First results on applying a non-linear effect formalism to

alliances between political parties and buy and sell dynamics

F. Bagarello

Dipartimento di Energia, Ingegneria dell’Informazione e Modelli Matematici,

Scuola Politecnica Ingegneria, Università di Palermo,

I-90128 Palermo, Italy

and I.N.F.N., Sezione di Torino

e-mail: fabio.bagarello@unipa.it

home page: www.unipa.it/fabio.bagarello

E. Haven

School of Management; Institute of Finance and IQSCS

University of Leicester, LE1 7RH Leicester, UK

e-mail: eh76@leicester.ac.uk

Abstract

We discuss a non linear extension of a model of alliances in

politics, recently proposed by one of us. The model is constructed in terms

of operators, describing the interest of three parties to form, or

not, some political alliance with the other parties. The time evolution of

what we call the decision functions is deduced by introducing a

suitable hamiltonian, which describes the main effects of the interactions

of the parties amongst themselves and with their environments,

which are generated by their electors and by people who still have

no clear idea for which party to vote (or even if to vote). The

hamiltonian contains some non-linear effects, which takes into account the

role of a party in the decision process of the other two parties.

Moreover, we show how the same hamiltonian can also be used to

construct a formal structure which can describe the dynamics of buying and

selling financial assets (without however implying a specific price setting

mechanism).

I Introduction

In a recent paper, [1], a model of interaction between political

parties has been proposed. The model describes a decision making

procedure, deducing the time evolution of three so-called decision

functions (DFs), one for each party considered in our system.

These functions describe the interest of each party to form or not an

alliance with some other party. Their decisions are driven by the

interaction of each party with the other parties, with their own electors,

and with a set of undecided voters (i.e. people who have not yet decided to

vote for which party (if at all they decide to vote)). The approach

adopted in [1] uses an operatorial framework (see also [2]), in which the DFs are suitable mean values of certain number

operators associated to the parties. The dynamics are driven by a

suitable hamiltonian which implements the various interactions between the

different actors of the system.

The limitation of the model, as described in [1], is that the

hamiltonian is quadratic and, as a consequence, the equations of motion are

linear. This simplifies quite a bit the analysis of the time evolution of

the system. In fact an exact solution can be deduced in that case,

but the price we pay is that the model is not entirely realistic, since the

hamiltonian does not include contributions which might be relevant in a

concrete situation. In this paper we introduce several non-linear

contributions in the model, and we solve, adopting a suitable

approximation, the related non-linear differential equations. These

non-linear terms are needed to introduce in the model some sort of three-body interactions, which were not included in [1]. The reason

why these terms are interesting is because they describe (please see below

for more details) the role of, say, the first party (), in

the explicit strength of the interaction between the other two parties, and . This is important, since it is

natural to assume that the DFs of both and also depend on what is doing.

It is important to notice that not many contributions exist in the

mathematical and physics literature on politics, and only very few of them adopt a quantum mechanical (or operator) point of view, as

the one used in [1]. We refer to [3, 4, 5, 6] for some recent and not so recent

contributions on this topic.

After a long discussion on politics, we also show how the same hamiltonian

can be used, with just some minor changes, to deduce the dynamics of a

buy-and-sell financial system.

The paper is organized as follows: in the next section we introduce the

model, we derive the differential equations and we propose an approximation

scheme to solve them. In Section III we show how to model a simple financial system using the same general settings. Section IV contains our

conclusions. To keep the paper self-contained, and to make it also more readable to those who are not familiar with quantum mechanics, we have

added an appendix where a few crucial aspects of operators and quantum

dynamics are reviewed.

II Modelling alliances in politics and its dynamics

In this section we discuss the details of our model and we will

first construct the vectors describing the players and the hamiltonian of

the system. We then deduce the differential equations of motion. To

keep the paper self contained, we recall first a few important

facts which were already discussed in [1].

