On the overlaps between eigenvectors of correlated random matrices

Abstract

We obtain general, exact formulas for the overlaps between the eigenvectors of large correlated random matrices, with additive or multiplicative noise. These results have potential applications in many different contexts, from quantum thermalisation to high dimensional statistics. We find that the overlaps only depend on measurable quantities, and do not require the knowledge of the underlying “true” (noiseless) matrices. We apply our results to the case of empirical correlation matrices, that allow us to estimate reliably the width of the spectrum of the true correlation matrix, even when the latter is very close to the identity. We illustrate our results on the example of stock returns correlations, that clearly reveal a non trivial structure for the bulk eigenvalues. We also apply our results to the problem of matrix denoising in high dimension.

I Introduction

The structure of the eigenvalues and eigenvectors of large random matrices is of primary importance in many different contexts, from quantum mechanics to high dimensional data analysis. Correspondingly, Random Matrix Theory (RMT) has established itself as a major discipline, at the frontier between theoretical physics, mathematics, probability theory, and applied statistics, with a somewhat intimidating corpus of knowledge Akemann et al. (2011). One of the most striking applications of RMT concerns quantum chaos and quantum transport Beenakker (1997), with renewed interest coming from problems of quantum ergodicity (“eigenstate thermalisation”) Deutsch (1991); Ithier and Benaych-Georges (2015), entanglement and dissipation (for recent reviews see Nandkishore and Huse (2015); Eisert et al. (2015)). In the context of signal processing, RMT is of primary importance in the analysis of high dimensional statistics Johnstone (2007); Bouchaud and Potters (2011); Paul and Aue (2014), wireless communication channels Tulino and Verdú (2004); Couillet et al. (2011), etc. Other examples cover the dynamics of complex systems – from random ecologies May (1972) to glasses and spin-glasses Fyodorov (2004).

Whereas the spectral properties of random matrices have been investigated at length, the interest has recently shifted to the statistical properties of their eigenvectors – see e.g. Deutsch (1991); Wilkinson and Walker (1995) and Ledoit and Péché (2011); Allez and Bouchaud (2012); Bourgade et al. (2015); Allez and Bouchaud (2014); Bloemendal et al. (2015); Couillet and Benaych-Georges (2015); Monasson and Villamaina (2015) for more recent papers. In particular, one can ask how the eigenvectors of a sample matrix resemble those of the population (or pure) matrix itself. We recently obtained in Bun et al. (2015) explicit formulas for the overlaps between these pure and noisy eigenvectors for a wide class of random matrices, generalizing results obtained for sample covariance/correlation matrices of Ledoit and Péché (2011) – obtained as where is a Wishart matrix – and for matrices of the form , where is a symmetric Gaussian random matrix Philippe Biane (2003); Allez and Bouchaud (2014); Allez et al. (2014). In the present paper, we want to generalize these results to the overlaps between the eigenvectors of two different realizations of such random matrices, that remain correlated through their common part . For example, imagine one measures the sample correlation matrix of the same process, but on two non-overlapping time intervals, characterized by two independent realizations of the Wishart noises and . How close are the corresponding eigenvectors expected to be? We provide exact, explicit formulas for these overlaps in the high dimensional regime. Precisely, we give a transparent interpretation to our formulas and generalize them to various cases, in particular when the noises are correlated. Perhaps surprisingly, these overlaps can be evaluated from the empirical spectrum of only, i.e. without any prior knowledge of the pure matrix itself. This leads us to propose a statistical test based on these overlaps, that allows one to determine whether two realizations of the random matrix and indeed correspond to the very same underlying “true” matrix either in the multiplicative and additive cases defined above. We shall also revisit the theory of rotational invariant estimators (RIE) James and Stein (1961) that encountered a lot of attentions recently (see Bun et al. (2017); Ledoit and Péché (2011); Bartz (2016); Karoui (2008) to cite a few).

