On Some New Dependence Models derived from Multivariate Collective Models in Insurance Applications

Abstract:

Consider two different portfolios which have claims triggered by the same events. Their corresponding

collective model over a fixed time period is given in terms of individual claim sizes and a claim counting random variable . In this paper we are concerned with the joint distribution function of the largest claim sizes . By allowing to depend on some parameter, say , then is for various choices of a tractable parametric family of bivariate distribution functions.

We investigate both distributional and extremal properties of .

Furthermore, we present several applications of the implied parametric models to some data from the literature and a new data set from a Swiss insurance company 111Data set can be downloaded here

http://dx.doi.org/10.13140/RG.2.1.3082.9203.

Key Words: Largest claims; copula; loss and ALAE; max-stable distribution; estimation; parametric family.

MSC: 62F10; 60G15

1. Introduction

Modelling the dependence structure between insurance risks is one of the main tasks of actuaries. For instance, the determination of a risk capital in the risk management framework needed to cover unexpected losses of an insurance portfolio and the allocation of the latter to each line of business is of importance when choosing the best model of dependence for multivariate insurance risks.

As discussed in Nelsen (1999), copulas are a popular multivariate distribution when modelling the dependency between insurance risks as they separate the marginals from the dependence structure, see Embrechts (2009), Genest et al. (2009) and references therein.

With motivation from Zhang and Lin (2016), in this contribution we propose a flexible family of copulas derived from the joint distribution of the largest claim sizes of two insurance portfolios.

Next, in order to introduce our model, we consider the classical collective model over a fixed time period of two insurance portfolios with

modelling the th claim sizes of both portfolios and the total number of such claims. If , then there are no claims, so the largest claims in both portfolios are equal to 0. When then denotes the maximal claim amounts in both portfolios. Commonly, claim sizes are assumed to be positive, however here

we shall simply assume that are independent with common distribution function (df) and is independent of everything else. Such a model is common for proportional reinsurance. In that case with being a positive constant. Another instance is if ’s model claim sizes and ’s model the expenses related to the settlement of ’s, see Denuit et al. (2005) for statistical treatments and further applications. The df of denoted by is given by

| (1) |

with the Laplace transform of . Clearly, is a mixture df given by

where

| (2) |

with and its Laplace transform.

Since both distributional and asymptotic properties of can be easily derived from those of , in this paper

we shall focus on assuming throughout that is an integer-valued random variable.

When the df is a product distribution, above corresponds to the frailty model, see e.g., Denuit et al. (2005),

whereas the special case

that is a shifted geometric random variable is dealt with in Zhang and Lin (2016).

We mention three tractable cases for :

Model A: In Zhang and Lin (2016), is assumed to have a shifted Geometric distribution with parameter which leads to

| (3) |

Model B: has a shifted Poisson distribution with parameter , i.e., with being a Poisson random variable with mean , which implies

| (4) |

Model C: has a truncated Poisson distribution with and thus

| (5) |

Since the distributions and their copulas are indexed by an unknown parameter , the new mixture copula family has several interesting properties. In particular, it allows to model highly dependent insurance risks and therefore our model is suitable for numerous insurance applications including risk aggregation, capital allocation and reinsurance premium calculations.

In this contribution we investigate first the basic distributional and extremal properties of for general . As it will be shown in Section 3, interestingly the extremal properties of are similar to those of .

With some motivation from Zhang et al. (2016), which investigates Model A and its applications, in this paper, we shall discuss parameter estimation and Monte Carlo simulations for parametric families of bivariate df’s induced by . In particular, we apply our results to actuarial modelling of concrete data sets from actuarial literature. Moreover we shall consider the implications of our findings for a new real data set from a Swiss insurance company. In several cases Model B and Model C give both satisfactory fit to the data. For the case of Loss and ALAE data set we model further the stop loss and the excess of loss reinsurance premium. One of the applications of the joint distribution of the largest claims of two insurance portfolios is the analysis of the impact of their sum on the risk profile of the portfolios. Over the last decades, many contributions have been devoted on the study of the influence of the largest claims on aggregate claims, see e.g., Peng (2014) , Asimit and Chen (2015) for an overview of existing contributions on the topic. This analysis is important when designing risk management and reinsurance strategies especially in non proportional reinsurance. Ammeter (1964) is one of the first contribution which addressed the impact of the largest claim on the moments of the total loss of an insurance portfolio , see also Asimit and Chen (2015) for recent results. In this paper we demonstrate by simulation the influence of the sum of the largest claims observed in two insurance portfolios on the distribution of . Moreover, using the covariance capital allocation principle we quantify the impact of and on the total loss . The paper is organised as follows. We discuss next some basic distributional properties of . An investigation of the coefficient of upper tail dependence and the max-domain of attractions of is presented in Section 3. Section 4 is dedicated to parameter estimation and Monte Carlo simulation with special focus on the cases covered by Model A-C above. We present three applications to concrete insurance data set in Section 5. All the proofs are relegated to Appendix.

