Exponentially concave functions and high dimensional stochastic portfolio theory

Abstract.

We consider the following problem in stochastic portfolio theory. Are there portfolios that are relative arbitrages with respect to the market portfolio over very short periods of time under realistic assumptions? We answer a slightly relaxed question affirmative in the following high dimensional sense, where dimension refers to the number of stocks being traded. Very roughly, suppose that for every dimension we have a continuous semimartingale market such that (i) the vector of market weights in decreasing order has a stationary regularly varying tail with an index between and and (ii) zero is not a limit point of the relative volatilities of the stocks. Then, given a probability arbitrarily close to one, two arbitrarily small , and an arbitrarily high positive amount , for all high enough dimensions, it is possible to construct a functionally generated portfolio such that, with probability at least , its relative value with respect to the market at time is at least , and never goes below during . There are two phase transitions; if the index of the tail is less than or larger than . The construction uses properties of regular variation, high-dimensional convex geometry and concentration of measure under Dirichlet distributions. We crucially use the notion of convex functions introduced by Erbar, Kuwada, Sturm [EKS15] in the context of curvature-dimension conditions and Bochner’s inequalities.

Key words and phrases:

Stochastic portfolio theory; relative arbitrage; short term arbitrage; exponentially concave functions; high-dimensional finance; Dirichlet concentration2000 Mathematics Subject Classification:

60J60; 60J70; 60J35; 91B281. Introduction

We start by recalling the usual set-up of stochastic portfolio theory. See the survey [FK09] for more details. Although we will use words such as portfolio, market, and stocks for alluding to their economic interpretation, no knowledge of these quantities are required for understanding the mathematical problem that follows. At a purely mathematical level we will be studying universal properties of stochastic integrals in high dimensions. However, the economic terminology will give us a real world interpretation of an interesting high-dimensional phenomenon.

Our state space is the open unit simplex in , , defined by

| (1) |

The dimension represents an equity market that has stocks. We consider time to be continuous. At any point of time , let be the market capitalization of stock (i.e., the total dollar amount raised through the shares) at time . Our primary focus is the market weight of stock , defined by

| (2) |

The vector is called the market at time . As time varies we have a function on . We will throughout assume a model under which is a continuous semimartingale.

At this point we will impose an extra structure over the usual set-up. We will assume that there exists a sequence of semimartingales . That is, we have a market for every dimension. It is possible to have them on different probability spaces, but for notational convenience we will assume that they are all represented on a single filtered probability space . This can be done without loss of generality. For , we have a trivial situation. To avoid constantly make exception to this case, we will let refer to the set . For any , we define a portfolio in dimension to be an -predictable process with state space , the closure of . In finance, this represents a self-financing long-only portfolio. The th coordinate of represents the fraction of its current value invested in stock . Here, the value or the wealth process of the portfolio refers to the growth (or decay) of invested in the portfolio at time zero.

The only class of portfolios we will be interested in is one where we have a function , where the range is the closed unit simplex. In other words, we define the following adapted process by applying the portfolio function on the current market weights. This gives us a portfolio . For example, if we take the identity map , then this portfolio is called the market portfolio. Its value can be thought of as a capitalization-weighted index (such as S&P 500 or Russell 1000) which represents the performance of the entire market.

What we are interested is the relative value of a portfolio with respect to the market portfolio, defined as the ratio of the value of the portfolio over that of the market portfolio. We will denote this relative value process by where . This process can be written as an exponential stochastic integral of the following form:

where for a continuous semimartingale is the process .

We now recall the definition of relative arbitrage from [FK09, page 113]. A portfolio is said to be a relative arbitrage (or, more colloquially, beats the market) if there is a time and a such that

We will now introduce a new definition by relaxing the above requirement.

Definition 1.

(Asymptotic short term relative arbitrage) We say that a sequence is an asymptotic short term relative arbitrage (ASTRA) opportunity if there are two sequences of positive numbers and such that

-

(i)

and .

-

(ii)

such that for all .

-

(iii)

Moreover, we have .

The definition of ASTRA is similar to that of asymptotic arbitrage introduced in [KK94] and studied further in [KS96], [KK98], [Kle00], and [CKT14].

Our main result shows the existence of such ASTRA opportunities under the following assumptions. A more general version involving regularly varying sequences appear as Theorem 13. Fix . Suppose is given by the coordinates

Plainly, has an asymptotic Pareto or Zipf distribution tail with slope . For a definition of Pareto or Zipf distribution see [SMS09]. Let refer to the Dirichlet probability distribution on with parameter .

Assumption 1.

We assume that there exists a positive sequence such that

and the following conditions hold.

-

(i)

(Initial Dirichlet distribution of norm) Consider the process . We assume that has the same distribution as when . Since the labeling of coordinates is arbitrary, the above statement demands some labeling of coordinate for which it is true.

-

(ii)

(Escape times are not too fast) Define , where . It has been proved later that . We assume that for all , the probability

-

(iii)

(Volatility bounded away from zero) We will assume that there is a positive constant such that, for all and all , we have

(3) Here refers to the mutual or quadratic variations of two semimartingales.

In Section 6 we show that the stationary Wright-Fisher diffusion model with invariant distribution or its deterministic time changes that runs times more slowly satisfy all the assumptions above. In stochastic portfolio theory, the Wright-Fisher model appears as the law of the market weights under the volatility-stabilized market models. See [FK05, Pal11].

The statements of our main results are slightly different depending on whether or whether . We will call the former case as the subcritical case, and the latter as the critical case. Define

Theorem 1.

Suppose we are given an . There exists a sequence of explicit portfolios and numbers , independent of , such that the following hold under Assumption 1.

-

(i)

Almost surely, for every .

-

(ii)

In the subcritical case, there exists a sequence satisfying , for some positive constant and such that

for some positive constant .

