Classification and regression tree methods for incomplete data from sample surveys

Abstract

Analysis of sample survey data often requires adjustments to account for missing data in the outcome variables of principal interest. Standard adjustment methods based on item imputation or on propensity weighting factors rely heavily on the availability of auxiliary variables for both responding and non-responding units. Application of these adjustment methods can be especially challenging in cases for which the auxiliary variables are numerous and are themselves subject to substantial incomplete-data problems. This paper shows how classification and regression trees and forests can overcome some of the computational difficulties. An in-depth simulation study based on incomplete-data patterns encountered in the U.S. Consumer Expenditure Survey is used to compare the methods with two standard methods for estimating a population mean in terms of bias, mean squared error, computational speed and number of variables that can be analyzed.

keywords:

[class=MSC]keywords:

,

,

and

t1Supported in part by NSF grant DMS-1305725 and an ASA/NSF/BLS research fellowship.

1 Introduction

We consider estimation of a population mean of a variable in simple random sampling without replacement from a finite population when the sample is incompletely observed. We first review several existing solutions and then propose some new solutions based on classification and regression trees and forests. We aim to show, by means of a realistic simulation study, that certain tree methods are as good as or better than two standard methods in four important respects: (i) bias, (ii) mean squared error, (iii) computational speed, and (iv) applicability to large numbers of prospective predictor variables. Within the large and complex space of incomplete-data methods for surveys, one does not expect any given computational procedure to dominate all other procedures uniformly with respect to each of criteria (i)–(iv). Instead, performance will depend on several factors, including (a) the number of prospective predictor variables, and the degree of association among those variables; (b) incomplete-data patterns encountered among the predictor variables; and (c) the extent to which the observed data and missing-data patterns are consistent with model conditions that are used implicitly or explicitly by a given computational procedure.

Let denote the number of subjects in and let be the subset containing the non-missing values. Let denote the value of for subject in . If the probability that is non-missing for subject is known, then is an unbiased estimate of (throughout this paper, expectations are evaluated with respect to both the sample design and the nonresponse mechanism). Let be an estimate of if the latter is unknown. The inverse probability weighted (IPW) estimate of is (see, e.g., Little, 1986; Seaman and White, 2013)

| (1.1) |

The bias of the IPW estimate depends on accurate specification and estimation of a model for . In applications where covariates are completely observed, logistic regression is typically used. The sample mean, , where is the number of observations in , is an IPW estimate with for .

An alternative approach is imputation of the missing values. Let be the subset of the sample with missing . Let denote the imputed value of for subject in . Then is estimated by the mean of the completed sample

| (1.2) |

The mean of the non-missing values is a special case of mean imputation with in (1.2). If predictor () variables are also observed, the may be obtained by regression imputation (Buck, 1960), where a regression model of on is fitted to the observations in and the are predicted from the values in . If the variables have missing values as well, the complete-case method fits the regression model to the subset of values with complete observations in the and variables.

Hot deck (Little and Rubin, 2002) methods impute missing values by random sampling of non-missing values within ‘adjustment cells’, which are prespecified partitions of the data. One way to construct the cells is to split the range of each variable into a small number of sets and use Cartesian products of the sets to define the cells. It can produce, however, cells with few or no observations. For example, in one analysis of the Current Population Survey, the U.S. Census Bureau had 11,232 cells constructed from seven variables (Bollinger and Hirsch, 2006). Alternatively, the cells can be defined by partitioning the sample according to the estimated probability that is missing, where these probabilities are estimated through the use of logistic regression (see, e.g., Little, 1986). A difficulty is the choice of variables for logistic regression if there are many or they have missing values too.

Another method is maximum likelihood, which draws random observations from a parametric model fitted to the observations. Assuming that (i) the parametric model is correct, (ii) the variables are completely observed, and (iii) the values are missing at random (MAR), that is, the probability that a value is missing does not depend on the value itself, conditional on the non-missing values of the variables, Rubin (1987) showed that inferences from multiply imputed data are statistically valid for large samples. If there are missing values, the EM algorithm (Dempster, Laird and Rubin, 1977) is often used to estimate the parameters in the model. In that case, there is no guarantee that the results are statistically valid. AMELIA (Honaker, King and Blackwell, 2011) uses multivariate normal likelihoods. Each categorical variable is first converted to a dummy 0-1 vector and then a multivariate normal model is fitted to all the variables. As a result, the minimum sample size for AMELIA depends on the number of ordinal variables and the number of dummy variables.

Yet another method is sequential regression (see, e.g., Raghunathan, 2016). It is a regression switching technique in which the missing values in the and variables are initially imputed by their means, medians, or modes. Then each variable is regressed in turn on the other variables and missing values are updated with the predicted values. The procedure is continued for several cycles to reduce the effects of the initial imputed values. MICE (van Buuren and Groothuis-Oudshoorn, 2011), which stands for multiple imputation by chained equations, is one implementation. It uses linear regression for imputation of ordinal variables and polytomous logistic regression for categorical variables. Theoretical arguments for the effectiveness of sequential regression have been given, but they are based on the restrictive assumption of a correct linear regression model relationship between the variable being imputed and the covariates (White and Carlin, 2010).

In practice, MICE can experience computational problems when there are many predictor variables with missing values. For example, linear regression can fail if there is multicollinearity and logistic regression fails if there is quasi-complete separation in the data (Albert and Anderson, 1984; Hosmer, Lemeshow and Sturdivant, 2013). To overcome these problems, Burgette and Reiter (2010) proposed replacing linear regression and logistic regression with CART (Breiman et al., 1984) classification and regression trees from the R tree package. Calling the algorithm CART-MICE, they compared it to MICE in a simulation experiment by generating observations from a quadratic regression model with 10 correlated and normally distributed variables, with 2 of the latter completely observed. Missing values in and the other 8 variables were simulated using an MAR mechanism that depended only on the 2 completely observed variables. Their results showed that the mean squared error and bias of the estimated regression coefficients from CART-MICE were better than those from MICE.

Rubin (1987) proposed imputing the missing values multiple times to obtain variance estimates. Although there are many simulation studies on multiple imputation (MI), almost all used normally distributed data and missingness mechanisms defined by linear logistic regression models (see, e.g., Allison, 2000; Schafer and Graham, 2002; Carpenter, Kenward and White, 2007; Burgette and Reiter, 2010; White and Carlin, 2010). Little is known about the performance of the methods in real-world settings where variables are not normally distributed (e.g., categorical variables) and probabilities of missingness are not determined by linear logistic regression.

To our knowledge, there are only three simulation studies that involve real data. Yu, Burton and Rivero-Arias (2007) used as their simulation population a data set with completely observed values on eight and five variables from 1060 participants in a clinical trial. Simulated samples of size 500 were drawn from the population by bootstrap sampling (i.e., sampling with replacement) and missing values in the dependent variables were artificially generated under a MAR assumption. There were no missing values in the variables. They compared several MI implementations in standard statistical packages and found that the relative performance of the methods depended on the skewness and proportion of zeros of the distribution; performance was similar across methods when deviated only slightly from normal.

Ambler, Omar and Royston (2007) used data from 20,378 patients in a clinical database. The variable was binary and there were 16 variables with varying amounts of missing values. Missing values in the database were imputed by MICE to produce a population without missing values. Then samples were drawn without replacement from the population. Missing values in the samples were generated randomly according to a logistic regression model fitted to the population. Finally missing patterns in were randomly generated with probabilities proportional to the frequencies of the top 16 missing patterns in the original data. The authors found that MICE was one of the best performers.

Andridge and Little (2010) took data from a health and nutrition survey of 16,739 respondents with completely observed values on a variable and seven variables as their simulation population. Simple random samples of size 500 were drawn from the population. A logistic regression model with three variables was used to simulate missing values in the variable. They compared several variations of hot deck imputation with MICE.

These three studies are limited by having fewer than 20 variables and, except for Ambler, Omar and Royston (2007), having no missing values. In this article, we use a data set from the Consumer Expenditure Survey with hundreds of variables and substantial amounts of missing values. We study several new methods based on the CART and GUIDE (Loh, 2002, 2009; Loh and Zheng, 2013) classification and regression algorithms and compare them with AMELIA and MICE in terms of bias, mean squared error and computational speed via simulation. The values are intentionally designed to be naturally missing; i.e., they are not artificially made missing as in previous studies and hence are not necessarily MAR. Only the variable is MAR. No previous simulation study comes close in terms of the number of variables and the real-world authenticity of their missingness mechanisms.

2 Consumer expenditure data

The Consumer Expenditure (CE) Quarterly Interview Survey is a longitudinal survey sponsored by the Bureau of Labor Statistics. It collects information on consumers’ expenditures and incomes as well as characteristics of the consumers. We use a subset of public-use microdata of the 2013 CE Survey. Answers from 25,822 consumer units (CUs) were obtained on more than 600 questions. For general background and further details on the survey, see Bureau of Labor Statistics (2016, chap. 6).

The data contain flag variables that explain whether the values of their associated variables are observed, missing, top-coded, etc. Variables with underscores at the end of their names are typically flag variables. For example, INTRDVX_ is the flag variable associated with INTDRVX, the amount received by a CU in interest or dividends during the past 12 months. Table 1 gives the possible values taken by the flag variables. In this article, we use INTRDVX as the variable and omit CUs with INTRDVX_ = A and T. This leaves a sample size of 4609 of which 1771 CUs have INTRDVX_ = C, i.e., INTRDVX is missing. We ignore the sampling weight here because the R software used in our simulations for AMELIA (Honaker, King and Blackwell, 2011) and MICE (van Buuren and Groothuis-Oudshoorn, 2011) do not allow sampling weights. Besides, the weights do not vary greatly in the CE data; for example, their coefficient of variation is 0.375.