2. Basic Properties of

Let denote the df of and write for its marginal df’s. Suppose that ’s are continuous and thus the copula of is unique. For , we have that the marginal df’s of are

Hence, the generalised inverse of is

where is the generalised inverse of . Consequently, since the continuity of ’s implies that of ’s, the unique copula of is given by

| (6) | |||||

where we set

Remarks 2.1.

The df of the bivariate copula in (6) can be extended to the multivariate case. Let be the -th claim sizes of the portfolio and . Thus, the df of is given by

where is the df of . Similarly to the bivariate case one may express the copula of as follows

where is the copula of . Without loss of generality, we present in the rest of the paper the results for the bivariate case.

Next, if has a probability density function (pdf) , then has a pdf given by

with the marginal pdf’s. Consequently, the pdf of is given by (set )

| (7) |

where and . The explicit form of for tractable copulas and Laplace transform is useful for the pseudo-likelihood method of parameter estimation treated in Section 4.

To this end, we briefly discuss the correlation order and its implication for the dependence exhibited by . Clearly, for any non-negative

Consequently, in view of the correlation order, see e.g., Denuit et al. (2005) we have that Kendall’s tau , Spearman’s rank correlation and

the correlation coefficient (when it is defined) are

bounded by the same dependence measures calculated to with df , respectively.

Moreover, if , then by applying Jensen’s inequality (recall almost surely) for any non-negative

| (8) |

with the smallest integer larger than . Since is a df, say of , then

again the correlation order implies that ,

and similar bounds hold for Spearman’s rank correlation and the correlation coefficient. In the following

we shall write also and (if instead of and

, respectively. Similarly, we denote and instead of and

, respectively.

3. Extremal Properties of

In this section, we investigate the extremal properties of and its copula. Assume that depends on and write instead of . Suppose for simplicity that and has unit Fréchet margins. Assume additionally the following convergence in probability

| (9) |

The above conditions can be easily verified in concrete examples, in particular it holds if almost surely.

In order to understand the dependence of , we can calculate Kendall’s tau as .

For instance, as shown in the simulation results in Table 1, if the copula of has a coefficient of upper tail dependence , then .

Note that by definition if exists, then it is calculated by

| (10) |

The following result establishes the convergence of both Kendall’s tau for and Spearman’s rank correlation to the corresponding measures of dependence with respect to an extreme value copula which approximates , i.e.,

| (11) |

where

| (12) |

for any with a convex function which satisfies

| (13) |

In the literature, see e.g., Falk et al. (2010); Molchanov (2008); Bücher and Segers (2014); Aulbach et al. (2015), is referred to as the Pickands dependence function.

If is different from the independence copula, and therefore for any , then we have (see e.g., Molchanov(2008))

| (15) |

To illustrate the results stated above, we compare by simulations the dependence properties of both and . To this end,

we simulate random samples from both copulas and compute the empirical dependence measures. Specifically, we generate a random sample from in which Step 1-Step 4 in Subsection 4.2 are repeated times. Also, we simulate from Model B and two cases of namely, a Gumbel copula with parameter and a Clayton copula with parameter .

Table 1 describes the simulated empirical Kendall’s tau and Spearman’s rho for the random samples generated from and .

| : Gumbel copula with | : Clayton copula with | |||||||

|---|---|---|---|---|---|---|---|---|

| 10 | 0.9059 | 0.9022 | 0.9871 | 0.9862 | 0.3533 | 0.8343 | 0.5030 | 0.9588 |

| 100 | 0.8980 | 0.9002 | 0.9848 | 0.9854 | 0.0518 | 0.8348 | 0.0775 | 0.9589 |

| 1’000 | 0.9007 | 0.9004 | 0.9856 | 0.9856 | 0.0043 | 0.8334 | 0.0064 | 0.9577 |

| 10’000 | 0.9016 | 0.9018 | 0.9857 | 0.9859 | 0.0019 | 0.8324 | 0.0027 | 0.9573 |

| 100’000 | 0.8997 | 0.8996 | 0.9851 | 0.9854 | -0.0104 | 0.8316 | -0.0156 | 0.9569 |

The table above shows that for the Gumbel copula case, the level of dependence of a bivariate risk governed by is lower or approximately equal to the one corresponding to when increases. For the case of Clayton copula, the bigger , the weaker the dependence associated with . In particular, for a copula with no upper tail dependence, Clayton copula in our example, it can be seen that when increases, tends to the independence copula. However, when is an extreme value copula, Gumbel copula in our illustration, the rate of decrease in the level of dependence with respect to is small. These empirical findings are due to the correlation order demonstrated in (8).

To verify the results obtained from simulations, we show that, under (15), for , we obtain and for the Gumbel copula which are in line with the simulation results presented in Table 1.

It should be noted that for the Gumbel copula, the Pickands dependence function can be written as follows

leading to a closed form for given by

Also, it is well-known that for Clayton copula (11) holds with being the independence copula, hence for this case by (14) we have , which confirms the findings in Table 1.