-

(iii)

In the critical case, there exists a sequence which satisfies for some positive constant , such that

It can be easily verified (will be shown later) that . Thus, is an ASTRA opportunity under our assumptions. Every portfolio is essentially a functionally generated portfolio and therefore explicit. Functionally generated portfolios are given as functions , where can be described as a gradient map of the logarithm of a positive concave function on the unit simplex. We recall the notion in Section 3. Also see [PW15] for its connection to optimal transport and the geometry of the unit simplex.

The idea of the construction is the following. In every dimension we construct a positive concave function around that is highly concave in every direction in a certain sense. However, this requires the diameter of the domain of the function to be . Although the diameter of the unit simplex is in every dimension, its ‘typical diameter’ under is about for large . Thus, such a concave function can be effectively constructed on a large enough subset of . By our assumption, the process spends a significant amount of time before its first exit from this large subset with a high probability. These facts, along with the increasing difference between the and norms of regularly varying sequences, gives the portfolio a very large relative value.

The proofs break down if either or . The latter case is understandable. The extreme inequality in the market weights effectively reduces the dimensionality of the problem. Since most volatility is generated by the largest market weights, increasing dimension gives us little advantage. The case of is more mysterious. This is the case of too little inequality and is probably related to the fact (see [Won15, Theorem 1]) that the equal-weighted portfolio () is optimal in a certain sense around a neighborhood of the barycenter of the unit simplex . It will be interesting to understand this transition better.

1.1. Discussion and comparison with previous work

The existence of relative arbitrage portfolios goes against the no-arbitrage theory that has been the fundamental assumption in mathematical economics and finance. However, Robert Fernholz [Fer99], [Fer02, Section 3.3] observed that such portfolios do exist under observable conditions in real-world markets (which martingales do not satisfy). See also [FK05] and [FKK05].

Fernholz assumed an Itô process satisfying two conditions. (i) such that . This condition is called diversity. And, (ii) a uniform nondegeneracy condition of the diffusion coefficient. This condition is called being sufficiently volatile. He then showed that exist explicit portfolio maps such that , irrespective of the law of .

The time that it takes to beat the market is of central importance. A natural question to ask is whether, given any small , there exists a relative arbitrage portfolio such that with probability one. The challenge, as in any problem of stochastic portfolio theory, is to make as few assumptions (preferably observable) as possible on the market process. Several recent articles have tried to resolve this question. In [FKK05], it was shown that such portfolios do exist under the condition of diversity. However, the solution is not practical, since to make any significant gain from those portfolios we require an astronomical initial investment. The authors also mention the difficulties of implementation on [FKK05, page 16].

Another solution was posed by [BF08], inspired by the previous work [FK05] under the condition that the smallest stock in the market has an extreme volatility. To describe their result, define volatility of market weights by . Then, [BF08] assumes that . In particular, let refer to the index such that . Since , then and is growing linearly with dimension . This leads to extreme fluctuation of lower ranked stocks in high dimension which is a drawback of this approach. Moreover, the amount of outperformance by this portfolio is super-exponentially small in the time to beat the market, as remarked on [BF08, page 451].

Recently, another solution has been proposed by Fernholz in [Fer15] where it is assumed that the entropy of the market weights satisfy an almost sure time-homogeneity property. As with the previous solutions, the outperformance is not significant enough for these portfolios to be feasible.

On a complimentary note, Fernholz, Karatzas, and Ruf [FKR15] have shown examples in finite dimensions where short-term relative arbitrages do not exist.

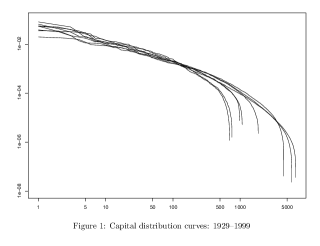

Let us justify our assumptions. Consider condition (i) in Assumption 1. It is well-known that market weights have Pareto tails. See Figure 1 which is taken from [Fer02]. Each curve represents log of ranked market weights in decreasing order against log of the rank, sampled once every decade from all major U.S. stock markets for eight decades. The curves are roughly linear, and hence the market weights are roughly Pareto, where the qualifier ‘some labeling’ in condition (i) refers to rearrangement according to decreasing size. The appearance of Zipf distribution is not an isolated incident. Pareto tail are ubiquitous in econometric data. See the articles [Axt01] and [Gab09], the book [SMS09], or the post [Tao09]. In Section 6, we work with real data from June to December of 2015. The Pareto curve with a slope in remains valid as can be seen in Figure 2.

Thus, for any , there exists some labeling of coordinates which makes the sequence approximately Pareto. The factor in reflects the natural scale of fluctuation. One way to think about it is that the uniform distribution over is where . Our is the same exponential family as the uniform distribution and keeps the same natural scaling. As will be clear from the proofs, our statements can be generalized to the case of , for some positive constant .

Consider condition (ii). Since Pareto is a stable configuration for the market weights, it cannot escape from a neighborhood of very fast. This is supported by real data as shown in Figure 3.

Condition (iii) is a weaker requirement that the condition that the relative volatilities of the stocks is bounded away from zero. To wit, suppose

then (3) follows by Itô’s rule. Hence, our condition is similar to but much weaker than the condition of Fernholz’s uniform nondegeneracy condition of the diffusion matrix of .

In Section 6 we show that the stationary Wright-Fisher diffusion whose invariant distribution is satisfy our assumptions. We also justify our assumptions on recent real data (Russell 1000, Jun-Dec 2015) and test the performance of our portfolio for .

1.2. Outline

Our results are true when the market weights decay as a regularly varying sequence of a range of indices. We recall the notion of regularly varying sequences in Section 2. In Section 3 we introduce the notion of exponentially concave functions and relate them the recent notion of convexity from [EKS15]. We also recall the concept of functionally generated portfolios. In Section 4, we prove a concentration of measure theorem for Dirichlet distributions with regularly varying parameters. In Section 5 we combine the ideas to prove a much more generalized version of Theorem 1. Finally in Section 6 we provide theoretical models that satisfy our assumptions and show that the strategy works on real market data.

