studied the problem parametrized by the critical value instead of the weight . In that parametrization, the objective is not concave, and therefore it is unclear how to efficiently incorporate additional constraints. As a key observation for this paper, in the weight parametrization, the function is the ROC curve of the Gaussian test, and is strictly concave if (e.g., Lehmann and Romano, 2005, p. 101).

Our Princessp method takes this observation to its natural conclusion, allowing arbitrary convex constraints for the weights. Specifically, let , be convex and twice continuously differentiable functions, encoding convex inequality constraints . Let be an matrix encoding equality constraints . We let the vector be the first row of , and be the first entry of . We assume . In the following examples, one can easily check these conditions.

The Princessp problem of computing constrained optimal weights for Bonferroni multiple testing is thus, in the Gaussian case:

| s.t. | |||

More generally, beyond one-sided Gaussian tests, we replace with the appropriate ROC curves. For instance, if we want to perform two-sided tests of a null hypothesis against , then the analogous objective function is

We will show in Proposition 2.2 that the objective is concave, despite only one term in each pair being concave in . That result applies more generally to continuous exponential families. For one-sided tests, we can handle even more general observations, arising from monotone likelihood ratio families (Sec. 2.1).

One of the most important convex constraints is monotonicity. For Gaussian data, suppose that our guesses for the means are sorted such that . Monotonicity requires that larger absolute effects have a larger weight, so that . Unconstrained Spjøtvoll weights are not monotone in general. However, monotonicity is clearly desirable in practice. We discuss monotone weights in Sec. 3.

In Sec. 4, we will also explain how to solve the Gaussian problem numerically. Despite its simplicity, the problem has interesting numerical aspects. We show that the log-barrier interior point method converges in theory, but it has serious numerical difficulties; namely, a severely ill-conditioned KKT system. For monotone weights, we show how to avoid ill-conditioning using a subsampling approach.

Returning to the issue mentioned above, in practice we will have some empirical estimates of the effect sizes, and solve the Princessp problem with those values substituted for , effectively conditioning on . Thus, in practice we will use the optimization formulation merely as a means to efficiently specify an algorithm for use on real data. The formal optimality properties of those plug-in weights are beyond our present scope.

2.1 Monotone likelihood ratio

For one-sided tests we have convex problems very generally in monotone likelihood ratio (MLR) families. Suppose is a real-parameter family of densities with respect to Lebesgue measure, supported on a common open interval , where the endpoints can be infinite. We assume that for all , so that the distribution functions are differentiable and strictly increasing on . Then the inverse functions are well-defined for . Our key assumption is that has a monotone increasing likelihood ratio in , for .

Define the ROC curve . This gives the power at of a one-sided test with rejection region , as a function of the level under .

Proposition 2.1 (MLR and concavity, e.g., Lehmann and Romano (2005) p. 101).

Suppose is a family of densities with monotone increasing likelihood ratio in , and satisfies the assumptions above. Then the ROC curve is strictly convex in for , and strictly concave for .

Proof.

Part of this result is stated, but not proved, on p. 101 of Lehmann and Romano (2005); therefore we provide a proof. We have . Hence, is strictly increasing for , and strictly decreasing if . Therefore, is strictly convex for , and strictly concave for . ∎

Suppose now that we have test statistics and we are testing against simultaneously. As is well known, the uniformly most powerful individual test rejects for . With the -values , the weighted Bonferroni test rejects the -th null if .

As before, suppose we have prior guesses for the parameters. The power of the -th test at is . To optimize the average power of the weighted Bonferroni method for this set of alternatives, we must solve

| (2) |

By Proposition 2.1, this objective is concave, and can be solved efficiently. In this setup, the Princessp problem adds general convex problem. This extension of Princessp to MLR allows us to handle one-sided tests in the following well-known statistical models:

-

•

One-dimensional exponential families with continuous support: Clearly, exponential families have monotone likelihood ratio in . Our framework includes one-sided tests on the natural parameter, such as the mean of a normal family ( fixed), the variance in a normal family ( fixed), beta distributions (with one shape parameter fixed), or gamma distributions (with either the shape or the rate parameter fixed).

-

•

Non-central distributions: The distribution of the -statistic with fixed degrees of freedom and non-centrality parameter has MLR in (e.g., Lehmann and Romano (2005), p. 224). Similarly, the distribution of the non-central and -statistics with fixed degrees of freedom have MLR (e.g., Lehmann and Romano (2005), p. 307).

-

•

Location families: Location families with strictly positive and almost surely smooth log-concave density have monotone likelihood ratio. Examples include double-exponential (Laplace) distributions with and logistic distributions .

We emphasize that the assumptions on the family of densities made in this section are essential, and not merely technical. Indeed, if the distributions do not have a density, then the ROC curve may be discontinuous, rendering the optimization problem discontinuous, and definitely nonconvex. For instance, if denotes the distribution function of a Bernoulli variable with success probability , then the ROC is the step function

Similar problems occur when the densities can be zero, or when the supports are non-overlapping.

An even more general convexity property holds for likelihood-ratio tests. As is well known in statistical folklore, and formalized for instance in Proposition 3.1 of Peña et al. (2011), the ROC curve of LR tests is often automatically concave. However, in our applications, the alternative is usually composite, parametrized by a scalar , not just a simple alternative. There is often some uncertainty in specifying from prior data. For this reason it is important to have good uniform optimality properties against composite alternatives. For this one essentially needs the MLR, which is why we chose that setting here.

2.2 Two-sided tests in exponential families

For two-sided tests, we can guarantee that Princessp works in exponential families, a setting more restricted than MLR, but more general than Gaussian. Suppose that we have observations with density with respect to some dominating measure. We want to test against . Suppose we reject the -th null if for critical values such that the test has level . Let be the power of this test at an alternative hypothesis . We analyze the convexity of the ROC curve in this setting. We are also interested in strong convexity, because it is needed for the convergence of the log-barrier method.

Proposition 2.2 (Concavity for two-sided tests in exponential families).

Consider two-sided tests against for observations following the exponential family .

-

1.

If , the ROC curve at is a concave function of the level . If , is convex.

-

2.

Moreover, if , then is strongly concave on any interval , . Similarly, if , is strongly convex on any interval , .

Proof.

Let be the cumulative distribution function of the observations under parameter . The critical value for the test is determined by the equation . Our assumptions guarantee that is well-defined. Indeed, takes value , is differentiable with non-negative derivative , and moreover, has limit as . In addition, for all such that either or belong to the support of . Therefore, if , then precisely on an interval for some . This implies that for any , the equation has a unique solution on , showing that is well-defined.

Moreover, for . In addition, the power of the test equals , therefore . We will only consider , the other case is analogous.

-

1.

To show is concave for , we must prove that is decreasing in . Since can be viewed as a decreasing function of , it is enough to show that is increasing in , where

Since we are in an exponential family, we see

It is a simple calculus exercise to show that this function is increasing in — and in fact on —if .

-

2.

To show strong concavity, we must check in addition that for a constant . Note that . Denoting by constants that do not depend on (or ) and whose meaning may change from line to line, we get

Without loss of generality we may assume that . Then the numerator equals . Hence,

Since , we have . Clearly, for small , are bounded away from and , so that there. For large , . Therefore, . So, if , then for all , showing that the power function is strongly concave.

∎

An example of special interest is testing normal observations for against . Then the two-sided analogue of Spjøtvoll weights amounts to the optimization problem

| (3) |

Note that the first term is concave in , but the second term is not. However, their sum is concave by Proposition 2.2. This reinforces that the results in this section go beyond those from the previous section.

We can also find a nearly explicit form for the two-sided optimal Gaussian weights. This leads to a fast algorithm for computing them, as well as insights about their behavior (see Sec. 3).

Proposition 2.3 (Explicit optimal weights for two-sided Gaussian tests).

Define the function and the constant . Define also the function . If all , and if , then the optimal weights for the two-sided normal problem are , where is the unique constant such that .

Proof.

Define . The Lagrangian for the two-sided normal problem is

Now, , where . Therefore, we have for all iff, denoting

or equivalently . This is equivalent to . Since , from this we obtain that the optimal maximizing the Lagrangian have the desired form for fixed , if . If we can show that there exists a such that the constraint holds, then it will follow that those weights also solve the original constrained problem.

For this, note that the function is continuous and strictly increasing on , going from to . Therefore, the weight is a strictly decreasing function of on , going from to . Hence is strictly decreasing on , with limit 0 at . By the assumption , it follows that there is a unique such that the constraint holds. This finishes the proof. ∎

2.3 Examples of convex constraints

The key flexibility of Princessp lies in the wide variety of user-specified convex constraints that it can be used with. To help potential users see how this is relevant in a variety of contexts, we now give several examples of such constraints.

-

1.

Monotone weights. Suppose in the Gaussian case that the means are sorted such that . Monotone weights require that larger absolute effects have a larger weight, so that .

Unconstrained Spjøtvoll weights are not monotone in general. However, monotonicity is intuitively desirable, as larger effects are worth more. Many popular weighting schemes are monotone, including exponential weights and cumulative weights , for , both proposed in Roeder et al. (2006). The weights of Li et al. (2013) based on normalized versions of , where are -values from independent expression Quantitative Trait Locus (eQTL) studies, are also monotone in the strength of the prior information. Princessp offers a principled way to incorporate monotonicity as a constraint in any weighting scheme.

-

2.

Bounded weights. Boundedness requires that for two constants . This ensures that the current -values get multiplied by at most . Hence, if and the original -value cutoff is—say—the conventional threshold for genome-wide significance, then each hypothesis with -value is significant, regardless of the strength of prior information. This is desirable as the prior information is often unreliable. Small weights are risky, as they can weaken strong -values. For instance if but , then the weighted -value is a meager .

Choosing the lower bound presents a bias-variance tradeoff. A large lower bound, say 0.5, has “low variance” as the weighted -values do not change much. However it potentially has “high bias” as the truly optimal weights may be small. Empirically, we found that a lower bound in the range 0.01-0.5 often works well (see the data analysis section).

