1 Introduction

Modeling credit risk has long been a critical issue in credit risk management. Attention has been given

to it especially since the global financial crisis in 2008.

Credit risk modeling has a lot of applications, for example,

pricing and hedging the credit derivatives,

as well as the management of credit portfolios.

Models adopted in the finance industry may be grouped into two major categories:

structural firm value models and reduced-form intensity-based models.

For the first class of models, it was pioneered by Black and Scholes (1973)

and Merton (1974).

The key idea of the structural firm’s value model is to model the default of a firm by using its asset value,

where the asset value is governed by a geometric Brownian motion.

When the asset value falls below a certain prescribed level,

the default of the firm is triggered.

For the second kind of model, it was pioneered by Jarrow and Turnbull (1995)

and Madan and Unal (1998).

The main idea of reduced-form intensity-based models is to consider the defaults as exogenous processes

and describe their occurrences with Poisson processes and their variants.

The interacting intensity-based default models are widely adopted to model

the portfolio credit risk and defaults.

Since we focus on contagion models in this paper as in, for example, Giesecke (2008),

we differentiate intensity-based credit risk models into top-down models and bottom-up models.

The top-down models focus on modeling the default times at the portfolio level without reference to the intensities of individual entities.

Based on this, one can also recover the individual entity’s intensity with some method like random thinning, etc.

Some works related to this class of models include

Davis and Lo (2001),

Giesecke, Goldberg and Ding (2005),

Brigo, Pallavicini and Torresetti (2006),

Longstaff and Rajan (2008)

and Cont and Minca (2011), etc.

While the bottom-up model focuses on modeling the default intensities of individual reference entities and their aggregation to form a portfolio default intensity.

Some works related to this class of models include

Duffie and Garleanu (2001),

Jarrow and Yu (2001),

Schönbucher and Schubert (2001),

Giesecke and Goldberg (2004),

Duffle et al. (2006)

and Yu (2007), etc.

The differences between these two classes of models are the form of individual

entity’s default intensities and the way the portfolio aggregation is formed.

In this paper we shall focus on a bottom-up model.

Based on the model developed by Lando (1998), Yu (2007)

extended the model and applied the extended model multiple defaults and their correlation.

In addition, Yu adopted the total hazard construction method proposed

by Norros (1986) and Shaked and Shathanthikumar (1987)

to simulate the distribution of default times which have interacting intensities.

Zheng and Jiang (2009) then adopted this method and derived closed-form formulas for the multiple default distributions under their contagion model.

Gu et al. (2013) introduced a recursive method to calculate the distribution of ordered default times, and Gu et al. (2014) further proposed a hidden Markov reduced-form model with a specific form of default intensities.

In this paper we develop a generalized reduced-form intensity-based credit model with hidden Markov process.

The model is applicable to a wide class of default intensities with various forms of dependent constructions.

For the hidden Markov process, we also discuss a flexible method to extract the hidden state process given the observations processes, which may hopefully have applications in diverse fields.

Then using the total hazard construction method by Yu (2007), we derive closed-form formulas for the joint default distribution. When the intensities are homogeneous, analytic algorithm for the calculation

of the joint distribution of ordered default times is provided. The explicit formula may enhance the computational efficiency in applications, for instance, pricing of credit derivatives. We remark that the results in Gu et al. (2014) is a special case of the method discussed here. In addition, we extend the total hazard construction method to the cases with hidden process to simulate the joint distribution of default times.

We remark that hidden Markov models have been employed in studying credit risk,

see for instance, Frey and Runggaldier (2010, 2011), Frey and Schmidt (2011), Elliott and Siu (2013) and Elliott et al. (2014).

The rest of this paper is structured as follows.

Section 2 gives a snapshot of the interacting intensity-based default model with hidden Markov process.

Section 3 presents the method for extracting the hidden state process from the observation processes.

Section 4 derives the closed-form expression for the joint default distribution based on the total hazard construction method, and also presents an analytic formula for the distribution of ordered default times. Besides, the extended total hazard construction method under a hidden Markov process to obtain the joint distribution of default times is also presented. Section 5 provides numerical methods for some situation in Section 3 which may be used in both Sections 3 and 4,

and error analysis is also discussed.