II Theoretical results

II.1. Inversion formula

Throughout the following, we consider symmetric random matrices and denote by the eigenvalues of and by the corresponding eigenvectors. Similarly, we denote by the eigenvalues of and by the associated eigenvectors. Note that we will sometimes index the eigenvectors by their corresponding eigenvalues for convenience. We emphasize that we allow the parameters that describe the randomness of S and to be different. The central object that we focus on in this study are the asymptotic () scaled, mean squared overlaps

| (1) |

that remain in the limit . In the above equation, the expectation can be interpreted either as an average over different realizations of the randomness or, for fixed randomness, as an average over small “slices” of eigenvalues of width , such that the result becomes self-averaging in the large limit. We will study the asymptotic behavior of (1) using the complex function

| (2) |

where . For large random matrices, we expect the eigenvalues and to stick to their classical locations, i.e. smoothly allocated with respect to the quantile of the spectral density. Differently said, the sample eigenvalues become deterministic in the large limit. Hence, we obtain after taking the continuous limit that where the limiting value is given by

| (3) |

with and the spectral density of and . Then, it suffices to compute

to deduce that

| (4) |

We may now invoke Sokhotski-Plemelj identity to obtain the inversion formula

| (5) |

with , its complex conjugate and . This last formula tells us that in the high-dimensional regime, we can study the mean squared overlap (1) through the bi-variate function which is easier to handle using tools from RMT (see below).

II.2. Multiplicative noise

The study of the asymptotic behavior of the function requires to control the resolvent of and entry-wise. It was shown recently that one can approximate these (random) resolvents entry-wise by deterministic equivalent quantities Burda et al. (2004a); Bun et al. (2015); Knowles and Yin (2014). We begin first with the Wishart multiplicative noise that we introduced in the introduction. More precisely, let and where and are two independent Wishart matrices with possibly two different observation ratios and . By independence, we have

| (6) |

where (resp. ) denotes the expectation value over the probability measure (resp. ) associated to (resp. ). Then, we use the deterministic estimate of the resolvent of S which yields for Burda et al. (2004a); Bun et al. (2015); Knowles and Yin (2014):

| (7) |

where we defined

| (8) |

with is the Stieltjes transform of S defined as the limiting value of . The estimate (7) holds as well for by replacing , and with , and . Note that we can deduce the fixed-point equation associated to by taking the normalized trace in (7), this yields for

| (9) |

where is the Stieltjes transform associated to the pure matrix C. Again, the value of is obtained from (9) by replacing with .

By plugging Eq. (8) into Eq. (6), we get

and then, using the identity

| (10) |

we obtain

From this last equation, we deduce

One notices from (9) that the two normalized trace terms in the latter equation are exactly given by and in the large limit. We therefore conclude that in the case of a multiplicative Wishart perturbation, the asymptotic value of (2) reads

| (11) |

which holds for any and . The striking observation in Eq. (11) is that the result does not depend explicitly on the population matrix C that we wish to estimate. This feature is crucial since it indicates that we shall be able to characterize the mean squared overlap (1) in terms of observable variables only.

Now that we have determined the asymptotic value , let us now compute the main quantity of interest, i.e. Eq. (1). To that end, it is convenient to work with the complex function . Indeed, by expressing (11) in terms of the function , we end up with

Defining , one obtains after some elementary computations (see Appendix A for details) the following general result:

| (12) |

where we defined

| (13) | |||||

The final result (12) is invariant under the exchange of with and does not depend on C explicitly, as expected. We will see in the next section that it is a crucial feature in order to establish an observable stability test.

It is easy to show that this formula reproduces the mean squared overlap between a given sample eigenvector and its true value in the limit (see e.g. Ledoit and Péché (2011); Bun et al. (2015)). To prove our claim, let us consider , for which where denotes the corresponding population eigenvalue Anderson (1963). In that specific framework, we have and . Hence, we deduce from (12) that

| (14) |

which is exactly the result of Ledoit and Péché (2011).

Next, we look at the case where we split our datasets in two windows of same size () which is relevant when ones wishes to measure the stability of the eigenvectors associated to the same eigenvalue. For , the eigenvalues and are now distributed according to the same density function so that . Moreover, we infer from (13) that the contribution of in (12) vanishes. The self-overlap limit needs to be handled with care as the formula (12) seems ill-defined when . Nevertheless, if we write with , one has

As a consequence, we conclude by plugging these two expressions into (12) and then setting that the self-overlap is given by

| (15) |

We now explain how we can extend these results to more general multiplicative noise. More specifically, let us consider matrices of the form , where is a random matrix chosen in the Orthogonal group according to the Haar measure and is a given random matrix independent from and (see e.g. Burda et al. (2005); Couillet and Benaych-Georges (2015); Bun et al. (2015) for similar models). The framework investigated above corresponds to the case where is a Wishart matrix. Using the results of Bun et al. (2015), we find for this general model that (11) still holds with where is the so-called Voiculescu’s -transform of the matrix Voiculescu (1991). If , then . However, it seems difficult at this stage to obtain an explicit formula for the mean squared overlap (1) in this general case since the analytic structure of the -transform depends on the choice of .