This section is concerned with the extremal properties of the df introduced in (1) in terms of and . The natural question which we want to answer here is whether the extremal properties of and are the same. Therefore, we shall assume that is in the max-domain of attraction of some max-stable bivariate distribution . Without loss of generality we shall assume that has unit Fréchet marginal df’s. Hence, our assumption is that

| (16) |

The max-stability of and the fact that its marginal df’s are unit Fréchet imply

| (17) |

see e.g., Falk(2010). In case is a shifted geometric random variable as in Model A, then the above assumptions imply for any non-negative (set )

Hence

| (18) |

or equivalently, using (17)

| (19) |

and thus is also in the same max-domain of attraction as .

Our result below shows that the extremal properties of are preserved for the general case when is finite. This assumption is natural in collective models, since otherwise we cannot insure such portfolios.

Proposition 3.2.

Remarks 3.3.

i) It is well-known, see e.g., Falk (2010), that if is in the max-domain of attraction of , then the coefficient of upper tail dependence of with copula exists and

By the above proposition, is also in the max-domain of attraction of , and thus

| (21) |

ii) Although and are in the same max-domain of attraction, the above proposition shows that the normalising constant for is different that for (here ) if .

4. Parameter Estimation and Monte Carlo Simulations

4.1. Parameter Estimation

This section focuses on the estimation of the parameters of the new copula i.e., of and of the copula . Hereafter, we denote .

There are three widely used methods for the estimation of the copula parameters. The classical one is the maximum likelihood estimation (MLE). Another popular method is the inference function for margins (IFM), which is a step-wise parametric method. First,

the parameters of the marginal df’s are estimated and then the copula parameter are obtained by maximizing the likelihood function of the copula with the marginal parameters replaced by their first-stage estimators.

Typically, the success of this method depends upon finding appropriate parametric models for the marginals, see Kim et al. (2007).

Finally, the pseudo-maximum likelihood (PML) method, introduced by Oakes (1989) consists also of two steps.

In the first step, the marginal df’s are estimated non-parametrically. The copula parameters are determined in the second step by maximizing the pseudo log-likelihood function. Specifically, let and where and are the unknown marginals df’s of and . For instance, if the data is not censored, a commonly used non-parametric estimator of and is their sample empirical distributions which are specified as follows

| (22) |

Therefore, in order to estimate the parameter , we maximize the following pseudo log-likelihood function

| (23) |

where denotes the pdf of the copula. This rescaling is used to avoid difficulties arising from the unboundedness of the pseudo log-likelihood function in (23) as or tends to 1, see Genest et al. (1995).

Kim et al. (2007) show in a recent simulation study that the PML approach is better than the well-known IFM and MLE methods when the marginal df’s are unknown, which is almost always the case in practice. Moreover, it is shown in Genest et al. (1995) that the resulting estimators from the PML approach are consistent and asymptotically normally distributed.

Therefore, for our study, we shall use the PML method for the estimation of which takes into account the empirical counterparts of the marginal df’s to find the parameter estimators.

As described in the Introduction, we consider three types of distributions for the random variable :

-

•

Model A: follows a shifted Geometric distribution with parameter .

The pdf of the Geometric copula is given by(24) where and

which yields the following pseudo log-likelihood function

-

•

Model B: follows a Shifted Poisson distribution with parameter .

The pdf of the shifted Poisson copula is of the form(25) where with and

The corresponding pseudo log-likelihood of the above copula is thus given by

-

•

Model C: follows a Truncated Poisson distribution with parameter .

The joint density of the truncated Poisson copula is given by(26) where

The resulting pseudo log-likelihood of the above copula can be written as follows

Remarks 4.1.

The copula of Model A and Model B include the corresponding original copula . In particular, if the pdf in (24) becomes the pdf of the original copula , see e.g., Zhang and Lin (2016), while the copula of Model B reduces to the original copula when .

Next, we generate random samples from the proposed copula models .

4.2. Monte Carlo Simulations

Based on the distributional properties of derived in Section 2, we have the following pseudo-algorithm for the simulation procedure which depends on the choice of and :

-

•

Step 1: Generate a value from .

-

•

Step 2: Generate random samples from the original copula .

-

•

Step 3: Calculate as follows

-

•

Step 4: Return , such that

Simulation results are important for exploring the dependence of . The simulation results in the table below complete those presented already in Table 1. In this regard, we generate random samples from the Joe copula with parameter .

| : Joe copula with | ||||

|---|---|---|---|---|

| 10 | 0.8982 | 0.8194 | 0.9849 | 0.9504 |

| 100 | 0.9005 | 0.8190 | 0.9857 | 0.9509 |

| 1’000 | 0.8997 | 0.8164 | 0.9855 | 0.9492 |

| 10’000 | 0.9004 | 0.8209 | 0.9857 | 0.9520 |

| 100’000 | 0.8999 | 0.8206 | 0.9852 | 0.9513 |

For the Joe copula, the Pickands dependence function can be written as follows

where , and .

