Analysis of the nonlinear option pricing model under variable transaction costs

Abstract

In this paper we analyze a nonlinear Black–Scholes model for option pricing under variable transaction costs. The diffusion coefficient of the nonlinear parabolic equation for the price is assumed to be a function of the underlying asset price and the Gamma of the option. We show that the generalizations of the classical Black–Scholes model can be analyzed by means of transformation of the fully nonlinear parabolic equation into a quasilinear parabolic equation for the second derivative of the option price. We show existence of a classical smooth solution and prove useful bounds on the option prices. Furthermore, we construct an effective numerical scheme for approximation of the solution. The solutions are obtained by means of the efficient numerical discretization scheme of the Gamma equation. Several computational examples are presented.

Key words. Black–Scholes equation with nonlinear volatility, quasilinear parabolic equation, variable transaction costs

2000 Mathematical Subject Classifications. 35K15 35K55 90A09 91B28

1 Introduction

The classical linear Black–Scholes option pricing model with a constant historical volatility was proposed in [7]. The model was derived under several restrictive assumptions, such as assumption on market completeness, continuous trading and zero transaction costs. According to this option pricing theory the price of a contingent claim written on the underlying asset at the time is a solution to the linear parabolic equation

| (1) |

where is the risk-free interest rate of a zero-coupon bond and is the historical volatility of the underlying asset which is assumed to follow a stochastic differential equation of the geometric Brownian motion, i.e.

| (2) |

However, practical analysis of market data shows the need for more realistic models taking into account the aforementioned drawbacks of the classical Black–Scholes theory. It stimulated development of various nonlinear option pricing models in which the volatility function is no longer constant, but is a function of the solution itself. We focus on the case where the volatility depends on the second derivative of the option price with respect to the underlying asset price .

| (3) |

where is a function of the product of the asset price and Gamma of the option (Gamma is the second derivative of with respect to ).

Motivation for studying the nonlinear extensions of the classical Black-Scholes equation (3) with a volatility depending on arises from classical option pricing models taking into account non–trivial transaction costs due to buying and selling assets (cf. Leland [26]), market feedbacks effects due to large traders choosing given stock–trading strategies (cf. Frey et al. [12, 13], Schönbucher and Wilmott [30]), risk from a volatile and unprotected portfolio (see Jandačka and Ševčovič [19]) or investors preferences (cf. Barles and Soner [6]).

One of the first nonlinear models taking into account transaction costs is the Leland model [26] for pricing the call and put options. This model was further extended by Hoggard, Whalley and Wilmott [16] for general type of derivatives. Qualitative and numerical properties of this model were analyzed by Grandits and Schachinger [14], Imai et al. [17], Ishimura [18], Grossinho and Morais [15] and others.

In this model the variance is given by

| (4) |

where is the so-called Leland number, is a constant historical volatility, is a constant transaction costs per unit dollar of transaction in the underlying asset market and is the time–lag between consecutive portfolio adjustments. The nonlinear model (3) with the volatility function given as in (4) can be also viewed as a jumping volatility model investigated by Avellaneda and Paras [3].

The important contribution in this direction has been presented in the paper [1] by Amster, Averbuj, Mariani and Rial, where the transaction costs are assumed to be a nonincreasing linear function of the form , (), depending on the volume of trading stock needed to hedge the replicating portfolio. A disadvantage of such a transaction costs function is the fact that it may attain negative values when the amount of transactions exceeds the critical value . In the model studied by Amster et al. [1] (see also Averbuj [4], Mariani et al. [28]) volatility function has the following form:

| (5) |

In [5] Bakstein and Howison investigated a parametrized model for liquidity effects arising from the asset trading. In their model is a quadratic function of the term :

| (6) |

The parameter corresponds to a market depth measure, i.e. it scales the slope of the average transaction price. Next, the parameter models the relative bid–ask spreads and it is related to the Leland number through relation . Finally, transforms the average transaction price into the next quoted price, .

The risk adjusted pricing methodology (RAPM) model takes into account risk from the unprotected portfolio was proposed by Kratka [22]. It was generalized and analyzed by Jandačka and Ševčovič in [19]. In this model the volatility function has the form:

| (7) |

where is a constant historical volatility of the asset price return and , where are non–negative constants representing cost measure and the risk premium measure, respectively.