Using an upper bound , no hypothesis with -value is rejected. For instance, if and , then only the -values have a chance of being rejected. The upper bound ensures that we do not place too much weight on any hypothesis. Princessp allows the user to conveniently specify arbitrary bounds for the weights.

-

3.

Stratified weights. Let be disjoint subsets of . With stratified weights, we want to assign an equal weight to the hypotheses in the same subset , for each . This is the linear equality constraint that , for all , and for all .

Stratification is natural when effects are grouped, say into different functional classes of genetic variants in genome-wide association studies. The stratified FDR method (Sun et al., 2006), is closely related.

Related ideas were also used more informally in previous work. In a study of nicotine dependence with approximately 3700 genetic variants, Saccone et al. (2007) improve power by giving nicotine receptor genes ten times the weight of other candidate genes. More generally, Roeder and Wasserman (2009) study binary weights that take only two possible values. Similarly, Sveinbjornsson et al. (2016) assign weights to classes of variants in GWAS based on functional annotation. As another example, Eskin (2008) groups polymorphisms by location in the genome, assigning them to a tag and requiring the same weight for each tag. Stratified weights can be incorporated in a direct was as convex constraints in Princessp.

-

4.

Smooth weights. If the hypotheses have some spatial structure, then it is reasonable to require that the weights be “smooth” with respect to this structure. For instance, genetic variants are aligned on chromosomes, and one could require the weights to be smoothly varying as a function the position. This can be achieved in many ways, borrowing from the vast literature on regularization in statistics. A simple example is to add a total variation constraint , for say.

A related idea appears in Rubin et al. (2006), who show in simulations that power improves substantially by applying a smoothing spline to the weights, when the true effects are smooth as a function of . Roeder and Wasserman (2009) also find that smoothing the weights improves power when weights are estimated by sample splitting. Ignatiadis et al. (2015) observe that adding a total-variation penalty or a penalty of the form can reduce variance. Princessp allows users to specify such constraints in a general principled framework.

In specific applications, there can be many other constraints that incorporate problem-specific information and requirements.

2.4 Related work

There are many methods for multiple testing with prior information, partially reviewed by Roeder and Wasserman (2009) and Gui et al. (2012), some mentioned earlier. Candidate studies—testing the top candidates based on prior information—are as old as statistics itself. They can be viewed as -value weighting methods with binary weights.

More general methods for multiple testing with prior information have been developed since at least the 1970’s. Most work focuses on single-step Bonferroni procedures maximizing the average power and controlling the family-wise error rate. In seminal work, Spjøtvoll (1972) described theoretically such procedures under very general conditions.

Later work extended Spjøtvoll’s results in several ways. Benjamini and Hochberg (1997) allowed weights in the importance of the hypotheses. Roeder and Wasserman (2009) and Rubin et al. (2006) found explicit optimal weights in the Gaussian model . Eskin (2008) and Darnell et al. (2012) extended their framework to genome-wide association studies, accounting for correlations.

Westfall et al. (1998) considered the model with proper priors on . They gave small-scale algorithms to find optimal weights for the Bonferroni method via nonconvex optimization. Dobriban et al. (2015) showed how to find the weights efficiently under a Gaussian prior.

Less is known beyond the Bonferroni method. Holm (1979)’s step-down method can use weights, and Westfall and Krishen (2001) and Westfall et al. (2004) considered finding optimal weights for small . Genovese et al. (2006) showed that the weighted Benjamini–Hochberg procedure controls the FDR and Roquain and Van De Wiel (2009) showed how to choose weights optimally in a special asymptotic regime. Peña et al. (2011) developed a general decision-theoretic framework for weighted family-wise error rate and FDR control.

Bretz et al. (2009) and follow-up work developed a graphical approach to stepwise multiple testing. To use this in large-scale applications, one needs to design a graph specifying how the levels are distributed upon rejection of each individual hypothesis.

Another line of work considers data re-use, by constructing weights using the same dataset where the tests are performed. Rubin et al. (2006) proposed a sample-splitting approach combined with smoothing. In a slightly different setup, Storey (2007) developed the Optimal Discovery Procedure, maximizing the expected number of true discoveries, subject to a constraint on the expected number of false discoveries. Sun and Cai (2007) developed a method maximizing the marginal False Nondiscovery Rate (mFNR) subject to controlling the marginal False Discovery Rate (mFDR), estimated the oracle procedure consistently in a hierarchical model.

Bourgon et al. (2010) proposed an independent filtering approach where test statistics are independent of the prior information only under the null, not under the alternative hypothesis. Recently, Ignatiadis et al. (2015) proposed the more general Independent Hypothesis Weighting framework. This promising approach focuses on the false discovery rate, relies on convex relaxations for efficient computations, and splits of the tests to ensure type I error control.

3 Monotone -value weights

The key practitioner constraints motivating Princessp were the need for monotonicity and boundedness of one-sided Gaussian weights. We now study that important example in detail. We develop algorithms to compute bounded monotone weights for one-sided Gaussian tests, and explore their performance in simulations and GWAS data analysis. This is a helpful example because unconstrained Gaussian Spjøtvoll weights are well understood and provide a solid background for comparison.

Assuming the prior means are sorted such that , the bounded monotone weights problem with lower bound and upper bound is:

| (4) | ||||

| s.t. | (5) |

One justification for monotonicity is that larger effects are worth more. Another justification is that for a sufficiently small significance level , the optimal Spjøtvoll weights are in fact monotone.

Proposition 3.1 (Monotonicity of one-sided Spjøtvoll weights for small ).

Let us denote and . Suppose that the significance level is small enough that . Then the unconstrained Spjøtvoll weights defined by Eq. (1) are monotone increasing in .

Proof.

As shown by Rubin et al. (2006) and Roeder and Wasserman (2009), the Spjøtvoll weights are , for the unique such that . Since all means are negative, is decreasing. By the assumption on , , hence .

Now, the map has derivative , which is negative if . By assumption on , and by the above conclusion, for all . Hence the map is decreasing in a range including all . Therefore the weights are monotonically decreasing as a function of , as desired. ∎

A similar but somewhat more involved statement also holds for two-sided Spjøtvoll weights.

Proposition 3.2 (Monotonicity conditions for two-sided Spjøtvoll weights).

Proof.

As shown in Proposition 2.3, under our conditions, the weights are , where , and is the unique constant such that . Clearly, the weights are an even function of .

To show that the weights are monotone increasing in , it is enough to ensure that the map is decreasing for . For this, let us re-parametrize by , and denote , so that . It is enough to show that is decreasing as a function of . Now , so that

To ensure , it suffices to argue that

or equivalently that Now, for , so, after taking logarithms, it is enough to show that . Suppose now that for some constant . Since is decreasing for , it suffices to show that , where . This is equivalent to , or , or also . Recalling the definition of , this inequality and are equivalent to

or also . The same inequality can be written as

Since this has to be true with for all , it is enough to ensure

Since is a strictly increasing function of going from to on , while is a strictly decreasing function of going from to on , there is a uniqe where . Choosing this , we obtain that the requirement is .

Since is defined by , and is strictly decreasing, this is equivalent to . This finishes the proof. ∎

While the above propositions hold under a mild constraint, the optimal weights are not bounded away from zero or infinity in general. This must be imposed as a separate constraint.