By using (15) and for and , we obtain and which are in line with the simulation results observed in Table 2 for and as increases.

Another benefit of our simulation algorithm is that we can assess the accuracy of our estimation method proposed above. Therefore, we simulate random samples of size from the copula with different distributions for : Model A, Model B and Model C and two types of copula for : the Gumbel copula and the Joe copula. Hereof, the parameters of and of are estimated from the dataset described in Subsection 5.1 and are presented in Table 3 .

| : Joe copula | : Gumbel copula | |||

|---|---|---|---|---|

| Model for | ||||

| Model A | 0.3254 | 2.3727 | 0.7630 | 2.2758 |

| Model B | 0.9537 | 2.6634 | 0.1490 | 2.3276 |

| Model C | 1.8660 | 2.5885 | 0.3133 | 2.3240 |

| Model A | Model B | Model C | ||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Diff. | Diff. | Diff. | Diff. | Diff. | Diff. | |||||||

| 100 | 0.2461 | -24 | 2.2255 | -6 | 1.0765 | 13 | 2.6597 | 0 | 1.7400 | -7 | 2.2535 | -13 |

| 1’000 | 0.3353 | 3 | 2.3262 | -2 | 0.9906 | 4 | 2.6999 | 1 | 1.9238 | 3 | 2.6491 | 2 |

| 10’000 | 0.3304 | 2 | 2.3260 | -2 | 0.9795 | 3 | 2.6651 | 0 | 1.8996 | 2 | 2.5999 | 0 |

| 100’000 | 0.3285 | 1 | 2.3462 | -1 | 0.9541 | 0 | 2.6600 | 0 | 1.8721 | 0 | 2.5877 | 0 |

| Model A | Model B | Model C | ||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Diff. | Diff. | Diff. | Diff. | Diff. | Diff. | |||||||

| 100 | 0.9565 | 25 | 2.3595 | 4 | 0.1712 | 15 | 2.4308 | 4 | 0.3164 | 1 | 2.3675 | 2 |

| 1’000 | 0.7376 | -3 | 2.3076 | 1 | 0.1563 | 5 | 2.3458 | 1 | 0.3084 | -2 | 2.3126 | 0 |

| 10’000 | 0.7660 | 0 | 2.3083 | 1 | 0.1545 | 4 | 2.3476 | 1 | 0.3136 | 0 | 2.3185 | 0 |

| 100’000 | 0.7596 | 0 | 2.2639 | -1 | 0.1506 | 1 | 2.3232 | 0 | 0.3279 | 5 | 2.3063 | -1 |

4.3. Influence of on total loss

In this subsection, we focus on the distribution of the aggregate claim of two insurance portfolios by excluding the largest claim of each portfolio. Specifically, we analyse the aggregate influence of on some risk measures of the total loss . Moreover, by considering the joint distribution of we quantify the individual impact of and on the distribution of . Let be the aggregate claim excluding the largest claims, based on some risk measure and suppose that ’s have a finite second moment, the influence of the largest claims on the aggregate claim is evaluated as follows

By the covariance capital allocation principle, the contribution of on the change of the distribution of is given by

To illustrate our results we have implemented the following simulation pseudo-algorithm:

-

•

Step 1: Generate the number of claims from .

-

•

Step 2: Generate random samples from the original copula .

-

•

Step 3: For each portfolio, simulate claim sizes by using the inverse method as follows

where is the df of and , respectively.

-

•

Step 4: Evaluate the total loss with and without the largest claims, respectively

To obtain the simulated distribution of and Step 1-4 are repeated times . The results presented in Table 6 is in million and is obtained from the following assumptions:

-

•

number of simulations ,

-

•

the original copula is a Gumbel copula with dependence parameter ,

-

•

the number of claims follows the Shifted Poisson (Model B) with parameter

-

•

the claim sizes are Pareto distributed as follows

| Risk measures | (in ) | |||||

|---|---|---|---|---|---|---|

| Mean | 101.77 | 100.21 | 1.57 | 1.54 | 0.38 | 1.19 |

| Standard deviation | 4.41 | 3.91 | 0.50 | 11.24 | 0.15 | 0.35 |

| VaR (99 %) | 112.75 | 109.65 | 3.10 | 2.74 | 0.90 | 2.20 |

| TVaR (99 %) | 117.08 | 111.03 | 6.05 | 5.17 | 1.75 | 4.30 |

It can be seen that a significant proportion of the aggregate claims is consumed by . For instance, based on the standard deviation as risk measure, of the total loss is driven by the largest claims. In this regards, has more important contribution to than . This result is helpful for the insurance company when choosing the appropriate reinsurance treaty in the sense that the main source of volatility of the correlated portfolios is quantified.

5. Real insurance data applications

In this section, we illustrate the applications of the new copula families in the modelling of three real insurance data. Specifically, we shall consider four copula families for : Gumbel, Frank, Student and Joe and three mixture copulas in which with parameter follows one of the three distributions: Shifted Geometric, Shifted Poisson and Truncated Poisson. The AIC criteria is used to assess the quality of each model fit relative to each of the other models.