In our system we have three parties, ,

and , which, together, form the system . Each party has to make a choice, and it can choose only ‘one’

or ‘zero’, which corresponds respectively to either form a coalition or not. This is, in fact, the only aspect of the parties

we are interested in. Hence, we have eight different possibilities, to which we associate eight different and mutually orthogonal vectors in an eight-dimensional Hilbert space .

These vectors are , with . As an

example, the first vector, , describes the fact that, at , no party wants to ally with the other parties. Of course, this

attitude can change during the time evolution. What is interesting

to know is: how does this attitude change? And how can one

describe this change? Let us consider another example. For

instance, , describes the fact that, at , and do not want to form any coalition,

while does. is an orthonormal basis for . A generic vector of , for , is a linear

combination of the form

(2.1)

where we assume in order to

normalize the total probability, [7]. In particular, for instance,

represents the probability that is, at , in a state , i.e. that , and have chosen ‘0’

(no coalition).

As in [1], and for the same reasons (see below), we construct the

vectors in a very special way, starting with the vacuum

of three fermionic operators, , and , i.e. three

operators which, together with their adjoint, satisfy the canonical

anticommutation relation (CAR)

and . Here , for all pairs and .

More in detail, is such that , . The other vectors can be constructed acting on with the operators ,

and :

and so on. Let now be the so-called

number operator of the -th party, which is constructed using and its adjoint, . Since , for , it

is clear that are eigenvectors of these

operators, while their eigenvalues, zero and one, correspond to the only

possible choices admitted for the three parties at . This is, in fact,

the main reason why we have used here the fermionic operators : they

automatically produce only these eigenvalues. Our first effort now consists

in giving a dynamics to the number operators , following

the general scheme proposed in [2]. Hence, we look for an

Hamiltonian which describes the interactions between the various

constituents of the system. Once is given, we can compute first the time

evolution of the number operators as , and we can then ascertain their mean values

on some suitable state describing the system at , in order to get what

we have already called decision functions, (DFs) (please see

below). The rules needed to write down are described in [2], and adopted in [1] where it is also discussed why the

three parties are just part of a larger system which must also include the set of electors. In fact, it is mainly this interaction which

creates the final decision. Hence, must be open, and we mean with this that there must exist some

large environment, , which interacts

with , and , and

it produces some sort of feedback used by to decide.

Fermionic operators (depending also on a continuous index) are also used to

describe their environment, [1].

The various elements of our model are described in Figure 1,

where the various arrows show all the admissible interactions.

Figure 1: The system and its multi-component reservoir.

In this figure represents the set of the electors of , while is the set of all the undecided

voters. Figure 1 shows, for instance, that

can interact with and , but neither with nor with . We also

see that interacts with both and . To define the hamiltonian which describes, in our

framework, the scheme in Figure 1, we start introducing the

following purely quadratic operator, which is, essentially, the one adopted

in [1]:

(2.2)

Here , , ,

and are real quantities, while and are real-valued functions. Their meaning is explained in detail

in [1]. As already anticipated, the following CAR’s for the

operators of the reservoir are assumed:

(2.3)

as well as

(2.4)

Moreover each anti-commutes with each

and with : for all , and for all , and we further assume that . Here

stands for or .

The full hamiltonian is now obtained by adding to another term, , which contains some non quadratic terms:

(2.5)

where, again, , , and are real quantities. Let us now explain the various terms

in .

The first contribution in (2.2) is , which describes the free

evolution of the operators of , where . If, in particular,

all the interaction parameters , and are zero, then . Hence, since in

this case , the number operators describing the choices

of the three parties (and their related DFs) stay constant in time. In other

words, in the absence of interactions, the original choice of each is not affected by the time evolution. Translating this in

the Schrödinger representation, this means that if is in an eigenstate of ,

then it remains in the same state also for . However, we should also

add that if is in the state in (2.1), we might have non trivial dynamics already at this level. As discussed in

[1], describes the interaction between the three parties

and their related groups of electors: describes

the fact that, when some sort of global reaction against alliance

(GRAA) increases, then tends to chose ‘0’ (no coalition).