There are 630 variables that can be used to predict . Tables 4–7 give definitions of those used in the analyses below; see Bureau of Labor Statistics (2013) for definitions of the other variables. Almost 20% (124) of the variables have missing values. Table 8 lists their names and numbers of missing values; 67 variables have more than 95% of their values missing (2 are missing all values).

| A | valid nonresponse: a response is not anticipated |

|---|---|

| C | “don’t know”, refusal or other type of nonresponse |

| D | valid data value |

| T | topcoding applied to value |

Note especially that these predictor variables include both variables defined at the Consumer Unit level (e.g., housing tenure) and variables defined for geographical areas. The latter variable type includes State, Region and PSU. The State identifier is subject to confidentiality restrictions in some cases. PSUs are small clusters of counties. Only “A” size PSUs are identified and other PSU labels are coded as missing in the CE public dataset due to confidentiality concerns. In 2013, each “A” size PSU is a cluster with a population of over 2.7 million people, and is self-representing under the CE design. Consequently, this paper treats “PSU” membership as a fixed effect, instead of random effect, for missing value imputation.

3 Methods

We study the following ten methods on their ability to estimate the population mean of INTRDVX accurately and quickly.

- AME.

-

This is AMELIA (Honaker, King and Blackwell, 2011) with default parameters except that the empirical prior level is set at 5. According to the manual, the prior shrinks the covariances of the data but keeps the means and variances the same. It helps when there are many missing values, small sample sizes, large correlations among the variables, or categorical variables with many levels.

- MICE.

-

This is the R software (van Buuren and Groothuis-Oudshoorn, 2011) with default options, including five multiple imputations. Problems due to multi-collinearity in linear regression and quasi-complete separation in logistic regression severely limits the number of variables it can employ. With the help of previous analyses with similar types of data, we identified 19 variables that do not cause the software to fail. Their names and numbers of missing values are given in Table 4. None are income variables. Only 5 of the 19 have missing values (and only 1 with a significant amount). This set of 19 is quite easy for all imputation methods.

- SIM.

-

This is the simple method that estimates with the mean of the non-missing values, ignoring the values of the variables.

\pstree[treemode=D]\TC [tnpos=l] ERANKH 0.006 \TC[fillcolor=yellow,fillstyle=solid] 368 [tnpos=l] 0.83 $952 \pstree[treemode=D]\TC [tnpos=l] STATE in \pstree[treemode=D]\TC [tnpos=l] LIQUIDX_ = C \TC[fillcolor=yellow,fillstyle=solid] 162 [tnpos=l] 0.70 $2465 \pstree[treemode=D]\TC [tnpos=l] PSU in \TC[fillcolor=yellow,fillstyle=solid] 277 [tnpos=l] 0.64 $3444 \pstree[treemode=D]\TC [tnpos=l] RETS_RVX = D or T \TC[fillcolor=green,fillstyle=solid] 404 [tnpos=l] 0.36 $3052 \pstree[treemode=D]\TC [tnpos=l] AGE2 60 \pstree[treemode=D]\TC [tnpos=l] FEDR_NDX = C \TC[fillcolor=yellow,fillstyle=solid] 77 [tnpos=l] 0.66 $1210 \TC[fillcolor=green,fillstyle=solid] 911 [tnpos=r] 0.32 $1556 \TC[fillcolor=yellow,fillstyle=solid] 161 [tnpos=r] 0.66 $3499 \pstree[treemode=D]\TC [tnpos=l]RETS_RVX = C \TC[fillcolor=yellow,fillstyle=solid] 73 [tnpos=l] 0.93 $6080 \pstree[treemode=D]\TC [tnpos=l] FEDR_NDX = C \pstree[treemode=D]\TC [tnpos=l] ROOMSQ 7 \TC[fillcolor=green,fillstyle=solid] 88 [tnpos=l] 0.41 $1448 \TC[fillcolor=yellow,fillstyle=solid] 51 [tnpos=r] 0.76 $4365 \TC[fillcolor=green,fillstyle=solid] 2037 [tnpos=r] 0.21 $1903

Figure 1: GUIDE classification tree for predicting missingness in INTRDVX (INTRDVX_ = C) from 4609 observations and 630 variables, with minimum node size 50. At each split, an observation goes to the left branch if and only if the condition is satisfied. The symbol ‘’ stands for ‘ or missing’. Set = {CO, DE, FL, HI, IL, LA, MA, MO, NJ, NY, OH, PA, SC, TN, WA, WI}; set = {1102, 1110, 1423}. PSU codes are given in Table 9. Numbers beside each terminal node are the proportion missing INTRDVX (top) and the mean INTRDVX of the non-missing values; the sample size is beneath the node. Yellow and green nodes have proportions of INTRDVX missing greater and less, respectively, than 0.50. - GCT.

-

This uses a GUIDE classification tree (Loh, 2009) to form adjustment cells for conditional mean imputation. Figure 1 shows the GUIDE tree for predicting INTRDVX_ = C or D. The first split of the tree sends 368 CUs with ERANKH either missing or to the left node where 304 (83%) of the CUs are missing INTRDVX (i.e., INTRDVX_ = C). The mean INTRDVX ($952) among the 64 CUs in the node with non-missing INTRDVX is used to impute the value of INTRDVX for the other 304 CUs in the node. Repeating this at all the terminal nodes and substituting the imputed values in (1.2) gives the estimate of . The same answer can be obtained with the IPW method too. Let denote a terminal node of the tree and the proportion of non-missing in . Then setting for all CUs in each in (1.1) gives the same estimate.

\pstree[treemode=D]\TC [tnpos=l]INC__ANK = D \pstree[treemode=D]\TC [tnpos=l]RETS_RVB = A \pstree[treemode=D]\TC [tnpos=l] STATE in \pstree[treemode=D]\TC [tnpos=l] SLRF_NDX D \TC[fillcolor=green,fillstyle=solid] 1814 [tnpos=l] 0.22 $1981 \TC[fillcolor=yellow,fillstyle=solid] 97 [tnpos=r] 0.62 $1972 \pstree[treemode=D]\TC [tnpos=l]SMSASTAT = 2 \TC[fillcolor=green,fillstyle=solid] 271 [tnpos=l] 0.17 $1412 \pstree[treemode=D]\TC [tnpos=l] PSU in \pstree[treemode=D]\TC [tnpos=l] FAM_TYPE in \TC[fillcolor=green,fillstyle=solid] 450 [tnpos=l] 0.29 $1790 \pstree[treemode=D]\TC [tnpos=l] INC_HRS1 51 \TC[fillcolor=green,fillstyle=solid] 60 [tnpos=l] 0.20 $1755 \pstree[treemode=D]\TC [tnpos=l] FEDR_NDX = C \TC[fillcolor=green,fillstyle=solid] 212 [tnpos=l] 0.40 $3359 \TC[fillcolor=yellow,fillstyle=solid] 239 [tnpos=r] 0.64 $2725 \pstree[treemode=D]\TC [tnpos=l] STATE in \pstree[treemode=D]\TC [tnpos=l] FEDR_NDX D \pstree[treemode=D]\TC [tnpos=l] BUILDING 2,5 \TC[fillcolor=green,fillstyle=solid] 646 [tnpos=l] 0.35 $1931 \TC[fillcolor=yellow,fillstyle=solid] 61 [tnpos=r] 0.69 $1963 \TC[fillcolor=yellow,fillstyle=solid] 54 [tnpos=r] 0.83 $70 \TC[fillcolor=yellow,fillstyle=solid] 198 [tnpos=r] 0.69 $3963 \TC[fillcolor=yellow,fillstyle=solid] 140 [tnpos=r] 0.92 $3873 \TC[fillcolor=yellow,fillstyle=solid] 367 [tnpos=r] 0.83 $952

Figure 2: RPART classification tree for predicting missingness in INTRDVX (INTRDVX_ = C) from 4609 observations and 630 variables, with minimum node size 50. Set = {AL, AK, AZ, CA, CT, DC, GA, ID, IN, KS, KY, ME, MD, MN, MO, NE, NV, NH, OR, TX, UT, VA, WV}; = {1103, 1111, 1207, 1208, 1210, 1320}; = {2, 7, 8, 9}; = {AZ, DE, LA, NY, PA, SC, TN}. Codes for PSU, FAM_TYPE and BUILDING are given in Tables 9, 10 and 11. Numbers beside each terminal node are the proportion missing INTRDVX (top) and the mean INTRDVX of the non-missing values; the sample size is beneath the node. Yellow and green nodes have proportions of INTRDVX missing greater and less, respectively, than 0.50. - RCT.