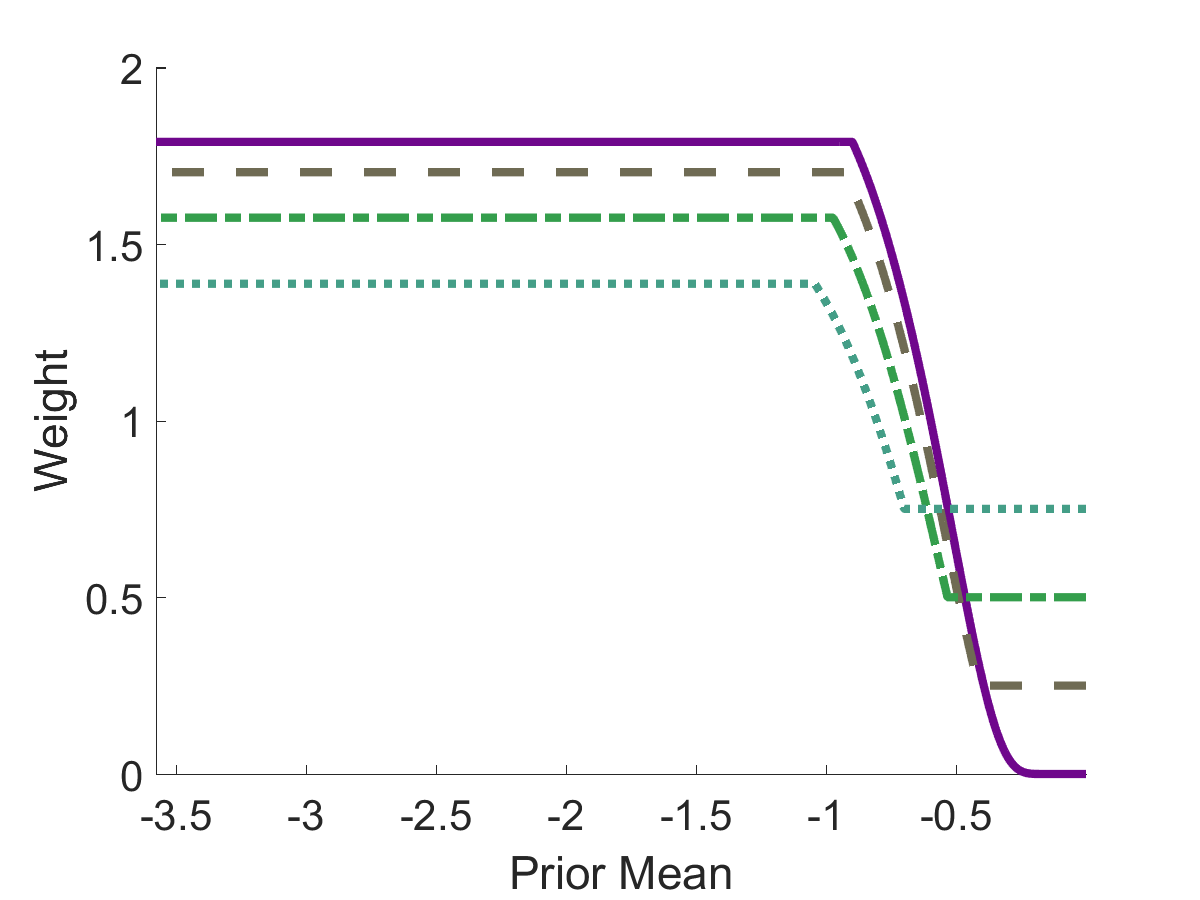

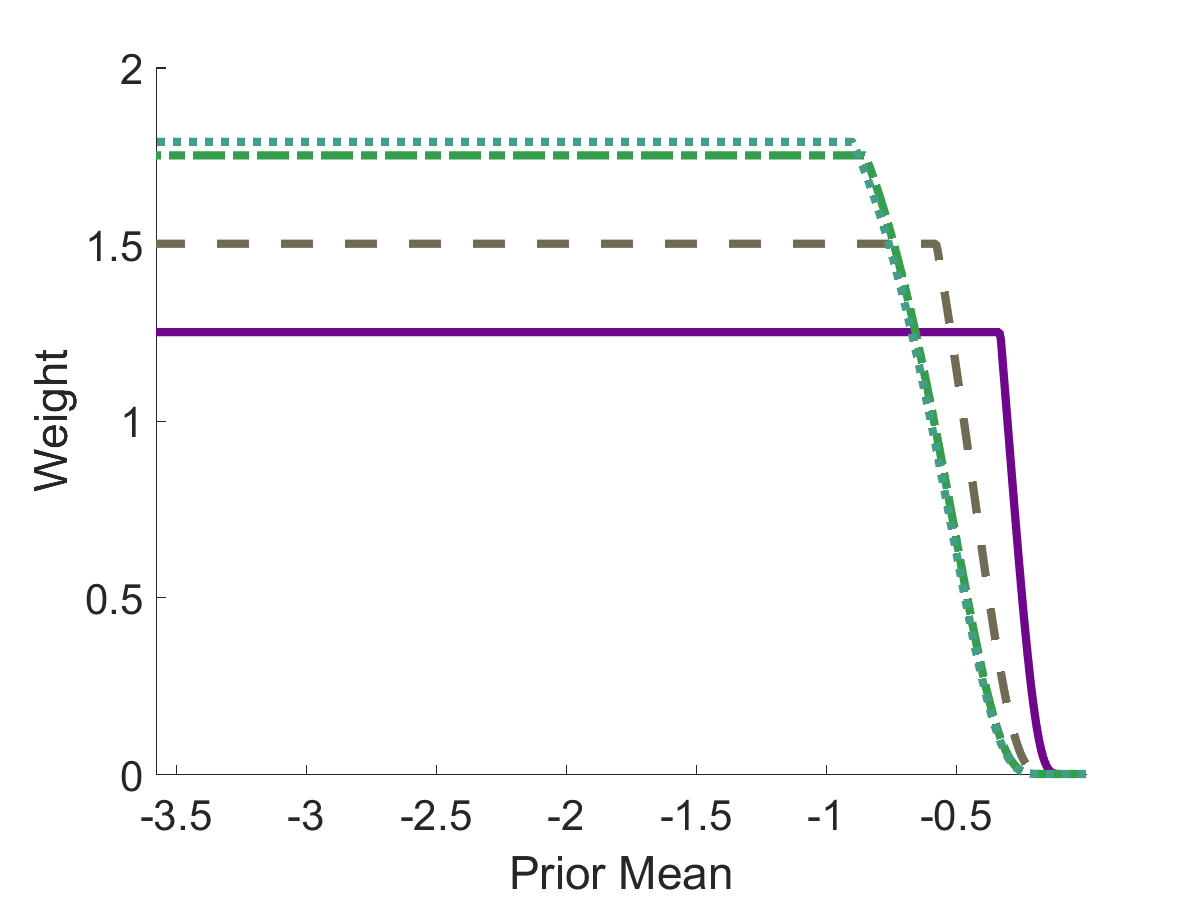

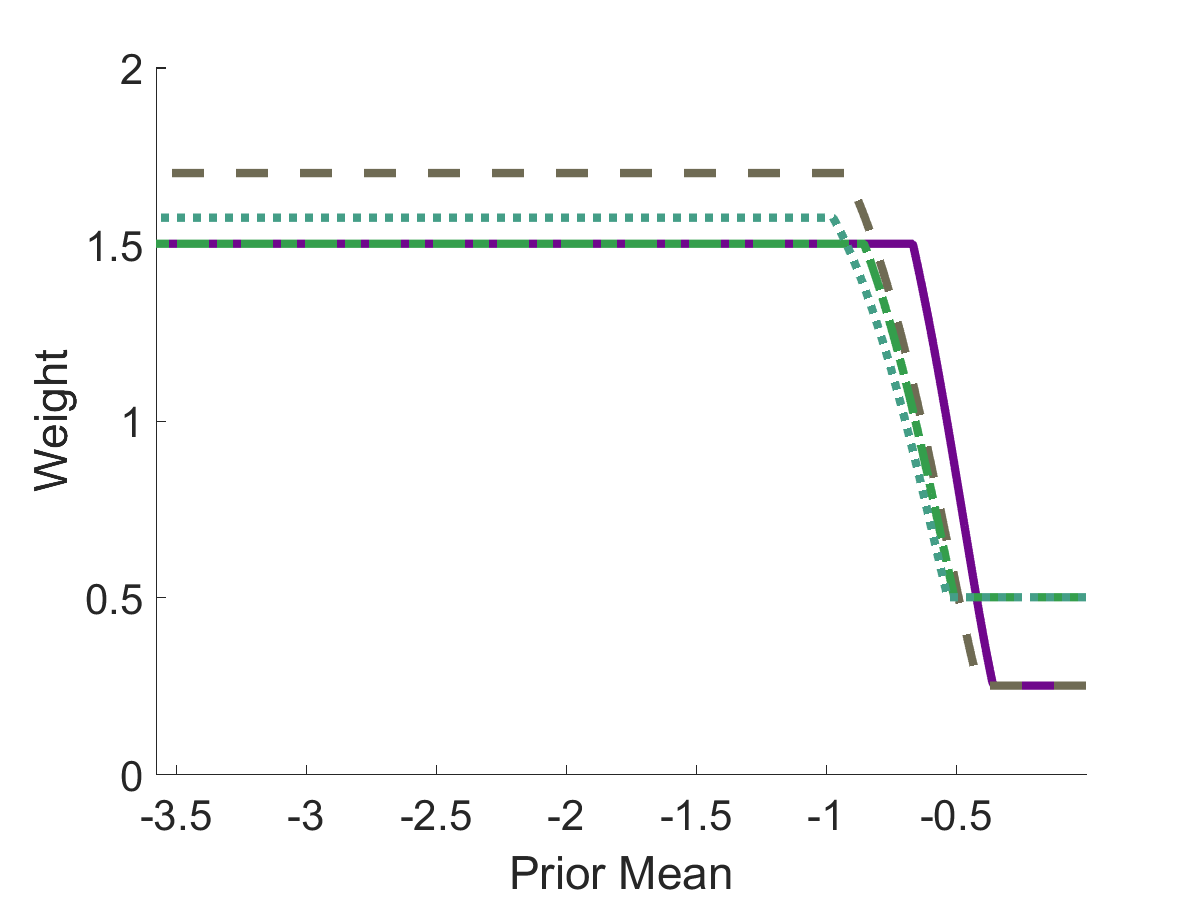

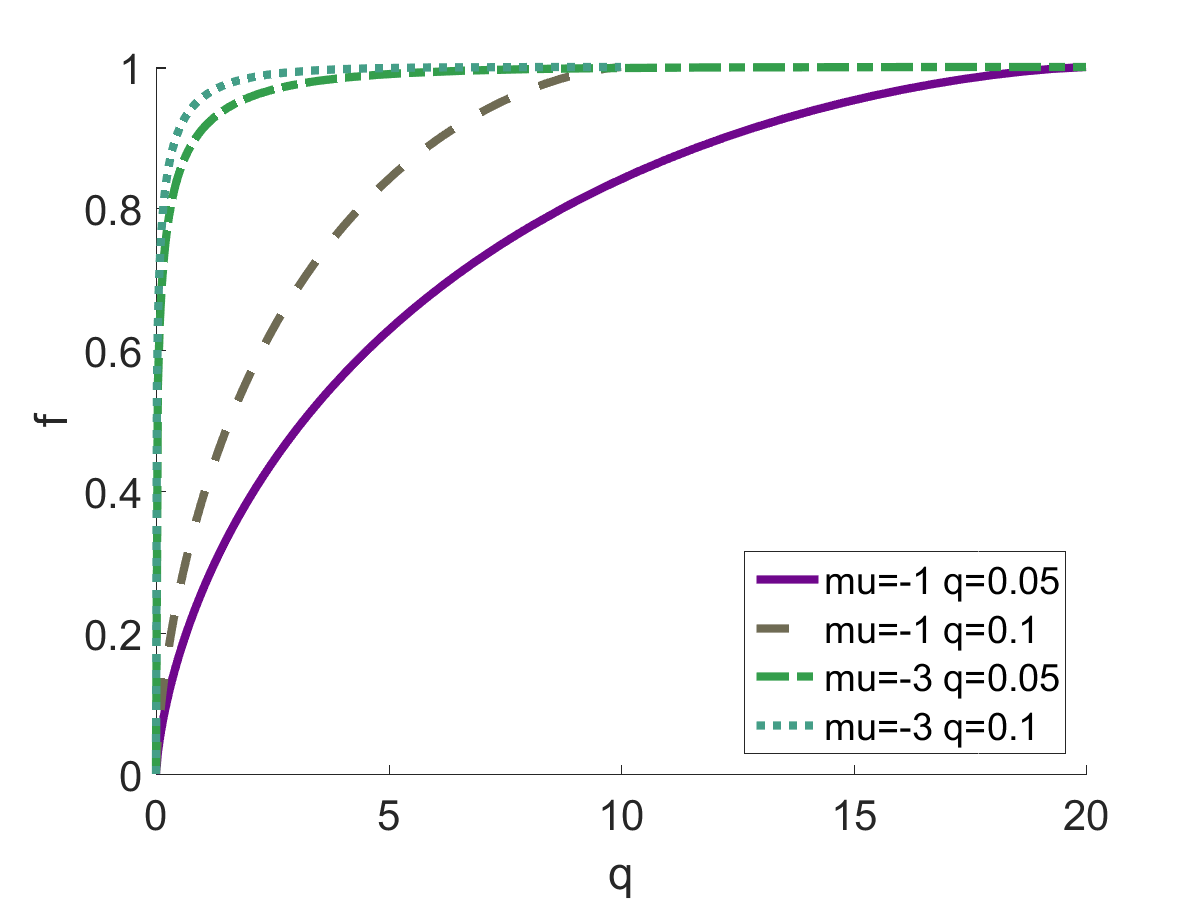

We illustrate monotone weights, and their dependence on the bounds. We take hypotheses, set the -value cutoff , and draw random effect sizes , where are iid standard normal. First we vary from 0 to 0.75 in steps of size 0.25, keeping . Next we vary from 1.25 to 2 in steps of size 0.25, keeping the (Fig. 1).

Lower bounded weights (Fig. 1(a)) are flat near the two endpoints, and increase sharply in between. This may be surprising because flatness is not required in the optimization problem. In addition, increasing the lower bound also leads to a decreased upper bound, a property that is not immediately obvious theoretically. Upper bounded weights (Fig. 1(b)) have a similar but steeper shape. The weights are still flat, however, they are not automatically lower bounded (strictly above 0) anymore. Finally, we vary both and (Fig. 1 (c)), with in , and in . The weights have the same general shape.

3.1 Power loss compared to Spjøtvoll weights

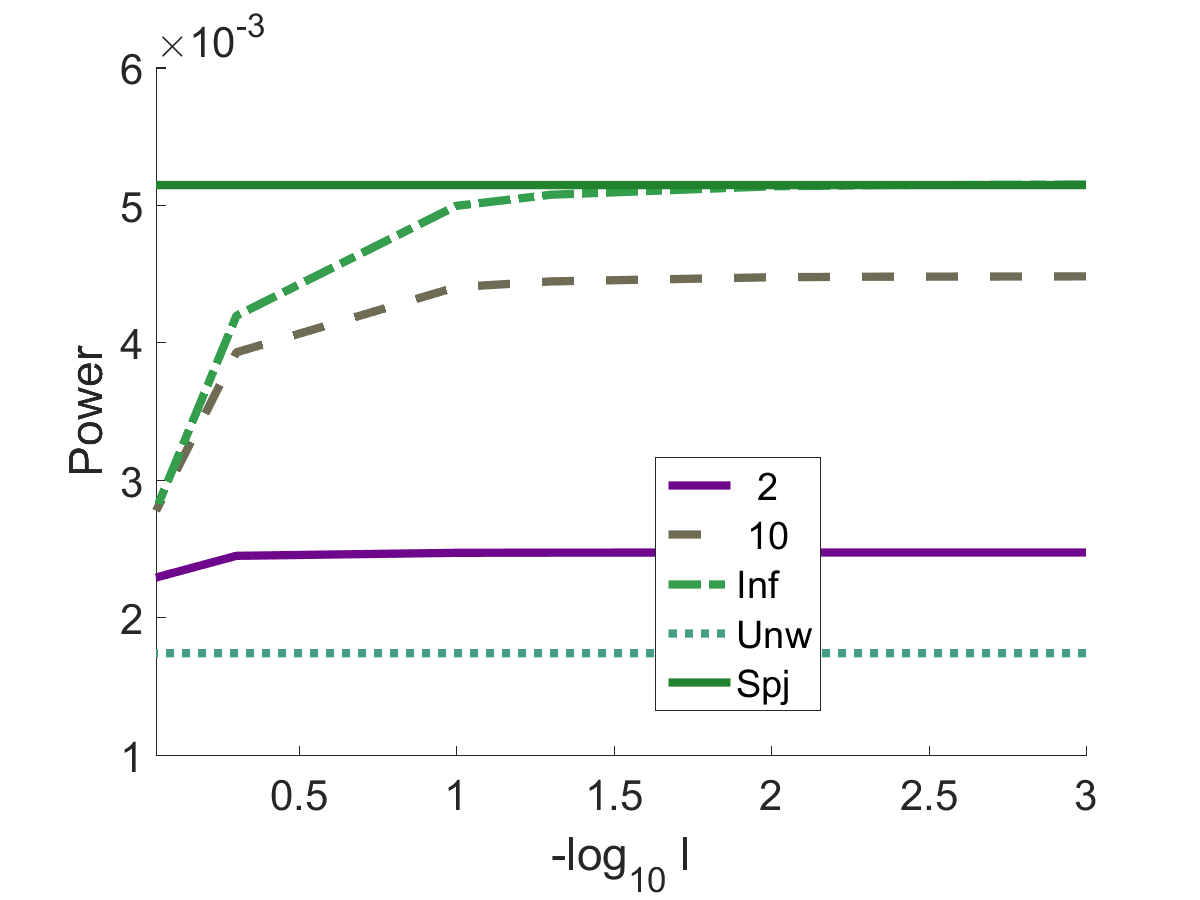

Since bounded weights are suboptimal to Spjøtvoll weights when the model is correct, it is interesting to understand the loss in power. This may help to form heuristics for the choice of lower and upper bounds. On Fig. 2 we report the results of a simulation where , , the means are generated as iid negative absolute Gaussian, while the lower bounds are and the upper bounds are . We define the power as the value of the maximized objective function in Eq. (4). We also display the power of the unweighted Bonferroni method (lowest horizontal line), and the optimal Spjøtvoll weighted Bonferroni method (highest horizontal line).

In this setting, an upper bound of two leads to a severe power loss of at least 50%, regardless of the lower bound. However, an upper bound of 10 leads to only a small loss in power, while an upper bound of leads to nearly full power if the lower bound is at most . We conclude that lower bounds below 0.1 and upper bounds above 10 seem to lead to a small loss in power.

3.2 Data analysis example