2. Preliminaries

2.1. Notations on orders of magnitude

We will throughout use the following standard notations. The letters and will always refer to positive constants. No two occurrences might refer to the same constant, unless otherwise stated or is obvious.

For any two sequences of positive numbers and the following hold.

-

(i)

means that for some positive constant .

-

(ii)

means .

-

(iii)

means that for some positive constant .

-

(iv)

means for some positive constants .

-

(v)

mean .

2.2. Regularly varying sequences

Consider a non-increasing sequence in . We will denote the th partial sequence by . Define the usual norms by

If is suppressed from the norm notation, , then, is assumed to be .

We will use the following notations:

-

(i)

for the norm .

-

(ii)

And, for the ratio of the norm over the square of the norm:

(4)

The number can be thought of as a measure of inequality among the coordinates of . We will work under the following assumption on the sequence that require the coordinates of to decrease fast but not too fast.

Assumption 2.

We assume the following regarding our sequence .

-

(i)

.

-

(ii)

Moreover, we require

The primary example we will follow throughout this paper is the following. Fix and consider the sequence . Then . We will call this sequence as the hyperharmonic sequence. The name harmonic sequence will be reserved for the case of .

Clearly, condition (i) in Assumption 2 is satisfied only when . In that regime, we will throughout employ the following asymptotic estimate:

| (5) |

Now, . Thus, if , we have

| (6) |

Hence, condition (ii) of Assumption 2 holds as well. In fact, it continues to hold at when and , and hence

| (7) |

However, when , we get

Hence, condition (ii) on Assumption 2 fails. Thus, Assumption 2 is valid for the range but not elsewhere.

To generalize the above calculations for other sequences we need to assume more regularity conditions on our sequence . We begin by recalling the definition of regularly varying sequences introduced in [GS73].

Definition 2.

We call a sequence of positive terms to be regularly varying with index if there is another positive sequence such that

-

(i)

, for some positive constant ,

-

(ii)

and .

When we call the sequence slowly varying.

Regularly varying sequences admit a Karamata representation in the spirit of regularly varying functions on the positive half line. The following result is from [GS73, Section 2].

Theorem 2.

If is a regularly varying sequence of index then it has the representation

| (8) |

where and . Here can be taken to be the sequence .

Remark 1.

For , let . The hyperharmonic sequence is a regularly varying sequence of index . Here, we take . The fact that it satisfies the definition is the consequence of the estimate (5). Notice that, for , we have

In that case, we can take and representation (8) is valid for the choice (say) , .

Lemma 3.

Proof.

Condition (i) follows from the result in [GS73] that regularly varying sequences can be embedded in regularly varying functions by defining on . However, regular varying functions with a positive index diverge at infinity.

For condition (ii) we note that for every . Hence . On the other hand

Hence, by our assumption of regular variation, . Therefore,

the last bound is due to the fact that . When , it follows from Karamata representation that .

∎

The case of slowly varying sequences have to be dealt separately since sequences that admit finite positive limits are also slowly varying and do not satisfy Assumption 2 (i). Moreover, as we see from (7), the case of is also delicate due to the presence of logarithmic terms. For these two boundary cases, we will make appropriate assumptions later in the text. In any case, for the rest of the text we will always assume that the sequence is such that is regularly varying of index and satisfies Assumption 2.

3. exponentially concave functions

We begin with a definition. 111Thanks to Prof. W. Schachermayer for suggesting this apt definition.

Definition 3.

A real-valued function on an open convex domain in is said to be exponentially concave if is a concave function on . For usual practices in convex analysis, we will assume our functions to take the value outside their domains, thereby extending them to the entire space.

As shown in [PW15], the gradient maps of the above class of functions arise as solutions to a novel and interesting optimal transport problem. Independently, the closely related concept of convexity has been very recently introduced in an article by Erbar, Kuwada, and Sturm [EKS15]. It is related to the curvature-dimension condition ( standing for a lower bound on the Ricci curvature while is an upper bound on the effective dimension) and leads to fascinating behavior of entropy over heat flows. For our purpose, we will modify the definition slightly.

Definition 4.

For and , a function is said to be exponentially concave if is a concave function on satisfying

The right hand side above represents the scalar multiplied with the identity matrix and the inequality is in the sense of two nonpositive-definite matrices. If the Hessian does not exist in the classical sense, interpret it as a measure in the sense of Alexandrov.

Alternatively, one can write the above as

The above inequality is the usual ordering of two nonpositive-definite matrices.

We will focus exclusively on the case when and , the number of stocks. Thus, in , we will only consider exponentially concave functions. The following is a fundamental example.

Lemma 4.

For any , the function on the domain is exponentially concave.

Moreover, consider any exponentially concave function and let be its maximizer. Then, for any , the following inequality holds:

In particular, the domain of any exponentially concave function must be a subset of .

Proof.

For the first claim, it suffices to consider . Consider any two points and consider the line , , connecting the two. Let . Then

On our domain both and are positive. This observation and the Cauchy-Schwartz inequality implies that . Since this holds for every choice of , it proves our claim.

For the second claim, it is clear that the maximizer exists for this strictly concave function and that . If does not exist at , we do a standard approximation by approximating the function with infimal convolutions with a sequence of smooth convex functions. The claim now follows from [EKS15, Lemma 2.2, part (iii)] by considering, as before, the line . The cited lemma is itself a consequence of comparison theorem for one-dimensional concave functions considered as a function of over the geodesic .

The final statement is now obvious. ∎

Remark 2.

By a change of coordinates it is easy to see that the concept of can be generalized in the following way. Let be an nonnegative definite matrix. Define a norm . Consider the function over the domain . Then, satisfies the inequality

and is the maximal one satisfying the above in the sense of Lemma 4.

Definition 5.