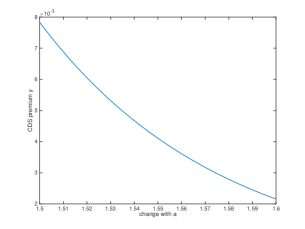

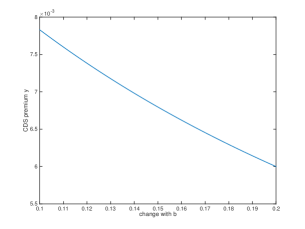

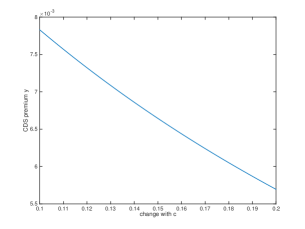

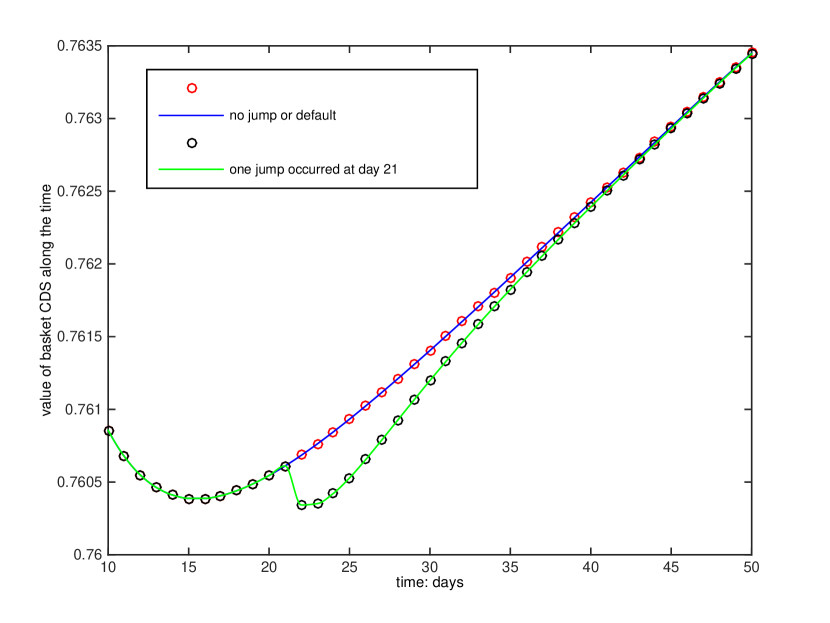

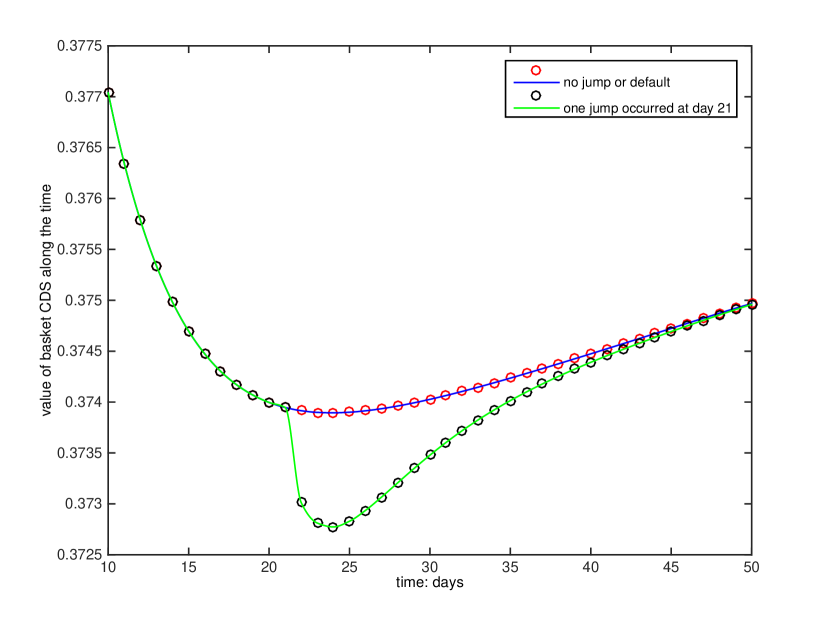

Section 6 illustrates an application of the proposed method in pricing credit derivatives.

Finally, Section 7 concludes the paper.

2 Model Setup

Let be a complete probability space

where is a risk-neutral probability measure, which is assumed to exist.

Suppose there are interacting entities, and we let ,

where is a stopping time, representing the default time of credit name , for each .

Suppose we have an underlying state process

describing the dynamics of the economic condition.

Let

where represents all the null subsets of in and is the minimal -algebra containing both the -algebras and .

We also let

where

|

|

|

We assume that for each ,

possesses a nonnegative, -adapted,

intensity process satisfying

|

|

|

(1) |

such that the compensated process

|

|

|

(2) |

is an -martingale.

Note that after the default time , will stay at the value one, so

there is no need to compensate for after time , see, for example, Elliott et al. (2000).