To illustrate the empirical performance of Princessp, and specifically of bounded monotone weights, we analyze a standard set of datasets on genome-wide association studies (GWAS). We follow the protocol and methodology laid out in Dobriban et al. (2015). There, we analyzed five studies on four complex human traits and diseases: CARDIoGRAM and C4D for coronary artery disease (Schunkert et al., 2011; Coronary Artery Disease Genetics Consortium, 2011), blood lipids (Teslovich et al., 2010), schizophrenia (Schizophrenia Psychiatric Genome-Wide Association Study Consortium, 2011), and estimated glomerular filtration rate (eGFR) creatinine (Köttgen et al., 2010).

In addition to these, here we also include the 90Plus dataset (Deelen et al., 2014), which compares the lifespan of a sample of Caucasian individuals living at least 90 years with matched controls (see the Supplement). These studies have -values for the marginal association of 500,000–2.5 million single nucleotide polymorphisms (SNPs) to the outcome. More detail is provided in Sec. 6.

Testing SNPs one at a time using unweighted Bonferroni is typically the first analysis performed in genome-wide association studies (see e.g., Schunkert et al., 2011; Coronary Artery Disease Genetics Consortium, 2011; Teslovich et al., 2010; Schizophrenia Psychiatric Genome-Wide Association Study Consortium, 2011; Köttgen et al., 2010). Therefore, in our data analysis we compare directly the state of the art unweighted Bonferroni method to weighted Bonferroni methods.

We analyze several pairs of these datasets, starting with those that were already included in Dobriban et al. (2015). As a positive control for our method, we use CARDIoGRAM as prior information for C4D. Motivated by the Bayesian analysis of Andreassen et al. (2013), we use the blood lipids study as prior information for the schizophrenia study. Motivated by the comorbidity between heart disease and renal disease (Silverberg et al., 2004), we use the creatinine study as prior information for the C4D study.

In addition to these pairs, we add four new examples:

-

1.

We switch the roles of the two heart disease studies, and use C4D as prior information for CARDIoGRAM.

-

2.