Let be an exponentially concave function on whose domain includes . Assume is differentiable on its domain. We define a map by the following recipe. For every , let denote the gradient of at . Denote the coordinates of by . Then,

| (9) |

In other words, the vector of coordinate ratios is the projection of the gradient on the hyperplane .

The above portfolio can now be traded on process of market weights . Assume that is twice continuously differentiable on its domain. Let . Then the following expression for is known as the Fernholz’s decomposition formula. See [Fer02, Theorem 3.1.5].

| (10) |

Here and throughout, refers to the sum of all the elements of the Hadamard product of and the matrix of infinitesimal mutual variations . That is,

and is well-defined when considered as a measure. We will call the following nonnegative nondecreasing process to be the drift process:

We now define the class of portfolios which we will use to construct our ASTRA sequence.

Definition 6.

[Cosine portfolios] Fix , , a point and consider the portfolio generated by the exponentially concave function as per Definition 5. We will refer to this class of portfolios as the cosine portfolios.

4. The Dirichlet concentration

Suppose we are given a sequence as in Subsection 2.2. For every , consider the unit simplex in , given in (1). We can get an element in by defining .

Fix for some . Recall the Dirichlet distribution with parameter , denoted by . This is a probability distribution on the unit simplex given by the joint density at a point :

Here refers to the gamma function.

Consider a sequence satisfying Assumption 2. Consider a sequence of Dirichlet distributions with parameters , for . This Dirichlet distribution has mean and the same concentration as the uniform distribution over . In fact, if the following formulas hold

| (11) |

We start with the following proposition.

Proposition 5.

Consider the vector as above. Let and let . Then

| (12) |

Remark 3.

Since , we get is essentially in the interval for large enough .

Proof.

The upper bound follows from Jensen’s inequality:

The final inequality is due to the fact that .

For the lower bound, we note that the function is convex on . Thus, again by Jensen’s inequality, we get

| (13) |

We recall the following fact about the Beta distribution. Suppose for , then (see [Wal96, Page 14]):

The last approximation is due to Stirling’s formula.

Since each is distributed as , putting the above formula back in (13) we get

This completes the proof. ∎

Proposition 5 shows that the family of random variables has bounded mean. We will now prove concentration estimates for the distributions in this sequence around their means.

It is not hard to believe that if is distributed according to the uniform distribution on the unit simplex, then has exponentially decaying tails away from its mean. However, when itself is atypical for the uniform distribution this exponential decay starts failing.

We are now ready to prove our concentration estimate. As always, we will assume that is regularly varying of index . However, the proofs are somewhat different for the following two cases: (i) the subcritical case when , and (ii) the critical case when . We start with (i).

Suppose we are given the sequence . We will use the following well-known construction of Dirichlet random variables. Let be a sequence of independent gamma random variables of scale one such that . Let denote the sequence of their partial sums. Then the vector

is distributed as . It also follows that, independent of the vector of ratios above, is distributed as Gamma, a gamma random variable with mean and scale one.

We start with by a standard large deviation estimate of around its mean . The result is well-known but we include a short argument anyway.

Lemma 6.

Fix . For all we have

| (14) |

Proof of Lemma 6.

The convex conjugate of the log-moment generating function of is given by

For any consider to be the closed interval . Since is zero at , increasing on and decreasing on , then

We now use Cramér’s non-asymptotic bound (see Remark (c) on page 27 of [DZ98]). Fix . For any such that , we get

| (15) |

This completes the proof of the lemma. ∎

We now consider the subcritical case. Recall is distributed as and the notation refers to the -norm . Every concentration bound we prove below is for a two sided deviation around the mean, i.e., of the type

However, for simplicity of notations and keeping our application in mind, we will prove bounds on the following deviations

This suffices for our purpose since, by Proposition 5, lies in the interval for all large .

Proposition 7.

(The subcritical case) Suppose the sequence is regularly varying with index and . Then

| (16) |

for some choice of positive constant depending on the sequence.

A similar bound holds, possibly with different constants, for the probability

Proof.

Fix . Changing to the gamma random variables , we get that for every ,

| (17) |

Define the event . Then, by Lemma 6, we get

| (18) |

Define a sequence , . Then

We are going to partition the set in two parts and . We are going to treat the random variables and separately. Notice that, by our assumption on regular variation

| (19) |

Recall from [GS73], that can be embedded in a regularly varying sequence . It follows that (see [BGT89, Theorem 1.5.2, page 22]) that, for any , we have

uniformly for . Hence, by choosing , we get . Substituting in (19), we get

| (20) |

We are going to assume, for all large enough for any , we have , and, for any , we have . Of course, this may not be true at all. But, as will be apparent from the argument, one can repeat the argument by redefining such that , for , and , for , and then let to get the same bound.

Fix large enough for the above conditions to hold. Let and denote the vectors and , respectively. Similarly, partition in two parts, and .

Now, it is known that a gamma distribution with mean at least one, being a log-concave density, satisfies a Poincaré inequality: . If the mean is , the Poincaré constant can be taken to be . See, for example, [BW09, Remark 1, page 2716]. Since every , , has a mean of more than , by the tensorization property of the Poincaré inequality, their product measure satisfies a Poincaré inequality with a constant

The following concentration lemma is a special case of results on general modified log-Sobolev inequalities in [BL97]. See Theorem 3.1 and Corollary 3.2.

Lemma 8.

Consider an that satisfies

Then, with respect to the joint distribution of the following concentration estimate holds:

| (21) |

for some universal constant .

Proof.