II.3. Additive noise

All the arguments that we use for the multiplicative noise model can be repeated nearly verbatim for the additive noise. In the case of additive real symmetric Gaussian noise, referred to as the Gaussian Orthogonal Ensemble (GOE) in the literature, we have and with and two independent GOE matrices with variance and . Each entry of the resolvent may also be approximated by a deterministic value in the high-dimensional regime Knowles and Yin (2014); Allez and Bouchaud (2014); Bun et al. (2015):

| (16) |

where we defined 111Here and henceforth, the superscript denotes the additive noise.

| (17) |

Once again, the asymptotic limit (16) holds for by replacing , and by , and . By performing the same computations as above, we obtain for the limiting value of :

| (18) |

As for Eq. (11), Eq. (18) depends only on a priori observable quantities since it does not involve explicitly the unknown population matrix . Consequently, we will obtain an observable expression for (1) using the inversion formula (5).

We can now turn on the computation of the mean squared overlap (1) in the additive Gaussian model. From (18), we find that

where we used the notation . Defining and performing similar algebraic manipulations as above (see Appendix B for details), we eventually get

| (19) |

with given by the same expression as in Eq. (13) with the substitutions and and

| (20) |

We notice that the contribution of the term again vanishes when we suppose that both Gaussian noises have the same variance. As in the multiplicative case, the self-overlap is reached by expanding (19) in power of with . This eventually yields by taking :

| (21) |

Similarly to the multiplicative case, the additive model can be generalized to with the same definitions for and . In that case, the above result (18) holds but now with where is the -transform of the matrix Voiculescu (1991) – which is simply equal to when is a Gaussian random matrix, as considered above.

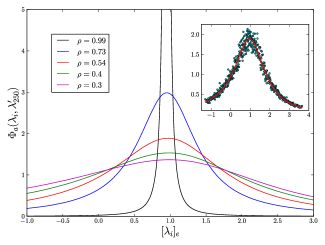

Another interesting and important extension of the result (19) is when the noises , are correlated – while the above calculations referred to independent noises. In the additive case, the trick is to realize that one can always write (in law) and , where , are now independent, as above. Since our formulas do not rely on the common matrix , it can therefore be replaced by . Then, Eq. (21) trivially holds with replaced by with and the width of the noisy matrices and (see Appendix C for more details). Similarly, is replaced by . Note that in the case where the noises parameter are identical, is simply multiplied by . The corresponding shape of for different values of and is shown in Fig. 1. We also provide in the inset a comparison with synthetic data for a fixed , . The empirical average is taken over 200 realizations of the noise and again, the agreement is excellent.

Considering correlated noises in the multiplicative model is of crucial importance since it describes the case of correlation matrices measured on overlapping periods, such that and (see Section III.2 below). This case turns out to be more subtle and is the subject of ongoing investigations.

II.4. Convolution formula

Before investigating some concrete applications of these formulas, let us end this theoretical section with an interesting interpretation of the above formalism. We first introduce the set of eigenvectors of the pure matrix , labeled by the eigenvalue . We define the overlaps between the ’s and the ’s as , where were explicitly computed in Bun et al. (2015) for a wide class of problems, and are random variables of unit variance. Now, one can always decompose the ’s as:

| (22) |

where is the spectral density of . Using the orthonormality of the ’s, one then finds:

If we square this last expression and average over the noise, and make an “ergodic hypothesis” Deutsch (1991) according to which all signs are in fact independent from one another, one finds the following, rather intuitive convolution result for squared overlaps:

| (23) |

It turns out that this expression is completely general and exactly equivalent to Eqs. (12) and (19) in the corresponding cases. However, whereas this expression still contains some explicit dependence on the structure of the pure matrix , it has disappeared in Eqs. (12) and (19). Nevertheless, this second interpretation will be useful in order to obtain an efficient way to estimate C from large noisy matrices.

III Application

Eqs. (12) and (19) are exact in the high-dimensional limit (HDL) and are the main new results of this work. Note that from Ref. Knowles and Yin (2014), we expect these results to hold with fluctuations of order but a more rigorous analysis of the subleading terms can be useful for practical purposes. We leave this question for future works. Throughout this section, we shall focus on the case of sample covariance/correlation matrices but most of the results that will follow can be easily transposed to the additive noise. We emphasize that in the special case of sample correlation matrices, the HDL is defined as

| (24) |

where is the sample size. We will assume throughout this section that the variance of each variable can be estimated independently with great accuracy in the HDL so that we will not distinguish further covariances and correlations henceforth.