We use the 90Plus dataset as a target study, and check if studies on heart disease and schizophrenia can increase the number of hits. This is a challenging example, as the 90Plus data set has weak signal (Deelen et al., 2014). We use the above three datasets as prior information as they seem to be the most promising from our prior work (Fortney et al., 2015).

| Un | Spjot | Filter() | Bayes() | Mon() | |||||||

| Parameter | 2 | 4 | 6 | 1 | 10 | ||||||

| Pruned | |||||||||||

| CG C4D | 4 | 11 | 10 | 10 | 6 | 10 | 8 | 4 | 11 | 10 | 9 |

| C4D CG | 9 | 14 | 22 | 11 | 3 | 14 | 12 | 9 | 16 | 15 | 15 |

| Lipids SCZ | 4 | 1 | 2 | 2 | 2 | 1 | 1 | 5 | 2 | 2 | 4 |

| eGFRcrea C4D | 4 | 2 | 1 | 0 | 1 | 2 | 4 | 4 | 4 | 4 | 4 |

| CG 90Plus | 1 | 1 | 1 | 0 | 0 | 1 | 1 | 1 | 1 | 1 | 1 |

| C4D 90Plus | 1 | 1 | 1 | 1 | 0 | 1 | 1 | 1 | 1 | 1 | 1 |

| SCZ 90Plus | 1 | 0 | 0 | 0 | 0 | 0 | 1 | 1 | 1 | 1 | 1 |

| Score (Pruned) | 0 | -1 | -1 | -2 | -5 | -1 | 1 | 1 | 1 | 1 | 2 |

| Unpruned | |||||||||||

| CG C4D | 29 | 45 | 40 | 48 | 34 | 44 | 39 | 29 | 45 | 43 | 40 |

| C4D CG | 38 | 39 | 68 | 48 | 30 | 39 | 39 | 38 | 53 | 52 | 48 |

| Lipids SCZ | 116 | 214 | 217 | 96 | 39 | 214 | 223 | 123 | 217 | 220 | 225 |

| eGFRcrea C4D | 29 | 18 | 1 | 0 | 1 | 18 | 23 | 29 | 23 | 25 | 29 |

| CG 90Plus | 4 | 3 | 1 | 0 | 0 | 4 | 4 | 4 | 4 | 4 | 4 |

| C4D 90Plus | 1 | 2 | 2 | 1 | 0 | 2 | 1 | 1 | 2 | 2 | 2 |

| SCZ 90Plus | 2 | 0 | 0 | 0 | 0 | 0 | 2 | 2 | 2 | 2 | 2 |

| Score (Unpruned) | 0 | 1 | 1 | -2 | -6 | 2 | 2 | 1 | 3 | 3 | 4 |

| Total Score | 0 | 0 | 0 | -4 | -11 | 1 | 3 | 2 | 4 | 4 | 6 |

For each pair of studies, we restrict to the SNPs that appear in both. For each SNP, we have a two-sided -value in the prior study, typically computed from a normal meta-analysis. From this we can back out the prior -score . We choose the sign so that , and optimize our weights for a a one-sided follow-up test in the same direction. This corresponds to a test for replicated sign. We do this because we have discussed monotone bounded weights for one-sided tests. We rescale the effect size , as in (Dobriban et al., 2015, Sec. 6.2) to estimate the effect size in the new study. Here and are the current and prior sample size for the -th variant, respectively. We control the family-wise error rate at .

We then compute optimal -value weights with various methods. In Dobriban et al. (2015), we reported the results of five weighting schemes: unweighted Bonferroni testing, as well as weighted Bonferroni testing using Spjøtvoll weights, Bayes weights (Dobriban et al., 2015), filtering, and exponential weights (Roeder et al., 2006). Filtering selects all tests below a prior -value cutoff, weighting them equally. Here we report new results using Princessp, specifically bounded monotone weights with lower bounds , and upper bound . The results for upper bound are very similar. We exclude exponential weights, as other methods performed better in our earlier work.

As in Dobriban et al. (2015), we prune the significant single nucleotide polymorphisms for linkage disequilibrium using the DistiLD database (Palleja et al., 2012). We compute a score for each weighting method on each data set . This is defined as if the weighting method increases the number of hits compared to unweighted testing, 0 if it leaves it unchanged, and otherwise. The score of a weighting method is the sum of scores over datasets. We compute scores separately for the pruned and unpruned analysis, and add them to find the final score. Table 2 shows the number of significant loci.

Princessp, i.e. monotone weighting, shows a good performance for all settings. In the pruned analysis, it has a score of two for the lower bound . It increases the number of rejections in two out of the seven settings, and keeps it the same in the others. In the unpruned analysis, it has a score of four with , increasing the number of hits in four settings, and never decreasing it. Monotone weights with other lower bounds also lead to more hits in some cases, but they can also decrease the number of discoveries.

Monotone weights perform well compared to the other methods. In particular, filtering decreases the number of hits in many cases, especially when the -value cutoff is or . Bayes weights, especially for , have a relatively stable performance. With , they decrease the number of hits in only two settings, while increasing it in five pairs. However, they decrease the number of hits more frequently for other values. Moreover, monotone weights have a larger number of discoveries than Bayes weights.

No weighting scheme increases the number of pruned SNPs in the 90Plus study. Even in this challenging example, however, monotone weights seem more stable than the others, as they do not decrease the number of hits.

4 Optimization methods

4.1 General remarks

The Princessp optimization problems presented in Sec. 2 are convex programs with convex inequality constraints. Here we propose using the log-barrier interior point method, which is a general approach to such problems (e.g., Boyd and Vandenberghe, 2004, Sec. 11). However, it is not immediate a priori that this approach will work well in our case. Indeed, we find that for monotone weights the straightforward application of the method leads to severely ill-conditioned KKT systems for large problems. Therefore, we develop a new subsampling method to avoid ill-conditioning.

For concreteness, we will focus on Gaussian one-sided weights presented at the beginning of Sec. 2, but the more general case is similar; only the ROC function changes. To start, we discuss a few analytic properties of the optimization problem. The ROC function (plotted on Fig. 3) is defined without ambiguity on , and can be defined by continuity at the two endpoints. Indeed, as , , so that . Similarly at the other endpoint. Further, is concave on , and importantly, its derivatives are convenient to compute. Indeed, denoting the -score , we have and . Thus is concave in for all , and it is strictly concave for . The second derivative is unbounded as , because is much larger than the other terms.

The log-barrier method solves a sequence of equality-constrained problems indexed by , replacing the inequality constraints by a penalty for an increasing sequence of . The equality-constrained problems are solved using Newton’s method. Under the assumptions stated at the beginning of Sec. 2, it follows from the general convergence analysis for the barrier method, see p. 577, Sec. 11.3.3, in Boyd and Vandenberghe (2004) that the barrier method converges for solving the convex constrained Spjøtvoll weights optimization problem. Since we assumed that an optimal exists, strong convexity is ensured by compactness of the set .

In the two-sided normal testing example, the log-barrier method converges when restricted to the region for , where the problem is strongly convex.

4.2 Monotone weights

In this section we explain our method for computing monotone bounded weights (Eq. (4)). To enable efficient computation for problems with tens of millions of weights, we need to exploit the tridiagonal structure of the Hessian and solve the KKT systems arising the in the Newton steps in -time directly. For this we need to implement several steps of the optimization method (Algorithm 1).

The method involves a number of optimization parameters, for which we use the default settings from Boyd and Vandenberghe (2004) Sec. 11. In addition, we need to choose a strictly feasible starting point . For this, we let , and be the mean-centered version of . Then we let

| (6) |

where is the all ones vector and is a small constant such that the vector is strictly feasible. This is clearly possible if .

4.2.1 Centering problem

From now on we flip the sign of the objective, so that we are minimizing a convex function. For a penalty parameter , the logarithmic barrier problem—or centering step—is the convex program:

| (7) | ||||

| (8) |

Here we define the constants , for brevity.

We now show that the Karush-Kuhn-Tucker (KKT) matrix is a sum of a tridiagonal and a rank one matrix, so that the KKT system can be solved in time. Let be the objective function, its gradient, and its Hessian. Let us also denote by the Newton step for , and by the scalar dual variable corresponding to the sum constraint (Boyd and Vandenberghe, 2004, p. 577). Then the KKT system for finding at a particular (suppressed for ease of notation) is

| (9) |

Assuming is invertible, standard linear algebra shows that the solution has the form:

The Newton decrement is defined as

| (10) |

To solve the Newton system, we must calculate and . First, the components of the gradient are:

where we denoted the -score . Next, the diagonal components of the Hessian are

and the off-diagonal terms vanish except those on the band just one-off the diagonal, which are . Hence, the Hessian matrix is tridiagonal. With the notation , the Hessian has the form where is the tridiagonal matrix

and is the diagonal matrix Finally is invertible because it is the sum of two positive definite matrices. Indeed the diagonal terms in are strictly positive if . Further is positive definite, as for a vector , the quadratic form equals Now for all , so implies that all are equal to 0. This shows that is positive definite.

Hence, we have shown that is positive definite, and thus invertible. Therefore, the KKT system involves the solution of a tridiagonal-plus-rank 1 linear system, taking time. This is implemented using a standard sparse tridiagonal linear solver in MATLAB, which is stable since is positive definite.

4.2.2 Subsampling

Based on the earlier simulation results (e.g., Fig. (1)), and on intuition from isotonic regression, we expect that the solution may have many equal terms, lying on the boundary of the feasible set. It is known that this can lead to an ill-conditioned KKT system (e.g., Nocedal and Wright, 2006, Ch. 17).

To deal with this problem, we propose a subsampling method. If is larger than a constant , we subsample means evenly spaced among the indices . Here we choose . To avoid ties, we then subsample the remaining means starting from and discard the remaining terms , until the first index where . We then repeat this starting from , and so on. We choose the small constant . We use the barrier method to compute weights on the subsample, and then interpolate linearly to the remaining means.

This new subsampling approach is crucial to enable the application of Princessp to large-scale problems with millions of hypotheses. We also show in Section 4.3.1 that subsampling does not affect too much the accuracy of the weights on smaller problems. On larger problems, it usually avoids the ill-conditioned KKT systems encountered by the naive barrier method.

4.3 Experiments

In this section we report the results of several experiments with our optimization method.