-

This is the RPART version of GCT where instead of GUIDE, RPART is used to construct the classification tree shown in Figure 2. GUIDE differs from CART and RPART in several major respects, one being selection bias. Because CART employs greedy search to split each node, it is biased toward selecting variables that permit more splits of the data (Loh and Shih, 1997). Examples are ordinal variables with many distinct values and categorical variables with many levels. GUIDE does not have the bias. There is a hint of the bias if we compare the GCT and RCT trees. RCT splits on four categorical variables: STATE twice and PSU, FAM_TYPE and BUILDING once each. GCT splits once on STATE and PSU and on no other categorical variables. Because STATE, PSU, FAM_TYPE and BUILDING have 39, 21, 9, and 10 levels, respectively, they allow approximately , , , and splits of the data. The codes for PSU, FAM_TYPE and BUILDING are given in the Appendix. Another difference between GUIDE and CART is their treatment of missing values. GUIDE sends all missing values on a split variable to one node or the other while CART and RPART use surrogate splits. See Loh (2009) for more information.

- GCF.

-

This is an alternative IPW method to GCT where, instead of a single tree, a GUIDE classification forest (Loh, 2014) is used to estimate . GUIDE forest is an ensemble of 500 unpruned classification trees, each constructed from a bootstrap sample of the data to predict whether INTRDVX is missing. The Random forest (Breiman, 2001) R implementation (Liaw and Wiener, 2002) cannot be used directly here because: (1) it requires missing values to be imputed beforehand and (2) it does not allow categorical variables with more than 32 levels.

- GRT.

-

This is a conditional mean imputation method that uses a GUIDE piecewise-constant regression tree (Loh, 2002) to impute missing INTRDVX values. Unlike GCT and GCF, it uses only the subset of 2838 CUs with non-missing INTRDVX. The tree is shown in Figure 3. It splits first on AGE_REF = missing or 57. About half of the 2838 CUs satisfy this condition; their mean ($907) is used to impute the missing INTRDVX values in the node. Repeating this procedure at each terminal node yields a completed set of INTRDVX values for application in (1.2).

\pstree[treemode=D]\TC [tnpos=l] AGE_REF 57 \TC[fillcolor=blue,fillstyle=solid] 1433 [tnpos=l]$907 \pstree[treemode=D]\TC [tnpos=l] ETOTA 24030 \pstree[treemode=D]\TC [tnpos=l] STOCKX 27500 \pstree[treemode=D]\TC [tnpos=l] BATHRMQ 2 \pstree[treemode=D]\TC [tnpos=l] PSU in \TC[fillcolor=blue,fillstyle=solid] 111 [tnpos=l]$714 \pstree[treemode=D]\TC [tnpos=l] RENTEQVX 794 \TC[fillcolor=blue,fillstyle=solid] 252 [tnpos=l]$749 \pstree[treemode=D]\TC [tnpos=l] STATE in \pstree[treemode=D]\TC [tnpos=l] REGION = West \TC[fillcolor=yellow,fillstyle=solid] 86 [tnpos=l]$6694 \TC[fillcolor=yellow,fillstyle=solid] 200 [tnpos=r]$3237 \TC[fillcolor=blue,fillstyle=solid] 305 [tnpos=r]$1458 \pstree[treemode=D]\TC [tnpos=l]VEHQ 2 \TC[fillcolor=yellow,fillstyle=solid] 96 [tnpos=l]$6495 \TC[fillcolor=yellow,fillstyle=solid] 75 [tnpos=r]$2262 \TC[fillcolor=yellow,fillstyle=solid] 54 [tnpos=r]$8000 \pstree[treemode=D]\TC [tnpos=l] FFTAXOWE 8104 \TC[fillcolor=yellow,fillstyle=solid] 64 [tnpos=l]$8863 \TC[fillcolor=yellow,fillstyle=solid] 162 [tnpos=r]$4154

Figure 3: GUIDE regression tree for predicting INTRDVX from 2838 observations and 630 variables, with minimum node size 50. At each split, an observation goes to the left branch if and only if the condition is satisfied. The symbol ‘’ stands for ‘ or missing’. Set = {1102, 1103, 1109, 1313, 1419, 1420, 1429}; = {AL, AZ, CA, CT, FL, GA, ID, IN, KY, ME, MD, MI, MN, MO, NV, OH, OR, SC, TX, WA, WI}. Codes for PSU are given in Table 9. Sample sizes and means of INTRDVX are printed below and beside nodes. Blue and yellow nodes have mean INTRDVX below and above, respectively, the SIM estimate of $2009. - RRT.

-

This is the RPART version of GRT where RPART is used instead of GUIDE. The tree, shown in Figure 4, has the same top split as the GRT tree. It subsequently splits on STATE three times, likely because STATE permits more splits.

\pstree[treemode=D]\TC [tnpos=l] AGE_REF 58 \TC[fillcolor=blue,fillstyle=solid] 1433 [tnpos=l]$907 \pstree[treemode=D]\TC [tnpos=l] STATE not in \pstree[treemode=D]\TC [tnpos=l] RENTEQVX 1796 \pstree[treemode=D]\TC [tnpos=l] STATE not in \TC[fillcolor=blue,fillstyle=solid] 726 [tnpos=l]$1417 \pstree[treemode=D]\TC [tnpos=l] TOTXEST 42 \TC[fillcolor=blue,fillstyle=solid] 70 [tnpos=l]$1073 \pstree[treemode=D]\TC [tnpos=l] EARNCOMP 8 \TC[fillcolor=blue,fillstyle=solid] 55 [tnpos=l]$2003 \TC[fillcolor=yellow,fillstyle=solid] 61 [tnpos=r]$9006 \pstree[treemode=D]\TC [tnpos=l] STATE not in \pstree[treemode=D]\TC [tnpos=l] HEALTHPQ 1586 \TC[fillcolor=yellow,fillstyle=solid] 243 [tnpos=l]$2489 \TC[fillcolor=yellow,fillstyle=solid] 85 [tnpos=r]$5849 \TC[fillcolor=yellow,fillstyle=solid] 85 [tnpos=r]$8719 \TC[fillcolor=yellow,fillstyle=solid] 80 [tnpos=r]$9933

Figure 4: RPART regression tree for predicting INTRDVX from from 2838 observations and 630 variables, with minimum node size 50. At each split, an observation goes to the left branch if and only if the condition is satisfied. Set = {CO, ME, NV, SC, WA, WV}; = {FL, GA, MO, NH, OH, OR, VA, WI}; = {AL, CT, ID, IL, KY, MO, NY, TX}. Codes for EARNCOMP are in Table 12. Sample sizes and means of INTRDVX are printed below and beside nodes. Blue and yellow nodes have mean INTRDVX below and above, respectively, the SIM estimate of $2009. - GRF.

- GMICE.

-

CART-MICE cannot be used for the CE data due to limitations in the CART algorithm and software. The R TREE package (Ripley, 2015) used in CART-MICE cannot handle categorical variables with more than 32 levels. RPART (Therneau, Atkinson and Ripley, 2015) does not have this limitation, but both are too computationally expensive for imputation of categorical variables with many categories. GMICE is CART-MICE with GUIDE in place of CART, with ten iterations for each imputation.

To understand the differences between CART-MICE and GMICE, recall that at each node, CART searches for the best split on every variable and then chooses the split that most reduces node impurity. Suppose is categorical with more than two categories and is also categorical with categories. CART has to search through splits of the form “” to find the subset that yields the best split on . Because STATE has 39 categories in our data, there are splits. Other variables with large numbers of categories are HHID (household identifier), PSU, OCCUCOD1, and OCCUCOD2 (spouse occupation), with 46, 21, 15, and 15 levels, respectively.

GUIDE gets around the computation problem with a two-step approximate solution. In the first step, GUIDE selects an variable to split the node by means of chi-squared tests of association with . In the second step, GUIDE finds a split on the selected . Therefore GUIDE does not search for the best split on for every . There are two important benefits to this approach. One is the obvious significant reduction in computation time. The other, which is more subtle, is the first step eliminates the selection bias inherent in the CART approach (Loh and Shih, 1997; Kim and Loh, 2001).

Suppose in the second step that the selected variable has categories and has categories . GUIDE uses the following sequential procedure that reduces the search space if is large and .

-

1.

If , let be the ordered categories of such that and , . Search for the best split among the splits (Breiman et al., 1984, p. 101).

-

2.

Otherwise, if , search through all splits on .

-

3.

Otherwise, if and , define a new categorical variable by merging the categories of into categories. Specifically, for , let be the predicted value of that minimizes the node impurity among the observations with in the node. Define and split the node on , which has splits.

-

4.

If none of the above conditions holds, use linear discriminant analysis on to transform into an ordered variable . Define indicator variables , , and , where is the normalized vector corresponding to the largest discriminant coordinate (equivalent to maximizing the ANOVA F-statistic of on ). Find the split on that most reduces node impurity. Because takes at most ordered values, the search is on only splits. Further, because induces an order on the unordered values, a split of the form can be expressed in the form . This technique is borrowed from Loh and Vanichsetakul (1988).

Another important difference between GUIDE and CART is how they deal with missing values. If has missing values, GUIDE creates a “missing” level to use in the chi-squared tests for variable selection as well as for split set selection. As a result, all observations are used. CART uses surrogates splits, which has been shown to induce a selection bias on variables that have more missing values (Kim and Loh, 2001). Besides, there is empirical evidence that the GUIDE approach to missing values yields higher average classification accuracy than the RPART implementation of CART (Loh, 2009).