5.1. Loss ALAE from accident insurance

We shall model real insurance data from a large insurance company operating in Switzerland. The dataset consists of 33’258 accident insurance losses and their corresponding allocated loss adjustment expenses (ALAE) which includes mainly the cost of medical consultancy and legal fees. The observation period encompasses the claims occuring during the accident period 1986-2014222Data set can be downloaded here

http://dx.doi.org/10.13140/RG.2.1.1830.2481.

Let be the loss observed and its corresponding ALAE.

Some statistics on the data are summarised in Table 7.

| Loss | ALAE | |

|---|---|---|

| Min | 10 | 1 |

| Q1 | 13’637 | 263 |

| Q2 | 32’477 | 563 |

| Q3 | 95’880 | 1’509 |

| Max | 133’578’900 | 2’733’282 |

| No. Obs. | 33’258 | 33’258 |

| Mean | 292’715 | 5’990 |

| Std. Dev. | 2’188’622 | 42’186 |

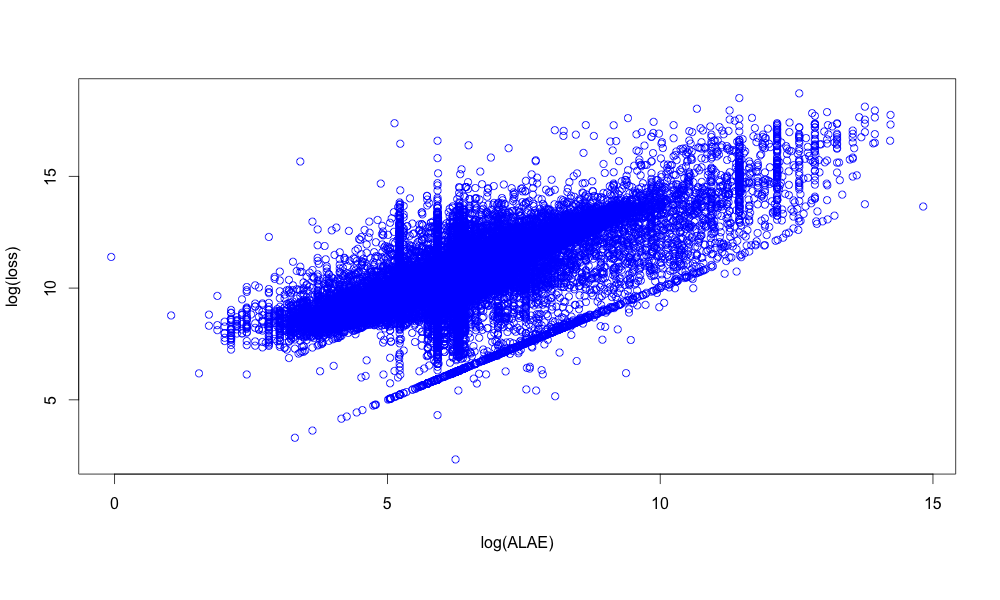

The scatterplot of (ALAE, loss) on a log scale is depicted in Figure 1. It can be seen that large values of loss is likely to be associated with large values of ALAE. In addition, the empirical estimator of some dependence measures in Table 8 suggests a positive dependence between and . For instance, the empirical estimator of the upper tail dependence of 0.6869 indicates that there is a strong dependence in the tail of the distribution of and .

| Pearson’s Correlation | 0.7460 |

|---|---|

| Spearman’s Rho | 0.7465 |

| Kendall’s Tau | 0.6012 |

| Upper tail dependence | 0.6869 |

Referring to the marginal’s estimator in (22), the estimation results for each copula model are found by maximizing (23) and are summarized in Table 9 below.

| Model | AIC | |||

|---|---|---|---|---|

| Gumbel | - | 2.3876 | - | -32’073 |

| Gumbel Geometric | 0.7630 | 2.2758 | - | -32’128 |

| Gumbel Truncated Poisson | 0.3133 | 2.3240 | - | -32’104 |

| Gumbel Shifted Poisson | 0.1490 | 2.3276 | - | -32’059 |

| Frank | - | 8.0774 | - | -30’137 |

| Frank Geometric | 0.9999 | 8.0772 | - | -30’134 |

| Frank Truncated Poisson | 0.0001 | 8.0773 | - | -30’135 |

| Frank Shifted Poisson | 0.0001 | 8.0773 | - | -30’135 |

| Student | - | 0.8142 | 1.9805 | -32’909 |

| Student Geometric | 0.1137 | 0.5492 | 1.9992 | -38’088 |

| Student Truncated Poisson | 0.0001 | 0.7841 | 9.6744 | -28’672 |

| Student Shifted Poisson | 0.0001 | 0.7885 | 8.7113 | -29’042 |

| Joe | - | 3.0967 | - | -30’655 |

| Joe Geometric | 0.3254 | 2.3727 | - | -33’015 |

| Joe Truncated Poisson | 1.8660 | 2.5885 | - | -32’578 |

| Joe Shifted Poisson | 0.9537 | 2.6634 | - | -32’411 |

It can be seen that the model which best fits the data is the Student Geometric copula followed by the Joe Geometric copula. We note in passing that the Student copula has an additional parameter which is the degree of freedom.