The structure of the paper is as follows. In the next section we present a nonlinear option pricing model under variable transaction cost. It turns out that the volatility function depends on . In particular case of constant or linearly decreasing transaction costs it is a generalization of the Leland [26] and Amster et al. model [1], respectively. Section 3 is devoted to transformation of the fully nonlinear option pricing equation into a quasilinear Gamma equation. We prove existence of classical Hölder smooth solutions and we derive useful bounds on the solution. In section 4 we propose a numerical scheme for solving the Gamma equation based on finite volume method. We also present several numerical examples of computation of option prices based on a solution to the nonlinear Black–Scholes equation under variable transaction costs.

2 Option pricing model under variable transaction costs

One of the key assumptions of the classical Black–Scholes theory is the possibility of continuous adjustment (or hedging) of the portfolio consisting of options and underlying assets. In the context of transaction costs needed for buying and selling the underlying asset, continuous hedging leads to an infinite number of transactions and the unbounded total transaction costs. The Leland model [26] (see also Hoggard, Whalley and Wilmott [16]) is based on a simple, but very important modification of the Black–Scholes model, which includes transaction costs and possibility of rearranging the portfolio at discrete times. Since the portfolio is maintained at regular intervals, it means that the total transaction costs are limited.

Our derivation of the variable transaction costs option pricing model follows ideas proposed by Leland in [26]. Therefore we recall crucial steps of derivation of Leland’s approach for modeling transaction costs. We assume that the cost per one transaction is constant, i.e. it does not depend on the volume of transactions. The underlying asset is purchased at a higher ask price and it is sold for a lower bid price . The price of is then computed as an average of ask and bid prices, i.e., . Then represents a constant percentage of the cost of the sale and purchase of a share relative to the price , i.e.

| (8) |

The value of the synthesized portfolio consisting of one option in a long position at the price and underlying assets at the price changes over the time interval by selling or buying short positioned assets. It means that the purchase or selling assets at a price of yields the additional cost for the option holder

| (9) |

Consequently, the value of the portfolio changes to:

| (10) |

during the time interval . The key step in derivation of the Leland model consists in approximation of the change of transaction costs by its expected value , i.e. , where the transaction costs measure is defined as the expected value of the change of the transaction costs per unit time interval and price :

| (11) |

Hence equation (10) describing the change in the portfolio has the form:

| (12) |

Since the underlying asset follows the geometric Brownian motion we have

| (13) |

where is the increment of the Wiener process. Now, assuming the change in the portfolio is balanced by a bond with the risk-free rate , i.e. , using Itō’s lemma for and applying the delta hedging strategy we obtain generalization of the Black–Scholes equation

| (14) |

Furthermore, applying Itō’s formula for the function we obtain

plus higher order terms in . Here a normally distributed random variable. Hence, in the lowest order we have that

| (15) |

For the case of constant transaction costs given by (9), using the fact that we obtain

where is the Leland number. Inserting the term into (14) we obtain the Leland equation (3) with the volatility function given by (4).

Following derivation of the Leland model we present our approach on modeling variable transaction costs. Large investors can expect a discount due to large amount of transactions. The more they purchase the less they will pay per one traded underlying asset. In general, we will assume that the cost per one transaction is a nonincreasing function of the amount of transactions, , per unit of time , i.e.

| (16) |

It means that the purchase of or sales of 0 shares at a price of , we calculate the additional transaction costs per unit of time :

| (17) |

Hence the transaction costs measure can be expressed as

| (18) |

where is the transaction costs function and is the number of purchased or sold shares per unit of time .

In order to simplify notation we introduce the so-called mean value modification of the transaction costs function defined as follows:

Definition 2.1

Let , , be a transaction costs function. The integral transformation of the function defined as follows:

| (19) |

is called the mean value modification of the transaction costs function. Here is the random variable with a standardized normal distribution, i.e., .

Applying definition (19) to equation (18) we obtain the following expression for the transaction costs measure:

| (20) |

Inserting the transaction costs measure into (14) we obtain generalization of the Leland model for the case of arbitrary transaction costs function .

Proposition 2.1

Let be a measurable and bounded transaction costs function. Then the nonlinear Black–Scholes equation for pricing option under variable transaction costs is given by the nonlinear parabolic equation

| (21) |

where

| (22) |

In the next two propositions we summarize several useful properties of the mean value modification of a transaction costs function.

Proposition 2.2

Let be a measurable bounded transaction costs function such that for all . Then its mean value modification is a smooth function for . Furthermore, it has the following properties:

-

1.