To accommodate MICE which works only for 19 variables in Table 4, we applied the methods to three nested sets of variables. The smallest is this set of 19. It is far from an ideal test-bed because there are only 5 variables with missing values (and 4 of them have trivially small numbers of missing values). The second set consists of 52 variables, obtained by combining three groups of variables: the 19 in Table 4 and the top 20 variables determined by the GUIDE importance ranking method (Loh, 2012; Loh, He and Man, 2015) for predicting INTRDVX_ and INTRDVX, respectively; see Tables 5 and 6. The third set is the full set of 630 variables.

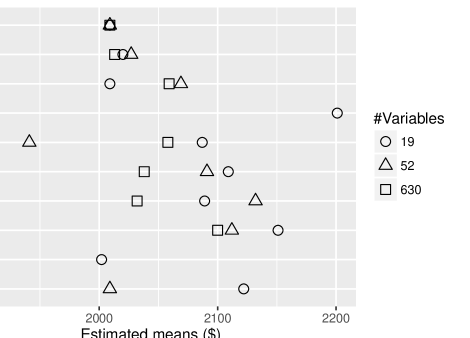

| RRT | RCT | GRT | GCT | GCF | GRF | GMICE | AME | MICE | |

| 19 predictor variables | |||||||||

| Mean | 2020 | 2009 | 2087 | 2151 | 2002 | 2109 | 2089 | 2122 | 2201 |

| Time | 0.2s | 0.1s | 3s | 3s | 9s | 207s | 54s | 147s | 443s |

| 52 predictor variables | |||||||||

| Mean | 2027 | 2069 | 1941 | 2112 | 1897 | 2091 | 2132 | 2009 | Fail |

| Time | 0.5s | 2s | 6s | 8s | 18s | 307s | 429s | 12h | Fail |

| 630 predictor variables | |||||||||

| Mean | 2013 | 2059 | 2058 | 2100 | 1886 | 2038 | 2032 | ? | Fail |

| Time | 5s | 20s | 118s | 134s | 259s | 29m | 27h | 33d+ | Fail |

SIM estimates the mean INTRDVX as $2009 for all three sets because it does not use variables. Results for the other methods are shown in Table 2 and graphed in Figure 5. Every method works on the set of 19 variables but MICE fails for the other two sets. The mean estimates range from a low of $1886 for GCF to a high of $2201 for MICE. Computation times (measured on a Linux computer with a 2.4 GHz AMD Opteron 16-core processor and 64 GB memory) vary greatly. MICE is the slowest on the only set of variables for which it does not fail. It takes 443 sec. for five imputations—more than 4000 times slower than RCT, which is the fastest at 0.1 sec. AMELIA is the next slowest at 147 sec. for this set. For the other two larger sets, AMELIA is the slowest, taking 12 hours for 52 variables and five imputations. For 630 variables, AMELIA ran for 33 days without producing a single imputed data set. In the next section, we report on a series of simulation experiments to compare the bias and accuracy of the estimates.

4 Simulation study

4.1 Experimental design

Simulation studies whose goal is to evaluate methods under realistic conditions usually start with a real data set and then generate artificial populations and samples from it in two steps:

- Step I.

-

Impute the missing values in and treat the resulting data set as a finite population from which the mean of is computed.

- Step II.

-

Generate a population from by making some and values in missing.

If the aim is for to be as similar to as possible, the choice of methods in these two steps is critical. Typically, MICE is used in Step I and a logistic regression propensity model is fitted to the missing value flag variable in to estimate the probability that the variable is missing in Step II. These choices have the three undesirable consequences.

-

1.

Using MICE in Step I limits the number of variables with missing values to no more than a few, due to problems with multi-collinearity and quasi-complete separation. This makes it impossible to apply to data sets such as ours, without preselection of variables. Besides, to impute a variable, MICE necessarily imputes all variables with linear and logistic regression models. This forces relationships among the variables in that do not exist in , thus producing simulated data that look more unlike the real data.

-

2.

In Step II, logistic regression propensity models cannot be constructed from variables with missing values. The latter must be imputed first or the propensity models must be built from subsets of variables or subsets of data. Neither solution is desirable. Imputing the variables (e.g., with MICE) distorts the data and building propensity models from subsets of data requires the artificial assumption that the variables are MAR. Some studies solve this problem by using only completely observed variables for propensity modeling (Burgette and Reiter, 2010), but this is artificial too because the probability of a missing value in often depends on variables with missing values. For example, whether or not interest and dividends is missing depends on the values and missingness of variables such as salary, income taxes paid, and value of stocks.

-

3.

Standard linear and logistic regression models with prespecified fixed sets of predictor variables are inapplicable if the number of variables exceeds the sample size.

The difficulties vanish if GUIDE forests are used instead of MICE and logistic regression in Steps I and II respectively.

- Step I.

-

Fit a GUIDE regression forest to the 2838 CUs in with non-missing INTRDVX values and let be the mean squared residual of the fitted model. Let () denote the predicted value of the th CU in with missing INTRDVX and be an independent random number drawn from a normal distribution with mean 0 and variance . Impute the missing INTRDVX value with . Adding to prevents the imputed values from being more smooth than the non-missing values. It also produces a different for each simulation trial. Truncation at 0 ensures that all INTRDVX values are nonnegative. Non-missing INTRDVX values in are carried over unchanged to .

- Step II.

-

Fit a GUIDE classification forest to all 4609 members of , using the missing value flag INTRDVX_ as dependent variable. Use the predicted values from the model to estimate the probability that INTRDVX is missing for each member of . Finally, make the value of INTRDVX (original or imputed) MAR in according to these probabilities.

A principal advantage of GUIDE forests over other methods, including Random forest, is that no imputation is required of missing values. As a result, their missing mechanisms in the simulated data are the same as in the real data, i.e., not MAR. Other advantages are fast computation speed, unlimited by number of variables and sample size, and absence of the multi-collinearity and quasi-complete separation difficulties that afflict linear and logistic regression.

In our simulation experiments, is the CE data set of 4609 CUs with 19, 52, or 630 variables. A GUIDE regression forest is fitted to each choice of and a population obtained. Each simulation trial then consists of generating and drawing a simple random sample without replacement from it. We use sampling fractions of 5%, 10%, and 25% (corresponding to sample sizes 230, 461, and 1152). Finally, each method being evaluated is applied to the sample to impute the missing INTRDVX values (for conditional mean imputation) or estimate (for IPW) and an estimate of computed.

4.2 Results

Let denote the number of simulation trials, where except for the case with 19 variables and 5% sampling when . For trial , let denote the mean of (which varies with ) and let its estimate be for a given method. The bias and root mean squared error (RMSE) of the method are estimated by

| Bias | ||||

| RMSE |

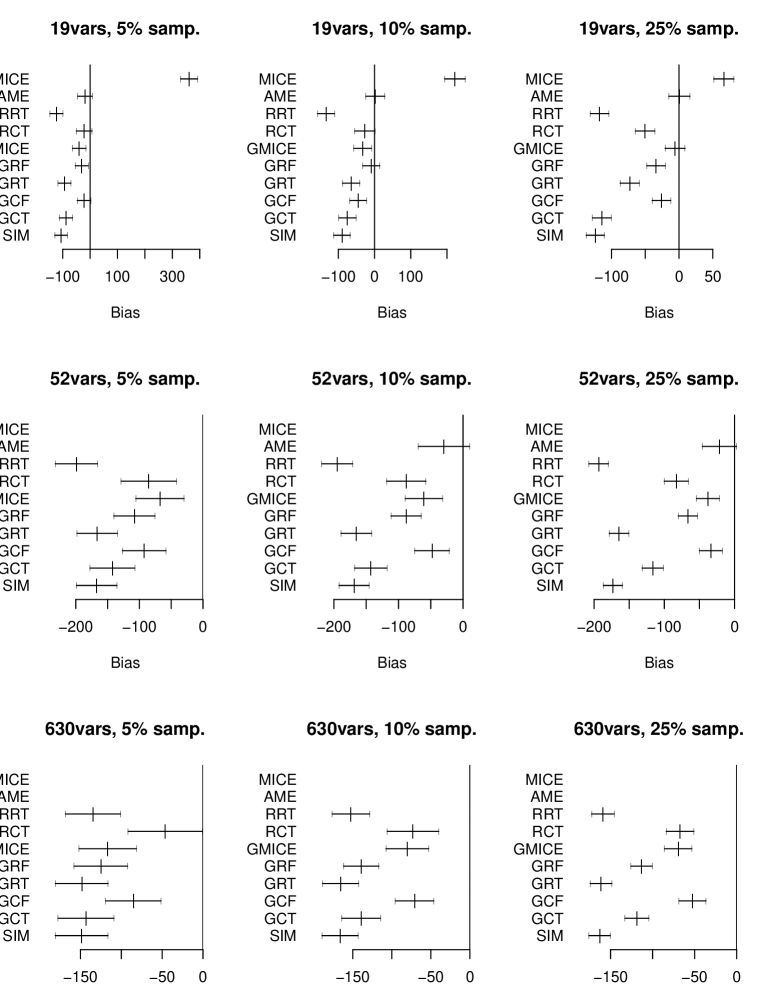

Figure 6 plots the estimated biases with 95% confidence intervals. We observe that:

-

1.

AMELIA has the smallest bias in the situations where it works, viz., where sample size is large relative to number of variables.

-

2.

MICE is the only method having positive bias. In the only situation where it works (19 variables), MICE has the largest bias at 5% and 10% sampling. This is surprising given that there is only one variable with a significant amount of missing values here.

-

3.

GMICE is always better than MICE in terms of bias. The former is consistently among the top three methods.