On the other hand, describes the fact that looks for some coalition when the GRAA of its

electors decreases. This is because of the raising and lowering operators and in these interaction terms, coupled

respectively with the lowering () and raising () operators of the electors of . A similar interpretation

holds for , with the difference that the interaction is now between

the parties and a single set of undecided voters. The last contribution in , , is introduced to describe the fact that the parties also attempt to talk to each other to get some agreement. Two

possibilities are allowed; i) the parties act cooperatively

(they make the same choice, and we have terms like ), and; ii) they make opposite choices. For

instance tries to form some alliance, while excludes this possibility (and we have terms like ). Of course, the relative magnitude of and decides which is the leading contribution

in . It is important to stress that all the terms in

are quadratic, so that the contributions they produce in the differential

Heisenberg equations turn out to be linear. This is the reason why it was

possible, in [1], to produce an analytical solution for the time

evolution of the system. However, the extra terms in (2.5) make, in

our opinion, the situation more interesting from the point of view of the

real interpretation. In fact, whilst in the will of to form or not an alliance with is

totally independent of what is doing, this is not so when

we also consider . For instance, let us consider the

interaction between and , and in

particular let us focus on the exchange term, which we now

rewrite as follows:

The meaning of the two contributions is now evident: the first term, i.e.

the one proportional to in the RHS, describes the fact

that the more is willing to ally with or

, the more these two parties tend to behave differently:

one is pleased with ’s attentions, the other is not.

The other term, the one proportional to , describes a

speculative behavior. and tend

to behave differently when the interest of to form a

coalition is low. In other words, what decides the relative strength of the interaction is not (only)

the relative value of and , but also, and

more interestingly, the attitude of to form (or not) a

coalition. The behavior of and is

related also to what is doing. Of course, a similar

analysis can be repeated for the other terms in , while for

what concerns the presence of or

introduces, again, different weights in the various terms of the

hamiltonian. However, the other two parties now tend to

behave in the same way. For instance, rewriting

we see that when wants to form some coalition, then both and react in the same way. They both try

to form (or not to form) a coalition, with , or between

themselves. Moreover, we are also considering the possibility in which the

strength of the interaction is proportional to rather than to

. Of course, we stress again that other than the value of ,

what is also crucial in deciding the strength of the various terms in , are the numerical values of the parameters and .

We are now ready to continue with the analysis of the dynamics of the

system. The Heisenberg equations of motion , [2], can be deduced by using the CAR (2.3) and (2.4) above.

The result can be written as follows:

(2.6)

where we have introduced the following quantities:

(2.7)

which are all linear in their entries, and these other functions, which are

not linear:

(2.8)

The last two equations in (2.6) can be rewritten as

and

which, assuming that and , , produce

(2.9)

and

(2.10)

Now, long but straightforward computations, allow us to rewrite and

is a simpler form. In particular we find

(2.11)

and

(2.12)

Here we have introduced the following simplifying notation:

for , as well as the operator-valued functions:

where

Remark:– We notice that these equations return those in [1]

when we put to zero all the coefficients measuring the non-linearity.

Therefore, in this case, they can be explicitly solved.

Once we have deduced , we need to compute the DFs ,

which are defined as follows:

(2.13)

. Here is a state over the full

system. These states, [2], are taken to be suitable tensor

products of vector states for and states on the

reservoir which obey some standard rules (please see below). More

in detail, for each operator of the form , being an operator of and

an operator of the reservoir, we put

(2.14)

Here is one of the vectors introduced at the

beginning of this section, and each represents, as discussed before,

the tendency of to form (or not) some coalition at .

Moreover, is a state on satisfying

the following standard properties, [2]:

(2.15)

as well as

(2.16)

for some suitable functions and , which we take here to be

constant in : and . Also, we assume , for all and . The reason why we use the state in (2.14) is because it

describes, in our framework, the fact that, at , ’s

decision is , while the overall feeling of the voters is , and that of the undecided ones is . Of course, these might

appear as oversimplifying assumptions, but they still produce in

many concrete applications, rather interesting dynamics for the model.