;

-

2.

if then ;

-

3.

for all ;

-

4.

if is nonincreasing (nondecreasing) then is a non- increasing (nondecreasing) function as well;

-

5.

if is a (non-constant) convex function then is a (strictly) convex function.

Proposition 2.3

Let be a measurable and bounded transaction costs function which is nonincreasing for .

-

•

If then the function is strictly convex for .

-

•

If for all then

P r o o f. a) Since where and then, by using substitution , we obtain the following identity:

because (if then ) and for where

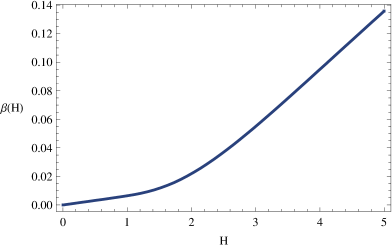

is a strictly positive function for depicted in Figure 2. It has a unique positive minimum at .

b) Again, as , we obtain

Since and we obtain , as claimed.

2.1 Piecewise linear nonincreasing transaction costs function

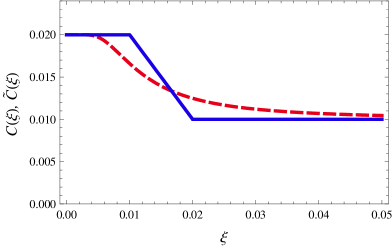

We present an example of a realistic transaction costs function which is nonincreasing with respect to the amount of transactions as in model studied by Amster et al. [1], Averbuj [4] Mariani et al. [28]. The benefit is the elimination of the problem of negative values of the linear decreasing costs function. We define the following piecewise linear function.

Definition 2.2

We define a piecewise linear nonincreasing transaction costs function as follows:

| (23) |

where we assume , and are given constants and .

This is a realistic transaction costs function. Indeed, for a small volume of traded assets the transaction costs rate equals . When the volume is large enough then a discount is applied with a lower transaction costs rate .

Notice that this function also covers several special cases studied before. Namely, the constant transaction costs function studied by Leland [26], Hoggard, Whalley and Wilmott [16] () as well as linearly decreasing transaction costs investigated by Amster et al. in [1] ().

Taking into account the fact that for and , otherwise, and using integration by parts we can easily derive that the mean value modification of a piecewise transaction costs function (23) is given by:

| (24) |

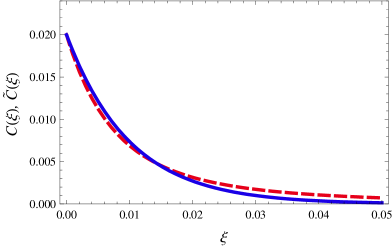

2.2 Exponentially decreasing transaction costs function

As an another example of a transaction costs function one can consider the following exponential function of the form

| (25) |

where and are given constants. Its mean value modification can be derived by expanding the function into power series:

and is the error function.

a) b)

3 Transformation of the fully nonlinear Black–Scholes equation to the quasilinear Gamma equation

The goal of this section is to study transformation of the nonlinear Black–Scholes equation into a quasilinear parabolic equation - the so-called Gamma introduced and investigated by Jandačka and Ševčovič in [19] (see also Ševčovič, Stehlíková and Mikula [29, Chapter 11]).

In what follows, we will use the notation

| (26) |

where is the volatility function depending on the term . Let be a numeraire for the underlying asset price, e.g. is the expiration price for a call or put option.

Proposition 3.1

Assume the function is a solution to the nonlinear Black-Scholes equation

| (27) |

Then the transformed function , where is a solution to the quasilinear parabolic (Gamma) equation

| (28) |

On the other hand, if is a solution to (28) such that and is finite then the function

| (29) |

is a solution to the nonlinear Black–Scholes equation (27) for any .

P r o o f. The first part of the statement can be shown directly by taking the second derivative of (27) with respect to . Indeed, as we have

Applying the operator to equation (27) and taking into account we conclude that is the solution to equation (28) (see also [19] and [29, Chapter 11]).

On the other hand, if is given by (29) then . Moreover, if is a solution to (28) then

Here we have used the fact that and is finite. Since

we finally obtain

Therefore solves the nonlinear Black–Scholes equation (27), as claimed.

Remark 3.1

If the initial condition is the Dirac -function then for the terminal pay-off diagram given by (29) we obtain

-

1.