4.3.1 Accuracy of subsampling

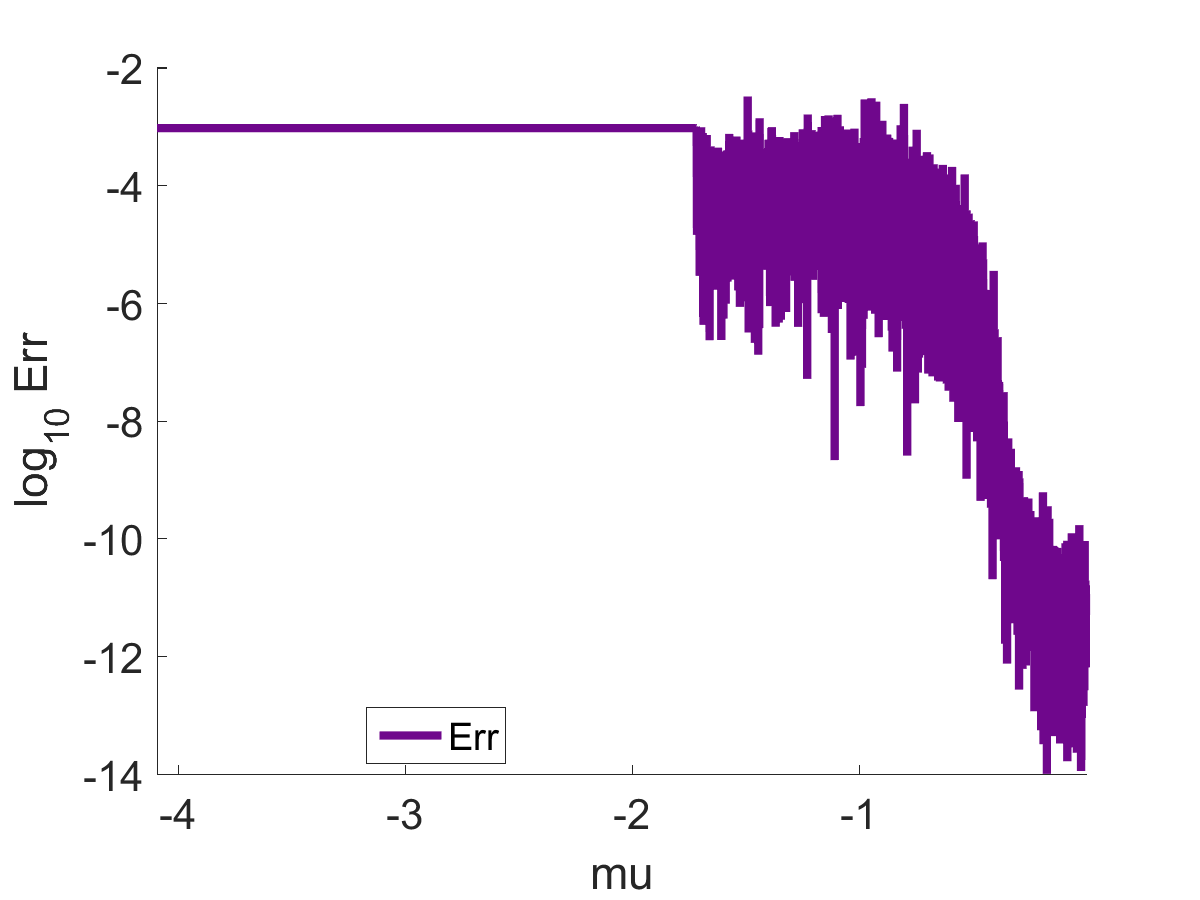

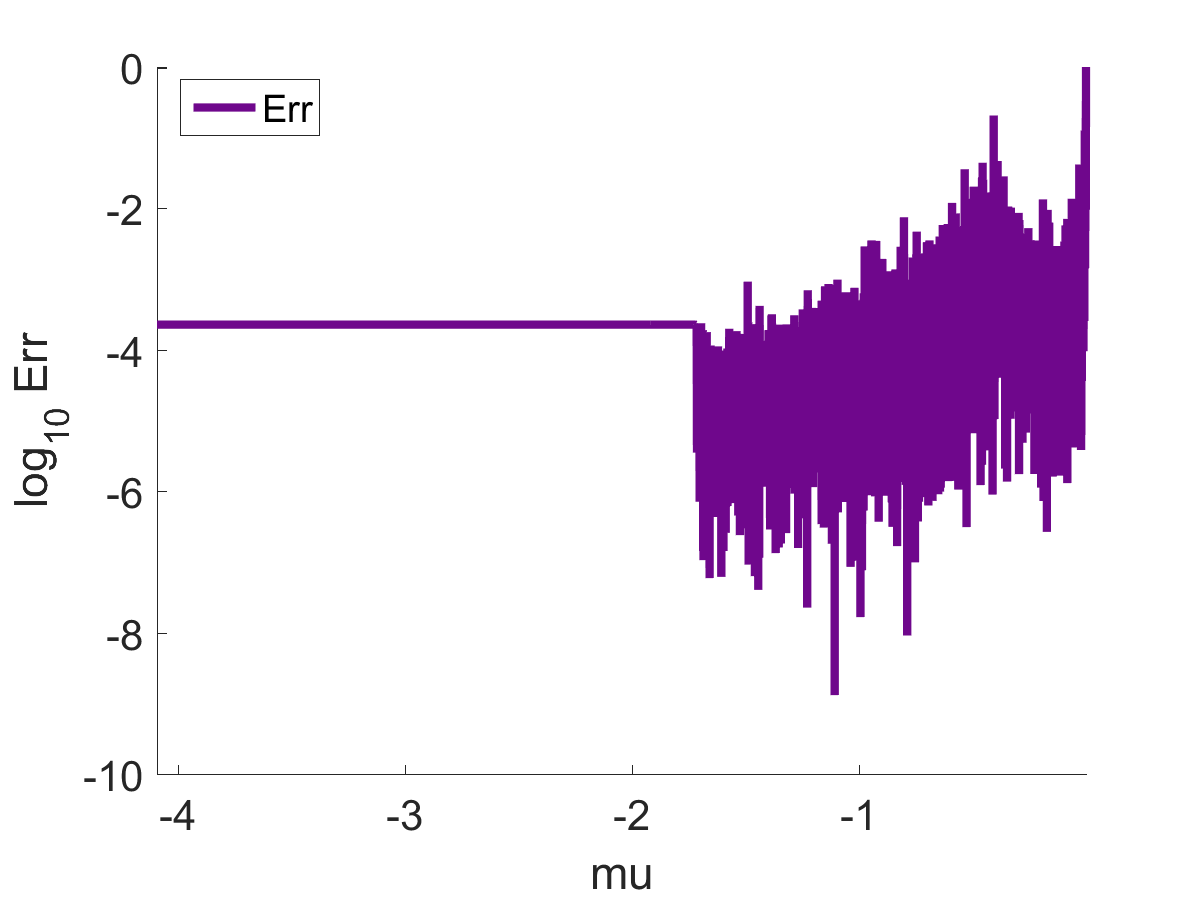

In Section 4.2.2 we introduced a subsampling method to avoid the ill-conditioning of the KKT system. Here we show that the method does not lose too much accuracy compared to the full barrier method. We set , , draw random where are iid standard normal, and set the bounds , . We compute weights using the standard barrier method (), and using the barrier method with subsampling (. We then compute the absolute error and relative error (defined pointwise as ). The two weighting schemes (Fig. 4) agree within at least two significant digits in terms of absolute error for all means. The relative error can be as large as , but only when the absolute error is smaller than , so that this still translates to a good accuracy.

4.3.2 Comparison with Spjøtvoll

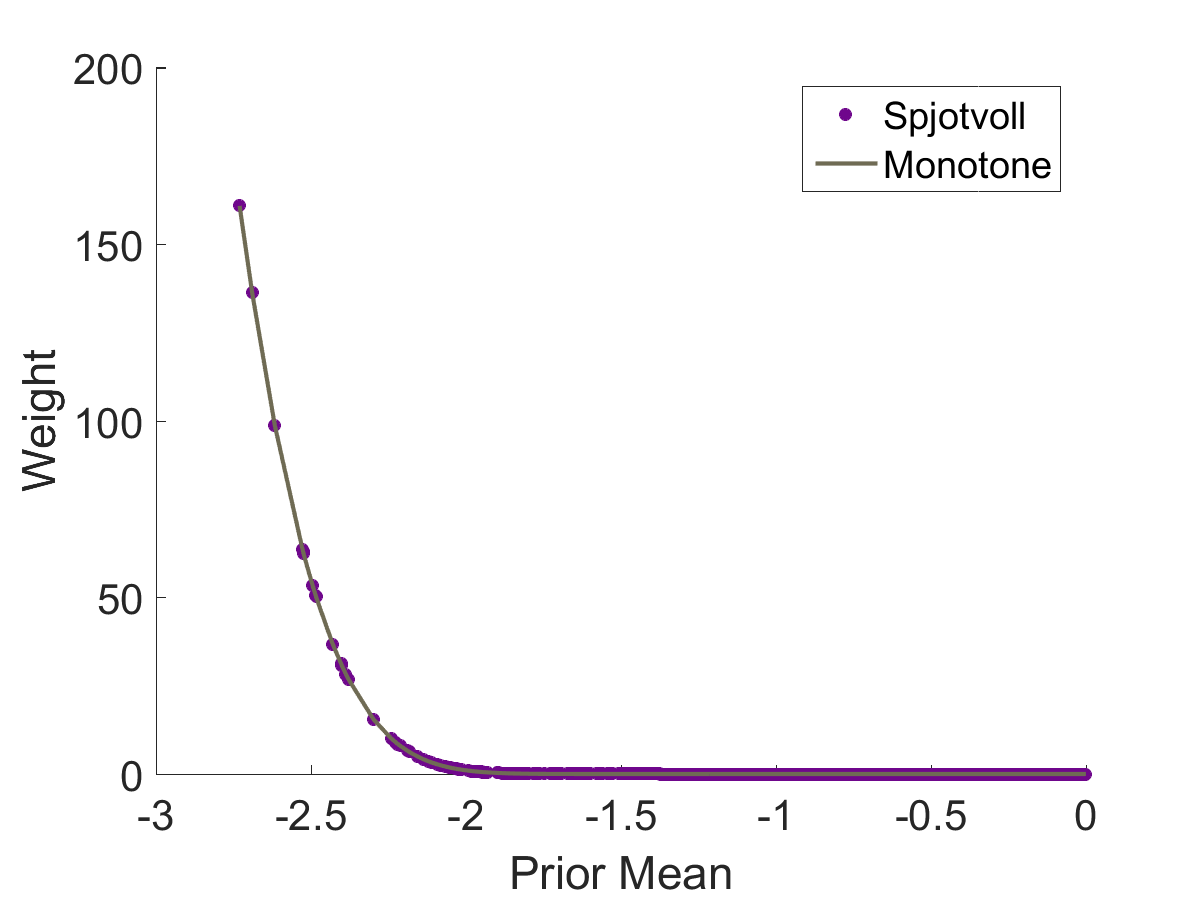

We showed in Proposition 3.1 that Spjøtvoll weights are monotone if is small. Thus we can compare the two methods on a problem where they should give the same results. We set , , draw random where are iid standard normal, and set , . Spjøtvoll weights (1) and monotone weights (4) are visually indistinguishable (Fig. 5(a)).