II.1 The solution

To begin with, we consider now a simple but still non-trivial

situation, which allows us to write the differential equations of the system

in a reasonably simple way and to find an approximate solution. This

suggests a strategy which can be easily generalized to other situations.

This is, in fact, what we will do in the last part of this section.

Let us assume for the moment that the coefficients in are such

while , and for

simplicity we call this difference : .

This makes the system non-linear, but not extremely complicated (at least

not from the point of view of the notation). The first three

equations of system (2.6), together with their adjoints, can be

rewritten as

(2.17)

where we have introduced the following vectors:

as well as the matrix

Solving exactly equation (2.17) is quite hard, if not impossible, due to

the non-linearity included in . However, it is easy to set

up a recursive approximation approach which might converge to, or at least

approximate, the solution. The idea is simple, and it works better

under the assumption that is sufficiently small. In this case we

replace (2.17) with the following, much simpler, equation: , which is linear and can be easily solved. The

solution is

where we have introduced, for reasons which will be clear in a moment, . We can now use this zero-th order approximation

of in , in equation (2.17), which becomes , where . Notice that is now a known function. The

solution of this equation is

Of course, we can iterate the procedure, and the -th approximation is

(2.18)

where , for .

Hence, at least in principle, we can reach the level of approximation we

want. However, we should also say that it is not guaranteed that the

sequence really converges to the solution of (2.17), even

if this might appear rather reasonable. Similar problems often occur when

non-linear differential equations are considered, as it happens in our

system. Summarizing, we cannot, a priori, say that (i) exists (in some suitable topology), and (ii) even if it

exists, if this limit is the solution of equation (2.17). Nevertheless,

what we can safely say, is that is a certain approximation of , and we suspect that this approximation is sufficiently good for small

and , and for large . Of course, more could be said only after

numerical computations or looking for some a priori estimates. This is indeed part of our

work in progress.

However, there is a situation in which the computations can be carried out explicitly. In fact, if for all , then, as already

observed, the equations reduce to those for the linear system111Incidentally we observe that this does not imply that all the parameters of are zero. It only means that they coincide in pairs.. Hence, they are exactly solvable and the

result has been discussed in [1]. Looking at the analytical form of in (2.5), this can be understood since it corresponds to the fact that, for instance, and react with the same strength to the will of to

either create or not an alliance.

In the next section we will briefly show that we can consider cases other than the one considered above. In fact, a general solution can also be found even when the parameters in are different from each other.

II.2 A more general situation

It is clear that when we give up the working assumptions we have considered

above (i.e. ), the explicit form of the non-linear term changes. This is due to the presence of several parameters and not of just one. Consequently, it is convenient to modify the

strategy and this can be done as follows: the starting point is the equation

where is

the strong non-linear contribution which extends the term in (2.17). Introducing now , and , the equation for becomes

which can be still be re-written in a more convenient form by introducing further the , and the new unknown . In fact, calling now , we get a very simple differential equation,

whose formal solution is

(2.19)

being an integration constant. Of course, this solution is formal because of several reasons: firstly, we don’t know a priori if exists. Secondly, we are not sure we can compute its integral. Thirdly, we are working with operators (and not with simple functions). This makes the situation even more complicated. However, in principle, formula (2.19) produces the solution of the general problem, without any approximation. Hence, from a certain point of view, it looks much more interesting than the solution deduced in the previous section. We will devote a future analysis to a deeper, and more explicit, analysis of the results arising from equation (2.19).

III Dynamics of buying and selling

We have already remarked in several papers (please see in

particular [8, 9] for recent results) that the above

extended hamiltonian framework could be applied to economics and

finance. We show now that this is true and in so doing we change the interpretation of the model considered here. In particular,

we will now discuss that the resulting framework becomes akin to a formal

structure which can describe the dynamics of buying and selling (of

financial assets for instance). However, the framework does not explicitly

provide for a mechanism by which prices can be generated. We note first that

when considering the different terms which are part of , we

can in effect make an argument that the hamiltonians , , are associated with public information which occurs at a macroscale,

since they are connected with some reservoirs which describe in fact (please see below), large groups of people. As is reported in [10], the reaction of traders on this public information is then

transferred onto smaller scales, i.e. to traders themselves. The scale at

which this happens is cast by the hamiltonians and .