5.2. Loss ALAE from general liability insurance

This data set describes the general liability claims associated with their ALAE retrieved from the Insurance Services Office available in the R package. In this respect, the sample consists of 1’466 uncensored data points and 34 censored observations. We refer to Denuit et al. (2006) for more details on the description of the data. Let be the loss observed and the ALAE associated to the settlement of . Each loss is associated with a maximum insured claim amount (policy limit) . Thus, the loss variable is censored when it exceeds the policy limit . We define the censored indicator of the loss variable by

Next, we shall use the Kaplan-Meir estimator to estimate and the empirical distribution for as in (22). In particular, the corresponding pseudo log-likelihood function is given by

| (27) |

where

and for , see Denuit et al.(2006).

By maximizing (27), the resulting estimators of for the considered copula models are presented in Table 10.

| Model | AIC | |||

|---|---|---|---|---|

| Gumbel | - | 1.4284 | - | -210.18 |

| Gumbel Geometric | 0.5425 | 1.3127 | - | -278.23 |

| Gumbel Truncated Poisson | 0.0001 | 1.4422 | - | -360.49 |

| Gumbel Shifted Poisson | 0.1410 | 1.4083 | - | -361.20 |

| Frank | - | 3.0440 | - | -321.44 |

| Frank Geometric | 0.7800 | 2.7464 | - | -174.40 |

| Frank Truncated Poisson | 0.0001 | 3.0375 | - | -306.40 |

| Frank Shifted Poisson | 0.0001 | 3.0375 | - | -306.41 |

| Student | - | 0.4642 | 10.0006 | -180.99 |

| Student Geometric | 0.7095 | 0.4252 | 9.1897 | -228.82 |

| Student Truncated Poisson | 1 | 0.4094 | 13.9922 | -271.40 |

| Student Shifted Poisson | 1 | 0.4016 | 13.9983 | -295.42 |

| Joe | - | 1.6183 | - | -179.00 |

| Joe Geometric | 0.4379 | 1.3864 | - | -292.41 |

| Joe Truncated Poisson | 0.0607 | 1.6356 | - | -331.21 |

| Joe Shifted Poisson | 0.8075 | 1.4629 | - | -361.76 |

Since the Joe Shifted Poisson copula has the the smallest AIC it represents the best model for describing the dependence in the dataset followed by the Gumbel Shifted Poisson copula.

5.3. Danish fire insurance data

The corresponding data set describes the Danish fire insurance claims collected from the Copenhagen Reinsurance Company for the period 1980-1990. It can be retrieved from the following website: . This data set has first been considered by Embrechts et al. (1998) (Example 6.2.9) and explored by Haug et al. (2011). It consists of three components: loss to buildings, loss to contents and loss to profit. However, in this case, we model the dependence between the first two components. The total number of observations is of 1’501. We only consider the observations where both components are non-null.

As indicated by the empirical dependence measures in Table 11, the level of dependence between these two losses is low.

| Pearson’s Correlation | 0.1413 |

|---|---|

| Spearman’s Rho | 0.1417 |

| Kendall’s Tau | 0.0856 |

| Upper tail dependence | 0.1998 |

The estimation results for each copula is summarized in Table 12 below.

| Model | AIC | |||

|---|---|---|---|---|

| Gumbel | - | 1.1762 | - | -133.18 |

| Gumbel Geometric | 0.9999 | 1.1762 | - | -131.17 |

| Gumbel Truncated Poisson | 0.0001 | 1.1762 | - | -131.18 |

| Gumbel Shifted Poisson | 0.0001 | 1.1762 | - | -131.17 |

| Frank | - | 0.8807 | - | -29.12 |

| Frank Geometric | 0.9999 | 0.8804 | - | -27.12 |

| Frank Truncated Poisson | 0.0001 | 0.8806 | - | -27.12 |

| Frank Shifted Poisson | 0.0001 | 0.8805 | - | -27.12 |

| Student | - | 0.1574 | 9.5998 | -47.86 |

| Student Geometric | 0.9999 | 0.1576 | 10.0063 | -45.84 |

| Student Truncated Poisson | 0.0001 | 0.1570 | 9.0048 | -45.81 |

| Student Shifted Poisson | 0.0001 | 0.1562 | 8.9833 | -45.42 |

| Joe | - | 1.3585 | - | -204.85 |

| Joe Geometric | 0.9999 | 1.3585 | - | -202.83 |

| Joe Truncated Poisson | 0.0001 | 1.3585 | - | -202.84 |

| Joe Shifted Poisson | 0.0001 | 1.3585 | - | -202.83 |

It can be seen that the model that best fits the data is the Joe copula followed by the Joe Truncated Poisson copula. The Frank mixture copulas and Student mixture copulas are not a good fit for the data as their AIC is higher by far compared to the Gumbel and Joe mixture copulas families.