The first application concerns a stability test for the eigenvectors of large correlation matrices. More precisely, we investigate whether or not the mean squared overlap between the eigenvectors of two correlation matrices measured with nearby non-overlapping samples is entirely explain by measurement noise. Differently said, we test the hypothesis that the dynamics of the eigenvectors is captured by the sample correlation matrix model. The second application involves the convolution formula. In particular, we link our results with the theory of RIEs that provides significant improvement over classical sample estimates in the HDL (see Bun et al. (2017) for a recent review).

III.1. Eigenvectors stability

The first application deals with the stability of the eigenvectors in the case of two non-overlapping adjacent samples. In order to give more insights, we begin with a theoretical example where the true correlation matrix is an inverse Wishart matrix of parameter , that corresponds to for Wishart matrices (see Bun et al. (2015) for details). In that case, the function can be explicitly computed. This finally leads to:

| (25) |

with and is within the interval , where the edges are given by . An interesting limit corresponds to , where tends to the identity matrix, and the overlaps are expected to become all equal to . Indeed one finds, for a fixed :

| (26) |

which is in fact universal in this limit, provided the eigenvalue spectrum of has a variance given by 222The analysis for the additive case leads to a very similar result. More precisely, taking with a GOE (independent from and ) of variance , one finds that is given by exactly the same formula (26) with the substitution .. This formula is interesting insofar as it allows one to estimate the width of the eigenvalue distribution of , even when it is close to the identity matrix, i.e. . One could think of directly using information on the empirical spectrum, for example the Marčenko-Pastur prediction , that in principle allows one extract the parameter through . However, this second method is numerically unstable and very imprecise when and finite (for one thing, the RHS can be negative, which would lead to a negative variance). Our formula based on overlaps avoid these difficulties. As an illustration, we check the validity of Eq. (25) in Figure 2 with , and . More precisely, we determine the empirical average overlap as follows: we consider 50 independent realization of the Wishart noise . For each pair of samples we compute a smoothed overlap as:

| (27) |

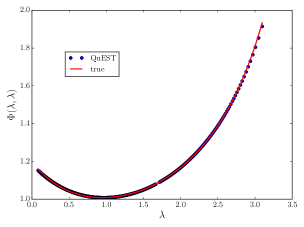

with the normalization constant and the width of the Cauchy kernel, that we choose to be in such a way that . We then average this quantity over all pairs for a given value of to obtain , and plot the resulting quantity as a function of the average eigenvalue position . We observe that the agreement with Eq. (25) is excellent, even when the true underlying matrix is close to the identity matrix. Note that the empirical estimate Eq. (27) is universal, i.e. independent of the underlying structure of C.

For a general and arbitrary population matrix C, evaluating Eq. (12) – or Eq. (19) – is rather difficult because of finite size effects, especially for the multiplicative case. Indeed, when we consider multiplicative noises, the eigenvalues of S are confined to stay positive meaning the presence of a hard wall at the origin 333Note that this problem does not appear in the additive case, so one can safely use concentration results from Knowles and Yin (2014).. Consequently, the use of local laws to estimate the Stieltjes transform , as in Knowles and Yin (2014), often leads to noisy results for very small eigenvalues. Hence, the determination of Eq. (12) from real data is rather difficult and one has to resort to numerical regularization schemes to do so. In the specific case of sample correlation matrix, one possible solution is to invert the celebrated Marčenko-Pastur equation Karoui (2008); Ledoit and Wolf (2016) to infer the eigenvalues of the population matrix C. Once this is done, one can evaluate the Stieltjes transform with high precision even near the origin. In the following, we shall use the so-called QuEST numerical scheme of Ledoit and Wolf (2016) to obtain these pure eigenvalues. We plot in Figure 2 the results obtained when using the estimated population eigenvalues from the QuEST algorithm (blue points) and note that the agreement is quite remarkable.