The above framework, we insist, hints back to the binary choice of

either buying and selling. The key reason for that is that the eigenvalues

of the number operators are either ‘’ or ‘’. The financial system

which we want to emulate with must contain interactions and

hence we can not be satisfied with just using . This interaction in

the framework proposed here can be either at the macroscale and/or the

microscale (i.e. between the traders). The division of two grand types of

information, i.e. public and private information occurs typically (and

intuitively) at respectively the macroscale and the microscale. One can of

course be rigorous about this. Work by [11] for instance

shows that private information has no effect at all on traders when they

behave in a rational expectations model.

To make sure we use some reference framework from the economics literature

on how to properly define public versus private information, we resort to

[12] who define public information as having the

potential to be known by everyone, whilst private information may be known

by one single individual. In our situation, the decision functions

describe the will of the three traders222Of course, we are sticking here to just three traders because of our

previous application to political alliances, but it is not difficult to

extend the model to more traders., , and

, to buy (zero) or to sell (one) some assets. This choice

is driven by public information (i.e. by and , see below) and by private information (i.e. by the mutual

interaction between the traders).

On the basis of public information, traders can adjust their portfolio

holdings and this, as [12] indicates, can affect prices in the

market. The opposite may well be true in the case of private information,

where a single party profits but with no necessary effect on price

behavior. What is interesting is the statement by [12] that almost

always (see p. 224), will there be processes operating which will

‘publicize’ private information. Please consider again ,

which was mentioned in the context of the politics example above. Assume we

have three traders who have the binary elemental task of either selling or

buying. Denote as the hamiltonian which describes the

dynamics of buying and selling over time, under the influence of both

private and public information. Besides the no-interaction hamiltonian, , the dynamic drivers which are associated to public information are,

as stated, and . From an economics point of view, the

baths , and now signify

a vast collection of informed traders with which our three traders

interact with (in view of performing the elemental task of buying and

selling). Whilst the bath consists of a vast collection

of traders, who can be interpreted as noise traders. This can be

easily achieved in our model by assuming some randomness of the in (2.2). A question arises whether we can be rigorous in

defining those two types of traders. In [13] noise traders are

defined as traders who act upon information which is more often than not,

spurious information. Informed traders have at their command information

which can be objectively used in decisions involving buying or selling.

The contribution of in (i.e. the full driver of the

dynamics of buying and selling) describes the interaction between the three

traders and the baths of informed traders. Clearly, we want to point out

that this interaction is occurring via the medium of public information,

given the size of the baths. The mechanism that

describes now leads to (say) the action of selling by traders given that some public information (from informed traders) has been released that

‘selling’ is what one should do. In identical fashion do we argue for a

buying signal when occurs. But note also the

contribution of , which now influences traders to sell or buy given

public information coming from noise traders. Both those buying and selling

signals, whether they either derive from the interaction with the baths , and or the bath, have the potential to ultimately influence price setting given

that public information is at stake.

What is contained in and are

communications between traders, without recourse to the public information

baths. We have three traders, and by virtue of this very small size, it is

perfectly intuitive to call the information, upon which traders make

decisions within this interaction setting, to be private information. But as

has been remarked above, whilst in the

individual’s traders decision of buying and selling does not affect their

‘partner’ traders, there is a very explicit dependence between the

individual’s traders built in when considering . However, private

information as such is not expected to influence price behavior. Private

information, as we have remarked above, seems to be subject to the act of

‘publicizing’ private information. Well known notions like information

leakage and uncertainty creation can be following from such an act. See [12] and [14] for a discussion. In [14] (see also