5.4. Reinsurance premiums

In this section, we examine the effects of the dependence structure on reinsurance premiums by using the proposed copula models. In practice, it is well known that insurance risks dependency has an impact on reinsurance. For instance, Dhaene and Goovaerts (1996) have shown that stop loss premium is greater under the dependence assumption than under the independence case. In what follows, we consider the insurance claims data described in Subsection 5.1 where we denote the loss variable, the associated ALAE and the number of claims for the next accident year. In addition, two types of reinsurance treaties are analyzed namely:

-

•

Excess-of-loss reinsurance, where the claims from ’s are attributed proportionally to the insurer and the reinsurer. For a given observation the payment for the reinsurer is described as follows, see Cebrian et al. (2003)

leading to a reinsurance premium of the form

(29) where is the retention level.

-

•

Stop loss reinsurance, where the premium is given by

(30) and is a positive deductible.

In order to calculate the reinsurance premiums defined above, Monte Carlo simulations have been implemented. Hereof, we assume that is Poisson distributed with a mean of , representing the expected number of claims estimated by the insurance company. Additionally, we use the empirical distributions of and for the simulation of the claims amount. Regarding the dependence model, the following copulas are considered: independent copula, Joe copula, Geometric Joe Copula, Truncated Poisson Joe copula and the Shifted Poisson Joe copula where the parameters are summarized in Table 9. The following steps summarize the implemented pseudo-algorithm:

-

•

Step 1: Generate the number of claims .

-

•

Step 2: Simulate from the considered copula .

-

•

Step 3: Generate the loss and ALAE claims as follows

where and are the inverse of the empirical df of and respectively, with

- •

-

•

Step 5: Step 1 -Step 4 are repeated times and the estimators of the reinsurance premiums are given by

The estimation results presented in Table 13 are obtained from repeating Step 1 -Step 4 100’000 times. These amounts are expressed in CHF million.

| Copula model | ||||||

|---|---|---|---|---|---|---|

| Independent | 13.1137 | 6.5692 | 3.0971 | 14.7530 | 7.5145 | 3.5738 |

| Joe | 13.6950 | 6.7776 | 3.2396 | 15.1056 | 7.7691 | 3.8233 |

| Joe Geometric | 13.4483 | 6.7365 | 3.1619 | 14.8975 | 7.6797 | 3.7177 |

| Joe Truncated Poisson | 13.4038 | 6.7183 | 3.0929 | 14.8016 | 7.6698 | 3.6493 |

| Joe Shifted Poisson | 13.4776 | 6.6789 | 3.1081 | 14.9250 | 7.6266 | 3.6702 |

Table 13 shows that the reinsurance premiums and are lower under the independence hypothesis. Hence, the portfolio is less risky when the loss variable and the ALAE variable are assumed to be independent.

Furthermore, when the retention limit increases for the excess of loss treaty, the reinsurance premiums estimates under the Joe mixture copula models tend to the estimated values under the independence assumption. Conversely, for the stop loss treaty, the higher the deductible the higher the deviation from the independence hypothesis.

Furthermore, by comparing the results for each copula model, it can be seen that the Joe copula generates the highest reinsurance premiums. This result is expected given that the strongest dependence structure is obtained under the Joe copula. On the other hand, the weakest dependence model for this data is observed under the Joe truncated Poisson copula as the reisurance premiums and are the smallest for different values of and .

6. Appendix

6.1. Proofs

Derivation of (25)-(26): We show first (7). The corresponding joint density of the df is given by

| (31) |

where

In view of (31), the partial derivative of with respect to is

leading to

We derive next the pdf in (25): In this case, follows a shifted Poisson distribution. In view of (7), we need to compute at first the following components:

where for , which implies and thus By replacing these components into (7), we have

Next, we show (26): Since follows a truncated Poisson distribution, in light of (7), the joint density is expressed in terms of (set )

where for , and with By substituting the above components in the joint density expressed in (7), we obtain

Proof of Proposition 3.1

Since has Fréchet marginals, by assumption (11), we have that

where has copula and thus . We have thus with using further (9)

| (32) |

for any such that and . Consequently,

where the convergence above follows by Lemma 4.2 in Hashorva (2007) (see also Resnick and Zeber (2013) and Kulik and Soulier (2015) for more general results). Next, the convergence in (32) implies

for any such that , where is the th marginal df of , and , respectively. Hence, with similar arguments as above, we have

establishing the proof.

Proof of Proposition 3.2 For we have

By the assumption that is finite we have

| (33) |

Since further

and then using (6) and (33) we obtain

hence the first claim follows. Next, in view of (16) we have

hence as

Let be non-negative constants such that . By the above and (33)

as . Setting now we have thus as

establishing the proof.

For our study, we consider several copula families for , which are described hereafter.

6.2. Gumbel Copula

The df of a Gumbel copula with a dependence parameter is given by

by differentiating with respect to we have

and the corresponding joint density is expressed as follows

where .