(call option) when ,

-

2.

(put option) when .

Remark 3.2

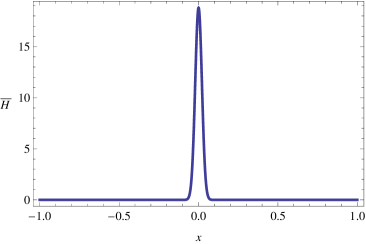

The initial Dirac -function can be approximated as follows:

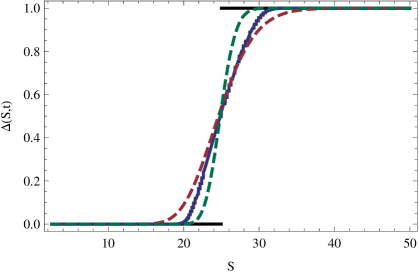

where is sufficiently small, is the PDF function of the normal distribution, and where . The idea behind such an approximation follows from observation that for a solution of the linear Black–Scholes equation with a constant volatility at the time close to expiry the value is given by . An approximation of the initial condition for is shown in Figure 3 (left).

3.1 Existence of classical solutions, comparison principle

The aim of this subsection is to analyze classical smooth solutions to the Cauchy problem for the quasilinear parabolic equation (28). Following the methodology based on the so-called Schauder’s type of estimates (cf. Ladyzhenskaya et al. [25]), we shall prove existence and uniqueness of classical solutions to (28).

We proceed with a definition of function spaces we will work with. Let be a bounded interval. We denote the space-time cylinder. Let . By we denote the Banach space consisting of all continuous functions defined on which are -Hölder continuous. It means that their Hölder semi-norm is finite. The norm in the space is then the sum of the maximum norm of and the semi-norm . The space consists of all twice continuously differentiable functions in whose second derivative belongs to . The space consists of all functions such that for any bounded domain .

The parabolic Hölder space of functions defined on a bounded cylinder consists of all continuous functions in such that is -Hölder continuous in the -variable and -Hölder continuous in the -variable. The norm is defined as the sum of the maximum norm and corresponding Hölder semi-norms. The space consists of all continuous functions on such that . Finally, the space consists of all functions such that for any bounded cylinder (cf. [25, Chapter I]).

We first derive useful lower and upper bounds of a solution to the Cauchy problem (28). The idea of proving upper and lower estimates for is based on construction of suitable sub- and super-solutions to the parabolic equation (28) (cf. [25]).

Lemma 3.1

Suppose that the initial condition is non-negative and uniformly bounded from above, i.e., . Assume is a smooth function for and satisfying the following strong parabolic inequalities:

for any where are constants. If the bounded solution to the quasilinear parabolic equation (28) belongs to the function space , for some , then it satisfies the following inequalities:

P r o o f. The quasilinear parabolic equation (28) can be rewritten in the form:

| (30) |

Notice that the right-hand side of (30) is a strictly parabolic operator because . Since the constant functions and are solutions to (30) then the statement is a consequence of the parabolic comparison principle for strongly parabolic equations (see e.g. [25, Chapter V, (8.2)]).

In the next Proposition we show that the diffusion function corresponding to the nonlinear Black–Scholes equation for pricing options under the variable transaction costs satisfies the strong parabolicity assumption.

Proposition 3.2

Let be a measurable bounded transaction costs function which is nonincreasing and such that for all . Let

Then for the diffusion function the following inequalities hold:

for all , where and .

P r o o f. For we have

Since is a nonincreasing function then and (see Proposition 2.2) then the inequality easily follows. According to Proposition 2.3 we have and so and the proof of the statement follows.

Theorem 3.1

Suppose that the initial condition belongs to the Hölder space for some and . Assume that satisfies for any where are constants.

Then there exists a unique classical solution to the quasilinear parabolic equation (28) satisfying the initial condition . The function is -Hölder continuous for all whereas is Lipschitz continuous for all . Moreover, and for all .

P r o o f. The proof is based on the so-called Schauder’s theory on existence and uniqueness of classical Hölder smooth solutions to a quasi-linear parabolic equation of the form (28). It follows the same ideas as the proof of [20, Theorem 5.3] where Kilianová and Ševčovič investigated a similar quasilinear parabolic equation obtained from a nonlinear Hamilton-Jacobi-Bellman equation in which a stronger assumption is assumed. Nevertheless, we sketch the key steps of the proof.