We follow the statement in [Led97, Corollary 4.6, page 62] which essentially covers our claim. We simply remark on the superficial differences. The i.i.d. structure in the statement of [Led97, Corollary 4.6, page 62] is unimportant since the only thing that is used in the proof is the common Poincaré constant. This has been remarked right afterwards by the author. We now need to find an estimate of the constant . The constant appearing in [Led97, Corollary 4.6, page 62] is bounded by the constant ‘’ as mentioned in the remark following [Led97, Theorem 4.5, page 62] for . The rest follows from [Led97, Corollary 2.11, page 38] with a choice of and . ∎

For example, if we apply the above lemma to the function on which satisfies and . This gives us

| (22) |

By shifting the mean, the vector of independent coordinates also satisfies the Poincaré inequality with the same constant as above. Hence, we also get,

| (23) |

This covers the concentration of . We have to now give a separate argument for which is not covered by the above arguments.

For , every (say). Thus every , , is stochastically dominated by an exponentially distributed random variable with mean one. In particular, by the union bound,

| (24) |

Let be the event that every , for , is at most . Then, one the event , we for all .

Consider the vector . The law of this vector is a product measure on . The function , for some fixed , is a convex Lipschitz function on this space. We can now use Talagrand’s Gaussian concentration inequality for convex, Lipschitz functions on the unit cube ([Tal88], [Led97, Corollary 3.3]) to claim

Here refers to the vector .

We will now adjust the expectation above. By triangle inequality,

| (25) |

where is distributed as exponential with mean one, and the inequality is due to stochastic domination. However,

Using the trivial bound , we get from (25),

| (26) |

And, therefore, using (24) and with a little adjustment to the expectation above,

| (27) |

for all large .

Let ; thus . By our choice of and regular variation, we get

| (28) |

Now, by elementary bounds, we obtain

| (29) |

By Karamata representation, for any and any . Thus we can compress the bound on the right side above and write

| (30) |

for some positive constants .

Recall the event defined above (18), and the subsequent discussion. We get

| (31) |

Now, on the event , the following estimates hold:

Note that, by our assumption on the decay of , we get

We have already shown that is with exponentially decaying tail away from its mean. The other two terms are going to zero in probability at the rate of at least . Thus, it is not hard to see that that the same exponential tail holds for as in (30), possibly with different values of the constants . Thus,

| (32) |

We simplify the above bound by noting that, since is regularly varying with index , it follows from Karamata representation that for any . On the other hand

Thus, combining the above two estimates, we get

Therefore, the bound in (32) can be simplified to

for some positive constant .

This completes the proof of the upper bound of the proposition for the subcritical case. The proof of the lower bound is similar by simply substituting by . ∎

We now handle the critical case when is slowly varying. Slowly varying sequences can display a wide range of properties. For examples, such sequences can have a finite limit. Thus, we will impose further regularity conditions.

Recall that a slowly varying sequence can be embedded in a slowly varying function by defining . The following definition is taken from [BGT89, page 24] and adapted to our purpose.

Definition 7.

[Zygmund class] A positive measurable function on is said to belong to the Zygmund class if, for every , the function is ultimately increasing and the function is ultimately decreasing. A slowly varying sequence is said to belong to the Zygmund class if the corresponding function in which it is embedded is in the Zygmund class.

Functions in Zygmund class (see [BGT89, Theorem 1.5.5, page 24]) are slowly varying and have the property that its Karamata representation can be written as where

for some positive and some measurable bounded function vanishing at infinity. That is, in the corresponding representation for sequences (8), one can replace the convergent sequence by the positive limit and get a normalized Karamata representation. The harmonic sequence is an example of a sequence in the Zygmund class as can be easily verified from definition.

We also define super-slow variation from the left inspired by the so-called super-slow varying functions introduced in [And78] for slowly varying functions. We adapt the definition for sequences.

Definition 8.

Suppose is a nondecreasing positive sequence satisfying . A slowly varying sequence is said to be super slowly varying from the left with respect to if

The following conditions generalize the harmonic sequence.

Lemma 9.

Suppose is in the Zygmund class and satisfies

-

(i)

.

-

(ii)

Representation (8) holds for , , and that .

Then, is super-slowly varying with respect to the sequence , . In particular, uniformly in , we have

Proof.

For simplicity let us ignore the floor notation from below although it will be implicitly assumed.

Let , . Then . By the Karamata representation and our assumptions, we get

Consider the function given by . Then, it follows by monotonicity

| (33) |

The lower bound in (33) is easy: For some positive constant , we get

For the upper bound in (33) we change variable to . By applying substitution to this piecewise continuously differentiable function we get

for some positive constant .

Since the upper and the lower bounds are asymptotically of the same order, we get

Since the right side goes to zero, this completes the proof of the first claim. The second estimate now follows easily. ∎

Proposition 10.

Assume that the sequence is slowly varying and assume that the conditions of Lemma 9 hold. Then the following holds

| (34) |

for some positive constants . A similar bound holds for the probability

Proof.

The first part of the proof of Proposition 7 remains unchanged. In particular, the definition of and the bound (18) remains the same.

The difference starts with the definition of . According to the notation in Lemma 9, consider the sequence where . Hence, is a nondecreasing sequence such that . We now show that this choice of satisfies a limit corresponding to (20).

Lemma 11.

We claim that .

Proof of Lemma 11.

By definition

By Lemma 9 and the assumed conditions, the above in limit is equal to the following

This completes the proof. ∎

As before, let . Then . The previous lemma again gives us a partition of in and such that has a log-concave density and is ‘small’. The difference starts again in (28), since in this case . In order to account for this difference, we are going to modify (22) and (30).

We get an identical tail bound for as in (22). For we will forgo the exponential bound and consider a moment bound. To wit, as before in (29), we get

The first term on the right can be estimated as before. For the second one we apply Cauchy-Schwarz inequality to get

We now compute the variance. By independence of the gamma variables, we get

| (35) |

Note that, by our assumption . Thus, . And hence,

| (36) |

for some universal positive constants .

Let . Therefore, by combining all the tail bounds we get

Considering the leading terms on the right and changing the constants as needed, we get the desired bound in the statement. ∎

5. Construction of the ASTRA sequence

We will now collect all the conditions we needed on our sequence in the following list.

Assumption 3.