-

4.

RRT has the next largest bias after MICE. Its bias can be larger than that of SIM, which does not use variables. On the other hand, RCT has relatively low bias.

-

5.

Comparing RPART versus GUIDE regression trees, RRT has larger bias than GRT for 19 and 52 variables; the two are about the same for 630 variables. The reverse is true for classification trees, with RCT doing consistently better than GCT.

-

6.

Among the GUIDE methods, GCF tends to have the smaller bias than GCT, GRT, and GRF.

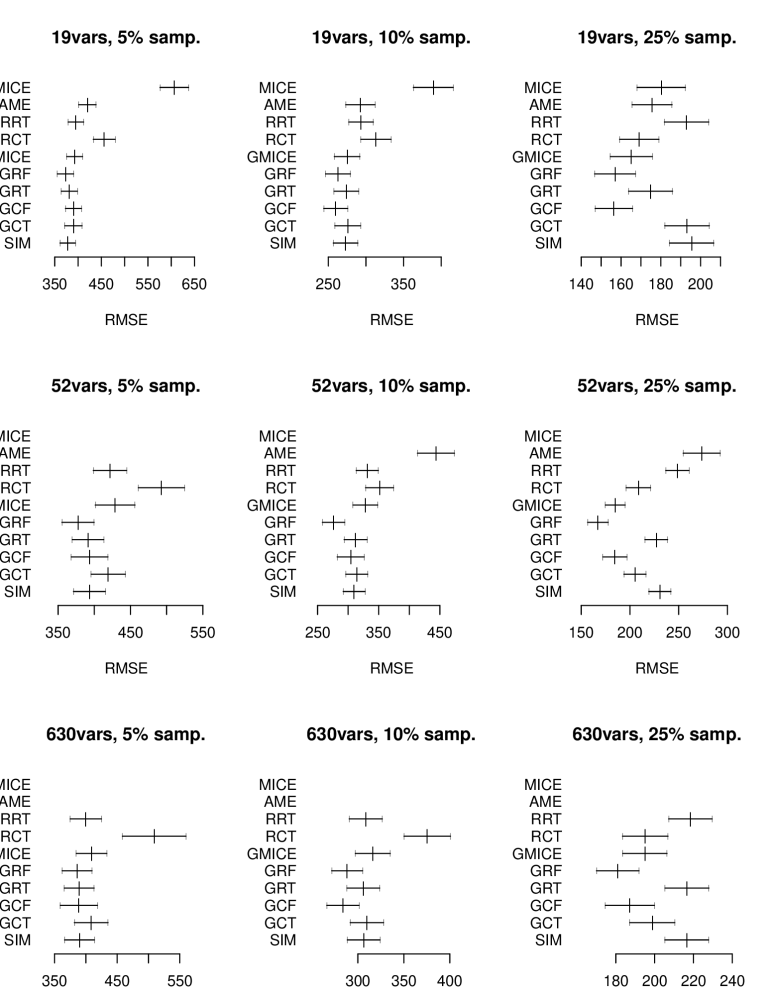

The RMSE results shown in Figure 7 reveal another aspect of the methods:

-

1.

MICE is again worst in two of the three situations where it works (5% and 10% sampling with 19 variables).

-

2.

AMELIA is not as good in RMSE as it is in bias—its RMSE is largest for 52 variables and 10% and 25% sampling (it fails due to inadequate sample size for 5% sampling).

-

3.

RCT and RRT tend to have larger RMSEs.

-

4.

The best method in terms of RMSE is GRF. It is followed by GCF and GMICE.

Overall, GCF and GRF have the best combination of bias and RMSE, and GMICE is third. When has 19 variables, MICE has the largest bias and RMSE for 5% and 10% sampling, though they are much improved for 25%. Its failure to work for larger numbers of variables, however, is its biggest weakness. AMELIA has the lowest bias but the highest RMSE when there are 52 variables.

Table 3 shows the average computational time to perform one simulation trial for each method. If has 19 variables, MICE is the slowest, taking 3 min. per simulation trial for 1152 observations (25% sampling). This is 4.4 times longer than AMELIA, the next slowest. GRF is just behind AMELIA in third place; GMICE is fourth, being 9.5 times faster than MICE. If has 52 variables (where MICE is out of contention), the difference in average time per simulation trial for sample size 1152 is 2.6 hours for AMELIA and 2.6 min. for GMICE. Finally, if has 630 variables, MICE and AMELIA are both out of contention. Then GMICE is slowest at 62 hours per simulation trial and the corresponding times for GCF and GRF, the next two slowest, are 33.7 and 32.3 sec., respectively. The fastest methods are RCT and RRT, which take from fractions of a second to at most 4 sec.

| Frac | RCT | RRT | GCT | GCF | GRT | GRF | GMICE | AME | MICE | |

|---|---|---|---|---|---|---|---|---|---|---|

| 19 variables | ||||||||||

| 5% | 230 | 0.02 | 0.02 | 0.5 | 1.6 | 0.2 | 2.1 | 3.2 | 7.3 | 70 |

| 10% | 461 | 0.05 | 0.02 | 1.1 | 3.9 | 0.4 | 6.3 | 7.3 | 16.3 | 113 |

| 25% | 1152 | 0.10 | 0.05 | 3.4 | 19.0 | 1.9 | 31.4 | 19.4 | 41.1 | 181 |

| 52 variables | ||||||||||

| 5% | 230 | 0.05 | 0.03 | 3.2 | 3.3 | 1.0 | 4.2 | 31.1 | FAIL | FAIL |

| 10% | 461 | 0.11 | 0.05 | 5.0 | 6.2 | 1.5 | 9.5 | 65.6 | 4272 | FAIL |

| 25% | 1152 | 0.32 | 0.11 | 10.2 | 22.3 | 4.1 | 37.1 | 156.9 | 9323 | FAIL |

| 630 variables | ||||||||||

| 5% | 230 | 0.57 | 0.33 | 6.0 | 33.3 | 5.8 | 27.8 | 2810 | FAIL | FAIL |

| 10% | 461 | 1.27 | 0.56 | 12.6 | 94.2 | 12.0 | 77.7 | 6957 | FAIL | FAIL |

| 25% | 1152 | 3.97 | 1.45 | 33.7 | 319.7 | 32.3 | 278.1 | 22204 | FAIL | FAIL |

5 Conclusion

We introduced several techniques to use classification and regression methods for mean estimation of incomplete data. Some employ regression trees to estimate conditional means in adjustment cells defined by the nodes of the trees. Others employ classification trees to estimate missing propensities for inverse probability weighting. Using a data set from the U.S. Consumer Expenditure Survey as a test bed, we performed a large simulation experiment to compare the methods with AMELIA and MICE. A major goal in the experimental design is the novelty of ensuring that the predictor variables are naturally missing, i.e., not constrained to be MAR, in the simulation populations. This is achieved by using GUIDE forests, which leave the predictor-value missingness patterns intact.

The results demonstrate that classification and regression tree methods have the following desirable properties that make them deserving of serious consideration for analysis of incomplete data.

-

1.

They are often superior to traditional methods (as represented by AMELIA and MICE) in terms of bias and mean squared error for mean estimation. This is due to the nonparametric nature of tree models. AMELIA and MICE are based on normality and multivariate linear model assumptions that are seldom satisfied in real complex data.

-

2.

Tree-modeling methods can adapt to available sample sizes. Conversely, parametric methods with a prespecified set of parameters to be estimated are problematic unless the sample size is substantially larger than the number of parameters.

- 3.

-

4.

For cases that involve large numbers of candidate predictors, tree methods can be orders of magnitude faster compared to traditional methods, which are impracticable on large data sets. The speed advantage increases exponentially with number of variables. Therefore it is invaluable to imputation of multiple data sets, bootstrapping, and other variance estimation techniques in large surveys.

In addition, note that the nodes in the tree models as displayed in Figures 1–4 can be interpreted as nonresponse adjustment cells. For example, Little and Vartivarian (2003) extended the ideas of Little (1986) to outline two strategies for reducing the number of adjustment cells: (a) choosing cells that are homogeneous with respect to the probability of response, and (b) choosing cells that are homogeneous with respect to outcome variable . They noted that weighting based on either of these methods of grouping removes non-response bias in estimating population means: The nodes produced by the classification tree method constitute cells that are homogeneous with respect to the estimated probability of response as shown in Figures 1 and 2, while the regression tree method produces cells that are homogeneous with respect to the predicted outcome variable, INTRDVX, as shown in Figures 3 and 4

This work here can be extended in several directions. First, it would be useful to consider design-adjusted versions of the procedures proposed here. This potentially would include the use of weights in the growth of individual trees or forests; in estimation of tree parameters; and in the corresponding estimation of (sub)population means. Of special interest would be evaluation of the extent to which a given procedure may be sensitive to specified patterns of heterogeneity in the weights. For example, as noted in Section 3, all tree and forest algorithms use approximations, and the properties of the resulting procedures can be sensitive to the extent to which a given dataset is consistent with the approximations used for that procedure; and some weight-heterogeneity patterns may exacerbate that sensitivity. In addition, several analyses here used some predictor variables that are equal to membership indicators for certain large primary sample units. It would be of interest to extend previous literature on the use of stratum and PSU labels in regression to the current case.