4.3.3 Running time

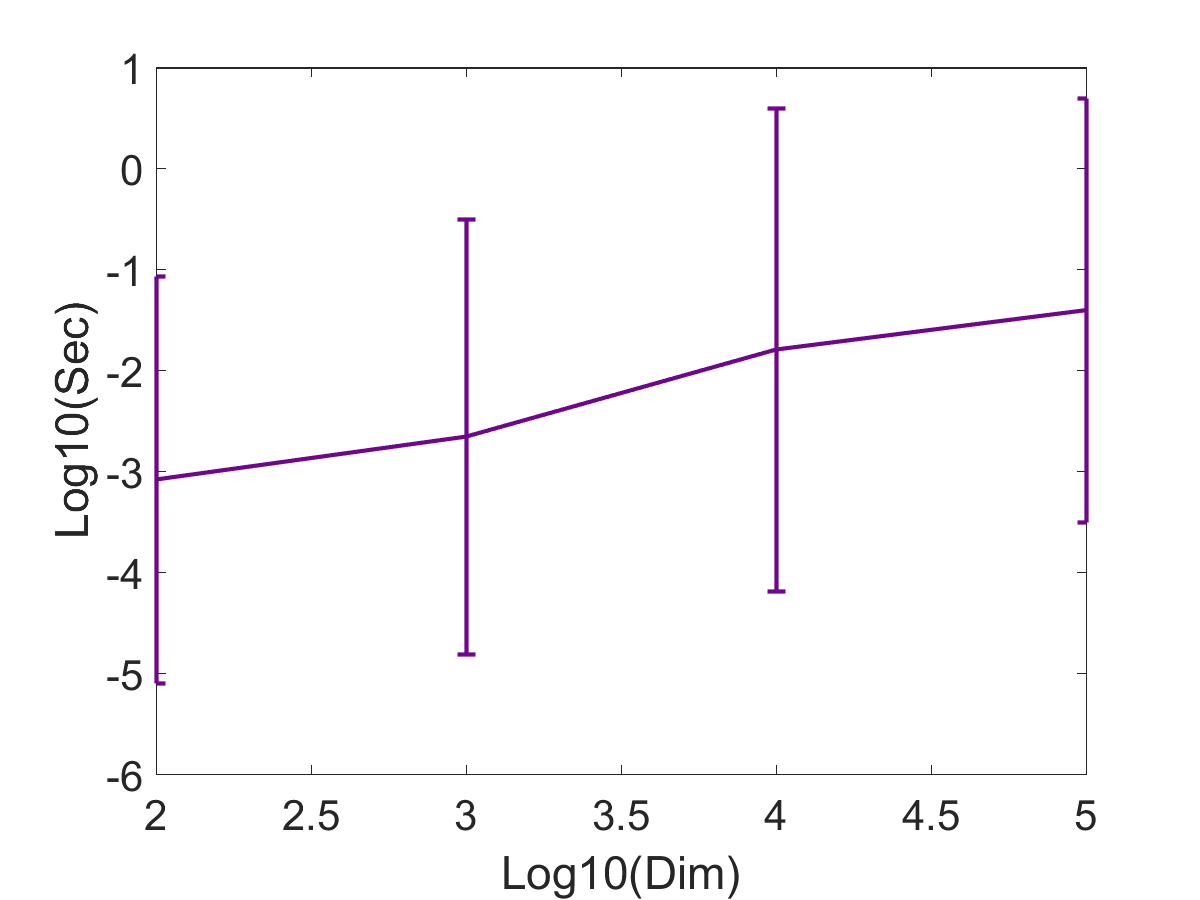

To test the running time of our method, we vary in the range of –, choosing as above. The parameters and are chosen randomly as , , where , are independent uniform random variables on the unit interval. We also take . The average running times over 50 simulations are shown in Fig. 5(b), and they are below a second even for the largest .

5 Discussion

In this paper we developed the Princessp method, employing convex optimization for large-scale weighted Bonferroni multiple testing. Our approach enabled many different constraints. We found that bounded monotone weights perform well empirically in the analysis of genome-wide association studies.

In particular, it appears that imposing a lower bound such as can improve the empirical performance of -value weighting methods. The reason is that the current -values are multiplied by a small constant—at most two in the example above—and hence significant effects stay significant. Many of the current state of the art weighting methods, such as Spjøtvoll, exponential, or Bayes weighting, do not have this property. Therefore, practitioners using them risk losing significant -values. Bounded weights offer a principled way to avoid this problem. We think that this observation may go a long way in making -value weighting methods more routinely applicable.

Acknowledgements

We thank Art Owen and Stuart Kim for discussion, and David Donoho for feedback on an earlier version of the manuscript. We acknowledge financial support from NSF grants DMS-1418362 and DMS-1407813, and an HHMI International Student Research Fellowship.

6 Data sources

6.1 CARDIoGRAM and C4D

CARDIoGRAM is a meta-analysis of 14 coronary artery disease genome-wide association studies, comprising 22,233 cases and 64,762 controls of European descent (Schunkert et al., 2011). The study includes 2.3 million single nucleotide polymorphisms. In each of the 14 studies and for each single nucleotide polymorphism, a logistic regression of coronary artery disease status was performed on the number of copies of one allele, along with suitable controlling covariates. The resulting effect sizes were combined across studies using fixed effects or random effects meta-analysis with inverse variance weighting. Finally, two-sided normal -values were computed.

C4D is a meta-analysis of 5 heart disease genome-wide association studies, totalling 15,420 coronary artery disease cases and and 15,062 controls (Coronary Artery Disease Genetics Consortium, 2011). The samples did not overlap those from CARDIoGRAM. The analysis steps were similar to CARDIoGRAM.

The consortia require that the following acknowledgment be included: Data on coronary artery disease / myocardial infarction have been contributed by CARDIoGRAMplusC4D investigators and have been downloaded from www.CARDIOGRAMPLUSC4D.ORG.

6.2 Chronic Kidney Disease Consortium

This is a genome-wide association study of kidney traits in 67,093 participants of European ancestry from 20 population-based cohorts (Köttgen et al., 2010). Estimated glomerular filtration rate creatinine was the trait with the largest sample size. There is no reported overlap with the samples from C4D. The analysis steps were similar to the previous two studies.

6.3 Blood Lipids

This is a genome-wide association study of blood lipids in a sample from European populations (Teslovich et al., 2010). Triglyceride levels were one of the traits, with sample size 96,598, chosen here out of all lipids because of its previous appearance in Andreassen et al. (2013). Standard protocols for genome-wide association studies were used: linear regression analysis controlling for study-specific covariates, combined using fixed-effects meta-analysis.

6.4 Psychiatric Genomics Consortium - Schizophrenia

This is a mega-analysis, which uses the raw data not just summaries of other studies, combining genome-wide association study data from 17 separate studies of schizophrenia, with a total of 9,394 cases and 12,462 controls (Schizophrenia Psychiatric Genome-Wide Association Study Consortium, 2011). They tested for association using logistic regression of schizophrenia status on the allelic dosages. The overlap with the blood lipids study consists of 1,459 controls, which amounts to of controls in the schizophrenia study. The overlapping controls are from the British 1958 Birth Cohort of the Wellcome Trust Case Control Consortium.

6.5 90Plus Study - Aging

Deelen et al. (2014) performed a genome-wide association meta-analysis of 5406 long-lived individuals of European descent (aged at least 90 years). They combined the results of 14 studies originating from seven European countries. The analysis steps were similar to the ones above. This dataset was used in Fortney et al. (2015), and it is the most conveniently available aging data set among those analyzed in that paper.

References

- Allen et al. (2008) N. C. Allen, S. Bagade, M. B. McQueen, J. P. Ioannidis, F. K. Kavvoura, M. J. Khoury, R. E. Tanzi, and L. Bertram. Systematic meta-analyses and field synopsis of genetic association studies in schizophrenia: the szgene database. Nature genetics, 40(7):827–834, 2008.

- Andreassen et al. (2013) O. A. Andreassen, S. Djurovic, W. K. Thompson, A. J. Schork, K. S. Kendler, M. C. O’Donovan, D. Rujescu, T. Werge, M. van de Bunt, A. P. Morris, et al. Improved detection of common variants associated with schizophrenia by leveraging pleiotropy with cardiovascular-disease risk factors. The American Journal of Human Genetics, 92(2):197–209, 2013.

- Benjamini and Hochberg (1995) Y. Benjamini and Y. Hochberg. Controlling the false discovery rate: a practical and powerful approach to multiple testing. Journal of the royal statistical society. Series B (Methodological), pages 289–300, 1995.

- Benjamini and Hochberg (1997) Y. Benjamini and Y. Hochberg. Multiple hypotheses testing with weights. Scandinavian Journal of Statistics, 24(3):407–418, 1997.

- Bourgon et al. (2010) R. Bourgon, R. Gentleman, and W. Huber. Independent filtering increases detection power for high-throughput experiments. Proceedings of the National Academy of Sciences, 107(21):9546–9551, 2010.