Recall that we have a non increasing sequence such that each . We assume the following conditions on this sequence.

-

(i)

The sequence of partial sums is regularly varying of index .

-

(ii)

Recall from (4). Then

-

(iii)

.

- (iv)

As we have argued before, the hyperharmonic sequences all satisfy the above requirements.

As mentioned in the Introduction, we assume that there is a probability space on which, for every dimension , there is a process of market weights that is a continuous semimartingale on the state space .

Let be the coordinates of . We will make three assumptions on the sequence of processes . To introduce these assumptions, choose the two numbers from Assumption 1. First assume that and let and . Then, . Consider two Euclidean balls in :

Clearly, .

Now consider the cosine portfolio generated by exponentially concave function from Definition 6 with and . Let denote its domain, i.e.,

Then both and are in . We are interested in the intersection .

If , choose a suitable in the cosine portfolio such that and apply the following argument which is independent of . Hence, for the rest of the argument we will assume that .

We recall our general set-up from Assumption 2. In particular, recall the sequences and .

Lemma 12.

Consider a semimartingale process satisfying (3). Let be a stopping time such that . Then, almost surely, we have the following lower bound on the drift

Proof.

By the exponential concavity of , whenever , we have

Therefore, for , we get

| (37) |

The last inequality is due to (3).

Now let be any arbitrary point in . By elementary algebra,

Therefore, summing over in the above inequality we get

| (38) |

Substituting the above lower bound for every in (37) gives us the statement of the lemma. ∎

We can finally write a statement on the existence of short term arbitrage generalizing Theorem 1. Recall from Assumption 1.

Theorem 13.

Assume that our sequence satisfy Assumption 3. Suppose that we are given an . Then there exists a sequence of portfolios such that the following conclusions are valid. Let denote the relative value of the portfolio at time . As usual, we always assume .

In the subcritical case, when , fix . Then the following hold.

-

(i)

Almost surely, for every .

-

(ii)

With probability , we have

In the critical case, when , the following conclusions hold.

-

(i)’

Almost surely, for every .

-

(ii)’

With probability , we have .

Proof.

First consider the case when . Choose such that . This is possible since . Consider the neighborhoods of accordingly. Now consider the portfolio generated by the exponentially concave function given in Lemma 4 with .

Consider the subcritical case. By Proposition 7 and Assumption 1, with probability at least , we get and the process does not exit by time . On this event, by Lemma 12, by time the total drift for this portfolio is , by Assumption 3 and the fact that . On the other hand, the range of insider is

Thus, it follows from (10) that the relative value of this portfolio never drops below . On the complement of this event, if exits before time , we convert our portfolio to the market portfolio. The maximum loss in log relative value is still . This proves the result for the subcritical case. The critical case is similar.

Now, fix any other . If , then we are covered by the case of . Suppose . Consider the cosine portfolio from Definition 6 by fixing a positive constant and considering the generating function

By Remark 2, on the above domain we get

Now, choose such that . Since is decreasing on and , this allows us to choose to satisfy the requirement of the previous paragraph. Now, as before, choose such that . We can now repeat the above argument for to reach the same conclusion. The constant is absorbed in the big-O notation.

The case of the remaining interval is now covered by the case of . ∎

6. Theoretical examples and data analysis

Of course, one might ask if there is any process that satisfies all the conditions in Assumption 1. We are going to show that the stationary Wright-Fisher (WF) model in dimension with parameters satisfies all the conditions of the theorem. We only consider the subcritical case of for simplicity.

6.1. Theoretical examples

We will refer to the WF process with parameters by . This is a diffusion process on state space that satisfies the following stochastic differential equation (SDE):

where

-

(i)

is a -dimensional standard Brownian motion.

-

(ii)

is the function given by the vector difference:

-

(iii)

is a map from to the space of nonnegative definite matrices. If , the th element of the matrix is given by

Alternatively, the process can be described via its generator acting on twice continuously differentiable functions :

| (39) |

It is known (see [Pal11, Goi09]) that the WF model is the process law of the vector of the market weights under a generalization of the volatility-stabilized model introduced in [FK05]. It is also known (see [Pal11]) that the unique invariant distribution of is . Thus, if and evolves according to the process remains stationary.

Let us now consider the process , . Consider the Euclidean distance function . We compute to get

Notice that we have the following inequality: .

Moreover, for any , consider the matrix . Then, it is clear from (39) that

where is the diagonal matrix with diagonal vector . Thus, for any , we get

Thus, by Itô’s rule

where is martingale with quadratic variation

Since never hits zero (follows from the skew-product result in [Pal11]), almost surely, one can apply Itô’s rule to derive the SDE of :

| (40) |

Here is a local martingale such that

By the Dambis-Dubins-Schwarz theorem [KS91, page 174], we get that there is a standard Brownian motion and a time change such that and for all .

Recall . Choose . Recall that is the first hitting time of . Consider the instantaneous drift coefficient of the process from (40). Suppose , then, during the interval , we get that the coefficient of the instantaneous drift must trivially lie in the interval

for some positive constants . Thus, we get that for , we get the following estimate

| (41) |

Now we have assumed that . Then, the event implies that either or must have happened. However, by comparing with Brownian motions in (41) we get

for some positive constants and for all large enough such that (say).

Similarly,

for some positive constants and for all large enough .

Combining the above two estimates we get

| (42) |

for some positive constant .

Now, fix , and consider the time interval . It suffices to take and this is what is followed below. Partition the unit interval in size , i.e., consider the subintervals . The event that is contained in the union , where

Since , we use Proposition 5 and the two sided concentration estimate in Proposition 7 under the Dirichlet distribution to obtain . Also, from the estimate in (42) we get . Hence, by the union bound estimate we get

| (43) |

for some positive constant . This verifies condition (ii) in Assumption 1 for any bounded sequence .

Notice that the same is true if we consider a deterministic time-change and consider the time-changed stationary Wright-Fisher diffusion.