Second, development of appropriate variance estimators would provide important tools for use in pruning of trees, and for inference related to tree- or forest-based mean estimators. This would require tree- and forest-related extensions of standard theorems on the properties of replication-based variance estimators under complex sample designs. Of special importance would be conditioning arguments arising from the fact that the structure of a given tree is data-driven and not determined a priori.

Third, the current paper focused on estimation of the means of the “interest and dividend” variable, and a related missing-data flag, for the U.S. Consumer Expenditure Survey. Some users of CE data, however, are interested in carrying out econometric analyses based on, e.g., regression, related generalized linear models and more complex hierarchical models. For those situations, one may need to impute simultaneously a substantial number of missing income and expenditure variables for a given consumer unit, and evaluation criteria for the properties of the resulting imputation procedure may be more complex, as discussed in, e.g., Rubin (1996).

Appendix A Details of variables

Table 4 lists the 19 variables in the simulation experiment where MICE did not fail. Tables 5 and 6 list the top predictors of INTRDVX_ and INTRDVX according to GUIDE. Table 7 gives definitions of five additional variables that appear in the tree diagrams. Table 8 gives the names of the 124 variables with missing values (the number missing is beside name). Tables 9–12 give the value codes of the categorical variables appearing in the trees in Figures 1–4.

| Rank | Name | Definition | # |

|---|---|---|---|

| 1 | AGE_REF | Age of reference person | 0 |

| 2 | BATHRMQ | Number complete bathrooms in unit | 21 |

| 3 | BEDROOMQ | Number of bedrooms in unit | 25 |

| 4 | BLS_URBN | Urban or rural | 0 |

| 5 | BUILDING | Which best describes this building? | 0 |

| 6 | CUTENURE | Housing tenure (owned with or without mortgage, rented, etc.; 6 unordered values | 0 |

| 7 | EARNCOMP | Composition of earners (8 unordered values) | 0 |

| 8 | EDUC_REF | Education of reference person (9 ordered values) | 0 |

| 9 | FAM_TYPE | CU type based on relationship of members to reference person; “own” children include blood-related sons and daughters, step children and adopted children | 0 |

| 10 | MARITAL1 | Marital status of reference person (5 categories) | 0 |

| 11 | NO_EARNR | Number of earners | 0 |

| 12 | NUM_AUTO | Number of owned automobiles | 0 |

| 13 | OCCUCOD1 | Occupation (18 categories) | 1697 |

| 14 | REF_RACE | Race of reference person (6 categories) | 0 |

| 15 | REGION | Region of country (NE, MW, S, W) | 33 |

| 16 | ROOMSQ | Number of rooms in unit | 30 |

| 17 | SEX_REF | Sex of reference person (2 categories) | 0 |

| 18 | ST_HOUS | Are these living quarters presently used as student housing by a college or university? (yes/no) | 0 |

| 19 | ETOTA | Total outlays last and current quarters | 0 |

| Rank | Name | Definition | # |

|---|---|---|---|

| 1 | RETS_RVX | Flag variable for RETSURVX (amount received in retirement, survivor or disability pensions in past 12 months) | 0 |

| 2 | FEDR_NDX | Flag variable for Federal income tax refund | 0 |

| 3 | STATE | State (39 categorical values) | 486 |

| 4 | LIQUIDX_ | Flag variable for checking, savings, money market accounts, and CDs | 0 |

| 5 | SLRF_NDX | Flag variable for refund state and local income tax refund | 0 |

| 6 | PSU | Primary sampling unit (21 categorical values) | 2579 |

| 7 | IRAX_ | Flag variable for value of all retirement accounts | 0 |

| 8 | ERANKH | Percent expenditure outlay rank | 367 |

| 9 | INC_RANK | Percent income rank | 367 |

| 10 | SLOC_AXX | Flag variable for state and local income taxes paid | 0 |

| 11 | FEDRFNDX | Amount of federal income tax refund | 2530 |

| 12 | POV_PY | Is CU income below previous year’s poverty threshold? | 0 |

| 13 | POV_CY | Is CU income below current year’s poverty threshold? | 0 |

| 14 | RETS_RVB | Flag variable for range of retirement, survivor or disability pensions | 0 |

| 15 | RETS_VBX | Flag variable for median value of bracket range for RETSURVB (retirement, survivor, or disability pensions) | 0 |

| 16 | INC__ANK | Flag variable for percent income rank | 0 |

| 17 | ERANKH_ | Flag variable for percent expenditure outlay rank | 0 |

| 18 | RESPSTAT | Completeness of income response (yes/no) | 0 |

| 19 | ROYESTX_ | Flag variable for income from royalty or estates and trusts | 0 |

| 20 | FEDTAXX_ | Flag variable for Federal income tax paid by all CU members | 0 |

| Rank | Name | Definition | #NA |

|---|---|---|---|

| 1 | AGE_REF | Age of reference person | 0 |

| 2 | CUTENURE | Housing tenure (owned with or without mortgage, rented, etc.; 6 unordered values | 0 |

| 3 | STATE | State (39 unordered values) | 316 |

| 4 | RENTEQVX | Expected monthly rent of home, if rented out | 444 |

| 5 | AGE2 | Age of spouse | 1201 |

| 6 | INCNONW1 | Reason reference person did not work in past 12 months (6 unordered values | 1869 |

| 7 | STOCKX | Value of all directly-held stocks, bonds, and mutual funds | 2612 |

| 8 | INCOMEY1 | Employer from which reference person received most earnings (6 unordered values) | 969 |

| 9 | STOCKYRX | Median value of bracket range for STOCKX | 2630 |

| 10 | FJSSDEDX | Estimated amount contributed to Social Security | 0 |

| 11 | EARNCOMP | Composition of earners (8 unordered values) | 0 |

| 12 | INC_HRS1 | Number hours usually worked per week by reference person | 969 |

| 13 | PERSOT64 | Number of persons over 64 in CU | 0 |

| 14 | NO_EARNR | Number of earners | 0 |

| 15 | FRRETIRX | Social Security and Railroad Retirement income | 0 |

| 16 | RENT_QVX | Flag variable for RENTEQVX | 0 |

| 17 | PROPTXPQ | Property taxes paid last quarter | 0 |

| 18 | INC_RANK | Percent income rank | 64 |

| 19 | INCO_EY1 | Flag variable for employer type | 0 |

| 20 | INCN_NW1 | Flag variable for reason did not work in past 12 months | 0 |

| Name | Definition |

|---|---|

| SMSASTAT | Does CU reside inside a Metropolitan Statistical Area? (yes/no) |

| TOTXEST | Estimated total taxes paid |

| FFTAXOWE | Weighted estimate for federal tax liabilities at the tax unit level |