[13]), information leakage is defined as “situations where agents wish to reveal truthfully their private possessed

information to others”. Such type of release of

information invites in cooperation amongst agents and it also very clearly

creates an interdependence between agents. Information leakage can be

selective, i.e. agent 1 can release information only to agent 2 and thereby

alienate agent 3. Similarly, in the case of so called ‘uncertainty

creation’, information is created which is on purpose false or erroneous, so

as to induce other agents in error so it can serve one’s own investment

strategy. This is again an example of private information which, on purpose,

creates dependencies between traders. One can even get more precise by

considering the quality of the private information. Trader 1 can release

private information with noise to trader 2 but without any noise to trader

3. See [15] (p. 71). One can even be more refined and

introduce so called knowledge operators in the modeling of information. See

again [15] (p. 4-). Of course, these several different effects

all suggest the relevance of the full hamiltonian in (2.5), and

importance is given to its various contributions also in this

economics context. Incidentally, this means that the differential equations

governing this particular application are again (2.6), so that

the same approximation procedure discussed in Section II.1 can be

adopted. Needless to say, that for this particular application, our next

step will surely be to produce numerical solutions and/or analytical

estimates. This is, for the present model, a hard task. However, it can be

easily done in the linear case, simply by adapting what we have

done in [1] to the present situation. Before doing that, we would

like to mention that this analogy presented here in this section does query

however, how departures from equilibrium can be caused by

and if we align those hamiltonians with the existence of private

information. As such buying and selling ensuing from private information is

unlikely to affect price behavior. Hence, this is unlikely to affect the

equilibrium price obtained out of public information-based buying and

selling.

III.1 Back to the linear case

In this section we see what happens when , i.e. when for all

and . In this case, , which is quadratic in creation and

annihilation operators, and the differential equations (2.17) become

linear. Essentially, we go back to what we have done, in a political

context, in [1]. In fact the numerical plots are completely

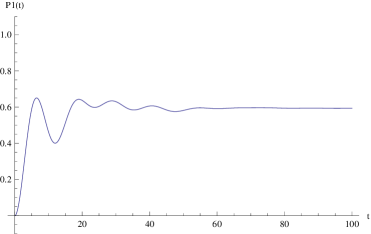

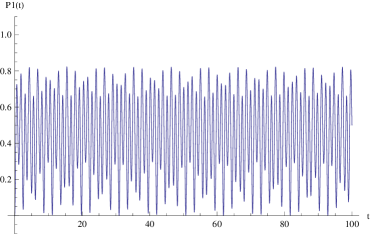

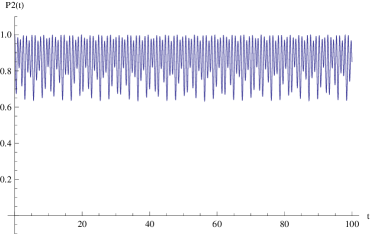

analogous. For instance, Figures 2 and 3 show the three

DFs for two different choices of the parameters of the hamiltonian and for

certain initial conditions (please see the figure’s

caption). These two sets of parameters correspond to two different

situations. In the first situation, Figure 2, each trader

interacts with its related , but not with . They also interact amongst them, but only adopt the mutual different

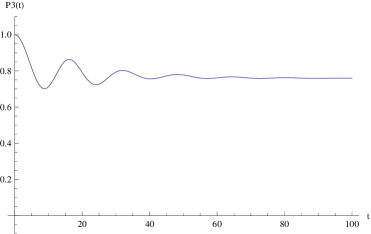

mechanism described by terms like in (2.2). In the second situation, Figure 3,

we describe a similar situation but with the difference that the only

possible interaction between the traders is of the cooperative

type: only terms like survive.

Figure 2: (top left), (top right)

and (bottom) for , , , , , , , , , , , , and , , , .

Figure 3: (top left), (top right)

and (bottom) for , , , , , , , , , , , , and , , .