The Schauder theory requires that the diffusion coefficient of a quasi-linear parabolic equation is sufficiently smooth. Therefore the function has to be regularized by a -parameterized family of smooth mollifier functions such that , and locally uniformly as . For any , the existence of the unique classical bounded solution to the Cauchy problem:

follows from [25, Theor. 8.1 and Rem. 8.2, Ch. V, pp. 495–496]. Here .

By virtue of Lemma 3.1, , is uniformly bounded in the space for any bounded cylinder . Using the inequality [25, Chapter I, (6.6)] we can prove that , is also uniformly bounded in the Sobolev space . It means that there exists a subsequence weakly converging to a function as . As a consequence of the Rellich-Kondrashov compactness embedding theorem (cf. [25, Chapter II, Theorem 2.1]) the limiting function is a weak solution to the quasi-linear parabolic equation (28). Since we obtain . Furthermore, because . Hence, belongs to the parabolic Sobolev space which is continuously embedded into the Hölder space for any .

Finally, the transformed function is a solution to the quasi-linear parabolic equation in the non-divergent form:

where and is the inverse function to the increasing function . The function is -Hölder continuous. Thus is Hölder continuous as well. Now, we can apply a simple boot-strap argument to show that is sufficiently smooth. Clearly, it is a solution to the linear parabolic equation in non-divergence form

where . The functions and belong to the Hölder space because . With regard to [25, Theorem 12.2, Chapter III] we have and the proof now follows because the domain was arbitrary.

4 Numerical full space-time discretization scheme for solving the Gamma equation

The purpose of this section is to derive an efficient numerical scheme for solving the Gamma equation. The construction of numerical approximation of a solution to (28) is based on a derivation of a system of difference equations corresponding to (28) to be solved at every discrete time step. We make use of the numerical scheme adopted from the paper by Jandačka and Ševčovič [19] in order to solve the Gamma equation (28) for a general function including, in particular, the case of the model with variable transaction costs. The efficient numerical discretization is based on the finite volume approximation of the partial derivatives entering (28). The resulting scheme is semi–implicit in a finite–time difference approximation scheme.

Other finite difference numerical approximation schemes are based on discretization of the original fully nonlinear Black–Scholes equation in non-divergence form (3). We refer the reader to recent publications by Ankudinova and Ehrhardt [2], Company et al. [9], Düring et al. [11], Liao and Khaliq [27], Zhou et al. [33]. Recently, a quasilinearization technique for solving the fully nonlinear parabolic equation (3) was proposed and analyzed by Koleva and Vulkov [21]. Our approach is based on a solution to the quasilinear Gamma equation written in the divergence form, so we can use existing finite volume based numerical scheme to solve the problem efficiently (cf. Jandačka and Ševčovič [19], Kútik and Mikula [23]).

For numerical reasons we restrict the spatial interval to where is sufficiently large. Since it is sufficient to take in order to include the important range of values of . For the purpose of construction of a numerical scheme, the time interval is uniformly divided with a time step into discrete points , where . We consider the spatial interval with uniform division with a step , into discrete points where.

The proposed numerical scheme is semi–implicit in time. Notice that the term can be expressed in the form , where is the derivative of with respect to . In the discretization scheme, the nonlinear terms are evaluated from the previous time step whereas linear terms are solved at the current time level.

Such a discretization scheme leads to a solution of a tridiagonal system of linear equations at every discrete time level. First, we replace the time derivative by the time difference, approximate in nodal points by the average value of neighboring segments, then we collect all linear terms at the new time level and by taking all the remaining terms from the previous time level . We obtain a tridiagonal system for the solution vector :

| (31) |

where and . The coefficients of the tridiagonal matrix are given by

It means that the vector at the time level is a solution to the system of linear equations where the matrix . In order to solve the tridiagonal system in every time step in a fast and effective way, we can use the efficient Thomas algorithm.

Finally, with regard to Proposition 3.1 and Remark 3.1 the option price can be constructed from the discrete solution by means of a simple integration scheme:

4.1 Numerical results for the nonlinear model with variable transaction costs

In this section we present the numerical results for computation of the option price. As an example for numerical approximation of a solution we consider the nonlinear Black–Scholes equation for pricing options under variable transaction costs described by the piecewise linear nonincreasing function, depicted in Figure 1. The function corresponding to the variable transaction costs function has the form

where is the modified transaction costs function. We assume that the hedging time is such that .