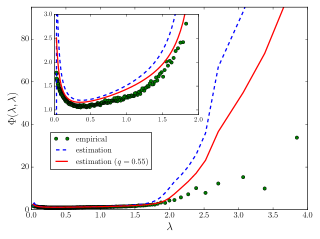

Now that we have an estimate of the population eigenvalues, we can investigate an application to real data. Here, we study the case of US stock market but the results below can be extended to other region Bun et al. (2017). The difficulty when dealing with real data is to measure the empirical mean squared overlaps (27) between two non-overlapping correlation matrices S and as in Eq. (27) because we may not have enough data points to evaluate accurately an average over the noise as required in Eq. (1). To circumvent this problem, we use a Bootstrap procedure to increase the size of the data 444This technique is especially useful in machine learning and we refer the reader to e.g. (Friedman et al., 2001, Section 7.11) for a more detailed explanation.: we take a total period of 2400 business days from 2004 to 2013 for the most liquids assets of the S&P 500 index that we split into two non-overlapping subsets of same size of 1200 days, corresponding to 2004 to 2008 and 2008 to 2013. We restrict to stocks such that all of them are present throughout the whole period from 2004 to 2013. Then, for each subset and each Bootstrap sample , we select randomly distinct days to construct two “independent” sample correlation matrices and , with . We then compute the empirical mean squared overlap (1) and also the theoretical limit (12) – using the QuEST algorithm – from these bootstrap data-sets.

For our simulations, we set and plot in Figure 3 the resulting estimation of Eq. (1) we get from the QuEST algorithm (blue dashed line) and the empirical bootstrap estimate (27) (green points) using US stocks. We also perform the estimation with an effective observation ratio (red plain line) as advocated in Bun et al. (2016) for the S&P 500 index, to account for correlation or heavy tail effects.

It is clear from Figure 3 that the eigenvectors associated to large eigenvalues are not well described by the theory: we notice a discrepancy between the (estimated) theoretical curve and the empirical one even after accounting for an effective ratio . The difference is even worse for the market mode (not shown). This is presumably related to the fact that the largest eigenvectors are expected to genuinely evolve with time, as already argued in Allez and Bouchaud (2012). Note also the gap at the left edge between the theoretical and empirical prediction in the inset of Figure 3 that is partly corrected with . This suggests that one can still improve the Marčenko-Pastur framework by adding e.g. autocorrelation or heavy tailed entries which allows one to widen the LSD of S (see e.g. Burda et al. (2005); Bartz and Müller (2014) for autocorrelation and Biroli et al. (2007); Burda et al. (2004b); El Karoui et al. (2009); Couillet et al. (2015) for heavy tailed entries). Finally, all these remarks hold for other markets as well Bun et al. (2017).

III.2. Rotational invariant estimator

Aside from the statistics of eigenvectors, the theoretical framework presented is actually very useful for the estimation of C from large noisy matrices in the specific class of rotational invariant estimators (see Bun et al. (2017) and references therein for a recent review on this topic). For this class of estimators, the crux is to find an observable way to estimate the oracle eigenvalues

| (28) |

where the are the eigenvectors of , and we omit their dependence on in the RHS of the last equation. There exist several way to approximate this estimator in the HDL: using the anisotropic local law Bun et al. (2017), numerical inversion of Marčenko-Pastur equation Ledoit and Wolf (2016) and the so-called cross-validation (CV) estimator of Bartz (2016). The remarkable feature of all these methods is that the resulting estimator only depends on observable quantities, while it is clearly not the case for (28). Even if the first two techniques are interesting on their own, we will rather focus on the last one as it turns to be related to the convolution formula derived in Section II.4.

From now on, we consider the multiplicative but the following arguments can easily be generalized for the additive case. Let us consider the quantity

| (29) |

where we recall that is independent from . We again assume that we are in the regime (24) and we thus infer from (23) that

| (30) |

The term in the bracket can be simplified by using the very definition of :

and we rewrite this last line thanks to the eigenvalue equation as

with the -th eigenvalue of the white Wishart matrix and the corresponding eigenvector. Finally, we invoke that for all to conclude that in the HDL,

| (31) |

and we therefore have

| (32) |

Plugging this last equation into (III.2), we obtain for any the following result:

| (33) |

where the last equivalence comes from the definition (28) of the oracle estimator in the continuous limit.

This result is very interesting and indicates that one can approximate the oracle estimator (28) by considering the quadratic form between the eigenvectors of a given realization of C – say – and another realization of C – say – even if the latter is characterized by a different value of the quality ratio .