| HEALTHPQ | Amount health care last quarter |

| VEHQ | Number of owned vehicles |

| AGE2 1879 | INCWEEK2 1879 | OTHASTBX 4589 | ROOMSQ 30 |

| APTMENT 4535 | INC_HRS1 1697 | OTHASTX 4564 | ROYESTB 4570 |

| BATHRMQ 21 | INC_HRS2 2832 | OTHFINX 4571 | ROYESTBX 4570 |

| BEDROOMQ 25 | INC_RANK 367 | OTHLNYRB 4605 | ROYESTX 4364 |

| BUILT 585 | INTRDVX 1771 | OTHLNYRX 4559 | SEX2 1879 |

| CNTRALAC 1459 | IRAB 4432 | OTHLOAN 3424 | SLOCTAXX 3990 |

| CREDFINX 4282 | IRABX 4432 | OTHLONB 4606 | SLRFUNDX 3167 |

| CREDITB 4584 | IRAX 3853 | OTHLONBX 4606 | STATE 486 |

| CREDITBX 4584 | IRAYRB 4407 | OTHLONX 4555 | STCKYRBX 4531 |

| CREDITX 4233 | IRAYRBX 4407 | OTHLYRBX 4605 | STDNTYRB 4591 |

| CREDTYRX 4248 | IRAYRX 3899 | OTHREGB 4594 | STDNTYRX 4483 |

| CREDYRB 4573 | LIQDYRBX 4448 | OTHREGBX 4594 | STDTYRBX 4591 |

| CREDYRBX 4573 | LIQUDYRB 4448 | OTHREGX 4338 | STOCKB 4550 |

| DEFBENRP 3490 | LIQUDYRX 3876 | OTHRINCB 4603 | STOCKBX 4550 |

| DIRACC 154 | LIQUIDB 4481 | OTHRINCX 4483 | STOCKX 4319 |

| EDUCA2 1879 | LIQUIDBX 4481 | OTHSTYRB 4585 | STOCKYRB 4531 |

| EITC 1032 | LIQUIDX 3827 | OTHSTYRX 4572 | STOCKYRX 4347 |

| ERANKH 367 | LMPSUMBX 4600 | OTHSYRBX 4585 | STUDFINX 4511 |

| FEDRFNDX 2530 | LUMPSUMB 4600 | OTRINCBX 4609 | STUDNTB 4598 |

| FEDTAXX 3752 | LUMPSUMX 4378 | POPSIZE 33 | STUDNTBX 4598 |

| FMLPYYRX 4514 | MEALSPAY 9 | PORCH 997 | STUDNTX 4473 |

| FS_MTHI 4560 | MISCTAXX 4520 | POV_CY 378 | SWIMPOOL 4045 |

| HHID 4531 | MLPAYWKX 4514 | POV_PY 378 | WELFAREX 4596 |

| HISP2 1879 | MLPYQWKS 4508 | PSU 2579 | WELFREBX 4609 |

| HLFBATHQ 23 | NETRENTB 4582 | RACE2 1879 | WHLFYRB 4564 |

| HORREF1 4448 | NETRENTX 4258 | REGION 33 | WHLFYRBX 4564 |

| HORREF2 4495 | NETRNTBX 4582 | RENTEQVX 660 | WHLFYRX 4444 |

| INCNONW1 2912 | OCCUCOD1 1697 | RETSRVBX 4542 | WHOLIFB 4571 |

| INCNONW2 3656 | OCCUCOD2 2832 | RETSURVB 4542 | WHOLIFBX 4571 |

| INCOMEY1 1697 | OFSTPARK 1160 | RETSURVM 3289 | WHOLIFX 4428 |

| INCOMEY2 2832 | OTHASTB 4589 | RETSURVX 3520 | WINDOWAC 3977 |

| 1109 | New York, NY |

|---|---|

| 1110 | New York, Connecticut suburbs |

| 1111 | New Jersey suburbs |

| 1102 | Philadelphia – Wilmington – Atlantic City, PA – NJ – DE - MD |

| 1103 | Boston – Brockton – Nashua, MA – NH – ME CT |

| 1207 | Chicago – Gary – Kenosha, IL – IN - WI |

| 1208 | Detroit – Ann Arbor – Flint, MI |

| 1210 | Cleveland – Akron, OH |

| 1211 | Minneapolis – St. Paul, MN – WI |

| 1312 | Washington, DC – MD – VA – WV |

| 1313 | Baltimore, MD |

| 1316 | Dallas – Ft. Worth, TX |

| 1318 | Houston – Galveston – Brazoria, TX |

| 1319 | Atlanta, GA |

| 1320 | Miami – Ft. Lauderdale, FL |

| 1419 | Los Angeles – Orange, CA |

| 1420 | Los Angeles suburbs, CA |

| 1422 | San Francisco – Oakland – San Jose, CA |

| 1423 | Seattle – Tacoma – Bremerton, WA |

| 1424 | San Diego, CA |

| 1429 | Phoenix – Mesa, AZ |

| 1 | Husband and wife (H/W) only |

|---|---|

| 2 | H/W, own children only, oldest child under 6 years old |

| 3 | H/W, own children only, oldest child 6 to 17 years old |

| 4 | H/W, own children only, oldest child over 17 years old |

| 5 | All other H/W CUs |

| 6 | One parent, male, own children only, at least one child age under 18 years old |

| 7 | One parent, female, own children only, at least one child age under 18 years old |

| 8 | Single persons |

| 9 | Other CUs |

| 1 | Single family detached (detached structure with only one primary residence; however, the structure could include a rental unit(s) in the basement, attic, etc.) |

|---|---|

| 2 | Row or townhouse inner unit (2, 3 or 4 story structure with 2 walls in common with other units and a private ground level entrance; it may have a rental unit as part of structure) |

| 3 | End row or end townhouse (one common wall) |

| 4 | Duplex (detached two unit structure with one common wall between the units) |

| 5 | 3-plex or 4-plex (3 or 4 unit structure with all units occupying the same level or levels) |

| 6 | Garden (a multi-unit structure, usually wider than it is high, having 2, 3, or possibly 4 floors; characteristically the units not only have common walls but are also stacked on top of one another) |

| 7 | High-rise (a multi-unit structure which has 4 or more floors) |

| 8 | Apartment or flat (a unit not described above; could be located in the basement, attic, second floor or over the garage of one |

| 1 | Reference person only |

|---|---|

| 2 | Reference person and spouse |

| 3 | Reference person, spouse and others |

| 4 | Reference person and others |

| 5 | Spouse only |

| 6 | Spouse and others |

| 7 | Others only |

| 8 | No earners |

Acknowledgments

The authors thank Steve Henderson and Geoff Paulin for very productive discussions of the U.S. Consumer Expenditure Survey and to Matthew Blackwell for help with the AMELIA software. The views expressed in this paper are those of the authors and do not necessarily reflect the policies of the U.S. Bureau of Labor Statistics.

References

- Albert and Anderson (1984) {barticle}[author] \bauthor\bsnmAlbert, \bfnmA.\binitsA. and \bauthor\bsnmAnderson, \bfnmJ. A.\binitsJ. A. (\byear1984). \btitleOn the existence of maximum likelihood estimates in logistic regression models. \bjournalBiometrika \bvolume71 \bpages1-10. \endbibitem

- Allison (2000) {barticle}[author] \bauthor\bsnmAllison, \bfnmP. D.\binitsP. D. (\byear2000). \btitleMultiple imputation for missing data. A cautionary tale. \bjournalSociological Methods and Research \bvolume28 \bpages301-309. \endbibitem

- Ambler, Omar and Royston (2007) {barticle}[author] \bauthor\bsnmAmbler, \bfnmG.\binitsG., \bauthor\bsnmOmar, \bfnmR. Z.\binitsR. Z. and \bauthor\bsnmRoyston, \bfnmP.\binitsP. (\byear2007). \btitleA comparison of imputation techniques for handling missing predictor values in a risk model with a binary outcome. \bjournalStatistical Methods in Medical Research \bvolume16 \bpages277-298. \endbibitem

- Andridge and Little (2010) {barticle}[author] \bauthor\bsnmAndridge, \bfnmR. R.\binitsR. R. and \bauthor\bsnmLittle, \bfnmR. J. A.\binitsR. J. A. (\byear2010). \btitleA review of hot deck imputation for survey non-response. \bjournalInternational Statistical Review \bvolume78 \bpages40–64. \bdoi10.1111/j.1751-5823.2010.00103.x \endbibitem

- Bollinger and Hirsch (2006) {barticle}[author] \bauthor\bsnmBollinger, \bfnmC. R.\binitsC. R. and \bauthor\bsnmHirsch, \bfnmB. T.\binitsB. T. (\byear2006). \btitleMatch bias from earnings imputation in the Current Population Survey: The case of imperfect matching. \bjournalJournal of Labor Economics \bvolume24 \bpages483-519. \endbibitem

- Breiman (2001) {barticle}[author] \bauthor\bsnmBreiman, \bfnmLeo\binitsL. (\byear2001). \btitleRandom Forests. \bjournalMachine Learning \bvolume45 \bpages5–32. \endbibitem

- Breiman et al. (1984) {bbook}[author] \bauthor\bsnmBreiman, \bfnmL.\binitsL., \bauthor\bsnmFriedman, \bfnmJ. H.\binitsJ. H., \bauthor\bsnmOlshen, \bfnmR. A.\binitsR. A. and \bauthor\bsnmStone, \bfnmC. J.\binitsC. J. (\byear1984). \btitleClassification and Regression Trees. \bpublisherWadsworth, \baddressBelmont. \endbibitem

- Buck (1960) {barticle}[author] \bauthor\bsnmBuck, \bfnmS. F.\binitsS. F. (\byear1960). \btitleA method of estimation of missing values in multivariate data suitable for use with an electronic computer. \bjournalJournal of the Royal Statistical Society, Series B \bvolume22 \bpages302–306. \endbibitem

- Bureau of Labor Statistics (2013) {bmanual}[author] \bpublisherBureau of Labor Statistics (\byear2013). \btitlePublic-use Interview Survey Data Dictionary. \baddressU.S. Department of Labor \bnotehttp://www.bls.gov/cex/2013/csxintvwdata.pdf. \endbibitem

- Bureau of Labor Statistics (2016) {bmanual}[author] \bpublisherBureau of Labor Statistics (\byear2016). \btitleHandbook of Methods. \baddressU.S. Department of Labor \bnotehttp://www.bls.gov/opub/hom/pdf/homch16.pdf. \endbibitem

- Burgette and Reiter (2010) {barticle}[author] \bauthor\bsnmBurgette, \bfnmL. F.\binitsL. F. and \bauthor\bsnmReiter, \bfnmJ. P.\binitsJ. P. (\byear2010). \btitleMultiple imputation for missing data via sequential regression trees. \bjournalAmerican Journal of Epidemiology \bvolume172 \bpages1070-1076. \bdoi10.1093/aje/kwq260 \endbibitem

- Carpenter, Kenward and White (2007) {barticle}[author] \bauthor\bsnmCarpenter, \bfnmJ. R.\binitsJ. R., \bauthor\bsnmKenward, \bfnmM. G.\binitsM. G. and \bauthor\bsnmWhite, \bfnmI. R.\binitsI. R. (\byear2007). \btitleSensitivity analysis after multiple imputation under missing at random: a weighting approach. \bjournalStatistical Methods in Medical Research \bvolume16 \bpages259-275. \endbibitem

- Dempster, Laird and Rubin (1977) {barticle}[author] \bauthor\bsnmDempster, \bfnmA. P.\binitsA. P., \bauthor\bsnmLaird, \bfnmN. M.\binitsN. M. and \bauthor\bsnmRubin, \bfnmD. B.\binitsD. B. (\byear1977). \btitleMaximum likelihood from incomplete data via the EM algorithm (with discussion). \bjournalJournal of the Royal Statistical Society, Ser. B \bvolume39 \bpages1-38. \endbibitem