From both figures we see that, with these choices of parameters and initial

conditions, the three DFs begin oscillating and then reach some asymptotic

value, which is not just zero or one. In [1] we have discussed why

this is so, and when a sharp result can be really deduced. The conclusion,

here, is that it is quite unlikely that the traders reach some decision they

are completely satisfied with. However, see for instance

and in Figure 3, the asymptotic values of both

these DFs are close to one. Hence, we see that the decision process

produces a sort of unique decision. On the other hand, is not really sure of what he has to do, since for large

approaches 0.4, which is not so close to zero.

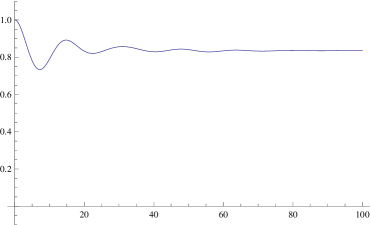

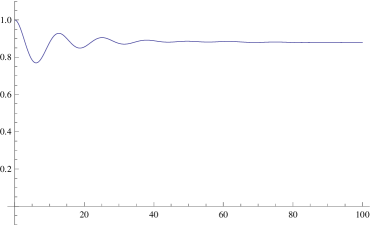

A different story is described by Figure 4, where we are assuming

that the traders only interact among themselves and not with any or with . When this happens it is clear

that none of the traders is able to reach a final decision on whether to buy

or sell the asset. They just oscillate between different feelings,

but a conclusion can only be reached when the traders also have some input

from the larger sets of informed and noise traders.

Figure 4: (top left), (top right)

and (bottom) for , , , , , , , , , , and , , , .

IV Conclusions

In this paper we have shown how to use operatorial techniques, and an

Heisenberg-like dynamics, to describe two different, but somehow related,

decision making processes. One such process is related to political

alliances and the other process relates to buy and sell phenomena.

A non-linear model which extends the model proposed in [1], has been introduced and an approximate procedure for the solution of the

related equations of motion has also been proposed. We postpone to a second

part of the paper the explicit analysis of these solutions, and a detailed

analysis of the role of the parameters of the model. We claim that, for

small values of the parameters governing the non-linearity, and for time

intervals sufficiently small, these solutions do not differ significantly

from those deduced in [1]. It is of course of interest to check what

happens for longer intervals, and this will form part of a forthcoming project. Also, it can be interesting to extend the system

described in Figure 1 adding more arrows. In particular, a

natural extension of the model discussed in Section II can be

constructed by admitting that, for instance, also

interacts with and (i.e. to try to

convince them to change their intentions of vote).

Acknowledgements

This work was partially supported by the University of Palermo and by

G.N.F.M. The authors thank Prof. Andrei Khrennikov for many useful

discussions. F.B. acknowledges the warm hospitality of the IQSCS institute

at the University of Leicester.

Appendix: A few results on the number representation

To keep the paper self-contained, we discuss here a few important

facts in quantum mechanics and in the so–called number representation.

Let be a Hilbert space, and the set of all

the (bounded) operators on . Let be our physical

system, and the set of all the operators useful for a

complete description of , which includes the observables

of . For simplicity, it is convenient (but not really

necessary) to assume that coincides with

itself. The description of the time evolution of is related to

a self–adjoint operator which is called the hamiltonian of , and which in standard quantum mechanics

represents the energy of . In this paper, we have adopted the

so–called Heisenberg representation, in which the time evolution of

an observable is given by

(A.1)

or, equivalently, by the solution of the differential equation

(A.2)

where is the commutator between and . The time

evolution defined in this way is a one–parameter group of automorphisms of .

An operator is a constant of motion if it

commutes with . Indeed, in this case, equation (A.2) implies that , so that for all .

In some previous applications, [2], a special role was played by

the so–called canonical commutation relations. Here, these are

replaced by the so–called canonical anti–commutation relations

(CAR): we say that a set of operators satisfy the CAR if the conditions

(A.3)

hold true for all . Here, is the identity

operator and is the anticommutator of and .