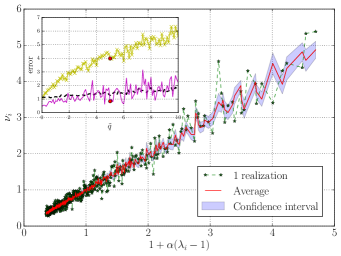

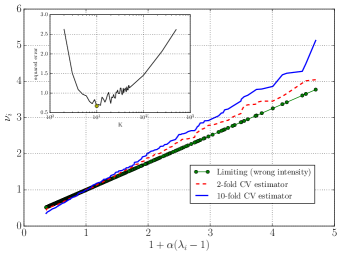

To illustrate this last point, let us consider an Inverse-Wishart matrix with parameter as the population correlation matrix of size . Both noisy matrices are drawn from a multivariate Gaussian distribution but with different parameters: the first noisy matrix S is computed using while the second one corresponds to . With this prior, the oracle estimator is given in the HDL by the linear shrinkage with intensity and . In Figure 4, we plot the prediction obtained from (33) with S fixed and a single realization of (dotted star line) and we see that although noisy, the prediction is already fairly accurate. We also plot in the same figure the average value of (33) over 20 independent realizations of (plain red line) and we observe that the agreement with limiting value (given by the line in Figure 4) is excellent, with only very small fluctuations (see the confidence interval given by the blue shaded area).

Quite surprisingly, we can significantly improve the accuracy of the estimation by applying an ad-hoc regularization even for a single realization of . More specifically, we see from Figure 4 that the prediction (33) does not necessarily preserve the order of the eigenvalues due to the finite size of the sample. However, observing a non-monotonic cleaning scheme may be an unwanted feature within a rotational invariant assumption. Indeed, there is no reason a priori to expect that it is optimal to modify the order of the eigenvalues, that is to say, the variance associated to the principal components.

There are several ways to regularize the estimation obtained from (4). We can either sort the cleaned eigenvalues Bun et al. (2017) or perform an isotonic regression Bartz (2016). We provide an illustration of the sorting regularization in the inset of Figure 4 over a single realization of (purple plain line). The improvement over (33) (yellow crossed-line) in terms of squared error is significant. Moreover, even if the estimation becomes quite noisy for large values of , we notice that the quality of estimation is still on par with the average value over 20 realizations of (black dashed line), which is quite remarkable.We also want to emphasize that in all cases, the error we obtain is always less than 9, which is the error we get when keeping the sample eigenvalues of S (see Inset of Fig. 4).

A takeaway from Figure 4 is that we can indeed use the result (33) even when . Hence, this gives a simple way to check the quality of the estimation by comparing the in-sample result (i.e. the estimator we obtain using the information of S) and the out-of-sample result (obtain with the information of ). It therefore demonstrates the validity of the out-of-sample test of Bun et al. (2017) for assessing the quality of empirical optimal RIE using financial data. The second finding is that it is possible to estimate quite accurately the optimal oracle for a fixed value of by using a relatively small amount of independent data from a single realization.

III.3. Cross-validation estimator

Another interesting discussion is the comparison of the above results with the cross-validation (CV) estimator proposed in Bartz (2016). Suppose that we want to estimate (28) out of independent samples that we split into non-overlapping sets whose indices are denoted by . The CV estimator then reads

| (34) |

where each set has equal size such that , is the eigenvector associated to the -th eigenvalue obtained from the sample correlation matrix in which we removed all the observations belonging to the set for a fixed and is the corresponding observation ratio. If we denote by the sample correlation matrix associated to the observations of the set , then we can rewrite (34) as

| (35) |

which can be thought as an average version of the estimator (33).

The crucial difference resides in the observation ratios associated to the eigenvector and associated to the matrix . Hence, we clearly have a trade-off in the choice of the cardinality of the : choosing too large implies that deviates strongly from while a too small cardinality leads to the noisy limit in which the convergence (33) becomes dubious. We therefore understand from this rewriting why the leave-one-out case, i.e. , will not return a reliable estimate of the optimal value (28) even after averaging since . For a suitable value of the cardinality , one can expect that is small enough in order to be in the regime of Eq. (33) and, more importantly, that is not too far from . In that case, provided that the samples are independent to each other, we shall have

| (36) |

We provide a numerical check of this result in Figure 5 in the case of a sorted 10-fold CV estimate (blue plain line) where we reconsider the same configuration of Figure 4. Note that a -fold CV leads to a “test” set of size meaning that which is not that far from the true value of . We see that the agreement with the optimal value is excellent showing that for this specific choice of , the convergence (36) holds. In order to illustrate the trade-off discussed above, we also plot the -fold CV estimator for which . In that case, the result we obtain from (34) rather coincides with the linear shrinkage with an intensity of . This demonstrates that the choice of in (34) is crucial in order to obtain a consistent estimation of (28) (see the inset of Figure 5).

From a practical viewpoint, the estimator (35) is quite appealing since it can be generalized to more general classes of random processes. It provides a simple tool to approximate the oracle estimator (28) with great accuracy in the high-dimensional regime beyond the sample correlation matrix model. From a theoretical perspective, we see that there is still some work to be done in order to understand the convergence expressed by (36). Indeed, the relationship between and , which corresponds to the overlapping/correlated case discussed above in the additive case, should provide insights to establish the convergence result as a function of the cardinality of . Moreover, the study of subleading terms in Eq. (33) can be of particular interest to understand the phase transition that occurs depending on the value of and .