For all the market participants, we assume that they cannot observe the underlying

process directly.

Instead, they observe the process ,

revealing the delayed and noisy information of ,

and also observe the default process .

Hence, the common information set available to the market participants at time is

where .

We further assume that

is an “exogenous” process to , i.e., For any , the -fields

and

are conditionally independent

given and

.

To simplify our discussion, throughout the paper, we suppose that

is a two-state Markov chain taking a value in .

We assume the transition rates of the chain for

“” and “” are

and , respectively.

The observable process is again a two-state Markov chain

taking value in , with transition rates depending on ,

i.e.,

and ,

where and are real-valued functions.

At time , we suppose that is in state and is in state .

The methods introduced later in our paper may still be

applicable when the Markov chains and have more than two states though more complicated notation may involve.

3 Extraction of Hidden State Process with Observable Processes

To specify the form of the intensities, we give the following notations.

Suppose that at time , defaults have already occurred at

such that

|

|

|

Then we denote the ordered default times

and the corresponding defaulters,

and the th defaulted obligor is .

We assume that and , where is the obligor ’s default time. Each process (), is -predictable, that is to say is known given information about the chain and all the default processes prior to time .

Then the intensity of may be written as

where is the state of chain at time .

Note that .

Since the path of is unobservable,

while the path of and , () are observable,

we can use the relationship between , and , ()

to find the probability law of .

We apply the recursive method proposed in Gu et al. [15]

to calculate the conditional probability , (). Before discussing the method, we need to find the expressions for all

the unknown items in the recursive formulas.

In the process of finding the expressions,

we also present moment generating function method to achieve our goal.

3.1 Some Preliminaries

Let be the union of subintervals of time of

the chain in state in the time interval

given the chain starts from

and ends at .

For each , we let

|

|

|

where .

Note that .

Since jumps in chain and defaults are Poisson processes,

using the concept of moment generating function, we define

|

|

|

Note that is an arbitrary integrable function.

This means, in this case, we can adopt this moment generating function.

For instance, can be the transition rates of jumps in chain

or the default rates which are the default intensities accumulated by all the entities by time before default.

Proposition 1

Let , where is the probability that a process in state will be in state after a time of , and . Then

|

|

|

(3) |

where .

Proof:

|

|

|

We also have

|

|

|

Replace by ,

we can then get the system of equations in the proposition.

We find that when the expression of satisfies some “good” property,

Eq. (3) in the above proposition has a unique solution.

The property is that does not have any direct relationship with time even though it may have implied relationship with .

This means can be written as .

Then, not only the problem of solving Eq. (3) can be simplified,

but some related definitions can also be simplified as well.

Similar as before, let be the occupation time of

the chain in state in the time interval

given the chain starting from

and ending at . For each , we let

|

|

|

The moment generating function of is given by

|

|

|

Apply the same method to as we have done to ,

and let

|

|

|

We can also get the equivalent Eq. (3) for , ,

replacing with , with in Eq. (3).

Then to solve the equivalent equation, it suffices to solve a linear

system of O.D.E.s (c.f. Gu et al. [15]):

|

|

|

where

|

|

|

This linear system of O.D.E.s is known as the fundamental matrix equation in the literature. Then it is well-known that the equation has a unique solution which is called the fundamental matrix solution with the initial condition

as

|

|

|

where

is the two-dimensional column vector

with all entries being equal to .

Hence we can get the solution for by

|

|

|

In practice, when the expressions of , ( are given,

we can substitute them into the above Eq. (3),

then intuitively we can check whether it has a solution.

Note that the expressions of , determine

whether the system is solvable.

If it is solvable, then we can obtain the solution

), .

Note that the results in [15] can be regarded as a special case that has a unique solution.

3.2 Recursive Formulas for Extracting Hidden Process

For ,

we can express in a more clear way as follows:

|

|

|

where

-

•

,

-

•

,

-

•

,

-

•

counts the number of jumps in chain by time ,

-

•

counts the number of defaults by time ,

-

•

is the collection of ordered jump times of the chain by time ,

i.e., ,

-

•

is the collection of ordered default times by time , i.e., ,

-

•

is the collection of ordered corresponding name of defaulters by time , , name defaults at time .

Here can be interpreted as the state of the stochastic dynamical system at time . Given the information up to time , i.e., ,

we divide the time period into ()

sub-periods, , , …, .

In each of them, exactly one default or one jump in is observed.

When there is no default or jump occurred by time ,

the calculation of can be simplified and

we shall introduce it later.

Define .

Suppose that and are two endpoints of one sub-period.