- Boyd and Vandenberghe (2004) S. Boyd and L. Vandenberghe. Convex Optimization. Cambridge University Press, 2004.

- Bretz et al. (2009) F. Bretz, W. Maurer, W. Brannath, and M. Posch. A graphical approach to sequentially rejective multiple test procedures. Statistics in medicine, 28(4):586–604, 2009.

- Burton et al. (2007) P. R. Burton, D. G. Clayton, L. R. Cardon, N. Craddock, P. Deloukas, A. Duncanson, D. P. Kwiatkowski, M. I. McCarthy, W. H. Ouwehand, N. J. Samani, et al. Genome-wide association study of 14,000 cases of seven common diseases and 3,000 shared controls. Nature, 447(7145):661–678, 2007.

- Coronary Artery Disease Genetics Consortium (2011) Coronary Artery Disease Genetics Consortium. A genome-wide association study in Europeans and South Asians identifies five new loci for coronary artery disease. Nature Genetics, 43(4):339–344, 2011.

- Darnell et al. (2012) G. Darnell, D. Duong, B. Han, and E. Eskin. Incorporating prior information into association studies. Bioinformatics, 28(12):i147–i153, 2012.

- Deelen et al. (2014) J. Deelen, M. Beekman, H.-W. Uh, L. Broer, K. L. Ayers, Q. Tan, Y. Kamatani, A. M. Bennet, R. Tamm, S. Trompet, et al. Genome-wide association meta-analysis of human longevity identifies a novel locus conferring survival beyond 90 years of age. Human Molecular Genetics, 23(16):4420–4432, 2014.

- Dobriban et al. (2015) E. Dobriban, K. Fortney, S. K. Kim, and A. B. Owen. Optimal multiple testing under a Gaussian prior on the effect sizes. Biometrika, 102(4):753–766, 2015.

- Efron (2012) B. Efron. Large-scale inference: empirical Bayes methods for estimation, testing, and prediction, volume 1. Cambridge University Press, 2012.

- Eskin (2008) E. Eskin. Increasing power in association studies by using linkage disequilibrium structure and molecular function as prior information. Genome Research, 18(4):653–660, 2008.

- Fortney et al. (2015) K. Fortney, E. Dobriban, P. Garagnani, C. Pirazzini, D. Monti, D. Mari, G. Atzmon, N. Barzilai, C. Franceschi, A. B. Owen, and S. K. Kim. Genome-wide scan informed by age-related disease identifies loci for exceptional human longevity. PLoS Genet, 11(12):e1005728, 2015.

- Genovese et al. (2006) C. R. Genovese, K. Roeder, and L. Wasserman. False discovery control with p-value weighting. Biometrika, 93(3):509–524, 2006.

- Gui et al. (2012) J. Gui, T. D. Tosteson, and M. E. Borsuk. Weighted multiple testing procedures for genomic studies. BioData Mining, 5(4), 2012.

- Holm (1979) S. Holm. A simple sequentially rejective multiple test procedure. Scandinavian Journal of Statistics, 6(2):65–70, 1979.

- Ignatiadis et al. (2015) N. Ignatiadis, B. Klaus, J. Zaugg, and W. Huber. Data-driven hypothesis weighting increases detection power in big data analytics. bioRxiv, 2015. doi: 10.1101/034330.

- Jager and Leek (2013) L. R. Jager and J. T. Leek. An estimate of the science-wise false discovery rate and application to the top medical literature. Biostatistics, page kxt007, 2013.

- Köttgen et al. (2010) A. Köttgen, C. Pattaro, C. A. Böger, C. Fuchsberger, M. Olden, N. L. Glazer, A. Parsa, X. Gao, Q. Yang, A. V. Smith, et al. New loci associated with kidney function and chronic kidney disease. Nature Genetics, 42(5):376–384, 2010.

- Lehmann and Romano (2005) E. L. Lehmann and J. P. Romano. Testing Statistical Hypotheses. Springer Science & Business Media, 2005.

- Li et al. (2013) L. Li, M. Kabesch, E. Bouzigon, F. Demenais, M. Farrall, M. F. Moffatt, X. Lin, and L. Liang. Using eqtl weights to improve power for genome-wide association studies: a genetic study of childhood asthma. Frontiers in Genetics, 4(103), 2013.

- Nocedal and Wright (2006) J. Nocedal and S. Wright. Numerical Optimization. Springer Science & Business Media, 2006.

- Palleja et al. (2012) A. Palleja, H. Horn, S. Eliasson, and L. J. Jensen. DistiLD Database: diseases and traits in linkage disequilibrium blocks. Nucleic Acids Research, 40(D1):D1036–D1040, 2012.

- Peña et al. (2011) E. A. Peña, J. D. Habiger, and W. Wu. Power-enhanced multiple decision functions controlling family-wise error and false discovery rates. The Annals of Statistics, 39(1):556–583, 2011.

- Rietveld et al. (2014) C. A. Rietveld, T. Esko, G. Davies, T. H. Pers, P. Turley, B. Benyamin, C. F. Chabris, V. Emilsson, A. D. Johnson, J. J. Lee, et al. Common genetic variants associated with cognitive performance identified using the proxy-phenotype method. Proceedings of the National Academy of Sciences, 111(38):13790–13794, 2014.

- Roeder and Wasserman (2009) K. Roeder and L. Wasserman. Genome-wide significance levels and weighted hypothesis testing. Statistical Science, 24(4):398–413, 2009.

- Roeder et al. (2006) K. Roeder, S.-A. Bacanu, L. Wasserman, and B. Devlin. Using linkage genome scans to improve power of association in genome scans. The American Journal of Human Genetics, 78(2):243–252, 2006.

- Roquain and Van De Wiel (2009) E. Roquain and M. A. Van De Wiel. Optimal weighting for false discovery rate control. Electronic Journal of Statistics, 3:678–711, 2009.

- Rubin et al. (2006) D. Rubin, S. Dudoit, and M. Van der Laan. A method to increase the power of multiple testing procedures through sample splitting. Statistical Applications in Genetics and Molecular Biology, 5(1):1–19, 2006.

- Saccone et al. (2007) S. F. Saccone, A. L. Hinrichs, N. L. Saccone, G. A. Chase, K. Konvicka, P. A. Madden, N. Breslau, E. O. Johnson, D. Hatsukami, O. Pomerleau, et al. Cholinergic nicotinic receptor genes implicated in a nicotine dependence association study targeting 348 candidate genes with 3713 snps. Human Molecular Genetics, 16(1):36–49, 2007.

- Schizophrenia Psychiatric Genome-Wide Association Study Consortium (2011) Schizophrenia Psychiatric Genome-Wide Association Study Consortium. Genome-wide association study identifies five new schizophrenia loci. Nature Genetics, 43(10):969–976, 2011.

- Schunkert et al. (2011) H. Schunkert, I. R. König, S. Kathiresan, M. P. Reilly, T. L. Assimes, H. Holm, M. Preuss, A. F. Stewart, M. Barbalic, C. Gieger, et al. Large-scale association analysis identifies 13 new susceptibility loci for coronary artery disease. Nature Genetics, 43(4):333–338, 2011.

- Silverberg et al. (2004) D. Silverberg, D. Wexler, M. Blum, D. Schwartz, and A. Iaina. The association between congestive heart failure and chronic renal disease. Current Opinion in Nephrology and Hypertension, 13(2):163–170, 2004.

- Spjøtvoll (1972) E. Spjøtvoll. On the optimality of some multiple comparison procedures. The Annals of Mathematical Statistics, 43(2):398–411, 1972.

- Storey (2007) J. D. Storey. The optimal discovery procedure: a new approach to simultaneous significance testing. Journal of the Royal Statistical Society: Series B (Statistical Methodology), 69(3):347–368, 2007.

- Sun et al. (2006) L. Sun, R. V. Craiu, A. D. Paterson, and S. B. Bull. Stratified false discovery control for large-scale hypothesis testing with application to genome-wide association studies. Genetic Epidemiology, 30(6):519–530, 2006.

- Sun and Cai (2007) W. Sun and T. T. Cai. Oracle and adaptive compound decision rules for false discovery rate control. Journal of the American Statistical Association, 102(479):901–912, 2007.

- Sveinbjornsson et al. (2016) G. Sveinbjornsson, A. Albrechtsen, F. Zink, S. A. Gudjonsson, A. Oddson, G. Másson, H. Holm, A. Kong, U. Thorsteinsdottir, P. Sulem, et al. Weighting sequence variants based on their annotation increases power of whole-genome association studies. Nature Genetics, 48:314–317, 2016.

- Teslovich et al. (2010) T. M. Teslovich, K. Musunuru, A. V. Smith, A. C. Edmondson, I. M. Stylianou, M. Koseki, J. P. Pirruccello, S. Ripatti, D. I. Chasman, C. J. Willer, et al. Biological, clinical and population relevance of 95 loci for blood lipids. Nature, 466(7307):707–713, 2010.

- Tusher et al. (2001) V. G. Tusher, R. Tibshirani, and G. Chu. Significance analysis of microarrays applied to the ionizing radiation response. Proceedings of the National Academy of Sciences, 98(9):5116–5121, 2001.

- Westfall and Krishen (2001) P. H. Westfall and A. Krishen. Optimally weighted, fixed sequence and gatekeeper multiple testing procedures. Journal of Statistical Planning and Inference, 99(1):25–40, 2001.

- Westfall et al. (1998) P. H. Westfall, A. Krishen, and S. S. Young. Using prior information to allocate significance levels for multiple endpoints. Statistics in Medicine, 17(18):2107–2119, 1998.

- Westfall et al. (2004) P. H. Westfall, S. Kropf, and L. Finos. Weighted FWE-controlling methods in high-dimensional situations. In Recent Developments in Multiple Comparison Procedures, pages 143–154. Institute of Mathematical Statistics, 2004.