We now verify condition (3). It follows from the SDE that

Before it exits the set , it follows from (38) that the above is which is much bigger than . In fact, we can again time-change by . As long as , our assumptions continue to hold.

For the model if the following almost sure statement can be made which is akin to the definition of strong relative arbitrage.

Theorem 14.

Suppose that there is a probability space one which the entire sequence of processes can be realized. Assume that follows stationary WF model as above. Consider the sequence of portfolios and their relative values from Theorem 13. Then, w.p. one, for any sample point , there exists such that for all .

Proof.

Recall . Consider the bound in (43) to get . Apply Borel-Cantelli to get an almost sure statement. Since , we get . ∎

Of course, the above is not particularly practical since a priori we do not know which dimension to use. However, it is an interesting allusion to the asymptotic arbitrage theory.

6.2. Evidence from real data

For our data analysis we consider market capitalization data from the Russell 1000 universe. Russell 1000 is a capitalization-weighted index that constitutes of the largest 1000 companies in the U.S. equity markets. The total market capitalization of all the stocks listed in this index is more than of the entire market capitalization of all the listed U.S. stocks. We consider daily market capitalization data of stocks listed in this index for a period of 130 trading days starting on June 26, 2015, and ending on Dec 30, 2015.

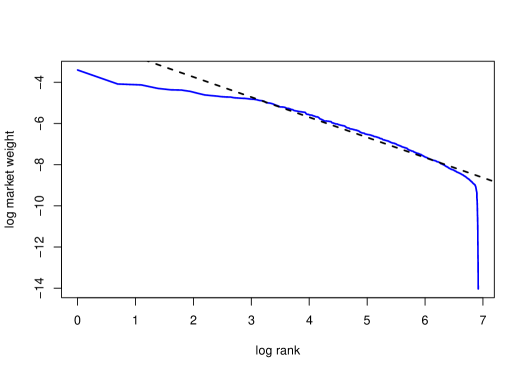

Let us analyze some features of the data to argue that our assumptions are valid. By the nature of the data we can only trade once a day for six months, which is not exactly short term. However, the assumptions do not break down completely. In Figure 2 we show the capital distribution curve as it appears on the first date, Jun 26, 2015. We have have ranked the market weights and plotted against . The graph shows a linear plot in the log-log scale for the top stocks and a steep fall for the last . The estimated Pareto slope for the top part is about . If we ignore the bottom non-Pareto portion, this data lies within the range we consider in this paper. Hence, we can take the dimension .

|

|

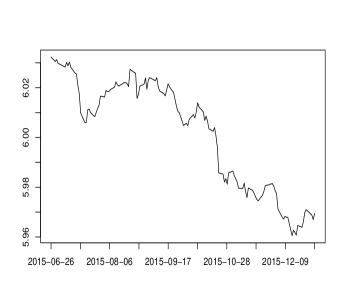

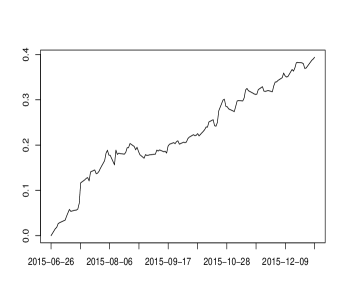

However, over the course of six months, this slope fluctuates slightly getting closer to one with time. This can be seen by plotting the entropy of the market weights as a time series, as done in the left hand image of Figure 3. The graph show the behavior of the Shannon entropy of the vector of market weights considered as a discrete probability distribution. The entropy decreases with time showing a greater concentration of wealth in the larger stocks and the Pareto slope tending to one. However, our Euclidean distance scaling of remains valid as can be seen on the right hand image of Figure 3. The graph shows the scaled Euclidean distance against time . The graph shows that this distance varies within giving credence to the idea that this scaled distance is of order one.

Thus, we face three problems here: (i) how to reduce this problem to justify short-term? (ii) how to account for a changing slope, and (iii) how to choose the correct constant in the cosine portfolio strategy (Definition 6) or equivalently in the Dirichlet distribution. We resolve these problems by dividing the days in periods of successive days. At the beginning of each period we take the initial market weights to be our , which then gets updated in the next period. We choose ad hoc from inspecting the right hand image in Figure 3.

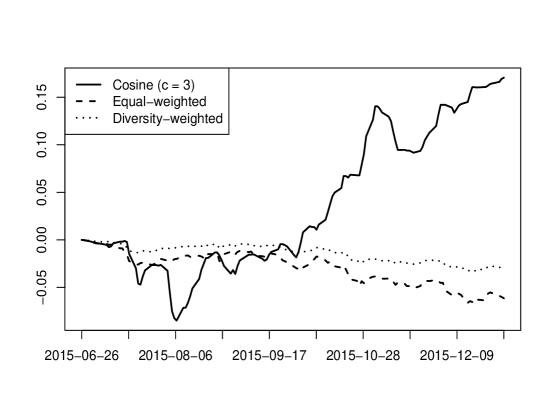

The result of our cosine portfolio (combined over the periods) for is show in Figure 4. The log relative value of the portfolio with respect to the index is plotted on the -axis in the bold line. For comparison, we have also shown the performance over the same data set of the equal weighted portfolio (in dash) and the diversity-weighted portfolio (in dots). For the definition of the latter see [FK09, page 119, eqn. (7.1)]. This time period is a particularly bad time for volatility-harvesting strategies. This has to do with the decrease in entropy and low volatility in the market. This is the reason why both equal-weighted and the diversity-weighted portfolios underperform the index at the end of six months. The cosine portfolio on the other hand makes significant gains, more than over six months which is an annual rate of ! But it does underperform initially (although not by much) which gets erased by the gains in the latter half. Better data should allow for a finer understanding of its performance and how to optimize parameters. Unfortunately, the author is limited by the data that he could access.