These operators, which are widely analyzed in any quantum mechanics textbook (see, for instance, [16, 17]) are those which are used to

describe different modes of fermions. From these operators we can

construct and , which are both self–adjoint. In

particular, is the number operator for the –th mode, while is the number operator of .

Compared with bosonic operators, the operators introduced here satisfy a

very important feature: if we try to square them (or to rise to higher

powers), we simply get zero: for instance, from (A.3), we have . This is related to the fact that fermions satisfy the Fermi

exclusion principle [17].

The Hilbert space of our system is constructed as follows: we introduce the

vacuum of the theory, that is a vector which

is annihilated by all the operators :

for all . Such a non zero vector surely exists. Then we

act on with the operators (but not

with higher powers, since these powers are simply zero!):

(A.4)

for all . These vectors form an orthonormal set and are

eigenstates of both and : and where . Moreover, using the CAR, we deduce that

and

for all . Then and are called the annihilation and the creation operators. Notice that, in some sense,

is also an annihilation operator since, acting on

a state with , we destroy that state.

The Hilbert space is obtained by taking the linear span of all

these vectors. Of course, has a finite dimension. In

particular, for just one mode of fermions, . This also

implies that, contrarily to what happens for bosons, all the fermionic

operators are bounded.

The vector in (A.4) defines a vector (or number) state over the algebra as

(A.5)

where is the scalar product in . As we

have discussed in [2], these states are useful to project

from quantum to classical dynamics and to fix the initial conditions of the

considered system.

References

[1] F. Bagarello, An operator view on alliances in politics, SIAM Journal on Applied Mathematics (SIAP), 75, (2), 564–584

(2015)

[2] F. Bagarello, Quantum dynamics for classical

systems: with applications of the Number operator, Wiley Ed., New York,

(2012)

[3] O. A. Davis, M. J. Hinich, P. Ordeshook, An Expository

Development of a Mathematical Model of the Electoral Process, The American

Political Science Review, 64, No. 2, 426-448 (1970)

[4] P. Khrennikova, E. Haven, A. Khrennikov, An

application of the theory of open quantum systems to model the dynamics of

party governance in the US Political System, International Journal of

Theoretical Physics, 53, No. 4, 1346-1360 (2014)

[5] S. Galam, Majority Rule, Hierarchical Structures, and

Democratic Totalitarianism: A Statistical Approach, Journal of Mathematical

Psychology, 30, 426-434 (1986)

[6] S. Galam, The Drastic Outcomes from Voting Alliances

in Three-Party Democratic Voting (19902013), Journal of

Statistical Physics, 151, 46-68 (2013)

[7] M. Asano, M. Ohya, Y. Tanaka, I. Basieva, A. Khrennikov,

Quantum-like model of brain’s functioning: decision making from

decoherence, Journal of Theoretical Biology, 281, 56-64 (2011)

[8] F. Bagarello, E. Haven, The role of information in a

two-traders market, Physica A, 404, 224–233, (2014)

[9] F. Bagarello, E. Haven, Towards a formalization of a

two traders market with information exchange, Physica Scripta, 90,

015203 (2015)

[10] R. Mantegna, E. Stanley, An introduction to

econophysics, Cambridge University Press, (2000)

[11] J. Scheinkman, W. Xiong, Hetergenuous

beliefs, speculation and trading in financial markets, Paris-Princeton

Lectures Lectures on Mathematical Finance. LNM 1847, Springer Verlag (2004)

[12] S. Bikhchandani, J. Hirshleifer, J. Riley, The

analytics of uncertainty and information, Cambridge University Press (2013)

[13] E. Haven, A. Khrennikov, Quantum social science,

Cambridge University Press (2013)

[14] C. Ma, Advanced asset pricing theory, Imperial

College Press (2011)

[15] M. Brunnermeier, Asset pricing under asymmetric

information, Oxford University Press (2001)

[16] E. Merzbacher. Quantum Mechanics, Wiley, New York (1970)

[17] P. Roman, Advanced quantum mechanics, Addison–Wesley, New

York (1965)