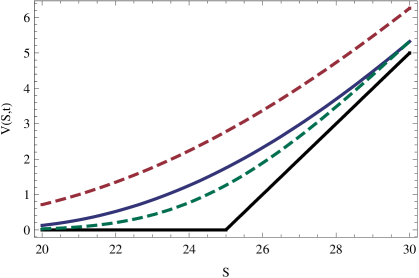

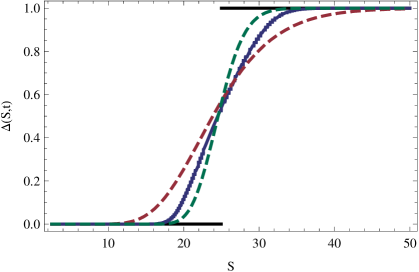

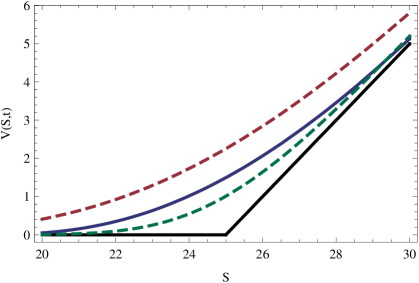

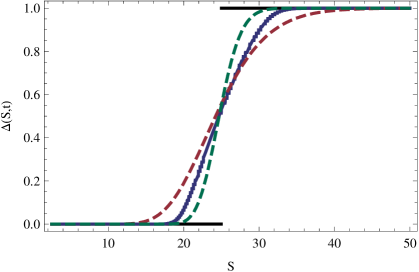

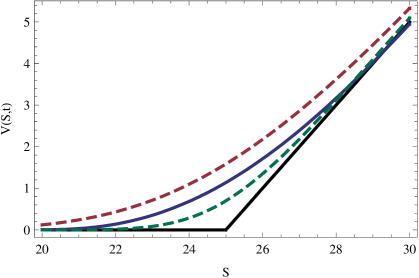

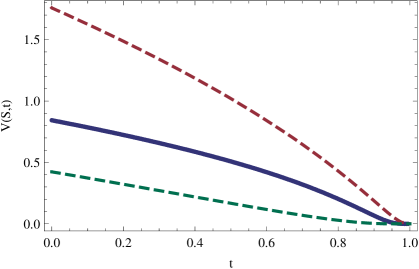

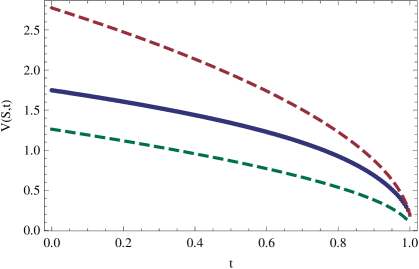

In our computations we chose the following model parameters describing the piecewise transaction costs function: . The length of the time interval between two consecutive portfolio rearrangements: . The maturity time , historical volatility and the risk-free interest rate . As for the numerical parameters we chose , and the parameter for approximation of the initial Dirac –function. The parameters and correspond to the Leland numbers and . In Table 1 we present option values for different prices of the underlying asset achieved by a numerical solution. In Figure 5 we plot the solution and the option price delta factor , for various times . The upper dashed line corresponds to the solution of the linear Black–Scholes equation with the higher volatility , where , whereas the lower dashed line corresponds to the solution with a lower volatility .

| 20 | 0.709 | 0.127 | 0.029 |

|---|---|---|---|

| 23 | 1.752 | 0.844 | 0.421 |

| 25 | 2.768 | 1.748 | 1.258 |

| 28 | 4.723 | 3.695 | 3.474 |

| 30 | 6.256 | 5.321 | 5.327 |

The empirically observed fact (see Table 1) that

can be proved analytically. It is a consequence of the parabolic comparison principle (cf. [25, Chapter V, (8.2)]). Indeed, the fully nonlinear Black–Scholes equation (27) can be considered as a nonlinear strongly parabolic equation

| (32) |

for the option price , where

Recall that for all and and so equation (32) is indeed a strongly parabolic equation. For the solution of the linear Black–Scholes equation with the constant volatility we have

because and so

Hence is a sub-solution to the strongly parabolic equation (32). Therefore, by the parabolic comparison principle, for all and . Analogously, the inequality follows from the parabolic comparison principle because .