Acknowledgement

I am grateful to Jan Maas for pointing out the article [EKS15] during my recent visit to Vienna. My thanks to Walter Schachermayer and Matthias Beiglböck for hosting me at Vienna and a lot of very useful discussion. Many thanks to Johannes Ruf and Leonard Wong for numerous comments on a previous draft. Alexander Vervuurt provided the Russell 1000 data. The data analysis was done by Alexander Vervuurt and Leonard Wong. I am very grateful to both of them.

References

- [And78] C. W. Anderson. Super-slowly varying functions in extreme value theory. J. R. Statist. Soc. B, 40(2):197–202, 1978.

- [Axt01] R.L. Axtell. Zipf distribution of U.S. firm sizes. Science, 293:1818–1820, 2001.

- [BF08] Adrian D. Banner and Daniel Fernholz. Short-term relative arbitrage in volatility-stabilized markets. Annals of Finance, 4(4):445–454, 2008.

- [BGT89] N.H. Bingham, C.M. Goldie, and J.L. Teugels. Regular Variation. Number 1 in Encyclopedia of Mathematics and its Applications. Cambridge University Press, 1989.

- [BL97] S. Bobkov and M. Ledoux. Poincaré’s inequalities and talagrand’s concentration phenomenon for the exponential distribution. PTRF, 107:383–400, 1997.

- [BW09] F. Barthe and P. Wolff. Remarks on non-interacting conservative spin systems: The case of gamma distributions. Stochastic processes and their applications, 119:2711–2723, 2009.

- [CKT14] C. Cuchiero, I. Klein, and J. Teichmann. A new perspective on the fundamental theorem of asset pricing for large financial markets, 2014. Arxiv preprint: 1412.7562.

- [DZ98] Amir Dembo and Ofer Zeitouni. Large deviations techniques and applications, volume 38. Springer, 1998.

- [EKS15] M. Erbar, K. Kuwada, and K.-T. Sturm. On the equivalence of the entropic curvature-dimension condition and bochner’s inequality on metric measure spaces. Invent. math., 201:993–1071, 2015.

- [Fer99] E.R. Fernholz. On the diversity of equity markets. J. Math. Econ., 31:393–417, 1999.

- [Fer02] E. R. Fernholz. Stochastic Portfolio Theory. Applications of Mathematics. Springer, 2002.

- [Fer15] R Fernholz. An example of short-term relative arbitrage. Preprint. ArXiv 1510.02292., 2015.

- [FK05] E. R. Fernholz and I. Karatzas. Relative arbitrage in volatility-stabilized markets. Annals of Finance, 1(2):149–177, 2005.

- [FK09] E. R. Fernholz and I. Karatzas. Stochastic portfolio theory: an overview. In P. G. Ciarlet, editor, Handbook of Numerical Analysis, volume 15 of Handbook of Numerical Analysis, pages 89 – 167. Elsevier, 2009.

- [FKK05] E. R. Fernholz, I. Karatzas, and C. Kardaras. Diversity and relative arbitrage in equity markets. Finance and Stochastics, 9(1):1–27, 2005.

- [FKR15] R. Fernholz, I. Karatzas, and J. Ruf. Volatility and arbitrage. Working paper, 2015.

- [Gab09] X. Gabaix. Power laws in economics and finance. Annu. Rev. Econ., 1(1):255–294, 2009.

- [Goi09] I. Goia. Bessel and volatility-stabilized processes., 2009. Ph. D. thesis. Columbia University.

- [GS73] J. Galambos and E. Seneta. Regularly varying sequences. Proceedings of the AMS, 41(1):110–116, 1973.

- [KK94] Y.M. Kabanov and D.O. Kramkov. Large financial markets: asymptotic arbitrage and contiguity. Teor. Veroyatnost. i Primenen, 39(1):222–229, 1994.

- [KK98] Y.M. Kabanov and D.O. Kramkov. Asymptotic arbitrage in large financial markets. Finance Stoch., 2(2):143–172, 1998.

- [Kle00] I. Klein. A fundamental theorem of asset pricing for large financial markets. Math. Finance, 10(4):443–458, 2000.

- [KS91] I. Karatzas and Shreve S.E. Brownian motion and stochastic calculus, Second edition, volume 113 of Graduate texts in mathematics. Springer-Verlag, 1991.

- [KS96] I. Klein and W. Schachermayer. Asymptotic arbitrage in non-complete large financial markets. Teor. Veroyatnost. i Primenen, 41(4):927–934, 1996.

- [Led97] M. Ledoux. Concentration of measure and logarithmic sobolev inequalities, 1997. Available at http://www.math.univ-toulouse.fr/~ledoux/Berlin.pdf.

- [Pal11] Soumik Pal. Analysis of market weights under volatility-stabilized market models. Ann. Appl. Probab., 21(3):1180–1213, 2011.

- [PW15] S. Pal and T.-K. L. Wong. The geometry of relative arbitrage, 2015. To appear in Mathematics and Financial Economics (Springer).

- [SMS09] A.I. Saichev, Y. Malevergne, and D. Sornette. Theory of Zipf’s Law and Beyond. Lecture Notes in Economics and Mathematical Systems. Springer Berlin Heidelberg, 2009.

- [Tal88] M. Talagrand. An isoperimetric theorem on the cube and the Khintchine-Kahane inequalities. Proc. Amer. Math. Soc., 104:905–909, 1988.

- [Tao09] T. Tao. Benford s law, zipf s law, and the pareto distribution, 2009. Available at terrytao.wordpress.com/2009/07/03/benfords-law-zipfs-law-and-the-pareto-distribution/.

- [Wal96] Christian Walck. Hand-book on statistical distributions for experimentalists. University of Stockholm, 1996. Available at http://www.fysik.su.se/walck/suf9601.pdf.

- [Won15] T.-K. L. Wong. Optimization of relative arbitrage. Annals of Finance, 11(3):345–382, 2015.