- Honaker, King and Blackwell (2011) {barticle}[author] \bauthor\bsnmHonaker, \bfnmJ.\binitsJ., \bauthor\bsnmKing, \bfnmG.\binitsG. and \bauthor\bsnmBlackwell, \bfnmM.\binitsM. (\byear2011). \btitleAmelia II: A Program for Missing Data. \bjournalJournal of Statistical Software \bvolume45 \bpages1-47. \endbibitem

- Hosmer, Lemeshow and Sturdivant (2013) {bbook}[author] \bauthor\bsnmHosmer, \bfnmD. W.\binitsD. W., \bauthor\bsnmLemeshow, \bfnmS.\binitsS. and \bauthor\bsnmSturdivant, \bfnmR. X.\binitsR. X. (\byear2013). \btitleApplied Logistic Regression, \beditionThird ed. \bpublisherWiley. \endbibitem

- Kim and Loh (2001) {barticle}[author] \bauthor\bsnmKim, \bfnmH.\binitsH. and \bauthor\bsnmLoh, \bfnmW. Y.\binitsW. Y. (\byear2001). \btitleClassification trees with unbiased multiway splits. \bjournalJournal of the American Statistical Association \bvolume96 \bpages589–604. \endbibitem

- Liaw and Wiener (2002) {barticle}[author] \bauthor\bsnmLiaw, \bfnmAndy\binitsA. and \bauthor\bsnmWiener, \bfnmMatthew\binitsM. (\byear2002). \btitleClassification and Regression by randomForest. \bjournalR News \bvolume2 \bpages18-22. \endbibitem

- Little (1986) {barticle}[author] \bauthor\bsnmLittle, \bfnmR. J. A.\binitsR. J. A. (\byear1986). \btitleSurvey nonresponse adjustments for estimates of means. \bjournalInternational Statistical Review \bvolume54 \bpages139-157. \endbibitem

- Little and Rubin (2002) {bbook}[author] \bauthor\bsnmLittle, \bfnmR. J. A.\binitsR. J. A. and \bauthor\bsnmRubin, \bfnmD. B.\binitsD. B. (\byear2002). \btitleStatistical Analysis With Missing Data, \beditionSecond ed. \bpublisherWiley, \baddressNew York. \endbibitem

- Little and Vartivarian (2003) {barticle}[author] \bauthor\bsnmLittle, \bfnmR. J. A.\binitsR. J. A. and \bauthor\bsnmVartivarian, \bfnmS.\binitsS. (\byear2003). \btitleOn weighting the rates in non-response weights. \bjournalStatistics in Medicine \bvolume22 \bpages1589-1599. \endbibitem

- Loh (2002) {barticle}[author] \bauthor\bsnmLoh, \bfnmW. Y.\binitsW. Y. (\byear2002). \btitleRegression Trees With Unbiased Variable Selection and Interaction Detection. \bjournalStatistica Sinica \bvolume12 \bpages361–386. \endbibitem

- Loh (2009) {barticle}[author] \bauthor\bsnmLoh, \bfnmW. Y.\binitsW. Y. (\byear2009). \btitleImproving the precision of classification trees. \bjournalAnnals of Applied Statistics \bvolume3 \bpages1710–1737. \endbibitem

- Loh (2012) {binproceedings}[author] \bauthor\bsnmLoh, \bfnmW. Y.\binitsW. Y. (\byear2012). \btitleVariable selection for classification and regression in large , small problems. In \bbooktitleProbability Approximations and Beyond (\beditor\bfnmA.\binitsA. \bsnmBarbour, \beditor\bfnmH. P.\binitsH. P. \bsnmChan and \beditor\bfnmD.\binitsD. \bsnmSiegmund, eds.). \bseriesLecture Notes in Statistics—Proceedings \bvolume205 \bpages133–157. \bpublisherSpringer, \baddressNew York. \endbibitem

- Loh (2014) {barticle}[author] \bauthor\bsnmLoh, \bfnmW. Y.\binitsW. Y. (\byear2014). \btitleFifty years of classification and regression trees (with discussion). \bjournalInternational Statistical Review \bvolume34 \bpages329-370. \bdoi10.1111/insr.12016 \endbibitem

- Loh, He and Man (2015) {barticle}[author] \bauthor\bsnmLoh, \bfnmW. Y.\binitsW. Y., \bauthor\bsnmHe, \bfnmX.\binitsX. and \bauthor\bsnmMan, \bfnmM.\binitsM. (\byear2015). \btitleA regression tree approach to identifying subgroups with differential treatment effects. \bjournalStatistics in Medicine \bvolume34 \bpages1818-1833. \bdoi10.1002/sim.6454 \endbibitem

- Loh and Shih (1997) {barticle}[author] \bauthor\bsnmLoh, \bfnmW. Y.\binitsW. Y. and \bauthor\bsnmShih, \bfnmY. S.\binitsY. S. (\byear1997). \btitleSplit selection methods for classification trees. \bjournalStatistica Sinica \bvolume7 \bpages815–840. \endbibitem

- Loh and Vanichsetakul (1988) {barticle}[author] \bauthor\bsnmLoh, \bfnmW. Y.\binitsW. Y. and \bauthor\bsnmVanichsetakul, \bfnmN.\binitsN. (\byear1988). \btitleTree-structured classification via generalized discriminant analysis (with discussion). \bjournalJournal of the American Statistical Association \bvolume83 \bpages715–728. \endbibitem

- Loh and Zheng (2013) {barticle}[author] \bauthor\bsnmLoh, \bfnmW. Y.\binitsW. Y. and \bauthor\bsnmZheng, \bfnmW.\binitsW. (\byear2013). \btitleRegression trees for longitudinal and multiresponse data. \bjournalAnnals of Applied Statistics \bvolume7 \bpages495-522. \bdoi10.1214/12-AOAS596 \endbibitem

- Raghunathan (2004) {barticle}[author] \bauthor\bsnmRaghunathan, \bfnmT. E.\binitsT. E. (\byear2004). \btitleWhat do we do with missing data? Some options for analysis of incomplete data. \bjournalAnnual Review of Public Health \bvolume25 \bpages99-117. \endbibitem

- Raghunathan (2016) {bbook}[author] \bauthor\bsnmRaghunathan, \bfnmT. E.\binitsT. E. (\byear2016). \btitleMissing Data Analysis in Practice. \bpublisherCRC Press, \baddressBoca Raton, FL. \endbibitem

- Ripley (2015) {bmanual}[author] \bauthor\bsnmRipley, \bfnmB.\binitsB. (\byear2015). \btitletree: Classification and Regression Trees \bnoteR package version 1.0-36. \endbibitem

- Rubin (1987) {bbook}[author] \bauthor\bsnmRubin, \bfnmD. B.\binitsD. B. (\byear1987). \btitleMultiple Imputation for Nonresponse in Surveys. \bpublisherWiley. \endbibitem

- Rubin (1996) {barticle}[author] \bauthor\bsnmRubin, \bfnmD. B.\binitsD. B. (\byear1996). \btitleMultiple imputation after 18+ years. \bjournalJournal of the American Statistical Association \bvolume91 \bpages473-489. \endbibitem

- Schafer and Graham (2002) {barticle}[author] \bauthor\bsnmSchafer, \bfnmJ. L.\binitsJ. L. and \bauthor\bsnmGraham, \bfnmJ. W.\binitsJ. W. (\byear2002). \btitleMissing data: our view of the state of the art. \bjournalPsychological Methods \bvolume7 \bpages147-177. \endbibitem

- Seaman and White (2013) {barticle}[author] \bauthor\bsnmSeaman, \bfnmS. R.\binitsS. R. and \bauthor\bsnmWhite, \bfnmI. R.\binitsI. R. (\byear2013). \btitleReview of inverse probability weighting for dealing with missing data. \bjournalStatistical Methods in Medical Research \bvolume22 \bpages278-295. \endbibitem

- Therneau, Atkinson and Ripley (2015) {bmanual}[author] \bauthor\bsnmTherneau, \bfnmT.\binitsT., \bauthor\bsnmAtkinson, \bfnmB.\binitsB. and \bauthor\bsnmRipley, \bfnmB.\binitsB. (\byear2015). \btitlerpart: Recursive Partitioning and Regression Trees \bnoteR package version 4.1-10. \endbibitem

- van Buuren and Groothuis-Oudshoorn (2011) {barticle}[author] \bauthor\bsnmvan Buuren, \bfnmS.\binitsS. and \bauthor\bsnmGroothuis-Oudshoorn, \bfnmK.\binitsK. (\byear2011). \btitlemice: Multivariate Imputation by Chained Equations in R. \bjournalJournal of Statistical Software \bvolume45 \bpages1–67. \endbibitem

- White and Carlin (2010) {barticle}[author] \bauthor\bsnmWhite, \bfnmI. R.\binitsI. R. and \bauthor\bsnmCarlin, \bfnmJ. B.\binitsJ. B. (\byear2010). \btitleBias and efficiency of multiple imputation compared with complete-case analysis for missing covariate values. \bjournalStatistics in Medicine \bvolume29 \bpages2920-2931. \endbibitem

- Yu, Burton and Rivero-Arias (2007) {barticle}[author] \bauthor\bsnmYu, \bfnmL. M.\binitsL. M., \bauthor\bsnmBurton, \bfnmA.\binitsA. and \bauthor\bsnmRivero-Arias, \bfnmO.\binitsO. (\byear2007). \btitleEvaluation of software for multiple imputation of semi-continuous data. \bjournalStatistical Methods in Medical Research \bvolume16 \bpages243-258. \endbibitem