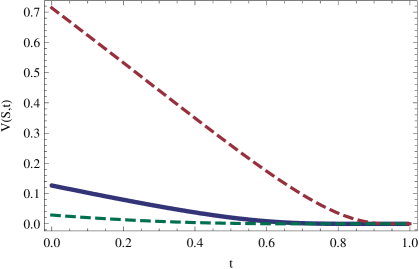

The dependence of the call option price on time for with is shown in Figure 6. We can also see that the price converges to zero at expiration for .

4.2 Some practical implications in financial portfolio management

Numerical results obtained in the previous subsection can be interpreted from the financial portfolio management point of view. For example, temporal behavior of the call option price shown in Fig. 6 for the underlying asset price indicates that the option price given by the solution of the nonlinear variable transaction cost model is closer to the lower bound for initial times . But in later times when the price is closer to the upper bound . It can be interpreted as follows: at the beginning of the contract the portfolio manager need not perform many transaction in order to hedge the portfolio. The transaction costs per one transaction is equal to . On the other hand, when the time approaches expiration then it is necessary to make frequent rearrangements of the portfolio and so the traded volume of assets increases. Hence the investor pays discounted lower transaction costs value per one transaction of the short positioned underlying asset. Consequently, the option price is higher.

The comparison principle (see also Table 1) has the following practical implication: if the transaction cost per unit share depends on the volume of traded shares and it belongs to the interval the option price can be estimated from above (below) by the option price corresponding to the constant transaction costs ().

Conclusions

In this paper we have analyzed a nonlinear generalization of the Black–Scholes equations arising when options are priced under variable transaction costs for buying and selling underlying assets. The mathematical model is represented by the fully nonlinear parabolic equation with the diffusion coefficient depending on the second derivative of the option price. We have investigated properties of various realistic variable transaction costs functions. Furthermore, for a general class of nonlinear Black–Scholes equation we have developed a transformation technique, by means of which the fully nonlinear equation can be transformed into a quasilinear parabolic equation. We have proved existence and uniqueness of classical solutions to the transformed equation. Finally, we have presented a numerical approximation scheme and we computed option prices for pricing model under variable transaction costs.

References

- [1] Amster, P., Averbuj, C. G., Mariani, M. C., Rial, D. (2005): A Black–Scholes option pricing model with transaction costs. J. Math. Anal. Appl., 303, 688–695.

- [2] Ankudinova J., Ehrhardt, M. (2008): On the numerical solution of nonlinear Black–Scholes equations. Computers and Mathematics with Applications, 56, 799–812.

- [3] Avellaneda, M., Levy, A., Paras, A. (1995): Pricing and hedging derivative securities in markets with uncertain volatilities. Applied Mathematical Finance, 2, 73–88.

- [4] Averbuj, C. G. (2012): Nonlinear Integral-differential evolution equation arising in option pricing when including transaction costs: A viscosity solution approach. Revista Brasileira de Economia de Empresas, 12(1), 81–90.

- [5] Bakstein, D., Howison, S. (2004): A non–arbitrage liquidity model with observable parameters. Working paper, http://eprints.maths.ox.ac.uk/53/

- [6] Barles, G., Soner, H. M. (1998): Option Pricing with transaction costs and a nonlinear Black–Scholes equation. Finance and Stochastics, 2, 369-397.

- [7] Black, F., Scholes, M. (1973): The pricing of options and corporate liabilities. J. Political Economy 81, 637–654.

- [8] Casabán, M. C., Company, R., Jódar, L., Pintos, J. R. (2011): Numerical analysis and computing of a non–arbitrage liquidity model with observable parameters for derivatives. Computers and Mathematics with Applications, 61, 1951–1956.

- [9] Company R., Navarro E., Pintos J.R. and Ponsoda E. (2008): Numerical solution of linear and nonlinear Black-Scholes option pricing equations. Computers an Mathematics with Applications, 56, 813–-821.

- [10] Dremkova, E., Ehrhardt, M. (2011): High-order compact method for nonlinear Black–Scholes option pricing equations of American options. International Journal of Computer Mathematics, 88, 2782–2797.

- [11] During, B., Fournier, M., Jungel, A. (2003): High order compact finite difference schemes for a nonlinear Black–Scholes equation. Int. J. Appl. Theor. Finance, 7, 767–789.

- [12] Frey, R., Patie, P. (2002): Risk Management for Derivatives in Illiquid Markets: A Simulation Study. In: Advances in Finance and Stochastics, Springer, Berlin, 137–159.