6.3. Frank Copula

The df of a Frank copula with a dependence parameter is of the form

which yields the partial derivative of with respect to as follows

and the associated pdf is given by

6.4. Joe copula

The Joe copula with dependence parameter has df

Deriving with respect to we obtain

The associated pdf is obtained by differentiating with respect to and leading to

where .

6.5. Student Copula

Let be the df of a Student random variable with degree of freedom and write for its inverse. The df of the Student copula, with correlation and degree of freedom can be expressed as follows

Its partial derivative with respect to is given by

whereas the corresponding pdf is

where for

Acknowledgments. Thanks to reviewers and the Editor for several suggestions. E. Hashorva is partially supported by the Swiss National Science Foundation grants 200021-13478, 200021-140633/1. G. Ratovomirija is partially supported by the project RARE -318984 (an FP7 Marie Curie IRSES Fellowship) and Vaudoise Assurances.

References

- [1] Ammeter, H. (1964). Note concerning the distribution function of the total loss excluding the largest individual claims. Astin Bulletin, 3(02), 132–143.

- [2] Asimit, A.V. and Chen, Y. (2015). Asymptotic results for conditional measures of association of a random sum. Insurance: Mathematics & Economics, 60, 11–18.

- [3] Aulbach, S. , Falk, M, Hofmann, M. & Zott, M. (2015). Max-stable processes and the functional -norm revisited. Extremes, 18(2), 191–212.

- [4] Aulbach, S. , Falk, M. & Zott, M. (2015). The space of -norms revisited. Extremes, 18(1), 85–97.

- [5] Bücher, A. & Segers, J. (2014). Extreme value copula estimation based on block maxima of a multivariate stationary time series. Extremes, 17(3), 495–528.

- [6] Cebrian, A.C. , Denuit, M. & Lambert, P. (2003). Analysis of bivariate tail dependence using extreme value copulas: An application to the SOA medical large claims database. Belgian Actuarial Journal, 3(1), 33–41.

- [7] Denuit, M., Dhaene, J., Goovaerts, M. & Kass, R. (2006). Actuarial Theory for Dependent Risks: Measures, Orders and Models. Chichester: John Wiley & Sons.

- [8] Denuit, M., Purcaruff, O. & Van Keilegorni, I. (2006). Bivariate Archimedean copula models for censored data in non-life insurance. Journal of Actuarial Practice, 13.

- [9] Dhaene, J. & Goovaerts, M.J. (1996). Dependency of risks and stop-loss order. Astin Bulletin, 26(02), 201–212.

- [10] Embrechts, P. (2009). Copulas: a personal view. Journal of Risk and Insurance, 76(3), 639–650.

- [11] Embrechts, P., Klüppelberg, C. & Mikosch, T. (1998). Modelling extremal events for insurance and finance. Astin Bulletin, 28(02), 285–286.

- [12] Falk, M., Hüsler, J. & Reiss, R.D. (2010). Laws of Small Numbers: Extremes and Rare Events. Springer Science & Business Media.

- [13] Genest, C., Gendron, M. & Bourdeau-Brien, M. (2009). The advent of copulas in finance. The European Journal of Finance, 15(7-8), 609–618.

- [14] Genest, C., Ghoudi, K. & Rivest, L.P. (1995). A semiparametric estimation procedure of dependence parameters in multivariate families of distributions. Biometrika, 82(3), 543–552.

- [15] Hashorva, E. (2007). Extremes of conditioned elliptical random vectors. Journal of Multivariate Analysis, 98(8), 1583–1591.

- [16] Haug, S., Klüppelberg, C. & Peng, L. (2011). Statistical models and methods for dependence in insurance data. Journal of the Korean Statistical Society, 40(2), 125–139.

- [17] Kim, G., Silvapulle, M.J. & Silvapulle, P. (2007). Comparison of semi-parametric and parametric methods for estimating copulas. Computational Statistics and Data Analysis, 51(6), 2836–2850.

- [18] Kulik, R. & Soulier, P. (2015). Heavy tailed time series with extremal independence. Extremes, 18(2), 273–299.

- [19] Molchanov, I. (2008). Convex geometry of max-stable distributions. Extremes, 11(3), 235–259.

- [20] Nelsen, R.B. (1999). An Introduction To Copulas . New York: Springer-Verlag.

- [21] Oakes, D. (1989). Bivariate survival models induced by frailties. Journal of the American Statistical Association, 84(406), 487–493.

- [22] Peng, L. (2014). Joint tail of ECOMOR and LCR reinsurance treaties. Insurance: Mathematics & Economics, 58, 116–120.

- [23] Resnick, S.I. & Zeber, D. (2013). Asymptotics of Markov kernels and the tail chain. Advances in Applied Probability, 45(1), 186–213.

- [24] Zhang , K. & Lin, J. (2016). A new class of copulas involved geometric distribution: Estimation and applications. Insurance: Mathematics & Economics, 66, 1–10.