IV Conclusion

In summary, we have provided general, exact formulas for the overlaps between the eigenvectors of large correlated random matrices, with additive or multiplicative noise. Remarkably, these results do not require the knowledge of the underlying “pure” matrix and have a broad range of applications in different contexts. We showed that the cross-sample eigenvector overlaps provide unprecedented information about the structure of the true eigenvalue spectrum, much beyond that contained in the empirical spectrum itself. For example, the width of the bulk of the spectrum of the true underlying correlation matrix can be reliably estimated, even when the latter is very close to the identity matrix. We have illustrated our results on the example of stock returns correlations, that clearly reveal a non trivial structure for the bulk eigenvalues. We have also discussed about the application to matrix denoising and we saw in particular that it is possible to make use of these overlaps between independent samples to approximate the so-called oracle estimator with great accuracy.

Acknowledgments: We want to thank R. Allez, D. Bartz, R. Bénichou, R. Chicheportiche, B. Collins, A. Rej, E. Sérié and D. Ullmo for very useful discussions.

References

- Akemann et al. (2011) G. Akemann, J. Baik, and P. Di Francesco, The Oxford handbook of random matrix theory (Oxford University Press, 2011).

- Beenakker (1997) C. W. Beenakker, Reviews of modern physics 69, 731 (1997).

- Deutsch (1991) J. M. Deutsch, Physical Review A 43, 2046 (1991).

- Ithier and Benaych-Georges (2015) G. Ithier and F. Benaych-Georges, arXiv preprint arXiv:1510.04352 (2015).

- Nandkishore and Huse (2015) R. Nandkishore and D. A. Huse, Annual Review of Condensed Matter Physics 6, 15 (2015).

- Eisert et al. (2015) J. Eisert, M. Friesdorf, and C. Gogolin, Nature Physics 11, 124 (2015).

- Johnstone (2007) I. M. Johnstone, in Proceedings on the International Congress of Mathematicians I (2007), pp. 307–333.

- Bouchaud and Potters (2011) J.-P. Bouchaud and M. Potters, in The Oxford handbook of Random Matrix Theory (Oxford University Press, 2011).

- Paul and Aue (2014) D. Paul and A. Aue, Journal of Statistical Planning and Inference 150, 1 (2014).

- Tulino and Verdú (2004) A. M. Tulino and S. Verdú, Communications and Information theory 1, 1 (2004).

- Couillet et al. (2011) R. Couillet, M. Debbah, et al., Random matrix methods for wireless communications (Cambridge University Press Cambridge, MA, 2011).

- May (1972) R. M. May, Nature 238, 413 (1972).

- Fyodorov (2004) Y. V. Fyodorov, Physical review letters 92, 240601 (2004).

- Wilkinson and Walker (1995) M. Wilkinson and P. N. Walker, Journal of Physics A: Mathematical and General 28, 6143 (1995).

- Ledoit and Péché (2011) O. Ledoit and S. Péché, Probability Theory and Related Fields 151, 233 (2011).

- Allez and Bouchaud (2012) R. Allez and J.-P. Bouchaud, Physical Review E 86, 046202 (2012).

- Bourgade et al. (2015) P. Bourgade, L. Erdős, H.-T. Yau, and J. Yin, Communications on Pure and Applied Mathematics (2015).

- Allez and Bouchaud (2014) R. Allez and J.-P. Bouchaud, Random Matrices: Theory and Applications 3, 1450010 (2014).

- Bloemendal et al. (2015) A. Bloemendal, A. Knowles, H.-T. Yau, and J. Yin, Probability Theory and Related Fields pp. 1–94 (2015).

- Couillet and Benaych-Georges (2015) R. Couillet and F. Benaych-Georges, arXiv preprint arXiv:1510.03547 (2015).

- Monasson and Villamaina (2015) R. Monasson and D. Villamaina, EPL (Europhysics Letters) 112, 50001 (2015).

- Bun et al. (2015) J. Bun, R. Allez, J.-P. Bouchaud, and M. Potters, arXiv preprint arXiv:1502.06736 (2015).

- Philippe Biane (2003) Philippe Biane, Quantum Probability Communications 11, 55 (2003).

- Allez et al. (2014) R. Allez, J. Bun, and J.-P. Bouchaud, arXiv preprint arXiv:1412.7108 (2014).