- [13] Frey, R., Stremme, A. (1997): Market Volatility and Feedback Effects from Dynamic Hedging. Mathematical Finance, 4, 351–374.

- [14] Grandits, P., Schachinger, W. (2001): Leland’s approach to option pricing: the evolution of a discontinuity. Mathematical Finance, 11, 347–355.

- [15] Grossinho, M.R., Morais, E. (2009): A note on a stationary problem for a Black-Scholes equation with transaction costs. International Journal of Pure and Applied Mathematics, 51, 557–565.

- [16] Hoggard, T., Whalley, A. E., Wilmott, P. (1994): Hedging option portfolios in the presence of transaction costs. Advances in Futures and Options Research, 7, 21–35.

- [17] Imai, H., Ishimura, N., Mottate, I., Nakamura, M. (2007): On the Hoggard–Whalley–Wilmott Equation for the Pricing of Options with Transaction Costs Asia-Pacific Financial Markets, 13, 315-326.

- [18] Ishimura, N. (2010): Remarks on the Nonlinear Black-Scholes Equations with the Effect of Transaction Costs. Asia-Pacific Financial Markets, 17, 241–259.

- [19] Jandačka, M., Ševčovič, D. (2005): On the risk adjusted pricing methodology based valuation of vanilla options and explanation of the volatility smile. Journal of Applied Mathematics, 3, 235–258.

- [20] Kilianová, S., Ševčovič, D. (2013): A Transformation Method for Solving the Hamilton-Jacobi-Bellman Equation for a Constrained Dynamic Stochastic Optimal Allocation Problem. ANZIAM Journal, 55, 14–38.

- [21] Koleva, M.N., L. G. Vulkov, L.G. (2013): Quasilinearization numerical scheme for fully nonlinear parabolic problems with applications in models of mathematical finance. Mathematical and Computer Modelling, 57, 2564–2575.

- [22] Kratka, M. (1998): No Mystery Behind the Smile. Risk, 9, 67–71.

- [23] Kútik P., Mikula K. (2011): Finite Volume Schemes for Solving Nonlinear Partial Differential Equations in Financial Mathematics, in Proceedings of the Sixth International Conference on Finite Volumes in Complex Applications, Prague, June 6-10, 2011, Springer Proceedings in Mathematics, Volume 4, 2011, Eds: J.Fořt, J. Fürst, J.Halama, R. Herbin and F.Hubert, 643-561,

- [24] Kwok, Y. K. (1998): Mathematical Models of Financial Derivatives. Springer-Verlag.

- [25] Ladyženskaja, O. A., Solonnikov, V. A., and Ural’ceva, N. N. Linear and quasilinear equations of parabolic type. Translated from the Russian by S. Smith. Translations of Mathematical Monographs, Vol. 23 (American Mathematical Society, Providence, R.I., 1968).

- [26] Leland, H. E. (1985): Option pricing and replication with transaction costs. Journal of Finance, 40, 1283–1301.

- [27] Liao W., Khaliq A. Q. M. (2009): High-order compact scheme for solving nonlinear Black–Scholes equation with transaction costs. International Journal of Computer Mathematics, 86, 1009–1023.

- [28] Mariani, M.C., Ncheuguim, E., Sengupta, I. (2011): Solution to a nonlinear Black-Scholes equation. Electronic Journal of Diff. Equations 2011(158), 1–10.

- [29] Ševčovič, D., Stehlíková, B., Mikula, K. (2011): Analytical and numerical methods for pricing financial derivatives. Nova Science Publishers, Inc., Hauppauge, 309 pp.

- [30] Schönbucher, P., Wilmott, P. (2000): The feedback-effect of hedging in illiquid markets. SIAM Journal of Applied Mathematics, 61, 232–272.

- [31] Wilmott, P., Dewynne, J., Howison, S.D. (1995): Option Pricing: Mathematical Models and Computation. UK: Oxford Financial Press.

- [32] Wilmott, P., Howison, S., Dewynne, J. (1995): The Mathematics of Financial Derivatives. USA: Press Syndicate of the University of Cambridge.

- [33] Zhou, S., Han, L., Li, W., Zhang, Y., Han, M. (2015): A positivity-preserving numerical scheme for option pricing model with transaction costs under jump-diffusion process. Computational and Applied Mathematics, 34, 881–900.