The following characterizes the computational method for

. For ,

|

|

|

(4) |

and

|

|

|

(5) |

where

|

|

|

Similarly, we have for ,

|

|

|

(6) |

and

|

|

|

(7) |

where

|

|

|

Combining Eqs. (4), (5), (6) and (7),

we obtain a recursive method for computing

in terms of

and .

That is to say, with the fact that and , we can apply them to Eq. (4) or Eq. (6)

according to , and then to get which are unknown in

the calculation of in

Eq. (5) or Eq. (7).

The equation to calculate should be chosen according to as well.

By repeating this recursion procedure, we can obtain the desired conditional probabilities.

To get the expressions for the desired and , we need to use the method introduced in section 3.1.

Replace by , and we know that

there exists unique solutions for . Replace by , in Eq. (3), we then could have a direct sense of whether it is solvable or not. If it is solvable and has an analytical solution, then from the definition of and , we get

|

|

|

|

|

|

where and

|

|

|

If up to time , no jump or default has been observed, then we have the following:

for no jump or default observed in ,

|

|

|

where

|

|

|

Note that if the jump intensities of chain : (), are not as simple as in our assumptions and they are also related with time directly, i.e., ,

all the algorithms introduced above are still applicable and we just need to replace by , .

This replacement holds only when Eq. (3)

given has an analytical solution.

If Eq. (3) does not admit an analytical solution given , (),

we also provide numerical method in Section 5.

Now we know how to get .

5 Numerical Approximation Method

In this section, we consider an outstanding problem in Section

3.

If Eq. (3) does not admit an analytical solution given , ()

then we shall try to use another method to approximate the conditional probability .

We can consider approximating directly.

As we mentioned before, it is because of the default intensities

, () which give

Eq. (3) with

|

|

|

does not have an analytical solution,

and hence we cannot obtain closed-form expressions for .

Thus, we need to approximate the moment generating function

when the default intensities are applied.

If the error of is less than any arbitrary

then according to the expression of

and given below, we know that their relative errors can be controlled.

Furthermore, from the recursive method for presented in Section 3,

the error of this conditional probability may be controlled.

In the following, we are going to illustrate how the approximation works.

When the length of the time interval length is small enough,

without loss of generality, we can approximately assign in the default intensities

to be the left value of the concerned time interval,

i.e., when the time interval is .

Then we can still apply the moment generating function given , and we know the corresponding Eq. (3) has a unique solution. But we need to ensure that by using this method,

the error of can be controlled such that it can be less

than any arbitrarily given .

Proposition 5

The error control , where is arbitrary, can be achieved by requiring to satisfy

|

|

|

where

|

|

|

and

|

|

|

and

|

|

|

and

|

|

|

Proof:

Note that there are entities, so when the default intensity is applied, i.e.,

|

|

|

we notice the relationships that

|

|

|

and

|

|

|

Since all are nonnegative,

therefore, we have the following relationship:

|

|

|

if and only if

|

|

|

if and only if

|

|

|

We can simply let ,

it is enough to make the error of controllable.

Here we are in the position to approximate .

First, we partition the time interval evenly with step size equal to

, and denote

.

That is to say,

|

|

|

Moreover, we do the same thing for the remaining time interval:

and denote .

We denote and .

Now the explicit approximation formula is given as follows:

|

|

|

Similarly, we can get

|

|

|

|

|

|

where and .

|

|

|

where .

Now we know how to ensure , and have the formulas for calculating , and .

We can then discuss how to choose such that the relative error of them can be controlled as small as we wish, i.e., .

Taking as an example in the following discussion, the results related to the others are similar.

Proposition 6

To ensure the relative error of , i.e.,

|

|

|

where denotes the real value, denotes the value calculated according to the approximation formula, be less than any arbitrary percentage , we can require the error of , where , to satisfy the following conditions:

|

|

|

Proof:

Notice that when , the following relationship

|

|

|

would always be valid. That is to say, when we choose the numerical time step size to ensure the error of be less than , this step size would also ensure the error of where be less than as well.

Because and are always less than ,

from the expressions for calculating above,

to make sure that the error be less than , we have the following relationships

|

|

|

which implies

|

|

|

and

|

|

|

which implies

|

|

|

where .

Notice that in the above would always be greater than which is equal to .

Thus we can replace each in the above with to find according to .

Also, note that

|

|

|

then the above equations can be rewritten as follows:

|

|

|

All the conditions related to the relative errors of , and similar to the above proposition should be satisfied to find a suitable . Therefore, the relative errors are controlled and the error of is also controlled.

We remark that suppose the expiry time is denoted as , then all in proposition and proposition could simply be replaced by .