- James and Stein (1961) W. James and C. Stein, in Proceedings of the fourth Berkeley symposium on mathematical statistics and probability (1961), vol. 1, pp. 361–379.

- Bun et al. (2017) J. Bun, J.-P. Bouchaud, and M. Potters, Physics Reports 666, 1 (2017).

- Bartz (2016) D. Bartz, arXiv preprint arXiv:1611.00798 (2016).

- Karoui (2008) N. E. Karoui, The Annals of Statistics pp. 2757–2790 (2008).

- Burda et al. (2004a) Z. Burda, A. Görlich, A. Jarosz, and J. Jurkiewicz, Physica A: Statistical Mechanics and its Applications 343, 295 (2004a).

- Knowles and Yin (2014) A. Knowles and J. Yin, arXiv preprint arXiv:1410.3516 (2014).

- Anderson (1963) T. W. Anderson, Annals of Mathematical Statistics pp. 122–148 (1963).

- Burda et al. (2005) Z. Burda, J. Jurkiewicz, and B. Wacław, Physical Review E 71, 026111 (2005).

- Voiculescu (1991) D. Voiculescu, Inventiones mathematicae 104, 201 (1991).

- Ledoit and Wolf (2016) O. Ledoit and M. Wolf, Tech. Rep., Department of Economics-University of Zurich (2016).

- Bun et al. (2016) J. Bun, J.-P. Bouchaud, and M. Potters (2016).

- Bartz and Müller (2014) D. Bartz and K.-R. Müller, in Advances in neural information processing systems (2014), pp. 1592–1600.

- Biroli et al. (2007) G. Biroli, J.-P. Bouchaud, and M. Potters, arXiv preprint arXiv:0710.0802 (2007).

- Burda et al. (2004b) Z. Burda, J. Jurkiewicz, M. A. Nowak, G. Papp, and I. Zahed, Physica A: Statistical Mechanics and its Applications 343, 694 (2004b).

- El Karoui et al. (2009) N. El Karoui et al., The Annals of Applied Probability 19, 2362 (2009).

- Couillet et al. (2015) R. Couillet, F. Pascal, and J. W. Silverstein, Journal of Multivariate Analysis 139, 56 (2015).

- Friedman et al. (2001) J. Friedman, T. Hastie, and R. Tibshirani, The elements of statistical learning, vol. 1 (Springer series in statistics New York, 2001).

Appendix: Supplementary Material

Appendix A Mean squared overlap for independent sample covariance matrices

We keep the notations of Section II.2 and shall often omit the arguments and in and in the following when there is no confusion. Using the definition , we rewrite (11) as

| (37) |

which is equivalent to

| (38) |

We can then express the function as a function of and only:

| (39) |

To use the inversion formula Eq. (5), we need to evaluate . Using the short handed notation , we find

| (40) |

where we omitted the explicit expressions of the imaginary part since this is not important for Eq. (5). Then, using the representation and , one finds

| (41) |

and

| (42) |

Straightforward computations yields

| (43) | |||||

which is exactly the denominator in (12). For the numerator, elementary complex analysis in Eq. (40) yields

| (44) |

and

| (45) |

By regrouping these last three equations with the prefactors in (40), and recalling that and , so we obtain by using the inversion formula (5) the following result:

| (46) |

which is exactly Eq. (12).

Appendix B Mean squared overlap for deformed GOE matrices

The derivation of the overlaps (19) for two independent deformed GOEs is very similar to sample covariance matrices. Hence, we shall omit most details that can be obtained by following the arguments of the above Appendix. Again, we shall skip the arguments and where there is no confusion.

Appendix C The case of correlated Gaussian additive noises

In this section, we give the exact derivation of Eq. (19) with correlated noises. Let

| (51) |

where are two correlated GOE matrices (independent from ) satisfying

| (52) |

where we denoted by the Gaussian measure and used the abbreviation . Using the stability of GOE under addition, let us rewrite the noise terms as

| (53) |

where that satisfies

| (54) |

and and are two GOEs matrices independent from with

| (55) |

One can check that this parametrization yields exactly the correlation structure of Eq. (52). Therefore, using (C) into (51), we have the equivalence (in law)

| (56) |

where we defined

| (57) |

with a GOE matrix with variance . Since the noises are now independent and that the mean squared overlap , given in Eq. (19), is “independent” from the exact structure of , we can therefore replace by . Hence, we deduce that the overlaps for this model will again be given by Eq. (19) with , and , as announced.